Page 1

TITLE :

ASSESSMENTS OF ACCOUNTING INFORMATIONS

RELEVANCE AND RELIABILITY OF A LISTED COMPANY

BETWEEN 2009 AND 2010

COURSE :

BBAW2130

FINANCIAL ACCOUNTING

NAME:

FADZLUL AKMAL BIN AHMAD FISOL

MATRIC NO.:

860104025713001

NIRC: 860104-02-5713

TELEPHONE NO.:

016-806 8177

TUTOR:

FUJIAH BINTI KASSIM

([email protected] )

012-824 5188

SEMESTER 3/JANUARY 2012

Page 2

APPENDIX

1.0 INTRODUCTION

1.1 Objectives of Assignment

1.2 Introducing Dutch Lady

1.3 Products

2.0 QUALITATIVE CHARACTERISTICS OF ACCOUNTING INFORMATION

2.1 Primary Qualitative of Accounting Information

2.1.1 Relevant

2.1.2 Reliability

2.2 Secondary Qualitative of Accounting Information

2.2.1 Comparability

2.2.2 Consistency

3.0 FINANCIAL STATEMENT ANALYSIS

3.1 Basis of Comparison

3.2 Techniques of Analysis

3.3 Calculation Formulae for Horizontal Analysis for 2 Years

3.4 Examples of Calculation

3.5 Specimen of Assignments

4.0 FINANCIAL STATEMENTS OF DUTCH LADY MILK INDUTSRIES

4.1 Balance Sheet

4.2 Income Statement

4.3 Statement of Changes in Equity

4.4 Statement of Cash Flow

5.0 NOTES TO FINANCIAL STATEMENT

5.1 Basis of Preparation

5.1.1 Statement of Compliance

5.1.2 Basis of Measurement

5.1.3 Functional and Presentation of Currency

5.1.4 Use of Estimates and Judgements

5.2 Significant Account Policies

5.2.1 Foreign Currency Transactions

5.2.2 Loans and Receivables

5.2.3 Cash Flow Hedge

5.2.4 De-recognition

5.2.5 Depreciation

5.2.6 Other Intangible Assets

5.2.7 Subsequent Expenditure

5.2.8 Amortisation

5.2.9 Inventories

5.2.10 Receivables

5.2.11 Cash and cash equivalents

Page 3

1.0 INTRODUCTION

Dutch Lady Milk Industries Berhad is one of among outstanding listed

company in Malaysian Stock Exchange (Bursa Saham Malaysia). Therefore, choosing

this company would be definitive example of successful listed company over years,

which suit as specimen for this assignment.

1.1 Objectives of Assignment

The purpose of this assignment is to compare and assess the primary

qualitative characteristics of accounting information of chosen listed

company’s financial statement between year 2009 and 2010. As listed

company would disclose their financial report annually for public assessment

via its prospects, web page or stock exchange web page, it ease shareholders

or investor or anyone whom interested or planning to invest in this to give a

look at the company’s performance in terms of profit and current financial

progress.

1.2 Introducing Dutch Lady (History and Formation)

After World War II, sweetened condensed milk was imported

wholesale from its origin company in Holland (Dutch) via local importers and

wholesalers. In 1954, a trading company Friesland (Malaya) Pte. Ltd., based

in Singapore, was formed to market Holland’s sweetened condensed milk in

Malaya and Singapore. Among several brands was a certain Dutch Baby

brand.

In 1965, formed as Dutch Pacific Milk Industries (Malaya), the

company established its first factory and started to manufacture condensed

milk. Three years later, Dutch Pacific Milk Industries (Malaya) was converted

into public company and became the first milk company to be listed on Stock

Exchange of Kuala Lumpur and Singapore. Later in year 2000, the company

changed its name again to Dutch Lady Milk Industries Berhad thus listed in

Malaysian Stock Exchange (Bursa Saham Malaysia).

Page 4

1.3 Products

Dutch Lady Milk Industries Berhad is well known for nutritious milk

products. Other than that, the company offers yogurt, fruit juices (under the

brand JOY), growing milk for baby and still dairy milk. For generations, the

company supply quality dairy and infant nutrition products to the nation.

Today, Dutch Lady Malaysia ranks as the leading dairy producer in Malaysia

While Dutch Lady Malaysia first established itself as a manufacturer

of sweetened condensed milk, Dutch Lady Milk Industries Berhad’s extensive

product range now spans from infant formula and growing up milk to fruit

juice and yoghurt snacks. Every product innovation in our rapidly developing

infant and child formula range is backed by extensive research both locally

and internationally.

