Page 1

The Pennsylvania State University

The Graduate School

College of Agricultural Sciences

THREE ESSAYS ON TECHNOLOGY DEVELOPMENT AND FDI IN CHINA: REGIONAL

SPILLOVER, FACTOR BIAS SPILLOVER, AND CHANGE OF ENERGY INTENSITY

A Dissertation in

Agricultural, Environmental and Regional Economics

by

Yong Hu

© 2012 Yong Hu

Submitted in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

May 2012

Page 2

i

The dissertation of Yong Hu was reviewed and approved* by the following:

Karen Fisher-Vanden

Associate Professor of Agricultural Economics

Dissertation Adviser

Chair of Committee

David G. Abler

Professor of Agricultural Economics

Spiro E. Stefanou

Professor of Agricultural Economics

Zhen Lei

Assistant Professor of Energy and Environmental Economics

Ann Tickamyer

Professor and Head, Department of Agricultural Economics and Rural Sociology

* Signatures are on file in the Graduate School.

Page 3

ii

ABSTRACT

This thesis investigates how the spillover effect of R&D expenditures and foreign direct investment (FDI)

affect firms’ productivity, technology development, and energy efficiency in China. Specifically, the first

essay uses firm-level panel data from Chinese enterprises to examine how regional differences influence

the impact of technology spillovers on firms’ productivity. This essay contributes to the existing literature

in the following aspects: providing regional evidence that vertical channels are more important than

horizontal channels to generate positive spillovers; providing empirical evidence on how regional

differences, including geographical endowments, economic factors, and government policies, affect

within-region and outside-region spillovers; providing empirical evidence to support the fact that China’s

“Grand Western Development Program” helped to reduce the economic disparity between the Western

region and Coastal region. We find within-region spillover effects improve the productivity of firms in the

Eastern region, which may due to the “Coastal Development Strategies” and the Eastern region’s

geographical advantages; firms in the Northeastern region receive significant cost-increasing outside-

region spillover effects, which is in some extent caused by the low performances of SOEs in the Northeast;

firms in the Southwestern region, which has the lowest GDP among five Chinese regions, receive

significant cost-saving within-region and outside-region spillover effects, which may be a result of the

fact that Coastal region has bigger positive impacts on the Western region after the implementation of

“Grand Western Development Program”. The second essay investigates the factor-bias spillover effect of

FDI in China. Specifically, we examine how domestic enterprises guide their technology development

direction in response to FDI in their horizontal industry, upstream industry, or downstream industry.

Moreover, we will investigate the impact on FDI spillovers, resulting from China’s joining of the World

Trade Organization in 2001. Our empirical results show that foreign capital invested in upstream

industries results in the use of more materials; foreign capital in downstream industries induces the use of

more capital, but less labor; and foreign capital in horizontal industries induces saving in capital, but

using in materials. Competition from foreign firms in the same industry spurs domestic firms to reduce

Page 4

iii

their production cost by more intensively utilizing their relative factors endowment, which is capital-

scarce, labor- and material-abundant. FDI in upstream industry produces higher quality outputs inducing

Chinese firms to outsource more. Benefiting from technology transferred from downstream foreign

consumers, local suppliers exhibit technical change with capital-using, labor- and material-saving factor

bias. The third essay investigates how R&D expenditures and FDI, as well as other factors, influence the

energy intensity in four Chinese high energy consumption industries. Results suggest that China’s

increased openness to the world and R&D expenditures only bring benefits a couple of industries in

improving their energy efficiency, while rising energy costs and China’s industrial policy—“grasping the

large, letting go off the small” are significant contributors to the decline in energy intensity in all four

industries.

Page 5

iv

TABLE OF CONTENTS

List of Figures ……………………………………………………………………………..…….vi

List of Tables ………………………. ………………………………………………..…...….……..vii

ACKNOWLEDGEMENTS……………………………………………………………………………….….…ix

1 Chapter one: Introduction......................................................................................................................................1

1.1 Background & Motivation........................................................................................................................................1

1.2 Objectives & brief outline........................................................................................................................................5

References………………………………………………………………………………………………..……………7

2 Chapter two: Region Development and Technology Spillover in China............................................8

2.1 Introduction…………………………………………………………………………………………..…….……..8

2.2 Literature review….…………………………………………………………………………………..………….11

2.3 Data……………………………………………………………………………………………………..…….....15

2.4 Model specification and methodology…….…………………………………………………………..…………24

2.5 Results and interpretation……………………………………………………………………………………….29

2.5.1 Empirical Result…….……………………………………………………………………………….….…29

2.5.2 Rapid Growth in the Eastern Region…………………………………………………………...……..…..33

2.5.3 The Impact of “Grand Western Development Program” on the Southwestern Region………….…..….36

2.5.4 SOE Reform in the Northeastern Region…………………………………………………………...…….39

2.7 Conclusion…………………………………………………………………………………………………...…...45

References…………………………………………………………………………………………………………….72

3 Chapter three: Factor Bias Spillover Effect of FDI in China………………………………..76

3.1 Introduction……………………………………………………….…………………………………………….76

3.2 Literature review………………………………………………………………………………………………..85

3.3 Data……………………………………………………………………………………………………………..90

3.4 Model specification and Methodology………………………………………………………………………….93

3.5 Results and Interpretation……………………………………………………………………………..………..97

3.6 Conclusion…………………………………………………………………………………..…………………104

References……………………………………………………………………………………..……………………114

Page 6

v

4 Chapter four: Factors Influencing Energy Intensity in Four Chinese Industries………….…..118

4.1 Introduction…………………………………………………………………………………………………….118

4.2 Energy Consumptions and Development Policies in Four Chinese Industries………..…………..…...………122

4.3 Literature Review & Research Hypothesis………………………………………………………….………….126

4.4 Data…………………………………………………………………………………………………………….130

4.5 Model Specification…………………………………………………………………………………………….132

4.6 Results and Interpretation………………………………………………………………………………………134

4.7 Robustness Analysis…………………………………………………………………………………………….139

4.8 Conclusion…………………………………………………………………………………………………...…141

References…………………………………………………………………..…………………………………….....155

Page 7

vi

List of Figures

Figure 2.1 Annual Growth Rate in Each Chinese Region (1992-2004)………..……….……....49

Figure 2.2 FDI in Eastern China…………………………………………………………………49

Figure 3.1 FDI in China (Year 1981-2004)………………………………………………..…...106

Page 8

vii

List of Tables

Table 2.1 Shares of LMEs and Balanced-LME sample in Aggregate industry, 2004……………….…..50

Table 2.2 Region summary: Basic statistics……………………………………………………………...51

Table 2.3Region summary: Total investment in fixed assets in China by regions………………………51

Table 2.4 Industry distribution by regions………………………………………………………………..52

Table 2.5Technology development expenditure by regions, 1995-2004…………….………………..….53

Table 2.6 Foreign Capital Shares by region, 1995-2004……….…………………………………...……53

Table 2.7 Horizontal and Vertical Industry Stocks……………………………………………………….54

Table 2.8 Within-region and outside-region spillover effect……………………………………….…….55

Table 2.9 Timeline of the Eastern Regional Preferential Policies………………………………..………56

Table 2.10 Regression Results (North)………………………………………….……..………..………...57

Table 2.11 Regression Results (Northeast)…………………………………………………..……………58

Table 2.12Regression Results (East)……………………………………………………………….……..59

Table 2.13 Regression Results (South)……………………………………………………………………60

Table 2.14 Regression Results (Southwest)……………………………………………………………….61

Table 2.15 Contribution to the Change in Total Cost, 1995-2004 (North)…………….………………….62

Table 2.16 Contribution to the Change in Total Cost, 1995-2004(Northeast)……………..……………..63

Table 2.17 Contribution to the Change in Total Cost, 1995-2004(East)…………………………...……..64

Table 2.18 Contribution to the Change in Total Cost, 1995-2004(South)………………………...………65

Table 2.19 Contribution to the Change in Total Cost, 1995-2004(Southwest)………………….…….….66

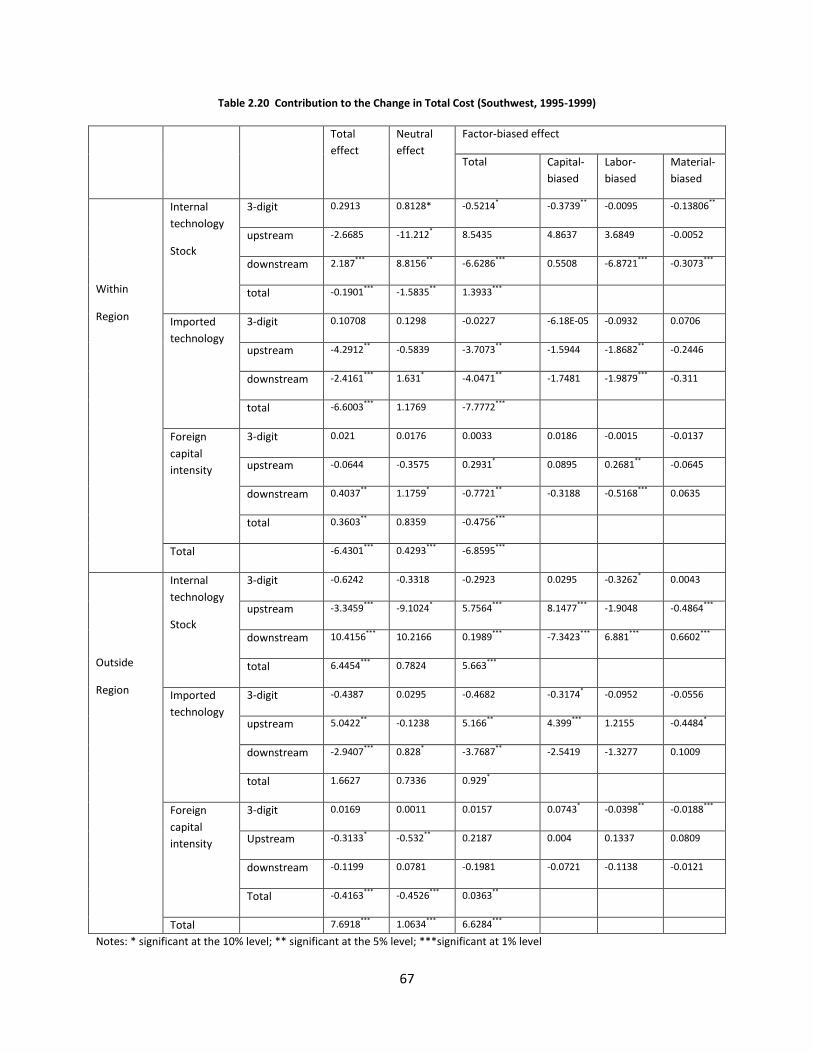

Table 2.20 Contribution to the Change in Total Cost, 1995-2004, (Southwest, 1995-1999)……………..67

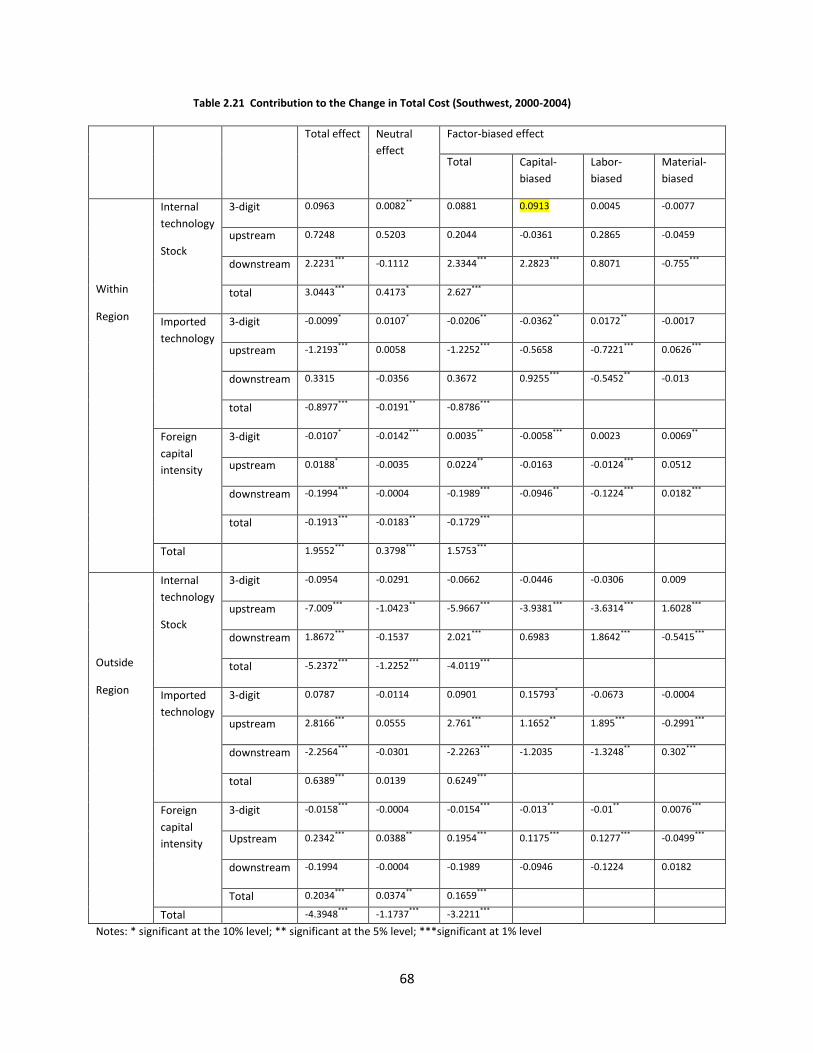

Table 2.21Contribution to the Change in Total Cost, 1995-2004, (Southwest, 2000-2004)………….…..68

Table 2.22 New Product innovation expenditure of an average firm in the Northeast……………….…..69

Table 2.23 Ratios of new product innovation expenditure over total cost…………………………….....69

Table 2.24 Total investment in the Northeastern Region, by regions……………………………….……70

Table 2.25 Ratios of technology development personnel to total employees……………………….……70

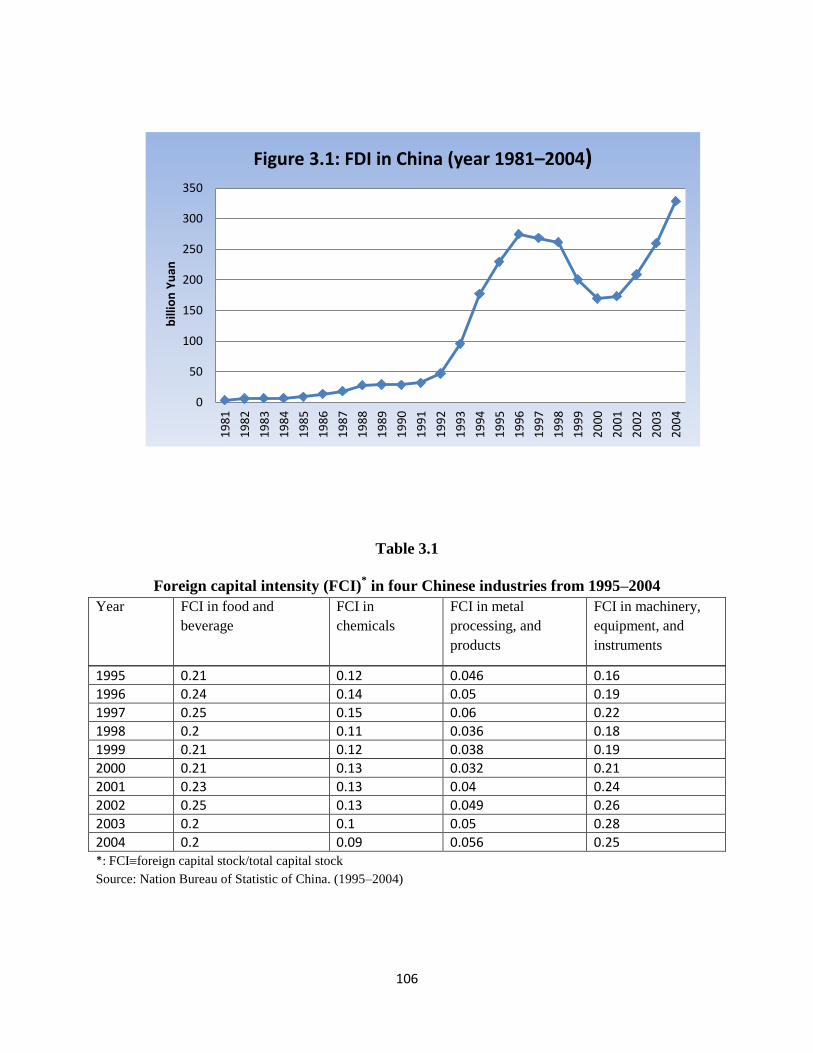

Table 3.1 Foreign capital intensity (FCI) in four Chinese industries from 1995–2004……………..….106

