25

PRESENTATION 2: TERMS AND CONCEPTS

| Date post: | 18-Aug-2015 |

| Category: |

Education |

| Upload: | careers-australia |

| View: | 21 times |

| Download: | 1 times |

PRESENTATION 2: TERMS AND CONCEPTS

PRESENTATION 2 OUTLINE

The following areas are covered in this presentation:

• Types of Business Structures

• Business Categories

• Accounting Terms and Concepts

• Accounting Reports

• Chart of Accounts

• Double Entry Accounting

• Depreciation

TYPES OF BUSINESS STRUCTURES

Sole traders (or sole proprietorships)

Owned and controlled by one person

Sole owner provides all capital for the business and in turn receives all profit

made.

Advantage: simplicity

Disadvantage: no limit to the owner’s liability

Have limited ability to raise finance, as they are usually the sole source of funds

and working capital.

TYPES OF BUSINESS STRUCTURES

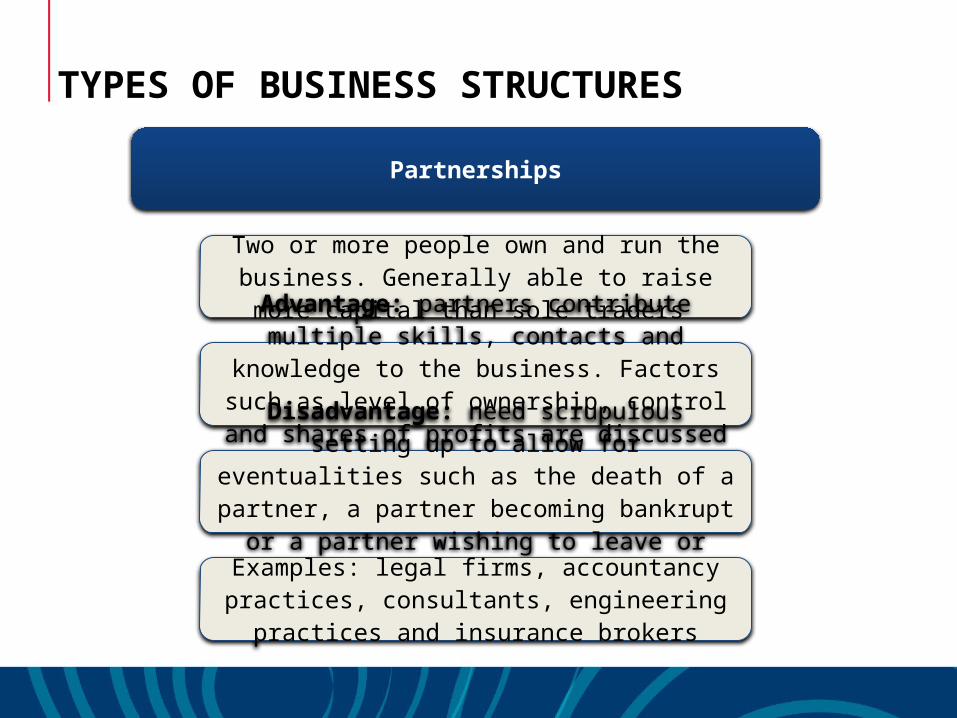

Partnerships

Two or more people own and run the business. Generally able to raise more

capital than sole traders Advantage: partners contribute multiple

skills, contacts and knowledge to the business. Factors such as level of

ownership, control and shares of profits are discussed and decided upon by partnersDisadvantage: need scrupulous setting up to allow for eventualities such as the death of a partner, a partner becoming

