33

Review: Time Value of Money MGF 641 Financial Policies and Strategies

| Date post: | 20-Jul-2016 |

| Category: |

Documents |

| Upload: | sagar-bansal |

| View: | 12 times |

| Download: | 0 times |

Review:

Time Value of Money

MGF 641

Financial Policies and Strategies

Outline

• Mapping costs and benefits into cash flows with a

timeline

• Three rules of time travel

• Valuing a stream of cash flows & Net present value

• Special cash flow patterns: Perpetuities and Annuities

• Spreadsheet exercises

From Costs and Benefits to Cash Flows (1)

• Common sense decision making process

– Identify the costs and benefits of an investment

– If the benefits outweigh costs, it is a “good” investment

• Decision to get an Master in Finance while working as a

corporate financial analyst

– Costs: tuition; efforts to study; sacrifice of leisure &

family time; less time for work

– Benefits: better career opportunities; higher salaries;

becoming an enlightened person

From Costs and Benefits to Cash Flows (2)

• In financial analysis, we monetize these costs and benefits

and call them “cash flows”

• Costs:

– Tuition: cash outflow of $3,000 each year for 3 years

(after taking into account employer reimbursement)

– Efforts to study: cash outflow of $4,000 each year for 3

years

– Sacrifice of leisure & family time: cash outflow of

$3,000 each year for 3 years

– Less time for work: (?)

From Costs and Benefits to Cash Flows (3)

• Benefits:

– Better career opportunities and higher salaries: cash

inflow of $20,000 each year for 10 years after getting

the degree

– Being enlightened: (?)

Time Line

• +: cash inflows; -: cash outflows

• Time 0: current date (decision making time)

• Assuming cash flows taking place at the end of each year

• Why the timeline? Because time value of money matters

Year 0 1 2 3 4 5 6 7 8 9 10 11 12

Tuition -3 -3 -3

Efforts -4 -4 -4

Time -3 -3 -3

Career & salaries +20 +20 +20 +20 +20 +20 +20 +20 +20 +20

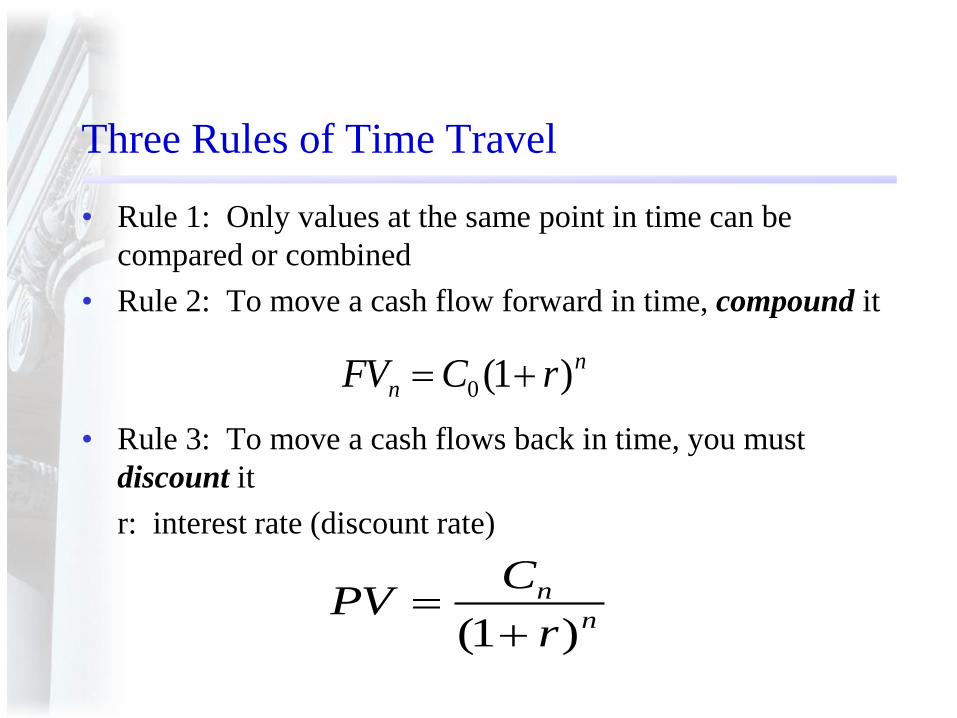

Three Rules of Time Travel

• Rule 1: Only values at the same point in time can be

compared or combined

• Rule 2: To move a cash flow forward in time, compound it

• Rule 3: To move a cash flows back in time, you must

discount it

r: interest rate (discount rate)