Page 9

viii

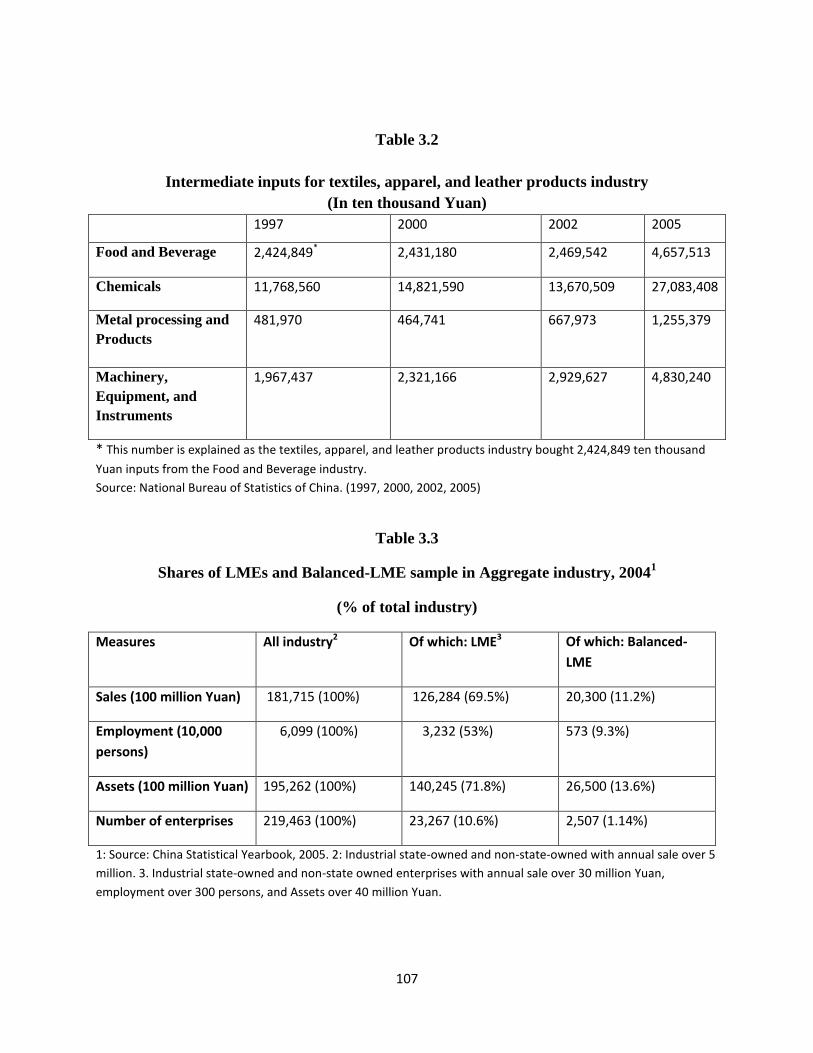

Table 3.2 Intermediated inputs for textiles, apparel, and leather products industry (in ten

thousands Yuan)…………………………………………………………………………….....107

Table 3.3 Shares of LMEs and Balanced-LME Sample in Aggregate Industry, 2004………………….107

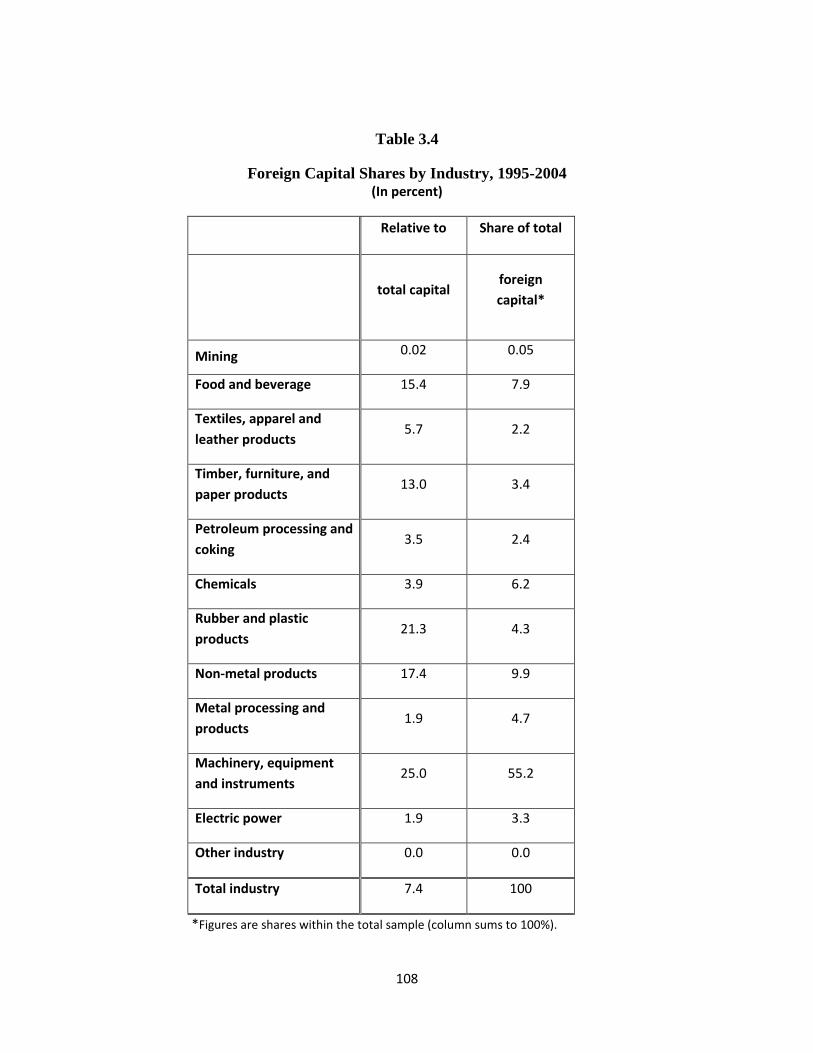

Table 3.4 Foreign Capital Shares by Industry, 1995-2004.……………………………………………...108

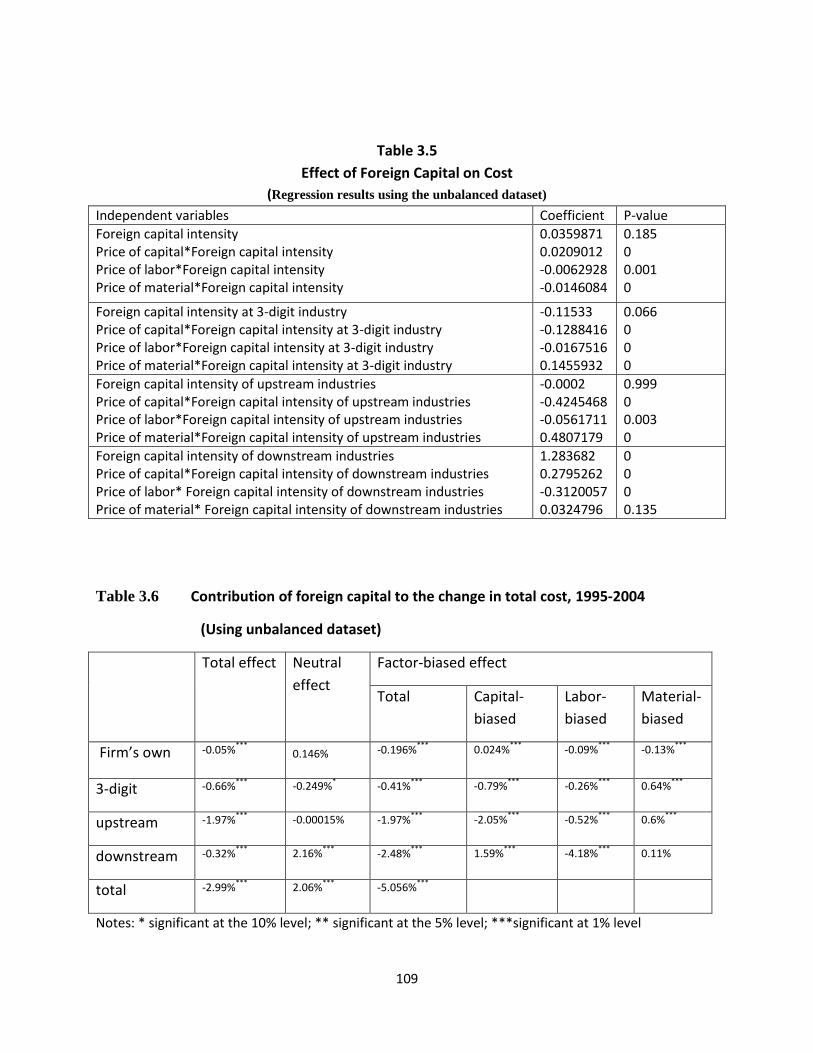

Table 3.5 Effect of Foreign Capital on Cost (on unbalanced data)………………………………………109

Table 3.6 Contribution of foreign capital to the change in total cost, 1995-2004………………...……..109

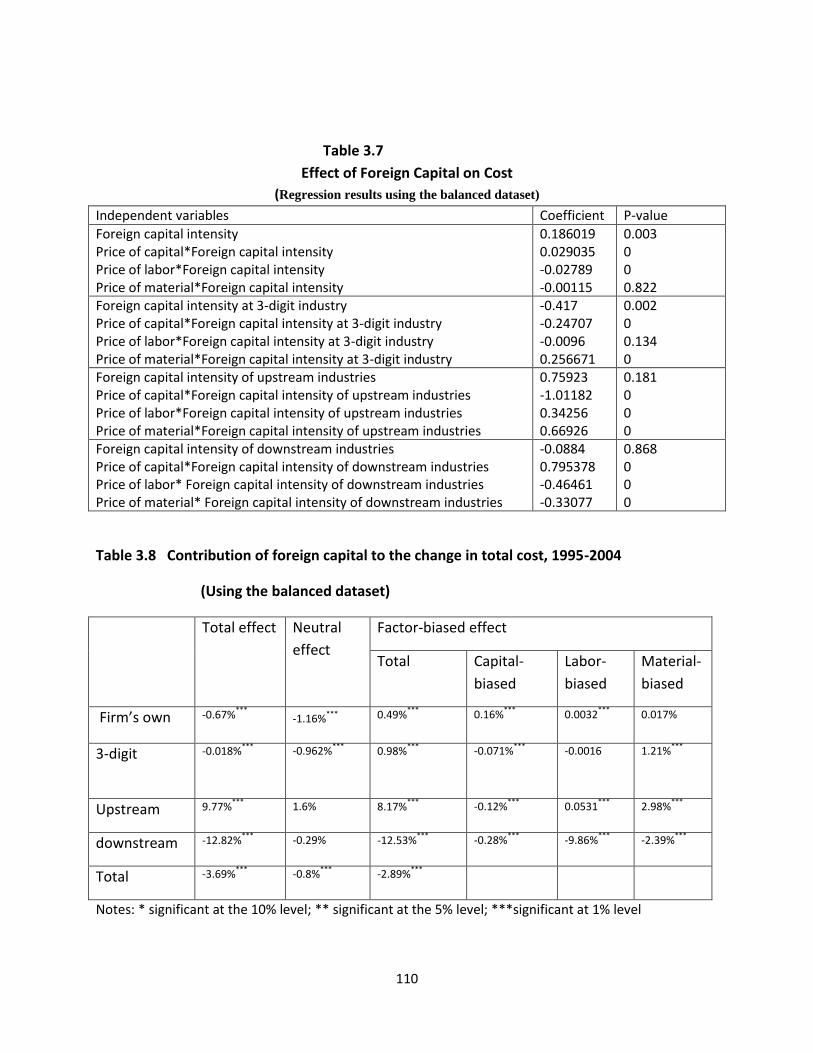

Table 3.7 Effect of Foreign Capital on Cost (on balanced data)…………………………………………110

Table 3.8 Contribution of foreign capital to the change in total cost, 1995-2004……………………….110

Table 3.9 Effect of Foreign Capital on Cost: 1995-2001 versus 2002-2004 (on unbalanced data)….….111

Table 3.10 Effect of Foreign Capital on Cost: 1995-2001 versus 2002-2004 (on balanced data)……...112

Table 3.11 Employment of China Urban from year 1995 to year 2004……………………………....…113

Table 4.1 Firm distribution by ownership type (number of enterprises)……….……………………..…143

Table 4.2 Firms distribution by region (number of enterprises)………………………………..…….….143

Table 4.3 Intensity of Foreign capital and R&D stocks by industry, 1999-2004………………..………144

Table 4.4 Number of firms during 1997-2004, by missing year observations………………….………144

Table 4.5 Comparison of firm sizes in unbalanced dataset and balanced dataset, year 2004………..…145

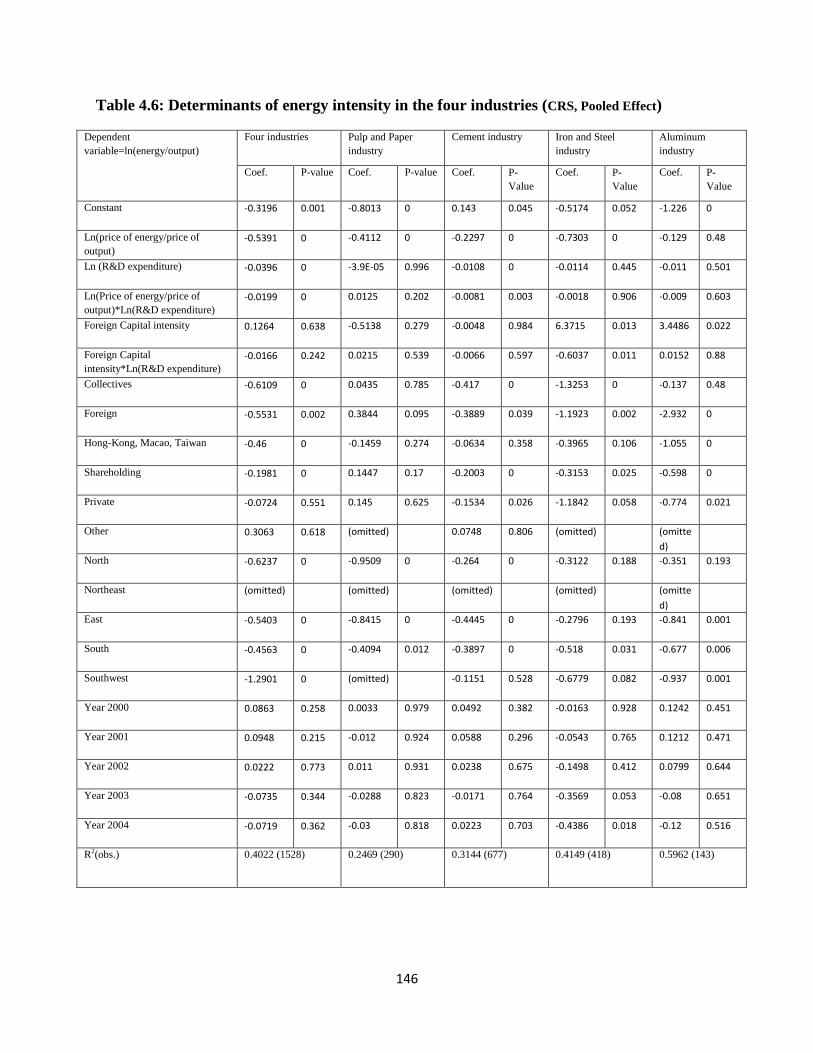

Table 4.6 Determinants of energy intensity in the four industries (CRS, Pooled Effect)……………....146

