22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 1/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 2/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 3/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

3

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

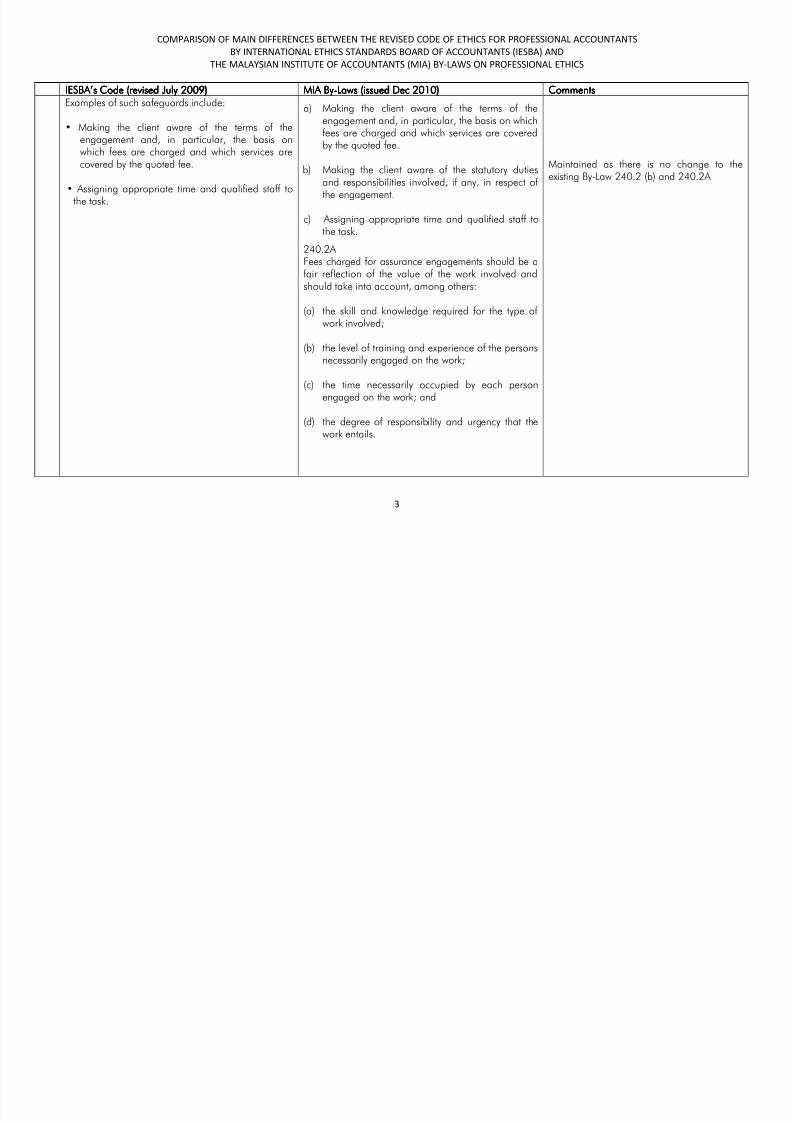

Examples of such safeguards include:

• Making the client aware of the terms of theengagement and, in particular, the basis onwhich fees are charged and which services arecovered by the quoted fee.

• Assigning appropriate time and qualified staff tothe task.

a) Making the client aware of the terms of theengagement and, in particular, the basis on whichfees are charged and which services are coveredby the quoted fee.

b) Making the client aware of the statutory dutiesand responsibilities involved, if any, in respect of

the engagement.

c) Assigning appropriate time and qualified staff tothe task.

240.2A Fees charged for assurance engagements should be afair reflection of the value of the work involved andshould take into account, among others:

(a) the skill and knowledge required for the type of work involved;

(b) the level of training and experience of the personsnecessarily engaged on the work;

(c) the time necessarily occupied by each personengaged on the work; and

(d) the degree of responsibility and urgency that thework entails.

