116

Topics and percentages

• 8-12% Basic Economic Concepts

• 12-16% Measurement of Economic Performance

• 10-15% National Income and Price Determination

• 15-20% Financial Sector

• 20-30% Inflation, Unemployment, and Stabilization Policies

• 5-10% Economic Growth and Productivity

• 10-15% Open Economy: International Trade and Finance

8-12% Basic Economic Concepts

A. Scarcity, choice, and opportunity costs

B. Production possibilities curve

C. Comparative advantage, absolute advantage,

specialization, and exchange

D. Demand, supply, and market equilibrium

E. Macroeconomic issues: business cycle, unemployment,

inflation, growth

Production Possibilities • Assumptions:

• Full Employment • Fixed Resources and Technology

• Movements • Along curve shows opportunity cost • Outward shift illustrates economic growth • Inward shift indicates destruction of resources

• Producing Capital Goods will lead to greater economic growth than producing consumer goods. (Butter will lead to more growth than guns)

Production Possibilities Graph

Capital

Goods

Consumer Goods

A

B

C

D

E

Points A,B,C, are efficient pts.

Point D is underutilization

Point E is economic growth

May Lead to most

Future growth

May Lead to most

Future economic growth

F.E. F.E.1

Supply and Demand Factors

• Demand Changes when:

• Income changes

• Related Products, complements and substitutes, (price or quality change)

• Expectations (future price change)

• Consumers (more or less added)

• Tastes, Fads, Preferences change

Demand Increase: As Demand Increases, Price and Quantity Increase as well.

P1

P2

Q1 Q2

S1

D1

D2

Price

Quantity

Demand Decrease: As Demand Decreases, Price and Quantity decrease as well

D1

D2

S1

P1

P2

Q1 Q2

Price

Quantity

Supply Factors

• Supply Changes When:

• Input prices change (resources and wages)

• Government (tariffs, quotas, and subsidies)

• Number of sellers change

• Expectations (about price and product profitability change)

• Disasters (weather, strikes, etc..)

Supply Increase: As Supply Increases, Quantity Increases, but Price Falls.

Price

Quantity Q1 Q2

P1

P2

S1

S2

D1

Supply Decrease: As Supply Decreases, Quantity Decreases, but Price Increases.

Price

Quantity

S1

S2

D1

P1

P2

Q1 Q2

Comparative Advantage • A nation should specialize in producing goods in which it

has a comparative advantage: ability to produce the good at a lower opportunity cost.

Example: Cheese Wine Spain: 2 pounds 2 Cases France 2 pounds 6 Cases Spain should produce cheese (1C = 1W) France should produce wine (1W = 1/3C) :

Currency Terms • Appreciation: Currency is increasing in

demand (stronger dollar)

• U.S. Currency will appreciate when more foreigners: travel to the U.S., buy more U.S. goods or services, or buy the U.S. dollar to invest in bonds

Currency Terms • Depreciation: Currency is decreasing in

demand (weaker dollar) Being SUPPLIED in exchange for other currency. • U.S. Currency will depreciate when fewer

foreigners: travel to the U.S., buy fewer U.S. goods or services, or sell the U.S. dollar to invest in their own bonds

15

Business Cycles • The increases and decreases in Real GDP

consisting of four phases:

• Peak: highest point of Real GDP

• Recession: Real GDP declining for 6 months

• Trough: lowest point of Real GDP

• Recovery: Real GDP increasing (trough to peak)

16

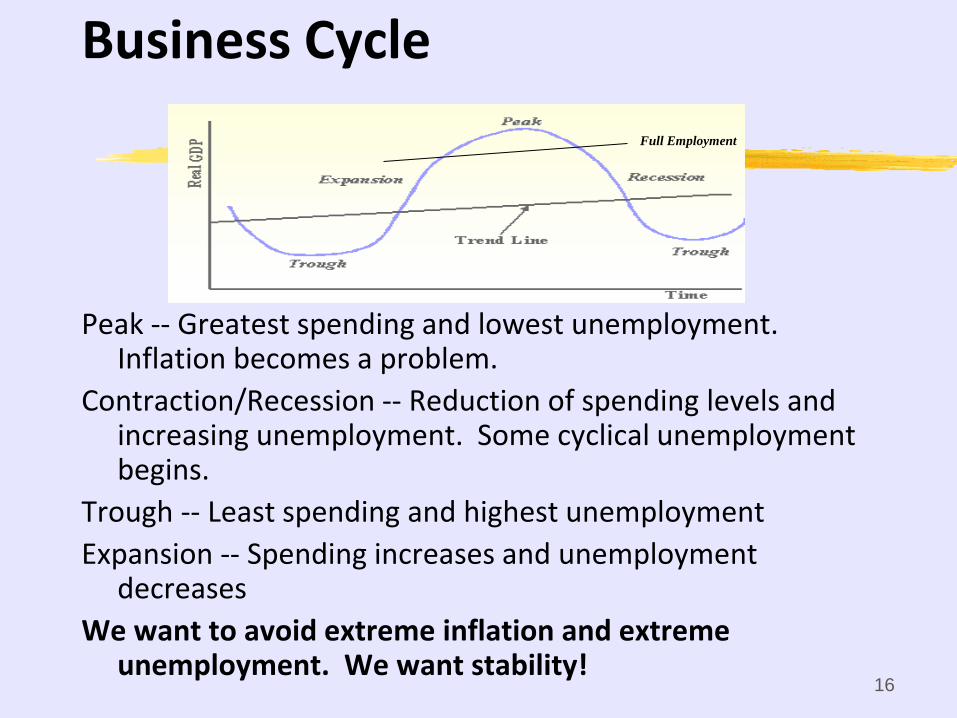

Business Cycle

Peak -- Greatest spending and lowest unemployment. Inflation becomes a problem.

Contraction/Recession -- Reduction of spending levels and increasing unemployment. Some cyclical unemployment begins.

Trough -- Least spending and highest unemployment

Expansion -- Spending increases and unemployment decreases

We want to avoid extreme inflation and extreme unemployment. We want stability!

Full Employment

17

The two big problems…

The two big problems that plague the economy are: INFLATION UNEMPLOYMENT • People generally prefer steady, stable growth to

large “ups” and “downs.” Therefore, government policies, both fiscal and monetary (see later sections), are aimed at flattening the business cycle.

• The government wants not only to stimulate the economy when it’s slow, but also to slow it down when it’s growing too quickly.

18

12-16% Measurement of Economic Performance

A. National income accounts

1. Circular flow

2. Gross domestic product

3. Components of gross domestic product

4. Real versus nominal gross domestic product

B. Inflation measurement and adjustment

1. Price indices

2. Nominal and real values

3. Costs of inflation

C. Unemployment

1. Definition and measurement

2. Types of unemployment

3. Natural rate of unemployment

Circular Flow of Economic Activity

• Households supply resources (land, labor, capital, entrepreneurial ability) to the resource market. Households demand goods and services from businesses.

• Businesses demand household resources and supply goods and services to the product (factor) market.

20

GDP (Gross Domestic Product): The total dollar (market)

value of all final goods and services produced in a given year.

