96

Titan Europe Plc Annual Report & Accounts 2009

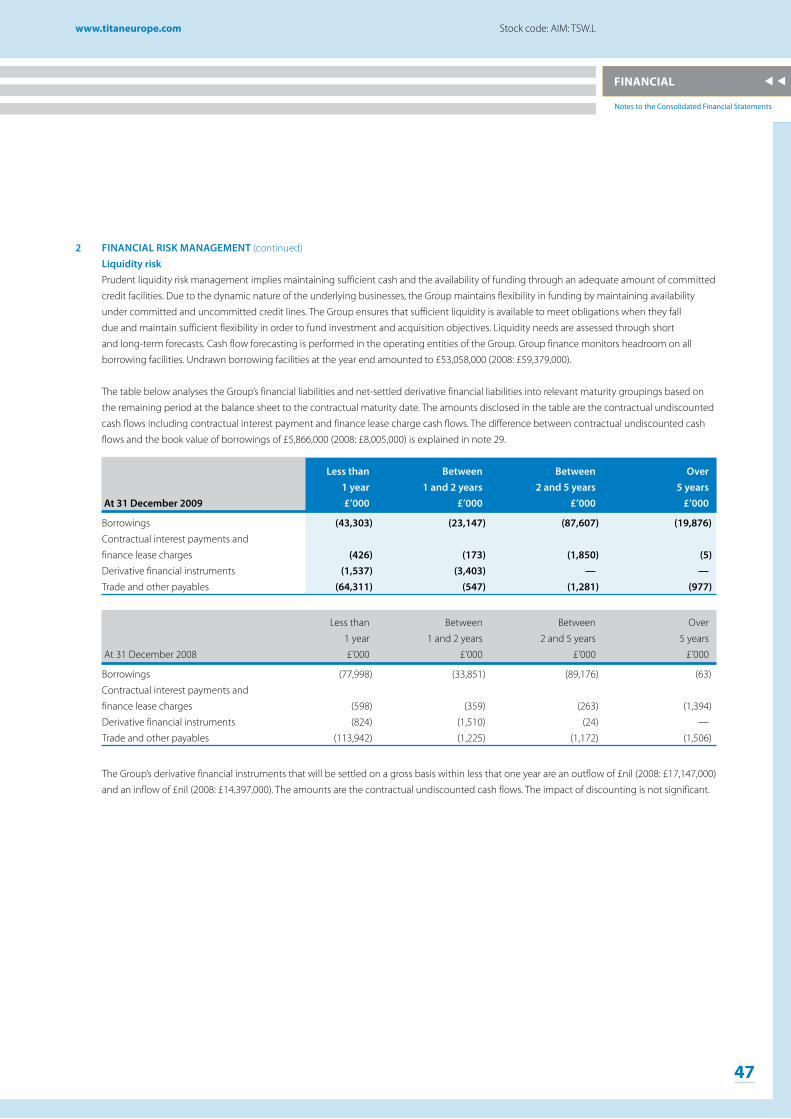

17643 25/05/10 Proof6 17643 25/05/10 Proof6

Titan Europe Plc Annual Report &

Accounts 2009

Titan Europe PlcAnnual Report & Accounts 2009

Titan Europe PlcTitan Europe HeadquartersBridge Road, CookleyKidderminster, WorcestershireDY10 3SDUnited Kingdom

Tel: +44 (0)1562 850561Fax: +44 (0)1562 852554

Registered in England No. 3018340

17643 25/05/10 Proof 6 17643 25/05/10 Proof 6

Titan Europe Plc Annual Report & Accounts 2009

WHO WE ARE

OUR BUSINESS

01 Summary of Financial Results02 Global Reach — Local Presence04 10 Reasons to do business with Titan Europe06 Wheels10 Undercarriage

PERFORMANCE

14 Chief Executive’s Report

GOVERNANCE

20 Directors & Advisers22 Directors’ Report30 Corporate Governance Statement31 Independent Auditors’ Report

FINANCIAL

32 Consolidated Income Statement33 Consolidated Statement of Comprehensive Income34 Consolidated Balance Sheet35 Consolidated Statement of Changes in Equity36 Consolidated Cash Flow Statement37 Reconciliation of Cash Flow to Net Debt38 Notes to the Consolidated Financial Statements81 Independent Auditors’ Report82 Company Balance Sheet83 Movements in Shareholders’ Funds84 Notes to the Company Financial Statements

TITAN EUROPE Plc

à A world leading engineering group designing, developing, manufacturing and distributing products and services for the global construction, agricultural and mining machinery markets

à Recognised as a technical innovator and leading provider of integrated solutions. Focused on its markets and customers, Titan Europe delivers products to global OEM customers and their associated aftermarkets

à Titan Europe's objective is to excel at supporting customers through local production and distribution locations, a strategy which helps to differentiate the business from many of its competitors

à Titan Europe currently has two distinct product ranges, organised into two divisions, Wheels and Undercarriage

17643TITANEU cvr(spine).indd 217643TITANEU cvr(spine).indd 2 25/05/2010 10:1525/05/2010 10:15

17643 25/05/10 Proof6

Summary of Financial Results

www.titaneurope.com Stock code: AIM: TSW.L

01

our business

www.titaneurope.com Stock code: AIM: TSW.L

our business

01

summary of financial results

Wheels divisionThe Wheels division is a leading global designer, manufacturer and distributor of technically advanced wheels and brakes. In addition, Continental/General and Titan tyres are distributed from its centre in the UK.

The 1,100 staff support global customers from eleven locations worldwide.

undercarriage divisionThe Undercarriage division (“Titan ITM”) is a multinational specialist designer, manufacturer and distributor of undercarriage frames and components to OEMs and customers operating in the aftermarket worldwide.

1,200 people are employed across nine locations across the world.

Year ended Year ended

31 December 31 December

2009 2008

£’000 £’000

Revenue 258,570 452,313

Trading (loss)/profit (18,130) 31,164

Restructuring and rationalisation costs (14,682) (3,944)

Significant legal costs (651) —

Movement on fair value of forward foreign exchange contracts — (4,110)

(Loss)/profit from operations (33,463) 23,110

Net financing costs (9,361) (12,461)

Share of profit/(loss) of associate and joint venture 1,383 (1,014)

(Loss)/profit before income tax (41,441) 9,635

Income tax credit/(expense) 7,050 (4,144)

(Loss)/profit for the year (34,391) 5,491

Net debt (148,030) (158,165)

Cash generated from operations 11,834 34,819

www.titaneurope.com Stock code: AIM: TSW.L

02

titan europe Plc Annual Report & Accounts 2009

17643 25/05/10 Proof6

GLobaL ReaCh — LoCaL pReseNCe

Titan Europe has developed long-term relationships with OEM customers across the world over many years

americas euroPe

TiTaN’s MaRKeT

Titan continues to respond to the changing pattern of its customers’ needs, by further developing its global manufacturing footprint from its traditional European focus.

The new undercarriage factory in China is expected to be in full production during the third quarter of 2010 and a second phase of further expansion to support demand from customers is now being planned. Titan already supplies Western manufacturers based in China with undercarriage assemblies. This demand is stronger than expected.

Titan is well positioned to take advantage of growth in the South American markets with the existing Brazilian undercarriage facility and the mining wheels businesses in Chile and Peru. Titan has further projects that will assist the expansion of Titan’s mining market penetration in the Americas and Australasia for both wheel and undercarriage products. Titan has further opportunities in the significant growth markets of India and Russia.

www.titaneurope.com Stock code: AIM: TSW.L

03

our business

17643 25/05/10 Proof6

Global Reach — Local Presence

● Wheels ● Undercarriage

Pacific basin

“Titan continues to respond to the changing pattern of its customers’ needs, by further developing its global manufacturing footprint from its traditional European focus.”

17643 25/05/10 Proof6

04

titan europe Plc Annual Report & Accounts 2009

technical innovationTitan Europe invests in R&D to innovate products and processes to uniquely add value to the customers it serves.

1✔

responsivenessThrough investment and working closely with customers, Titan Europe ensures that customers’ requirements are met within controlled lead times.

3✔

cost-effective solutionsBy engineering excellence, products are optimised for their applications. Investments in low labour cost locations have delivered significant benefits.

5✔

QualityFrom international standards such as ISO to tightly controlled processes, Titan Europe delivers excellence in quality in its products and services.

2✔

technical supportFrom the central engineering resources, through the local technical support, Titan Europe ensures technical queries are dealt with promptly at the customers’ locations anywhere in the world.

4✔

ReasoNs To Do busiNess wiTh TiTaN euRope

www.titaneurope.com Stock code: AIM: TSW.L

05

our business

17643 25/05/10 Proof6

www.titaneurope.com Stock code: AIM: TSW.L

05

our business

10 Reasons to do business with Titan Europe

Global reach — local presenceTitan locates its plants close to its customers to ensure rapid response times and a well-managed supply chain which is flexible.

7✔

DiversificationTitan Europe has a unique position with facilities to support mining locally, with undercarriage, wheel and tyre needs through its service centres.

9✔

customer serviceTitan Europe sells products but more importantly a complete service to its customers, through ongoing support and technical assistance.

6✔

excellence in manufacturingWith a focus on lean manufacturing and an experienced management team, Titan Europe has highly efficient manufacturing plants across the world.

8✔

off-highway core focusTitan Europe is completely focused on its markets and its customers in the off-highway businesses.

10✔

17643 25/05/10 Proof6

06

titan europe Plc Annual Report & Accounts 2009

wheeLstitan europe is a specialist designer, manufacturer and service provider of wheels for all kinds of off-highway vehicles serving the agricultural, construction, material handling and mining industries.