Page 5

2.0 QUALITATIVE CHARASTERISTICS OF ACCOUNTING INFORMATION

Qualitative characteristics can be best explained as characteristics that must be

present and contrast in the accounting information to make it useful. In other words,

qualitative characteristics not only about showing figure in accounting format but

measurement of profit or loss, cash flows, equity owned and shareholders as well as

dividend given annually. For example, Dutch Lady Milk Industries Berhad has shown

their accounting or financial report via web page, which is useful for internal and

external users to refer and to take a look around for business and investment purposes.

Means, the company’s financial report can be an advantage to captivate investor’s

interest. These characteristics are divided into 2 categories;

2.1 Primary Qualities of Accounting Information

Primary quality of accounting information is basis quality that must be

present in a financial report. It consists of 2 aspects;

2.1.1 Relevant

In accounting, relevant is described as something that makes a

difference in reaching a decision. It has a strength or complication that

may influence or affects the decision being made. For example, new

projects or products of a company within five years may derived from

its performance and profitability figure, thus shows a company’s

progress and these details will be shown in financial report. Thus,

whether a company’s financial account shows profit or negative profit,

it might influence the investor’s decision.

To become relevant, the information must have feedback value,

forecast value and timeliness. These means the relevancy must be able

to assist users in correcting early expectations, be able to assist users in

forecasting and it must be obtained before it becomes obsolete.

Page 6

2.1.2 Reliability

Reliability means users can rely or depend on specific

information to make good decisions. Average users might not have the

time or expertise to evaluate some information. Therefore, users

simply depend on information issued by official entity or the company

itself, then that information is reliable in decision making. For

example, an investor may simply take a look of Dutch Lady’s annual

financial report via official web page to learn about Dutch Lady’s

performance.

2.2 Secondary Qualities of Accounting Information

Secondary qualities of accounting information can be supporting element of

qualitative characteristics. These elements may extend the advantage of benefits that

can be obtained through accounting information. Secondary qualities of qualitative

characteristics can be divided into 2 categories;

2.2.1 Comparability

Comparability means the information can be compared whether

among companies, industries, or the company’s performance itself for

different periods. This will enable users to identify similarities or

differences that could exist through accounting information. For

example, an investor may compare Dutch Lady’s profit between year

2010 and 2011. If profit obtained in 2010 was RM 14 millions and

profit obtained in 2011 was RM 15.8 millions, it shows the increase

profit of RM 1.8 millions. Therefore, that comparison shows increase

of profit in these 2 years.

Let say if an investor study the financial report of a rival

company to Dutch Lady. If in 2010 that company obtained RM 10

Page 7

millions of profit and in 2011 it obtained RM 11 millions of profit, it

can be said Dutch Lady has performed much better in terms of profit

because the rival company unable to compete with Dutch Lady in

terms of dividend sharing. Plus, the increase of profit is still slow thus

assuming that the rival company’s performance is least interesting.

2.2.2 Consistency

Consistency means an entity or company must use the same

accounting procedures or method in every period for the purpose of

enabling comparison to be made more effectively. If a company wants

to change the accounting method, then the company must make

complete disclosure in the financial report to explain why changes are

made and the effect of the changes towards the financial report.

Page 8

3.0 FINANCIAL STATEMENT ANALYSIS

The main function or purpose of financial statement analysis is to assist users

make better decisions via detailed comprehension or contrast quick look upon

financial report, whether for internal or external users of the company concerned.

Internal users of accounting information are individuals involved in the

management and operations of the organization. They include auditors, accountants,

consultants and parties involved in decision making process. In other hand, internal

users are responsible for planning strategies for company profitable progress. The

purpose of financial analysis is to provide them adequate information in order to

improve efficiency and effectiveness in producing goods or services.

External users of accounting information are not directly involved in the

operation of the organization. They comprise shareholders, creditors, non-executive

directors, investor and suppliers.

3.1 Basis of Comparison

In this assignment, basis of comparison used to compare or measure

Dutch Lady’s performance is by using intra-company or within the company

basis. By using this basis, the company will compare the figure and items in its

financial statements relating to 3 different years or more. The comparison of

current year’s financial statement with previous years will show and indicate a

company’s profit or loss, as well as trend used for future prediction.