Maintained as there is no change to theexisting By-Law 240.2 (b) and 240.2A

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 4/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 5/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 6/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 7/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 8/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

8

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

290.147The position of Company Secretary has differentimplications in different jurisdictions. Duties mayrange from administrative duties, such as personnelmanagement and the maintenance of companyrecords and registers, to duties as diverse as ensuringthat the company complies with regulations or providing advice on corporate governance matters.Generally, this position is seen to imply a closeassociation with the entity.290.148If a partner or employee of the firm serves asCompany Secretary for an audit client, self-reviewand advocacy threats are created that wouldgenerally be so significant that no safeguards couldreduce the threats to an acceptable level. Despiteparagraph 290.146, when this practice is specificallypermitted under local law, professional rules or practice, and provided management makes allrelevant decisions, the duties and activities shall belimited to those of a routine and administrativenature, such as preparing minutes and maintainingstatutory returns. In those circumstances, thesignificance of any threats shall be evaluated andsafeguards applied when necessary to eliminate thethreats or reduce them to an acceptable level.

290.149Performing routine administrative services to supporta company secretarial function or providing advice in

290.147(Intentionally left blank)

290.148(Intentionally left blank)

290.149(Intentionally left blank)

Maintained as there is no change to theexisting By Laws 290.150, 290.151, &290.152 which excludes provisions related toCompany Secretarial since it is governedunder Companies Act provision.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 9/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 10/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 11/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 12/22

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 13/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

13

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

290.173Despite paragraph 290.172, a firm may provideaccounting and bookkeeping services, includingpayroll services and the preparation of financialstatements or other financial information, of aroutine or mechanical nature for divisions or related

entities of an audit client that is a public interest entityif the personnel providing the services are notmembers of the audit team and:

(a) The divisions or related entities for which theservice is provided are collectively immaterial tothe financial statements on which the firm willexpress an opinion; or

(b) The services relate to matters that are collectivelyimmaterial to the financial statements of thedivision or related entity.

Emergency Situations290.174 Accounting and bookkeeping services, which wouldotherwise not be permitted under this section, may beprovided to audit clients in emergency or other unusual situations when it is impractical for the auditclient to make other arrangements. This may be the

client.

290.173 [This section is intentionally left blank]

290.174 [This section is intentionally left blank]

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 14/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

