29

Tight Oil Resource Company Spring 2013

Tight Oil Resource Company

Spring 2013

TORC Advisory

2

Forward‐Looking Statements:

Certain information in this presentation including management's assessment of future plans and operations, the effect of the Arrangement on Vero and TORC, timing of matters relatedto the approval of the Arrangement and implementation thereof, production levels, capital expenditures, operating costs, reserves estimates, commodity mix, working capital and debtlevels, tax pools, business strategy, future development and growth opportunities, prospects and anticipated benefits from the Arrangement are forward‐looking statements underapplicable securities laws. Since forward‐looking statements address future events and conditions, by their very nature they involve inherent risks and uncertainties including, withoutlimitation, the risks associated with the oil and gas industry in general such as operational risks in development, exploration, production, marketing and transportation; loss of markets;delays or changes in plans with respect to exploration or development projects or capital expenditures; the uncertainty of estimates and projections relating to reserves, production, costand expenses; health, safety and environmental risks; commodity price and exchange rate fluctuations; marketing and transportation; loss of markets; environmental risks; competition;inability to retain drilling rigs and other services; capital expenditure costs, including drilling, completion and facilities costs; unexpected decline rates in wells; delays in projects and/oroperations resulting from surface conditions; wells not performing as expected; incorrect assessment of the value of acquisitions including the Arrangement; failure to realize theanticipated benefits of acquisitions including the Arrangement; ability to access sufficient capital from internal and external sources; delays resulting from or failure to obtain requiredregulatory and other approvals; and changes in legislation, including but not limited to tax laws, royalties and environmental regulations. An Arrangement Agreement has not beenentered into and there are no assurances that one will be executed.

There are risks also inherent in the nature of the proposed Arrangement, including failure to realize anticipated production increases and anticipated cost savings and other synergies;risks regarding the integration of Vero and TORC; incorrect assessment of the value of Vero and/or TORC; and failure to obtain the required shareholder, court, regulatory and otherthird party approvals. This presentation also contains forward‐looking information concerning the anticipated completion of the Arrangement and the anticipated timing thereof. TORChas provided these anticipated times in reliance on certain assumptions that it believes are reasonable, including assumptions as to the time required to prepare meeting materials formailing, the timing of receipt of the necessary regulatory and court approvals and the satisfaction of and time necessary to satisfy the conditions to the closing of the Arrangement.These dates may change for a number of reasons, including unforeseen delays in preparing meeting materials, inability to secure necessary regulatory or court approvals in the timeassumed or the need for additional time to satisfy the conditions to the completion of the Arrangement. In addition, there are no assurances the Arrangement will be completed. As aconsequence, actual results may differ materially from those anticipated in the forward‐looking statements and readers should not place undue reliance on the forward‐lookinginformation contained in this presentation.

Forward‐looking statements or information are based on a number of factors and assumptions which have been used to develop such statements and information but which may proveto be incorrect. Although TORC believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed onforward‐looking statements because TORC can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified inthis document, assumptions have been made regarding, among other things: the impact of increasing competition; the general stability of the economic and political environment inwhich Vero and TORC operate; the timely receipt of any required regulatory and shareholder approvals; the ability to obtain financing on acceptable terms; the performance of existingwells; the success obtained in drilling new wells; future well production rates, decline rates and reserve volumes; the ability to replace and expand oil and natural gas reserves; thetiming and costs of pipeline, storage and facility construction and expansion and the ability to secure adequate product transportation; future oil and natural gas prices; the sufficiencyof budgeted capital expenditures in carrying out planned activities; the availability and cost of labour and services; currency, exchange and interest rates; the regulatory frameworkregarding royalties, taxes and environmental matters in the jurisdictions in which Vero and TORC operate; and the ability to successfully market oil and natural gas products.

Readers are cautioned that the foregoing list of factors and assumptions is not exhaustive. Furthermore, the forward‐looking statements contained in this presentation are made as atthe date of this presentation and TORC does not undertake any obligation to update publicly or to revise any of the included forward‐looking statements, whether as a result of newinformation, future events or otherwise, except as may be required by applicable securities laws.

