51

TIME BARRED MORTGAGES IN BANKRUPTCY 2.0 Joseph Towne, Esq. Lender Legal Services, LLC

| Date post: | 12-Aug-2015 |

| Category: |

Documents |

| Upload: | joseph-towne |

| View: | 102 times |

| Download: | 3 times |

TIME BARRED MORTGAGES IN BANKRUPTCY 2.0Joseph Towne, Esq.

Lender Legal Services, LLC

Why is this issue important?

Why is this issue important?

- Both State and Federal Law are in a deep state of disagreement and flux

- Filling a Proof of Claim on a consumer debt Barred by the Statute of Limitations or Repose may be a Fair Debt Collection Practices Act violation.

Why is this issue important?- Debtors can use negative notice and a motion to determine

secured status under 11 U.S.C. § 506 as a core proceeding to discharge mortgages in bankruptcy court after confirmation. See In re Brown, 2014 WL 983532 (Bankr. M.D. Fla.) Quiet Title as an adversary proceeding may also available.

- Attorneys who file Proofs of claim on a time barred debts may be subject to penalties under Bankruptcy Procedure Rule 9011

- Candor to the court under Fla. R. Prof Conduct 4-3.3(a)(1)

FDCPA Liability-Recent Cases

- Crawford v. LVNV Funding, LLC, 758 F.3d 1254 (11th Cir. 2014).

- Facts: Creditor regularly purchases stale debts and files proofs of claim in bankruptcy court. Creditor filed a proof of claim on a debt barred under Alabama law and debtor filed an adversary proceeding alleging FDCPA violation. Creditor admitted that the debt at issue in this case would be unenforceable in state court and the creditor.

FDCPA Liability

- Crawford v. LVNV Funding, LLC, 758 F.3d 1254 (11th Cir. 2014).

- Held: since the debt was unenforceable under state law, filing a proof of claim was an FDCPA violation.

- The reasonable consumer standard applies to proofs of claims filed by attorneys in the bankruptcy context

FDCPA Liability

- However the second circuit, the Northern District of Illinois, Southern District of Illinois, and the Eastern District of Pennsylvania hold that a proof of claim on a time barred debt is not an FDCPA violation

FDCPA Liability- LVNV Strikes Back

- Donaldson v. LVNV Funding, LLC, 1:14-cv-01979-LJM-TAB; 2015 WL 1539607 (S.D. Ind. 2015 April 7, 2015).

- Facts: Debtor files Ch.13. LVNV files proofs of claims on credit cards that were barred under Indiana law because more than 6 years passed from the last payment made. Debtor files complaint for violation of the FDCPA.

FDCPA Liability- LVNV Strikes Back

- Donaldson v. LVNV Funding, LLC, 2015 WL 1539607 (S.D. Ind. 2015 April 7, 2015).

Held: Not false or deceptive when debtor lists debt on his schedules.

Under Indiana law debt was still owed even though it was barred.