n

n rCFV )1(0

n

n

r

CPV

)1(

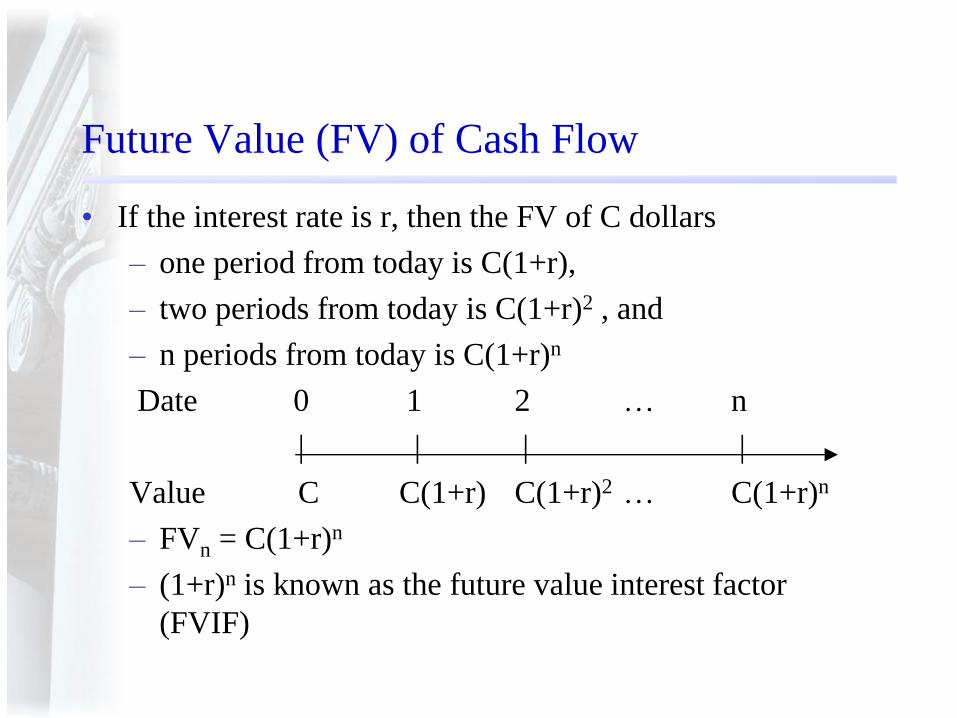

Future Value (FV) of Cash Flow

• If the interest rate is r, then the FV of C dollars

– one period from today is C(1+r),

– two periods from today is C(1+r)2 , and

– n periods from today is C(1+r)n

Date 0 1 2 … n

| | | |

Value C C(1+r) C(1+r)2 … C(1+r)n

– FVn = C(1+r)n

– (1+r)n is known as the future value interest factor

(FVIF)

Example:

• The employee profit sharing program of your company

allows you to deduct a certain amount from the payroll

each month. It earns 0.5% per month. How much is the

$50 I deduct from my first paycheck worth when I quit 6

years later?

Answer: $50x(1+0.005)72 = $71.60

Future Value (FV) of a $100 Cash Flow

2.5% 0.05 0.1 0.2

Year r=2.5% r=5.0% r=10.0% r=20.0%

1 103$ 105$ 110$ 120$

2 105$ 110$ 121$ 144$

3 108$ 116$ 133$ 173$

4 110$ 122$ 146$ 207$

5 113$ 128$ 161$ 249$

10 128$ 163$ 259$ 619$

20 164$ 265$ 673$ 3,834$

50 344$ 1,147$ 11,739$ 910,044$

100 1,181$ 13,150$ 1,378,061$ 8,281,797,452$

Future Value (FV) of a $100 Cash Flow:

Power of Compounding

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

0 5 10 15 20

Fu

ture V

alu

e

Years

r=2.5%

r=5.0%

r=10.0%

r=20.0%

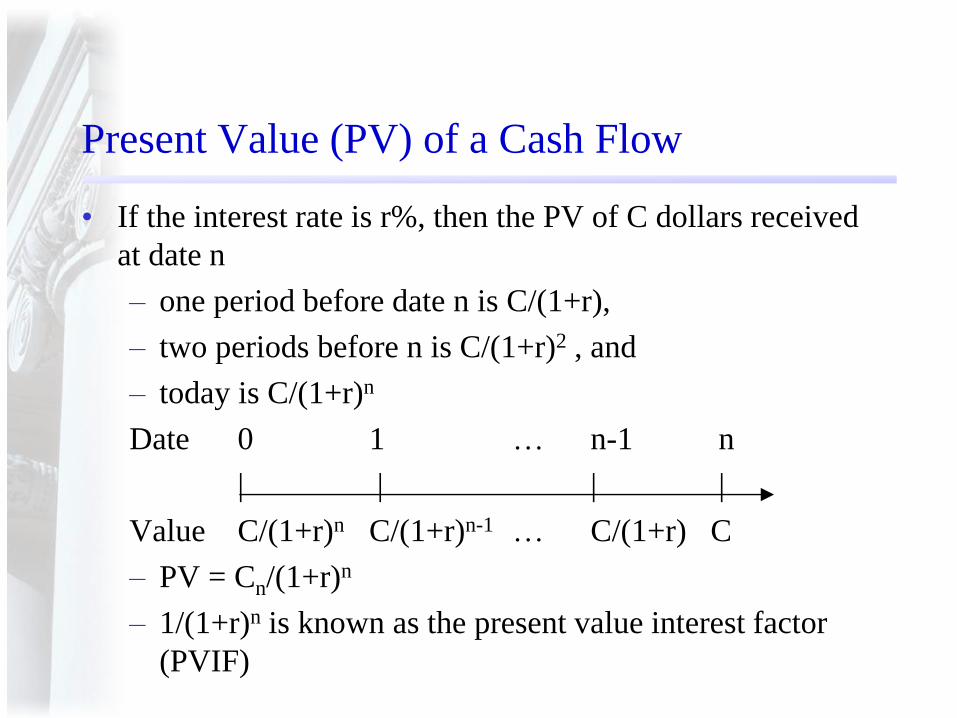

Present Value (PV) of a Cash Flow

• If the interest rate is r%, then the PV of C dollars received

at date n

– one period before date n is C/(1+r),

– two periods before n is C/(1+r)2 , and

– today is C/(1+r)n

Date 0 1 … n-1 n

| | | |

Value C/(1+r)n C/(1+r)n-1 … C/(1+r) C

– PV = Cn/(1+r)n

– 1/(1+r)n is known as the present value interest factor

(PVIF)