Expenditure Formula: • Consumption (C) +

• Business Investment (I) +

• Government Spending (G) +

• Net Exports (Xn)

Gross Domestic Product

GDP: What Counts:

• Goods Produced but not Sold (I)

• Goods produced by a foreign country (Japan) in the U.S. (Honda, Toyota)

• Government spending on the military

• Increase in business inventories

GDP: What DOES NOT count:

• Intermediate Goods (Tires sold by Firestone to Ford)

• Used Goods

• Non-Market Activities (Illegal, Underground)

• Transfer Payments (Social Security)

• Stock Transactions

Shortcomings of GDP: Leading to GDP being

understated.

• Nonmarket activities: (services of homemakers) does not count.

• Leisure: Does not include the value of leisure.

• Does not include improvements in product quality.

• Underground economy

GDP: Overstated

• Includes damage to the environment

• Includes more spending on healthcare-Americans being unhealthy.

• Includes money spent to fight crime-more police officers, more jails, etc…

Real GDP • Real GDP= Nominal GDP adjusted for

inflation.

• Calculation: • Real GDP = Nominal GDP

Price Index ( deflator)

Example:

U.S. 2005 Real GDP= $12,4558 (billions)

113 (based on 2000)

$11.048 Trillion

Real GDP Per Capita

• Most commonly used to compare and measure each country’s standard of living and overall economic growth.

• Real GDP/Nation’s Population

28

Inflation

• Rise in the general level of prices

• Reduces the purchasing power of money

• Measured with the Consumer Price Index (CPI)

• Reports the price of a market basket , more than 300 goods that are typically purchased by an urban household

Calculating Inflation

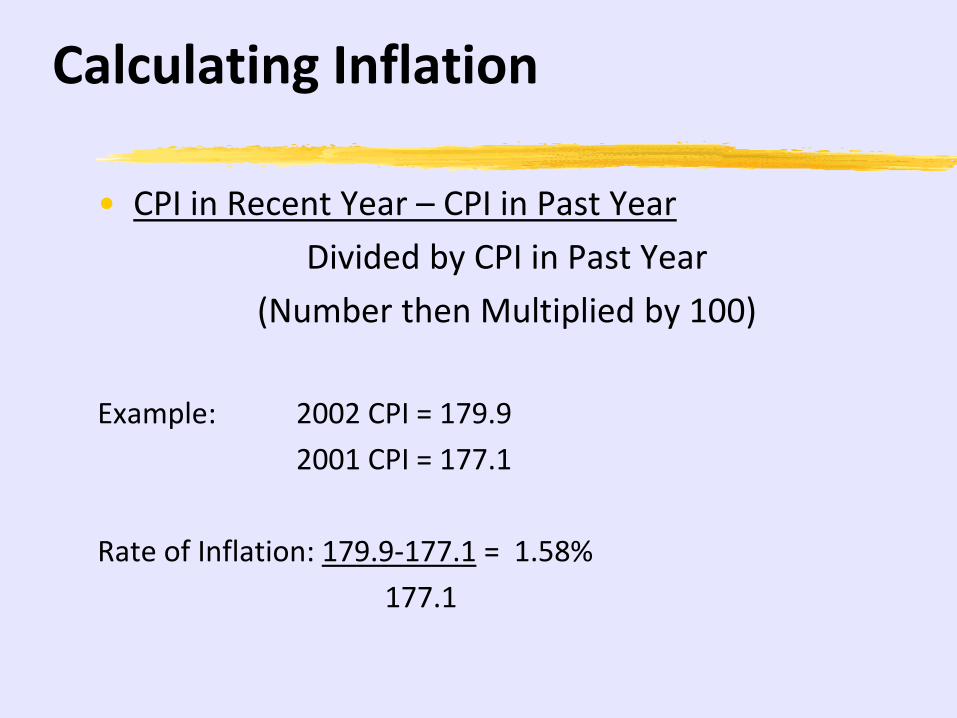

• CPI in Recent Year – CPI in Past Year

Divided by CPI in Past Year

(Number then Multiplied by 100)

Example: 2002 CPI = 179.9

2001 CPI = 177.1

Rate of Inflation: 179.9-177.1 = 1.58%

177.1

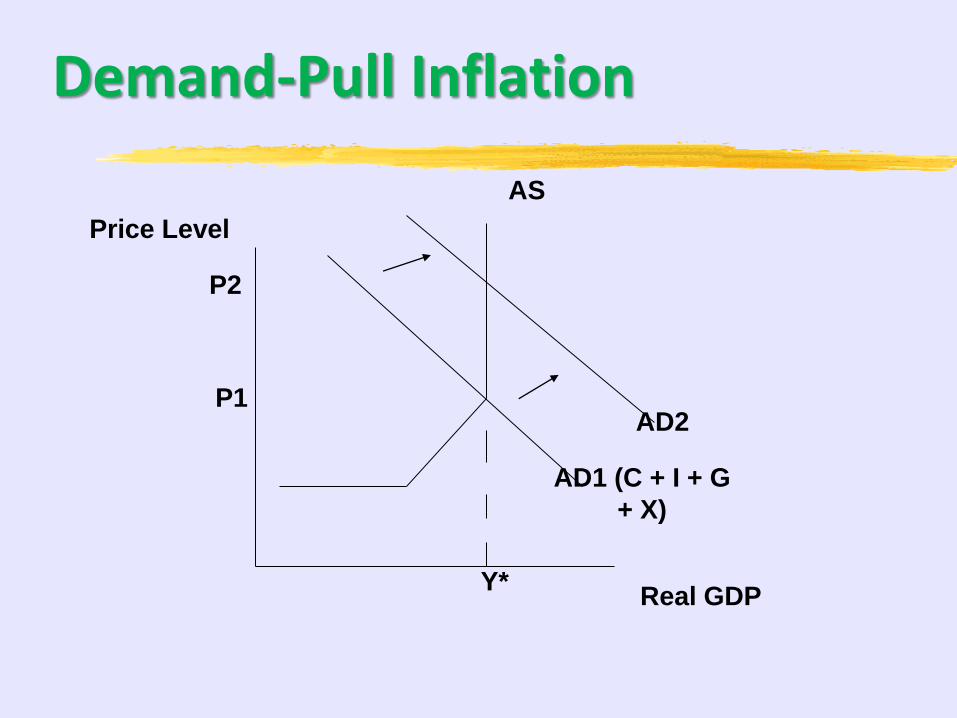

Types of Inflation

• Demand Pull Inflation: ‘too much money chasing too few goods.”