DPIIPAny references to oil resource or oil in place are intended to be the equivalent of Discovered Petroleum Initially In Place (DPIIP) which is defined as quantity of hydrocarbons that areestimated to be in place within a known accumulation, plus those estimated quantities in accumulations yet to be discovered. There is no certainty that it will be commercially viable toproduce any portion of the resources. A recovery project cannot be defined for this volume of DPIIP at this time, and as such it cannot be further sub‐categorized.

BOES:Disclosure provided herein in respect of barrels of oil equivalent (boe) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf: 1 Bbl is based on an energyequivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price ofcrude oil as compared to natural gas is significantly different from the energy equivalency of 6:1; utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

March 2013

Corporate Profile

3

Strategy: Acquire / Exploit / Explore

Focus: High quality, large light oil‐in‐place reservoirs

Production Guidance:4,250 boepd (> 75% light oil and NGLs) – 2013E Average4,900 boepd (> 75% light oil and NGLs) – 2013E Exit

2013E Capex: $125mm

Reserves (Dec. 31, 2012):10.5 mmboe (Proved)18.9 mmboe (P+P)

Undrilled Resource:

Cardium• > 90 net oil focused sections

> 300 net undrilled locations> 240 net unbooked locations

Monarch• > 150 net prospective sections

Net Cash (Dec. 31, 2012): $35mm

Bank Line: $100mm undrawn

Tax Pools (Dec. 31, 2012): > $480mm

Shares Outstanding: 193mm; 219mm Fully Diluted

Symbol: “TOG” on TSX

TORC Strategy – Exposure to Light Oil Resource

4

• Consistent vision – focus on high quality, tight light oil resource plays

• Positioned for material growth through balance of development prospects andemerging resource plays

• 3‐Phase Strategy:

• Integrated philosophy for Production Growth: Acquire / Exploit / Explore

Production Growth2013+

PublicCo (Nov 2012)

Delineation2012

PrivateCo

Resource Capture2011

PrivateCo

TORC Position – Exposure to Light Oil Resource

5

Positioned for material growth through balance of development prospects and emerging resource plays

Cardium Trend• Lower risk development

• Significant, high quality, undrilled inventory

Monarch

• Significant oil in place

• Continued delineation in 2013

• Goal is to move a significant portion of the play to development by 2014

• Represents a step‐change to TORC’s development inventory

Edmonton

Calgary

Alberta

Cardium Trend:Core Development Asset

Monarch: Emerging Light Oil Resource Play

2012 – Year of Delineation + Acquisition

6

Cardium:(lower risk development)

• 16 wells (9.6 net) drilled ‐ 94% success

• 8 of 16 wells were farmin wells

• Cardium F&D (incl FDC) of $22.94/boe

• No development wells were drilled prior to acquiring Vero

Monarch:(step‐change asset)

• 9 wells (9.0 net) drilled ‐ 89% success

• 100% exploration

• Confirmed geological concepts over a geographical area spanning 40 miles

• Confirmed oil resource – moving to engineering phase

Acquisition:(Acquire/Exploit/Explore)

• Acquired Vero on November 19, 2012

• Total 2012 acquisition cost of $169mm (incl capex on acquired lands) –acquired 10.4 mmboe (Dec 31/12)

• Total 2012 acquisition cost of $16.24 per P+P boe($23.79 per P+P boe including FDC)

• Direct overlay of asset base

• Focused acquisition ‐ only Cardium assets

• Public market vehicle

0.0

20.0

40.0

60.0

80.0

100.0

120.0

0.0

5.0

10.0

15.0

20.0

Beg 2012 Jan 2012 + Organic Adds End 2012P+

P Re

serves per 100

0 Shares

P+P Re

serves (m

mbo

e)

2012 Reserves Growth

2012 Reserves Growth

7

Significant reserves growth in 2012 despite delineation focus

• 8 of 16 Cardium wells were farm‐in wells

• 65% of 2012 capital budget was focused on exploration

• No development wells were drilled prior to acquiring Vero

Key Measures

• FD&A (P+P incl. FDC) was $26.58/Boe

• 1.6x recycle ratio

• FDC of $200mm (1.6x 2013 Capex)

• Only 1.6 mmBoe booked at Monarch(~ 8.5% of total P+P reserves)

