This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:22PM Dec 06 2012

CEB Middle Market Impact Report

CEB Middle Market impact report: Thriving in TurbulenceMiddle Market companies are driving growth by using data and people in new ways to spur innovation, disrupt business models, and adapt with greater agility than large companies.By Scott Engler, Senior Executive Advisor | Mark Clauss, Managing Director, CEB Middle Market

Executive Summary

Despite a drop in overall global business confidence, Middle Market1 executive confidence continues to hold firm, even rising slightly in the fourth quarter despite concerns about a “fiscal cliff” in the US, and continued euro zone weakness. That confidence is clearly shown in the top line expectation from CEB’s Middle Market Impact Index with 13% more Middle Market executives expecting much higher revenue than large company executives, but that growth expectation is coupled with an eye toward fiscal prudence, 64% of companies are also reporting higher cost pressure. The data shows a clear divergence of Middle Market company expectations from the large enterprise corporate universe, which has an important implication for Middle Market companies: Middle Market companies can use their flatter and more flexible organizational structures to drive faster decision-making and course correction.

Four Middle Market Imperatives

In what is widely believed to be a constant VUCA (volatile, uncertain, chaotic, adaptive) environment, companies are now focused on using data to understand the market, react and outflank larger companies and move quickly to take advantage of changes in the landscape to drive growth.

CEB has identified four Middle Market company macro trends with important consequences for mid-sized company leaders.

1. Grow and Scale: Driving for and scaling to support new growth in new markets.

2. Listen and Distill: Improving business foresight through big data analytics and trend sensing with a heavy emphasis on IT investment.

3. Connect and Execute: A reinvestment and focus on human capital, with an new emphasis on enterprise connectivity and leadership skills.

4. Disrupt and Innovate: Capitalizing on business disruption to gain a competitive advantage.

“The ability to quickly employ new developments in analytics and organizational design gives middle market companies a marked advantage in a chaotic business environment.”

CEOHigh Tech Company

1 Middle Market is defined as companies with US$25 MM to US$1 B in revenue.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:22PM Dec 06 2012

the State of Middle Market Companies

Middle Market overview: the Growth imperative

In contrast to large companies, the Middle Market is clearly focused on growth and scaling to support it. 91% of Middle Market CFOs in the Finance Leadership Exchange assumptions survey of 150 mid-sized company CFOs rated driving core revenue growth and expansion as a top strategic objective for 2013.2 The near term trends point to a focus on driving new sales while reinvesting in the core with a heavy emphasis on utilizing marketing, people, and IT.

Fifty percent of Middle Market companies are projecting growth of greater than 5% for 2013, with 27% of companies projecting double digit growth for their core business and 33% of companies projecting double digit growth from new initiatives.

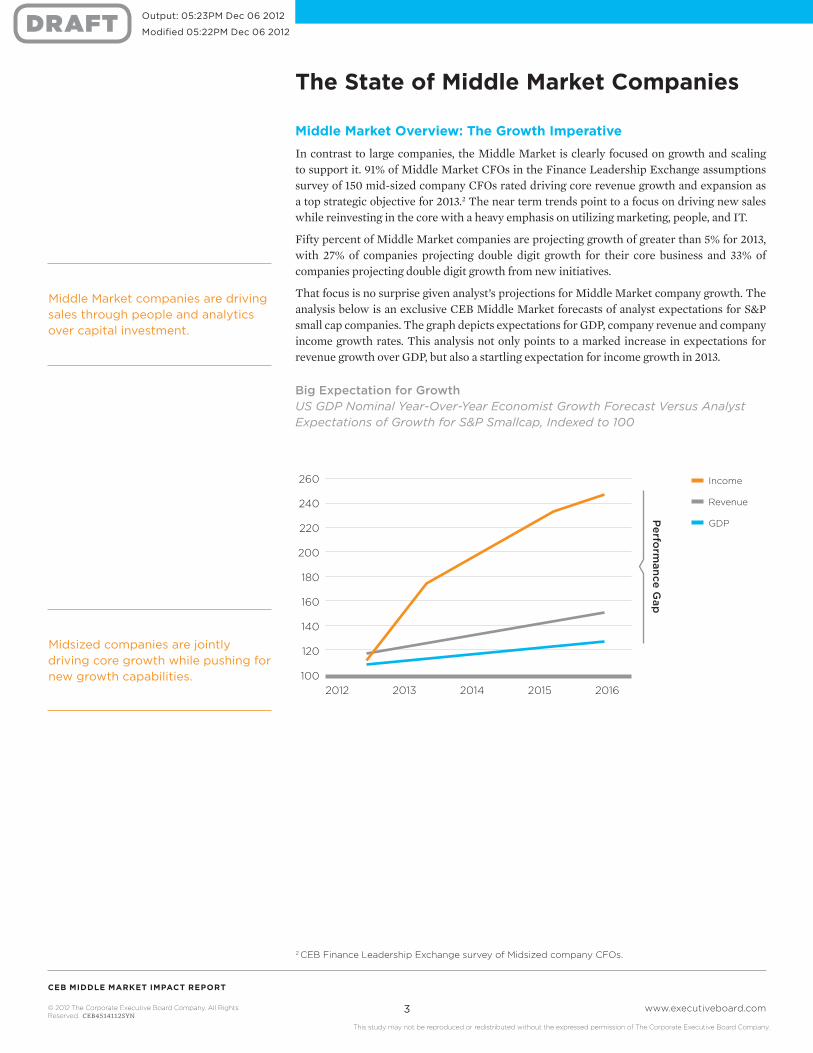

That focus is no surprise given analyst’s projections for Middle Market company growth. The analysis below is an exclusive CEB Middle Market forecasts of analyst expectations for S&P small cap companies. The graph depicts expectations for GDP, company revenue and company income growth rates. This analysis not only points to a marked increase in expectations for revenue growth over GDP, but also a startling expectation for income growth in 2013.