• AD Curve will shift to the right, resulting in a higher

Price Level and greater Output (until reaching Y*

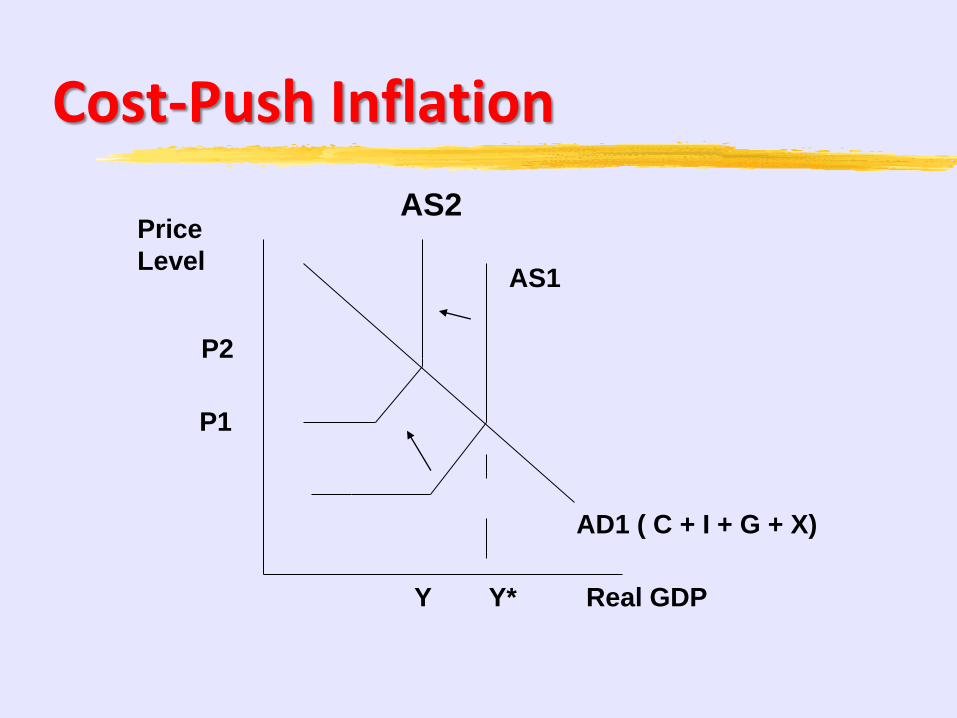

• Cost-Push Inflation: Major cause is a supply shock-OPEC cutting back on oil production

• AS Curve will shift to the left resulting in a higher Price

Level and a decrease in Real GDP.

Real and Nominal Terms

• Real Income = Nominal Income

Price Index (Hundredths)

• Real Interest Rate = Nominal Interest Rate – Inflation Rate

• Nominal Interest Rate = Real Interest Rate + Inflation Premium

(anticipated inflation)

Inflation: Winners & Losers

• Winners: • Debtors who borrow money that will be repaid with

“cheap” dollars. • Those who have anticipated inflation

• Losers: • Savers (especially savings accounts) • Creditors (Banks will be repaid with those “cheap”

dollars • Fixed-Income Recipients (retirees receiving the same

monthly pension)

33

Unemployment • Calculation: Number of Unemployed Labor Force (Multiplied by 100 to put as a %) The Labor Force is the total of employed and

unemployed workers. U.S. unemployment should be about 5%

Employed

• You are considered to be employed if:

• You work for 1 hour as a paid employee (so part-time workers count)

• You are temporarily absent from work (illness, strike, vacation)

• You work 15 hours or more as an unpaid worker (family farms are common)

Unemployed

• Must be looking for work (at least 1 attempt in the past 4 weeks)

• Are reporting to a job within 30 days

• Are temporarily laid off from their job

Not In Labor Force

• A person who is not looking for work:

• Full-time students

• Stay at home parents

• Discouraged workers: those who have given up hope of finding a job.

• Retirees

37

Unemployment • 100% of the people will never be employed, so the

government considers 4-6% unemployment to be “full employment.”

• Types of Unemployment

• Frictional - temporary and unavoidable

• Structural - results from changes in technology or a business restructure (ex. Merger)

• Seasonal- occurs when industries slow or shut down for a season

• Cyclical - results from a decline in the business cycle.

We can never be at Full Employment if there is any percentage cyclically unemployed.

38

10-15% National Income and Price Determination

A. Aggregate demand

1. Determinants of aggregate demand

2. Multiplier and crowding-out effects

B. Aggregate supply

1. Short-run and long-run analyses

2. Sticky versus flexible wages and prices

3. Determinants of aggregate supply

C. Macroeconomic equilibrium

1. Real output and price level

2. Short and long run

3. Actual versus full-employment output

4. Economic fluctuations

Consumption and Saving

• As income increases, both consumption and savings will increase.

• The determinants of overall consumption and savings are: (More

money or a positive outlook will increase consumption and reduce savings. Less money or a negative outlook will increase savings and reduce consumption. • Wealth (financial assets) • Expectations about future prices and income • Real Interest Rates • Household Debt • Taxes

Marginal Propensities

• Marginal Propensity to Consume (MPC) and the Marginal Propensity to save (MPS) must equal 1.

• The MPS is used to derive the spending multiplier, which equals: 1_

MPS

If the MPS is .2, the spending multiplier is 5.

Any increase in spending must be multiplied by 5 to determine the overall increase in Real GDP.

Aggregate Demand

AD (C + I + G + X)

Price

Level

Real GDP

Downward sloping:

1. Price Effect: change

in purchasing power

2. Interest-Rate Effect: Higher

interest rates curtail spending

3. Net Export Effect:

Substitute foreign products for

U.S. products

Aggregate Demand

• Determinants of AD:

• C + I + G + Xn (Yes, its GDP)

• An increase in any of these, due to lower interest rates or optimism will increase AD and shift the curve to the right.

• A decrease in any of these: more debt, less spending, tax increase, will cause a decrease in AD and shift the curve to the left

Aggregate Demand Determinants

• Consumption • Wealth

• Expectations

• Debt

• Taxes

• Investment • Interest Rates

• Expected Returns

• Technology

• Inventories

• Taxes

• Government • Change in Gov. spending

• Net Exports • National Income Abroad

• Exchange Rates

Aggregate Supply Factors:

• R: resource prices (The CELL/ wages and materials, as well as OIL)

• E: environment [legal-institutional] (Taxes, Subsidies, more regulation)

• P: productivity (better technology)

Aggregate Supply

• Short Run: • Assumes that nominal wages

are “sticky” and do not respond to price level changes.

• Is Upward sloping as businesses will increase output to maximize profits

• Generally considered to be a year or less.

• Long Run: • Curve is vertical because the

economy is at its full-employment output.

• As prices go up, wages have adjusted so there is no incentive to increase production.

• Generally considered to be longer than a year.