Applied the competent lawyer standard, not least sophisticated consumer standard

FDCPA Liability

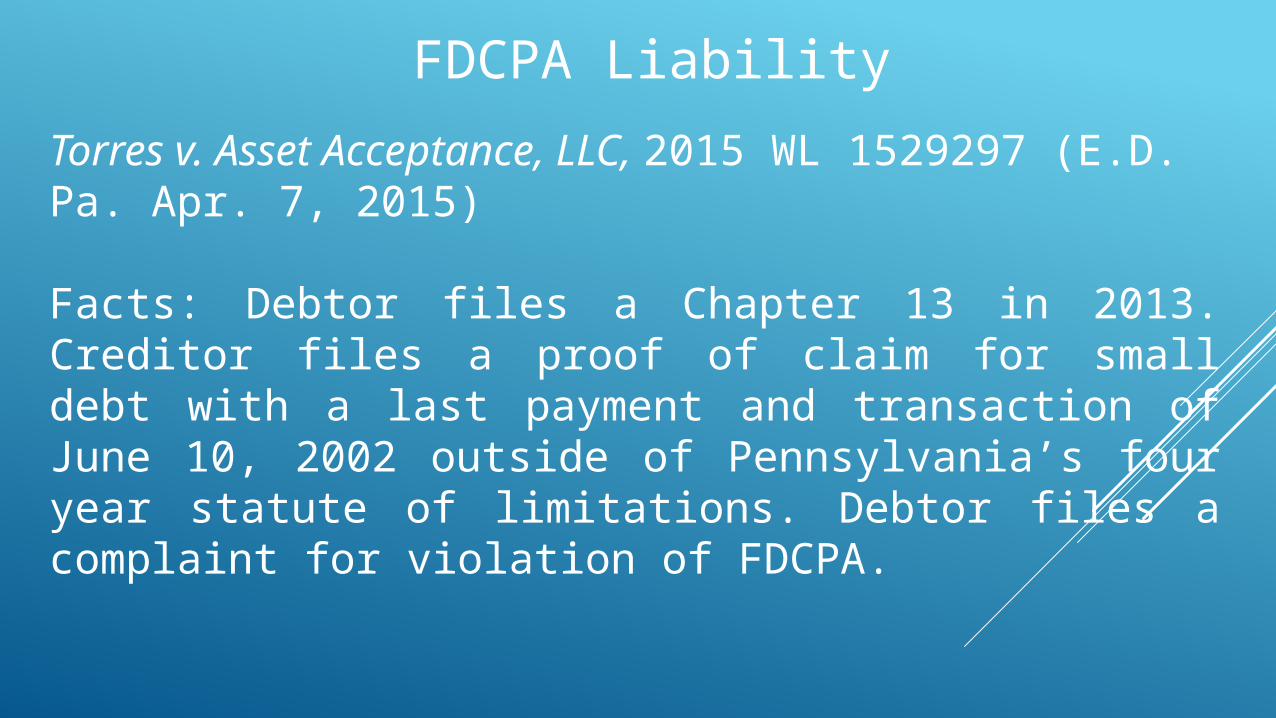

Torres v. Asset Acceptance, LLC, 2015 WL 1529297 (E.D. Pa. Apr. 7, 2015)

Facts: Debtor files a Chapter 13 in 2013. Creditor files a proof of claim for small debt with a last payment and transaction of June 10, 2002 outside of Pennsylvania’s four year statute of limitations. Debtor files a complaint for violation of FDCPA.

FDCPA LiabilityTorres v. Asset Acceptance, LLC, 2015 WL 1529297 (E.D. Pa. Apr. 7, 2015)

Held: Not possible to sue under the FDCPA for any violation in a proof of claim filed under the Bankruptcy Code.

The remedies under the Code (9011) were sufficient

“the Court will not insert judicially created remedies into Congress’s carefully calibrated bankruptcy scheme, thus tilting the balance of rights and obligations between debtors and creditors.”

FDCPA Liability

Bad News:

We don’t live in those jurisdictions

So how do we avoid liability until SCOTUS resolves the conflict?

First, find out if your debt is barred

State Law: Its not just the place you find the homestead

exemption anymore

Choice of law for determining the limitations statute for mortgages is the same under both Federal and Florida – local laws of situs subject to preemption

State Law: Its not just the place you find the homestead

exemption anymore

- Judgment – collateral estoppel law of the state is applied to determine judgment’s preclusive effect- However, the bankruptcy court retains exclusive

jurisdiction to determine dischargeability. St. Laurent v. Ambrose, 991 F.2d 672, 675 (11th Cir. 1993).

WHAT IS A MORTGAGE?

- Any written instrument securing money or advances (i.e. a Note).

- Installment Notes, Balloon Notes, Revolving Credit Agreements, Equitable Mortgages

COVENANTS- Payments- Due on Sale Clause- Occupancy- Acceleration based on a government

taking- Taxes- Insurance- Miscellaneous – e.g. mortgagor provide

service Dogs

Which Statute of Limitations applies to Mortgages?

Trick Question: 2 statutes – statute of limitations and statute of repose

Statute of Limitations

- Fla. Stat. § 95.11(2)(C) – within 5 years of accrual

- A procedural Statute that prevents the enforcement of the cause of action that has accrued. Houck Corp.