14

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

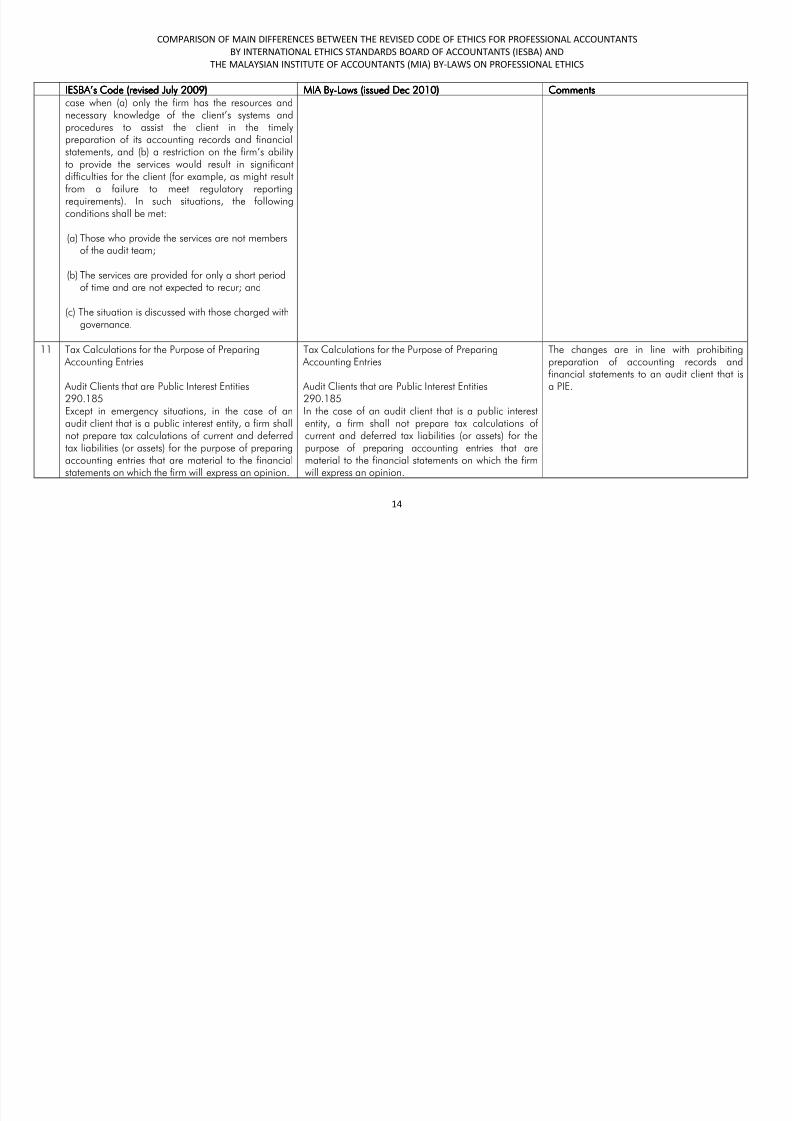

case when (a) only the firm has the resources andnecessary knowledge of the client’s systems andprocedures to assist the client in the timelypreparation of its accounting records and financialstatements, and (b) a restriction on the firm’s abilityto provide the services would result in significantdifficulties for the client (for example, as might resultfrom a failure to meet regulatory reporting

requirements). In such situations, the followingconditions shall be met:

(a) Those who provide the services are not membersof the audit team;

(b) The services are provided for only a short periodof time and are not expected to recur; and

(c) The situation is discussed with those charged withgovernance.