Big Expectation for GrowthUS GDP Nominal Year-Over-Year Economist Growth Forecast Versus Analyst Expectations of Growth for S&P Smallcap, Indexed to 100

Middle Market companies are driving sales through people and analytics over capital investment.

Midsized companies are jointly driving core growth while pushing for new growth capabilities.

Income

Revenue

GDP

Perfo

rmance G

ap

260

240

220

200

180

160

140

120

1002012 2016201520142013

2 CEB Finance Leadership Exchange survey of Midsized company CFOs.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:22PM Dec 06 2012

66%

32%

55%

15%

50%

17%

47%

45%

6% 15–20%

7% < 0%

2% 20+% 13%

20+%

8% 15–20%

12% 10–15%

18% 5–10%

19% 10–15%

38% 5–10%

33% 0–5%

42% 0–5%

2% < 0%

Companies Expecting Growth from Core Business

Companies Expecting Growth from New Initiatives

a Focus on Strategy

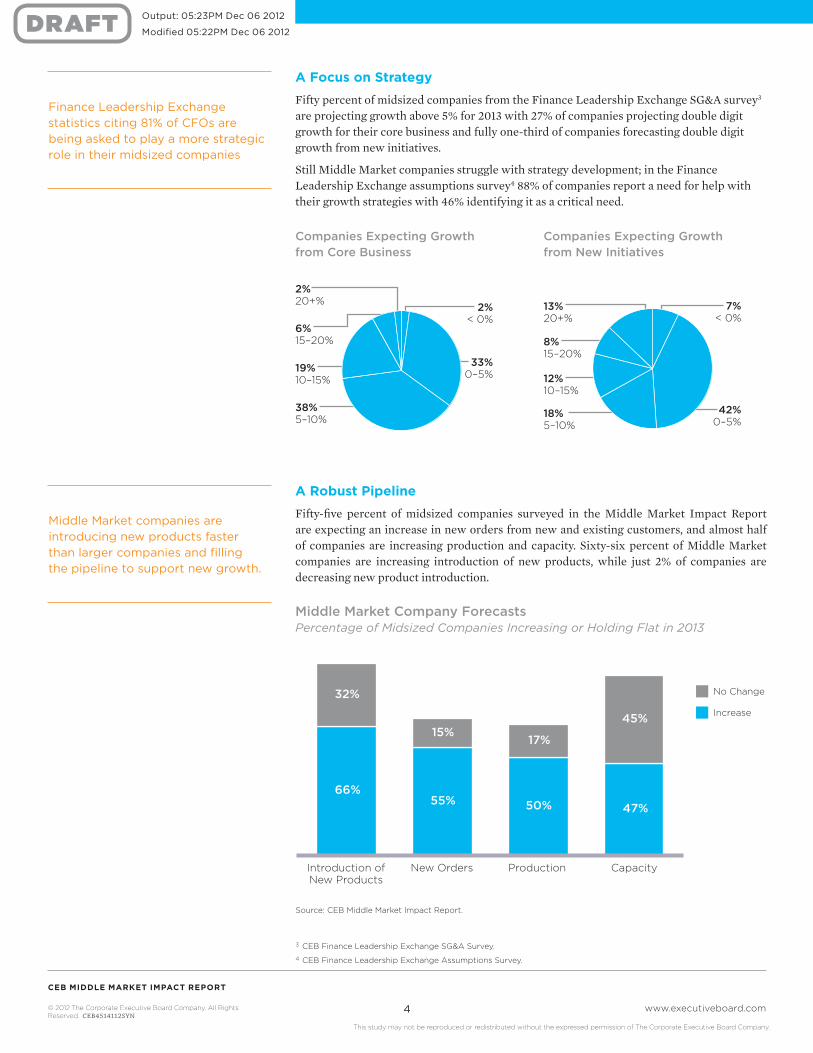

Fifty percent of midsized companies from the Finance Leadership Exchange SG&A survey3 are projecting growth above 5% for 2013 with 27% of companies projecting double digit growth for their core business and fully one-third of companies forecasting double digit growth from new initiatives.

Still Middle Market companies struggle with strategy development; in the Finance Leadership Exchange assumptions survey4 88% of companies report a need for help with their growth strategies with 46% identifying it as a critical need.

Middle Market Company ForecastsPercentage of Midsized Companies Increasing or Holding Flat in 2013

a robust pipeline

Fifty-five percent of midsized companies surveyed in the Middle Market Impact Report are expecting an increase in new orders from new and existing customers, and almost half of companies are increasing production and capacity. Sixty-six percent of Middle Market companies are increasing introduction of new products, while just 2% of companies are decreasing new product introduction.

Middle Market companies are introducing new products faster than larger companies and filling the pipeline to support new growth.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:22PM Dec 06 2012

Strong Midsized Company Labor MarketPercentage of Midsized Companies Increasing Hiring or Holding Steady