Statute of Limitations

- Prevents the enforcement of the remedy rather than the termination of the substantive rights of the parties. Allie v. Ionata

Five years from What?- Last Element occurs. Fla. Stat. § 95.11(2)(c)

- 4 elements of a foreclosure action- (1) an agreement (2) a default (3)

acceleration of debt to maturity (4) damages. Ernest v. Carter, 368 So.2d 428, 429 (Fla. 2d DCA 1979)

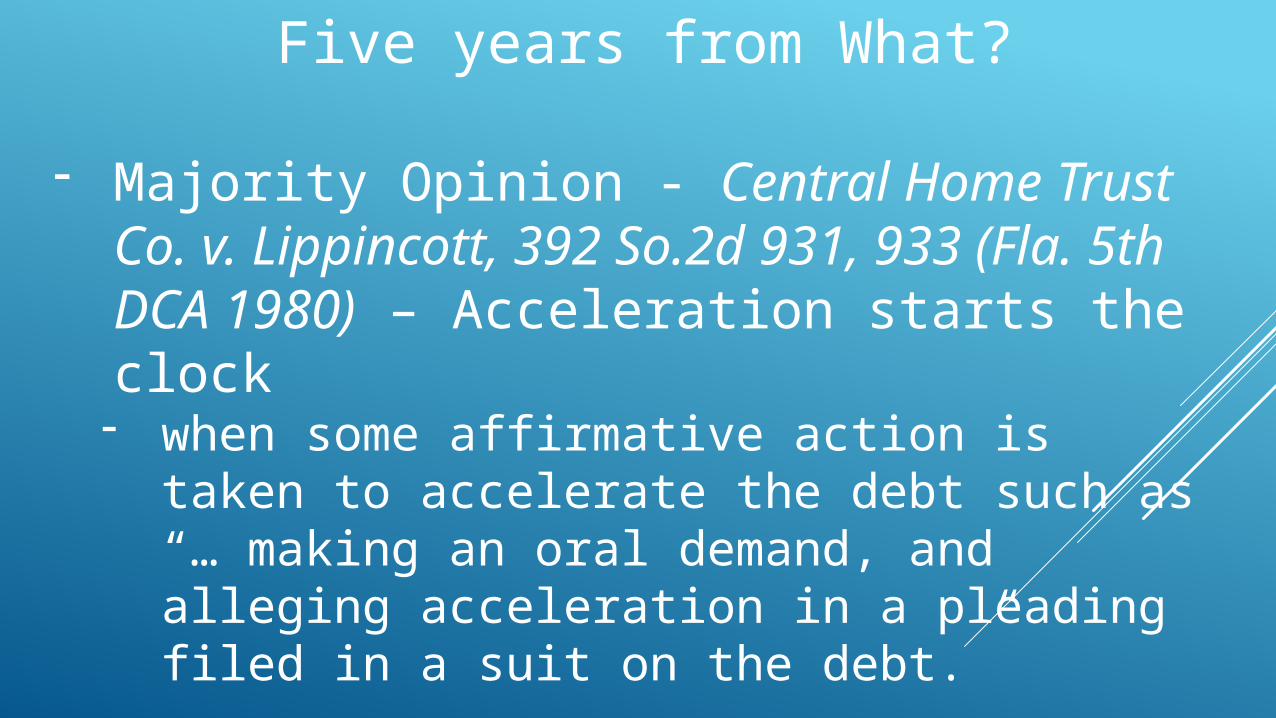

Five years from What?

- Majority Opinion - Central Home Trust Co. v. Lippincott, 392 So.2d 931, 933 (Fla. 5th DCA 1980) – Acceleration starts the clock- when some affirmative action is taken to

accelerate the debt such as “… making an oral demand, and alleging acceleration in a pleading filed in a suit on the debt.”