44%

wheels divisionGroup revenue

wheels market split by region

Europe 69%

North America 6%

UK 3%

ROW 20%

South America 2%

06

www.titaneurope.com Stock code: AIM: TSW.L

07

our business

17643 25/05/10 Proof6

Wheels

www.titaneurope.com Stock code: AIM: TSW.L

07

our business

“Titan Europe has invested heavily to support agricultural machinery manufacturers and to increase flexibility in its plants.”

MaNufaCTuRiNG

Titan Europe has wheel manufacturing facilities across Central and Southern Europe, South America and Australasia. These facilities are ideally located to provide the support to a global Original Equipment Manufacturer (OEM) customer base.

earthmover wheels

Titan Europe has the largest specialist earthmover wheel plant in the world, located in the UK. This award-winning operation supplies a global customer base, utilising design and manufacturing excellence to provide a highly competitive package for customers wherever they are located.

Not only has this plant been awarded the Queen’s Award for Industry three times, in 2009 it was awarded the Caterpillar ‘Gold Level’ supplier standard. These awards acknowledge Titan Europe’s dedication to quality of product, service and continuous improvement.

Regular investment has been made into modern welding, rolling and machining technology, along with the application of up-to-date lean manufacturing techniques. This, combined with a range of innovative new products, has ensured Titan Europe is well placed to support future customers’ needs and new model programmes.

agriculture wheels

Titan Europe has invested heavily to support agricultural machinery manufacturers and to increase flexibility in its plants. Further investment has been made into product innovation, developing a range of larger and faster running wheels to reflect the growth in machine size across Europe.

Titan Europe is the only manufacturer of the very largest high speed wheels and has also continued its specialisation in the ultra thin wheels in its flexible French manufacturing facility.

At the less innovative and more cost conscious end of the market, Titan Europe has leveraged its Turkish joint venture to produce a highly competitive range of smaller wheels.

Tyres

Titan Europe has formed key logistics operations for its suppliers by supplying ‘just in time’ (‘JIT’) tyre and wheel assemblies. This operation has been expanded through Titan Europe’s Gevelsberg facility in Germany, resulting in closer ties with customers.

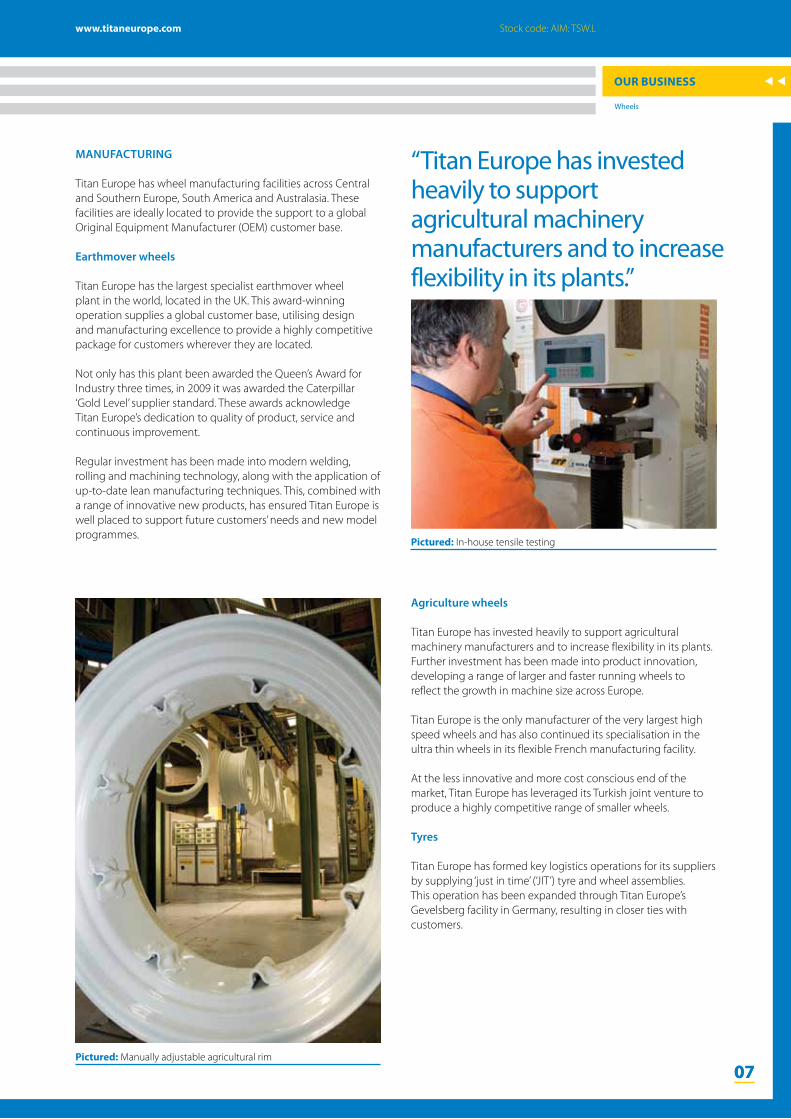

Pictured: In-house tensile testing

07Pictured: Manually adjustable agricultural rim

17643 25/05/10 Proof6

08

titan europe Plc Annual Report & Accounts 2009

wheeLs continued

Pictured: Special dockside wheel

08

pRoCess iNNovaTioN

Titan Europe’s focus on process improvement has accelerated during 2009.

Through the application of lean manufacturing tools, such as quick change over and six sigma, areas of the business have shown significant improvement with reduced inventory levels, greater flexibility and reduced costs.

QuaLiTY

Titan Europe delivers excellence in quality: product quality comes as standard throughout all of Titan Europe’s wheel products and operations. This is evident from construction and crane wheels with high toleranced roundness and concentricity levels, to a focus on welding processes. All operations are accredited to ISO 9001 with the UK also having achieved ISO 14001 for excellence in environmental performance.

Titan locations have use of, or facilities for, testing and development, including the ability to test the largest diameter wheels in Europe. This ensures that product is engineered for the most demanding applications of today and the future.

RespoNsiveNess

Due to the focus on flexibility in all of its plants, Titan Europe is in a position to service customers for both high and low volume production. A programme of dedicated mining service centres located close to the mines is working well in Australia; this programme will be expanded both in this locality and to other mining areas.

Case sTuDY:

ouTsiDe veRTiCaL MouNT (ovM) The OVM wheel was developed by Titan Wheels Australia to reduce the downtime caused by tyre maintenance on large earthmoving and mining vehicles out in the field. Since the introduction of the OVM wheel, mine sites have measured and recorded 50% to 60% savings in downtime, maintenance costs and commensurate increased safety margins.

As well as revenue generated in Australia, in 2009 we also began supplying these wheels to the largest iron ore producer in Canada.

Features and benefits:

Vehicles can have the outside tyres vertically mounted in the same manner as the front tyres and not have the wheel fixing nuts re-tensioned.

●● The inside tyre can be removed over the outside wheel, eliminating the need to remove the outside wheel.

●● Wheels can stay on one truck for the duration of their scheduled testing period, making it easier to track accumulated hours.

●● Tyre life is improved, as it is easier to rotate tyres suffering uneven wear.

●● Incidents of wheel damage due to wheel nuts not being tensioned correctly are reduced.

●● Minimal levels of stocks are required.

●● The need for servicemen to use impact guns is limited.

www.titaneurope.com Stock code: AIM: TSW.L

09

our business

17643 25/05/10 Proof6

Wheels

www.titaneurope.com Stock code: AIM: TSW.L

09

our business

09

“Titan Europe delivers excellence in quality: product quality comes as standard throughout all of Titan Europe’s wheels products and operations.”

17643 25/05/10 Proof6

10

titan europe Plc Annual Report & Accounts 2009

uNDeRCaRRiaGetitan europe’s undercarriage division (‘titan itm’) designs, manufactures and supplies undercarriage components and complete undercarriage assemblies to the global market for construction, agricultural and mining equipment. a key titan itm objective is to provide solutions to customers’ needs and to create value through technology and innovation in products, processes and services. titan itm is a preferred supplier to many global oem manufacturers and aftermarket customers.

56%

undercarriage divisionGroup revenue

undercarriage market split by region

Europe 50%

ROW 19%

North America 12%

South America 16%

UK 3%

10

www.titaneurope.com Stock code: AIM: TSW.L

11

our business

17643 25/05/10 Proof6

Undercarriage

www.titaneurope.com Stock code: AIM: TSW.L

11

our business

11

MaNufaCTuRiNG

The new Stock OptimizatiON (SOON) manufacturing planning system was fully implemented in all Titan ITM facilities during 2009. This project has resulted in a reduction in stock of £26.4m since the start date of April 2008. The system has additional benefits of a reduction in lead times to customers and improved manufacturing flexibility.

Lean manufacturing in the Italian Titan ITM plants has also contributed to reduced set up times and the elimination of non-added-value operations, improving overall flexibility. A complete review of the Potenza plant layout and the consolidation of the other Italian plants completed in 2008 will create a very strong base from which to serve our European customers and benefit from future growth opportunities.

In February 2009, Titan ITM obtained the business licence for a new Chinese manufacturing plant, Titan ITM Tianjin Ltd. This new subsidiary has already started assembling frames for our key European customers in China. The plant will be completed in June 2010, improving both profitability and flexibility from the second half of 2010 within Titan ITM.

Demand levels from our target customers in China have been stronger than originally expected.

“Titan ITM is continually adapting products and processes to improve performance.”

pRoDuCT iNNovaTioN

Titan ITM is continually adapting products and processes to improve performance. Investment has been made in the design and development of a new generation of complete machines for key OEMs.

New products have also progressed with an extended life for extreme working conditions. Examples of completed projects include the new generation 140 ton mining excavators, the 60 ton telecrane undercarriage and the new generation of road mills and paver machines. 2009 also saw the development of new rollers, chains and shoes for heavy duty and mining applications. Large mining applications were enhanced with the introduction of a new range of D11 undercarriage components to support the range of Titan ITM products worldwide. The success of these projects has increased Titan ITM market share with existing and new customers, significantly adding to Titan ITM’s profile, giving the division the opportunity to differentiate from competition. Titan ITM will further benefit as its market recovers.