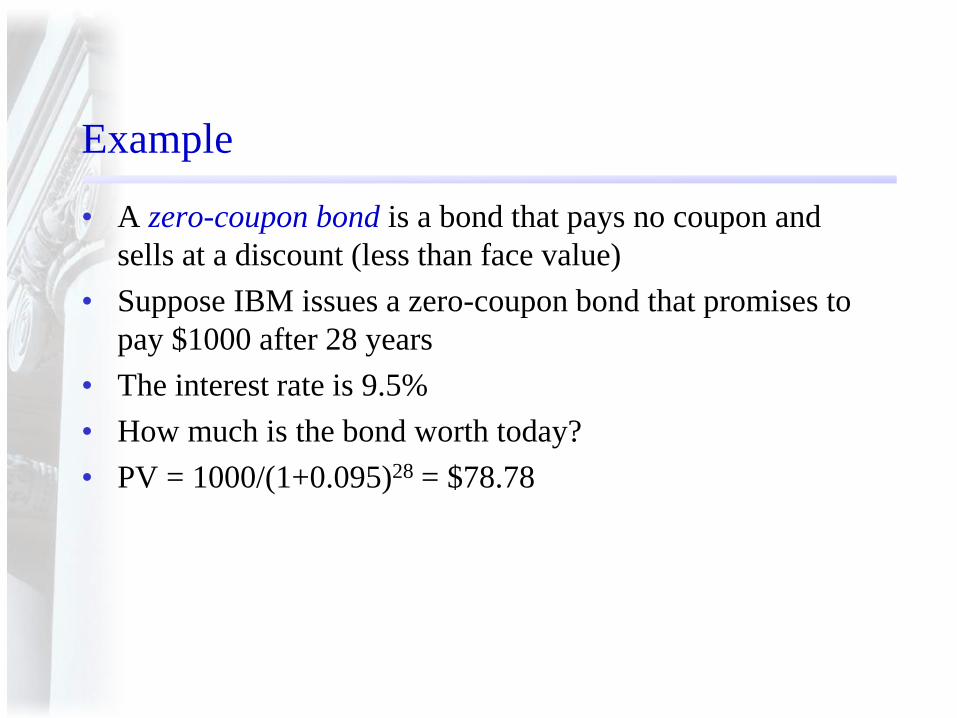

Example

• A zero-coupon bond is a bond that pays no coupon and

sells at a discount (less than face value)

• Suppose IBM issues a zero-coupon bond that promises to

pay $1000 after 28 years

• The interest rate is 9.5%

• How much is the bond worth today?

