23

Investor Relations Rio de Janeiro 21 Feb 2011 4Q10 & FY2010 Rio de Janeiro, 21 Feb. 2011 Results Presentation

Investor RelationsRio de Janeiro 21 Feb 2011

4Q10 & FY2010Rio de Janeiro, 21 Feb. 2011Results Presentation

Agenda

Results in Summary – Luca Luciani

Turnaround Accomplished – Lorenzo Lindner

Financial Results 4Q10 – Claudio Zezza

Strategy – Rogério Takayanagi

Perspectives – Luca Luciani

1

2010 Summary

Customer Base

Q4 10Δ YoY

51 0 Mln

FY 2010Δ YoY

+24%

IFRS Brazil, R$ Mln GuidanceCompliance

Customer Base

Growth

• Market Share

• Incremental Market Share

+150 bps

51.0 Mln

25.1%

34.2%

+24%

EBITDA Margin

• Service Revenues

Net Revenues 3,926

30 6%

3,627

+9.9%

+20 bps

+6.0%

14,457

29 0%

13,572

+5.2%

+320 bps

+6.1%

EBITDA Margin

• EBITDA

• EBIT

• Net Income

30.6%

1,201

515

+20 bps

+10.7%

+46.4%

29.0%

4,194

1,200

2 212

+320 bps

+18,4%

+136%

+176%

Profitability

• Net Income

Operating FCF

• Cashflow (EBITDA – CAPEX)

• CAPEX

2,212

1,358

2 836

+176%

+62%

+4 9%

1,372 +110%

• CAPEX

• CAPEX as % of Sales

• Net Financial Position

• Net Debt to EBITDA

2,836

19.6%

984

0,23x

+4.9%

-10 bps

-700

2

Agenda

Results in Summary – Luca Luciani

Turnaround Accomplished – Lorenzo Lindner

Financial Results 4Q10 – Claudio Zezza

Strategy – Rogério Takayanagi

Perspectives – Luca Luciani

3

TIM Brasil – 2 years later

Fundamentals Strategy Achievements

• Top of Mind

• High Preference Low Rejection

Brand “Quality, Innovation, Convenience”

• High Preference, Low Rejection

• Inverted erosion trend both in Pre-paid

and Post-paid

L di g i t l k t h

Customer Base Leverage TIM Community

• Leading incremental market share

• ~2 x MOU vs Q1 09 (129 minutes)

• Leading Long Distance segment (volume)

• Infinity web: 4x daily unique users in 4

Drivers of Growth TIM’s value proposition distinctiveness:

• Voice: Long unlimited call concepts: “One Nation

One Tariff” (Long Distance) • Infinity web: 4x daily unique users in 4

months (prepaid)

One Tariff (Long Distance)

• Data: Unlimited concepts: foster smartphone

penetration in a “no subsidy frame”

• +18% Ebitda growth while Customer Financials Combine Growth with Profitability: • +18% Ebitda growth while Customer

Base +24%

• Boosting business generated (out-calls,

data) while reducing business received

(incoming)

Financials Combine Growth with Profitability:

• Revenues rebounded and re-mixed (out vs. in)

• Focus on cash generation

(incoming)

• EBITDA – CAPEX at R$ 1.4 Bln (+62% YoY)

Network • Integrate Intelig Network, and start a new

Turnaround• TIM’s leased lines cost flattish vs. MOU

and data jump

4

Turnaround

• Focus resources on core business

(Network vs. Commercial)

and data jump

• Intelig Revenues +37% YoY

• +50% GSM capacity vs. YE 2008

• 10x 3G cities covered

Brand Repositioning – Preference and Top of Mind

Brand Preference

ΔYoY

Top of Mind

%

2523

2122

25

28Preference#1

#328

25

3130

29

27

+6pp

-2pp

ΔYoY

Player 1

15 16

15 15 #4

25

2223

2122

20

2pp

-2pp

2

18106

Player 2

Player 3

11 10

1H08 2H08 1H09 2H09 1H10 2H10

Rejection #1 20 20 -2pp

2009 20102008

y

H1 08 H2 08 H1 09 H2 09 H1 10 H2 10

233939Network

#1

YE’10Innovation and OfferingPreference

YE’10Rejection:YE’10 TIM

P1P2

2828 151617

23Quality

Innovation

#1

#1

P2P3

232425

40TIM

P1P2

P3

43

2020

5

10

15

20

25

30

1014

156

2

4

6

8

10

12

14

16

18

5

Convenience #1212223

43TIM

P1P2

P3

Source: Image Survey 13° wave, November/10

0 0

Player 1Player 2 Player 2Player 3 Player 1 Player 3

Customer Base Market Share Recovery

51 0 L d i I l

Mln lines EoP, % % lines EoP

Customer Base– Inverted erosion trend Market Share (Total and Incremental)