Table 4.7 Determinants of energy intensity in the four industries ( CRS, Fixed Effect)………………..147

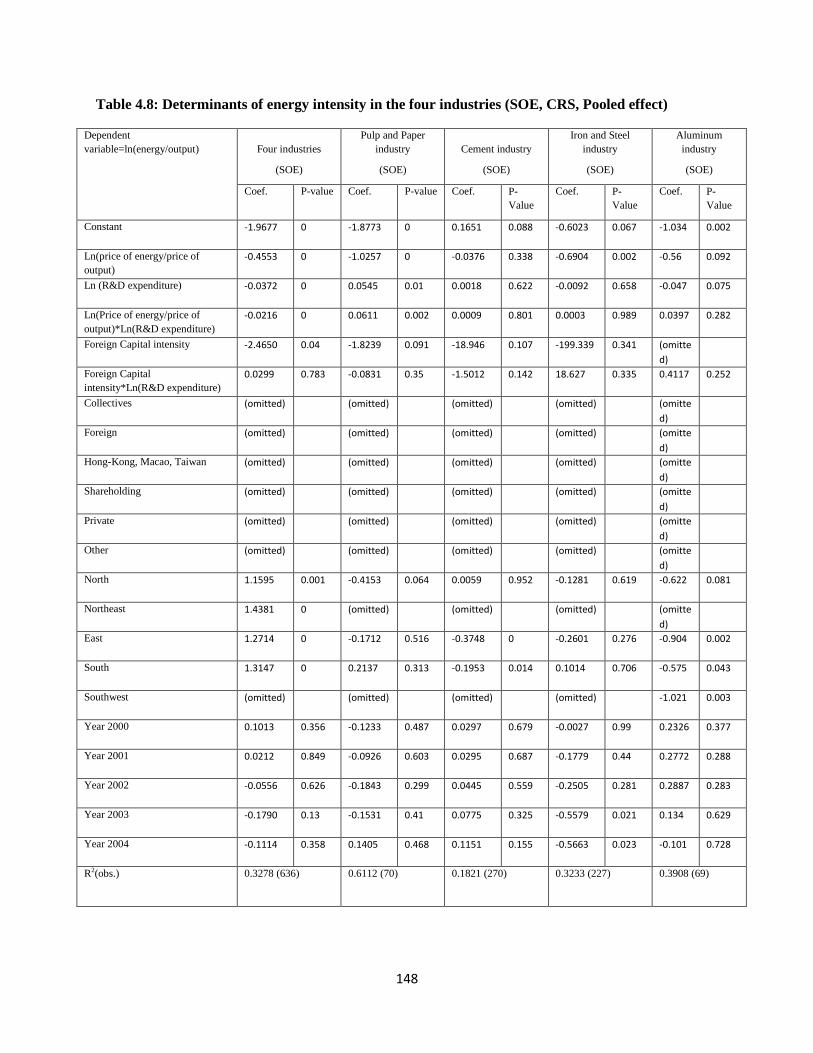

Table 4.8 Determinants of energy intensity in the four industries (SOE, CRS, Pooled effect)…………148

Table 4.9 Determinants of energy intensity in the four industries (NonSOE, CRS, Pooled effect)…….149

Table 4.10 Determinants of energy intensity in the four industries (1999-2001, CRS, Pooled

effect)…………………………………..…………………………………………...………..150

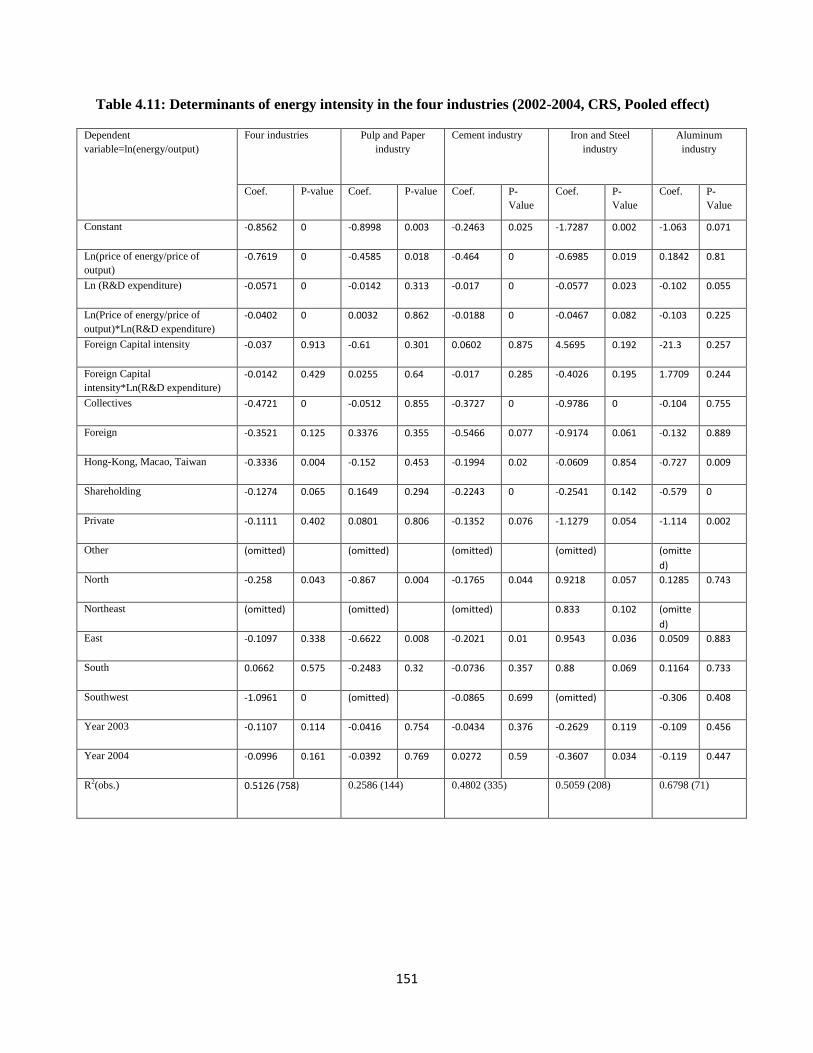

Table 4.11 Determinants of energy intensity in the four industries (2002-2004, CRS, Pooled

effect)……………………………………...……………………………….………………..151

Table 4.12 Determinants of energy intensity in the four industries (NonCRS, Pooled Effect)………....152

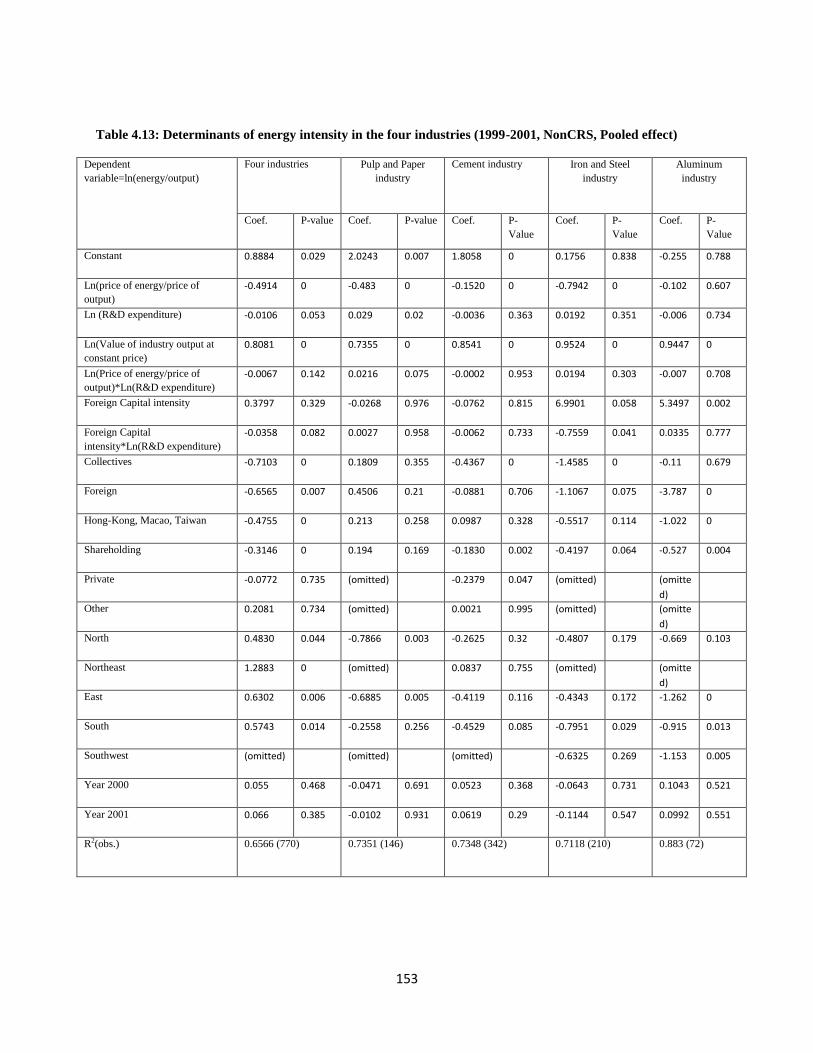

Table 4.13 Determinants of energy intensity in the four industries (1999-2001, NonCRS, Pooled

effect)…………………………………………………………………………...…………..153

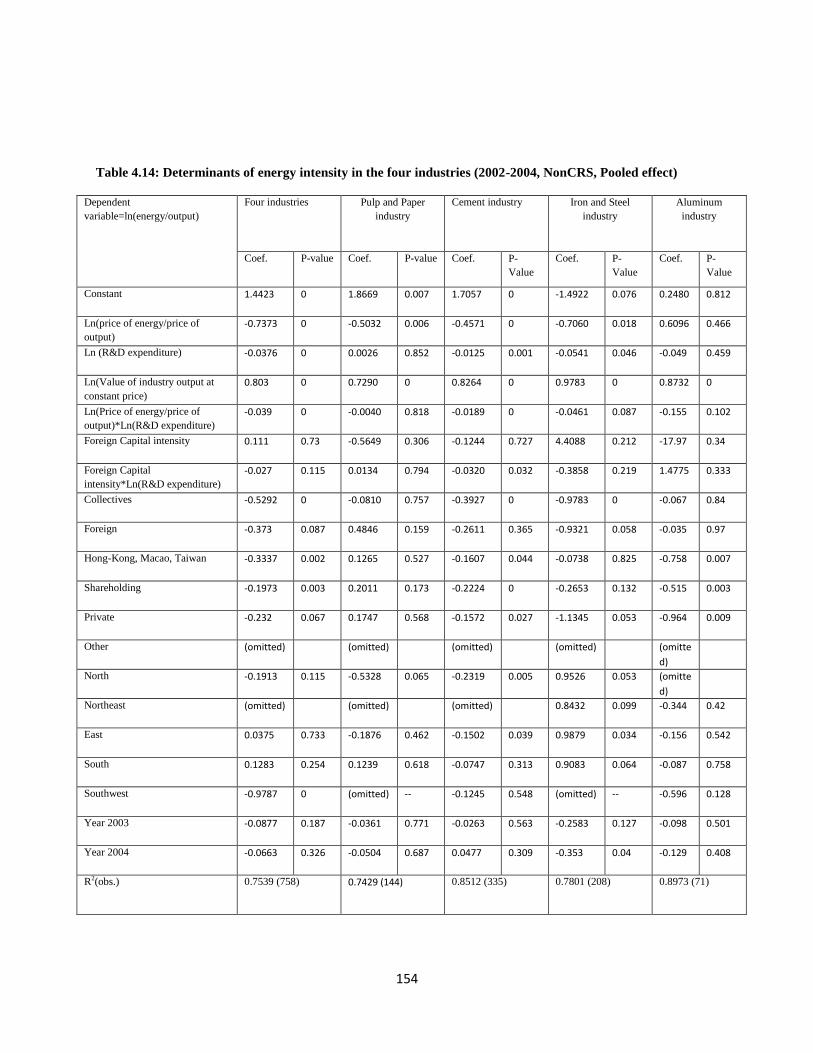

Table 4.14 Determinants of energy intensity in the four industries (2002-2004, NonCRS, Pooled

effect)……………………………………………………………………………………….154

Page 10

ix

Acknowledgements

I am grateful to many people for their encouragement, guidance, and helpful insights during my

dissertation writing. Particularly, I express my deepest gratitude to my advisor Dr. Karen Fisher-

Vanden for making this dissertation possible. Not only she helps me in my dissertation through

providing me many precious comments and revising many intermediate drafts, but also grants me

with life-long treasure by training me to be a good researcher. I feel so fortunate with my advisor. It

would have been next to impossible to write this thesis without her help and guidance. I am also

grateful to other committee members: Dr. David Abler, Dr.Spiro E. Stefanou, and Dr. Zhen Lei, who

provide profound suggestions into this dissertation. Last but not least, I owe special thanks to my

family, who provide support and encouragement throughout the years of my study at Penn State.

Page 11

1

Chapter 1

Introduction

1.1 Background and Motivation

Since the “Open-Door” policy and economic reforms began in the late 1970s, China’s economy

has undergone extraordinary growth, and its GDP rank in the world has risen from 10th in 1978

to second in 2011. However, in the past decade, China’s economic growth heavily depended on a

large increase in the use of inputs. Many economists argue that in the near future China will face

a growth limit, and its current high growth rate will be unsustainable unless its technology

largely improves during the next ten years (Ernst et al, 2005). Therefore, an essential focus for

Chinese enterprises is technological innovation and an increase in their knowledge stocks.

Among different methods to increase knowledge stocks, in-house research and development

activities, imported technologies, and foreign direct investment (FDI) will be examined in this

essay. In-house R&D focuses on process innovation, which utilizes the country’s comparative

advantage to reduce its production costs, while imported technologies concentrate on

development of new products, which reward firms with great advantages, such as obtaining

higher profits or attracting customers’ minds, in the market competition. Besides these direct

impacts on a firm’s knowledge stocks, a firm’s in-house R&D and imported technologies, as

well as FDI, also influence other firms’ knowledge stocks through spillovers.

Much previous literature investigated whether or not local firms benefit from spillovers from

other firms ’R&D activities and advanced technologies (Coe and Helpman, 1995; Hu and

Jefferson, 2002; Kokko, 1994). However, most of these studies encompass the entire country. In

the first essay, we extend this analysis of spillover effect to the regional level. This extension is

Page 12

2

also motivated by the fact that the economic disparity among five Chinese regions remains

significant in the recent years; therefore, investigating regional technological spillovers’

interactions with regional economies in China is important.

Foreign direct investment in China has experienced impressive growth in foreign direct

investment (FDI) over the past thirty years, expanding from less than 10 billion Yuan in 1980 to

approximately 330 billion Yuan in 2004 (NBSC, 2005). Although foreign firms may impose an

intense competition on Chinese domestic firms, such as taking away a portion of Chinese

domestic market share from local firms and raising payments for skilled workers, they

undoubtedly enhance the productivity of Chinese firms in several ways: The international

standards of research environment provided by the multinational companies will attract a large

number of world-class technical experts to work in China. The movement of experts across

different R&D institutions and the cooperation between multinational companies and local

companies will accelerate the diffusion of technological information. The exemplary role of

multinational R&D institutions will provide local enterprises with expertise in management and

marketing.