Hiring outlook remains Strong

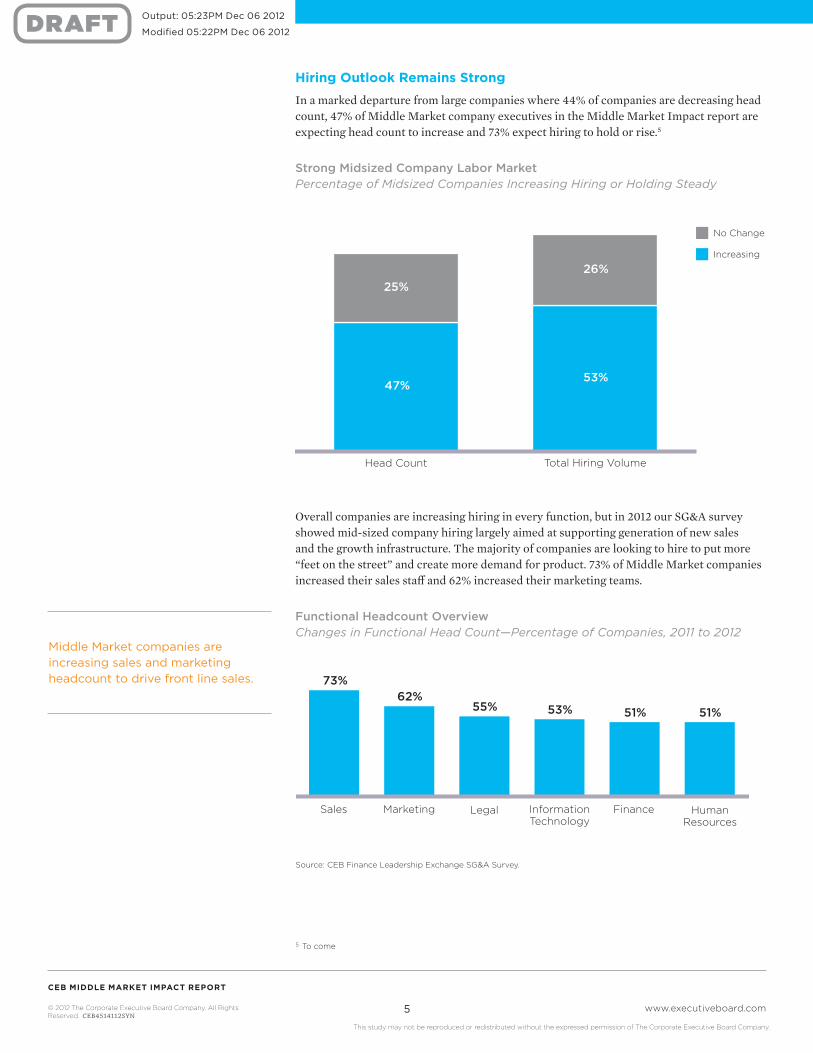

In a marked departure from large companies where 44% of companies are decreasing head count, 47% of Middle Market company executives in the Middle Market Impact report are expecting head count to increase and 73% expect hiring to hold or rise.5

Head Count Total Hiring Volume

47%

25%

53%

26%

No Change

Increasing

Overall companies are increasing hiring in every function, but in 2012 our SG&A survey showed mid-sized company hiring largely aimed at supporting generation of new sales and the growth infrastructure. The majority of companies are looking to hire to put more “feet on the street” and create more demand for product. 73% of Middle Market companies increased their sales staff and 62% increased their marketing teams.

Functional Headcount OverviewChanges in Functional Head Count—Percentage of Companies, 2011 to 2012

Middle Market companies are increasing sales and marketing headcount to drive front line sales.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

38%

27%

35%

36%

46%

18%

25%

42%

33%

24%

35%

41%

23%

39%

38%

optimism with Caution

The drive for growth is tempered by concern about the overall business environment. Middle Market companies see weakening consumer confidence, government spending and growth in the US and EMEA. Emerging markets continue to be a bright spot with 37% of executives expecting higher growth and 77% expecting emerging markets to hold steady or improve.

Economic Expectations for 2013

investment CapEX is Weak

The optimism around growth comes with a caveat, a hold on big spending. The investment outlook remains depressed. Only 39% of executives expect to increase CAPEX spending down from 43% in Q3. There was a pull back for R&D expenditures as well: 36% of executives expect greater R&D in the next 12 months, compared to 39% in Q3 2012.

Investment Expectations for 2013

Middle Market companies are planning for growth despite a tepid economic outlook.

Despite anticipating growth, Middle Market companies are holding off on major investments.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

the drive for adaptive Growth

This low CAPEX investment combined with increased revenue and SG&A projections point to a flexible or “accordion” approach to growth, where companies have the ability to expand and contract with changes in the environment.

Sales spend by far continues to make up the largest budget as a proportion of sales revenue with a budget three times that of any other function, set to grow by 10% next year. Marketing spend makes up just 2% of revenue, but is growing at 12%. IT and HR are the next fastest growing budgets as companies look to leverage the information boom and develop their people.

Conclusion

While growth remains a key focal point for Middle Market companies, the pre-recession “growth at any cost” mentality has been replaced by a targeted growth approach to increase expenses to drive new business, while improving capabilities to take advantage of the ongoing turbulence.

“The days of putting out supply and waiting for demand are gone; growth investments need a laser focus now.”

CFOBusiness Services Company

Functional Spends in 2012Median Functional Spend as Percentage of Revenue by Change in Spend YOY, 2012

Per

cent

age

Cha

nge

YO

Y

Marketing Sales Human Resources

Information Technology

Finance Legal

Functional Area

2%

1%

1%

10%

Percent of Sales

12%

10%

8%

6%

4%

2%

0%

3%

3%

∆ = 12.2%∆ = 10.0%

∆ = 7.9%∆ = 7.3%

∆ = 4.1%

∆ = 1.0%

Middle Market companies are expanding SG&A spending in areas that drive growth, but are careful to keep a flexible “cost base” to remain agile.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Middle Market divergence report