These developments are co-ordinated through Titan ITM’s global engineering headquarters in Germany. As reported in 2008, significant investment has also been made in additional testing capacity. Titan ITM testing is now operating in Italy alongside other Group testing facilities. The combination of German and Italian engineering teams gives Titan ITM the potential capability to support future undercarriage developments and customers’ new model programmes.

Pictured: Material handling using robot in a forging plant

Pictured: 3-Axis CLM interface for forging tools

17643 25/05/10 Proof6

12

titan europe Plc Annual Report & Accounts 2009

uNDeRCaRRiaGe continued

12

In 2009, Titan ITM further recognised the need for aftersales customer support by assigning a senior engineer to head up this function. His team’s role is primarily focused on ensuring an effective aftersales service to the customers, at the same time gathering key indicators from the field to maintain continuous and direct improvements in product performance.

QuaLiTY

Titan ITM maintains a global reputation for high quality products designed and manufactured worldwide, using a combination of local experience and support from our central engineering functions. The ITM quality standards are the same for customers worldwide, independent of the location of manufacture.

RespoNsiveNess

Titan ITM manufactures a full range of undercarriage components and, uniquely, the complete undercarriage frame assembly; this provides a clear differentiation in the market. With customers demanding more and more ‘full service support’, Titan ITM is in a position to deliver this. For the aftermarket, successful flexible sales and marketing techniques previously used in Europe have been transferred to South America. This has supported and driven growth despite difficult general market conditions.

GLobaL pReseNCe aND CosT-effeCTiveNess

The financial crisis and dramatic downturn of the markets in which Titan ITM operates have accelerated the process of delocalisation of the main Western OEMs with relocation, mainly to the Far East. This relocation is aimed at serving the local growth in demand as well as to address continuous pressure on price for some products. Recognising the OEM demands for cost improvement and local sourcing, Titan ITM is positioned to address its customers’ globalisation strategy.

Titan ITM’s manufacturing platform is well balanced to serve global customers worldwide. This will be further enhanced with the new plant in China, unique in manufacturing lower cost undercarriage products to service Western OEM customers who have transferred production to China. In addition to this, the efficient and modern plant in Brazil services the South and North American markets. Global customers will benefit from products supplied with the traditional high levels of Titan ITM quality at lower costs.

European plants continue to service local OEMs effectively and also retain the manufacture of special products for mining and heavy duty applications. The technical knowledge and developments from local Titan ITM experts are always supported by the central Titan ITM engineering resources.

Pictured: Track group assembly with Z bar shoes

Pictured: Single flange roller with shaft

www.titaneurope.com Stock code: AIM: TSW.L

13

our business

17643 25/05/10 Proof6

Undercarriage

www.titaneurope.com Stock code: AIM: TSW.L

13

our business

13

Case sTuDY:

italtractor Landroni LTDa received the ‘partner-level’ supplier award from John DeereIn January 2009, Italtractor Landroni LTDA received the highest classification award possible for a supplier to John Deere do Brazil. This ‘Partner-level’ Supplier Award formally recognises Titan’s dedicated service and support on behalf of its customers. Only six suppliers from almost 400 global suppliers received this award which was accredited through the ‘Achieving Excellence’ programme.

‘Achieving Excellence’ is a strategy for world class supplier relationships that evaluates the performance of the supplier in terms of ‘Quality’, ‘Delivery’, ‘Technical Support’, ‘Wavelength’ and ‘Cost Management’.

17643 25/05/10 Proof6

14

titan europe Plc Annual Report & Accounts 2009

Chief exeCuTive’s RepoRT

14

“Titan continues to have a strong presence with key OEMs with long-term relationships and with a 100% top customer retention.”

miKe aKers Chief Executive

www.titaneurope.com Stock code: AIM: TSW.L

15

our business

17643 25/05/10 Proof6

Chief Executive’s Report

www.titaneurope.com Stock code: AIM: TSW.L

15

Performance

iNTRoDuCTioN

The Group continues to be the only specialist manufacturer of tracked and wheeled movement systems to the construction, agricultural and mining industries.

The impact of the recession on these industries has been reported so widely that it needs no further embellishment here. It can however be reported that Q3/Q4 2009 were, as predicted, the worst trading periods for the business with the ‘bottom’ occurring somewhere in Q3.

It has been evident that within the industries that Titan supplies, 2009 end-user sales have been significantly higher than equipment manufacturers’ build rates. This destocking effect has had a significantly geared impact on revenue. As a consequence, without end market increases, volumes of manufacture for Titan’s market segments will rise in 2010.

For Titan the main impact of the recession has fallen in Europe and North America, whilst the Australian and South American businesses fared relatively well. Equally, key areas for restructuring of Titan’s manufacturing resources have been in the ‘traditional’ manufacturing base of Western Europe, particularly Italy. The programme of locating production into new growth areas is expected to continue and subsequently, this will have a permanent impact on some of Titan’s more traditional manufacturing supply routes.

The programme of reducing fixed costs has continued, in terms of physical assets and, unavoidably, personnel. During the year average employee numbers reduced by 20% to 2,336 (2008: 2,920); in addition to this reduction, various government schemes around the world have allowed a temporary reduction in employees which accounted for a reduction of a further 486 people (21%). Furthermore, as part of this programme, there have been substantial changes in manufacturing methods which have resulted in greater flexibility, faster changeover times and lower inventory costs.

Titan continues to have a strong presence with key OEMs with long-term relationships and with a 100% top customer retention.

ResuLTs

The Group produced revenue of £258.6m (2008: £452.3m). This was a decrease of 42.8% over 2008, and was affected by the move in exchange rates, the impact of which is clearly set out in the Directors’ Report on page 23.

The Wheels division recorded revenue (including share of joint venture) at £118.0m (2008: £197.2m), down 40.2% on 2008 levels, and produced a trading loss (excluding share of joint venture) of £4.2m (2008: £22.6m profit).

The Undercarriage division accounted for revenue of £143.5m (2008: £259.5m), down 44.7% on 2008 levels, and recorded a trading loss of £13.9m (2008: £8.6m profit).

The reduction in revenue in the Undercarriage division was higher than the Wheels division due to the higher exposure of the Undercarriage division to the construction market which was more severely impacted by the recession.

Overall, the Group trading loss was £18.1m (2008: £31.2m profit). The impact of significant one-off items (largely relating to restructuring and in 2008, movements in fair value of exchange contracts) left operating loss at £33.5m (2008: £23.1m profit), pre-tax loss at £41.4m (2008: £9.6m profit) and the post-tax loss for the year ended December 2009 at £34.4m (2008: £5.5m profit).

Case sTuDY:

CaTeRpiLLaR As part of Caterpillar’s supplier quality excellence process

certification, Titan Steel Wheels Ltd was awarded the

prestigious ‘Gold Level’ standard in 2009. This noteworthy

recognition follows Titan’s achievement in previously

attaining Caterpillar’s ‘Supplier of the Year’.

The Caterpillar award at ‘Gold Level’ puts Titan Steel Wheels

at the very pinnacle of suppliers to Caterpillar and is a

measure of outstanding product quality, and the application

of modern manufacturing techniques and methods.

On announcing the award, Jennifer Franklin from Caterpillar

Global Quality and part of the Caterpillar Production Centre

of Excellence said:

“Our ‘Gold Level’ standard recognises not only quality of process

and product but also reflects the standards invested by our

suppliers through their teams. Congratulations to the employees

at Titan Steel Wheels on this achievement and we look forward

to working with them as we look to the future.”

15

Pictured: Group management team

17643 25/05/10 Proof6

16

titan europe Plc Annual Report & Accounts 2009

Chief exeCuTive’s RepoRT continued

“The global downturn in industrial activity has not changed the outstanding quality of Titan’s physical assets and human resources.”Basic loss per share was 41.44p (2008: 6.62p earnings), however, the pre-exceptional level was 28.70p loss per share (2008: 13.43p earnings).

Although there was a significant operating loss, the Group’s net cash inflow from operating activities was £3.3m (2008: £22.6m), mainly as a result of the £24.8m reduction in working capital.

Net debt at the year end was £148.0m (2008: £158.2m). This again was significantly impacted by exchange rates; as the majority of the Group’s debt is in euros, reflecting the Group’s asset base and trading activities being heavily skewed to the Euro Zone. The impact of exchange rates on net debt is further explained in the Directors’ Report on page 23.

The Group’s property, plant and equipment had a net book value of £150.2m (2008: £171.0m) being mainly freehold land and buildings, and plant and machinery. Capital expenditure was reduced to £5.4m (2008: £18.2m), which is considered by the Board to be a minimum consistent with health and safety, and key strategic business needs.

opeRaTioNs

The global downturn in industrial activity has not changed the outstanding quality of Titan’s physical assets and human resources. The Group has manufacturing plants in Europe, South America, North America and Australia and will begin manufacturing in China during 2010. Many of these plants command major market shares in industry sectors with a high cost of entry and significant shipping cost barriers for non-indigenous manufacturers.

The Group’s technical excellence continues to ensure that its sales are dependent not only on price and quality, but the ability of engineers to “design & build” unique solutions to meet customers’ needs.

wheeLs DivisioN

Revenue from the agricultural market restated at 2008 rates was down 39.1% to £66.0m (2008: £108.4m). Agricultural revenues represented 61% of total revenues (2008: 55%).

Revenue from the construction market restated at 2008 rates was down 57.2% to £33.1m (2008: £77.4m). Construction revenues represented 30% of total revenues (2008: 39%).