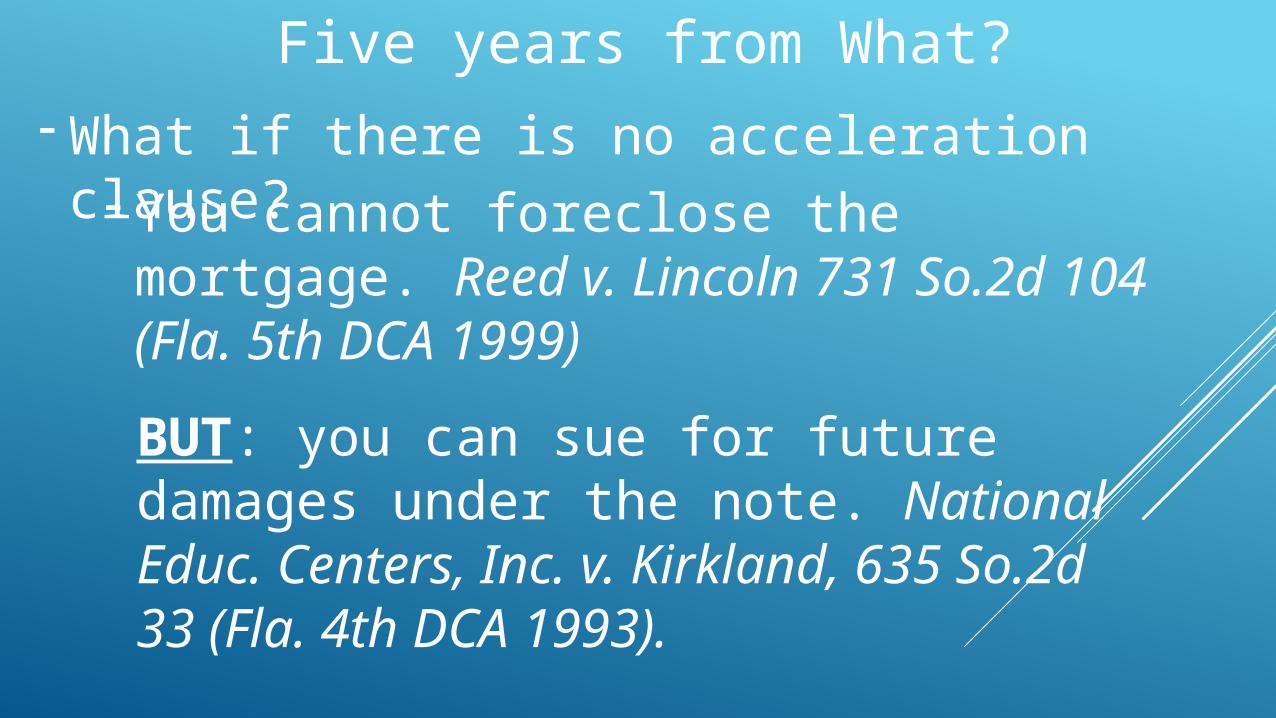

Five years from What?

- What if there is no acceleration clause?- You cannot foreclose the mortgage. Reed

v. Lincoln 731 So.2d 104 (Fla. 5th DCA 1999)

BUT: you can sue for future damages under the note. National Educ. Centers, Inc. v. Kirkland, 635 So.2d 33 (Fla. 4th DCA 1993).

Optional vs. Absolute Acceleration Clauses

- Optional – says acceleration does not occur until plaintiff exercises the option. i.e. Lippencott

- Absolute – Says that upon default future payments are immediately accelerated. Baader v. Walker, 153 So.2d 51 (Fla. 2d DCA 1963).

Optional vs. Absolute Acceleration Clauses- Can a presuit letter be the “acceleration”?

Held: not an acceleration because conduct was to occur in the future.

Snow v. Wells Fargo Bank, N.A., 156 So.3d 538 (Fla. 3d DCA 2015) “If you do not pay the full amount of the default, we shall accelerate the entire sum of both principal and interest due and payable....”. Mortgage contained an optional acceleration clause.

Minority/Dicta Position – Date of Default

- Mostly Dicta and inaccurate restatement of Florida Law

- CCM Pathfinder Palm Harbor Management, LLC v. Unknown Heirs of Gendron, 40 Fla. L. Weekly D244 (Fla. 2d DCA 2015); Dorta v. Wilmington Trust Nat. Ass’n, No. 5:13-cv-185-Oc-10PRL, 2014 WL 1152917 (M.D. Fla. March 24, 2014); Kaan v. Wells Fargo Bank, N.A., 2013 WL 5944074 (S.D.Fla. Nov. 5, 2013)

Statute of Repose

- Fla. Stat. § 95.281

- a substantive statute which not only bars enforcement of an accrued cause of action but may also prevent the accrual of a cause of action where the final element necessary for its creation occurs beyond the time period established by the statute. Houck Corp. v. New River, Ltd, 900 So.2d 601 (Fla. 2d DCA 2005).