Therefore, combining the competition effect (crowding-out effect) and the positive effect (such

as knowledge spillovers and movement of experts), determining whether or not FDI eventually

brings benefits to host country is difficult to determine, despite investigation by much empirical

literature. However, few studies examined the effects of FDI on the direction of technological

development and firms’ decisions for choices of inputs.

One well-known hypothesis of biased technological change is the induced innovation hypothesis,

which posits that changes in the prices of input factors will spur technology development toward

Page 13

3

economic use of the input factor which becomes relative inexpensive (Hicks, 1932). Therefore,

price changes in input factors affect a firm’s decision regarding R&D investment and efforts, and

influences the rate and direction of innovation, resulting in biased technological change. In the

case of foreign firms investing in an upstream industry, more intense competition occurs in the

intermediate inputs’ market, and consequently, engenders cheaper intermediate inputs for

downstream firms (Mankiw, Principles of Economics). According to the induced innovation

hypothesis, cheaper intermediate inputs (material) affect firms’ decisions towards the direction of

material-using innovation. Based on this observation, we will empirically examine whether or

not the presence of FDI in an upstream industry induces downstream local firms to develop new

technologies with a material-using bias.

More generally, inspired by Acemoglu (2002), who argued that the bias for technological change

slants toward particular factors, the second essay investigates the factor bias spillover effect of

FDI in China. Specifically, the examination considers how domestic enterprises’ guide the

direction of their technological developments (in choosing capital, labor, or material inputs) in

response to the presence of FDI in a horizontal industry, an upstream industry, or a downstream

industry.

During the past thirty years, China’s economy has undergone remarkable growth at an average

annual rate of 9.7% (He and Wang, 2007). Such rapid economic development drove an increase

in Chinese total energy use. However, China’s energy intensity, the ratio of total energy

consumption in physical quantities to real GDP, has steadily declined, on average, 3.6% annually

from 1993 to 2005 (He and Wang, 2007).

Page 14

4

Several factors may account for the change. The first factor is technological change, including

subsector productivity changes and R&D input. For example, Ma and Stern (2008) found

technological change to be the most important factor in reducing the energy intensity of Chinese

enterprises from 1980 to 2003. The second factor is the spillover effect of FDI. Fisher-Vanden et

al. (2004) asserted that the energy intensity of foreign firms in China, on average, is lower than

that of local firms. Empirical results in Fisher-Vanden et al. (2009) showed that spillover effects

of FDI tend to save energy. He and Wang (2007) also provided empirical evidence to suggest

that foreign capital has had an effect on lowering the energy intensity of Chinese enterprises. The

third factor is market reform, including structural changes to production and governmental

ministries’ changes. Fisher-Vanden et al (2004) found that sectoral shift has improved

enterprises’ energy efficiency. These researchers’ empirical results indicated that sectoral shift

accounted for almost 50% of the decline in total energy intensity during 1997 to 1999. Besides

these three factors, other elements, such as rising energy prices and scale effects, may have

impacted the change in energy intensity in China.

Other numerous previous studies examined these factors’ effects on energy intensity in China;

however, most of them employed industry-level data or conducted aggregate, industry level

investigations. The third essay uses a unique set of firm-level data from China’s most energy-

intensive large and medium enterprises to investigate the impact of these factors on energy

intensity in four specific Chinese industries: pulp and paper, cement, iron and steel, and

aluminum. The reason for choosing these four industries is that they lead the nation in energy

consumption and comprise a large share of China’s industrial output. For instance, in 2007,

energy consumption in the Cement industry accounted for 5.6% of China’s total energy

consumption (Cai et al. 2011). China’s Iron and Steel industry became the largest producer of

Page 15

5

crude steel in the world in 1996 (Wei et al. 2007) and, more recently, has become the largest

energy consuming sector in the nation.

1.2 Objectives and Brief Outline

Many studies have investigated the spillover effect of R&D and FDI. However, few of them

explicitly distinguish the spillover effects generated from firms located in the targeted region

with the effects from firms located outside the targeted region. My first essay will contribute to

existing literature by: 1) do firms location and distance matter in spillovers, both within-region

spillover effect and outside-region spillover effect? 2) investigate the impact of regional

differences, including government policies, economic factors, and natural endowments, on

within-region and outside-region spillovers; 3) testing whether or not developed regions benefit

more from both within-region and outside-region spillover effects than less developed regions;

To complete these analyses, we divide China into five regions in terms of geographic location

and level of economic development (GDP, infrastructure and household income, etc.). Then we

categorize technological innovations into three types: internal technology development within-

firm, purchases of imported technology, and foreign direct investment (FDI). We distinguish

between “within-region” spillover effects from industries located in the same region as the

targeted firm, and “outside-region” spillover effects from industries located outside the region of

the targeted firm. These two region-related spillover effects track the horizontal and vertical

spillover effects of three forms of technological activities. Using a balanced, firm-level dataset,

which contains 2000 large- and medium- sized Chinese enterprises during 1995 to 2004, we run

Page 16

6

a seeming unrelated regression to obtain the empirical results. We end the first essay with an

interpretation of the results.

The second essay investigates the factor biased FDI spillover effect through vertical linkages (i.e.

the effect of upstream foreign capital on downstream Chinese local firms, and, conversely, the

effect of downstream foreign capital on upstream local firms). An additional examination

considers domestic firms’ bias direction of technological development if foreign firms enter the

same industry as domestic firms.

Moreover, the investigation considers the impact on FDI spillover, caused by China’s joining of

the World Trade Organization (WTO) in 2001. In order to complete this analysis, we divide our

data set into two periods: 1995 to 2001 and 2002 to 2004; we then run the corresponding

regression for each dataset and compare the spillover during different time periods to investigate

the impact of China’s joining of the WTO on FDI spillover.

The third essay investigates the factors that explain the decline in energy intensity in four

Chinese industries: pulp and paper, cement, iron and steel, and aluminum. Completing this

analysis requires, first, outlining energy consumption and developmental policies in these four

industries and identifying the important industrial-common or industrial-specific policies, which

induce changes in energy intensity in these four industries. A summary of previous research

analyzing China’ energy intensity decline follows. After these two steps, we will use a unique set

of firm-level data to empirically examine how China’s energy-saving programs, liberalization of

domestic markets, openness to the world economy, and other government policies’ contributions

to the decline in energy intensity in these industries. We conclude this essay with an

interpretation of the results and a test for robustness.

Page 17

7

References:

Acemoglu, Daron, 2002, “Direct Technical Change”. Review of Economic Studies, 69, 781-809

Cai, Bofeng, Dong Cao, Ying Zhou, and Zhangsheng Zhang, 2011, “Characteristics Analysis of Energy

Consumption in Chinese Cement Industry.” Environment Engineering, vol. 2.

Coe, David T and Elhanan Helpman, 1995, "International R&D spillovers", 1995, European economic review, 39(5)

Ernst, Dieter, Thomas George Ganiatsos, and Lynn Krieger Mytelka, 2005, Technological Capabilities and Export

Success in Asia, Taylor & Francis e-Library

Fisher-Vanden, Karen, Gary H. Jefferson, Yaodong Liu, and Jinchang Qian, 2009, “Open Economy Impacts on

Energy Consumption: Technology Transfer & FDI Spillovers in China’s Industrial Economy,” manuscript,

Pennsylvania State University

Fisher-Vanden, Karen, Gary Jefferson, Hongmei Liu, and Quan Tao, 2004, “What is Driving China’s Decline in

Energy Intensity?” Resource and Energy Economics, 26: 77-97

He, Canfei, and Junsong Wang, 2007, “Energy Intensity in Light of China’s Economic Transition.” Eurasian

Geography and Economics, 48(4): 439-468

Hicks, J. R., 1932, The Theory of Wage, Macmillan, London

Hu, Albert, G., and Gary Jeffersons, 2002, “FDI Impact and Spillover: Evidence from China’s Electronic and

Textile Industries.” The World Economy, 25(8): 1063-1076

Kokko, Ari, 1994, “technology, market characteristics, and spillover,” Journal of Development Economics, 43(2):

279-293

Ma, Chunbo and David I. Stern, 2008, “China’s Changing Energy Intensity Trend: a Decomposition Analysis.”

Energy Economics, 30:1037-1053

Mankiw, Gregory, Principles of Economics, South-Western College Pub, 5 Edition

NBSC, 2005, China Statistical Yearbook on Science and Technology, Beijing, China Statistical Press.

Wei, Yi-Ming, Hua Liao, and Ying Fan, 2007, “An Empirical Analysis of Energy Efficiency in China’s Iron and

Steel Sector.” Energy, 32(12): 2262-2270.

Page 18

8

Chapter 2

Regions Development and Technology Spillover in China

2.1 Introduction

Since the onset of economic reform in the late 1970s, the Chinese economy has experienced

phenomenal economic growth. However, due to disparities in region-specific endowments and

government policies across different regions, the growth in each region exhibits great

heterogeneity. Using the zoning codes adopted by the National Bureau of Statistics of China

(NBSC), we combine China provinces into five regions: North, Northeast, East, South and

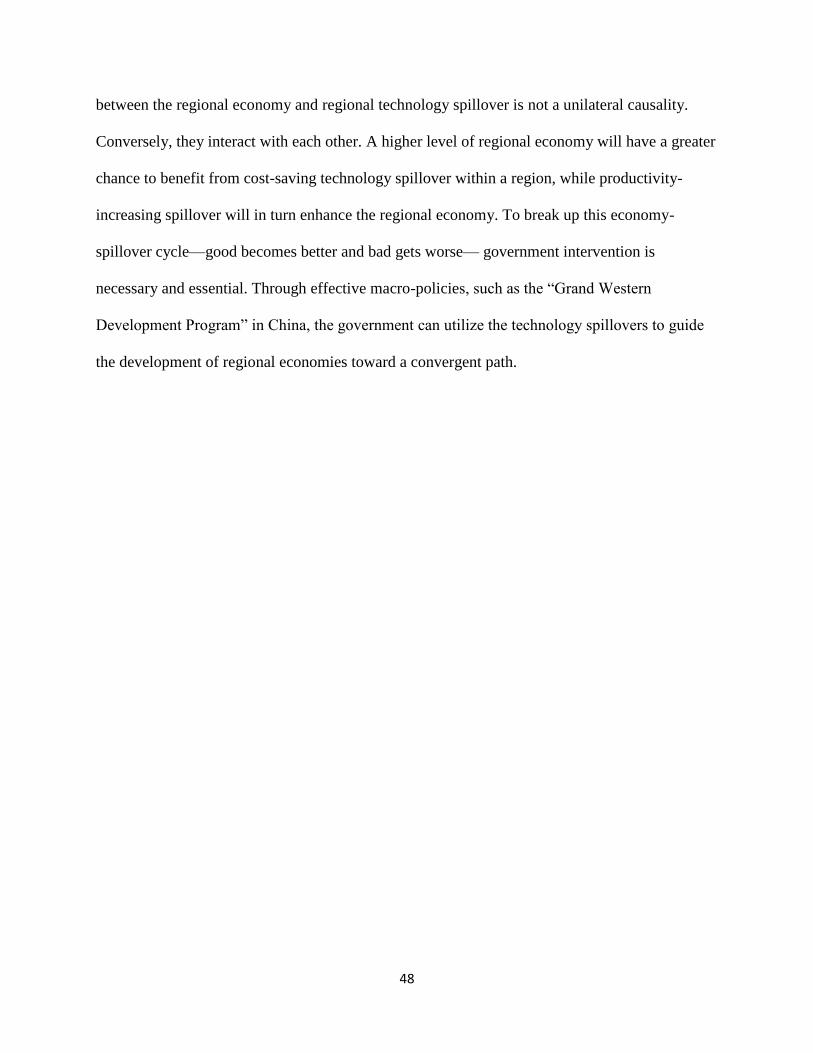

Southwest. Figure 2.1 lists the annual growth rate of per capita income in each region over the

period 1992-2004.1 Three features capture our attention: the growth rate of per capita income in

the Southwest is not far behind those of other regions except the East, which is somewhat

surprising since the Southwest had the worst infrastructure and lowest per capita income in the

early years of economic reform2. The Northeast had the lowest growth rate during this time

period and the East had the highest growth rate during this period.

What factors account for the disparities in GDP growth rates across different regions? Initial

economic status, government preferential policies, and natural endowments are some of the

factors affecting regional growth. However, differences in the level of the technological advance

play a critical role in explaining the difference in growth rates among regions. Technology

1 The reason that we choose per capita income instead of GDP in each region as a proxy to regional economy is that

there are huge differences among different regions in term of population and number of provinces. For example, the

Northeast only consists of 3 provinces while the East consists of 7 provinces. Per capita income is more likely to

truly exhibit the economic development status in each region.

2In year 1992, Per capita income is 1435 Yuan in the Southwest, 2026 Yuan in the South, 2564 Yuan in the North,

2668 Yuan in the East, and 2908 Yuan in the Northeast.

Page 19

9

development activities in each firm not only have significant impacts on their own productivity,

but also bring spillover effects to firms operating in horizontal, upstream, downstream industries.

In this essay, we will focus on how the within-region and outside-region technology spillovers

differ across regions, how these different regional spillovers affect the economic disparity in

regional growth, and what factors cause these differences in regional spillovers.

There have been many studies that investigate the spillover effects of R&D activities and FDI;

however, they did not explicitly distinguish between within-region and outside-region effects.

For example, there is a vast amount of literature that focuses on examining whether host

countries, as an entire country, benefit from spillover effects (Shen, 1999; Hubert and Pain, 2001;

Liu, 2002). We will extend this work to regional cases and test how local firms’ costs are

affected by spillover effects both within and outside Chinese five regions. There are also many

previous studies investigating through which channels, for example, horizontal channel and

vertical channel, spillover effects have the biggest impact on host countries ( Blalock and Gertler,

2003; Jacorvik, 2004; Fisher-Vanden et al 2009). We will extend the comparison between

horizontal spillovers and vertical spillovers to the cases of within and outside regions, and test

whether vertical spillovers still have bigger impacts on local firms than horizontal spillovers. A

few studies conduct research on the regional spillover effects, including on Chinese regions

( Bottazzi and Perri, 1999; Brun, 2002; Kuo and Yang, 2008; Qi et al, 2009). In our paper, we

will test whether developed regions will benefit more from both within-region and outside-region

spillover effects than less developed regions.

Page 20

10

In this paper, using the zoning codes adopted by the National Bureau of Statistics of China

(NBSC), we categorize Chinese provinces into five Chinese regions -- North, Northeast, East,

South and Southwest -- and calculate the within-region R&D stock and outside-region R&D

stock using the science and technology data obtained from NBSC. Applying the seeming

unrelated regression method, we empirically calculate the different spillover effects of

innovation expenditures. We subdivide innovation expenditures into three categories: internal

technology expenditure, imported technology expenditure, and foreign direct investment (FDI).

We then compare among different regions to assess both spillover effects generated within the

region and those transferred from other regions.

Results of within-region total spillover effects and outside-region total spillover effects show that

the cost-saving spillover effects in both developed and less developed regions mainly come from

upstream and downstream industries. Results of outside-region spillover effects suggest that

distance and economic similarity do matter in the outflow of technology and knowledge across

regions. The result – that the Eastern region benefits significantly from within-region total

spillovers – is consistent with previous results, which found spillovers in developed countries

exhibit positive effects, due to mature markets and infrastructure. Results for the Northeastern

and Southwestern regions confirm the influence of two Chinese development policies: the

“Grand Western Development Program” and “Revitalizing the Old Industrial Base in the

Northeast”. Both helped to reduce the regional development inequality, and one of them has

already contributed to the inland firms’ productivity improvement through more effective

spillover effects.