Revenue from the mining market restated at 2008 rates was down 23.7% to £7.1m (2008: £9.3m). Mining revenues represented 7% of total revenues (2008: 5%).

Other revenue amounted to £2.2m (2008: £2.1m).

Titan Italia, Titan France, and the 50% joint venture with Titan Jantsa, all of which produce agricultural wheels, saw substantial volume reductions. Titan Italia was able to use the temporary lay off (‘CIG’) system to reduce the effective headcount and therefore cost. A somewhat slower recovery is expected in the agricultural market to that in the mining and construction sectors. Management expectations are that volumes are likely to increase during Q2 2010.

Titan Steel Wheels, manufacturing wheels for mining and construction, saw the biggest individual revenue fall. There was a heavy programme of redundancy in this plant, but, as demand through the supply chain increases, volumes are now rising and new staff are being hired.

The mining activities in Australia, Chile and Peru fared better than other wheel areas and are already seeing full recovery to pre-recession levels of activity.

The associate company, Wheels India Limited (‘Wheels India’), in which Titan hold a 35.9% equity stake, started to recover during 2009 with only an 11.4% decline in revenues. The share of the pre-exceptional profits of Wheels India amounted to £0.5m (2008: £1.2m). This is further explained in the Directors’ Report on page 25.

Pictured: Wheels management team

www.titaneurope.com Stock code: AIM: TSW.L

17

our business

17643 25/05/10 Proof6

Chief Executive’s Report

www.titaneurope.com Stock code: AIM: TSW.L

17

Performance

uNDeRCaRRiaGe DivisioN

Revenue from the agricultural market restated at 2008 rates was down 24.4% to £6.2m (2008: £8.2m). Agricultural revenues represented 5% of total revenues (2008: 3%).

Revenue from the construction market restated at 2008 rates was down 53.2% to £81.4m (2008: £174.0m). Construction revenues represented 64% of total revenues (2008: 67%).

Revenue from the mining market restated at 2008 rates was down 47.0% to £38.4m (2008: £72.5m). Mining revenues represented 30% of total revenues (2008: 28%).

Other revenue amounted to £1.9m (2008: £4.8m).

The Undercarriage division experienced an unprecedented year with a reduction in revenues of 50.7% (at constant exchange rates) and an even more dramatic reduction in manufacturing activity of about 65%. Volume in manufacturing started to decline, particularly in North America, during 2007 and continued to decline in 2008 and 2009.

Case sTuDY:

New ChiNa pLaNTAcknowledging the increasing numbers of Western OEMs

moving production to China to gain market share, the

Undercarriage division began work on a new plant in this

region during early 2009, obtaining the business licence in

February 2009. This facility became active in the final quarter

of 2009.

Located in Tianjin, the nearest port to the city of Bejing,

and at an anticipated total cost of €5,000,000 over the next

3 years, the manufacturing operation services the local

demands of OEMs, and also protects margins on worldwide

AMKs by focusing on the more competitive range of small

chains and rollers.

Production during phase one is concentrated on roller and

chain components, though by phase three in 2012, the plant

is expected to have expanded its capacity, also enabling it to

provide idler and shoe components.

Against this backdrop, the key target for the division was the control of working capital and cash in the business together with the reduction of fixed costs. The division identified and implemented the most appropriate solutions in terms of temporary or permanent redundancy agreements with workers and unions in the different regions in which Titan operates.

Important cutbacks in capacity and a plant closure were completed in 2008, but these did not fully compensate for the further volume reductions experienced in 2009. The speed of the continuous reduction in volume and the necessity to adjust the manufacturing activity almost on a “day by day” basis did not allow the management of the workforce and fixed cost reductions in an efficient manner, therefore impacting Titan’s profitability.

The management of the working capital and the continuous focus on stock reduction has driven a negative impact on margins due to rework costs and in some cases higher transport costs.

Whilst the operating environment was very difficult, Titan continued its strategic programme of consolidation of the manufacturing activity in Europe and globalisation of the manufacturing footprint in line with Titan’s key Western OEMs strategies. A key issue for the Group’s OEMs during 2009 was the ability of key suppliers to deliver a strategy in line with their global sourcing requirements mainly in China, India and Brazil.

Brazil, since acquisition in 2005, has become a very efficient and competitive manufacturing operation, making small/medium components for undercarriage vehicles in South and North America. It has been a very important solution not only to address local demand, but also to win new business in North America in the face of competition mainly from the Far East.

China has been the key focus of 2009 in the global strategy. Titan obtained the business licence in February 2009 and Titan has dedicated resources to set up a new manufacturing operation in China to serve the local demand from Western OEMs. The activity of serving this market started during the fourth quarter of 2009.

Pictured: Undercarriage management team

17643 25/05/10 Proof6

titan europe Plc Annual Report & Accounts 2009

18

Year ended

Year ended 31 December Year ended

31 December 2009 31 December

2009 at 2008 rates 2008

£m £m £m

Market

Agricultural 80.0 72.2 116.6

Construction 126.0 114.5 251.4

Mining 51.0 45.5 81.8

Other 4.5 4.1 6.9

Total revenue 261.5 236.3 456.7

Revenue and trading profit by division Year ended Year ended 31 December Year ended

31 December 2009 31 December

2009 at 2008 rates 2008

£000 £000 £000

Revenue

Wheels (including

share of joint venture) 118,049 108,427 197,224

Undercarriages 143,451 127,908 259,526

Revenue including

share of joint venture 261,500 236,335 456,750

Less share of joint

venture (2,930) (2,969) (4,437)

Group revenue 258,570 233,366 452,313

Trading (loss)/profit

Wheels (excluding

share of joint venture) (4,192) (4,102) 22,571

As a percentage of

revenue (3.6%) (3.9%) 11.7%

Undercarriages (13,938) (12,040) 8,593

As a percentage of

revenue (9.7%) (9.4%) 3.3%

Group trading (loss)/profit (18,130) (16,142) 31,164

Chief exeCuTive’s RepoRT continued

The focus on the European business based on engineering excellence and servicing our major customers with a ‘design and build’ solution for their complete undercarriage needs has continued.

Further progress has been made towards creating a ‘Centre of Excellence’ for engineering in the facility at Gevelsberg, Germany, with the fully assembled frame business being supplied from this location and from the Intertractor America location in Elkhorn, Wisconsin. This engineering resource is able to focus on large scale applications; manufacturing facilities are expected to move in a similar direction. The testing site has been completed at the Group testing department in Italy and started to operate with all new testing machines in 2009.

The Italian manufacturing plants are being re-engineered to focus on mid to large range products with a more flexible manufacturing process system using less work in progress and with shorter lead times.

Other developments which have been reported in the past, such as mining and service centres, are working well and will be a blueprint for the future.

In all, the Undercarriage division has overcome the worst part of the global recession whilst continuing to operate efficiently as a global player in a global market, and is well placed to respond as demand increases.

Revenue by geographical destination and market (including share of joint venture) Year ended

Year ended 31 December Year ended

31 December 2009 31 December

2009 at 2008 rates 2008

£m £m £m

Destination

UK 7.8 7.3 20.7

Europe 153.0 138.4 264.8

North America 24.0 20.8 55.2

South America 26.2 24.3 28.6

Rest of the World 50.5 45.5 87.4

Total revenue 261.5 236.3 456.7

www.titaneurope.com Stock code: AIM: TSW.L

19

our business

17643 25/05/10 Proof6

Chief Executive’s Report

www.titaneurope.com Stock code: AIM: TSW.L

19

Performance

DiviDeND

As part of the amendment and restatement agreement with our primary bankers Intesa Sanpaolo SpA and Unicredit SpA, no dividend distributions will be made until after the Company has recommenced payments of the loan in January 2011 and are subject to the Company achieving a leverage ratio of 3.5:1 or less.

2010 ouTLooK

Entering Q2 of the 2010 financial year, the Group is now seeing order volumes at a level approximately 45% higher than in the second half of 2009.

Overall, the Board believes that the business has created a strong platform for the ongoing development of the Group, with stronger engineering and quality presence in the market, supported by more efficient manufacturing. This is confirmed by the recent awards from Caterpillar (‘Gold Level’ for the Titan Steel Wheels business in the UK) and John Deere (the ‘Partner-level’ Supplier Award for the Italtractor Landroni business in Brazil).

Titan continues to respond to the changing pattern of its customers’ needs, by further developing the global manufacturing footprint from its traditional European focus. The new undercarriage factory in China is expected to be in full production during Q3 and a second phase of further expansion to support demand from customers is now being planned. Titan already supplies Western manufacturers based in China with undercarriage assemblies. This demand is stronger than expected.

This greater diversity of location, stronger market presence and manufacturing efficiencies, combined with a substantial reduction in fixed costs, leaves the Group well placed to benefit from the recovery in its markets.

posT-YeaR eND eveNTs

amendment of banking facilitiesDue to the significant impact on the 2009 results as a result of the global downturn, the Group has negotiated an amendment to the covenants which includes no testing until the June 2011 results and revised covenants based on the Group’s revised business plans. This does not affect the capital repayment profile as renegotiated in May 2009.

Mike akersChief Executive7 June 2010

Pictured: Fabricated idler with precision machined brackets

Pictured: MAVT adjustable tractor wheels

This outlook may contain forward-looking statements with respect to the financial condition, results, operations and businesses of Titan Europe Plc. Such statements and forecasts involve risk and uncertainty because they relate to events and depend upon circumstances that will occur in the future. There are a number of factors that could cause actual results or developments to differ materially from those expressed or implied by forward-looking statements and forecasts. Forward-looking statements and forecasts are based on the directors’ current view and information known to them at the date of this statement. Nothing in this statement should be construed as a profit forecast.

17643 25/05/10 Proof6

20

titan europe Plc Annual Report & Accounts 2009

DiReCToRs & aDviseRs

1. 2. 3.