33 8 35.2 36.4 36.137.8

39.641.1 42.4

44.446.9

51.0 30.9%

25.9%

25 0%25.4%25.1%

29.7%

Leader in IncrementalShare 2010 (%)

11%25%30%34%

0

0

0

0

0

0

0

Incremental Market Share

Vivo

Claro32.5 33.8 35.2 25.0%

17.9%19.4%

2007 2008 2009 2010

0

0

TIM Vivo Claro Oi27%17% 18%

12%-10%

29% 27%19%

24%

34% 40% 36%

Inversion of Market Share erosion trend

Claro

Oi

23.6%24.2%

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

Customer Base Quality (Postpaid Base and Bad Debt)Commercial EfficiencyR$

2007 2008 2009 2010

Mln lines, % of Gross Total revenues, mobile

54

85

6.8 6.8 6.86.6

6.2 6.2 6.36.5

6.66.9

7.27.5

6%3.2

SAC*

SAC*/

Inversion of High Value Base erosion

trend

~ +20%~ -10%

-36%

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10

5%3% 3% 3%

2% 2% 2% 2% 2% 1% 1%

2.3

3.2 SAC*/ARPU

trend

Bad debt% Gross Rev.

-29%

6

2009 2010

*SAC = Subsidy + Commision + AdvertisingNote: Bad Debt/ Revenues – BRGAAP for 2008 and IFRS Brazil for 2009 and 2010