3.2 Techniques of Analysis

Horizontal analysis is normally used for comparison within the company. It is

a technique used to assess the trend of the items in the financial statement in

terms of amount or percentage of fluctuation. In this assignment, the

comparison is made on every item in the financial statement for two years or

two accounting period. The basis of comparison consists of current year and

previous year will be set by using the financial statement of the previous year

as the base to determine an increase or decrease.

Page 9

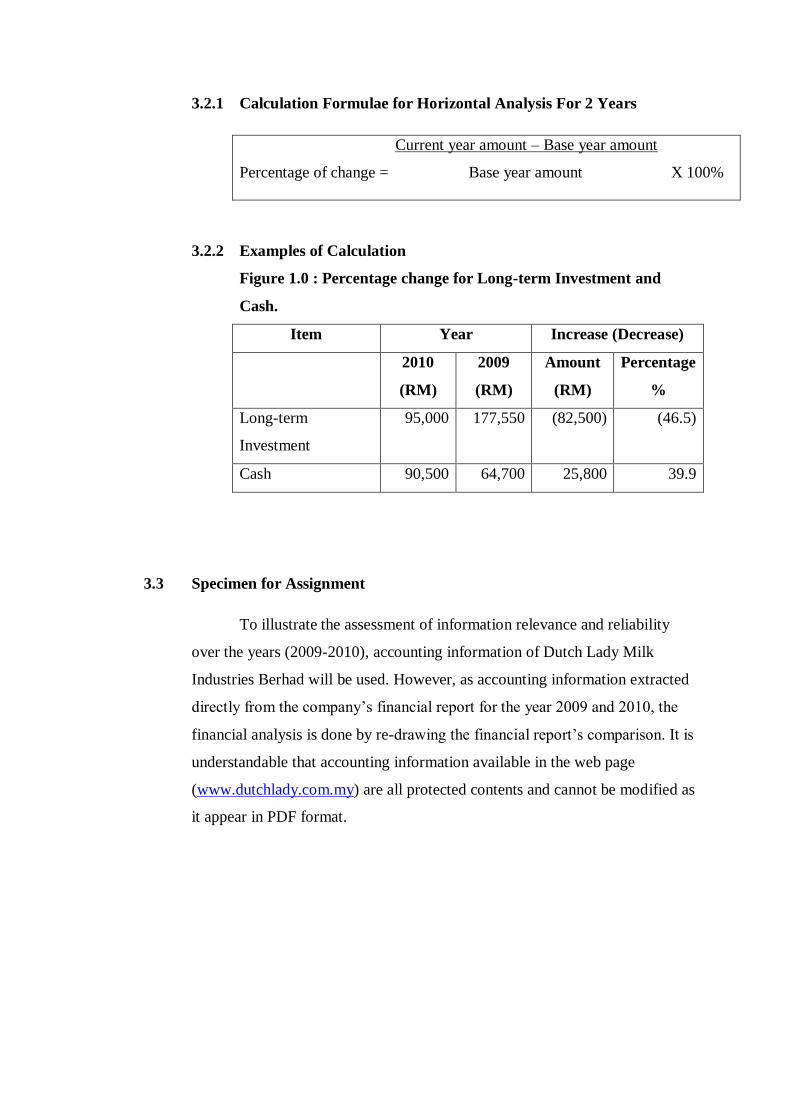

3.2.1 Calculation Formulae for Horizontal Analysis For 2 Years

Current year amount – Base year amount

Percentage of change = Base year amount X 100%

3.2.2 Examples of Calculation

Figure 1.0 : Percentage change for Long-term Investment and

Cash.

Item Year Increase (Decrease)

2010

(RM)

2009

(RM)

Amount

(RM)

Percentage

%

Long-term

Investment

95,000 177,550 (82,500) (46.5)

Cash 90,500 64,700 25,800 39.9

3.3 Specimen for Assignment

To illustrate the assessment of information relevance and reliability

over the years (2009-2010), accounting information of Dutch Lady Milk

Industries Berhad will be used. However, as accounting information extracted

directly from the company’s financial report for the year 2009 and 2010, the

financial analysis is done by re-drawing the financial report’s comparison. It is

understandable that accounting information available in the web page

(www.dutchlady.com.my) are all protected contents and cannot be modified as

it appear in PDF format.

