42

Deciphering Financial Statements Tips & Tricks for Attorneys Jeff Roberts, CPA, CFE, CFF Senior Managing Consultant Forensics & Valuation Services [email protected] November 7, 2012

Deciphering Financial Statements Tips & Tricks for Attorneys

Jeff Roberts, CPA, CFE, CFF

Senior Managing Consultant

Forensics & Valuation Services

November 7, 2012

Goals for Webinar

• Overview of financial statements

• Meaning behind the numbers

• Understanding the information you request/receive

• How financial statements can be manipulated

2

Breaking Down Accounting Myths

• Myth 1: Accounting is precise

• Myth 2: Accounting has rules, eliminating judgment

• Myth 3: “Audited” means all errors found

• Myth 4: Accounting terminology has universal meaning, e.g., revenue, expenses, assets

3

Financial Statements

• Balance sheet

• Income statement

• Statement of cash flows

4

Balance Sheet

A snapshot of what a company owns (assets) & what it owes (liabilities) as of a specific date. The difference is the equity or net worth of the company.

Key points

• Find how much cash, receivables, inventory & debt

• Not necessarily current market values

• Assess financial health of the company

• Focus on the quality of the assets

• Not forward looking

5

Groupon’s Balance Sheet

Intangible

6

Groupon’s Balance Sheet

Difference between current assets & current

liabilities is working capital

Income Statement (Profit & Loss)

Shows a company’s income & expenses over a period of time – most typically a month, quarter or year.

Key points

• Different methods – cash, accrual, income tax basis

• Revenues on income statement ≠ cash in the door

• Historical – not forward looking

8

Groupon’s Income Statement

9

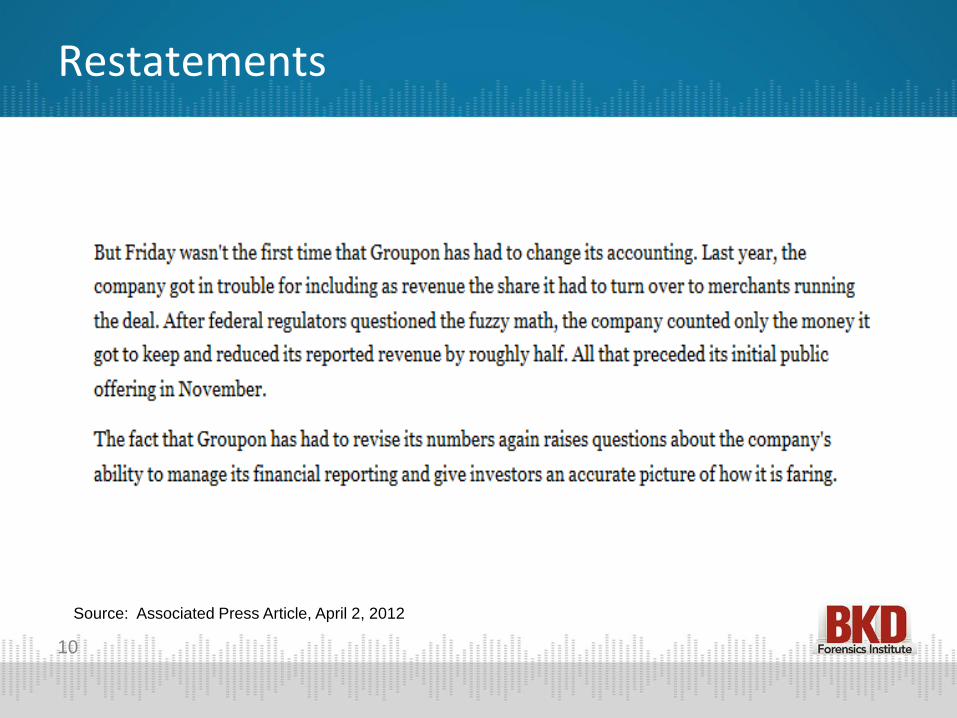

Restatements

Source: Associated Press Article, April 2, 2012

10

Cash Flow Statement

Shows a company’s sources & uses of cash during a period of time.

Key points

• How is company generating cash?

• Somewhat harder to manipulate

• Does the company have net income, but fail to generate cash? Could be a red flag.