The rest of paper is organized as following: Section 2 review the literature, in which I briefly

introduce previous studies on technology spillover effects. Section 3 introduces the data used in

Page 21

11

the analysis along with data descriptions. Section 4 presents the model specification and

methodology. Section 5 exhibits the empirical results and interpretation. Lastly, Section 6 offers

concluding remarks.

2.2 Literature review

There is much debate about whether firms will benefit from the technological spillover. For

example, Jacorvik (2004) finds FDI spillover effects in developing countries are not significant

and sometimes even negative. Hu and Jefferson (2002) find negative spillover effects in China’s

electronic and textile industry. In contrast, Coe and Helpman (1995) find that foreign R&D

spillovers increase domestic firms’ productivity. Jacob and Szirmai (2007) find that knowledge

spillovers in Indonesia largely increase labor productivity. Hubert and Pain (2001) use industry-

level panel data of the UK manufacturing sector to examine the effects of FDI. Results show that

FDI has a positive impact on UK firms through intra-industry and inter-industry spillover.

Shen(1999) contends that a one per cent increase in foreign direct investment in China will

increase total factor productivity (TFP) in China by 37 percent through technology spillover

effects.

In addition to examining whether local firms gain from spillover effects, many previous studies

have investigated whether spillover effects are intra-industry or inter-industry. Saxena (2011)

finds empirical evidence of horizontal spillover effects in the manufacturing industry in India.

Bin (2008) also finds that horizontal R&D spillovers significantly improve firms’ productivity in

China’s manufacturing industry. Halpern and Muraközy (2007) examine whether FDI has

horizontal or vertical spillover effects on Hungarian domestic manufacturing firms. Employing a

Page 22

12

large amount of data from Hungarian firms, Halpern and Muraközy ran a regression of output on

capital, labor, a horizontal measure of spillover, and a vertical measure of spillovers. The results

showed positive vertical spillovers and no horizontal spillover effects, except for those firms in

close proximity with foreign-owned firms.

Javorcik (2004) proposed that spillover effects from downstream industries usually happen in the

following ways: the direct knowledge transfer from the downstream industry to the upstream

suppliers; indirect technology or managerial improvement forced by the higher quality standard;

and on-time delivery required by downstream customers. The empirical tests of Javorcik (2004)

confirm that local suppliers receive positive productivity spillover effects, such as technologies

transfer, from the downstream customers through the backward linkage. Using Chinese industrial

firm-level data, Fisher-Vanden et al (2009) found that spillover effects from downstream

industries have more impact on the total productivity of Chinese firms than in-house research

and horizontal spillover effects.

Some previous studies have examined the factors that affect cross-region spillovers. For example,

Jacobs (1969) argues tacit knowledge is difficult to transfer across distances and requires

significant interaction, such as face-to-face communication. Therefore, areas closer to those

sources of tacit knowledge will have a better chance to receive and understand knowledge

outflows. Adams and Jaffe (1996) and Adams (2002) show that spillover effects are affected by

the distance and the effects will be strongest within certain distances. Andretsch and Feldman

(2004) also find distance matters for technology spillovers and plays an important role in making

use of those knowledge outflows. Bottazzi and Peri (1999) use data on European regions to

investigate spatial spillovers of R&D as well as knowledge, and address the importance of such

diffusion on innovation. The regression results of Bottazzi and Peri (1999) show that pure

Page 23

13

technological similarities have fewer spillover effects than pure spatial distance. Absorptive

abilities are also important in determining cross-region spillovers. Qi et al (2009) explore the

feature of various absorptive abilities across different Chinese provinces. Qi et al believe that if

the gap between the local firms and foreign firms is too big, local firms will not have the

capacity to understand and absorb the outflow of advanced technology and knowledge: a

threshold of absorptive capacity determines whether the spillover can be assimilated. Empirical

results of Qi et al (2009) revealed the absorption abilities of many Chinese provinces had not

reached the necessary threshold to benefit from the presence of outside firms with high

technology and advanced managerial skills. The crowding-out effect of foreign capital may

prevail in many Chinese provinces.

The economic system and level of development of market economics, such as a financial market

and labor market, also play an important role in the process of digestion and absorption of

spillover effects originating from outside regions or countries. Alfaro et al (2010) postulate that a

mature financial market has a big impact on the FDI spillover effect, and their results show that

countries with such markets find it not only easier to integrate the spillover effect, but also to

gain more positive effects from the spillovers of foreign advanced technology than those with

poor financial market.

Several studies investigated spillovers across regions and effects specific to different regions.

Lehto (2007) finds that R&D of firms outside the region where the targeted firm is located but in

the same industry positively contribute to the productivities of the targeted firm. However,

Bottazzi and Peri (2003) find that spillovers are localized and exist only within a distance of

300km. There are several studies examining technology spillovers across Chinese regions. For

example, Brun et al (2002) investigate whether there are sufficient spillover effects from coastal

Page 24

14

provinces to inland provinces to achieve the Deng’s policy of using advanced coastal provinces

to boost western province economies. Their results reveal that spillover effects from coastal

provinces to inland provinces are not sufficient to reduce the regional disparities in China. Kuo

and Yang (2008) investigate the effect of knowledge capital (both R&D capital and technology

imports) and technology spillover on regional economic growth. Their results find a positive

impact of regional spillover effects on regional growth. This suggests that a well-developed

region will stimulate its neighbor’s economy, which will be confirmed in our results.

Based on these studies, we will test the following hypotheses in this paper:

Hypothesis 1: Based on previous studies, for example, Fisher-Vanden et al (2009), the spillover

effects from downstream industries have more impact on the total factor productivity of Chinese

firms than horizontal spillover effects; therefore we would expect that spillover effects generated

through vertical channels are more significant—either more cost-saving or more cost-decreasing-

--than effects generated through horizontal channels, both for within and outside the region.

Hypothesis 2: Based on the fact that local firms need to reach a threshold of absorptive ability in

order to effectively assimilate the spillover effect (Qi et al, 2009), and the fact that the Eastern

region has advanced factor markets and most imported technology expenditure and FDI in China,

we would expect the East to experience has received significant cost-saving within-region

spillover effects.

Hypothesis 3: Based on previous studies (Jacorvik, 2004; Hubert and Pain, 2001) which find

spillover of FDIs in developing countries to be not significant or even negative, we expect in our

empirical results that developed regions will receive more benefits from within-region spillover

effects than less developed regions. Specifically, we expect the benefit from the within-region

Page 25

15

spillover effect in the Southwest is the lowest among all five regions since the Southwestern

region is the poorest region and has the worst infrastructure among five Chinese regions in the

late 1980s.

Hypothesis 4: The Northeastern region has the highest ratio of capital in state-owned enterprises

to total capital3. However, state-owned enterprises in China have many shortcomings: low

efficiency and the lack of an effective incentive mechanism. Dual identity of SOEs’ CEOs, as

businessman and government officials, gives way to irrational behavior as these two objectives

may produce conflicting interests (Lin and Li, 2005; Chen et al, 2005). Therefore, we expect that

within-region and outside-region spillovers bring few benefits and may even increase total cost

of firms operating in the Northeastern region.

2.3 Data

Our dataset is firm-level panel data containing over 2000 large- and medium-size Chinese

enterprises during 1995-2004. This data is part of a survey annually updated by National Bureau

of Statistics of China. Data used in our regression merges two datasets: one consists of economic

and financial variables, covering around 22,000 large and medium-size firms4 over the ten year

period from 1995 to 2004. The other consists of science and technology variables. Among all

variables, our paper focuses on internal technology development and imported technology. The

former measure includes regular R&D spending, the expenditure for process innovation and

3Huang (2004) mentioned that assets of SOEs accounted for 79.34% of total assets in the Northeast Old Industrial

Base, which was much higher than the nation average of 60.93%. 4 National Bureau of Statistics of China defines large- and medium-size enterprises according to enterprise’s

production capacity or original value of fixed assets, see Table 2.1.

Page 26

16

quality improvement of existing products. The latter is the purchase of advance technology from

foreign countries.

Because the size of firms shrank during this time period, or due to the change of ownership

related to industry reformation, mergers, or changes of address, there are many exiting firms,

new entry firms, or changes of firm ID during the 10-year period. Therefore, many firms are

missing at least one observation during 1995-2004. In order to maintain the continuity of data,

necessary for the composition of R&D stock, we have to drop the firms that are not continuously

observed during 1995-2004 and create a balanced dataset consisting of only 2000 firms per year

during 1995-2004. This causes a significant drop of observations from the two original datasets

to the balanced dataset.5

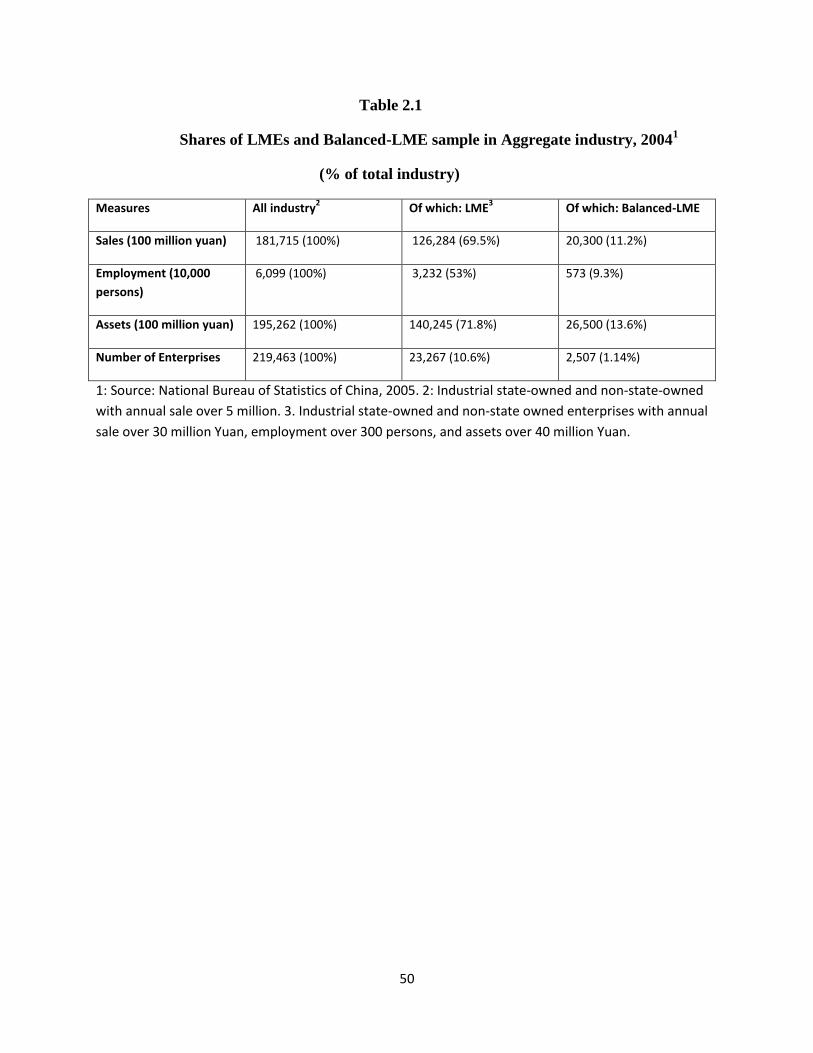

As in Table 2.1, we compare our “Balanced-LME sample” with both total industry and with

large- and medium-size enterprises data in three dimensions—sales revenue, employment, and

fixed assets. We find although our sample only contains slightly over one percent China’s

industrial enterprises with annual sales over 30 million Yuan, employment over 300 persons, and

total assets over 40 million Yuan, it captures 11.2 percent of industrial sales, 9.3 percent of

industrial employment, and 13.6 percent of industrial assets.

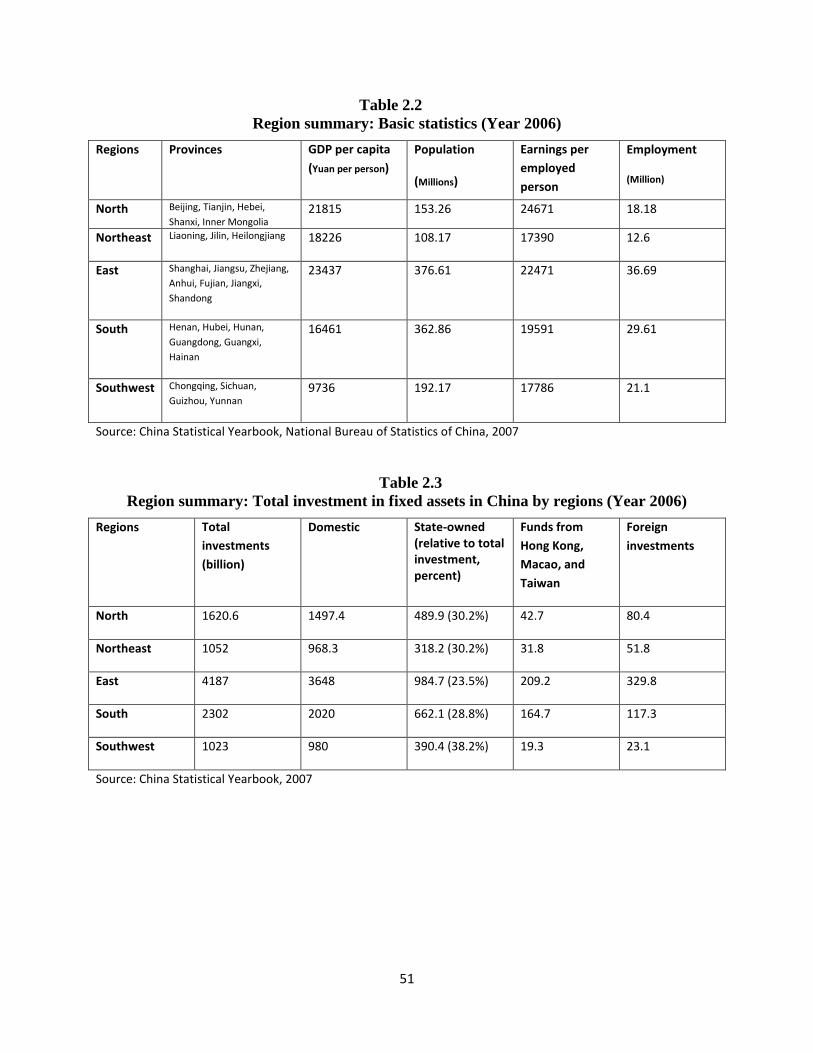

In Table 2.2 and 2.3, we provide summary statistics for each region. As shown, the East and

North are two richest regions while the Southwest is the poorest region in China in term of GDP

per capita or earnings per employed person. Table 2.3 shows that the East has the highest state-

owned investment while the percent to its own total investment is the lowest among five regions.

5We construct horizontal, upstream, downstream stocks based on the unbalanced dataset. For one specific industry,

we sum up all the technology expenditure flows of the firms operating in this industry. Then we use the perpetual

inventory method to convert the technology expenditure flow of the industry into the technology expenditure stock

of the industry. After the construction of horizontal stocks, we apply input-output tables to obtain upstream and

downstream stocks. Details are explained in the following subsections.

Page 27

17

The Southwest is exactly opposite: its state-owned investment is the lowest among five regions

while its ratio of state-own investment over total investment is the highest.

