Toward option values of near machine preci sion using Gaussian Q uadrature San–Lin Chung Department of Finance National Taiwan University Taipei 106. Taiwan, R.O.C. Mark B. Shackleton Department of Accounting and Financ e Lancaster University, LA1 4YX, UK.

Transcript

Toward option values of near machine precision using Gaussian

QuadratureSan–Lin Chung

Department of FinanceNational Taiwan UniversityTaipei 106. Taiwan, R.O.C.

Mark B. ShackletonDepartment of Accounting and Finance

Lancaster University, LA1 4YX, UK.

AbstractIn this paper, we combine the best features of two

highly successful Quadrature option pricing papers. Adopting the recombining abscissa or node approach used in Andricopoulos, Widdicks, Duck, and Newton (2003) (AWDN) with the Gauss Legendre method of Sullivan (2000) yields highly accurate and efficient option prices for a range of standard and exotic specifications including barrier, compound, reset and spread options.

Introduction

• Numerical integration is at the heart of almost all option pricing.

• Numerical integration involves evaluation and summation of an integrand (typically the maximum of a payoff or a continuation value) with probability weights over a number of particular stock price points.

Introduction

• Tree or finite difference techniques perform the valuation and interim storage activity by

“integrating” over a regular series of locations

(triangular or rectangular).• Most efficient exotic options algorithms require sto

rage structures that can be adapted to the payoff in question on the exotic; e.g. it is usually easier to price a barrier option if a node is located on the barrier at each barrier monitoring time. See Boyle and Lau (1994) and Ritchken (1995) etc.

Introduction

• Against node positioning flexibility we also need to avoid the so called curse of dimensionality where (unless self similar structures are employed) the number of required calculations increases geometrically with the number of time slices considered.

i.e. avoid using non-recombining trees! See Amin (1991) and Ho, Stapleton, and Subrahmanyam (1995) etc.

Literature Review

Omberg (1988) – Gauss-Hermite method

-- Introduce the idea of Gauss Hermite method into the lattice approach.

Sullivan (2000) – Gassian Legendre method

-- First apply Gassian Legendre method to option pricing.

Andricopoulos, Widdicks, Duck, Newton (2003) – Simpson’s Rule

Numerical option valuation A typical option valuation problem is like:

It essentially involves numerical integration in the above problem.

11 1

1 1

( , ) [ ( , )]ir ti i Q i i

i i i

V S t E e V S t

t t t

11 1 1 1

0

( , ) ( , ) ( )ir ti i i i i iV S t e V S t f S dS

Numerical option valuation

ondistributinormalofpdfisxf

dxxftxSVetSV

i

iiiiitr

iii

)(

)()),exp(*(),(

1

11

0

111

The disadvantage in Sullivan (2000) method is that the abscissas in next period depends on the previous period.Therefore it is path dependent in the sense that number ofnodes will increase exponentially.

Numerical option valuation

The advantage in AWDN (2003) method is that the abscissas in next period can chosen arbitrarily. Therefore it is path independent in the sense that number of nodes will increase linearly.