11

Groupon’s Cash Flows

12

Groupon’s Cash Flows

13

Groupon’s Cash Flows

14

Groupon - Cash Flow Summary

Three Months Ended March 31

2012 2011

Operating activities $83,714 $17,940

Investing activities (46,444) (44,294)

Financing activities ( 8,275) 112,106

15

Visual Summary - Financial Statements

Balance Sheet

Financial condition at a point in time

Balance Sheet

Financial condition at a point in time

Beginning of Year January 1, 2012

End of Year December 31, 2012

Income Statement

Summary of activity for a period of time

Statement of Cash Flows

Summary of activity for a period

of time

Reporting of Business Activity

16

Accounting Lingo to Know

General Ledger: The system where all accounting transactions are recorded

Payroll records

Sales records

Bills Paid

17

It’s Accrual World

Cash Basis Accounting

Common with small businesses

Accounting entries based on money in & out

Downside: Timing issues, skewing results

Accrual Basis Accounting

Accounting based on the event – not money in/out

Better to assess true operating results

Required to conform with GAAP

Know which one – it can have a significant impact on the financial

statements you are reviewing.

18

Cash or Accrual? One Way to Find Out

Excerpt from tax return

19

The Rest of the Story: Notes to Financial Statements

• Explains accounting methodologies, assumptions

• Provides explanations for many line items

• Information you won’t find in financial statements

• Not in every set of financial statements

• For public companies read the “MD & A”

20

Notes to the Financial Statements: Devil is in the Details

21

Manipulation of Financial Statements

22

Financial Statement Fraud

“Fraudulent financial reporting need not be the result of a grand plan or conspiracy. It may be that management representatives rationalize the appropriateness of a material misstatement, for example, as an aggressive rather than indefensible interpretation of complex accounting rules...”

Statements on Auditing Standards #99

23

Top Methods of Manipulating Financials

• Fictitious/dubious revenues

• Omitting or delaying expenses

• Capitalizing expenses to increase or “smooth” profits

• Use of “cookie jars” & “cushions”

• Recording fictitious assets, e.g., inventory

24

Spotting Red Flags

Enron more than tripled its reported “revenues”

without a corresponding increase in earnings

25

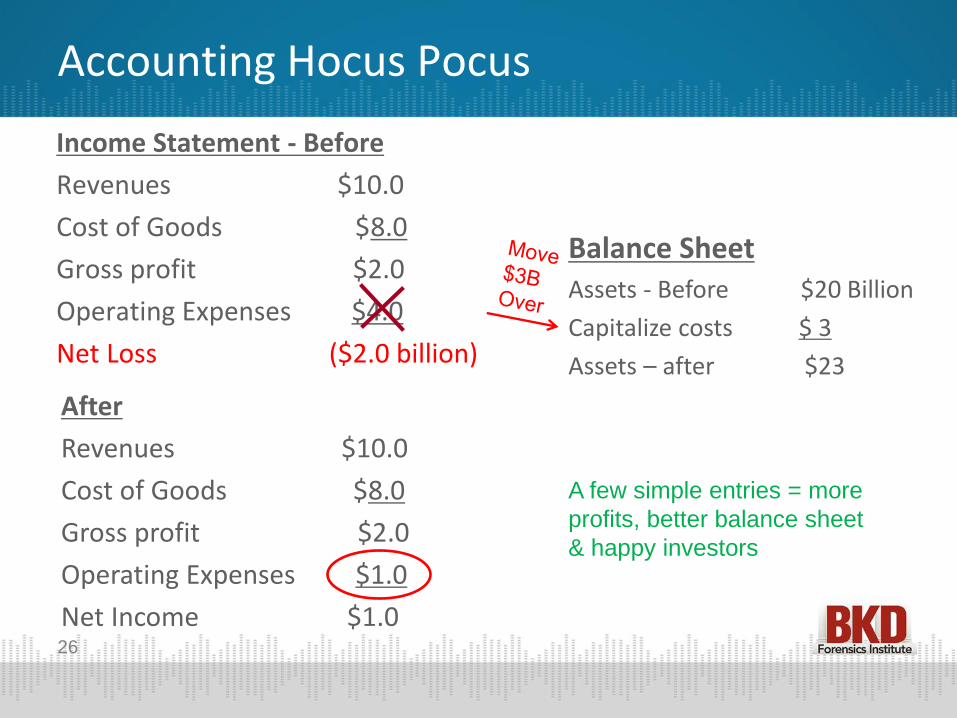

Accounting Hocus Pocus

Income Statement - Before

Revenues $10.0

Cost of Goods $8.0

Gross profit $2.0

Operating Expenses $4.0

Net Loss ($2.0 billion)