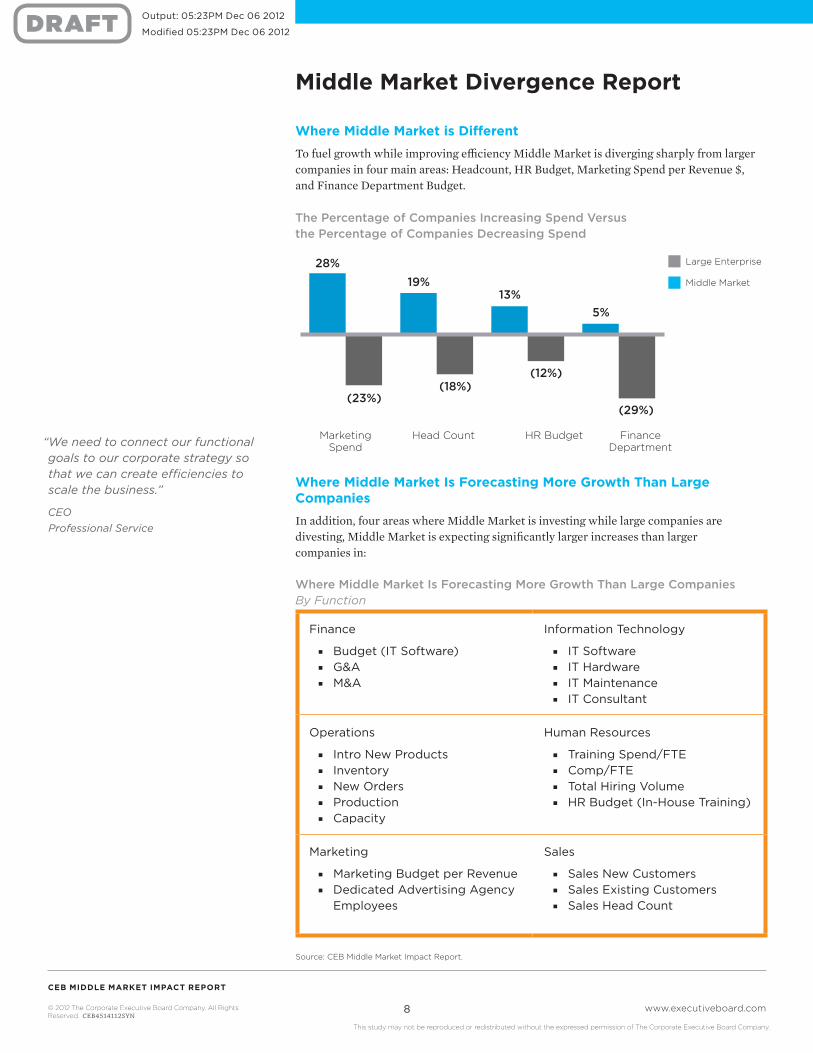

Where Middle Market is different

To fuel growth while improving efficiency Middle Market is diverging sharply from larger companies in four main areas: Headcount, HR Budget, Marketing Spend per Revenue $, and Finance Department Budget.

“We need to connect our functional goals to our corporate strategy so that we can create efficiencies to scale the business.”

CEOProfessional Service

Finance

■ Budget (IT Software) ■ G&A ■ M&A

Information Technology

■ IT Software ■ IT Hardware ■ IT Maintenance ■ IT Consultant

Operations

■ Intro New Products ■ Inventory ■ New Orders ■ Production ■ Capacity

Human Resources

■ Training Spend/FTE ■ Comp/FTE ■ Total Hiring Volume ■ HR Budget (In-House Training)

Marketing

■ Marketing Budget per Revenue ■ Dedicated Advertising Agency

Employees

Sales

■ Sales New Customers ■ Sales Existing Customers ■ Sales Head Count

Where Middle Market is Forecasting More Growth than large Companies

In addition, four areas where Middle Market is investing while large companies are divesting, Middle Market is expecting significantly larger increases than larger companies in:

Where Middle Market Is Forecasting More Growth Than Large Companies By Function

The Percentage of Companies Increasing Spend Versus the Percentage of Companies Decreasing Spend

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Middle Market imperative #1

DRIVING FOR AND SCALING TO SuPPORT NEw GROwTH IN NEw MARkETS.

Middle Market companies are far more focused on growth than their larger siblings and that focus has led to a renewed interest in strategy as Middle Market companies look to move beyond their core through new product offerings into adjacent markets, expand into emerging markets and grow through M&A.

Strategy

Ninety-one percent of Middle Market companies in the Finance Leadership Exchange assumptions survey rated driving core revenue and expansion as a top strategic priority. This implied dual top-line bottom-line pressure has brought Middle Market CFOs into the strategic spotlight, with 81% of CFOs now being asked to play a more strategic role. Still Middle Market companies struggle with strategy development, 88% of companies report needing help with their growth strategies, and 46% identifying it as a critical need.

Growth with Scale

Middle Market companies are scaling and centralizing to drive efficiency while taking advantage of a more fragmented customer market to seize growth opportunities. Almost a third of Middle Market companies are focused on growth through product innovation where their smaller decision management structures give them a distinct agility and allocation advantage over the large companies. For example, Middle market is increasing R&D while large enterprise is cutting back. Another area Middle Market is exploiting an advantage is in marketing and sales, two areas where large enterprise is decreasing investment. The result is that Middle Market new product introduction, new orders and production are all increasing faster than large companies.

Beating large Enterprise at their own Game

Middle market is also looking to beat large enterprise on their own turf, as changes in technology, cultural advances, travel and information availability have lowered entry barriers abroad. Middle market is following large corporate companies into emerging markets where large companies with big geographic footprints have traditionally enjoyed a strategic advantage.

M&a our Way

M&A remains a consistent focus for midsized companies with 26% of Middle Market companies highlighting M&A as a top priority; here their challenge is distinct from large companies. Middle market companies generally only do a few deals per year at most and they struggle to find targets that are strategically aligned, available and priced correctly.

Efficiency and Scale

While companies are driving growth they’re also driving efficiencies. 60% of companies identifying cost containment and centralization as a top strategic priority and more than 50% of companies focused on growth are doing so with a secondary focus on cost and centralization. Operationally Middle Market companies can realize greater efficiencies through scale and centralization as they migrate up the revenue ladder. They’re centralizing and scaling core functions to drive efficiencies.

GROW AND SCALE

Middle Market companies are intently focused on growth, but with a keen eye on building efficiencies and an infrastructure to support long-term growth.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Middle Market imperative #2

IMPROVING BuSINESS FORESIGHT THROuGH DATA ANALYTICS AND TREND SENSING wITH A HEAVY EMPHASIS ON IT INVESTMENT.

Big data creates a dual imperative, to gather and glean insight to act ahead of the competition without becoming so inundated with data decision-making becomes paralyzed. In addition to the obvious IT implications, the acute need for actionable data has implications across functions demanding new skills in metric development and application, understanding risk, and converging functional tasks.