bankrupt or a partner wishing to leave or retire

Examples: legal firms, accountancy practices, consultants, engineering

practices and insurance brokers

TYPES OF BUSINESS STRUCTURES

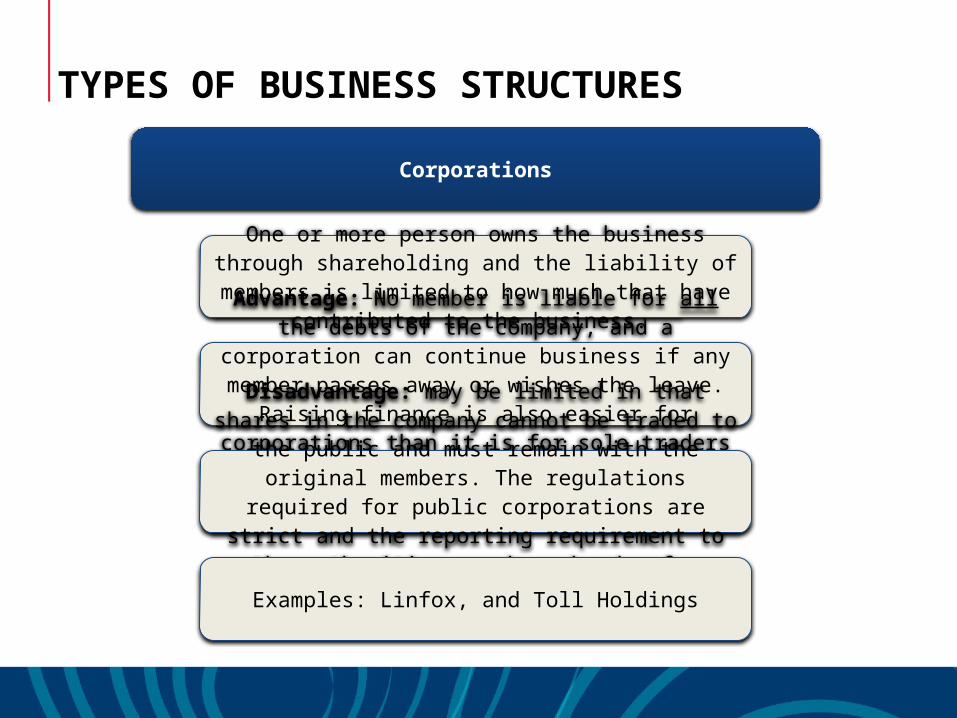

Corporations

One or more person owns the business through shareholding and the liability of members is

limited to how much that have contributed to the business. Advantage: No member is liable for all the

debts of the company, and a corporation can continue business if any member passes away

or wishes the leave. Raising finance is also easier for corporations than it is for sole traders

and partnerships.Disadvantage: may be limited in that shares in the company cannot be traded to the public and

must remain with the original members. The regulations required for public corporations are

strict and the reporting requirement to the authorities can be a burden for smaller public

companies.

Examples: Linfox, and Toll Holdings

BUSINESS CATEGORIES

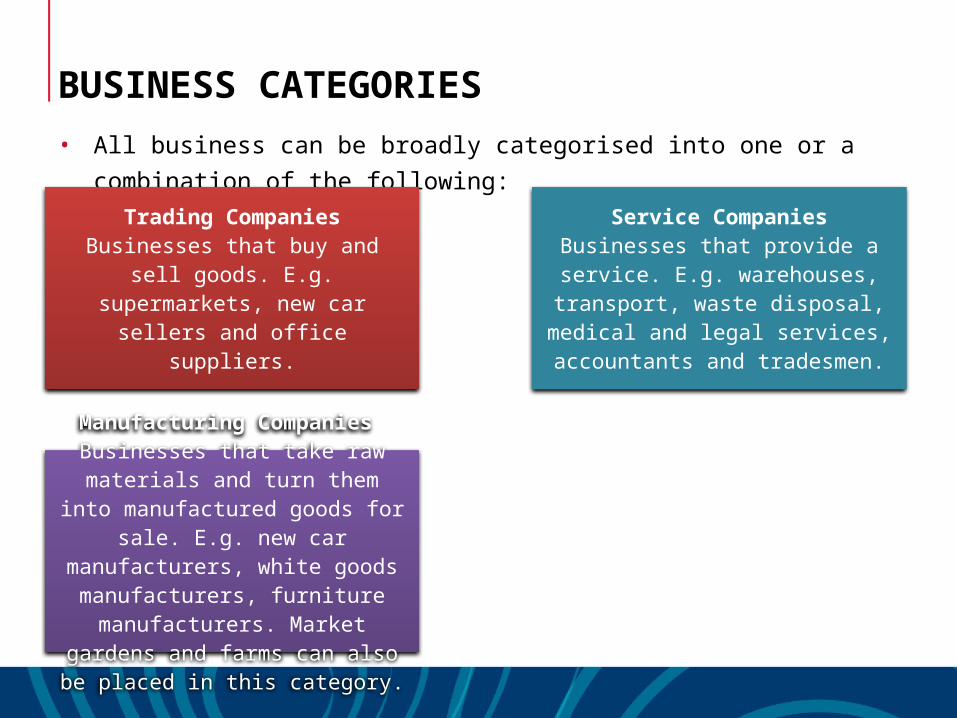

• All business can be broadly categorised into one or a combination

of the following:

Trading CompaniesBusinesses that buy and sell

goods. E.g. supermarkets, new car sellers and office suppliers.