Page 10

4.0 FINANCIAL STATEMENT OF DUTCH LADY MILK INDUSTRIES

4.1 Balance Sheet

Dutch Lady Milk Industries Berhad

Comparison Balance Sheet

As at 31 December 2010 and 2009

2010 2009

(RM’000) (RM’000)

Increase (Decrease)

Amount

(RM’000)

Percentag

e (%)

ASSETS

Property, plant & equipment

Intangible Assets

69,803

3,443

82,327

4,879

(12,524)

(1,436)

(15.21%)

(29.43%)

TOTAL NON-CURRENT ASSETS

Inventories

Trade and other receivables

Prepayments

Cash and cash equivalents

73,246

87,206

(13,960)

(16.00%)

72,722

75,176

689

85,657

57552

94,369

131

41,732

15,170

19,193

558

43,925

26.36%

(20.34%)

425.95%

105.25%

TOTAL CURRENT ASSETS 234,244 193,784 40,460 20.88%

TOTAL ASSETS 307,490 280,990 26,500 9.43%

EQUITY

Share Capital

Retained Profit

64,000

133,472

64,000

115,985

-

17,487

-

15.08%

TOTAL EQUITY 197,472 179,985 14,487 9.72%

LIABILITIES

Deferred tax liabilities

3,757

4,150

(393)

9.47%

TOTAL NON-CURRENT

LIABILITIES

3,757

4,150

(393)

9.47%

Trade and other payables

Provision

Current tax liabilities

99,638

348

6,275

91,905

283

4,667

7,733

65

1,608

8.41%

22.97%

34.45%

TOTAL CURRENT LIABILITIES 106,261 96,855 9,406 9.71%

TOTAL LIABILITIES 110,018 101,005 8,963 8.87%

TOTAL EQUITY AND

LIABILITIES

307,490

280,990

26,500

9.43%

Page 11

4.2 Income Statement

Dutch Lady Milk Industries Berhad

Comparison Income Statement

For the Year Ended 31 December 2010 and 2009

2010 2009

( RM’000) (RM’000)

Increase (Decrease)

Amount

(RM’000)

Percentage

(%)

Revenue

Cost of sales

710,588

(447,961)

691,847

(462,510)

18,741

(14,549)

2.71%

(3.15%)

GROSS PROFIT 262,627 229,337 33,290 14.52%

Other Income

Distribution expenses

Administrative expenses

Other expenses

1,147

(106,091)

(22,657)

(45,805)

1,561

(98,697)

(19,048)

(31,122)

(414)

7,394

3,609

14,683

(26.52%)

7.49%

18.98%

47.18%

RESULT FROM OPERATING

EXPENSES

Interest Income

Finance Cost

89,221

883

-

82,031

451

(1)

7,190

432

(1)

8.76%

95.79%

(100%)

PROFIT BEFORE TAX

Income tax expenses 90,104

(26,217)

82,481

(22,801)

7,623

3,416

18.73%

18.73%

PROFIT FOR THE YEAR

OTHER COMPREHENSIVE

INCOME

63,887

-

60,400

-

3,487

-

5.77%

-

TOTAL COMPREHENSIVE

INCOME FOR THE

YEAR

63,887

60,400

3,487

5.77%

BASIC EARNINGS PER

ORDINARY SHARE (SEN)

99.80

94.40

5.40

5.72%

Page 12

4.3 Statement of Changes in Equity

Dutch Lady Milk Industries Berhad

Statement of Changes in Equity

For the year ended 31 December 2010

Attributable to owners of the company

Share

Capital

RM’000

Distributable

Retained

Profits

RM’000

Total

Equity

RM’000

AT 1 JANUARY 2009

Total comprehensive income for the year

Dividends to owners of the Company

64,000

-

-

97,585

60,400

(46,400)

161,585

63,887

(46,400)

AT DECEMBER 2009 /

1 JANUARY 2010

Total comprehensive income for the year

Dividends to owner of the Company

64,000

-

-

115,985

63,887

(46,400)

179,985

63,887

(46,400)

At 31 DECEMBER 2010 64,000 133,472 197,472

Page 13

4.4 Statement of Cash Flow

Dutch Lady Milk Industries Berhad

Comparison Statement of Cash Flow

For the year ended 31 December 2010 and 2009

2010

RM’000

2009

RM’000

Increase

(Decrease)

RM’000

Percentage

(%)

CASH FLOW FROM

OPERATING ACTIVITIES

Cash receipts from customers

And other receivables

Cash paid to suppliers and

employees

730,398

(607,007)

721,781

(612,482)

8,617

(5,457)

1.19%

0.895

CASH GENERATED

FROM OPERATIONS

Tax paid

123,391

(25,002)

109,299

(19,922)