Organic Adds

Acquisitions

Organic Adds

Cardium – Development

8

Cardium: Significant Undrilled Development Inventory

9

TORC Land

Large Oil Resource: > 5 million bbls/section

Cardium Oil Focused Land: > 90 net oil sections

Drilled Cardium Wells: 59 net PDP wells

Booked Undrilled Cardium Wells: 49 net wells

2013 CAPEX: ~ $85mm

2013 Net Wells: 32 (22.3 net)

Undrilled Cardium Locations: > 300 net locations

Unbooked Cardium Locations: > 240 net locations

Significant inventory for continued organic growth

Cardium: Economics – Robust, Predictable Light Oil Inventory

10

• Focused Cardium acquisitions have resulted in high quality inventory: > 300 net undrilled locations

Large Oil Resource: > 5 million bbls/section

Estimated RF: ~ 15%

Estimated EUR/well: 185‐190 mbbls

Wells/section: 4

0.0

50.0

100.0

150.0

200.0

250.0

300.0

0 6 12 18 24

Oil Ra

te (b

bl/d)

Time (months)

SPROULE CARDIUM TYPE WELL OIL RATE

Type 140Type 185Type 240

Oil Reserves bbl 185,000

Total Reserves boe 244,693

Cost 1 $mm $3.9

NPV10% (BT) 2 $mm $3.1

Netback 3 $/boe $42.00

F&D (boe) $/boe $15.94

Recycle Ratio x 2.6x

Note:

1. Assumes 20 stage x 25 ton per stage fracs

2. Sproule Dec 31, 2012 price deck ‐ see Appendix

3. Based on $85.00 Edm Light

Cardium: Beyond Four Wells Per Section

11

> 2,000 Hz oil wells have now been drilled in the Cardium play since 2009(> $6 Bln has been spent)

UPSIDE

Technology Evolution

• Optimizing completion techniques continues to lower costs and improve results

• Initially 8 stage fracs, now 20+ stages

• Increased tonnage

• Fit‐for‐purpose frac fluids

Well Spacing

• Well density increasingly being expanded

• Current well spacing per section: 4

• Future well spacing per section: 5‐8

• Competitors have drilled up to 8 wells per section

Enhanced Recovery

• Pembina Cardium Pool, developed vertically, has been under water flood since the 1950s

• Water flooding and other enhanced oil recovery schemes have potential to increaserecovery factors and lower capital efficiencies over time

• Similar geological characteristics to Viewfield Bakken pool, which is now undergoingwater flood

Large light oil resource plays continue to evolve

Monarch – Exposure to Light Oil Opportunity For Step‐Change in Value

12

Monarch: Large Oil Resource Prospect

13

EVOLU

TION

History Current Status

TORC’s strategy

Monarch identified in 2010 as a significant light oil prospect

Combine:

• High quality Lower Risk Development Inventory (Cardium)

with

• Material exposure to Emerging Light Oil Resource

• Focus on estimated oil per section

• Estimated at 10‐25 mmbbls per section

Discovery well drilled in 2011

Initial delineation confirmed

Confirmed:

• Light oil (30°+ API)

• Overpressured

• Producibility

• Geological interpretation

• Geographical span

• Large size of the prize (1.5 ‐2.0 bln bbls net to TORC)

Technological challenges experienced on delineation wells

Completion evolution

• Efficient sand placement

• Effective frac length

• Sand crushing

• Increased fluid volumes to create larger and longer path

• Increased gel loading to more effectively carry proppant

• Use ceramic proppant below 2000m to avoid sand crushing

Monarch: Large Oil Resource Exposure

14

Deep3500m

Shallow

1750

m

Key CharacteristicsProspective Land: > 150 net sections Depth: 1750 – 3500m

Oil Resource/section: Estimated 10‐25 million bbl oil/section Pressure: > 50% over‐pressured

Total Oil Resource: Estimated 1.5 to > 2 billion bbl oil net to TORC Oil Quality: 30 ‐ 43° API

Operations(to end of 2012):

13 (13.0 net) wells drilled (85% success)6 (6.0 net) on production5 (5.0 net) awaiting completion or equipping