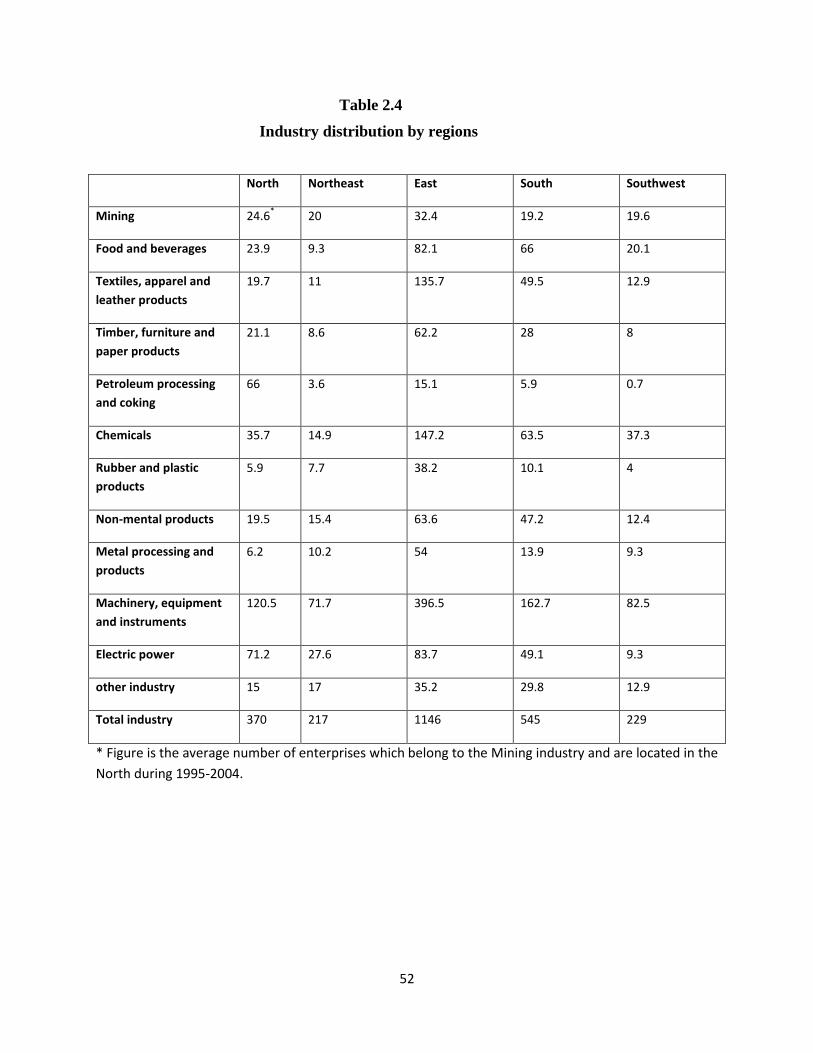

As shown in Table 2.4, over fifty percent of firms in our dataset are located in the Eastern region.

In all five regions, the machinery, equipment and instruments industry contains the largest

number of firms. As shown in Table 2.5, the firms in the Eastern region own the largest stock of

technology development expenditures, 51.4 percent of internal technology development, and

48.7 percent of imported technology expenditure. The Northeastern region has the lowest ratio of

total technology development expenditure, the sum of internal technology development

expenditure and imported technology expenditure, to the value of industrial output at constant

price among the five regions. Table 2.6 shows that the East captures 46 percent of total foreign

capital in China and is the region with the most foreign capital in China. The second region is the

North with a share of 19.2 percent of total foreign capital in China. The Southern region is the

region with the highest foreign capital intensity—foreign capital over total capital, followed by

the East.

2.3.1: Stock of technology development expenditure

For estimation purposes, we use the perpetual inventory method to construct stocks of

technology development expenditure for each firm in our data set. The stocks are constructed as

the accumulation of reported technology development expenditures minus depreciation; i.e.

KR,i,t = (1-δ)KR,i,t-1 + IR,i,t-1

where

KR,i,t ≡ stock of R&D of firm i at time t;

Page 28

18

IR,i,t-1 ≡ flow of R&D expenditures of firm I at time t-1; and

δ ≡ depreciation rate (assumed to be 15%).

The NBS data set covers the flow of technology development expenditures over the period 1995-

2004. We estimate KR,i,1995 as followings:

KR,i,1995 = IR,i,1995 / (δ+γ)

where γ is the growth rate of IR estimated as the average annual growth rate of the 2-digit

industry of firm I during 1995-2004.

2.3.2: “Within-region” technology development expenditure and FDI intensity

A: Horizontal

, are stocks of internal technology development

expenditure, and imported technology expenditure, respectively, in a firm’s 3-digit SIC industry

within its region. First, we will construct the flows of internal technology development

expenditure, and imported technology expenditure, respectively, in the industry within a firm’s

region. They are the sum of flows of internal technology development expenditure, and imported

technology expenditure, respectively, of firms which meet two conditions: they should belong to

the same 3-digit SIC industry as the targeted firm and they should belong to the same region as

the targeted firm. Then we apply the perpetual inventory method to convert these flows of

internal technology development expenditure (imported technology expenditure) in the industry

within region into stocks of internal technology development expenditure (imported technology

expenditure) in the industry within region.

Page 29

19

is the foreign capital stock intensity of firm’s 3-digit SIC industry within

region constructed as follows:

Where is the foreign capital stock in the firm’s 3-digit SIC industry within

region, which is the sum of foreign capital stocks of firms which satisfy the two conditions

defined above.

is total capital stock in the firm’s 3-digit SIC within region, which is the sum of

total capital stocks of firms which meet the two conditions defined above.

B: vertical

, are the weighted average stocks of internal

technology development expenditure, and imported technology expenditure, respectively, in a

firm’s 2-digit SIC upstream industries within region. Suppose the targeted firm’s 2-digit SIC

upstream industries are industry i, where i ranges from 1 to I. The input-output share for industry

i to the targeted firm is . Suppose the stock of internal technology development expenditure of

industry i within the same region with the target firm is

( ) ∑

A similar formula was applied to construct , , and

Page 30

20

, are the weighted average stock of foreign capital, and total

capital, respectively, in firm’s 2-digit SIC upstream industries within region. The construction of

these two stocks are identical to the construction of .

is the weighted average of foreign capital intensity in firm’s 2-digit SIC

upstream industries within region and is constructed as follows:

The construction procedure of , the weighted average of foreign

capital intensity in firm’s 2-digit SIC downstream industries within region, is almost identical to

the construction of except that we use downstream industries instead of

upstream industries.

2.3.3: “Outside-region” technology development expenditure and FDI intensity

We approximate the distance of two provinces by the distance between their capitals (Kuo and

Yang, 2008). After we obtain the distance of two provinces, we use the following equation to

construct the distance between two regions which usually contain several provinces:

∑

Where

is the distance between region k and region l

is the distance between province i and province j

is the GDP share of province i among region k

Page 31

21

is the GDP share of province j among region l

As in Kuo and Yang (2008), the distance weight is an exponential function with a distance

decay parameter β:

Adopting the specification in Funke and Niebuhr’s (2005), we define β as:

( )

Where is the average distance between two adjacent regions, and is the transformed

distance decay parameter. Usually ranges from 0 to 1, we use only 0.5 in our study.

A: Horizontal

, are the weighted average stocks of internal

technology development expenditure, and imported technology expenditure, respectively, in the

firm’s 3-digit SIC industry outside region. Assuming the targeted firm is in the Eastern region, as

we define above, is the distance weight between region and the Eastern region, where

belong to set Ω={Northern, Northeastern, Southern, Southwestern}. First, we will construct the

weighted average flow of internal technology development expenditure in the industry outside

region. For each firm located in region r that belongs to the same industry with the targeted firm,

we label its flow of internal technology expenditure as , where ranges from 1 to . Then:

( ) ∑ ∑

Then we use the perpetual inventory method to convert to obtain

The same method was applied to construct .

Page 32

22

, are the weighted average foreign capital stock, and total

capital stock, respectively, in the firm’s 3-digit SIC industry outside region. Their construction is

identical to the construction of except that we use foreign capital stock,

and total capital stock, respectively, instead of internal technology expenditure.

is the weighted average foreign capital stock intensity of the firm’s 3-

digit SIC industry outside region:

B:Vertical

, , , are the

weighted average stock of internal technology development expenditure, imported technology

expenditure, foreign capital, and total capital, respectively, in the firm’s 2-digit SIC upstream

industries outside region. Here we use regional input-output shares as the weight. Assuming the

targeted firm is in the Eastern region, the target firm’s 2-digit SIC upstream industries are

industry i, where i ranges from 1 to I. Suppose the input-output share in region r from industry i

to the targeted firm is , and the stock of internal technology development expenditure of

industry i within region r is :

( ) ∑ ∑

where is the distance weight between region and the Eastern region, Ω where

Page 33

23

Ω ={Northern, Northeastern, Southern, Southwestern}

The same approach was used to construct , ,

.

is the weighted average of foreign capital stock intensity in firm’s 2-digit

SIC upstream industries outside region, employing the following formula:

, , ,

are the weighted average stock of internal technology development expenditure, imported

technology expenditure, foreign capital, and total capital, respectively, in the firm’s 2-digit SIC

downstream industries outside region. The construction of the variables is identical to

, , , ,

respectively, except we use downstream industries instead of upstream industries.

is the weighted average of foreign capital stock intensity in the firm’s 2-

digit SIC downstream industries outside region, and it is the ratio of over

.

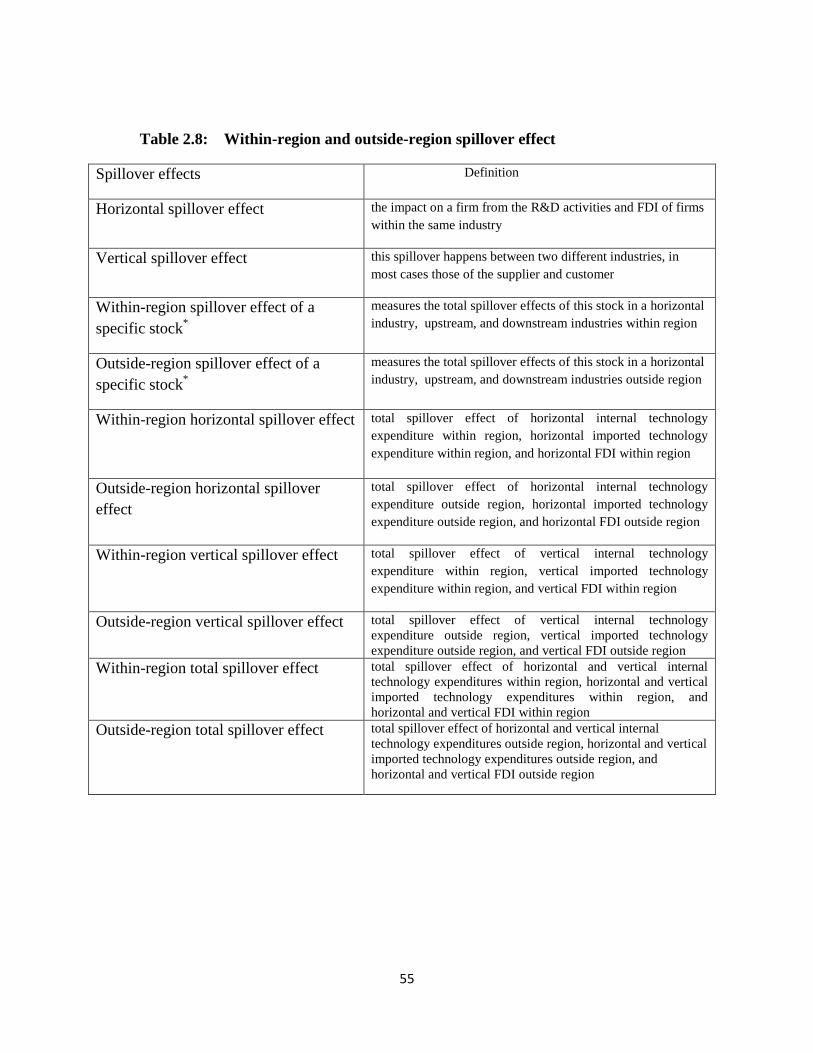

Table 2.7 provides a summary description of the eighteen industry stocks. Table 2.8 provides a

summary definition of within-region and outside-region spillover effects.

Page 34

24

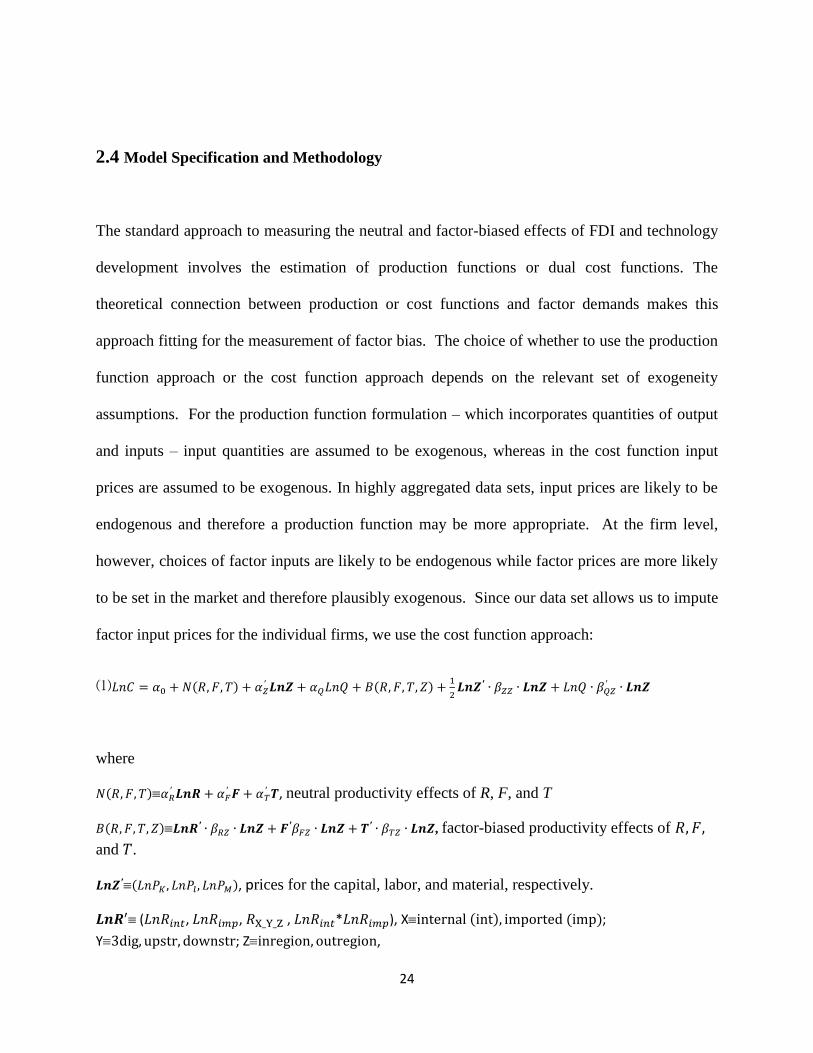

2.4 Model Specification and Methodology

The standard approach to measuring the neutral and factor-biased effects of FDI and technology

development involves the estimation of production functions or dual cost functions. The

theoretical connection between production or cost functions and factor demands makes this

approach fitting for the measurement of factor bias. The choice of whether to use the production

function approach or the cost function approach depends on the relevant set of exogeneity

assumptions. For the production function formulation – which incorporates quantities of output

and inputs – input quantities are assumed to be exogenous, whereas in the cost function input

prices are assumed to be exogenous. In highly aggregated data sets, input prices are likely to be

endogenous and therefore a production function may be more appropriate. At the firm level,

however, choices of factor inputs are likely to be endogenous while factor prices are more likely

to be set in the market and therefore plausibly exogenous. Since our data set allows us to impute

factor input prices for the individual firms, we use the cost function approach:

⑴ ( ) ( )

where

( )

, neutral productivity effects of R, F, and T

( ) , factor-biased productivity effects of

and .

( ), prices for the capital, labor, and material, respectively.