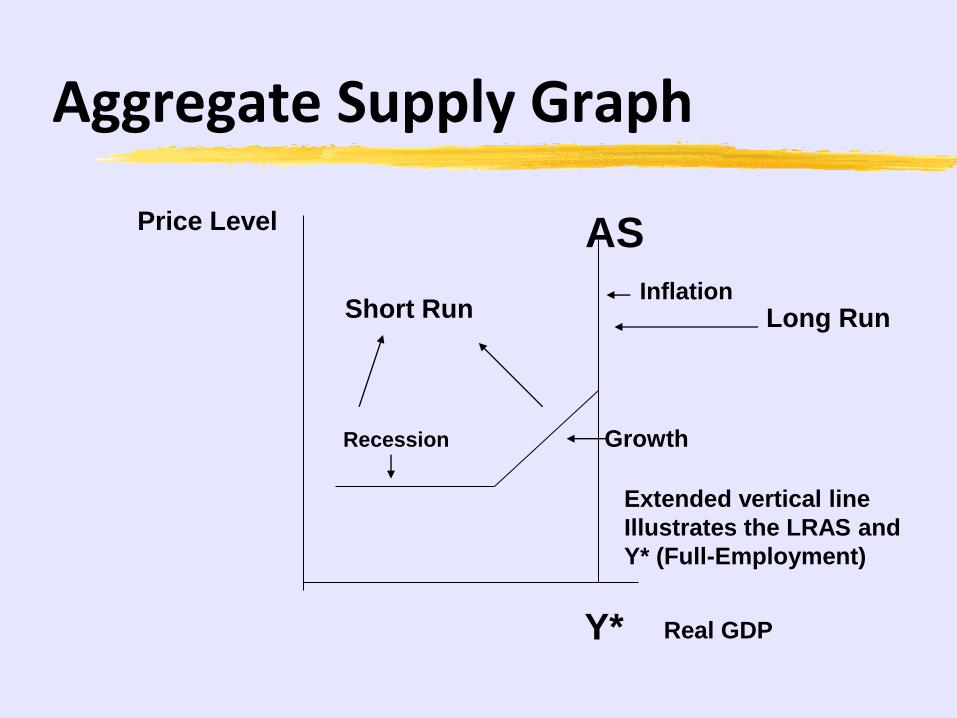

Aggregate Supply Graph

Price Level AS

Recession Growth

Inflation Short Run Long Run

Y*

Extended vertical line

Illustrates the LRAS and

Y* (Full-Employment)

Real GDP

Another look as AS

PL

RGDP

PL

Y*

LRAS

SRAS

AD

Changes that

lead to a new

equilibrium

on the left of

LRAS =

Recession

Changes that

lead to a new

equilibrium

on the right

of LRAS =

Inflation

(AKA “an

overheated

economy”)

NOTE!!

• For the AP exam, assume that there are only two determinants that simultaneously affect BOTH short term aggregate supply and aggregate demand

• business tax changes and

• foreign currency changes.

• A change in business taxes shifts AD and AS in the same direction

• A change in FX sends both curves in the opposite

directions.

Demand-Pull Inflation

AD1 (C + I + G

+ X)

AD2

AS

Price Level

Real GDP Y*

P1

P2

Cost-Push Inflation

Y* Y

P1

P2

Price

Level

Real GDP

AD1 ( C + I + G + X)

AS1

AS2

51

Demand-Pull Inflation

vs.

Cost-Push Inflation

52

DEMAND-PULL INFLATION

o

P1

AS1

ASLR

AD1

a

Q1

Pri

ce L

evel

Real domestic output

b P2

P3

AD2

AS2

c

53

Q2

COST-PUSH INFLATION

o

P1

AS1

ASLR

AD1

a

Q1

Pri

ce L

evel

Real domestic output

b P2

AS2

Occurs when short-run AS shifts left

54

Q2

COST-PUSH INFLATION

o

P1

AS1

ASLR

AD1

a

Q1

Pri

ce L

evel

Real domestic output

b P2

P3

AD2

AS2

Government response with increased AD

c

Even

higher

price

levels

55

COST-PUSH INFLATION

o

P1

AS1

ASLR

AD1

a

Q1

Pri

ce L

evel

Real domestic output

b P2

AS2

If government allows a recession to occur

Q2

56

Q2

COST-PUSH INFLATION

o

P1

AS1

ASLR

AD1

a

Q1

Pri

ce L

evel

Real domestic output

b P2

AS2

If government allows a recession to occur

Nominal

wages fall &

AS returns

to its original

location

57

15-20% Financial Sector (Money and Banking)

A. Money, banking, and financial markets

1. Definition of financial assets: money, stocks, bonds

2. Time value of money (present and future value)

3. Measures of money supply

4. Banks and creation of money

5. Money demand

6. Money market

7. Loanable funds market

B. Central bank and control of the money supply

1. Tools of central bank policy

2. Quantity theory of money

3. Real versus nominal interest rates

58

Money Supply Terms

• M1= Checkable Deposits and Currency

• M2= M1 + Savings deposits, money market accounts, small time deposits (less than $100,000)

• Velocity of Money Equation: • MV = PQ ( GDP) (M= Money Supply and V =

Velocity (number of times per year the average dollar is spent on goods and services.

59

Banks and Balance Sheets Assets Liabilities Reserves $15,000 $100,000 DD Securities $15,000 Loans $70,000 If the current reserve requirement is 10%: 1. What is the amount of new loans this bank can generate? Answer: $100,000 Checkable deposits X a 10% reserve requirement =

$10,000 required reserves. If the bank has $15,000 in reserves, $5,000 of those are excess reserves and can be loaned out .

2. How much in new loans can be generated by the entire banking system? Answer: Money Multiplier = 1/Required Reserve Ratio=1/.10 10 X $5,000 = $50,000

60

FED and the Money Market

MS1 MS2

MD

Nominal Interest

Rate

Quantity of Money

nir1

nir2

Q1 Q2

Vertical curve-Supply controlled

By the FED. An increase in MS

leads to a rightward shift and

lower nominal interest rates.

61

Interest Rate-Investment

• Expected Rate of Return: Amount of Profit (expressed as a percentage) a business expects to gain on a project/investment. • This rate must be greater than the interest in

order to be profitable.

• The Real Rate of Return is most important. An expected profit of 10%, that costs 5% in interest = The real rate of return: 5%.

62

Investment Demand Curve:

Quantity of Investment

Real Rate of

Return

ID

r1

r2

Q1 Q2

At lower real interest rates businesses will

Increase investment , leading to an increase

In AD (aggregate demand). At higher rates of

Interest, less money will be invested

63

Shifts of the Investment Demand Curve

Expected Rate of

Return

( Real Interest Rate.)

Quantity of Investment

ID1

ID2

ID3

A shift from ID1 to ID2

Represents an increase in

Investment demand. A shift

From ID1 to ID3 represents a

decrease in investment

Demand.

Loanable Funds Market and Expansionary Fiscal Policy

• Used for FISCAL POLICY (Government spending-Deficit Spending)

Quantity of Funds

Real Interest Rate

DLF1

DLF2

An increase in Gov.

spending increases the

demand for loanable

funds and raises real

interest rates

R1

R2

Q1 Q2

SLF

Loanable Funds Market and Contractionary Fiscal Policy

• Used for FISCAL POLICY (Government spending-Deficit Spending)

Quantity of Funds

Real Interest Rate

DLF2

DLF1

A decrease in Gov.

spending decreases the

demand for loanable

funds and lowers real

interest rates

R2

R1

Q2 Q1

SLF

66

Nominal: with Inflation

Real:

without Inflation

67

GDP

• Nominal GDP: GDP measured in terms of current Price Level at the time of measurement. (Unadjusted for inflation)

• Real GDP: GDP adjusted for inflation; GDP in a year divided by a GDP deflator (Price Index) for that year

68

INCOME

• NOMINAL INCOME: number of dollars received by an individual or group for its resources during some period of time

• REAL INCOME: amount of goods and services which can be purchased with nominal income during some period of time; nominal income adjusted for inflation

69

INTEREST RATE (I%)

• NOMINAL I%: interest rate expressed in terms of annual amounts currently charged for interest; not adjusted for inflation