Data is being used in three main ways by midsized companies

1. To identify customer trends and direct marketing and sales efforts.

2. To uncover industry trends and uncover strategic shifts.

3. To drive effienciency across the business.

The obvious investment spot is IT and the CEB Finance Leadership Exchange SG&A survey finds that IT investment rose 7.3% in Middle Market companies and with that company IT spend tilting slight toward software and away from hardware.

The move toward more and better data has encouraged Middle Market functional heads to take the lead in making many technology investment decisions, with IT shifting into the consultative role of helping other functional heads identify and implement software choices.

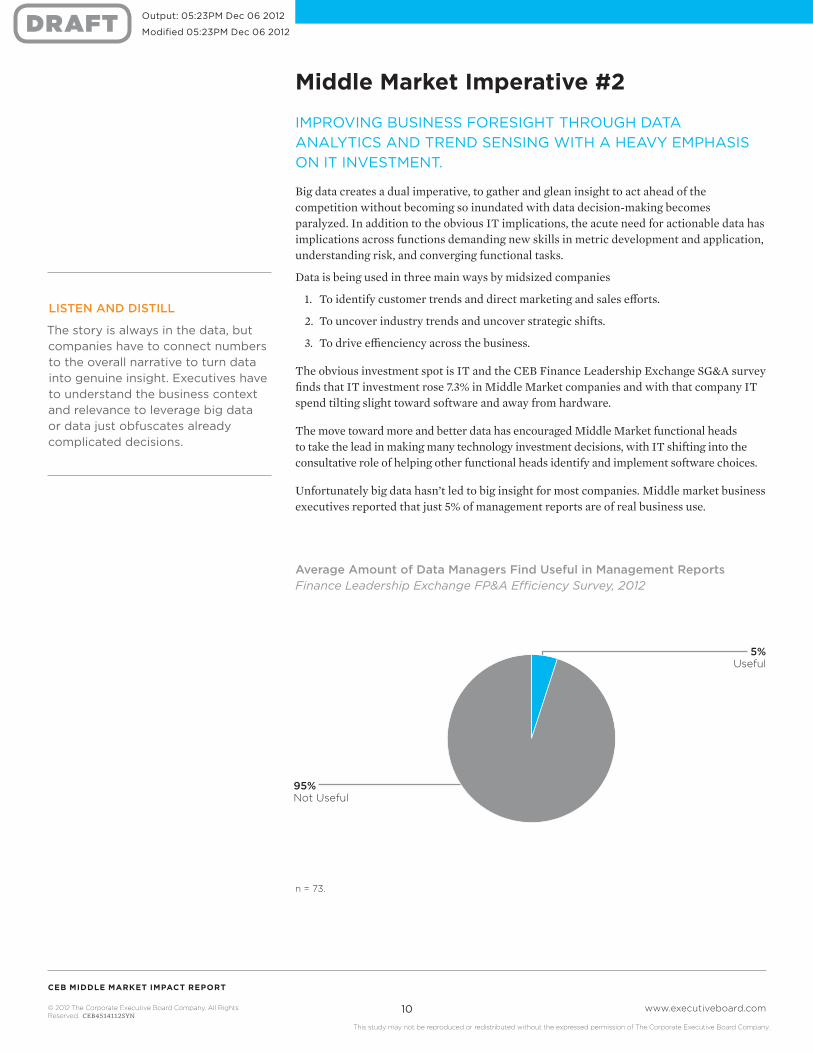

Unfortunately big data hasn’t led to big insight for most companies. Middle market business executives reported that just 5% of management reports are of real business use.

LISTEN AND DISTILL

The story is always in the data, but companies have to connect numbers to the overall narrative to turn data into genuine insight. Executives have to understand the business context and relevance to leverage big data or data just obfuscates already complicated decisions.

Average Amount of Data Managers Find Useful in Management Reports Finance Leadership Exchange FP&A Efficiency Survey, 2012

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

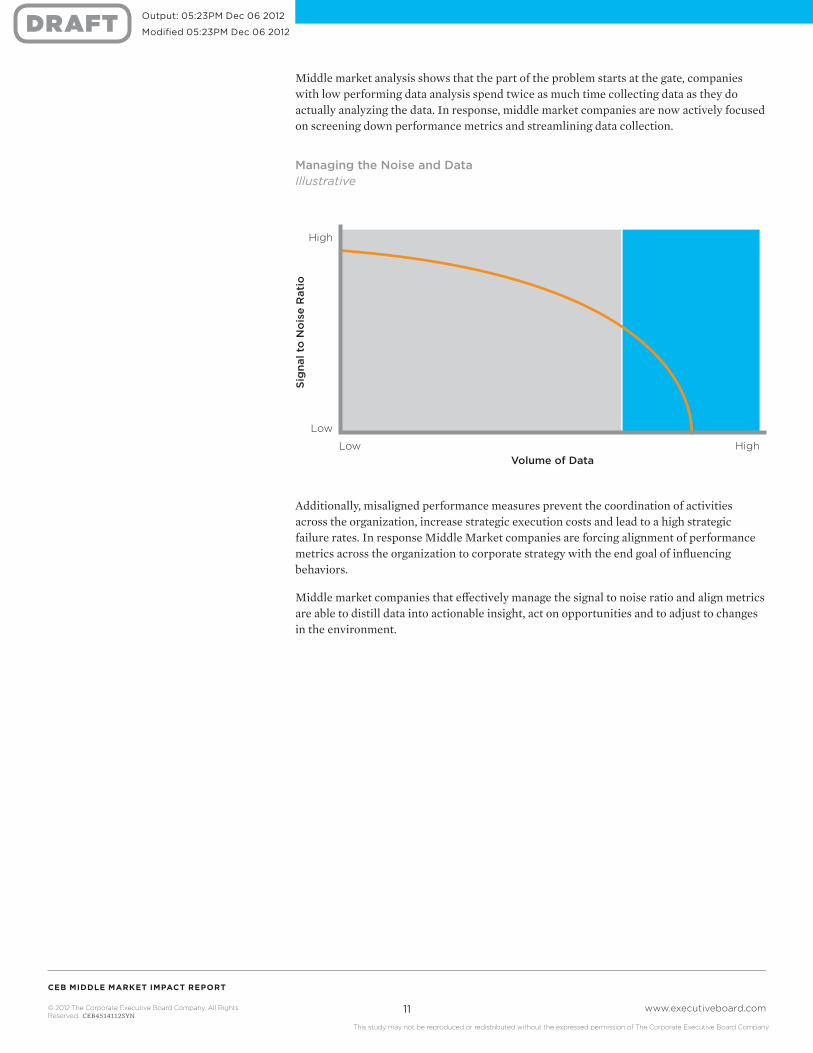

Middle market analysis shows that the part of the problem starts at the gate, companies with low performing data analysis spend twice as much time collecting data as they do actually analyzing the data. In response, middle market companies are now actively focused on screening down performance metrics and streamlining data collection.