( , , , * ), X ( ) ( );

Y ; Z ,

Page 35

25

( , , ln * , ln * , ), X ;

Y ,

( ), year dummy variables,

C total cost of production,

Q gross value of industrial output in constant prices,

price of fixed assets, which is calculated as (Value added-wage bills-welfare payments)/(net

value of fixed assets),

price of labor , which is calculated as (wage bills+ welfare payments)/(number of employed

persons),

price of material, which is calculated as weighted average of industrial prices using the

input-output shares,

stock of technology development expenditures ( = internal (tdeint) or imported (tdeimp)),

weighted average stock of internal technology development expenditure (or imported

technology expenditure) in firm’s 3-digit SIC industry (or 2-digit SCI upstream or downstream

industry) within (or outside) region. ( = internal (tdeint) or imported (tdeimp), Y=3-dig or upstr

or downstr, Z=inregion or outregion)

foreign capital stock intensity, which is calculated as (foreign capital stock)/(total capital

stock),

weighted average foreign capital stock intensity of firm’s 3-digit SIC industry (or 2-

digit SIC upstream or downstream industry) within (or outside) region. (X=3-dig or upstr or

downstr, Y=inregion or outregion)

Page 36

26

T time dummies for the span of 1995 to 2004, which are used to capture the autonomous

technical progress during this time period.

Using Shephard’s Lemma, we derive the cost share equation associated with each factor input

by taking the derivative of the cost function with respect to the relevant input price; i.e.,

C

XP

P

C ii

i

ln

lni = K, L, M

Specifically, taking the derivative of equation (1) with respect to each input price, we obtain the

following cost share equations:

(2) ⁄

(3 ) ⁄

To ensure that the coefficients exhibit the usual properties of symmetry and homogeneous of

degree one in prices, we impose the following constraints:

βa,b = βb,a

i’∙Z = 1

βZZ∙ i = 0

βRZ∙ i = 0

βRTZ∙ i = 0

βTZ∙ i = 0

βQZ∙ i = 0

where i is a vector of ones.

Page 37

27

The reason that we do not adopt the random effects approach is that the unobserved effect may

be correlated with some of the dependent variables. An unobserved difference in leadership

ability at a firm is one situation in which issued of simultaneity may arise. Better leaders will be

more likely to make better decisions, have better negotiation skills and have more connections

with the upstream input and downstream sale industries. An effective manager can reduce the

production cost in the following ways: First, an effective manager can increase workers’

productivity through creating a friendly working environment, assigning different talent workers

to the suitable place, highlighting good performances, and creating events to increase employee.

Those efforts will motivate workers’ morale and increase efficiency. Second, an effective

manager will make appropriate financial decisions including budget control, balance between

facility maintenance and substitution, and future employment plans. Third, an effective manager

will be aware of market fashions and produce timely product upgrades, which will help reduce

the possibility of overstocked, out-date products. All those advantages of great leadership will

contribute to the low production cost and are included in the firm’s unobserved error term. In the

theory of economic development, Schumpeter (1934) emphasized that a firm’s leaders,

especially their ability to innovate, have significant effects on a firm’s development. Kirzner

(1973) proposed that the ability to handle the unbalanced situation of firm’s leader is important

to the firms.

On the hand, an effective manager will be more likely to make policies or regulations to use

R&D or FDI more effectively. For example, Elkins et al (2003) surveyed past empirical

literature investigating the impact of leader quality on the likelihood of success for R&D

organizations. The results indicate that leaders who can encourage project members with

Page 38

28

intellectual incentives, communicate effectively and motivate workers are more likely to

successfully guide an organization.

Therefore, an effective manager usually helps to reduce production costs and increase the

efficiency of R&D and FDI. However, leadership is unobserved in our dataset and regression

error terms. This will induce a counterfeit association between the low production cost and use of

R&D and FDI. In order to overcome this problem, we adopted the fixed effects estimation

procedure. For each firm that appeared in our panel dataset, we created a dummy variable and

incorporate these variables in our regression equations.

Also, measurement error would occur in our dataset. As Fisher-Vanden et al (2009) pointed out,

even with truthful reporting, the values of R&D expenditure and imported technology collected

in our dataset still are only an approximation. With the classical assumptions that measurement

error is not correlated with original error terms and explanatory variables, which seems to hold in

most situations -- and in our case, we have attenuation bias in our regression coefficients. The

absolute value of the estimated coefficients using our dataset will tend to underestimate the

coefficients. However, this attenuation bias, or downward bias, will reinforce our results. For

example, if the estimated coefficient of R&D turns out to be negative, then the true value of the

parameter should be also negative with a larger magnitude after we incorporate the downward

bias.

Page 39

29

2.5. Results and Interpretation

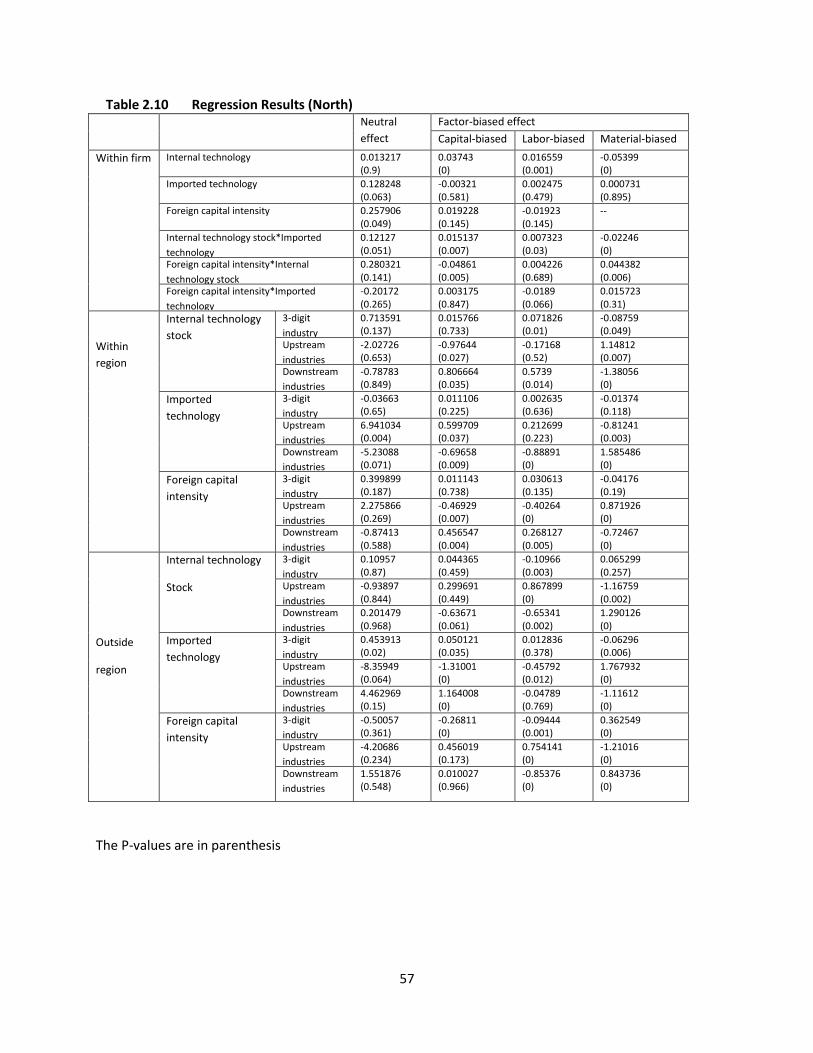

2.5.1 Empirical Results:

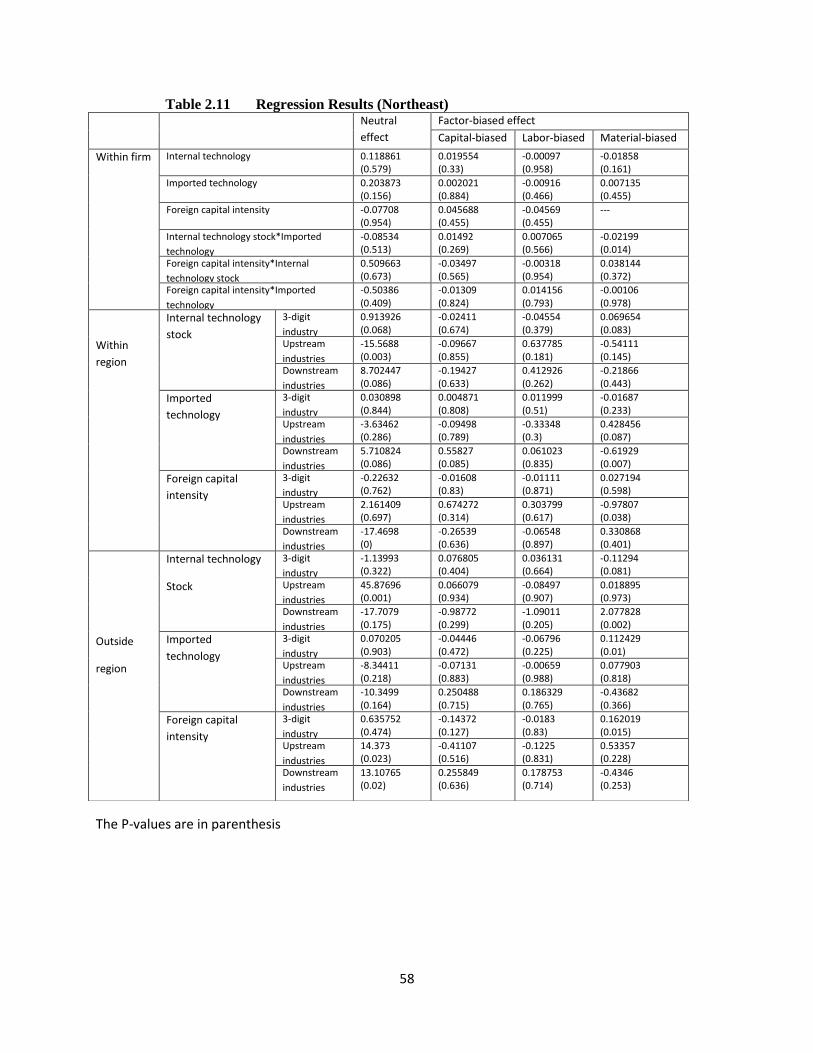

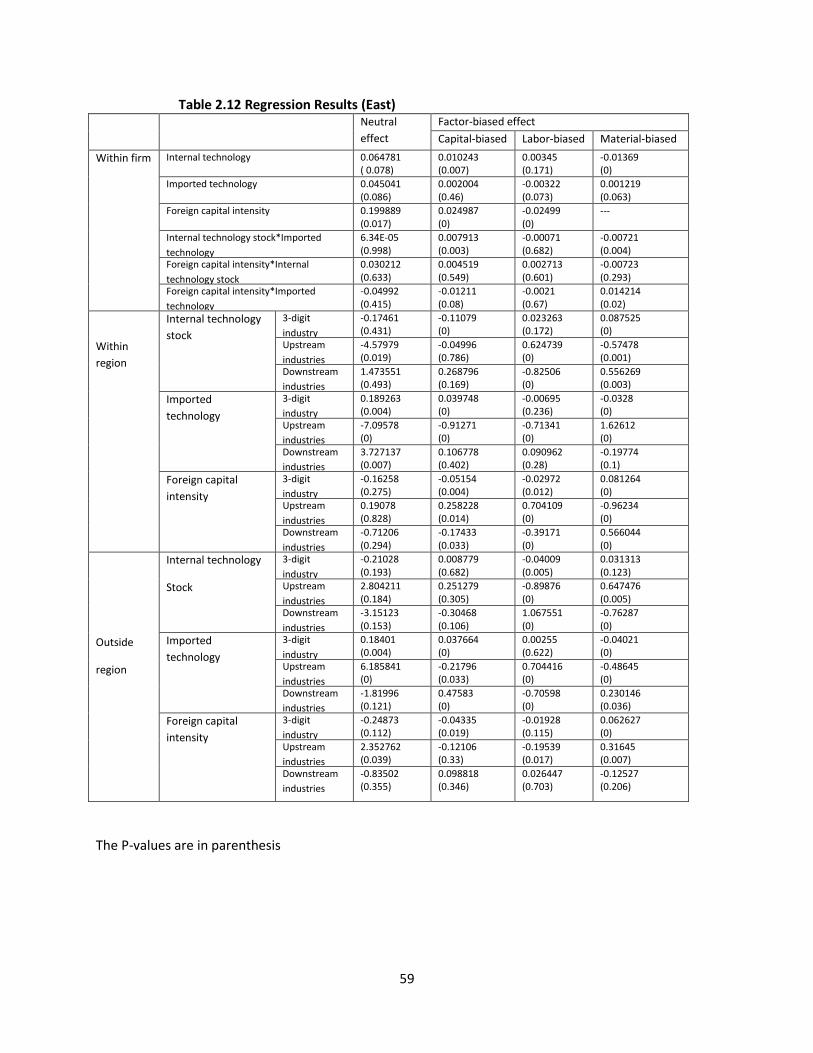

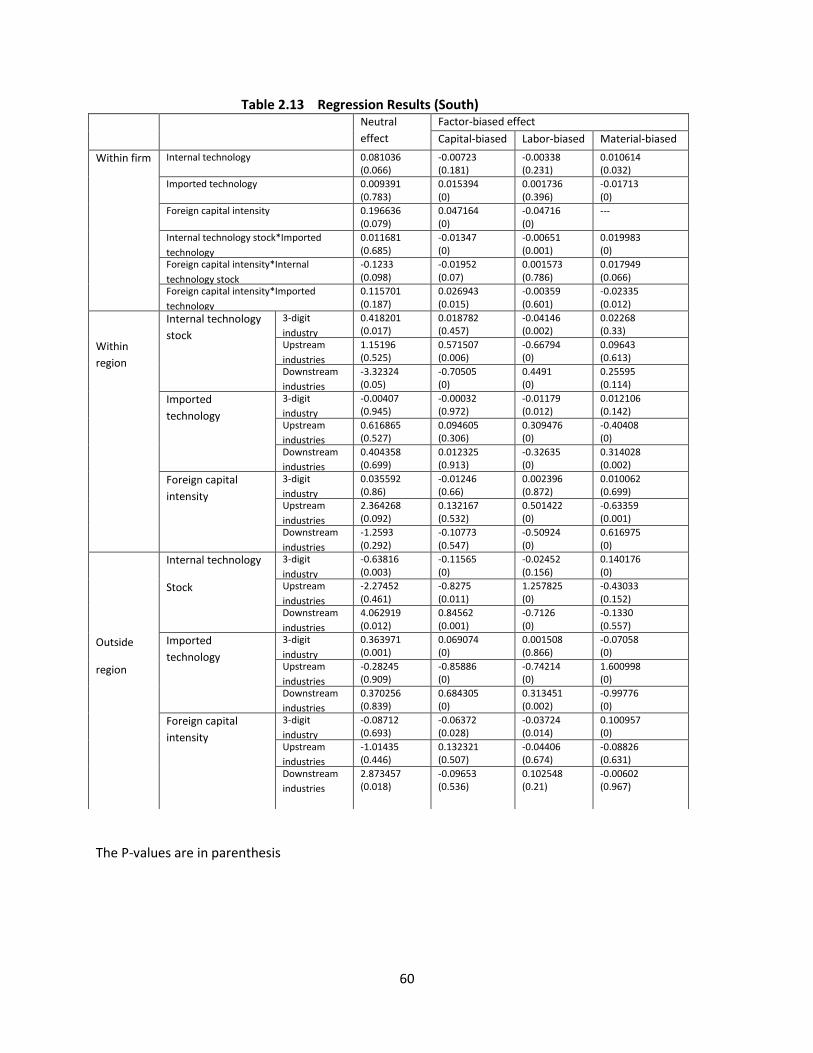

Tables 2.10--2.14 provide the regression results. As showed in Table 2.10, coefficients

associated with stock of internal technology expenditures, both in firm’s 3-digit SIC industry,

firm’s 2-digit SIC upstream industries, and firm’s 2-digit SIC downstream industries, within and

outside region are not robust. Therefore, internal technology expenditures-both within and

outside the Northern region—do not exhibit significant neutral spillover effects on the firms

located in the Northern region. However, the neutral impact of imported technology on total cost

is significant. For instance, the stock of imported technology at firm’s 3-digit industry outside the

Northern region has cost-increasing spillover effects, as well as the stock of imported technology

of upstream industries within the Northern region. On the contrary, cost-reducing effects

originated from the stock of imported technology of upstream industries outside the Northern

region and downstream industries within the northern region. As showed in Table 2.10, both

within-region and outside-region of foreign stocks don’t have significant cost effects. We can

conclude that, for firms located in the Northern region, imported technology has more significant

spillover effects than internal technology development and foreign capital.