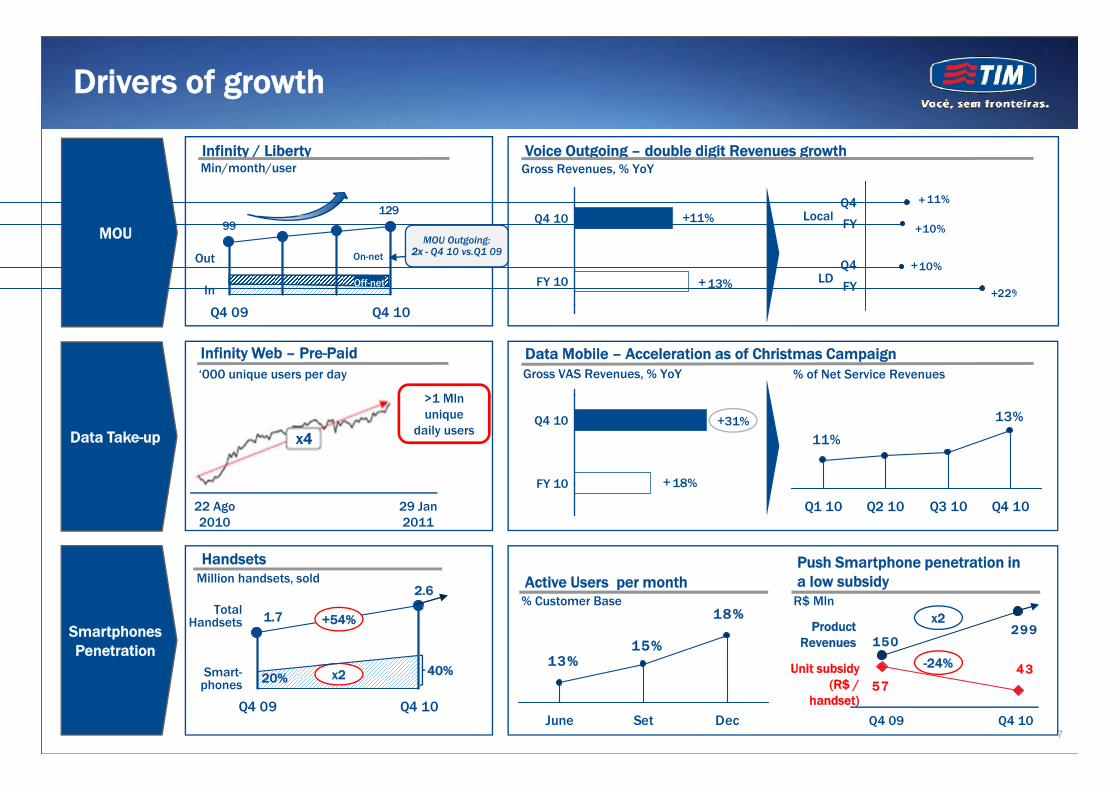

Drivers of growth

Infinity / LibertyMin/month/user

129

Voice Outgoing – double digit Revenues growth

11%Q4 10

Gross Revenues, % YoY

11%

LocalQ4

++

99

0

20

40

60

80

100

120

140

In

Out

13%

11%Q4 10

FY 10

MOU MOU Outgoing:2x - Q4 10 vs.Q1 09

22%

10%

10%Local

LD

FY

Q4

FY

+

+

+

+

+

On-net

Off-net

Infinity Web – Pre-Paid‘000 unique users per day

>1 Ml

Q4 09 Q4 10

Data Mobile – Acceleration as of Christmas CampaignGross VAS Revenues, % YoY % of Net Service Revenues

x4

>1 Mln unique

daily users

18%

31%Q4 10

FY 10

Data Take-up13%

11%

0

0

0

0

0

0

+

+

HandsetsMilli h d t ld

22 Ago 2010

29 Jan 2011

18%FY 100

Q1 10 Q2 10 Q3 10 Q4 10

+

Push Smartphone penetration in

150299

431

2

2

3

3

Total Handsets 1.7

2.6Million handsets, sold

SmartphonesPenetration

Active Users per month% Customer Base

+54%

U it b id

Product Revenues

x2

-24%

a low subsidyR$ Mln

18%

15%13% 0

0

0

0

0

0

7

43570

1

Q4 09 Q4 10

Smart-phones

40%20% x2 Unit subsidy(R$ /

handset)

24%

Q4 09 Q4 10

13%

0

0

0

0

0

June Set Dec

Revenues and Profitability

Net Revenues, R$ Bln EBITDA, R$ Bln

Revenues EBITDA and Margin %

IFRS Brazil

Total Revenues

EBITDA Margin %

4.2 12 7

13.614

15

15

13.714.4 +320bps+5.2%

29,0%

25,8%

+6.1%

EBITDA3.5

2009 2010

12.7

11

12

12

13

13

14

2009 2010

ServiceRevenues

+18%

R$ BlnR$ Bln

Cashflow (EBITDA - CAPEX) Net Financial Position

2009 20102009 2010

6%9%

1.361

2

R$ BlnR$ Bln

% of Net Revenues

0.47x

0.23x Net Debt /

EBITDA1.68

62%0.84

1

1

1

1

1

1

1

1

1

1

2009 2010

EBITDA -CAPEX

Net Debt0.98

0

1

1

1

1

1

2

-0.7+62%

8

2009 2010 2009 2010Operating

FCF 654 1,372+110%

Strenghtening Network Infrastructure

2G - Capacity# ‘000 TRX

CAPEX MixR$ Bln

2.7 2.8

IFRS Brazil3G – Coverage

Capital

Infrastructure

Commercial

120

67% 81%

19%33%

+50% 210

54%32%19%% urban

populationg

Capital allocation

CAPEX/ 60

70

80

90

100

110

2009 2010

19 7% 19 6%

# cities

5723

coverage

Intelig Revenues RevampingIntelig successfully integrated

CAPEX/ Sales

Network Opex Efficiency

2008 2009 201019.7% 19.6%

2008 2009 2010

YoY growth; 2010 vs 2009 Network and ITX Cost (R$ Bi, % YoY)

37%

29%26%

g ; ( , )

+ +

+

+0.3%Annual(4,227)

> 16.000 km backboneMAN at 15 cities

15%+

+0.1%4Q10 (1,084)

9

Q1 Q2 Q3 Q4

Agenda

Results in Summary – Luca Luciani

Turnaround Accomplished – Lorenzo Lindner

Financial Results 4Q10 – Claudio Zezza

Strategy – Rogério Takayanagi

Perspectives – Luca Luciani

10

Switching towards IFRS

Q1 Q2 Q3 Q4 FULL YEAR

Mln R$2010 2009

abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY VS. Guidance

Net Revenues 3.296 3.198 98 3,1% 3.559 3.512 47 1,3% 3.677 3.466 211 6,1% 3.926 3.571 354 9,9% 14.457 13.747 710 5,2%

of which Services 3.176 3.009 167 5,6% 3.350 3.144 206 6,6% 3.418 3.213 205 6,4% 3.627 3.422 205 6,0% 13.572 12.788 784 6,1%

of which Handsets 120 189 (69) -36,7% 209 368 (159) -43,2% 259 253 6 2,3% 299 150 149 99,6% 886 959 (73) -7,6%