• REAL I%: interest rate expressed in dollars of constant value (adjusted for Inflation) and equal to the NOMINAL I% minus the EXPECTED RATE OF INFLATION

70

Nominal

Interest

Rate

Real

Interest

Rate

Inflation

Premium

= 11%

5%

6%

+

ANTICIPATED INFLATION

71

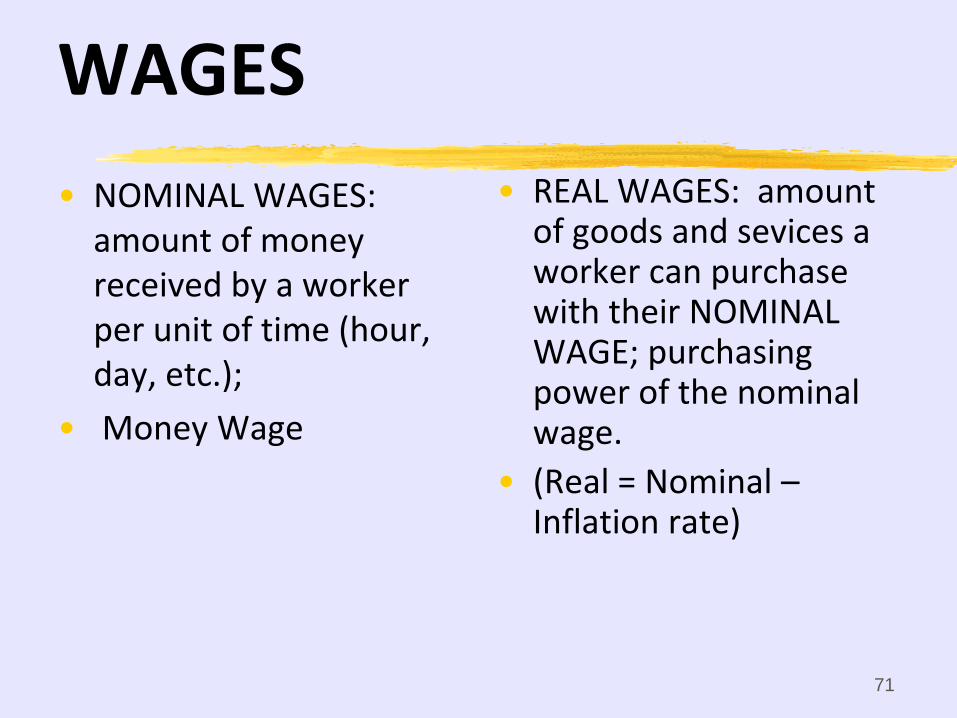

WAGES

• NOMINAL WAGES: amount of money received by a worker per unit of time (hour, day, etc.);

• Money Wage

• REAL WAGES: amount of goods and sevices a worker can purchase with their NOMINAL WAGE; purchasing power of the nominal wage.

• (Real = Nominal – Inflation rate)

72

NOMINAL/REAL TIPs

• If nominal rates INCREASE and Price Level INCREASE, the CHANGE in Real is “indeterminable.”

• If nominal Wage rates do NOT change and Price Level fall. REAL WAGES increase.

• NOMINAL RATES “PIGGY-BACK” REAL RATES & NOT VICE VERSA.

73

20-30% Inflation, Unemployment, and Stabilization Policies

A. Fiscal and monetary policies

1. Demand-side effects

2. Supply-side effects

3. Policy mix

4. Government deficits and debt

B. Inflation and unemployment

1. Types of inflation

a. Demand-pull inflation

b. Cost-push inflation

2. The Phillips curve: short run versus long run

3. Role of expectations

Fiscal Policy • Using Taxes and Government spending to stabilize the

economy. • Controlled by the President and Congress • Discretionary Fiscal Policy: Congress must take action

(change the tax rates) in order for the action to be implemented.

• Automatic Stabilizers: Unemployment benefits, Progressive

Tax System, these changes are implemented automatically to help the economy.

FISCAL POLICY CHANGES AD …. EXCEPT when the question specifically states

there is a change in business taxes.

Types of Fiscal Policy

• Expansionary • Used to Fight a

Recession

• LOWER TAXES

• INCREASE GOVERNMENT SPENDING

• Contractionary • Used to fight Inflation

• RAISE TAXES

• DECREASE GOVERNMENT SPENDING

Expansionary Fiscal Policy

Price Level

Real GDP

AD1 ( C + I + G + X )

AD2

AS1

P1

Y* Y1

P2

Contractionary Fiscal Policy

• Raising taxes or reducing government spending to fight inflation and stabilize the economy.

Price Level

Real GDP

AD1

P1

P2

AD2

Y*

AS

Tax Multiplier [-MPC/MPS] • Remember, if the government decreases

taxes, the result is not as great as a spending increase, since households will save a portion (MPS) of the tax cut.

• The Tax Multiplier = -MPC /MPS • Example: If the MPC is .8 and the MPS is .2

• Spending Multiplier = 1/.2 or 5

• Tax Multiplier = -.8 /.2 or -4

Crowding-Out Effect • An Expansionary Fiscal Policy as previously

diagrammed will lead to higher interest rates. • At higher interest rates, businesses will take out

fewer loans and there will be a decrease in INVESTMENT (I)

• At the same time there will be a decrease in CONSUMER SPENDING (C) as they will take out fewer loans as well.

• This CROWDING OUT EFFECT will reduce the gain made by the expansionary fiscal policy.

Net Export Effect & Expansionary Fiscal Policy

• Government spending has led to an increase in interest rates.

• At higher interest rates, foreigners demand more U.S. dollars to invest in bonds.

• This leads to an appreciation of the U.S. dollar.

• This leads to a decrease in Net Exports, as foreigners now have to exchange more of their currency for the U.S. dollar to buy exports.

• This decrease in Net Exports will reduce AD and counter to some extent the expansionary fiscal policy.

Net Export Effect & Contractionary Fiscal Policy

• A decrease in government spending has led to a decrease in real interest rates.

• At lower interest rates, foreigners demand less U.S. dollars to invest in bonds.

• This leads to a depreciation of the U.S. dollar.

• This leads to an increase in Net Exports, as foreigners now have to exchange less of their currency for the U.S. dollar to buy exports.

• This increase in Net Exports will increase AD and further strengthen the contractionary fiscal policy.

Criticisms of Fiscal Policy • Timing Problems

• Recognition Lag: identifying recession or inflation

• Administrative Lag: getting Congress/President to agree to take action

• Operational Lag: Time needed to see the results of the fiscal policy

• Political Business Cycles: Politicians may take inappropriate action to get reelected (lower taxes during an inflationary period). Plus it is difficult to raise taxes

The Federal Reserve System (FED)

• Control Monetary Policy

• Headquartered in Washington D.C.

• 12 Federal Reserve Districts

• Board of Governors (7 members) is the central authority

• Members are appointed by the President and confirmed by the Senate

Federal Open Market Committee (FOMC)

• Made up of 12 people: Board of Governors + New York FED President + 4 other regional presidents (who rotate)

• Meets regularly to direct OPEN MARKET OPERATIONS (buying or selling of bonds) to maintain or change interest rates

FED and the Money Market

MS1 MS2

MD

Nominal Interest

Rate

Quantity of Money

nir1

nir2

Q1 Q2

Vertical curve-Supply controlled

By the FED. An increase in MS

leads to a rightward shift and

lower interest rates.