Monarch: Recent Well Performance

15

• 2‐9 and 16‐2 have followed a significantly different decline profile relative to the initial 2‐17 discovery well

Continued production data will confirm production profile

0

100

200

300

400

500

600

0 5000 10000 15000 20000 25000 30000 35000 40000 45000 50000 55000 60000

Prod

uctio

n rate (b

bl/d)

Cumulative Production (bbls)

Pearce ‐ Penny Production Comparison (Rate vs. Cum Prod)

Pearce 02‐17 (130 mbbls)

Pearce 02‐09 (335 mbbls)

Penny 16‐02 (348 mbbls)

Sand Crushing Observed at 02‐17

Monarch: Western Flank

16

• The western flank of the Monarch play drops below 3000m

– Higher API to 40°+

– Higher potential productivity

– Higher gas drive (GOR 2000/2500 (25%))

• 2 wells on western flank – both have only been tested

• Significant improvement in sand placement in most recent well (3‐26)

• Increased gas (25%) resulted in the need to restrict exploration well production

(expect 100 – 125 bbls/d beginning in March 2013

– volume and pressure will be analyzed over time to predict unrestricted potential

Monarch: 2013 – Move Towards Development

17

• Goal in 2013 is to move portions of the play into the development phase

– Compete with Cardium $’s

• Plan to drill 4‐6 wells in 2013

– First well currently drilling

• Analyze production profiles

• Refine completion technique

• Refine cost analysis

Move to development phase would create step change in TORC’s inventory

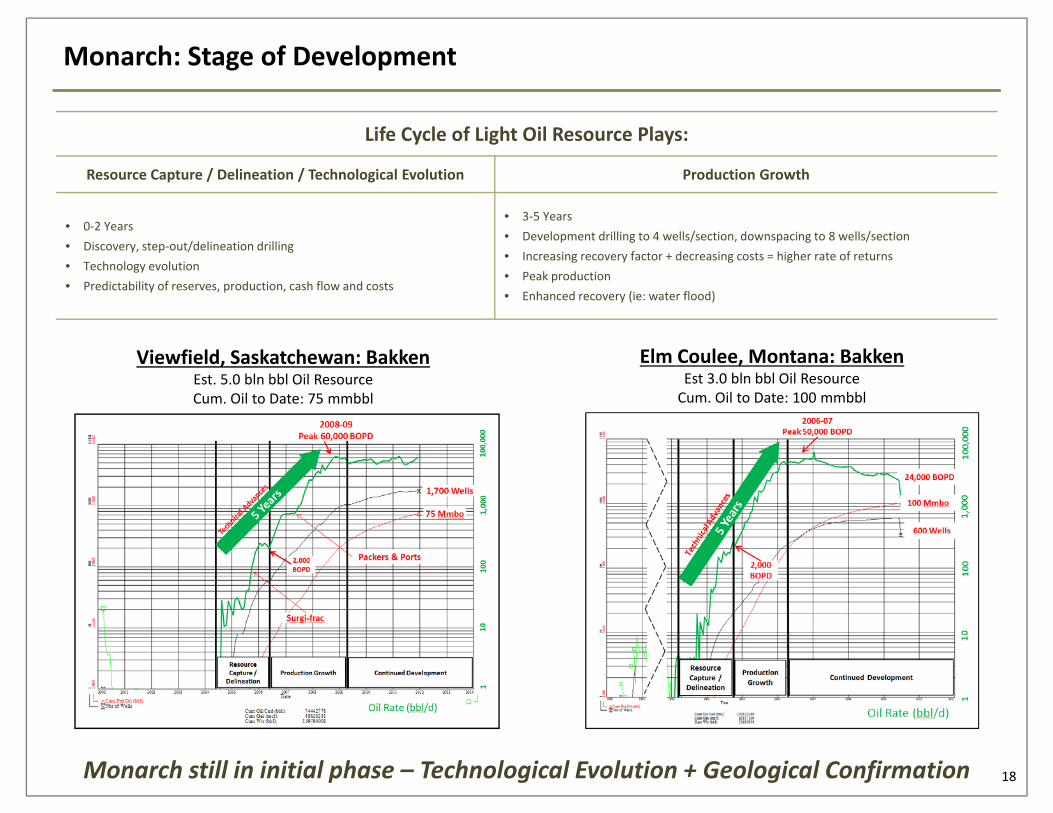

Monarch: Stage of Development

18

Viewfield, Saskatchewan: BakkenEst. 5.0 bln bbl Oil ResourceCum. Oil to Date: 75 mmbbl