Additionally, misaligned performance measures prevent the coordination of activities across the organization, increase strategic execution costs and lead to a high strategic failure rates. In response Middle Market companies are forcing alignment of performance metrics across the organization to corporate strategy with the end goal of influencing behaviors.

Middle market companies that effectively manage the signal to noise ratio and align metrics are able to distill data into actionable insight, act on opportunities and to adjust to changes in the environment.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

CONNECT AND EXECUTE

If you have a “sum of the parts” approach to the organization you’re going to be left behind. Smart companies are activating the ecosytems around strategic initiatives to harness and create synergies.

Middle Market imperative #3

A REINVESTMENT AND FOCuS ON HuMAN CAPITAL TRAINING AND ENTERPRISE CONNECTIVITY, COLLABORATION AND FuTuRE ENTERPRISE SkILLS.

Driven by their growth goals, Middle Market companies are investing in human resources, both in the function and in talent related activities, (while large enterprise is mostly downsizing HR.) Much of that Middle market spend is focused on training as companies executing on new strategies try to up-skill their smaller workforces. Middle Market is also hiring to meet strategic growth targets with 27% more Middle Market companies reporting a rise in hiring than their larger brethren.

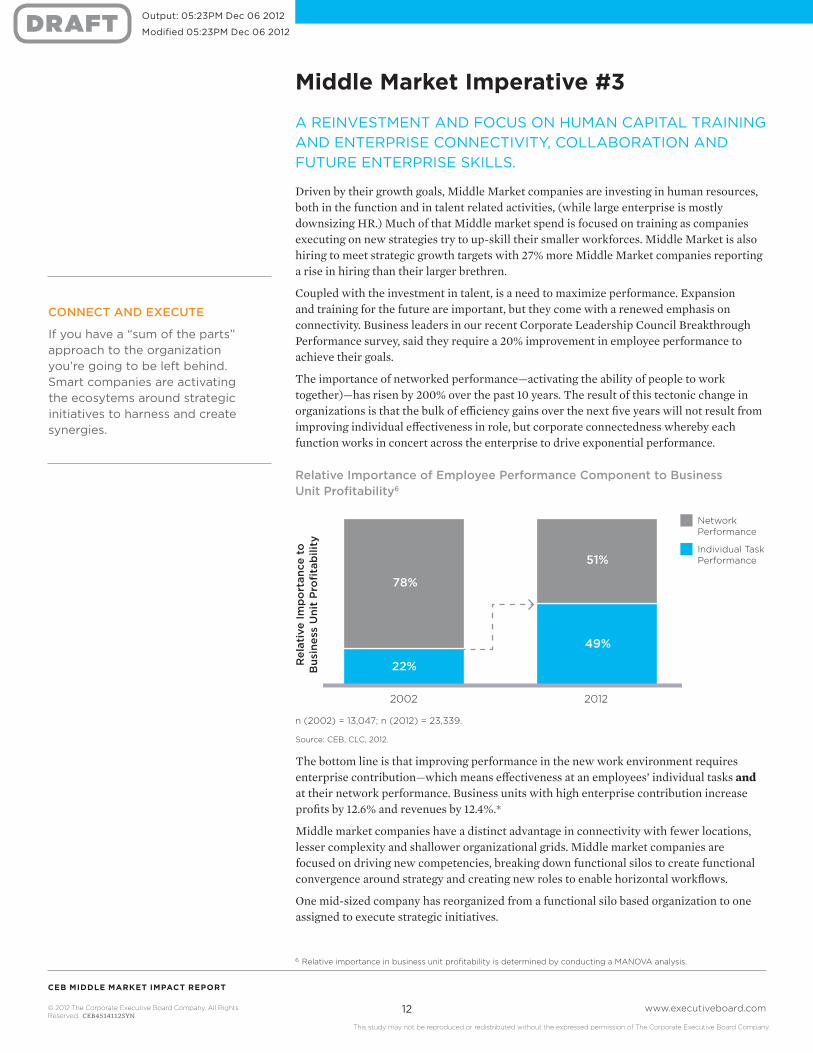

Coupled with the investment in talent, is a need to maximize performance. Expansion and training for the future are important, but they come with a renewed emphasis on connectivity. Business leaders in our recent Corporate Leadership Council Breakthrough Performance survey, said they require a 20% improvement in employee performance to achieve their goals.

The importance of networked performance—activating the ability of people to work together)—has risen by 200% over the past 10 years. The result of this tectonic change in organizations is that the bulk of efficiency gains over the next five years will not result from improving individual effectiveness in role, but corporate connectedness whereby each function works in concert across the enterprise to drive exponential performance.

Relative Importance of Employee Performance Component to Business Unit Profitability6

The bottom line is that improving performance in the new work environment requires enterprise contribution—which means effectiveness at an employees’ individual tasks and at their network performance. Business units with high enterprise contribution increase profits by 12.6% and revenues by 12.4%.*

Middle market companies have a distinct advantage in connectivity with fewer locations, lesser complexity and shallower organizational grids. Middle market companies are focused on driving new competencies, breaking down functional silos to create functional convergence around strategy and creating new roles to enable horizontal workflows.