Statute of Repose

- Either 5 years after the date of maturity if the maturity date is ascertainable from the record . . . OR

- If the maturity date is not ascertainable - 20 years after the date of the [execution of the] mortgage unless the note has a definite maturity date, etc.

Ascertainable from the record

- Must be clearly visible on the face of the recorded mortgage. CCM Pathfinder Palm Harbor Management, LLC v. Unknown Heirs of Gendron, 40 Fla. L. Weekly D244 (Fla. 2d DCA 2015).

Federal Preemption

Federal Preemption

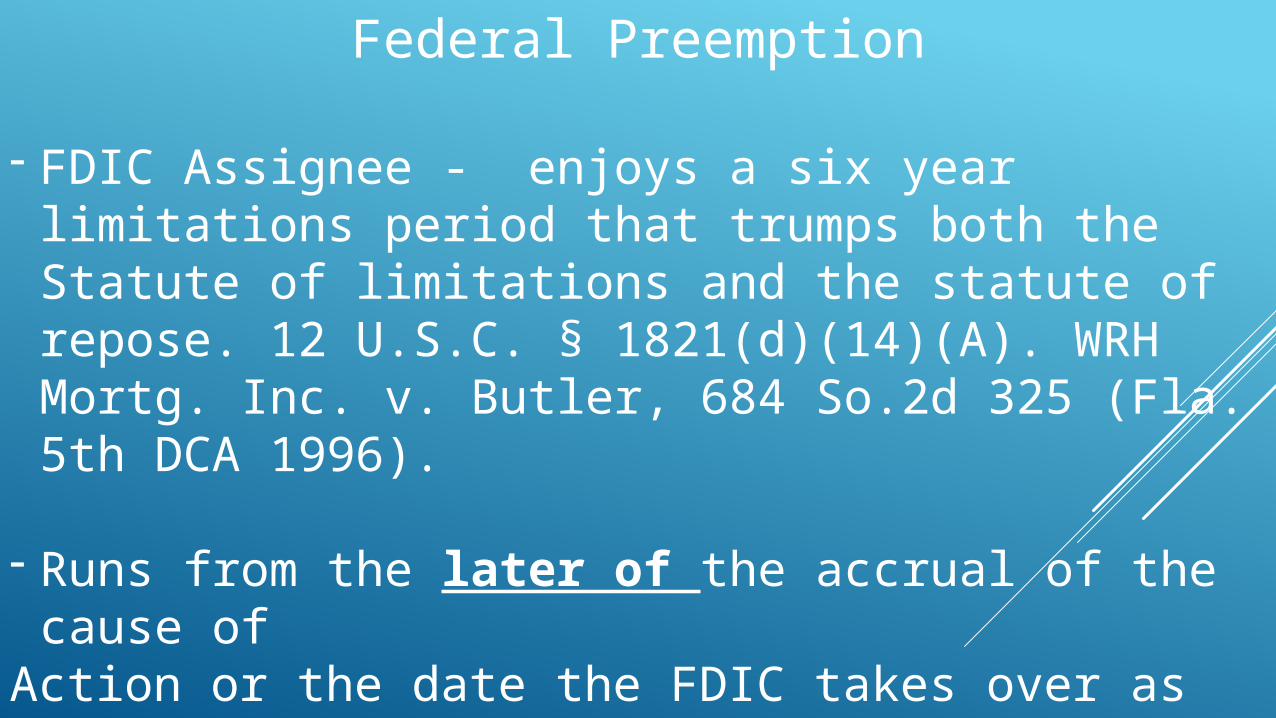

- FDIC Assignee - enjoys a six year limitations period that trumps both the Statute of limitations and the statute of repose. 12 U.S.C. § 1821(d)(14)(A). WRH Mortg. Inc. v. Butler, 684 So.2d 325 (Fla. 5th DCA 1996).