EBITDA 947 715 232 32 5% 1 010 864 146 16 9% 1 035 877 158 18 1% 1 201 1 086 116 10 7% 4 193 3 541 652 18 4%

IFRS *

>5%

EBITDA 947 715 232 32,5% 1.010 864 146 16,9% 1.035 877 158 18,1% 1.201 1.086 116 10,7% 4.193 3.541 652 18,4%

Ebitda Margin % 28,7% 22,4% 28,4% 24,6% 28,2% 25,3% 30,6% 30,4% 29,0% 25,8%

Capex 689 322 368 114,4% 520 535 (15) -2,7% 526 692 (166) -24,0% 1.100 1.154 (54) -4,7% 2.836 2.702 134 4,9%

EBITDA - Capex 258 393 (136) -34,5% 490 329 161 49,0% 509 185 324 175,5% 101 (68) 169 -247,8% 1.358 839 519 61,9%

>4 Bln

~3 Bln

Consistency in Growth/ Profitability Improvement during the Quarters

Q1 Q2 Q3 Q4 FULL YEAR

Mln R$2010 2009

abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY 2010 2009abs. YoY

% YoY

Net Revenues 3.269 3.174 96 3,0% 3.531 3.486 45 1,3% 3.648 3.440 208 6,1% 3.894 3.542 352 9,9% 14.342 13.641 701 5,1%

of which Services 3.146 2.985 161 5,4% 3.317 3.118 199 6,4% 3.387 3.186 201 6,3% 3.592 3.386 205 6,1% 13.442 12.675 767 6,1%

of which Handsets 124 189 (65) -34,5% 213 368 (155) -42,1% 261 254 7 2,8% 303 156 147 94,4% 900 967 (66) -6,8%

EBITDA 810 618 191 30,9% 887 764 123 16,1% 924 772 152 19,6% 1.132 982 150 15,3% 3.752 3.136 616 19,6%

Ebitda Margin % 24,8% 19,5% 25,1% 21,9% 25,3% 22,5% 29,1% 27,7% 26,2% 23,0%

Br Gaap

*

>25%

>5%

11

g 24,8% 19,5% 25,1% 21,9% 25,3% 22,5% 29,1% 27,7% 26,2% 23,0%

Capex 576 201 375 186,7% 436 429 7 1,6% 463 541 (78) -14,3% 1.072 1.003 69 6,8% 2.547 2.174 373 17,2%

EBITDA - Capex 234 418 (184) -44,0% 450 335 116 34,6% 461 232 229 99,0% 60 (22) 81 -376,0% 1.205 962 243 25,2%

* 2009 IFRS includes Intelig ProformaNote: Key difference between BRGAAP and IFRS is in the capitalization of handsets subsidy.

~2.5 Bln

Revenues Analysis

Outgoing voice double-digit solid growth (FMS)Gross Service Revenues

IFRS BrazilQ410 vs. Q409FY10 vs. FY09

7,8%19%

9%

30%

10%8,2%

TIM Intelig Total

Outgoing voice double digit solid growth (FMS)

Data take-up over 30% YoY in Q4

Intelig accelerating

YoY Growth, %

++ +

+

+

+

g

Acceleration of handsets sales to support data roll-out (small-screen browsing)