• PV = 1000/(1+0.095)28 = $78.78

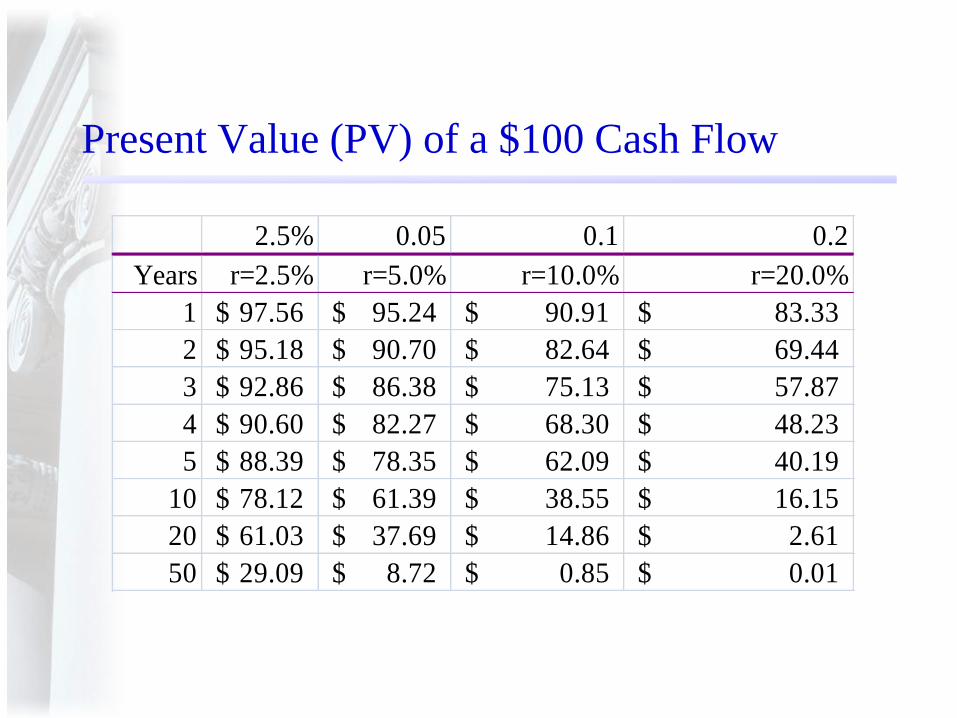

Present Value (PV) of a $100 Cash Flow

2.5% 0.05 0.1 0.2

Years r=2.5% r=5.0% r=10.0% r=20.0%

1 97.56$ 95.24$ 90.91$ 83.33$

2 95.18$ 90.70$ 82.64$ 69.44$

3 92.86$ 86.38$ 75.13$ 57.87$

4 90.60$ 82.27$ 68.30$ 48.23$

5 88.39$ 78.35$ 62.09$ 40.19$

10 78.12$ 61.39$ 38.55$ 16.15$

20 61.03$ 37.69$ 14.86$ 2.61$

50 29.09$ 8.72$ 0.85$ 0.01$

Present Value (PV) of a $100 Cash Flow

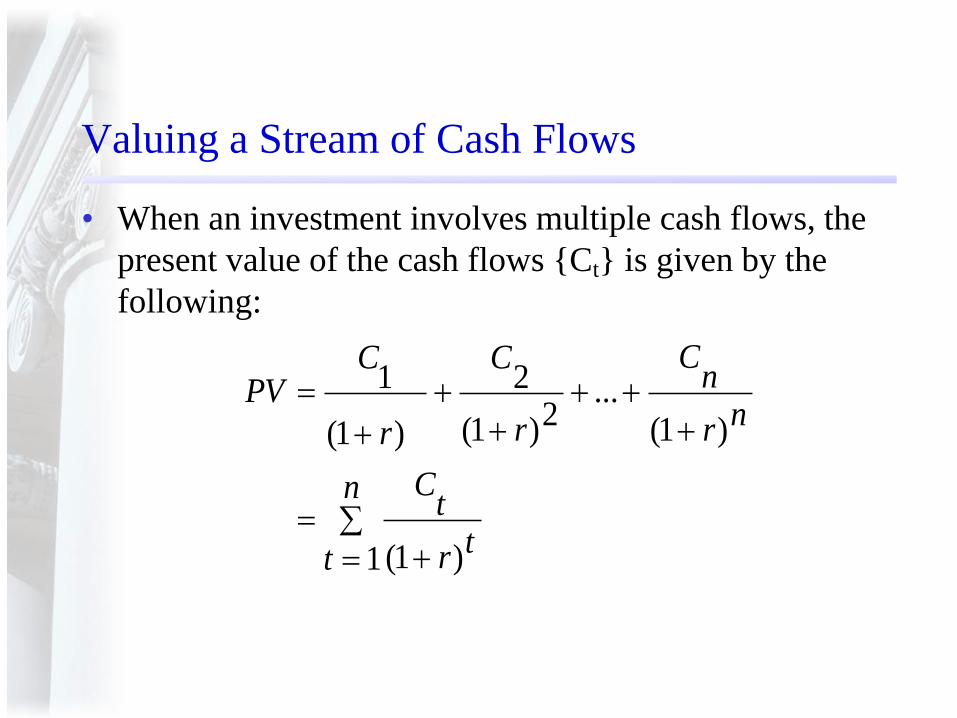

Valuing a Stream of Cash Flows

• When an investment involves multiple cash flows, the

present value of the cash flows {Ct} is given by the

following:

n

ttr

tC

nr

nC

r

C

r

CPV

1 )1(

)1(...