4. 5. 6.

7.

1. MoRRY TaYLoR

2. MiKe aKeRs

3. GaRY ChesTeRToN

4. CeCiLia La MaNNa

5. viNCeNT wiCKs

6. biLL biLLiG

7. phiL GaRTsiDe

www.titaneurope.com Stock code: AIM: TSW.L

21

our business

17643 25/05/10 Proof6

Directors & Advisers

www.titaneurope.com Stock code: AIM: TSW.L

21

GoVernance

Company and Registered officeTitan Europe PlcBridge Road, CookleyKidderminsterWorcestershire DY10 3SDTel: +44 (0)1562 [email protected]

Registered in england3018340

Company secretaryGary Chesterton FCCA

auditorsPricewaterhouseCoopers LLPChartered Accountants andRegistered Auditors19 Cornwall StreetBirmingham B3 2DT

financial public RelationsCitigate Dewe Rogerson Ltd1 Wrens Court, Lower Queen Street Birmingham B72 1RT

Legal adviserHBJ Gateley Wareing LLPOne Eleven, Edmund StreetBirmingham B3 2HJ

Nominated adviser and brokerSeymour Pierce Ltd20 Old Bailey London EC4M 7EN

MoRRY TaYLoRNon-executive Chairman

Morry is Chief Executive of Titan International Inc. He comes from an engineering family. He holds a degree in engineering from Michigan Tech. Morry developed a business as a manufacturers’ agent in the wheel business before founding, with one of his principals, Titan Wheel (then named “Can-Am”). Morry managed the growth and expansion of this business which became a leading specialist manufacturer of off-highway wheels and tyres in the US, taking the Company public first on NASDAQ and later on NYSE. Morry was appointed as a director of Titan Europe on 4 March 2004.

MiKe aKeRsChief executive

Mike has a background in the UK automotive components industry. He began organising the start-up of Titan Europe’s European operations in 1989 and became a member of Titan International Inc. management team in 1995. Mike has overseen the development of Titan Europe. He graduated with a first class honours degree in Engineering from the University of Cardiff, holds an MBA from Warwick University and sits on the Board of Warwick Business School. Mike was appointed as a director of Titan Europe on 2 February 1995.

GaRY ChesTeRToNGroup finance Director

Gary has over 26 years of internal audit and financial management experience gained from within the construction and engineering sectors. Before joining Titan Europe in 2006 to assist the Group Finance Director, he was European Financial Controller for a US construction company; prior to this he worked for a Fortune 200 diversified manufacturing company in both financial and general management roles. Gary became Group Finance Director in October 2008, focusing on the management of the Group’s finance and treasury functions.

CeCiLia La MaNNaexecutive Director

Cecilia is a chartered accountant and has a doctorate in accountancy. She trained and worked for Pricewaterhouse Coopers in Italy and in the UK. She joined Titan Europe in 1996 as Finance Controller of the Italian subsidiary and developed her career in the Group becoming Finance Director of Titan Europe in 2001. She was involved in the extensive acquisition programs including the Group’s expansion into the undercarriages sector. In 2006, she led the integration of Italtractor ITM into the Group. Her primary role is now as Managing Director of the Undercarriage division.

viNCeNT wiCKsexecutive Director

Vince is an experienced Company Secretary and Finance Director with a long career in UK manufacturing companies. He is a Chartered Secretary and also a Fellow of the Chartered Institute of Management Accountants. He joined the Company that is now Titan Steel Wheels Limited as Finance Director in 1989.

biLL biLLiGNon-executive Director

Bill is a well-known and respected figure in the automotive and engineering world on both sides of the Atlantic. Bill is Vice-Chairman of the Board of directors of Titan International Inc. and is also director and Chairman of MSX International Inc., a leading supplier of subcontract engineering to the automotive industry.

phiL GaRTsiDeNon-executive Director

Phil is an accountant with experience in the manufacturing industry at Chief Executive level. He has been a director of several UK public companies and now combines managing a number of engineering businesses with his role as Chairman of Bolton Wanderers Football Club. Phil was appointed as a director of Titan Europe on 4 March 2004.

17643 25/05/10 Proof6

22

titan europe Plc Annual Report & Accounts 2009

DiReCToRs’ RepoRT

The directors present their report and the audited financial statements of the Company and Group for the year ended 31 December 2009.

pRiNCipaL aCTiviTies

The principal activity of the Group is the manufacture and sale of steel wheels and undercarriages for the off-highway vehicles industry. Principal markets are construction, agriculture and mining. The principal activity of the Company is to act as a holding company.

busiNess Review

business environmentTitan Europe and its subsidiaries are the only worldwide manufacturer specialising in the technology of both tracked and wheeled vehicle movement systems for the construction, agricultural and mining industries. The overall demand for the products, which is driven primarily by the demand for construction, agricultural and mining equipment, has been severely affected by the global recession and the destocking process implemented by the Original Equipment Manufacturers (‘OEMs’).

The Group operates in a highly competitive market but is well placed because of its concentration in developing the technology of this highly specialised product area which is important to relationships with key OEMs such as Caterpillar, Agco, CNH, Liebherr and Hitachi. The Company continues to work closely with these OEMs on future product development.

strategyTitan’s strategy is designed to create the most effective supply systems for undercarriage assemblies, components and spare parts; and for wheels and wheel and tyre assemblies to customers at all levels in the supply chain throughout the construction, agricultural and mining world. These include OEMs, large users of fleets of equipment, dealers and distributors.

The Group has continued to support its OEM customers with their global repositioning such as the joint venture, Titan Jantsa in Turkey and the new plant in China which will begin production during 2010. There are further ongoing projects to enhance this strategy.

This manufacturing and distribution strategy will be supported by the best available research development design and testing facilities centrally located to achieve maximum efficiency and accessibility for our customers.

Finally, the Group aims to employ the best available international management team to obtain maximum benefit from its facilities.

Research and developmentTitan continually develops innovative products to add value to its customers’ machines by improving cost and performance. Titan’s focus on developing solutions for its customers with the centralised engineering development for undercarriage products in Germany has resulted in a significant number of new project opportunities with both existing and new customers.

Due to the global recession and an emphasis on cash preservation the Group reduced its capital expenditure to a minimum level consistent with health & safety and key strategic business needs. In 2009, there was a net cash outflow for capital expenditure of £4,000,000 (2008: £13,900,000).

TaxationThe effective tax rate for 2009 is 16.5%, as per the Key Financial Ratios on page 27, which is below the UK rate of corporation tax. This is due to the impact of our overseas entities, mainly Italian, suffering an average effective rate of 14.5%. Note 9 shows an impact of £3,321,000 (2008: (£760,000)) within “Movement in unrecognised deferred taxation”. Of this movement, the Italian subsidiaries account for £3,600,000 (2008: £nil) as a result of the write-off of deferred tax assets which expire in 2010 and 2011. future outlookAlthough generally the global markets continue to be weak across all sectors, there still exist opportunities for the Group specifically in the large mining wheels and undercarriages sectors. This, coupled with the impact of our cost reductions and working capital focus, will continue to strengthen the Group’s position as the global markets recover.

financing and going concernThe Group funds its operations through a mixture of retained earnings and borrowing facilities, including leasing. The relative proportions of equity and borrowings are governed by stipulated parameters. These are designed to preserve prudent financial ratios, including interest, dividend and cash flow cover, whilst also minimising the overall weighted average cost of capital to the Group.

All the Group’s borrowing facilities are arranged centrally and controlled by the Group Finance Director. The funds are raised in an appropriate way to serve the needs of the business in a range of currencies and locations. These funds may then be lent, directly or indirectly, to operating subsidiaries on commercial arm’s length terms.

The directors have assessed the future funding requirements of the Group and the Company. Having undertaken this review and considered a number of possible outcomes, the directors are of the opinion that the Group has adequate resources to fund its operations for the foreseeable future and so determine

www.titaneurope.com Stock code: AIM: TSW.L

23

our business

17643 25/05/10 Proof6

Directors’ Report

www.titaneurope.com Stock code: AIM: TSW.L

23

GoVernance

that it is appropriate to present these financial statements on a going concern basis.

principal risks and uncertaintiesThe management of the business and the execution of the Group’s strategy are subject to a number of risks. The key business risks are detailed below:

Cyclical nature of the industryThe wheel and undercarriage component industry is a cyclical industry affected to a significant extent by the general prevailing economic conditions and in particular by trends and the level of investment in the sectors in which the Group operates. Historically, and as demonstrated by the current year, the construction industry has suffered economic downturns every eight to ten years. There can therefore be no assurance that the Group will be able to maintain profitability during a period of economic downturn, or that there will be sufficient demand for the Group’s product output, including any planned additional production capacity.

The globalisation of the economy and financial markets volatility has increased the Group’s exposure to external factors such as changes in foreign exchange rates, interest rates and commodity prices which in turn make future forecasting of financial and operational performance more uncertain.

Customer concentration and relationshipsThe Group receives approximately 43% of its sales revenue from ten major global customers. The loss of, or damage to, any of these relationships or a significant worsening of commercial terms with these customers could have a material impact on the Group’s results. At the same time, there is a significant benefit from trading with customers of this nature and considerable resource is devoted to ensure that satisfactory relationships are maintained and developed.

CompetitorsThe Group operates in a highly competitive marketplace. In OEM markets there is always continual pressure on sales prices and a reluctance to accept price increases generated by input cost changes. The high cost of entry to the market acts in part as an effective barrier to new competitors, as does Titan’s ability to design its own capital equipment.

Regulatory environmentThe Group operates in countries in which the regulatory environment with regard to employment is less favourable to employers than employees and where unionisation of the workforce is common. This may, from time to time, have a negative impact on the Group. This environment also facilitates disputes with and claims by employees, particularly upon termination.