Service CompaniesBusinesses that provide a service. E.g. warehouses, transport, waste disposal,

medical and legal services, accountants and tradesmen.

Manufacturing Companies Businesses that take raw

materials and turn them into manufactured goods for sale. E.g. new car manufacturers, white goods manufacturers,

furniture manufacturers. Market gardens and farms can also be

placed in this category.

ACCOUNTING TERMS AND CONCEPTS

• All organisations, regardless of type or size, adopt a standard

accounting process. This can be simplified by the accounting

equation:

OR

Assets = Liabilities + Owner’s Equity

Owner’s Equity = Assets – Liabilities

ACCOUNTING TERMS AND CONCEPTS

Assets are what a business owns. They are classified into two areas:

Current AssetsCash and other assets that can be easily converted into cash

within a short period (such as 12 months). E.g. stock, debtors (customers owing money)

Non-Current AssetsLong life items such as property, machinery and equipment. They won’t be consumed during the

current accounting term and are acquired with the intent to be

used in business for a long period. These are also known as fixed assets or long-term assets.

ACCOUNTING TERMS AND CONCEPTS

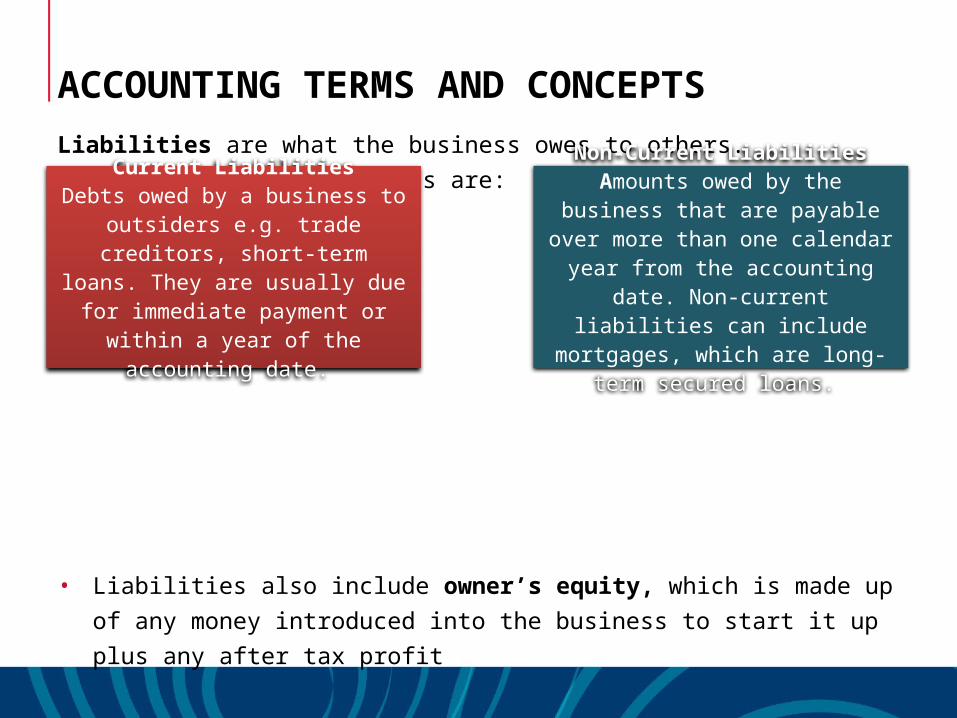

Liabilities are what the business owes to others. Subdivisions of

liabilities are:

• Liabilities also include owner’s equity, which is made up of any

money introduced into the business to start it up plus any after

tax profit

Current LiabilitiesDebts owed by a business to outsiders e.g. trade creditors,

short-term loans. They are usually due for immediate

payment or within a year of the accounting date.

Non-Current LiabilitiesAmounts owed by the business that are payable over more than

one calendar year from the accounting date. Non-current

liabilities can include mortgages, which are long-term secured

loans.