Higher discounts to support SIM-only strategy in

Mobile

Voice Data

Voice In Others

+ + ++

13% 18%31%

11%

postpaidVoice Out

Data

Net Revenues Service Revenues

-11%-8%

-41%

-6%

5.2%9.9%

Net Revenues

Total Net Revenues ++

YoY Growth, %

Service RevenuesYoY Growth, %

8.5%9.5%

Gross +

+

+

+

-7.6%

Handsets +99.6%15.1%

19.4%Taxes and discounts

+

+ +

12

6.1%6.0%Service

++

6,1%6.0%Net

+

+

Efficiency

Min/month, Mln R$ R$/ Gross add Mobile

Network Efficiency SAC

IFRS Brazil

% YoYMin/month, Mln R$

MOU

R$/ Gross add, Mobile

Network and

3.8 3.1 3.1 3.0 3.1

2.6 2.3 1.5

SAC*/ARPU99 100

110123 129

1.084 1 022 1 045 1.075 1.085

+30%

+0%

% YoY

ITX costs101 83 82 81 75 63 55 36

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

SAC*

1.084 1.022 1.045 1.075 1.085

4T 1T 2T 3T 4T

20102009

ProfitabilityBad Debt

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q420102009

1 222%

25%25%

30% 29% 28% 28%31%

R$ Bln, % Total Net Revenues

EBITDAMargin

% Gross Total Revenues

1 9%2.0%2.2%2.3%

3.2%

0.70.9 0.9

1.1 0.9 1.0 1.01.2

EBITDA

1.3%1.0%

1.9%2.0%1.7%

13

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q420102009

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q420102009

*SAC = Subsidy + Commision + 100% Advertising

Profitabilty and Cash Generation

Net Financial Position – Dec10

R$ Mln Cash

EBITDA Evolution (in R$ Mln)

- 42%+984

-274 -108 -12

+61

2,079

-1,252

1563 5414,194+18.4%

1,684, 156

984Oper FCF Non-Oper

FCF

3,541 18.4%

Q4 09 Q3 10 Q4 10

2,559 1,369 2,394

EBITDA 2009

25.8% 29.0%

EBITDA 2010

Business Generated +

Handsets

Business Received

(incoming)

Commercialexpenses

Network expenses

G&A + Others

expenses

+320Bpsp

R$ 3.38 bln (73% long term)

~22% of debt denominated in foreign currency (100% hedged against FX variation)Gross Debt

14

~22% of debt denominated in foreign currency (100% hedged against FX variation)

10.1% in Q4 10 vs. 9.67% in Q4 09 and 10.0% in Q3 10Average Annual Cost

Net Income and Proposed Dividend

Net Profit Proposed Dividend for 2010**

IFRS Brazil

Net Profit Proposed Dividend for 2010

497

R$ MlnR$ Mln2,212

+143%

777

171204+19%

5x

Total

Organic

801

129Tax

credit1,435Organic

Extraordinaryeffect

Taxcredit

Intelig* (564 mln)

672

2008 2009 2010

EPS 0,11 0,13 0,20

2009 2010

15*FX gain due to unhedged debt ** To be deliberate in the next Shareholder’s Meeting

Agenda

Results in Summary – Luca Luciani

Turnaround Accomplished – Lorenzo Lindner

Financial Results 4Q10 – Claudio Zezza

Strategy – Rogério Takayanagi

Perspectives – Luca Luciani

16

Brazil, a large and fast growing country

Gross Domestic Product (GDP)

US$ Tln 2010 Mln people

Middle Class Expansion

14.6

US$ Tln, 2010

13 20 31

200188175

A/B

Mln people

>4.8

Family Income(K R$/ month)

Expected to slow down to 4,5/5% in

2011

Possible impact from Govermt. saving program

of R$50bln

# 8

2.02 2.04 1.52.32.63.35.45.7

1.647

44

66 95 113

13

40

C

A/B

D

>4.8

1.1 –4.8

0.8 – 1.1

+3% +10% +3% +3% +2% +2% +1% +8% +3% +4%

4929 16

40E

2006 2009 2014< 0.8

USD 2 Trillion Gross Domestic Product 200 million people with average age 29 years oldUSD 2 Trillion Gross Domestic Product

+8% growth in 2010

~5% expected growth/ year for next years

200 million people with average age 29 years old

- Demographic bonus for next 10 years

- Middle-class explosion

• Class C behavior: An attractive country that

requires innovation on

17

- Very high willingness to use (everything)

- Willingness to pay (depends on new purchasing scheme)Go-To-Market to attack

emerging Class C/D people

TLC market driven by Mobile

Brazilian Telecom MarketCAGR 2010-2013

R$ BlnΔ R$ Bln13 vs. 10

+10+3-4%

CAGR 10-13Mobile

VOICE+5/7%

+40/45%

+6/8%

Incremental Revenues

120115

110 TotalDATA

Competitive positioning TIM

TIM: no trade-off in FMS

. More competition

. MTR reduction

51 55 62Mobile+11Broadband

FIXED

+20%

+40/45%

~25%

(voce)