Easy Money Policy on AD/AS • Buying Government Bonds, lowering the discount rate, or lowering

reserve requirements, to fight a recession, by decreasing interest rates, increasing investment spending and/or consumption and increasing AD.

Price Level

Real GDP Q1

P1

P2

QF

AS

AD2

AD1 (C + I + G + X)

Effects of an Easy Money Policy

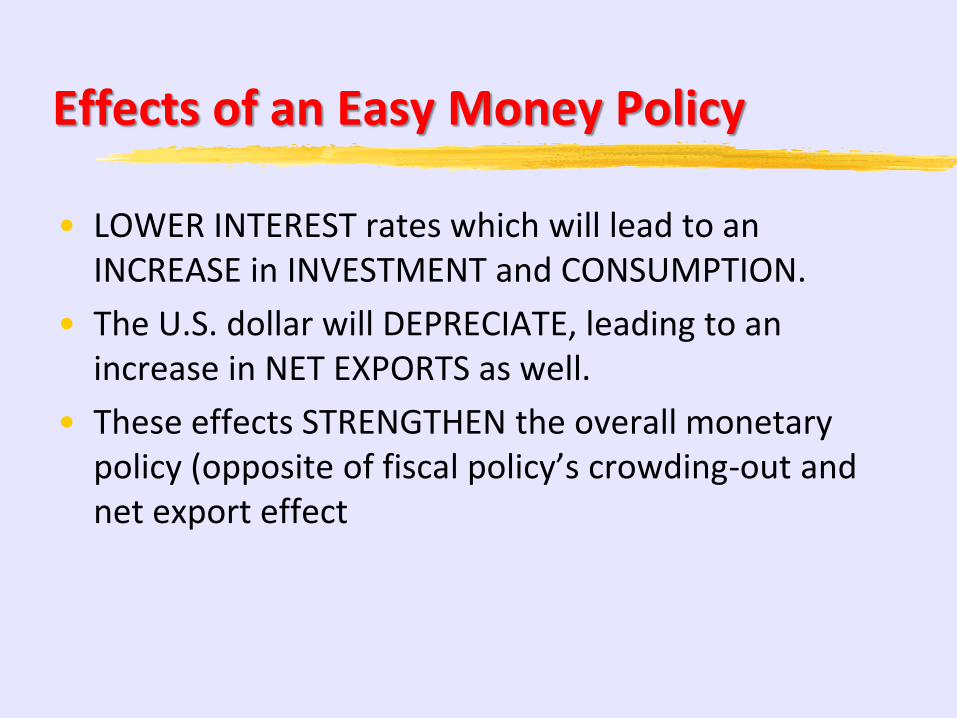

• LOWER INTEREST rates which will lead to an INCREASE in INVESTMENT and CONSUMPTION.

• The U.S. dollar will DEPRECIATE, leading to an increase in NET EXPORTS as well.

• These effects STRENGTHEN the overall monetary policy (opposite of fiscal policy’s crowding-out and net export effect

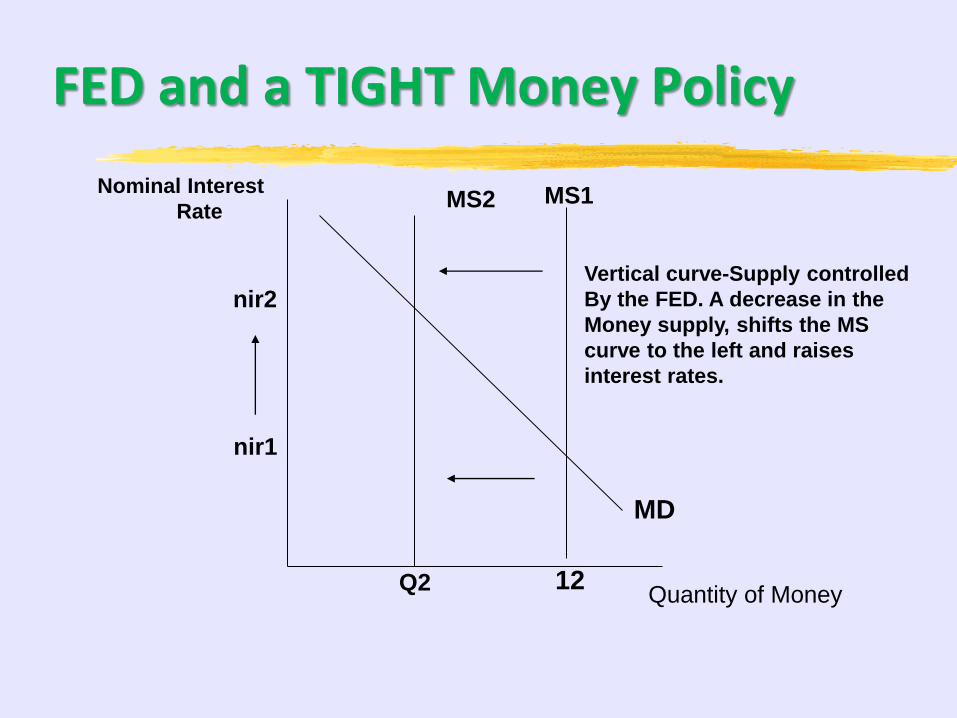

FED and a TIGHT Money Policy

MS2 MS1

MD

Nominal Interest

Rate

Quantity of Money

nir2

nir1

Q2 12

Vertical curve-Supply controlled

By the FED. A decrease in the

Money supply, shifts the MS

curve to the left and raises

interest rates.

Tight Money Policy and AD/AS • Selling bonds, raising the discount rate, or raising reserve requirements

to fight inflation which will raise interest rates, decrease investment and/or consumption and decrease Aggregate Demand (AD).