14,092

5,080

1.29%

25.50%

NET CASH FROM

OPERATING ACTIVITIES

98,289

89,377

8,912

9.97%

CASH FLOWS FROM

INVESTING ACTIVITIES

Additions of property, plant

and equipment

Additions of intangible assets

Proceeds from disposal of

property, plant and equipment

Interest received

(9,089)

(136)

278

883

(29,285)

(607)

5

451

(20,196)

471

273

432

68.96%

77.59%

5,460%

95.79%

NET CASH USED IN

INVESTING ACTIVITIES

(8,064)

(29,436)

21,372

72.60%

CASH FLOW FROM

INVESTING ACTIVITIES

Interest paid

Dividends paid

-

(46,400)

(1)

(42,000)

(1)

4,400

(100%)

10.48%

NET CASH USED IN

FINANCING ACTIVITIES

Net increase in cash and cash

equivalents

Cash and cash equivalents

At 1 January

(46,400)

43,925

41,732

(42,001)

17,940

23,792

4,399

25,985

17,940

10.47%

144.84%

75.40%

CASH AND CASH

EQUIVALENTS AT

31 DECEMBER

85,657

41,732

43,925

105.25%

Page 14

i)Cash and cash equivalents

Cash and cash equivalents

included in the statement of

cash flow comprise the

following statement of final

position amounts:

Cash at band and on hand

Deposits placed with a

licensed bank

2010

RM’000

46,657

39,000

2009

RM’000

23,732

18,000

Increase

(Decrease)

RM’000

22,925

21,000

Percentage

(%)

96.60%

116.67%

85,657 41,732 43,925 105.25%

Page 15

5.0 NOTES TO FINANCIAL STATEMENT

Dutch Lady Milk Industries Berhad is a public limited liability company,

incorporated and centralized in Malaysia and is listed in Main Market of Bursa

Malaysia Securities Berhad. These financial statements were authorized for issue by

the Board of Directors on 24 February 2011.

5.1 Basis of Preparations

5.1.1 Statement of compliance

The financial statements of the company have been prepared in

accordance with Financial Reporting Standards (FRSs), generally accepted

accounting principles and the Companies Act, 1965 in Malaysia.

5.1.2 Basis of measurement

The financial statements have been prepared based on the

historical cost basis except as disclosed in the notes to the financial

statement.

5.1.3 Functional and presentation of currency

These financial statements are presented in Ringgit Malaysia

(RM), which is the company’s functional currency. All financial

information is presented in RM and has been rounded to the nearest

thousand, unless otherwise stated.

5.1.4 Use of estimates and judgements

The preparation of the financial statements in conformity with

FRSs requires managements to make judgements, estimates and

assumptions that affect the application of accounting policies and the

reported amount of assets, liabilities, income and expenses. Actual

results may differ from these estimates.

Page 16

Estimates and underlying assumptions are reviewed on an

ongoing basis. Revisions to accounting estimates are recognized in the

period in which the estimates are revised and in any future periods

affected.

5.2 Significant Account Policies

The accounting policies set out above have been applied consistently to the

periods presented in concerned financial statements and have been applied

consistently by the company.

5.2.1 Foreign Currency Transactions

Transactions in foreign currencies are translated to the

functional currency of the company at exchange rates at the date of

transactions.

Monetary assets and liabilities dominated in foreign currencies

at reporting period are retranslated to the functional currency at the

exchange rate at that date.

Non-monetary assets and liabilities denominated in foreign

currencies are not translated at the end of the reporting date except for

any transaction that are measured at fair value.

Foreign currency differences arising on retranslation are

recognized in profit or loss.

5.2.2 Loans and receivables

Loans and receivables category comprises trade and other

receivables and cash and cash equivalent. Financial assets categorized

as loans and receivables are subsequently measured at amortised cost

using the effective interest method.

Page 17

5.2.3 Cash Flow Hedge

A cash flow hedge is a hedge of the exposure to variability in

cash flows that is attributable to a particular risk associated with a

recognized asset or liability or a highly profable forecast transaction

and could affect the profit or loss.

Cash flow hedge accounting is discontinued prospectively

when the hedging instrument expires or being sold, terminated or

exercised, the hedge is no longer highly effective, the forecast

transaction is no longer expected to occur or the hedge designation is

revoked.

5.2.4 De-recognition

A financial assets or part of it is derecognized when, and only

when, the contractual rights to the cash flows from the financial asset

expire or the financial assets is transferred to another party without

retaining control or substantially all risks and rewards of the assets.