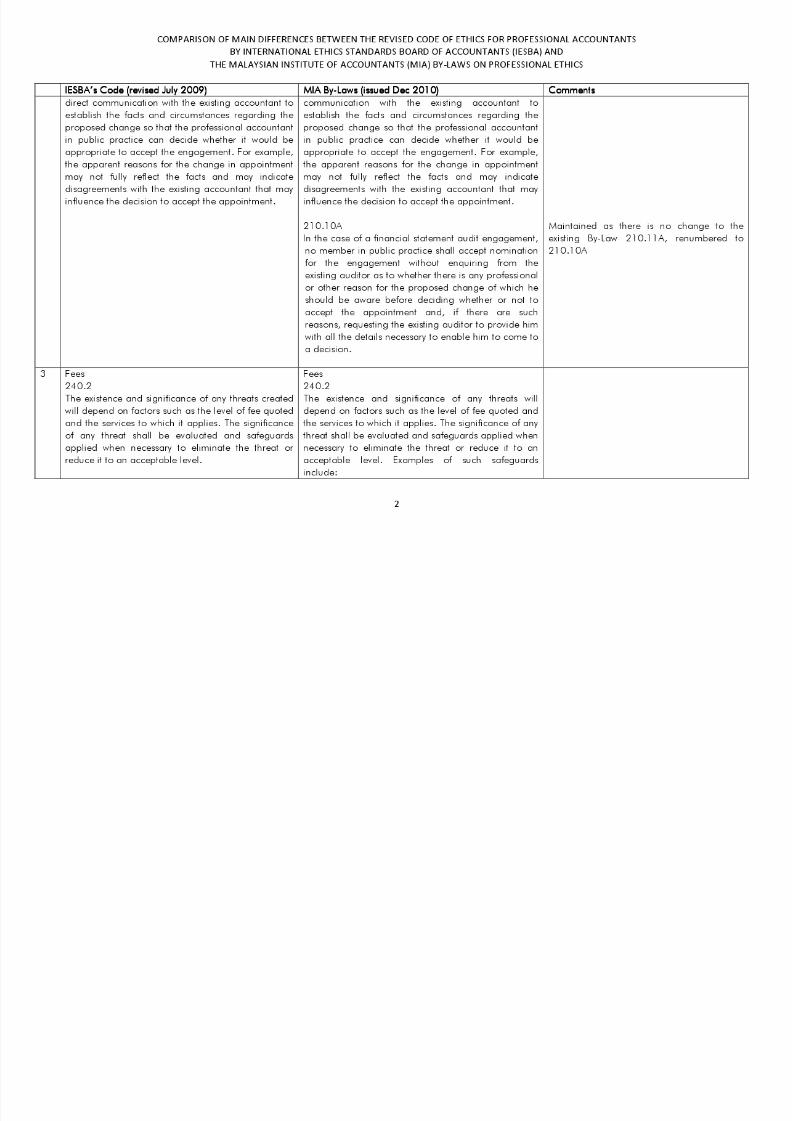

11 Tax Calculations for the Purpose of Preparing Accounting Entries

Audit Clients that are Public Interest Entities290.185Except in emergency situations, in the case of anaudit client that is a public interest entity, a firm shallnot prepare tax calculations of current and deferredtax liabilities (or assets) for the purpose of preparingaccounting entries that are material to the financialstatements on which the firm will express an opinion.

Tax Calculations for the Purpose of Preparing Accounting Entries

Audit Clients that are Public Interest Entities290.185In the case of an audit client that is a public interestentity, a firm shall not prepare tax calculations of current and deferred tax liabilities (or assets) for thepurpose of preparing accounting entries that arematerial to the financial statements on which the firmwill express an opinion.

The changes are in line with prohibitingpreparation of accounting records andfinancial statements to an audit client that isa PIE.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 15/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

15

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

290.186The preparation of calculations of current anddeferred tax liabilities (or assets) for an audit clientfor the purpose of the preparation of accountingentries, which would otherwise not be permittedunder this section, may be provided to audit clients inemergency or other unusual situations when it is

impractical for the audit client to make other arrangements. This may be the case when (a) onlythe firm has the resources and necessary knowledgeof the client’s business to assist the client in the timelypreparation of its calculations of current anddeferred tax liabilities (or assets), and (b) a restrictionon the firm’s ability to provide the services wouldresult in significant difficulties for the client (for

example, as might result from a failure to meetregulatory reporting requirements). In such situations,the following conditions shall be met:

(a) Those who provide the services are not membersof the audit team;

(b) The services are provided for only a short periodof time and are not expected to recur; and

(c) The situation is discussed with those charged withgovernance.

290.186 [This section is intentionally left blank]

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 16/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