Price Level

Real GDP

AD1

P1

P2

AD2

QF

AS

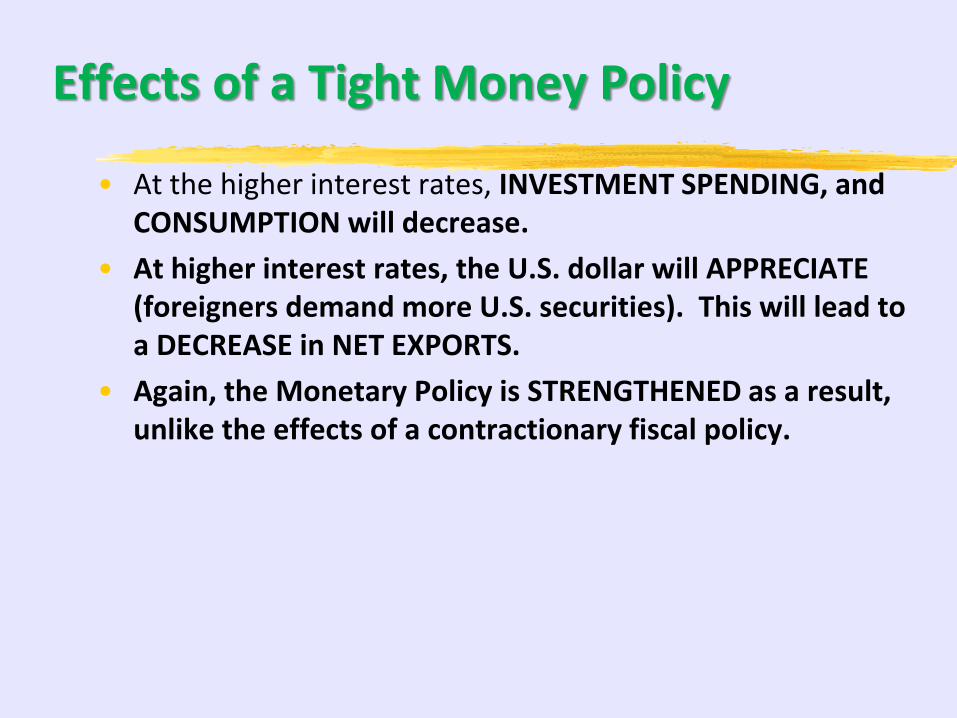

Effects of a Tight Money Policy

• At the higher interest rates, INVESTMENT SPENDING, and CONSUMPTION will decrease.

• At higher interest rates, the U.S. dollar will APPRECIATE (foreigners demand more U.S. securities). This will lead to a DECREASE in NET EXPORTS.

• Again, the Monetary Policy is STRENGTHENED as a result, unlike the effects of a contractionary fiscal policy.

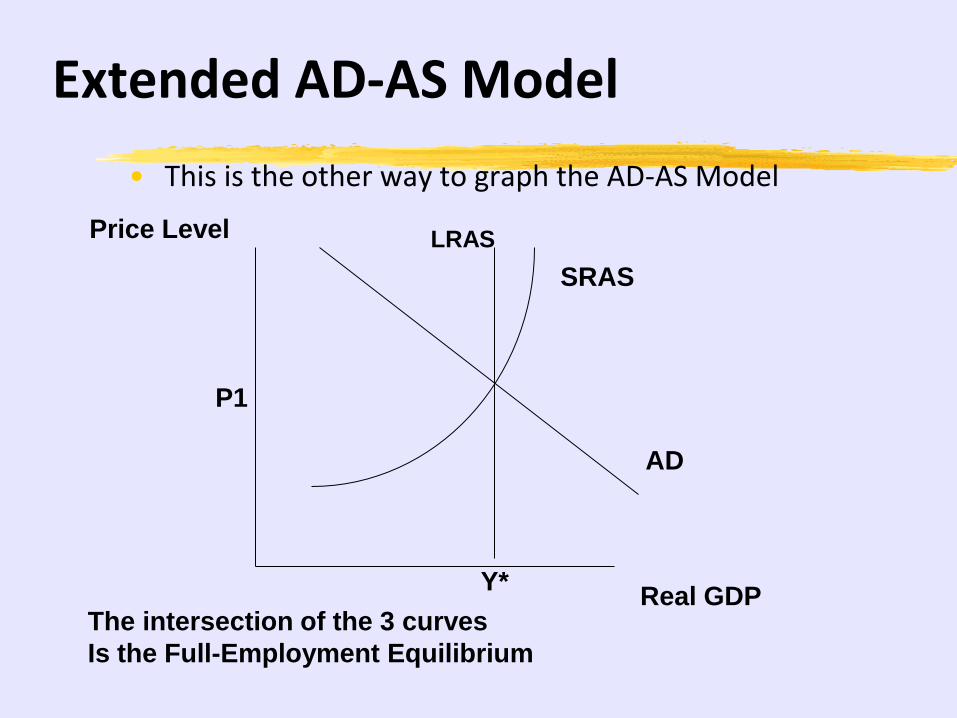

Extended AD-AS Model

• This is the other way to graph the AD-AS Model

AD

Price Level

Real GDP Y*

P1

SRAS

LRAS

The intersection of the 3 curves

Is the Full-Employment Equilibrium

Extended AD-AS Model and Demand-Pull Inflation

• In Demand-Pull Inflation, the AD curve has shifted to the right of the LRAS and SRAS intersection.

AD2

Price Level

Real GDP Y*

P2

SRAS

LRAS

Y2

The Price Level and Real GDP has increased.

AD1

PF

Extended AD-AS and Demand-Pull Inflation

• Mainstream economists will fight inflation as previously discussed: with either a tight monetary policy or a contractionary fiscal policy. The goal would be to move the aggregate demand curve to the left.

• Classical economists would argue to DO NOTHING.

As nominal wages rise, the SHORT-RUN AS curve will shift to the left (resources and wages are becoming more expensive), restoring the economy to its full-employment output level, but with a higher Price Level.

Extended AD-AS Model and Cost-Push Inflation

AD1

Price Level

Real GDP Y*

SRAS2 LRAS

Cost-Push inflation occurs when the SRAS has shifted to the left

Of the LRAS and AD intersection.

P1

Y1

Here the Price level has

Increased and REAL GDP

has decreased.

SRAS1

PF

Extended AD-AS and Cost-Push Inflation

• Mainstream economists must decide whether to target the Price Level or Unemployment, before taking any action.

• Classical economists would argue to DO NOTHING. Eventually, wages and resource prices must decrease and when they do the SRAS curve will shift back to the right, restoring the economy to its full-employment output level and the original Price Level.

Extended AD-AS Model and Recession

• In a recession due to a decrease in AD, the AD curve is to the left of the LRAS and SRAS intersection; showing a decrease in both

the Price Level and Real GDP.

AD

Price Level

Real GDP Y*

SRAS

LRAS

P1

Y1

PF

Extended AD-AS and Recession

• Mainstream economists will fight a recession as previously discussed: with either an easy money policy or an expansionary fiscal policy. The goal would be to move the aggregate demand curve to the right.

• Classical economists would argue to DO NOTHING.

The decrease in wages and resource prices will shift the SRAS curve to the right, restoring the economy to its full-employment output level, but with a LOWER price. (SELF-CORRECTION)

Short-Run Phillips Curve

• Suggests an inverse relationship between the inflation rate and the unemployment rate.

Inflation

Rate (percent)

Unemployment Rate (percent)

2

8

2 8

When the unemployment rate is

Low (2%), the inflation rate will

Most likely be high (8%).

When the

Unemployment rate

Is high, inflation will

likely be low.

SRPC1

Short-Run Phillips Curve

• When the Government fights unemployment, typically higher inflation will result. When the Government fights inflation, typically, more unemployment will result. Thereby, we move along the Short-Run Phillips Curve. (Changes in AD = movements on the SRPC.