Unlike the Northern region, for the Northeastern region, the three technology stocks—internal

technology expenditure, imported technology expenditure, and FDI all have significant spillover

effects on the local firms. As showed in Table 2.11 the stock of internal technology expenditures

in the following three channels has cost-increasing effects: 3-digit industry within the

Northeastern region; upstream industries outside the Northeastern region; downstream industries

within the Northern region. Only the stock of internal technology expenditures from upstream

Page 40

30

industries within the Northeastern region exhibit cost-saving effects. Imported technology from

downstream industries within the Northeastern region has cost-increasing effects. We also find

that foreign capital through two channels—upstream and downstream industries outside the

Northeastern region—exhibits cost-increasing spillover effects while foreign capital in

downstream industries within the Northeastern region has cost-saving spillover effects. We can

conclude that, for the Northeastern region, the primarily neutral cost effects happen through

vertical channel—both upstream and downstream.

Like the Northeastern region, for the Eastern region, all three type technology stocks have

significant spillover effect on the local firms. Moreover, similar to the Northeastern region, the

neutral spillover effect in the Eastern region mainly takes place through vertical channel except

for the imported technology stock. In most situations as showed in Table 2.12, the cost effects of

those two stocks are not significant, and only internal technology expenditures from upstream

industries within the Eastern region have cost-saving effect and Foreign capital of upstream

industries outside the Eastern region have cost-increasing effect. Imported technology from four

channels—3-digit industry within and outside the eastern region, upstream industries outside the

eastern region and downstream industries within the eastern region—display cost-increasing

effect. We can conclude that stocks within the Eastern region have more significant spillover

effects than stocks outside the Eastern region.

For the Southern region, similar to the Northeastern and Eastern region, all three technology

stocks exhibit robust spillover effects. As showed in Table 2.13, cost-increasing effects originate

from four stocks—internal technology expenditures of 3-digit industry within the Southern

region, imported technology from 3-digit industry outside the Southern region, foreign capital

form upstream industries within the Southern region and downstream industries outside the

Page 41

31

Southern region. Only internal technology expenditures from 3-digit industry outside the

Southern region and downstream industries within the Southern region have cost-saving

spillover effects.

For the Southwestern region, similar to the Northeastern and Eastern region, spillover effects

mainly take place through vertical channel-both upstream and downstream. As showed in Table

2.14, internal technology expenditures of downstream industries within the southern region and

imported technology of upstream industries outside the Southern region display cost-increasing

effects, while cost reducing effect only originate with the upstream stocks of internal technology

expenditure within the Southern region. While foreign capital does not have statistically

significant spillover effects.

In conclusion, for internal technology stock, most neutral spillover effects come from within

region’s stock while outside region’s stocks only have spillover effect though few channels in

some regions.(Actually, only two channel---3-digit outside region’s stock in South and upstream

outside region’s stock in Northeast). While for imported technology and foreign capital, both

within region’s stocks and outside region’s stocks have significant neutral spillover effects.

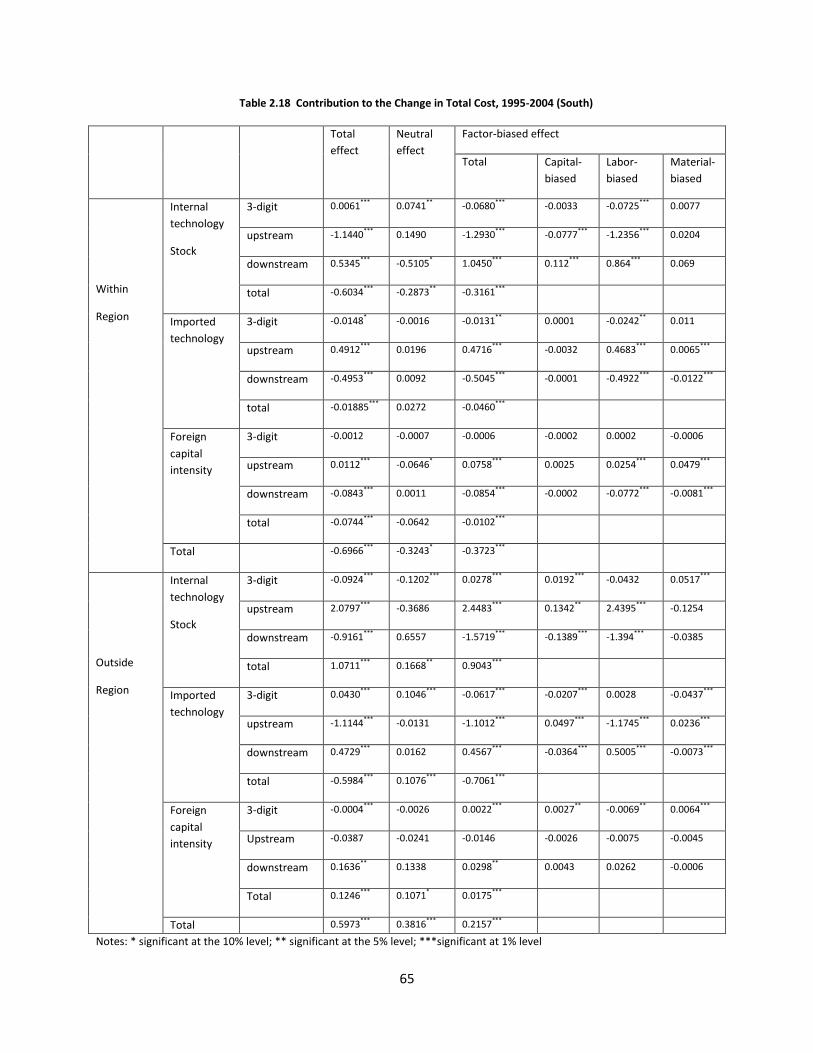

Table 2.15—2.19 use the results from Tables 2.10—2.14 to measure the change in total cost into

the change of amount of factors used, to evaluate the contribution of three types of technology

developments to the change in total cost. Using the coefficients from Table 2.10-2.14 and mean

values of each variable in our equation (1), we subtract the cost function in equation (1)

evaluating in year 2004 by the cost function in equation (1) evaluating in year 1995. Then we use

these differences to account for the percentage change in total cost contributed by each type of

Page 42

32

technology development expenditure. These results are listed from Table 2.15 to Table 2.19,

consist of the neutral effect, factor-bias effect and total effect, of three channels through which

three technology developments have spillover effects in five regions.

Vertical channels are the most effective channels that affect total cost, both for stocks within the

Northern region and outside the Northern region. This pattern holds for the Northeastern region,

the Eastern region, the Southern region and the Southwestern region. In addition to this result,

for one specific stock, Tables 2.15 to Table 2.19 reveal several interesting patterns. For instance,

for imported technology, except outside the Eastern region and outside the Southwestern region,

all other eight spillover effects are cost saving. Except for the Northern region, internal

technology development dominates the outside-region spillover effect in other four regions.

As we expected in Hypothesis 1, empirical results find that spillover effects generated through

vertical channels are more significant--either cost-saving or cost-increasing--than effects

generated through horizontal channel, both for within and outside region. This result extends the

studies of Javorcik (2004) and Fisher-Vanden et al (2009) who find strong cost-saving vertical

but weak horizontal spillover evidences to the case of within versus outside regions. Specifically,

like most previous studies, within-region vertical spillovers have more significant impact on total

cost than horizontal spillovers. However, few of previous studies has found that vertical

channels are also more effective than horizontal channel when examining the impact of outside

region’s stocks on the local firms’ production costs.

Page 43

33

2.5.2 Rapid Growth in the Eastern Region

For the Eastern region, all three types of technology stocks have significant spillover effects on

local firms. Table 2.12 shows that the neutral spillover effect in the Eastern region mainly takes

place through vertical channels. Table 2.17 shows that the within-region total spillover effect

reduces the average firm’s production cost by 179%, which ranks 2rd among all five Chinese

regions. This confirms Hypothesis #2.

What are the factors that contribute to the Eastern region receiving greater within-region

spillover than most other regions? Infrastructure, human capital (for instance, absorptive

capacity), and government macroeconomic policies may be several important factors.

Physical Infrastructure, especially the transportation infrastructure, is an important factor in

determining the extent of spillover. Higher transportation costs will force a firm to choose

suppliers that are close to their location, this is also the case for consumers. Therefore the vertical

spillover more likely takes place between firms that are geographically proximate. This hinders

the spread of advanced technology and managerial skills within the region or across regions.

Aggravated by China’s geography (mountains and hilly, few plains), transportation costs have

bigger impact on local firms’ costs. However, the coastal region has geographical advantages

over those inland. For example seven Coastal provinces, Hebei, Shandong, Jiangsu, Zhejiang,

Fujian, Guangdong, and Hainan, have 82% percent of their population living within 100

kilometers of the sea or navigable rivers (Démurger et al (2002)). The low cost of water

transportation makes it easier to exchange of goods within coastal region and export goods to

foreign countries.

Page 44

34

Aside from these geographical advantages, the Eastern region also enjoys advantages in

transportation infrastructure, including highways and railways. In the year 1998, the average

transportation network density in the East was over 500km/1000km2, while the density in the

Interior was between 350 and 500 km/1000 km2, the density in the West was even less 350

km/1000km2. (Démurger et al (2001))

The advantage in transportation facilities helped the Eastern region receive more significant cost-

savings from the within-regions spillover effect than most other Chinese regions.

Absorptive ability is essential to determine how well firms can recognize, digest, and apply new

knowledge to commercial ends. It becomes more important when the new knowledge is tacit

knowledge, which requires firms to reach a certain level of absorptive ability to understanding

and putting into practice. We use the variable of technology development personnel to roughly

measure firms’ absorptive ability. In the year 2001, our unbalanced dataset indicates that the

ratio of technology development personnel to total employees was 4.7% in the Eastern region,

which was higher than 3.6% in the Northern region, 3.2% in the Northeastern region, 4.4% in the

Southern region, and the 4.3% in the Southwestern region.

This advantage in absorptive ability among Chinese regions contributes to the fact that the

Eastern region receives more significant cost-savings from the within-region spillover effect than

many other Chinese regions.

In the early 1980s, in order to give priority to efficient regions and let coastal regions grow first,

China’s government formulated a series of coastal development strategies including many

preferential policies, which were made to reform the economy in coastal region into a market-

Page 45

35

orientated economy. In particular, many special economic zones were established in the coastal

region. Firms in these open economic zones could import intermediate inputs duty free, were

provided with various preferential tax-treatments, and were allowed to collaborate with foreign

firms in design, production, and distribution.

Table 2.9 lists the timeline of the establishment of economic zones in the Eastern region over the

period 1979-1994. The coastal development strategies, especially the preferential policies,

brought many benefits to the development of the economy in the Eastern region. These include a

huge influx of FDI into the Eastern region.

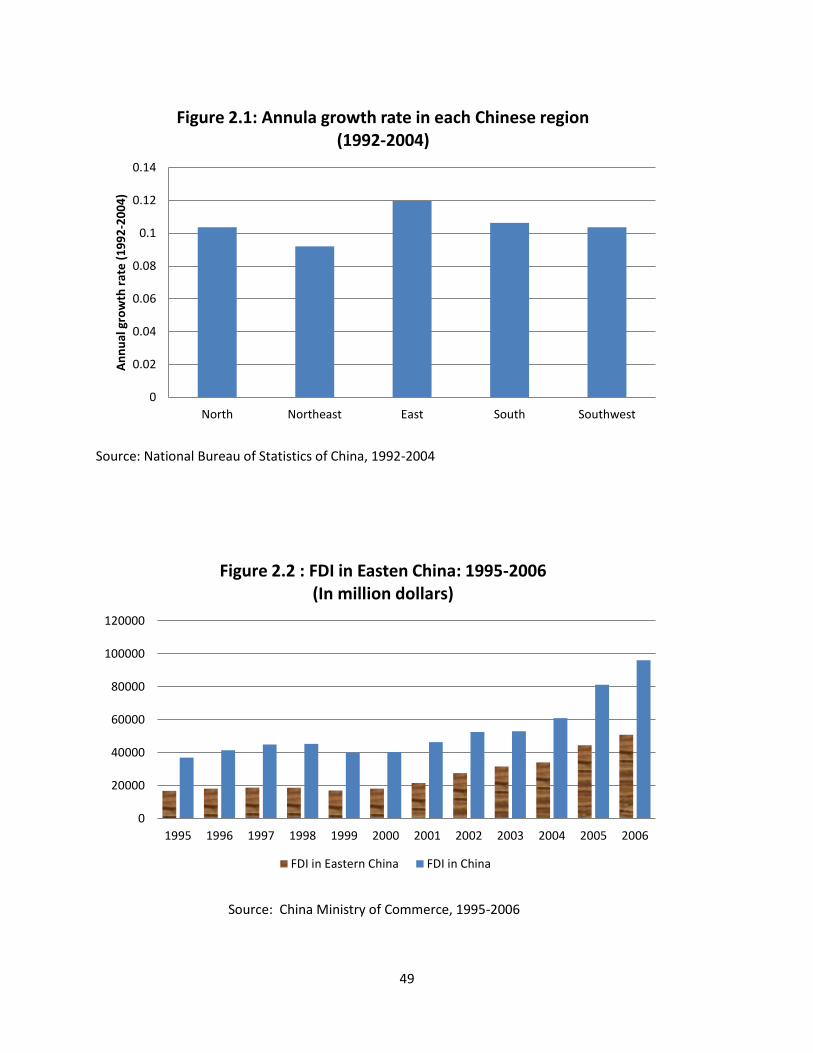

Figure 2.2 Shows that the value of FDI in the Eastern region and FDI in China over the period

1995-2006. We find FDI in the Eastern region has steadily grown from below 20,000 million

dollar in 1995 to around 90,000 million dollar in 2006. During 1995-2000, FDI in the Eastern

region of China accounts for around 40% of total FDI in China, while after 2000, this number is

more than 50%.

Convenient transportation facilities lower the cost of the exchange of inputs and final production,

provide higher freedom of movement for laborers, and speed up the spread of technology and

managerial skills. Firms’ high absorptive abilities help them to better recognize, understand, and

apply this newly acquired technology. Regional preferential policies and FDI spur the

introduction of advanced technology and growth of the regional economy. With the advantages

in these three aspects, the Eastern region has more sources of technology spillovers, more foreign

firms and more firms with advanced technology, a better economic environment for spillovers to

take place, an advanced transportation infrastructure and advantages embedded in the advanced

economy including a more mature labor market, financial market, and innovation mechanism et

Page 46

36

al, and a better ability to absorb and utilize the technology spillover. Therefore large cost-saving

within-region spillovers are expected to occur within the Eastern region. This is consistent with

our empirical results.

2.5.3 The Impact of “Grand Western Development Program” on the Southwestern Region

Hypothesis 3, which expect developed regions will receive more benefits from within-region

spillover effects than less developed regions, is not supported by our empirical results. Not only

did the relatively developed regions, such as the East, benefit from significant within-region

spillover, but also the less developed regions, such as the Southwest, gained largely from within-

region spillovers. In addition, outside-region spillovers have cost-saving effects on firms

operating in the Southwestern region. This may be a result of “Grand Western Development

Program” launched in 2000 to accelerate the economic development of the Central and Western

region.

In order to further analyze the impact of “Grand Western Development Program” on the

technological spillover and economic development in Western regions, we divided the dataset

into two time periods: 1995-1999 and 2000-2004, then ran almost identical regressions on these