After

Revenues $10.0

Cost of Goods $8.0

Gross profit $2.0

Operating Expenses $1.0

Net Income $1.0

Balance Sheet Assets - Before $20 Billion

Capitalize costs $ 3

Assets – after $23

A few simple entries = more

profits, better balance sheet

& happy investors

26

Other Red Flags

• Auditor switching

• Dubious auditors (Madoff)

• Numerous & questionable mergers/acquisitions

• Unexplained assets on balance sheet

• Large related-party transactions

• Ratio of accounts receivable to sales growing

• Inventory growing despite meager sales

27

Reliability Considerations

28

Polling Question

• What would provide the greatest level of assurance in a set of financial statements?

A: Compilation

B: Tax Return

C: Audit

D: Review

E: Not sure

29

What is an Audit?

• “Audit” is often used very loosely

• Internal vs. external audits

• Operational audits (process & procedures)

• Financial statement audit is a specific level of service

• Much different than o Compilation

o Review

• CPAs have professional standards specific to each service

• Read the “Accountant’s Report” to find out

30

Levels of Assurance – From Highest to Lowest

• Audit – Must be independent; audits required for publicly traded companies, by some regulators & many banks

• Review – Must be independent; required annually by some banks as condition of a loan

• Compilation – Independence not required, but lack of independence must be disclosed; not necessarily more reliable than internal financials

• Internal financial reports – Just that; may or may not be reliable; it depends on the circumstances

• Tax returns

31

What an Audit Isn’t

• Does not mean they are completely free of errors

• Does not look at every transaction, contract, agreement, etc.

• Does not mean there has been no misappropriation

• Is not an opinion on management’s abilities

32

You’re Overruled

• Historically, U.S. accounting largely rules based

• International Financial Reporting Standards (IFRS) more principles based

• Complex world, but not a rule for every situation

• If GAAP is silent, it must mean we can!

• Companies magically create their own accounting

33

Sample Independent Auditor’s Report

To the Board of Directors and Shareholders ABC Company

We have audited the accompanying balance sheets of ABC Company as of December 31, 2010, 2009 and 2008 and the related statements of income, retained earnings and cash flows for the years then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of ABC Company as of December 31, 2010, 2009 and 2008 and the results of its operations and its cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America.

34

INDEPENDENT ACCOUNTANT'S REPORT Mary Beth Addams Small Potatoes, Inc. Carlisle, Pennsylvania We have compiled the accompanying statement of assets and stockholders' equity - income tax basis of Small Potatoes, Inc., as of December 31, 1999, and the related statements of revenue, expenses and retained earnings - income tax basis, and cash flows - income tax basis for the year then ended, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. A compilation is limited to presenting information that is the representation of management in the form of financial statements. We have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or any other form of assurance on them. Carlisle, Pennsylvania January 31, 2000

Sample Accountant’s Compilation Report

35

Requesting Financial Information

• Financial statements (internal & external prepared)

• Federal income tax returns

• Payroll records & W-2s

• Payroll tax returns

• Customer list

• Bank & investment statements

• General ledger in electronic format

• Check register

• Related-party transaction detail

• List of all affiliates, subsidiaries & related entities

36

Terminology Pitfalls

Revenues, Income, Sales, Net sales…

Net profit, net income, pretax income, EBITDA…

Expenses, nonoperating expenses, outflows…

37

Summary of Key Points

• View the financial statements & notes as a package

• Accounting is not a precise science

• Great degree of judgment required

• Accounting rules can be exploited

• No universal meaning with many accounting terms

38

Jeffrey Roberts | Senior Managing Consultant | 417.865.8701| [email protected]

BKD Forensics Institute Upcoming Schedule

• Data Visualization: Taking Your Analytics from Blah to Bam! o Wednesday, November 14, 2012

o 11:30 a.m. – 12:30 p.m. CST

o Presented by Jeremy Clopton, CPA, ACDA, CFE

bkd.com/fi

40

Starbucks Gift Card & Certificate

• To help promote the event as an associate training tool, we are offering a bonus

o Associates who attend all three sessions will receive a Starbucks gift card & Certificate of Participation from BKD

41

Slides & Webinar Archive

• Today’s presentation slides are available at bkd.com/fi. A recorded copy of the webinar will be available at the same location at the conclusion of webinar series

• If you have any questions, please contact Dane Ryals @ [email protected]

• Thank you for attending today

42