ACCOUNTING TERMS AND CONCEPTS

There are a number of types of profit to be aware of:

Gross ProfitThe difference between sales revenue and the cost of the

good sold

Net ProfitThe excess of revenue over both the cost of sales and other expenses. If cost of sales and expenses are

greater than sales than it is a net loss, which decreases

owner’s equity as opposed to increasing it

ACCOUNTING TERMS AND CONCEPTS

Accountants sometimes differentiate between costs and expenses.

• The two terms are often interchangeable, but it is best to be aware

of the difference. CostsDefined as a sacrifice of cash

assets to purchase something that enables a sale or to make something

else. E.g. raw materials would be considered a cost

as these are used to produce something that is sold.

ExpensesDefined as a reduction in

owner’s equity that is used to produce a service or

manufactured good. The expense is the cost of doing

your business. E.g. fixed expenses such as rent,

power, and salaries.

ACCOUNTING REPORTS

• There are three main reports that are used to prepare a budget

and to ascertain the health of a business. These are:

1. Profit and Loss Statement

2. Balance Sheet

3. Cash Flow Statement

• Sometimes a report called the aged trial balance is included

with these three.

• These three reports are also referred to as the company’s financial

reports. Reading them and having a basic understanding of what

they contain is important if budgets are to be prepared accurately.

CHART OF ACCOUNTS

• In the chart of accounts a business’s various accounts are given

numbers to aid in referencing and facilitate processing. Accounting

data is collected and classified or coded into one of the following

categories:

Assets 1.000

Liabilities 2.000

Owner’s Equity 3.000

Income 4.000

Cost of Sales 5.000

Expenses 6.000

Other Income 7.000

CHART OF ACCOUNTS• This coding system is not universal, it is up to companies what

system they choose to use.

• Within each category or account further categorisation is made and

numbered.

• All accounts that have the number 1.XXX are asset accounts and all

accounts starting with a 6 are expense accounts.

• For example, with an expenses account you might have 6.001 as rent

and 6.002 as electricity. Whereas in the assets account you might

have 1.001 assigned to a truck.

• Liabilities can be further divided into current and non-current

liabilities but will still have account numbers beginning with 2.

• Similarly with assets, account numbers will still start with 1. For

example 1.100 would be current assets while 1.200 would be non-

current assets.

CHART OF ACCOUNTS

Example

Current Assets 1.100

Cash at bank 1.110

Accounts receivable

1.111

Petty Cash 1.112

Stock 1.120

GST input credit 1.115

Other Income 7.000

Non-Current Assets 1.200

Plant and equipment 1.201

Less depreciation 1.202

Motor vehicle –Hino 1.230

Less depreciation 1.231

Motor vehicle – Toyota 1.240

Less depreciation 1.241

Office equipment 1.270

Less depreciation 1.271

CHART OF ACCOUNTS

• The Other Income category is for income from bank interest or

interest-bearing investments. It is income not derived from selling

a product or service. A tax return would fit into this category.

• Every company will have their own chart of accounts specific for

them. A farm for example will have sales revenue from crops or

livestock or stud fees, expenses from fending, feed, veterinary

bills etc.

• Any expense, revenue, cost of business or income stream can be

given or assigned into one of the seven main account codes, then

further divided into an account code within that main category.

DOUBLE ENTRY ACCOUNTING

• System of recording financial transactions.

• When a debit is made to one account, a corresponding credit must

occur on an opposing account.

Example

• Buying a newspaper adds an asset, which is a debit account, and

the cost is taken from cash reserves and becomes a credit account

(an expense).

• Another way of looking at it is to debit the account that

receives and credit the account that gives.

• The newspaper example debits the account that receives (i.e. the

asset account) and credits the account that gives (i.e. the expense

account).

DOUBLE ENTRY ACCOUNTING• Each accounting transaction affects at least two accounts. One account is

debited with an amount and one or more accounts are credited with an equal

amount, and vice versa.

• In the following examples note how the DR (debit accounts) equal the credit

accounts (CR) for each transaction.

Example 1

• On 1st June, 2015, SJC Logistics Logistics purchased a second-hand vehicle

from Great Western Motors for $11,000 (GST inclusive) on credit.

• The chart of accounts number will be 1.230 as it is a motor vehicle and a non-

current asset, with a value of $10,000.