A financial liability or part of it is derecognized when, and only

when, the obligation specified in the contract is discharged or

cancelled or expires. On de-recognition of a financial liability, the

difference between the carrying amount of the financial liability

extinguished or transferred to another party and the consideration paid,

including any non-cash assets transferred or liabilities assumed, is

recognized in the profit or loss.

5.2.5 Depreciation

Depreciation is calculated over the depreciable amount, which

is the cost of an asset, or other substituted for cost, less its residual

value.

Depreciation is recognized in profit or loss on a straight-line

basis over the estimated useful lives of each part of an item of

Page 18

property, plant and equipment. Property, plant and equipment under

construction are not depreciated until the assets are ready for their

intended use.

Depreciation methods, useful lives and residual values are

reviewed, and adjusted as appropriate at end of the reporting period.

5.2.6 Other Intangible Assets

Costs that are directly associated with identifiable computer

software and that will probably generate economic benefits exceeding

cost beyond one year or cost savings to the company, and are not

intergrate with any other equipment are recognized as intangible assets.

5.2.7 Subsequent Expenditure

Subsequent expenditure is capitalized only when it increases

the future economic benefits embodied in the specific assets to which it

relates. All other expenditure is recognized in profit or loss as incurred.

5.2.8 Amortisation

Other intangible assets are amortised from the date they are

available for use. Amortization is recognized in profit or loss on a

straight-line basis over estimated useful lives of intangible assets.

Amortization methods, useful lives and residual values are reviewed at

the end of each reporting period and adjusted, whenever appropriate.

5.2.9 Inventories

Inventories are measured at the lower of cost and net realizable

value. The cost of inventories is measured based on first-in-first-out

principle and includes expenditure incurred in acquiring the

inventories, production or conversion costs incurred in bringing them

to their existing location. In the case of finished goods, cost includes an

appropriate share of production overheads based on normal operating

capacity.

Page 19

5.2.10 Receivables

Trade and other receivables are categorized and measured as

loans and receivables.

5.2.11 Cash and cash equivalents

Cash and cash equivalents consist of cash in hand, balances and

deposits placed with a licensed bank. They are categorized and

measured as loans and receivables.

6.0 CONCLUSION

Based on the financial statement above, all the transactions recorded in that

financial statement consisting every aspects and characteristics which necessary to be

appear in accounting information. As a financial statement that would be reported and

announced or published annually, Dutch Lady Milk Industries Berhad clearly shows

that their annual financial report was prepared based on standard procedures

accordance to specific accounting policies.

To become relevant, the information must have three characteristics, namely

feedback value, forecast value and timeliness. The company’s annual reports are

absolutely able to assist internal and external users in substantiating and correcting

early expectation matters at hand, thus injecting appropriate perspective over

concerned progress of any profit-based organization. As the company’s progress

seemed able to be forecasted, a report’s forecast value supposed to be outstanding and

timeliness value strengthened users intention to invest as financial report will be

issued annually.

To become reliable, the company’s financial report can be considered as

public-friendly report which it is published via website and in some cases, newspaper

or business magazines. The company’s financial report can be verified by anyone

Page 20

whom using the same method of accounting and it is presented according the actual

result of economic activities using specific methods.

Other than that, as the company’s financial reports are issued annually, users

may view or verify all of financial statements and its results consisting profit or loss

indications, where all relevant information can be used as comparison between years

of financial report. For example, by using horizontal analysis method, comparison of

two year’s financial statement can be done via specific method of calculation.

Therefore, comparability is clearly seen.

Last but not least, Dutch Lady Milk Industries Berhad strongly presenting

consistency in their financial account report by applying the same procedures and

policies in line to enable constant comparison to be made effectively. Changes might

be made but complete disclosure will be made to explain users about the changes and

why it has to be made.

In conclusion, as an established company, and moreover, the first milk

company in Malaysia, Dutch Lady Milk Industries Berhad succeed in maintaining the

status as being stable and keep listed in Malaysian Stock Exchange for decades. Years

by years, the company has successfully gaining investor’s trust regarding their

profitable progress over any economic condition to keep going. Every annual report

shall bringing good news to their shareholders, investors and public users themselves

due to increasing profit that are to be shared.

Page 21

7.0 REFERENCE

7.1 http://www.quickmba.com/accounting/fin/

7.2 http://en.wikipedia.org/wiki/Financial_accountancy

7.3 http://www.investopedia.com/terms/f/financialaccounting.asp

7.4 http://www.dutchlady.com.my

7.5 http://www.bursamalaysia.com

7.6 http://www.slideshare.net/amarhindu/comparison-of-accounting-

standards-presentation