- Runs from the later of the accrual of the cause of Action or the date the FDIC takes over as receiver

- SBA Administration Assignee – infinite time to foreclose because there is no limitations period stated in the Small Business Administration Act. See Magnolia Federal Bank for Savings v. The United States of America, (U.S.D.C. So. Dist. Miss. 1993). See generally, United States v. Alvarado, 5 F.3d 1425 (11th Cir. Fla. 1993).

- Assignee of the USA acquires right to unlimited time to foreclose. LPP Mtg Ltd. v. Tucker, 48 So.3d 115 (Fla. 3rd DCA 2010).

Federal Preemption

Federal Preemption

United States of America as Mortgagee – Same as SBA Unlimited time to foreclose- 28 U.S.C. § 2415(c) states “nothing herein shall be deemed to limit the time for bringing an action to establish the title to, or right of possession of real or personal property”.

Tolling

Tolling

Death or incapacitation of the Mortgagee before the expiration of the cause of action (Applies to both limitations and repose)

(if death) the action may be commenced within 12 months from the date of the mortgagee’s death. Fla. Stat. § 733.104

(if incapacitation) within one year of appointment by the guardian. Fla. Stat. § 744.394

Tolling

Future Advance Clause - If the mortgage contains a future advance clause under Fla. Stat. § 697.04, then future advances made under the mortgage can extend the maturity date from five years to 20 years. See Razak v. Marina Club of Tampa Homeowners Assn., Inc., 968 So.2d 616 (Fla. 2d DCA 2007).

Typically seen in construction loans

Tolling

- Bankruptcy 11 U.S.C.A. § 108 applies to both repose and limitations- If the cause of action was not barred before the

filing then you have the later of- The end of the original statute of limitations

OR- 30 days after the notice of termination or

expiration of the automatic stay.