• The GST input credit of $1000 is a CR, credit account liability code for the GST

will be 2.115. The liability account has a $10,000 entry with the code 2.300

(credit) has a $10,000 entry. So the total DR amount is now balanced by a CR

amount of $11,000. This is presented in the table in the following slide

DOUBLE ENTRY ACCOUNTING

Example 1

Example 2

• SJC Logistics receives bank interest of $1000. The DR entry is for

code 1.100, which is cash at bank. The CR code is 7.100, revenue

from interest.

Date Transaction Accounts Type Nature Account Codes

DR/CR $

1/6 Purchased second-hand vehicle from Great Western Motors for $11,000 on credit (GST included)

Motor Vehicles

AssetLiability

Liability

DebitCredit

Credit

1.2301.115

2.115

DRDR

CR

10 0001 00011 000

DOUBLE ENTRY ACCOUNTING

Example 3

• SJC Logistics pays its rent of $2000. The DR code is rent 6.100 (an

expense code). The CR code is the cash at bank code 1.100.

Remember debit the receiver (the landlord getting the rent) credit

the giver (SJC Logistics Logistics)

• A trial balance will report the above transactions over any period

of time as total debits and total credits with the credit column

total exactly equal to the debit column total.

DOUBLE ENTRY ACCOUNTING• GST is levied on many sales items (exemptions include fresh food) and is

a tax paid by all purchasers, paid to the Australian Taxation Office (ATO)

• Its role in a chart of accounts is usually as a liability. When you make a

sale you will have to add 10%, the current GST rate, to the value of the

item sold. The purchaser pays for the items with the 10% GST. This

amount will be recorded in the accounts as a liability, as it has to be

remitted to the ATO.

• GST you have paid when making purchases is credited against GST you

have raised from sales and the difference is paid at whatever period is

applicable.

• Large corporations collecting large amounts of GST pay weekly while

smaller businesses can pay either quarterly or annually; it all depends on

the business’ turnover. GST is a tax collected on behalf of the

government by consumers. GST really plays little role in budgeting, as it

is money passing through the company on its journey to the ATO.

DEPRECIATION

• The loss in the value of assets

• Considered a legitimate expense to the business.

• Methods of calculating depreciation include an agreed rate

applied, (for computers for example it is five years or 20%) to the

purchase price of the asset. This is the straight-line approach.

For example:

If a computer worth $1000 is depreciated at 20% per annum, it means that the computer loses $200 in value every year. At the end of five years, the value of this asset will be zero.

Depreciation can be calculated at any time before the period is up

For this computer, after 2 years the accumulated depreciation is:

2 x $200 = $400

DEPRECIATION

• Alternate methods of calculation include applying different rates

over different periods, and allowing for an asset to have some

value at the end of the depreciation period giving the asset what

is known as a right down value.

• For example for small businesses, for assets worth an excess of

$20,000, they can be pooled together and the lot depreciated by

15% in the first years and at 30% thereafter.

The timing of expenditure on a capital purchase, i.e. something large and expensive for which depreciation can be

claimed is important and can have an major effect on the budget

DEPRECIATION

• Phasing in simply means spreading an expense, if feasible, over

a broader time period or waiting for an opportune time to incur

the expense.

• Depreciation is subtracted as a separate operating expense from

the gross profit figure, on the profit and loss report. Tax is paid on

what is left so this is a definite consideration to the budget and

must be allowed for by any section of the workforce that has

budget items requiring expenditure during the year.

• Depreciation rates vary but can be as high as 20 to 25% per

annum depending on the type of assets. If this expenditure has

not been allowed for in the budget then the number of months

over which the extra expense is to be spread is an important

consideration with the timing of the asset purchase.

DEPRECIATION

Example

In SJC Logistics Logistics, it is decided to upgrade the pallet racking in the warehouse to enable an extra layer of storage from three high to four high. The cost of the new racking is $150,000.00. The racking can be depreciated over five years, which is a 20% (5 x 20 = 100) deduction rate.

So 20% of $150,000 is $30,000.

If the racking is purchased in July then each month for the rest of the financial year will have an expense of:

30,000/12 = $2,500

If the racking is purchased in June or May then the effect on the budget is only $5,000 for a May purchase or $2,500 for a purchase in June.

The next year’s budget can fully incorporate this added expense item during the budget preparation.