The Group may be adversely affected by changes in government regulations and policies.

The Group is subject to risks associated with environmental laws and regulations.

TaxationThe Group operates in many countries and as a consequence is subject to many tax laws and administrative procedures. Many of these rules are complex and subject to detailed scrutiny by tax authorities undertaking audits and ultimately litigation which may take several years to complete. Against this background, significant management judgement is taken in arriving at the estimate of income tax due in each jurisdiction in which the Group operates. Currency riskThe Group has transactional currency exposures arising from sales or purchases by operating subsidiaries in currencies other than the subsidiaries’ functional currency which are mostly naturally hedged and in certain cases are covered by the use of forward foreign exchange contracts.

The Group operates in a global environment with global customers and therefore transacts in a number of currencies which subjects the Group to foreign exchange risk.

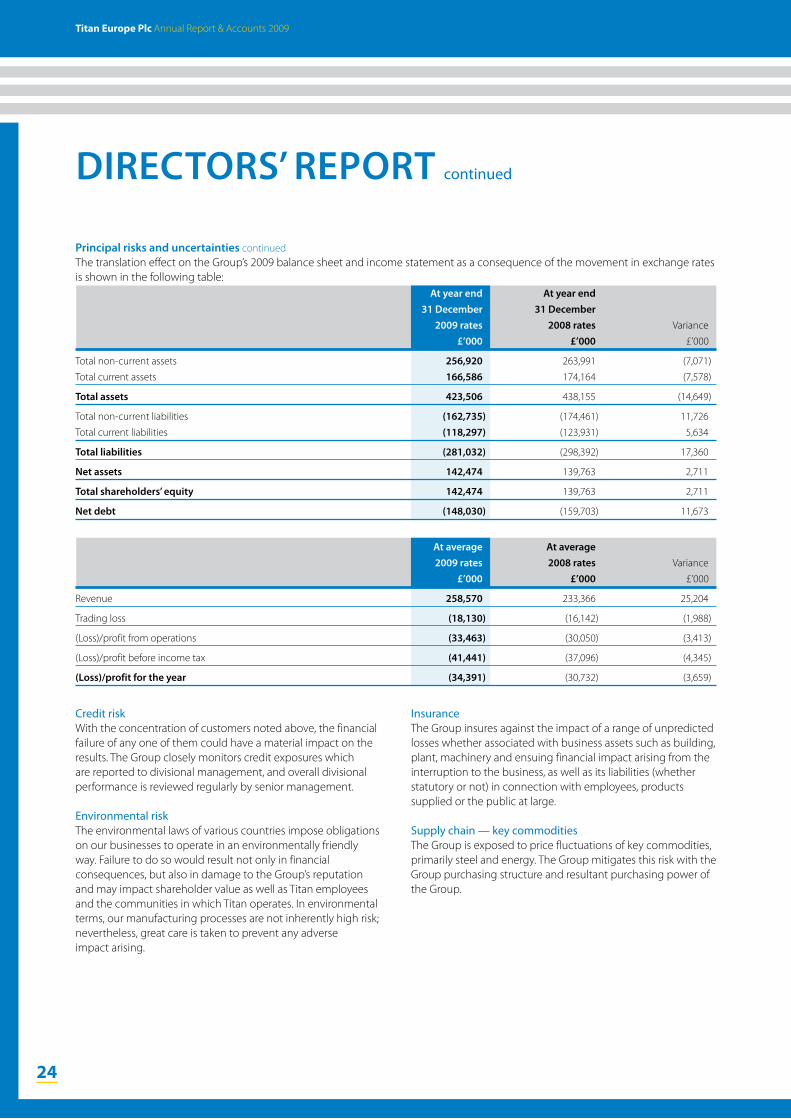

The key currencies to which the Group is exposed and the relevant exchange rates are detailed below:

2009 2008

euro

Average 1.123 1.260

Closing 1.111 1.027

us dollar

Average 1.565 1.855

Closing 1.593 1.448

brazilian real

Average 3.127 3.368

Closing 2.786 3.411

australian dollar

Average 1.994 2.189

Closing 1.784 2.098

This year was again affected by the movement in foreign exchange primarily due to the strengthening of sterling against the euro for the closing rate and a weakening of the average rate. Due to the significant impact on the UK companies the Group entered into simple forward foreign exchange contracts in 2009 which were all closed out by 31 December 2009. The Group continues to monitor its currency exposure and where appropriate will enter into simple forward contracts. The claim against the Royal Bank of Scotland is ongoing; see note 2 for further detail.

17643 25/05/10 Proof6

24

titan europe Plc Annual Report & Accounts 2009

DiReCToRs’ RepoRT continued

InsuranceThe Group insures against the impact of a range of unpredicted losses whether associated with business assets such as building, plant, machinery and ensuing financial impact arising from the interruption to the business, as well as its liabilities (whether statutory or not) in connection with employees, products supplied or the public at large.

Supply chain — key commoditiesThe Group is exposed to price fluctuations of key commodities, primarily steel and energy. The Group mitigates this risk with the Group purchasing structure and resultant purchasing power of the Group.

Credit riskWith the concentration of customers noted above, the financial failure of any one of them could have a material impact on the results. The Group closely monitors credit exposures which are reported to divisional management, and overall divisional performance is reviewed regularly by senior management.

Environmental riskThe environmental laws of various countries impose obligations on our businesses to operate in an environmentally friendly way. Failure to do so would result not only in financial consequences, but also in damage to the Group’s reputation and may impact shareholder value as well as Titan employees and the communities in which Titan operates. In environmental terms, our manufacturing processes are not inherently high risk; nevertheless, great care is taken to prevent any adverse impact arising.

principal risks and uncertainties continuedThe translation effect on the Group’s 2009 balance sheet and income statement as a consequence of the movement in exchange rates is shown in the following table: at year end at year end 31 December 31 December 2009 rates 2008 rates Variance

£’000 £’000 £’000

Total non-current assets 256,920 263,991 (7,071)

Total current assets 166,586 174,164 (7,578)

Total assets 423,506 438,155 (14,649)

Total non-current liabilities (162,735) (174,461) 11,726

Total current liabilities (118,297) (123,931) 5,634

Total liabilities (281,032) (298,392) 17,360

Net assets 142,474 139,763 2,711

Total shareholders’ equity 142,474 139,763 2,711

Net debt (148,030) (159,703) 11,673

at average at average 2009 rates 2008 rates Variance

£’000 £’000 £’000

Revenue 258,570 233,366 25,204

Trading loss (18,130) (16,142) (1,988)

(Loss)/profit from operations (33,463) (30,050) (3,413)

(Loss)/profit before income tax (41,441) (37,096) (4,345)

(Loss)/profit for the year (34,391) (30,732) (3,659)

www.titaneurope.com Stock code: AIM: TSW.L

25

our business

17643 25/05/10 Proof6

Directors’ Report

www.titaneurope.com Stock code: AIM: TSW.L

25

GoVernance

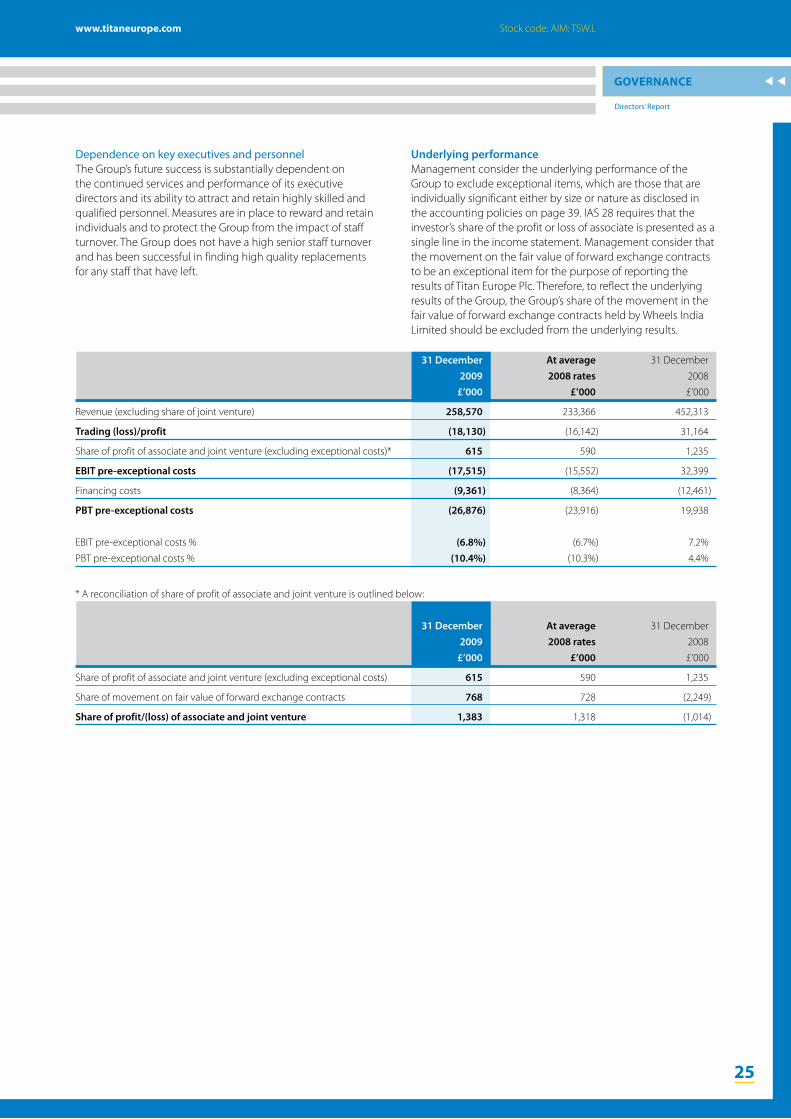

Dependence on key executives and personnelThe Group’s future success is substantially dependent on the continued services and performance of its executive directors and its ability to attract and retain highly skilled and qualified personnel. Measures are in place to reward and retain individuals and to protect the Group from the impact of staff turnover. The Group does not have a high senior staff turnover and has been successful in finding high quality replacements for any staff that have left.

underlying performanceManagement consider the underlying performance of the Group to exclude exceptional items, which are those that are individually significant either by size or nature as disclosed in the accounting policies on page 39. IAS 28 requires that the investor’s share of the profit or loss of associate is presented as a single line in the income statement. Management consider that the movement on the fair value of forward exchange contracts to be an exceptional item for the purpose of reporting the results of Titan Europe Plc. Therefore, to reflect the underlying results of the Group, the Group’s share of the movement in the fair value of forward exchange contracts held by Wheels India Limited should be excluded from the underlying results.