2)1(

2

)1(

1

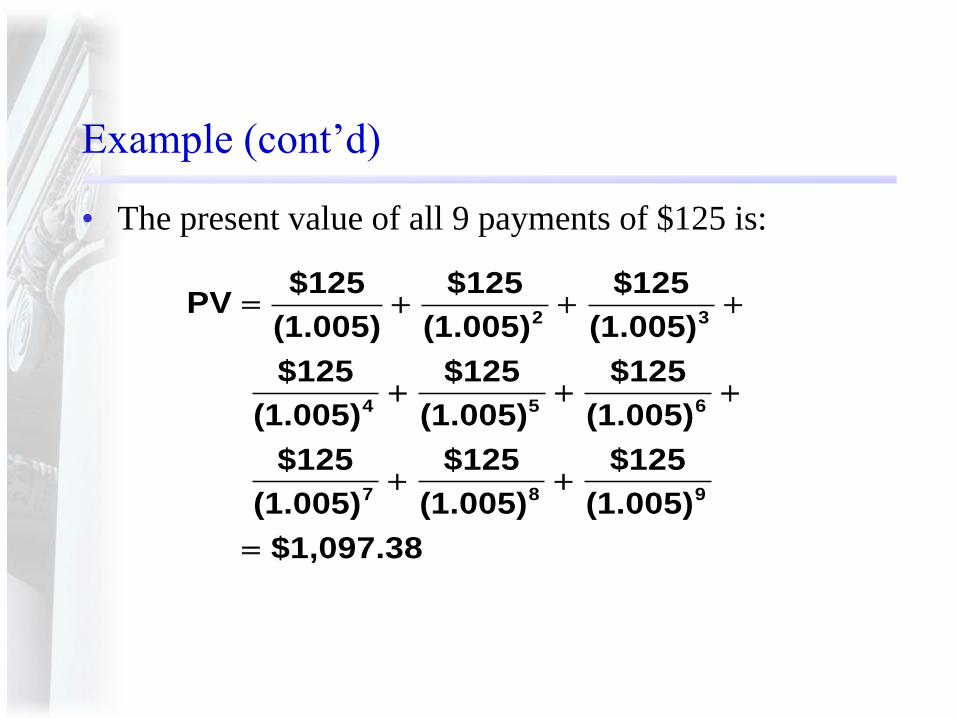

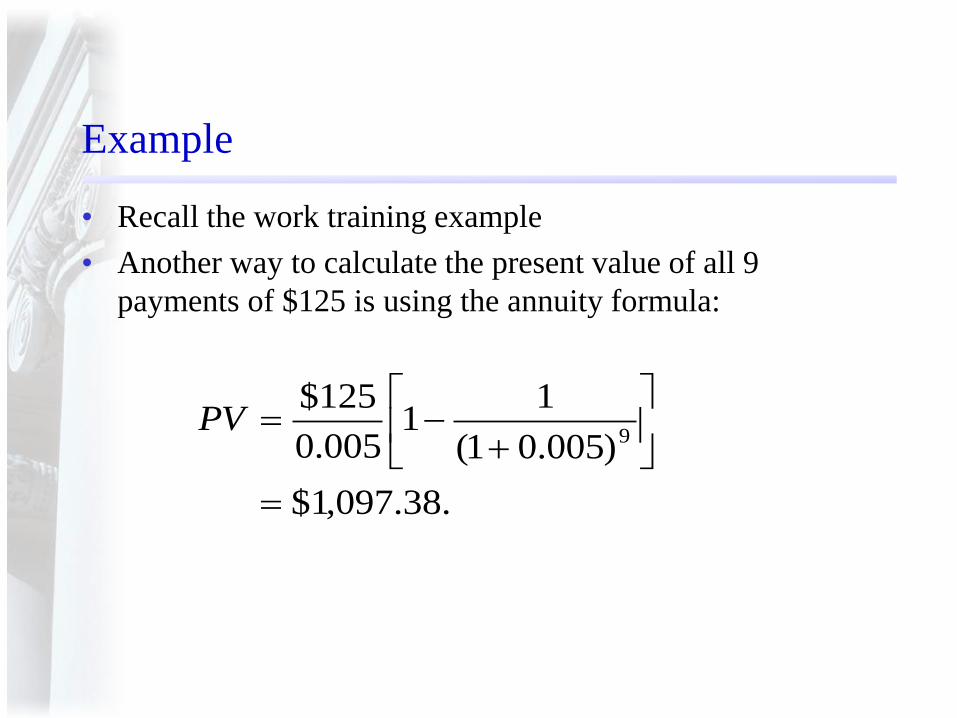

Example: Work Training

• Suppose you work 3 nights a week in a bar

• Plan to continue for the next 9 months

• They offer to train you to tend bar and pay you an extra

$125 a month after you are trained

• Suppose further, r=0.5% per month

• What is the present value of the training to you?

Example (cont’d)

• The present value of all 9 payments of $125 is:

PV$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$125

(1.005)

$1,097.38

2 3

4 5 6

7 8 9

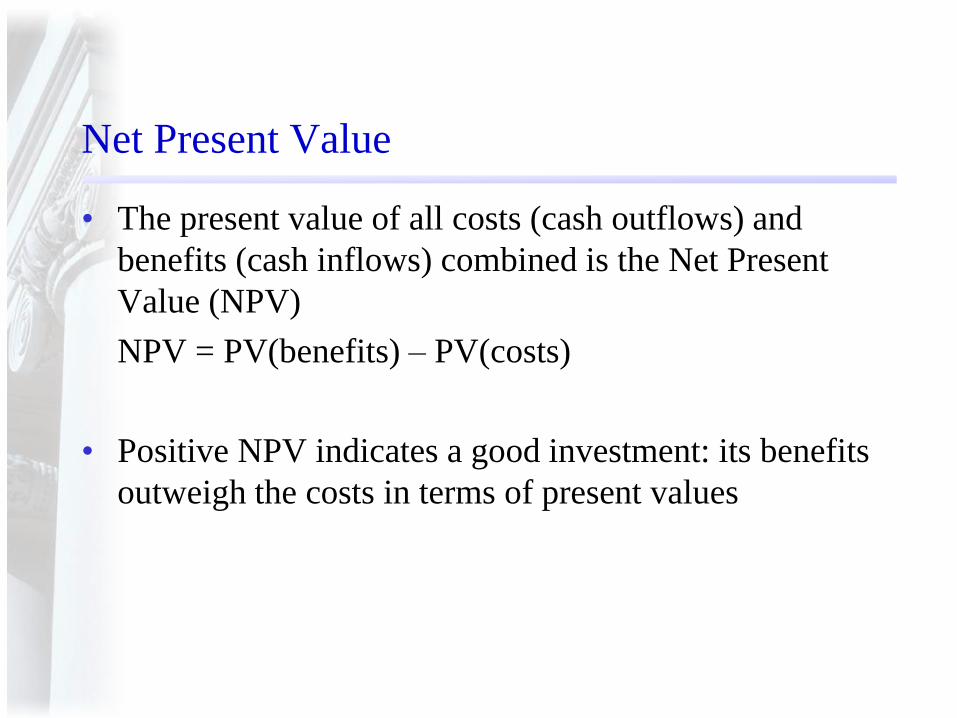

Net Present Value

• The present value of all costs (cash outflows) and

benefits (cash inflows) combined is the Net Present

Value (NPV)