Inflation

Rate (percent)

Unemployment Rate (percent)

A

B 7

2

3 6

SRPC1

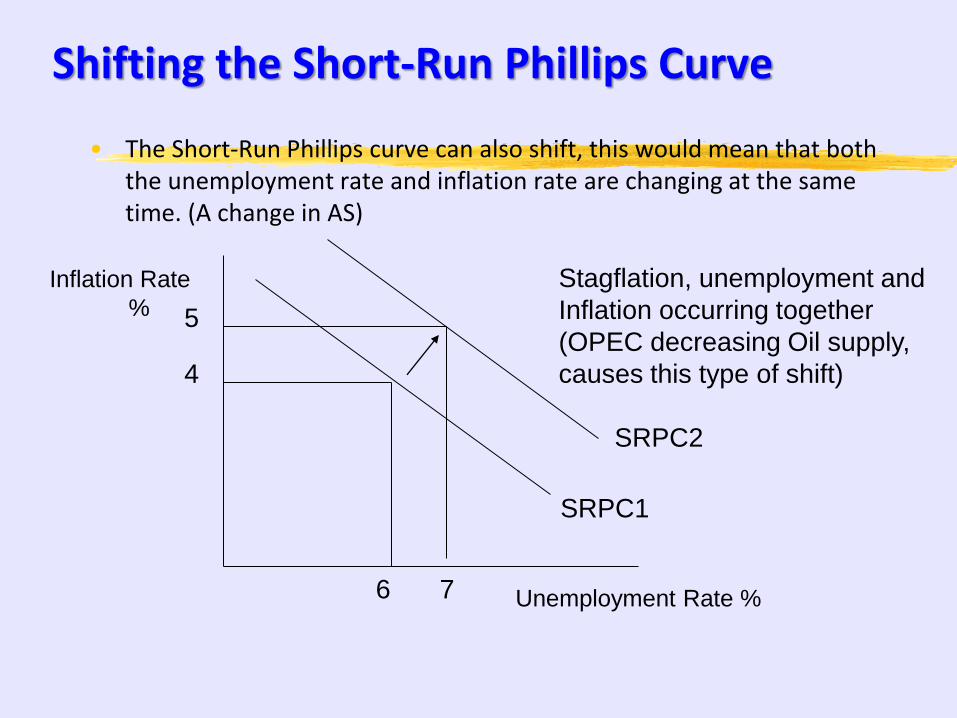

Shifting the Short-Run Phillips Curve

• The Short-Run Phillips curve can also shift, this would mean that both the unemployment rate and inflation rate are changing at the same time. (A change in AS)

SRPC1

SRPC2

4

5

6 7

Stagflation, unemployment and

Inflation occurring together

(OPEC decreasing Oil supply,

causes this type of shift)

Inflation Rate

%

Unemployment Rate %

Shifting the Short-Run Phillips Curve

• The Short-Run Phillips curve can also shift, this would mean that both the unemployment rate and inflation rate are changing at the same time.

SRP2

SRPC1

5

7

When Supply increases

(productivity surge in 90s)

more than demand, prices will

fall, while GDP and employment

Increase; shifting the curve to the left.

Inflation Rate %

Unemployment Rate %

3

5

The SRPC is

a mirror

image of AS

– If AS

moves right,

SRPC

moves left.

Long-Run Phillips Curve

• The Long-Run Phillips Curve is vertical, like the Long Run Aggregate Supply Curve. So, in the long run there is no tradeoff between inflation and unemployment. Only the Price Level will change.

Inflation Rate%

Unemployment Rate % 5

3

SRPC

LRPC

Laffer Curve • What is the optimal tax rate? A tax of 0% will provide no tax revenue. A

tax rate of 100% will also lead to no tax revenue (no incentive to work). Answer must be somewhere in between.

Tax Rate

Tax Revenue 0

100

Economic Philosophies

• Classical: Believes that the government SHOULD

NOT interfere in the economy. And believes in self-correction of economic problems.

• Keynesian: Believes that GOVERNMENT SHOULD interfere in the economy (taxes, government spending). Most “mainstream” economists are Keynesians

• Rational Expectations: Believes that monetary and fiscal policy have certain effects on the economy and take action to make these policies ineffective.

105

5-10% Economic Growth and Productivity

A. Investment in Human Capital

B. Investment in Physical Capital

C. Research and development, and technological progress

D. Growth Policy

Economic Growth

• Five Factors connected to long run economic growth.

• Supply Factors:

• Increase in natural resources (quantity and quality) • Increase in human resources (quantity and quality) • Increase in capital goods • Improvements in technology

• Demand Factors: • Increase in consumption by households, businesses, and

government

Illustrating Economic Growth

• Production Possibilities Curve

Capital Goods

Consumer Goods

A

B

PPC1

PPC2

Illustrating Long Run Growth

• Can also be illustrated with the extended AD-AS Model.

Real GDP

Price Level

AD1

AD2

SRAS1 SRAS2 LRAS1

LRAS2

Y1 Y2

P1

P2

109

10-15% Open Economy: International Trade and Finance

A. Balance of payments accounts

1. Balance of trade

2. Current account

3. Capital account

B. Foreign exchange market

1. Demand for and supply of foreign exchange

2. Exchange rate determination

3. Currency appreciation and depreciation

C. Net exports and capital flows

D. Links to financial and goods markets

International Trade

• Comparative Advantage and Specialization allows for economic growth and efficiency. (More of each good can be obtained by trading-Trading line illustrates this)

• Trade barriers create more economic loss than benefits.

• Today there is a trend towards free trade and a reduction in trade barriers.

• Strongest arguments for protection are the infant industry and military self-sufficiency arguments.

• WTO oversees trade agreements and disputes, but has become a target of protesters lately.

111

The value of a foreign nation’s currency in relation to

your own currency is called the exchange rate.

Exchange Rates and International Markets

• An increase in the value of a currency is called appreciation.

• A decrease in the value of a currency is called depreciation.

• Multinational firms convert currencies on the foreign exchange market, a network of about 2,000 banks and other financial institutions.

112

Types of Exchange Rate Systems

Fixed Exchange-Rate Systems

• A currency system in which governments try to keep the values of their currencies constant against one another is called a fixed exchange-rate system.

Flexible Exchange-Rate Systems

• Flexible exchange-rate systems allow the exchange rate to be determined by supply and demand.

Foreign Exchange Market

• Let’s say a U.S. citizen travels to Japan. This transaction will provide a supply of the U.S. dollar and result in a demand for yen. It will become cheaper for the Japanese to buy the dollar and more expensive for Americans to buy the Yen. The Yen is Appreciating and the dollar is Depreciating.

Quantity of U.S. Dollars Quantity of Yen

Yen Price of

dollar

(Y/$)

Dollar Price

of Yen

($/Y)

P1

Q1

D$1

S$1

S$2

P2

Q2

P1

Q1

DY1

SY1

DY2

Q2

P2

Balance of Payments: The sum of all transactions between U.S.

residents and residents of all foreign nations

• Current Account: Shows U.S. exports and U.S. imports of goods and services.

• Capital Account: Shows the U.S. investment (financial as well as capital-plants and factories) abroad and Foreign investment in the U.S.

• Credits: A credit are those transactions for which the U.S. receives income (exports, foreign purchase of assets)

• Debits: Those transactions that the U.S. must pay for: imports and purchasing of assets abroad.

Balance of Payments [continued] • The Current Account and Capital Account must be equal.

• Official Reserves Account: The Central Banks of all nations hold foreign currency to make up any deficit in the combined capital and current accounts.

• If the U.S. has more credits than debits it finances this difference by dipping into its reserve account.

116

So,………… That’s it!

Easy, huh?