31 December at average 31 December

2009 2008 rates 2008

£’000 £’000 £’000

Revenue (excluding share of joint venture) 258,570 233,366 452,313

Trading (loss)/profit (18,130) (16,142) 31,164

Share of profit of associate and joint venture (excluding exceptional costs)* 615 590 1,235

ebiT pre-exceptional costs (17,515) (15,552) 32,399

Financing costs (9,361) (8,364) (12,461)

pbT pre-exceptional costs (26,876) (23,916) 19,938

EBIT pre-exceptional costs % (6.8%) (6.7%) 7.2%

PBT pre-exceptional costs % (10.4%) (10.3%) 4.4%

* A reconciliation of share of profit of associate and joint venture is outlined below:

31 December at average 31 December

2009 2008 rates 2008

£’000 £’000 £’000

Share of profit of associate and joint venture (excluding exceptional costs) 615 590 1,235

Share of movement on fair value of forward exchange contracts 768 728 (2,249)

share of profit/(loss) of associate and joint venture 1,383 1,318 (1,014)

17643 25/05/10 Proof6

26

titan europe Plc Annual Report & Accounts 2009

DiReCToRs’ RepoRT continued

Key performance indicatorsThe Board monitors progress on the overall Group strategy with reference to the following key performance indicators and key financial ratios which have been calculated based on the sterling translated balances:

2009 at Definition, method of 2009 2008 rates 2008 calculation and analysis

Revenue growth (42.8%) (48.4%) 17.2% Year on year revenue growth. At constant

exchange rates the Undercarriage division was

lower than 2008 by 50.1% and the Wheels division

lower than 2008 by 45.0%.

Gross profit as a % of revenue 4.9% 5.1% 13.8% Profit before distribution, administration and

significant one-off items. Gross profit percentage

reduced due to inefficiencies and impact of fixed

costs on significantly reduced volumes.

EBITDA as a % of revenue 0.4% 0.6% 10.9% Trading (loss)/profit including underlying share

of associate and joint venture (as defined in

the reconciliation above), before depreciation

and amortisation. Impact of lower gross profit

percentage.

Revenue per employee £110,689 £99,900 £154,902 Total Group revenue divided by the average

number of employees. At constant exchange rates

down by 35.5% which is lower than the revenue

impact due to headcount reductions.

Inventory turn 2.9 2.6 3.1 Annual cost of sales divided by the year end

inventory balance. Reduced from 2008 due to

significant reduction in volumes not entirely

matched by overall inventory reduction.

Debtor days 70 84 70 Year end net trade debtors balance divided by

the annual sales multiplied by 365. At constant

exchange rates the result of a reduced level of

debt factoring in 2009 had an adverse effect of

7 days coupled with a change in the debtor mix

in the Undercarriage division, as the aftermarket

debtors (with longer terms) represented a higher

proportion of the debt.

Creditor days 66 77 84 Year end trade creditor balance divided by the

cost of sales plus distribution costs multiplied

by 365. This change is due to significant 2009

reductions in raw material purchases.

www.titaneurope.com Stock code: AIM: TSW.L

27

our business

17643 25/05/10 Proof6

Directors’ Report

www.titaneurope.com Stock code: AIM: TSW.L

27

GoVernance

ResuLTs aND DiviDeNDs

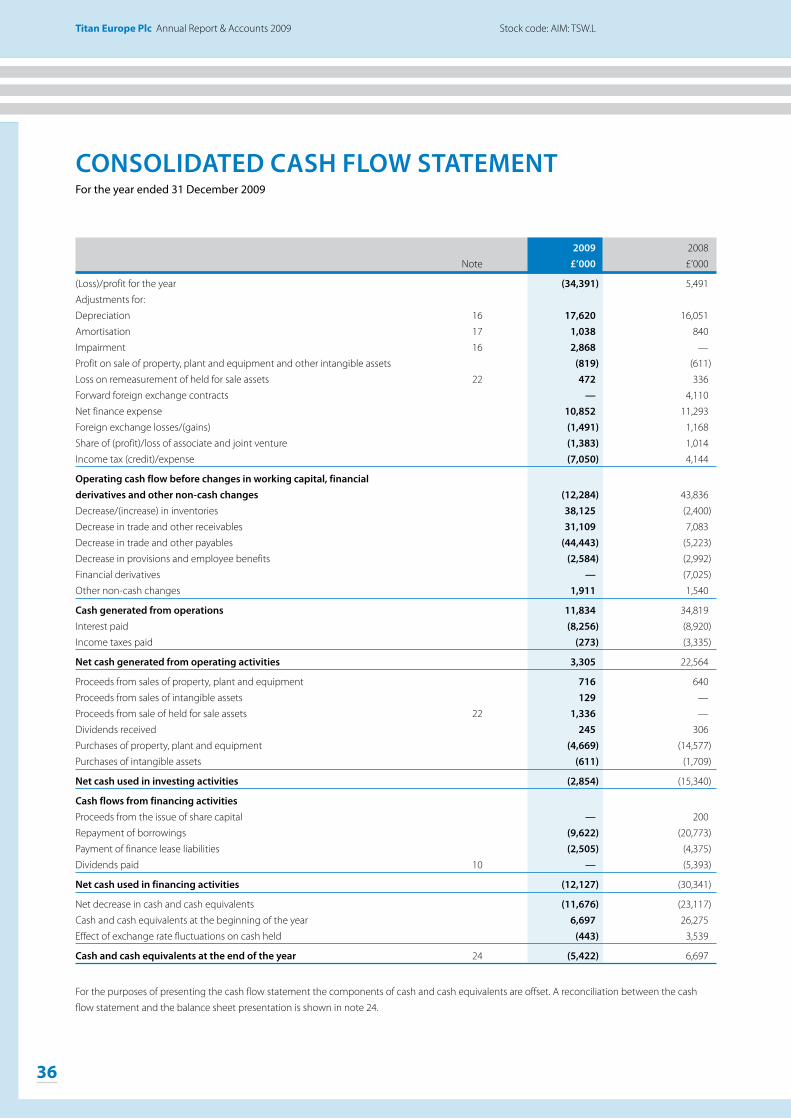

The Group’s loss after taxation for the year ended 31 December 2009 amounted to £34,391,000 (2008: £5,491,000 profit). The income statement is shown on page 32.

As part of the May 2009 amendment and restatement agreement with our primary bankers Intesa Sanpaolo SpA and Unicredit SpA no dividend distributions will be made until after the Company has recommenced payments of the loan in January 2011 and are subject to the Company achieving a leverage ratio of 3.5:1 or less.

On the basis of the above, no interim dividend per ordinary share was paid (2008: 2.17p), and the directors will not be proposing a final dividend. There was therefore no full dividend for the year (2008: 2.17p) and the total cost of dividends for 2009 was £nil (2008: £1,800,000).

DiReCToRs

The directors who served during the year and up to the date of signing these financial statements were as follows:J M A Akers E H BilligM C La Manna P A GartsideV M R Wicks G ChestertonM M Taylor

The Company has purchased and maintained throughout the year directors’ and officers’ liability insurance in respect of itself and its directors. The directors also have the benefit of the indemnity provisions contained in the Company’s Articles of Association. The insurance and indemnity provisions were in place during the year and are still in place at the date of this report.

DiReCToRs’ iNTeResTs

The beneficial interests of the directors in the 40p ordinary shares in the Company at 31 December 2009 are shown below:

fully paid ordinary shares

31 December 31 December

2009 2008

J M A Akers* 700,000 610,000

V M R Wicks* 500,000 500,000

G Chesterton* 65,000 —

E H Billig 40,000 40,000

P A Gartside 24,000 24,000

M C La Manna 288,000 288,000

* These ordinary shares are registered in the name of The Steel Wheels Executive Pension Scheme, a pension scheme of which J M A Akers, G Chesterton and V M R Wicks are beneficiaries.

Key financial Ratios

2009 at Definition, method of 2009 2008 rates 2008 calculation and analysis

Interest cover on EBITDA 0.1 0.2 4.4 EBITDA as defined above divided by the total net

financing cost excluding bond redemption costs

and other finance charges. Significant reduction

due to overall decline in EBITDA as a result of the

volume reductions.

Interest cover on EBIT (2.2) (1.9) 2.9 EBITDA as defined above adding back

depreciation and amortisation adjustments,

divided by total net financing costs excluding

bond redemption costs and other finance charges.

Significant change as a result of the loss at EBIT

level.

Effective tax rate 16.5% 16.6% 38.9% Income tax charge divided by profit before tax,

excluding share of associate and joint venture.

Distorted by level of losses mainly in the Italian

subsidiaries.

Gearing 104% 114% 91% Net debt divided by net assets. Net debt held at

similar levels but net assets reduced by net loss in

period.

Cash conversion ratio 101% 100% 31% Net cash generated from operating activities

less net cash used in investing activities, divided

by (loss)/profit from operations. Improvements

in working capital and control of capital

expenditures have enabled a positive cash

generation despite a loss from operations.