One mid-sized company has reorganized from a functional silo based organization to one assigned to execute strategic initiatives.

22%

78%

49%

51%

Network Performance

Individual Task Performance

2002 2012

Rel

ativ

e Im

po

rtan

ce t

o

Bus

ines

s U

nit

Pro

fita

bili

ty

6 Relative importance in business unit profitability is determined by conducting a MANOVA analysis.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Middle Market imperative #4

ADAPTING BuSINESS DISRuPTION TO GAIN A COMPETITIVE ADVANTAGE.

CEOs report a dramatic increase in market volatility, fast-changing consumer behaviors, and unpredictability. In response, Middle Market companies are moving aggressively to identify and adjust to strategic risks in the market place and use performance management techniques to uncover business insight.

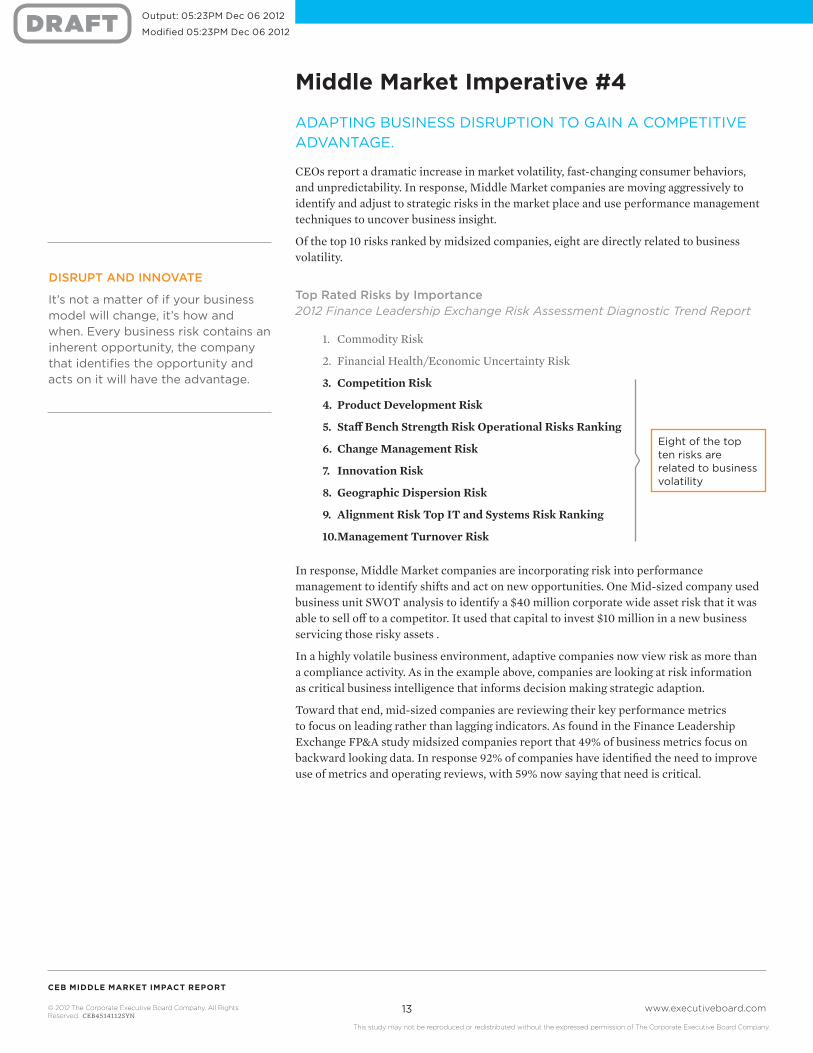

Of the top 10 risks ranked by midsized companies, eight are directly related to business volatility.

Top Rated Risks by Importance2012 Finance Leadership Exchange Risk Assessment Diagnostic Trend Report

In response, Middle Market companies are incorporating risk into performance management to identify shifts and act on new opportunities. One Mid-sized company used business unit SWOT analysis to identify a $40 million corporate wide asset risk that it was able to sell off to a competitor. It used that capital to invest $10 million in a new business servicing those risky assets .

In a highly volatile business environment, adaptive companies now view risk as more than a compliance activity. As in the example above, companies are looking at risk information as critical business intelligence that informs decision making strategic adaption.

Toward that end, mid-sized companies are reviewing their key performance metrics to focus on leading rather than lagging indicators. As found in the Finance Leadership Exchange FP&A study midsized companies report that 49% of business metrics focus on backward looking data. In response 92% of companies have identified the need to improve use of metrics and operating reviews, with 59% now saying that need is critical.

DISRUPT AND INNOVATE

It’s not a matter of if your business model will change, it’s how and when. Every business risk contains an inherent opportunity, the company that identifies the opportunity and acts on it will have the advantage.

Eight of the top ten risks are related to business volatility

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

implication of imperatives by FunctionIMPERATIVE #2: IMPROVING BuSINESS FORESIGHT THROuGH DATA ANALYTICS AND TREND SENSING wITH A HEAVY EMPHASIS ON IT INVESTMENT.

MARkETING

■ How Do We Build the Marketer of the Future

■ Accuracy and Speed with Analytics

INFORMATION TECHNOLOGY

■ Focusing on Information Over Process

■ Improving Business Partner Responsibility/Coaching

■ Enabling Knowledge Work

SALES

■ Partnering with Marketing

■ Developing the Right Sales Culture to Drive Sales Transformation Towards Insight Selling

■ Driving Forecasting Precision

■ Creating Smarter Coverage Models

■ Identifying What Should Be Keeping Customers up at Night

FINANCE

■ Revamping Dashboard, Metrics, and Operating Reviews

■ Improving Business Partnering and Analytics

■ Implementing Finance IT Systems and Data Governance

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

implication of imperatives by FunctionIMPERATIVE #3: A REINVESTMENT AND FOCuS ON HuMAN CAPITAL TRAINING AND ENTERPRISE CONNECTIVITY, COLLABORATION AND FuTuRE ENTERPRISE SkILLS.