Elm Coulee, Montana: BakkenEst 3.0 bln bbl Oil ResourceCum. Oil to Date: 100 mmbbl

Monarch still in initial phase – Technological Evolution + Geological Confirmation

Life Cycle of Light Oil Resource Plays:

Resource Capture / Delineation / Technological Evolution Production Growth

• 0‐2 Years• Discovery, step‐out/delineation drilling• Technology evolution• Predictability of reserves, production, cash flow and costs

• 3‐5 Years• Development drilling to 4 wells/section, downspacing to 8 wells/section• Increasing recovery factor + decreasing costs = higher rate of returns• Peak production• Enhanced recovery (ie: water flood)

Basic NAV

$mm Per Share2012 P+P NPV 10% 1 $303 $1.57Add: Positive Working Capital 2 $35 $0.18Total $338 $1.75

Unbooked Cardium

Net Risked Net EstimatedUnbooked Unbooked Capital / Total NPV / TVM PerLocations Locations 3 Well Capital Location 1 Total NPV 4 Adjusted 5 Share

$mm $mm $mm $mm $mm

Inventory 240 190 $3.9 $741 $3.1 $586 $440 $2.28

Total Base NAV plus Cardium Unbooked Upside $778 $4.03

Cardium Unbooked Inventory: Monarch:60 sections @ 5 mmbbls/section = 150 sections @ 10‐25 mmbbls/section =

300 mmbbls of Oil Resource vs >1.5‐2.0 blnbbls of Oil Resource

1. Sproule Evaluation, Dec 31, 2012

2. As at Dec 31, 2012

3. 4 wells per section and locations risked at 80%

4. Assumes all wells drilled immediately

5. Assumes 5 yr drilling program

Material Light Oil Exposure

19Monarch is 5x the size of the unbooked Cardium opportunity

Corporate

20

2013 Capital Program

Focus on Organic Development Growth in the Cardium and Further Delineation Drilling and Technology Refinement at Monarch

• $125mm capital program

– ~ 90% allocated to DCET (drill, complete, equip & tie‐in)

– Cardium program focused on production growth (~ 70% of DCET budget)

– Additional southern Alberta delineation wells prior to production growth phase (~ 30% of DCET budget)

– Guiding production to average 4,250 BOE/d (> 75% light oil and NGLs) with an exit rate of over 4,900 BOE/d (> 75% light oil and NGLs)

• Limited production growth platform forecast in southern Alberta

21

70%

30%

2013 Drill, Complete & Tie‐in Breakdown

Cardium Southern Alberta

92%

8%

2013 Capital Expenditure Breakdown

DCET Facilities & Other

Acquire / Exploit / Explore

Fundamentally Positioned

22

Reserve Value Focused light oil reserve base

Unbooked Cardium Value underpinned by low risk, predictable unbooked Cardium development

Southern AB Upside Exposure to material step‐change in value with oil resource at Monarch

Strong Balance Sheet Well capitalized oil resource company

Experienced Management Significant management & staff experience and continuity

Corporate Information

ManagementBrett HermanPresident & Chief Executive Officer

Jason ZabinskyVice President, Finance &Chief Financial Officer

Filippo AngeliniVice President & Controller

Shane ManchesterVice President, Operations

Eric StrachanVice President, Exploration

Jeremy WallisVice President, Land

Mike WihakVice President, Production

James PasiekaCorporate Secretary

DirectorsJohn BrussaRaymond ChanBruce ChernoffBrett HermanDavid JohnsonDale ShwedHank Swartout

Independent Reserve EngineersSproule Associates Limited

BanksBMO Bank of MontrealTDCIBCRBC

AuditorKPMG LLP

Legal CounselHeenan Blaikie LLP

Transfer AgentOlympia Trust Company

Corporate OfficeEighth Avenue PlaceSuite 1800, 525 – 8th Avenue SWCalgary, AB T2P 1G1