Information which fulfils the remaining requirements of the Business Review can be found in the Chief Executive’s Report on pages 14 to 19.

17643 25/05/10 Proof6

28

titan europe Plc Annual Report & Accounts 2009

DiReCToRs’ RepoRT continued

opTioNs

Options held Cancelled Granted options held at 1 January during during at 31 DecemberDirector 2009 the year the year 2009

J M A Akers 1,710,000 (1,710,000) 1,710,000 1,710,000M C La Manna 660,000 (660,000) 660,000 660,000V M R Wicks 180,000 (180,000) 180,000 180,000G Chesterton — — 200,000 200,000M M Taylor 180,000 (180,000) 180,000 180,000E H Billig 180,000 (180,000) 180,000 180,000P A Gartside 180,000 (180,000) 180,000 180,000

The share options cancelled during the year refer to those options that were granted on the admission to the AIM market on 7 April 2005 and those options granted on the readmission to the AIM market on 30 December 2005. These share options were cancelled on 1 June 2009 and replaced with options granted on 1 June 2009 under the Unapproved Share Option Scheme 2004. The shares were granted with an option price of 40p, the nominal value of the underlying shares. These options are exercisable during the period 1 June 2012 to 1 June 2019.

The options granted to G Chesterton have been granted on the same basis as the replacement options above, with an exercise price of 40p and exercisable during the period 1 June 2012 to 1 June 2019.

No director had any interest in contracts of the Company or the Group during the year.

eMpLoYee poLiCies

The directors recognise the considerable benefits which accrue from keeping employees at all levels informed of the progress of the business and involving them in the Group’s performance. The Group’s policy is to ensure that information and views are exchanged and considered in meetings with employee representatives and that employees are made aware of the financial and economic factors affecting the Group’s performance by the publishing of such information on noticeboards.

The Group considers any application for employment by disabled persons. In the event of any employee becoming disabled, the Group explores all options to retain the individual and to comply fully and fairly with legislation relating to such persons.

DoNaTioNs

Charitable donations made by the Group during the year in support of the local community amounted to £4,100 (2008: £7,100). During the year, the Group has not made any political donations (2008: £nil).

paYMeNTs To suppLieRs

The Group agrees terms and conditions for its business transactions with individual suppliers, ensures that suppliers are made aware of the terms of payment and makes payment in accordance with these terms. At the year end, the trade creditor days for the Group were 66 days (2008: 84 days) and for the Company the creditor days were 41 days (2008: 73 days).

subsTaNTiaL shaRehoLDiNGs

As at 9 April 2010, the Company was aware of the following interests in 3.0% or more in the ordinary share capital of the Company: Number % held

Mefro Wheels GmbH 24,788,853 29.9

Titan Luxembourg SARL. 18,993,821 22.9

AXA Framlington Investment Management 6,451,179 7.8

Carlson Capital LP 3,212,775 3.9

www.titaneurope.com Stock code: AIM: TSW.L

29

our business

17643 25/05/10 Proof6

Directors’ Report

www.titaneurope.com Stock code: AIM: TSW.L

29

GoVernance

fiNaNCiaL iNsTRuMeNTs

The Group’s financial risk management objectives and policies are explained in note 2. The Group uses credit insurance as appropriate to manage its credit risk on an individual customer basis where the risk is considered sufficient to merit the cover.

ReseaRCh aND DeveLopMeNT

Research is carried out by the Group to ensure that our position as market leaders in the businesses in which we operate, is maintained. The Group’s research and development costs are detailed in note 12 to the financial statements.

eNviRoNMeNT

The Group requires the management of its subsidiary companies to adopt policies to comply with local environmental requirements. The Group provides considerable local autonomy for capital expenditure needed for environmental compliance.

posT-baLaNCe sheeT eveNTs

The information that fulfils the requirements of post-balance sheet events disclosure in the Directors’ Report can be found on page 19.

sTaTeMeNT of DisCLosuRe of iNfoRMaTioN To auDiToRs

As far as the directors are aware there is no relevant audit information of which the Company’s auditors are unaware and the directors have taken all the steps that ought to have been taken to make ourselves aware of any relevant audit information and to establish that the Company’s auditors are aware of that information.

sTaTeMeNT of DiReCToRs’ RespoNsibiLiTies iN RespeCT of The aNNuaL RepoRT aND The fiNaNCiaL sTaTeMeNTs

The directors are responsible for preparing the Annual Report and the Group and the Company financial statements in accordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. Under that law the directors have prepared the Group financial statements in accordance with International Financial Reporting Standards (‘IFRSs’) as adopted by the European Union, and the Company financial statements in accordance with applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice). The Group and Company financial statements are required by law to give a true and fair view of the state of affairs of the Company and the Group and of the profit or loss of the Group for that period.

In preparing those financial statements, the directors are required to:

●● select suitable accounting policies and then apply them consistently;

●● make judgements and estimates that are reasonable and prudent;

●● state that the financial statements comply with IFRSs as adopted by the European Union and with regard to the Company financial statements that applicable UK Accounting Standards have been followed, subject to any material departures disclosed and explained in the financial statements; and

●● prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Group will continue in business, in which case there should be supporting assumptions or qualifications as necessary.

The directors confirm that they have complied with the above requirements in preparing the financial statements.

The directors are responsible for keeping proper accounting records that disclose with reasonable accuracy at any time the financial position of the Company and the Group and to enable them to ensure that the Group financial statements comply with the Companies Act 2006 and the Company financial statements comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Company and the Group and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The directors are responsible for the maintenance and integrity of the Company website. Legislation in the United Kingdom governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

auDiToRs

A resolution to reappoint PricewaterhouseCoopers LLP as auditors to the Company will be proposed at the Annual General Meeting.

By Order of the BoardG ChestertonGroup Finance Director 7 June 2010

17643 25/05/10 Proof6

30

titan europe Plc Annual Report & Accounts 2009

CoRpoRaTe GoveRNaNCe sTaTeMeNTiNTRoDuCTioN

The Board of Titan Europe Plc is committed to achieving good standards of corporate governance, integrity and business ethics for all activities. Under the rules of the Alternative Investment Market, the Group is not required to comply with the Combined Code. Nevertheless, the Group has taken steps to comply in so far as it can be applied practically and appropriately, given the size of the Group and the nature of its operations. The Board is continuing to consider other aspects of the Code for appropriateness and these may be introduced when it becomes relevant for the Group to do so.

boaRD CoMposiTioN

The Board of directors comprises four executive and three non-executive directors. The non-executive directors are:

M M TaylorE H BilligP A Gartside

auDiT CoMMiTTee

The Audit Committee, composed of the non-executive directors, reviews the Company’s financial reporting (including accounting policies) and internal financial controls.

The chairman is P A Gartside.

ReMuNeRaTioN CoMMiTTee

The Remuneration Committee, composed of the non-executive directors, is responsible for establishing and developing Titan Europe’s general policy on executive and senior management remuneration and determining specific remuneration packages for executive directors.

The chairman is M M Taylor.

fiNaNCiaL CoNTRoL

The Group has a comprehensive system for reporting financial results to the Board. Monthly trading results are prepared for each operating business and at consolidated level, with comparison against budget and prior year. The Board reviews these and meets periodically to determine appropriate action.

GoiNG CoNCeRN

The directors have reviewed the Group’s budget and cash flows for 2010 together with longer-term plans and are satisfied that it is appropriate to present these financial statements on a going concern basis.

p a GartsideChairman of the Audit Committee7 June 2010

www.titaneurope.com Stock code: AIM: TSW.L

31

our business

17643 25/05/10 Proof6

Corporate Governance StatementIndependent Auditors’ Report

www.titaneurope.com Stock code: AIM: TSW.L

31

GoVernance

iNDepeNDeNT auDiToRs’ RepoRT To The MeMbeRs of TiTaN euRope plcWe have audited the Group financial statements of Titan Europe Plc for the year ended 31 December 2009 which comprise the Consolidated Income Statement, the Consolidated Statement of Comprehensive Income, the Consolidated Balance Sheet, the Consolidated Statement of Changes in Equity, the Consolidated Cash Flow Statement, and the Reconciliation of Cash Flow to Net Debt and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and International Financial Reporting Standards (IFRSs) as adopted by the European Union.

We have reported separately on the Company financial statements of Titan Europe Plc for the year ended 31 December 2009.

RespeCTive RespoNsibiLiTies of DiReCToRs aND auDiToRs

As explained more fully in the directors’ responsibilities statement, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit the Group financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

This report, including the opinions, has been prepared for and only for the Company’s members as a body in accordance with Chapter 3 of Part 16 of the Companies Act 2006 and for no other purpose. We do not, in giving this opinion, accept or assume responsibility for any other purpose or to any other person to whom this report is shown or into whose hands it may come save where expressly agreed by our prior consent in writing.

sCope of The auDiT of The fiNaNCiaL sTaTeMeNTs

An audit includes obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Group’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and overall presentation of the financial statements.

opiNioN oN fiNaNCiaL sTaTeMeNTs

In our opinion the Group financial statements:

●● give a true and fair view of the state of the Group’s affairs as at 31 December 2009 and of its loss and cash flows for the year then ended;

●● have been properly prepared in accordance with IFRSs as adopted by the European Union; and

●● have been prepared in accordance with the requirements of the Companies Act 2006.

opiNioN oN oTheR MaTTeR pResCRibeD bY The CoMpaNies aCT 2006

In our opinion the information given in the Directors’ Report for the financial year for which the Group financial statements are prepared is consistent with the Group financial statements.

MaTTeRs oN whiCh we aRe ReQuiReD To RepoRT bY exCepTioN

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

●● certain disclosures of directors’ remuneration specified by law are not made; or

●● we have not received all the information and explanations we require for our audit.

oTheR MaTTeR