Tolling

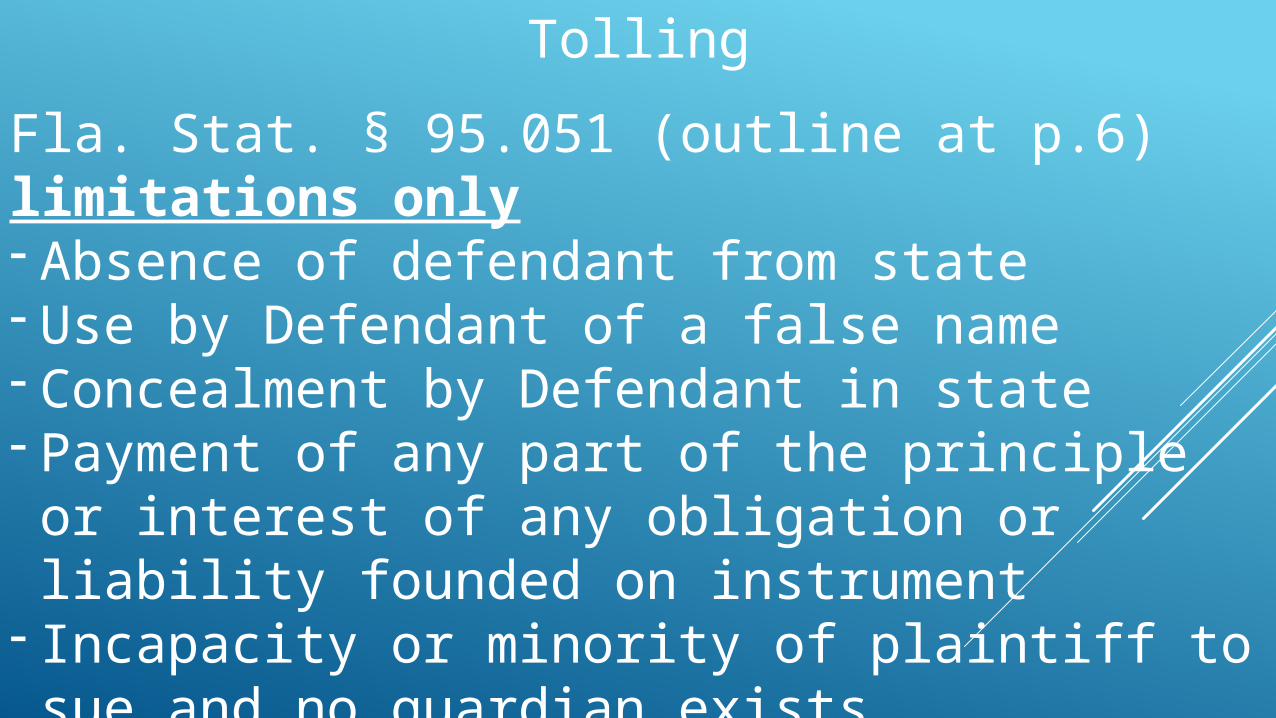

Fla. Stat. § 95.051 (outline at p.6) limitations only- Absence of defendant from state- Use by Defendant of a false name- Concealment by Defendant in state- Payment of any part of the principle or interest of

any obligation or liability founded on instrument- Incapacity or minority of plaintiff to sue and no

guardian exists

Tolling

- Equitable tolling – Prudent Plaintiff runs astray

Tolling

- Equitable tolling – Prudent Plaintiff runs astray- Does not require active deception on the part of

the defendant but focuses on the plaintiff with a reasonably prudent regard for his rights

- Examples: - Mislead or lulled into inaction- In some extraordinary way been prevented from

asserting rights- Timely asserted rights in wrong forum

Tolling

Equitable Estoppel a.k.a. Wrongdoing by Defendant

Tolling

Equitable Estoppel a.k.a. Wrongdoing by Defendant

- Plaintiff must plead that Plaintiff knew it had a cause of action but defendants wrong doing prevented plaintiff from bringing a timely action

- Plaintiff and defendant know about the facts giving rise to the suit but the wrongdoer prevails upon the other to forego enforcing his right until the statutory time has elapsed

Tolling

- Oral Promise to pay may also toll the statute of limitations

- Oral promise to pay or make partial payment if made prior to the statute of limitations tolls the statute of limitations. Jacksonville Am. Pub. Co. v. Jacksonville Paper Co., 197 So. 672, 676 (Fla. 1940)

Tolling

- Counterclaims for recoupment. See p.7 of outline

What happens when the statute of limitations runs?

What happens when the statute of limitations runs?

- Singleton v. Greymar Associates, 882 So.2d 1004, 1008 (Fla. 2004)

- Each new default is a breach which may be separately accelerated (in the context of res judicata)

What happens when the statute of limitations runs?

- U.S. Bank v. Bartram, 140 So.3d 1007 (5th DCA 2014).

- Each new default represents a new cause of action which may be an independent basis to accelerate the loan again

- Currently pending in supreme court – oral argument set for October 6, 2015.

What happens when the statute of limitations runs?

Third DCA - Deutsche Bank Trust Co. Amer. V. Beauvais, 2014 WL 7156961 (Fla. 3d DCA 2014). Bartram only applies to a subsequent action that follows a dismissal with prejudice. Dismissals without prejudice including voluntary dismissals do not reset statute of limitations. Deceleration notice may reset the action for SOL purposes, but unforeclosable lien remains in force until the expiration of the repose.

What happens when the statute of limitations runs?

- Clear Split of authority see chart on P. 11 of outline

FDCPA Liability Revisited

What do you do when you have a barred debt?

1. Is your debt barred? (see above)

2. Is your debt barred by SOL? If yes – 3 options1. File a proof of claim and advise your client they

will end up at the Supreme Court2. File a motion to determine the secured status of

your own claim and ask the court for an extension to file your proof of claim

FDCPA Liability RevisitedWhat do you do when you have a barred debt?1. Is your debt barred by SOL? If yes – 2 options:

1. File a motion to determine the secured status of your own claim and ask the court for an extension to file your proof of claim.

2. File the proof of claim and see what happens - If opposed, ask court to stay its ruling until Bartram is decided.

FDCPA Liability Revisited

What do you do when you have a barred debt?

1. Is your debt barred by the Statute of Repose?

- Is your debt really barred by the Statute of Repose? (see above)

- Tough luck – I like by bar license