NPV = PV(benefits) – PV(costs)

• Positive NPV indicates a good investment: its benefits

outweigh the costs in terms of present values

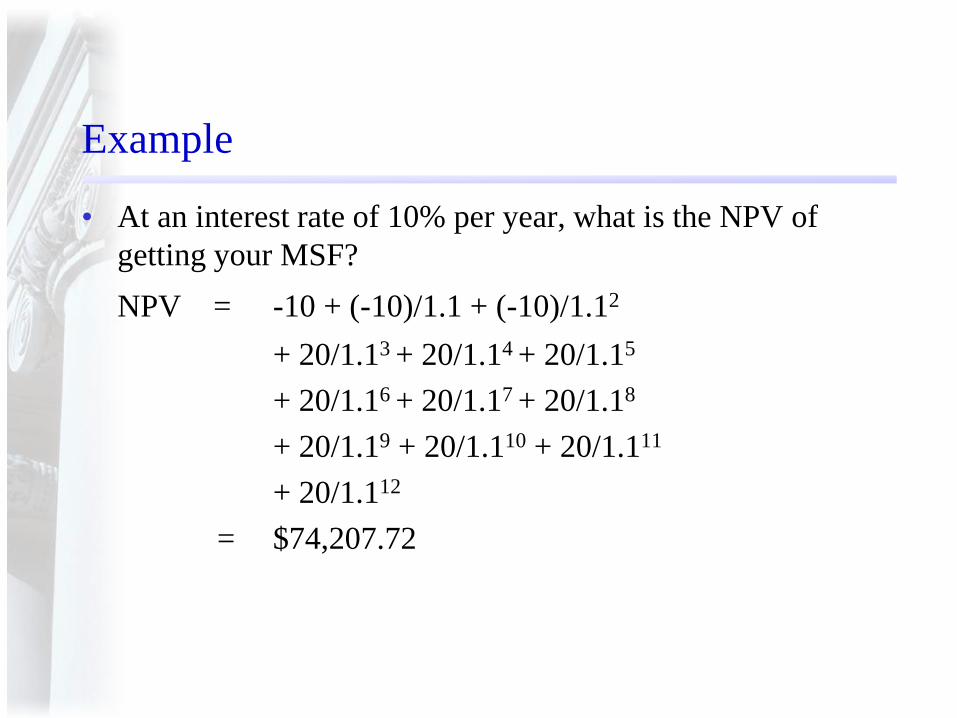

Example

• At an interest rate of 10% per year, what is the NPV of

getting your MSF?

NPV = -10 + (-10)/1.1 + (-10)/1.12

+ 20/1.13 + 20/1.14 + 20/1.15

+ 20/1.16 + 20/1.17 + 20/1.18

+ 20/1.19 + 20/1.110 + 20/1.111

+ 20/1.112

= $74,207.72

Special Cash Flow Patterns

• Perpetuity

• Annuity

• Growing Perpetuity

• Growing Annuity

Perpetuity

• A perpetuity is a constant payment of $C every period

forever

0 1 2 3 4 … t …

| | | | | |

C C C C … C …

• The present value of a perpetuity is:

r

C

tr

C

r

C

r

C

r

CPV

...)1(

...3)1(2)1()1(

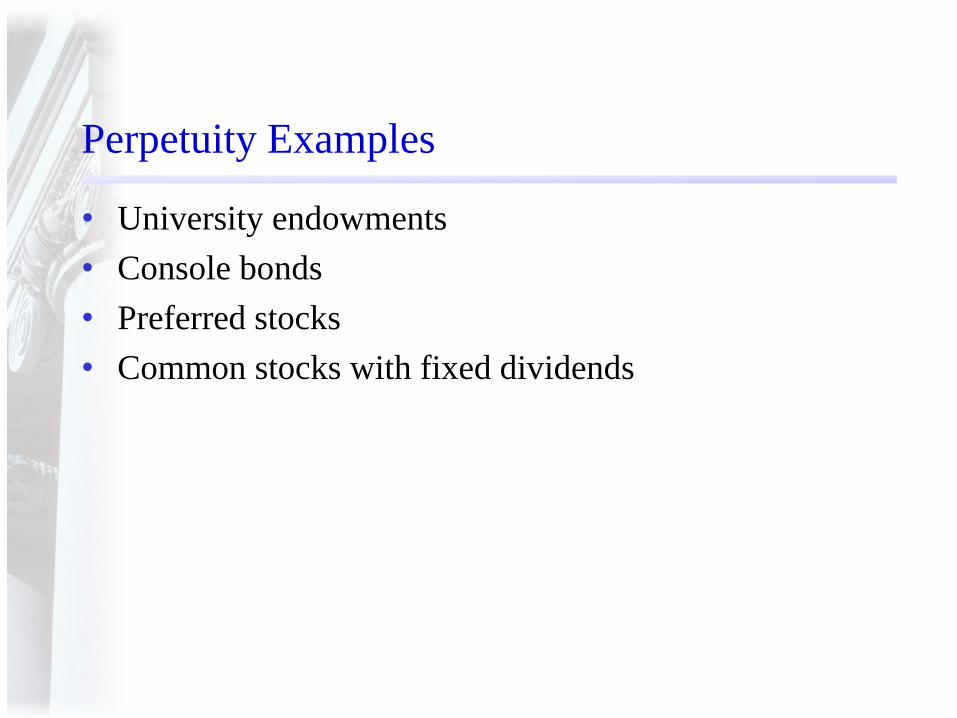

Perpetuity Examples

• University endowments

• Console bonds

• Preferred stocks

• Common stocks with fixed dividends

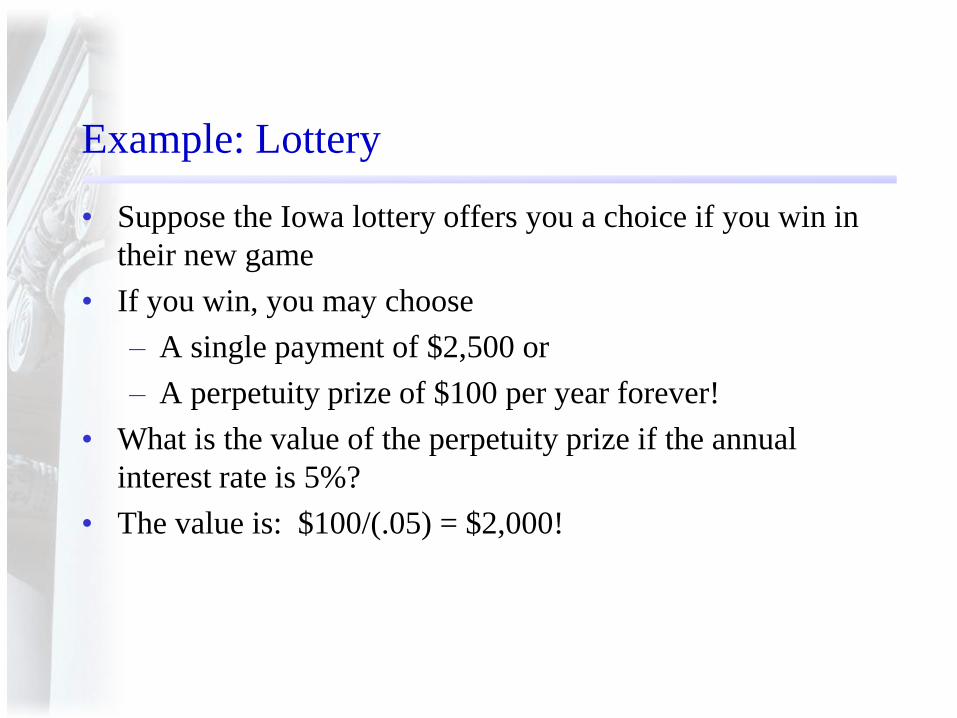

Example: Lottery

• Suppose the Iowa lottery offers you a choice if you win in

their new game

• If you win, you may choose

– A single payment of $2,500 or

– A perpetuity prize of $100 per year forever!

• What is the value of the perpetuity prize if the annual

interest rate is 5%?

• The value is: $100/(.05) = $2,000!

Annuity

• An annuity is a constant payment C every period until

date t

0 1 2 3 … t-1 t t+1 …

| | | | | | |

C C C … C C 0 …

• The present value of an annuity running from now

until date t is:

ttrr

PVIFArr

CPV

1

11

1

1

11

Annuity Examples

• Lotteries

• Bonds

• Payroll saving plans

• Loans and installment plans

Example

• Recall the work training example

• Another way to calculate the present value of all 9

payments of $125 is using the annuity formula:

.38.097,1$

)005.01(

11

005.0

125$9

PV

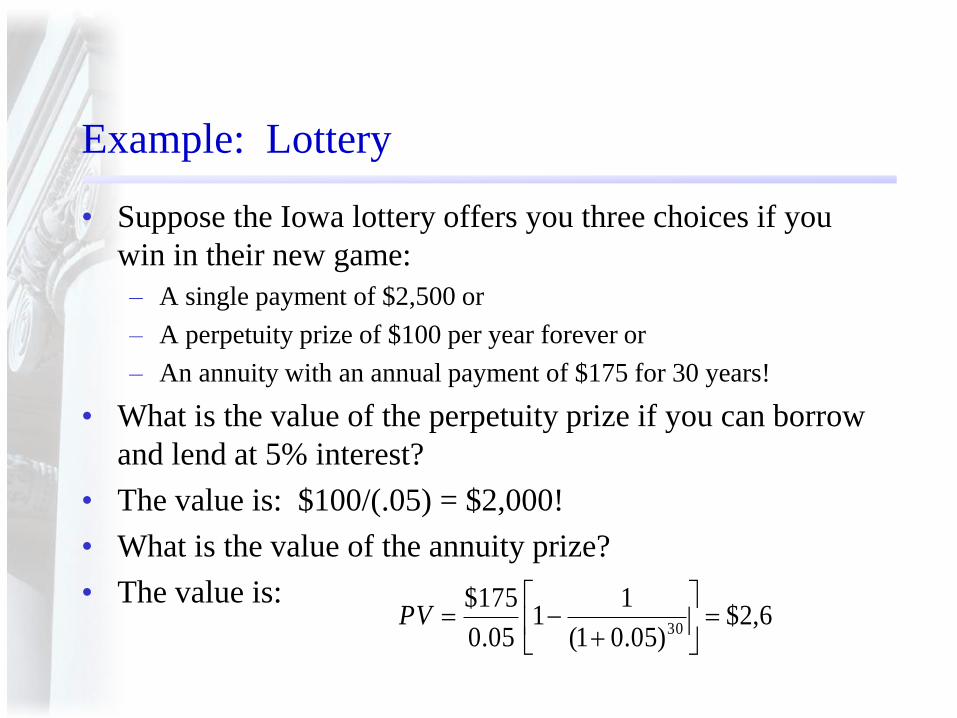

Example: Lottery

• Suppose the Iowa lottery offers you three choices if you

win in their new game:

– A single payment of $2,500 or

– A perpetuity prize of $100 per year forever or

– An annuity with an annual payment of $175 for 30 years!

• What is the value of the perpetuity prize if you can borrow

and lend at 5% interest?

• The value is: $100/(.05) = $2,000!

• What is the value of the annuity prize?

• The value is: .18.690,2$

)05.01(

11

05.0

175$30

PV

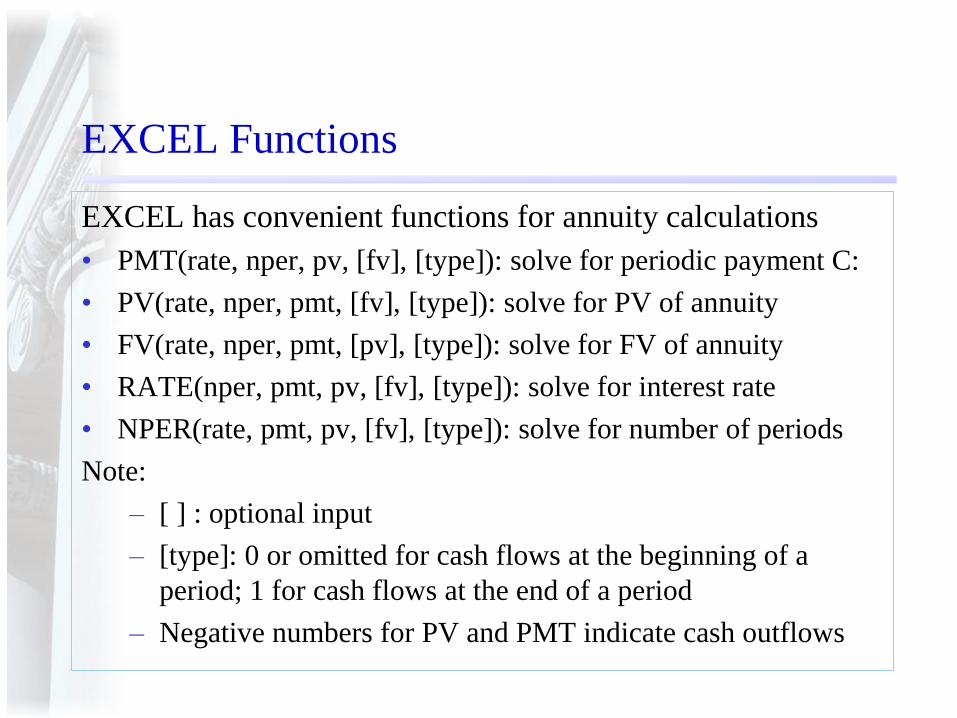

EXCEL Functions

EXCEL has convenient functions for annuity calculations

• PMT(rate, nper, pv, [fv], [type]): solve for periodic payment C:

• PV(rate, nper, pmt, [fv], [type]): solve for PV of annuity

• FV(rate, nper, pmt, [pv], [type]): solve for FV of annuity

• RATE(nper, pmt, pv, [fv], [type]): solve for interest rate

• NPER(rate, pmt, pv, [fv], [type]): solve for number of periods

Note:

– [ ] : optional input

– [type]: 0 or omitted for cash flows at the beginning of a

period; 1 for cash flows at the end of a period

– Negative numbers for PV and PMT indicate cash outflows

Growing Perpetuity

• The payment on a growing perpetuity grows at the

rate g:

0 1 2 3 4 … t …

| | | | | |

C C(1+g) C(1+g)2 C(1+g)3 … C(1+g)t-1…

• The present value of a growth perpetuity is:

gr

C

tr

tgC

r

gC

r

gC

r

CPV

...)1(

1)1(...

3)1(

2)1(

2)1(

)1(

)1(

Example

• A benefactor proposes to endow a chair

at the School of Management at the

University at Buffalo

• The proposal is to provide $150,000

initially plus a raise of 5% each year

• Suppose the interest rate earned by

endowments is 10%. How much should

the benefactor donate?

• Answer: A lot!

PV = 150,000/(10%-5%) = $3,000,000

Growing Annuity

• The present value of a growing annuity with the initial

cash flow c, growth rate g, and interest rate r is

defined as:

1 1 1

( ) (1 )

N

gPV C

r g r

Example

• Recall the endowment example. If the endowment plans to

last for only 10 years. How much should the benefactor

donate?

PV = 150,000/(10%-5%)*[1- (1.05/1.1)10]

= $1,115,972