Large room for growth in Mobile Internet access(data) for all (Class C

Mobile Attractiveness

50 48 42FixedVoice

-8

MOBILE

Fixed

FIXED (data) for all (Class C opportunity)

No brakesfor FMS

9 11 16

2010 2011 20132010 2011 2013

Voice

FixedBB

+7

Fixed

- 2%

VOICE -6%DATA

+20%Selective Intelig attack toCorporate/ SME segments(access, clouding)

Selected opportunities

(Big cities only)

18

2010 2011 20132010 2011 2013

* BRL/US$ = 1,70

Telecom expected dynamics

Acceleration of Fixed-Mobile Substitution

R$ / minute, voice

Difficulties to upgrade from BB fixed lines legacy

• Limited incumbent capability to upgrade

Annullement of mobile

price premiumMobile

<2

to adsl infrastructure:~ 5Km distance fromcentral switch

0.42 0.34

0.41 • Geo/demographic limit fi d BB i

5%

Fixed

% users per speed range, MBpsLow Speed Internet

>8 Mbps0 20 0.23

0.27 0.27

0.27 0.26 0.22

fixed BB expansion (very CAPEX intensive)

5%

77%

18%Between

2 e 8 Mbps

p

<2 MbpsQ3 10

0.20

2006 2007 2008 2009

Pure mobile has no trade-off between growth and Fixed cannibalization Difficult of fixed ops to combat FMS

Likely increase of competition in 2011 will further pressure mobile tariffs:

- Integration/Turn-around of

Need to access public funds to invest in broadband expansion

Likely to pressure for MTR cuts ( ibl glid th t ti g f id

19

existing players

- Launch of 5th national player

(possible glide path starting from mid 2011 with 10-20% reduction)

Strategy

Customer BaseSubscribers EoP Mln

Expected ResultsRationals

Natural expansion of TIM Subscribers EoP, Mln

Community matters(Size)

pCommunity pushed by word of mouthWin-back in selective 41

51

MOUMin/line/month, Average

geographic areas

Push FMS(TIM’ di ti ti i )

Price per minuteR$/min

2009 2010 2013

0.27 0.27

0 22 0.26

0.27

0.41

0 23

0.34

0.42

11683

> x2No brake for FMS

(Usage)

(TIM’s distinctiviness)Keep innovation as part of core business (push Infinity concept)

Mobile

Fixed0.22 0.23 0.20

2009 2010 2013

Digitalize the Foster webphone/ smartphone penetration

Q3 102009200820072006

Data RevenuesUnique usersInifinity Web daily unique users

1,8

13%

g ta e t einclusion of

TIM Community

(Data)

smartphone penetration Drop data price to leverage untapped demographic segment

x4> 1 Mln Infinity

Web

% on Service Revenues

DataRevenues

20

2009 2010 2013

( )LAN House substitution 22 Ago 10 29 Jan 11 (bln R$)

Agenda

Results in Summary – Luca Luciani

Turnaround Accomplished – Lorenzo Lindner

Financial Results 4Q10 – Claudio Zezza

Strategy – Rogério Takayanagi

Perspectives – Luca Luciani

21

TIM Brasil Conclusions

TIM Brasil tomorrowAttractiveness BrazilTIM Brasil 2010

4151

Bln R$, Mln lines

ServicesRevenues

Growth

5141

Customer BaseSubscribers EoP, Mln

Commu-nity “More

12.713.6

41

2009 2010

#3 Country on GDP growth*

Revenues

Customer Base

MOUMin/line/month, Average

09

mattersMore

people”10 11 12 13

25,8%29,0%

11683#4 worldwide Mobile Market

Profitability% of service revenues

EBITDA %

FMS “Talking More”

09 10 11 12 13

Internet users‘

19,6%19,6%

2009 2010

CAPEX% Data “Connected”

Internet users000 unique users

x4

22 Ago 29 Jan

25 FebruaryIndustrial Plan

2009 2010

Turnaround Accomplished

Company Repositioned

Opportunity of Brazilian mobile market

development

Competitive advantage for Pure Mobile

Perspectives

Revenues: Keeping the pace

22 Ago 2010

29 Jan 2011

22

Back to growth

Increasing profitability

Competitive advantage for Pure Mobile Ebitda: High single digit growth

Capex over Sales: Slight decrease

* Absolute growth: delta PIB 2010 – PIB 2009