16

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

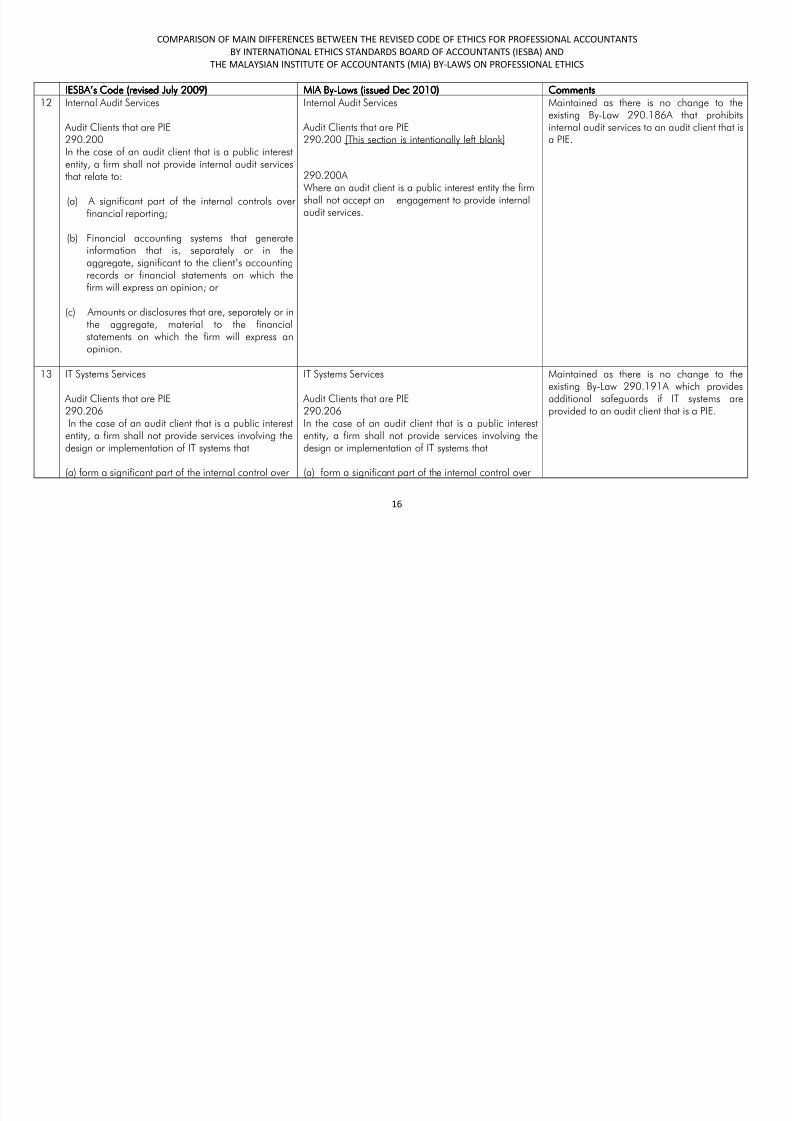

12 Internal Audit Services

Audit Clients that are PIE290.200In the case of an audit client that is a public interestentity, a firm shall not provide internal audit servicesthat relate to:

(a) A significant part of the internal controls over financial reporting;

(b) Financial accounting systems that generateinformation that is, separately or in theaggregate, significant to the client’s accountingrecords or financial statements on which thefirm will express an opinion; or

(c) Amounts or disclosures that are, separately or inthe aggregate, material to the financialstatements on which the firm will express anopinion.

Internal Audit Services

Audit Clients that are PIE290.200 [This section is intentionally left blank]

290.200A Where an audit client is a public interest entity the firm

shall not accept an engagement to provide internalaudit services.

Maintained as there is no change to theexisting By-Law 290.186A that prohibitsinternal audit services to an audit client that isa PIE.

13 IT Systems Services

Audit Clients that are PIE290.206In the case of an audit client that is a public interestentity, a firm shall not provide services involving thedesign or implementation of IT systems that

(a) form a significant part of the internal control over

IT Systems Services

Audit Clients that are PIE290.206In the case of an audit client that is a public interestentity, a firm shall not provide services involving thedesign or implementation of IT systems that

(a) form a significant part of the internal control over

Maintained as there is no change to theexisting By-Law 290.191A which providesadditional safeguards if IT systems areprovided to an audit client that is a PIE.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 17/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