INFORMATION TECHNOLOGY

■ Enabling Mobility Work at Home

■ Developing Influence/Coaching SKills

■ Enabling Network Microsegments

SALES

■ Meeting Demands for Mobile Sales Tools

■ Partnering with Marketing to Move up the Decision Chain

MARkETING

■ Partnering with Sales to Move up the Decisions Chain

FINANCE

■ Developing Business Partnering and Influence Skills

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Functional imperatives

SALESTo fuel growth Middle Market is investing in more sales “feet on the street.” Seventy-three percentage of Middle Market companies expect to sell more to existing customers (versus 52% for large companies,) 75% of Middle Market companies expect to sell more to new customers (versus 68% for large companies). Seventy-three percentage of midsized companies are increasing their sales forces with the majority of that increase bolstering field sales (62% of the sales budget) and to a lesser extent sales operations, inside sales and field sales management. Midsized companies are reporting less reliance on discounts and lower Average Sales cycle compared to large companies.

Executive Focus

■ Enabling an Insight-Led Sale (Marketing, HR)

■ How to Get in Early and Shape Demand (rather than reacting to demand) (Marketing, IT, Finance)

■ Partnering with Marketing

■ Developing the Right Sales Culture to Drive Sales Transformation Towards Insight Selling

■ Driving Forecasting Precision

■ Creating Smarter Coverage Models

■ Identifying What Should Be Keeping Customers up at Night

■ Meeting Demands for Mobile Sales Tools

■ Partnering with Marketing to Move up the Decision Chain

■ Capturing Unstructured Customer Intelligence Through Social Media Tools

OPERATIONSMidsized companies are introducing new products, ramping up capacity and production at faster rates than larger companies putting new demands upon Operations to find efficiencies and align strategically to support growth. Sixty- six percentage of companies are introducing more new products and 55% are expecting more new orders. Midsized companies, more than larger companies, have a greater opportunity to fine-tune processes for efficiency, rethink design, and work more closely with sales and managing inventory to drive expansion.

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Functional imperatives (Continued)

HUMAN RESOURCESWith hiring on the rise and HR budgets increasing, the increased importance of collaboration requires HR to think beyond role performance and about how enable efficient workflows across functions. On average Middle Market executives estimate that they’ll have to increase performance by 25% to meet those goals driving development and a demand new talent. Enterprise-wide needs to align the work force around strategy and manage a growing population are fueling a need to upgrade HRIS systems.

Executive Focus

■ Improving Manager Capabilities

■ Developing New Skill Sets to Support Strategy

■ Finding New Talent

■ Implementing/Upgrading HRIS Systems

■ Attracting Talent

■ Designing Roles for Collaboration

■ Up-Skilling Workforce Around New Competencies

■ Implementing Collaboration Software

■ Implementing

■ Collaboration Software

■ Driving Innovation

INFORMATION TECHNOLOGYAcross the board, midsized company IT spending is up, but the role of IT is rapidly changing. IT executives are prioritizing business outcomes over assets, enabling over providing and focused on end user outputs. Ultimately IT is moving into a more consultative role to the business to influence decisions and help the organization understand how the pieces fit together.

Executive Focus

■ Instituting End to End IT Services

■ Creating Business Partnership

■ Devising Strategic Roadmaps

■ Focusing on Information Over Process

■ Improving Business Partner Responsibility/Coaching

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Functional imperatives (Continued)

MARkETINGCore marketing and advertising spend drove marketing budgets up 12.2% from 2011 to 2012 with marketing spend focused on developing “upstream” customer channels for sales representatives, rebranding initiatives, and global marketing demands. On average, customers progress nearly 60% of the way through the purchase decision-making process before engaging a sales rep, which means marketing is now playing a key sales role by informing the customer earlier in the process. Marketing analytic skills are at a premium as well.

Executive Focus

■ Reshaping Buying Criteria with Content

■ Harness Data for Focus and Decision Making

■ Fusing Multi/Emerging Communication Channel

■ How Do We Build the Marketer of the Future

■ Accuracy and Speed with Analytics

■ Partnering with Sales to Move up the Decisions Chain

■ Understanding Customer Demand

■ Differentiating to Get Away from Commoditization

FINANCEFinance has evolved to becoming the key strategic compass of the organization with CFO’s now playing a co-CEO role in strategic development, risk sensing and execution. The increasing demand for more data puts a premium on executive skills at metric selection and analytics, influencing the business and increasing speed of principle decision making. To meet those higher level demands Middle Market finance departments are focused on efficiency through IT and process improvement.

Executive Focus

■ Driving Non-Incremental Strategy

■ Investing in FP&A

■ Revamping Dashboard, Metrics, and Operating Reviews

■ Improving Business Partnering and Analytics

■ Implementing Finance IT Systems and Data Governance

■ Coaching Performance Management

■ Developing Business Partnering and Influence Skills

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

Functional imperatives (Continued)

LEGALGrowth is putting pressure on Middle Market GCs to become more involved in business decisions earlier in the process to speed execution, support growth by understanding risk and IT by managing information risk and ensuring a compliance culture. Middle market companies are bringing more legal activities in-house and reducing outside legal spend in order to bring more expertise close to the business.

Executive Focus

■ Improving the Consistency and Speed of Commercial Contracting

■ Building or Improving Corporate Compliance and Ethics

This study may not be reproduced or redistributed without the expressed permission of The Corporate Executive Board Company.

Output: 05:23PM Dec 06 2012

Modified 05:23PM Dec 06 2012

about CEBCEB is the leading member-based advisory company. By combining the best practices of thousands of member companies with our advanced research methodologies and human capital analytics, we equip senior leaders and their teams with insight and actionable solutions to transform operations. This distinctive approach, pioneered by CEB, enables executives to harness peer perspectives and tap into breakthrough innovation without costly consulting or reinvention. The CEB member network includes more than 16,000 executives and the majority of top companies globally.