..),(

),)*5.0((~)(

)(),(),(

112

1

11111

dsandmeanwithondistributinormalisN

ttrxNxf

dxxftxVetxV

iiii

iiiitr

iii

Numerical option valuation

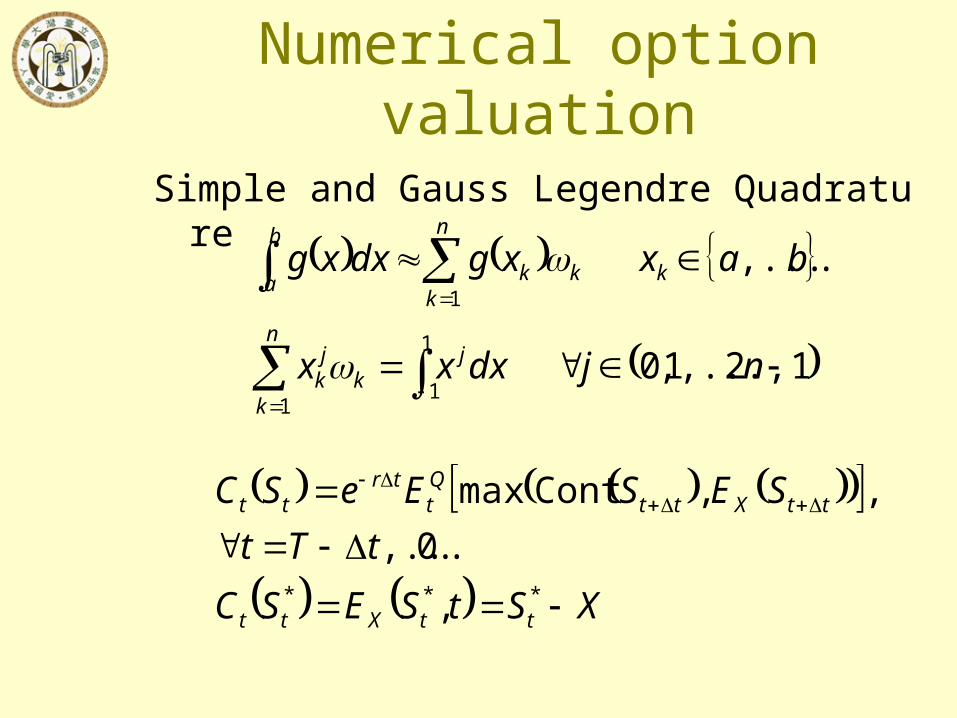

Simple and Gauss Legendre Quadrature

12,...,1,0

.,...,

1

1

1

1

njdxxx

baxxgdxxg

n

k

jk

jk

k

b

a

n

kkk

XStSESC

tTt

SESEeSC

ttXtt

ttXttQt

trtt

*** ,

.0,...

,,Contmax

Numerical option valuation

*ln

*

lnlnlnln

,,,,ScholesBlack

ttS

ttttttttttr

ttttt

SdSSSCe

trSSSC

n

kk

xxttt

trtt

kk etteSCeSC1

,

:000)Sullivan(2

n

kk

xxtt

S

ttttttttt

kk

tt

eeC

SdSSSC

1

ln

lnlnlnln*

Numerical option valuation

In Sullivan (2000), approximation errors will dominate the other numerical errors in the integration procedure.

7

0

absicca at on valueContinuatil

xTcth kllek

n

k lk

xxTctr

ttttt

kkll eee

trSSSC

1

7

0

*

,,,,ScholesBlack

Option types and benchmark prices

• European call• Discrete and moving barrier options• Compound/installment call and Bermudan

put• American call with variable strike/dividends• Reset calls and puts• Spread options• Options under GARCH processes

Numerical results(1/2)

Table 1: European call options under constant volatility

Table 2: Comparing with AWDN (2003)

Table 3: Daily reset option

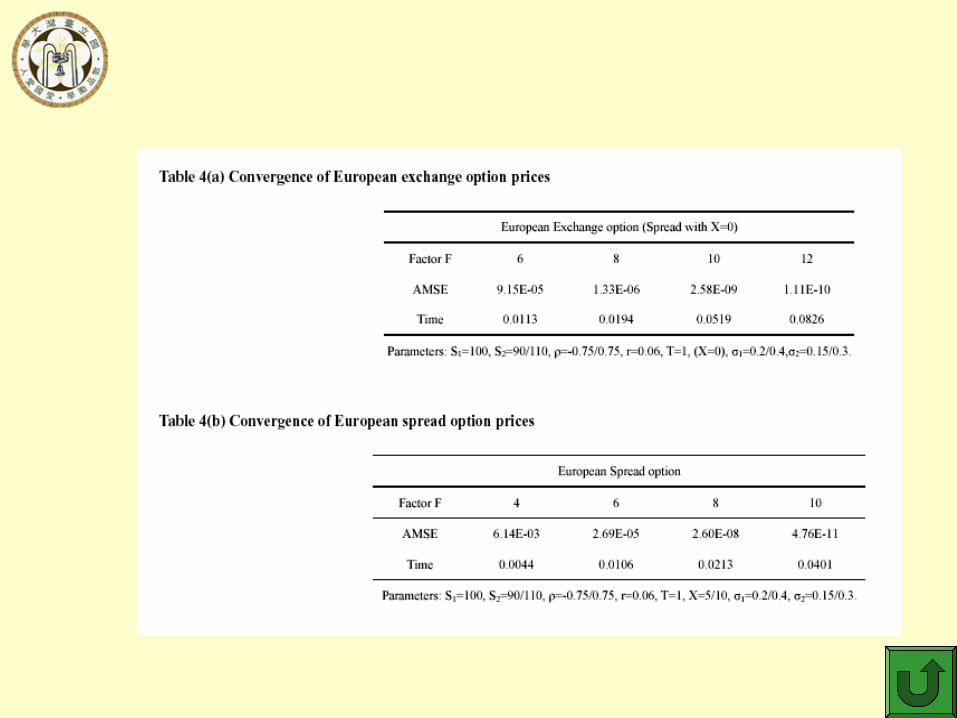

Table 4: European exchange and spread option

Numerical results(2/2)

Table 5: European put option under GARCH process (Duan and Simonato (2001))

Figure 1: Accuracy/Speed test with existing methods for pricing Bermudan put options

Figure 2: Accuracy/Speed test with existing methods for pricing barrier options

Conclusion

• High convergence order is not necessary the high accuracy method unless the integrand is a smooth function of the variables. • Most option values are smooth functions of state variables. Some exotic options need special treatment. For these options, we divide the integration range into subsets and the option value in each subset is a smooth function of the underlying variable(s).

Conclusion

• We try to claim that most numerical option valuation problems in the Black-Scholes economy is ending!!

• Our method provides benchmark values for testing other numerical techniques.

• Our method is potentially useful for empirical research using American and exotic option data.

Table 1 : European call options under constant volatility

Figure 1 : Accuracy/Speed test with existing methods for pricing American options

Figure 2 : Accuracy/Speed test with existing methods for pricing barrier options