17

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

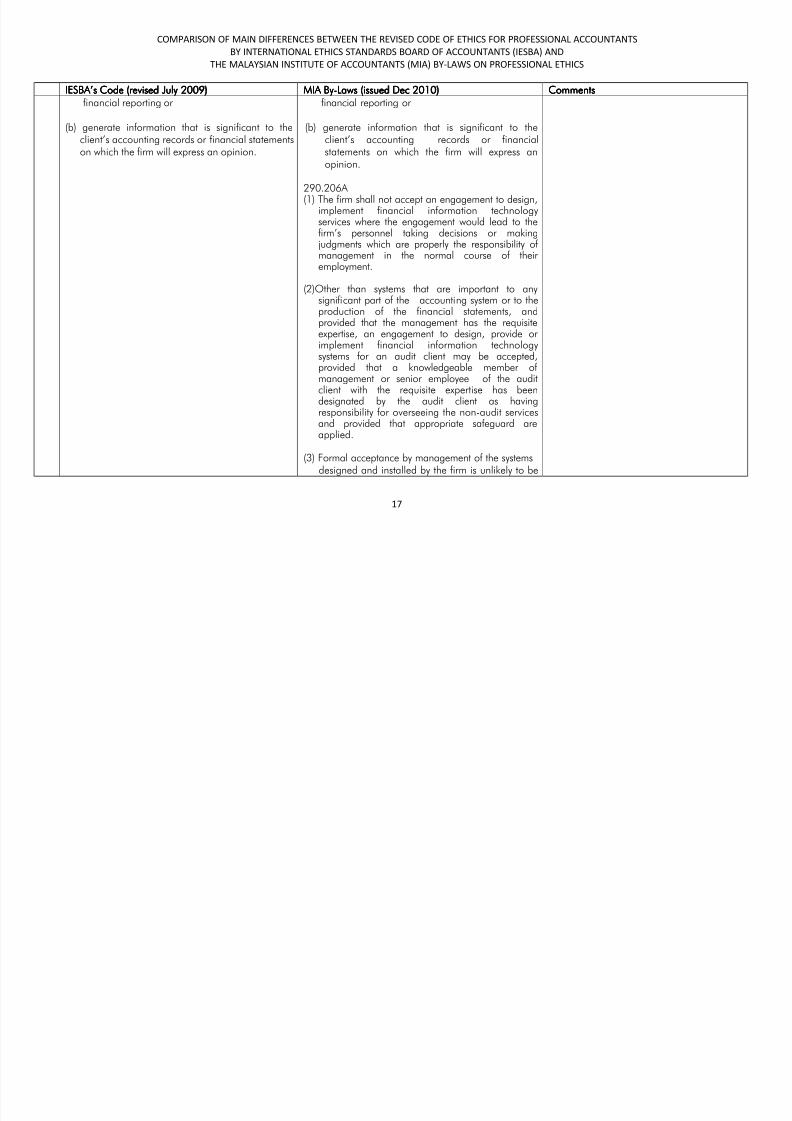

financial reporting or

(b) generate information that is significant to theclient’s accounting records or financial statementson which the firm will express an opinion.

financial reporting or

(b) generate information that is significant to theclient’s accounting records or financialstatements on which the firm will express anopinion.

290.206A

(1) The firm shall not accept an engagement to design,implement financial information technologyservices where the engagement would lead to thefirm’s personnel taking decisions or makingjudgments which are properly the responsibility of management in the normal course of their employment.

(2)Other than systems that are important to anysignificant part of the accounting system or to theproduction of the financial statements, andprovided that the management has the requisiteexpertise, an engagement to design, provide or implement financial information technologysystems for an audit client may be accepted,provided that a knowledgeable member of management or senior employee of the audit

client with the requisite expertise has beendesignated by the audit client as havingresponsibility for overseeing the non-audit servicesand provided that appropriate safeguard areapplied.