T: (403) 930‐4120F: (403) 930‐4159www.torcoil.com

Analyst CoverageBMO Capital MarketsJim Byrne

CIBC World MarketsAdam Gill

Cormark SecuritiesTodd Kepler

Dundee Capital MarketsBrian Kristjansen

FirstEnergy CapitalCody Kwong

GMP SecuritiesJason Konzuk

Macquarie CapitalChristina Lopez

National Bank FinancialDan Payne

Paradigm CapitalLyndon Dunkley

Raymond JamesKristopher Zack

RBC Capital MarketsShailender Randhawa

Scotia CapitalWilliam Lee

Stifel NicolausMichael Zuk

TD SecuritiesJuan Jarrah 23

Appendix

24

Hedging

25

Hedge Summary

Volume (Bbl/d) Type ($C/Bbl) Index

Low High

Oct 1, 2012 – Mar 31, 2013 500 Swap 95.05 95.05 WTI

Apr 1, 2012 – Mar 31, 2013 250 Collar 90.00 110.00 WTI

Jan 1, 2013 – Mar 31, 2013 250 Collar 95.00 107.15 WTI

Jan 1, 2013 – Dec 31, 2013 250 Collar 95.00 106.00 WTI

Jan 1, 2013 – Dec 31, 2013 250 Collar 95.00 106.00 WTI

Apr 1, 2013 – Dec 31, 2013 500 Collar 90.00 100.00 WTI

Approximately 30% of projected 2013 crude production is hedged

Sproule Oil Price Forecast

26

31‐Dec‐12 31‐Dec‐11

2013 $89.63 $94.902014 $89.93 $92.002015 $88.29 $97.422016 $95.52 $99.372017 $96.96 $101.352018 $98.41 $103.382019 $99.89 $105.452020 $101.38 $107.562021 $102.91 $109.712022 $104.45 na2023 $106.02 na

Escalation Rate of 1.5% Thereafter

Escalation Rate of 2.0% Thereafter

Sproule Price Forecasts (WTI)

Monarch Prospect

• Early exploration in the ABPS– Began in 2009 near AB/MT border

• Initial Industry Focus:

– Middle Bakken

• TORC Focus:

– Big Valley and Banff

– ~ 60 miles north of AB/MT border

27

TORC Land

JGJGG

GGG

G

G EGS

FJJFK

G

J GGGE

G

G

G

G

E

GLJJ

GGU

G

GGG

J

JJG

G

J

GU

GKG

G

GVGV

GJ A

VEVJGG

JE

V

G GU

J

EVGU

JJJ

JG

G

G

GVCVG

GV

GGGGGGG

G

GI

J

G

G

G

GCE

GJ GK

GVEV

E V

G

GGEV

G

GGJ

G

I

C

FC

G

G

G

GU GU GU GU

GG

GG GGJ

GG

GGG

GJG

DVEV

GEVG

G

EVGG

G

G

G

J

GF

GGFGGIE

GJ L

GE

GGG

GEEIEEIIU

KEECIKCF

IEEEIEGEEEJFGJECECG

GUGGGGLG JLGGC

CLIJI

GICC

G GJ

G

G

J

G

LGLJG

GC

GGEV

EVGV

LL G

GUGU

EE

G

GGGGGCEEKGUEUECGEUGEIEDGG

EIDEGEGEIGG GGG

G

GE

FGIUGE

EIEUSLDUSUIUCUEUAAEESU

JEE EAEIEAEGIEGSEEEECGESUEFEUMGEUAUIEGUGIE

GEUEEUMUGGGSEEUEUIE

GU JSSGIECDSSII ECICEUCUCUEVEUCUCUSEEUS

UEEUIE

JGUGU

AUCUJUDUEEU

EUEAMUEJEUECUGUEGSUIE

UCS ESEUE GEG EUSGEEGUGGUEUSAEEU

SSGJEEEES

EUESEEUEUSJSEUEDU SSEEUSEEFEUEUESSUEEUSUIESUEUSUIEIEUIUSEE

UDUEESUSUSUEEEGEUIUGGC

GUSSEEUE

EDUEUEUEUSEUESUSUEUEU

SEUGEUGUGUS

EEGEVEEVCVDVSESSVSCVEUDVEEGEEUEUEUSEUE

EVEGSEESSVSGGCEEEEEEVEUSEVDV EUEEUEUSUEEUEU G

GU

G

GGGG

LLKFG

GJG

GEIU

LULUKUCUCU G

LCC

GCGI

G

G

GEGG

G

GG

GG

G

EEEUJGJIUAU

GJISU

IUEUCFLJG

GGUJFGU

G LK

GUEUGVGUSEUSUEUEEUEEUSUSSUEUEUEUEUEUSUEU

EUEEUEUEUSUEUSEUEUEUEUEUSUEEUSU

EUEEDUEEUEGU

EEUEEUSESEEUESGEEUEU EUEUSUJUEUEUIEEUEUEUIUEEUEUJUCULU GU GUIUE

UECESULU GUSEUSEUEUEUEUEU

GUGUGEIG

GUI

EUGGJ

G IUGCUCUKU

J GGJ LLG

G

GJG

G

ICGGG

CUCUGEVGGGGG GGGG

G

G

C

G

JCGVEV

CVGV C

AV

JGJJGVEV

G

GEV

AVAV

AV

J

CVCV

AV

G EV

GVEV

GGU

AV

GUGUJU

G

CV

EVGGV

EVJGA

V

EV

GEV

EV A

V

CV

CV

EV EV

A

V

GGAV

EV

G

G

G

AV

GGCCG

GU

GG

CV AV EVEVCV

G E

VCVCVA

VC VA V

C VE V

E VGAVEVG

CVC V

I VG E

V

A VE V

G

EU

G

GEV

LCA

VAV

G

GGEV

C

GGGGCGU

G

FFFFUFFGUMU

J

GGGG

CGF

G

J

CV

JGVGEV

A

V

M

G

G

AV G

AV

AV

G CVGV

GEV

G

E

J

GG

GU

JUJUKU

G

G

G

FKF

FG

A

V

AV

G

J

A

V

J

G

E

G

GGG

GG

GVG

G

AV

GGCV

G

G

J

GG

GG

G

EEEEE

NoMiddle Bakken

Middle Bakken

Alberta (AB)

Montana (MT)

TORC Focus

Monarch Type Log

AB/MT Type Log

Lethbridge

Monarch focused on different geological concept relative to initial industry focus

00/14-20-010-27W4/0Spud: 1993-03-16

FormTD: WBMNFluid: N/A

SASKOIL AMELIA 14-20-10-27ProdForm:

TD: 3260.0 m [TVD]KB: 1002.2 m

00/05-16-002-22W4/0Spud: 1980-10-25

FormTD: PCMBFluid: N/A

AMOCO ET AL SPRING COULEE 5-16-2-22ProdForm:

TD: 2865.0 m [TVD]KB: 1319.4 m

3% LS

3% DOL

3% LS

3% DOL

Banff

Big ValleyMiddle Bakken

Banff

Bakken

Sha

les

Bakken Shale

28

Initial Industry FocusAB/MT Border Type Log

TORC FocusMonarch Type Log

Oil Resource/Section (mmbbl)Banff 1.9Middle Bakken Non‐reservoirBig Valley 1.2Total 3.1

Big Valley

Monarch Prospect Type Logs: Focus on Oil Resource

vs.

vs.

Oil Resource/Section (mmbbl)Banff 9.6Middle Bakken AbsentBig Valley 6.1Total 15.7

2013 Guidance

29

Capital:

• $125mm budget

― ~ $115mm drilling & completions

• ~ $80mm Cardium (~ 22 net wells)

• ~ $35mm Monarch (~ 4‐6 net wells)

― ~ $10mm facilities & other

Production:• 4,250 boepd (> 75% light oil and NGLs) – 2013 Average

• 4,900 boepd (> 75% light oil and NGLs) – 2013 Exit

Cash Flow:

• Assumptions

― Edmonton Light Oil Differential ‐ $4.00/bbl

― Natural Gas Differential + $0.40/mcf

― Average Royalty 15%

― OPEX & Transportation $15.00/boe

― G&A $4.00/boe