(3) Formal acceptance by management of the systemsdesigned and installed by the firm is unlikely to be

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 18/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

18

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

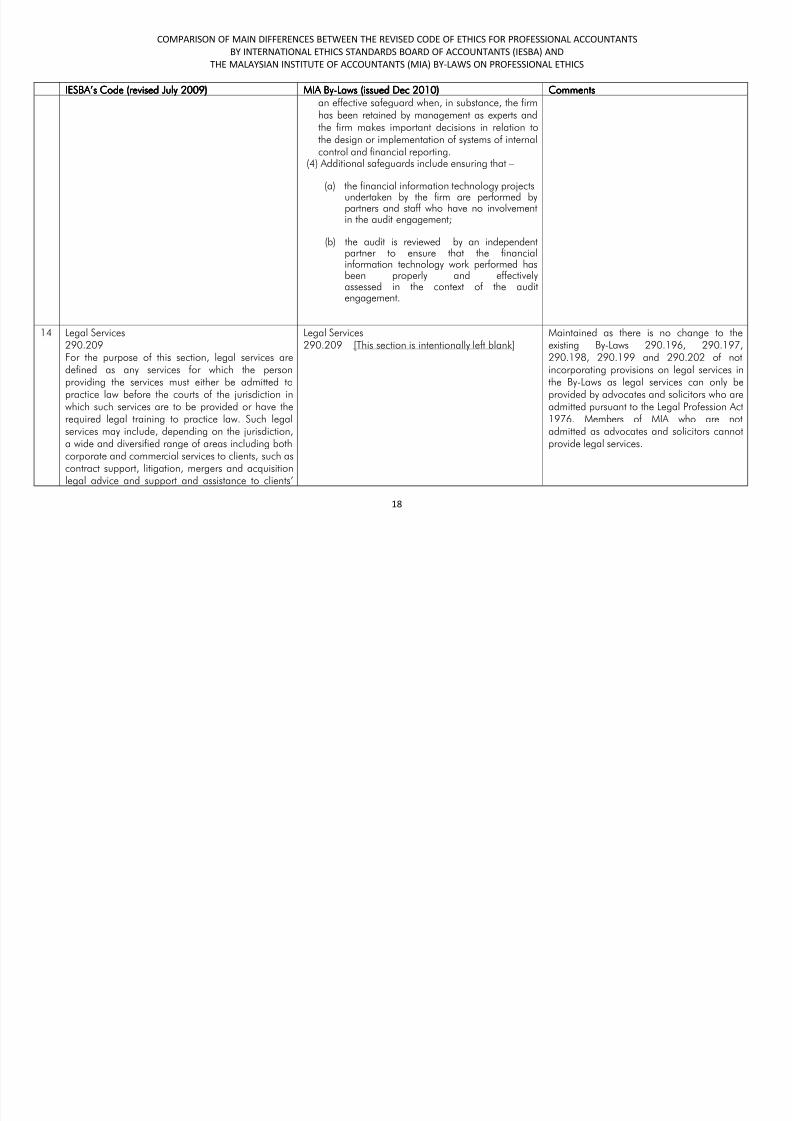

an effective safeguard when, in substance, the firmhas been retained by management as experts andthe firm makes important decisions in relation tothe design or implementation of systems of internalcontrol and financial reporting.

(4) Additional safeguards include ensuring that –

(a) the financial information technology projects

undertaken by the firm are performed bypartners and staff who have no involvementin the audit engagement;

(b) the audit is reviewed by an independentpartner to ensure that the financialinformation technology work performed hasbeen properly and effectivelyassessed in the context of the audit

engagement.

14 Legal Services290.209For the purpose of this section, legal services aredefined as any services for which the personproviding the services must either be admitted to

practice law before the courts of the jurisdiction inwhich such services are to be provided or have therequired legal training to practice law. Such legalservices may include, depending on the jurisdiction,a wide and diversified range of areas including bothcorporate and commercial services to clients, such ascontract support, litigation, mergers and acquisitionlegal advice and support and assistance to clients’

Legal Services290.209 [This section is intentionally left blank]

Maintained as there is no change to theexisting By-Laws 290.196, 290.197,290.198, 290.199 and 290.202 of notincorporating provisions on legal services inthe By-Laws as legal services can only be

provided by advocates and solicitors who areadmitted pursuant to the Legal Profession Act1976. Members of MIA who are notadmitted as advocates and solicitors cannotprovide legal services.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 19/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

19

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

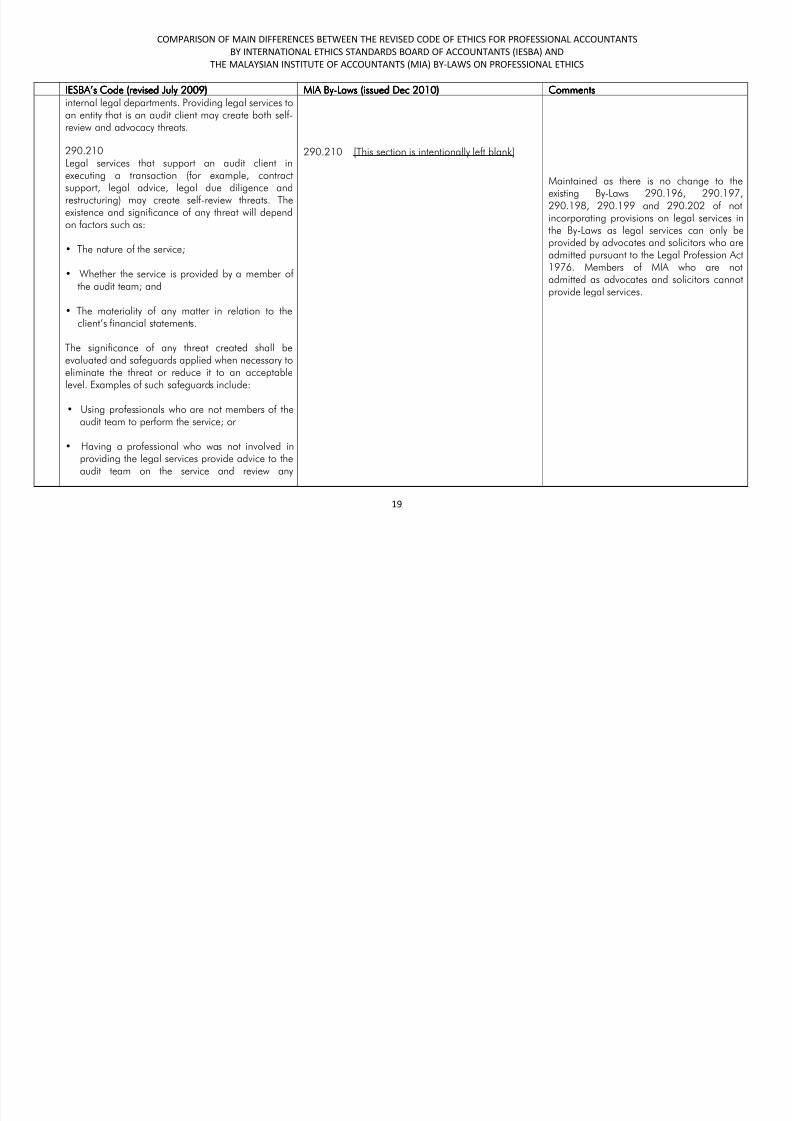

internal legal departments. Providing legal services toan entity that is an audit client may create both self-review and advocacy threats.

290.210Legal services that support an audit client inexecuting a transaction (for example, contractsupport, legal advice, legal due diligence and

restructuring) may create self-review threats. Theexistence and significance of any threat will dependon factors such as:

• The nature of the service;

• Whether the service is provided by a member of the audit team; and

• The materiality of any matter in relation to theclient’s financial statements.

The significance of any threat created shall beevaluated and safeguards applied when necessary toeliminate the threat or reduce it to an acceptablelevel. Examples of such safeguards include:

• Using professionals who are not members of theaudit team to perform the service; or

• Having a professional who was not involved inproviding the legal services provide advice to theaudit team on the service and review any

290.210 [This section is intentionally left blank]

Maintained as there is no change to theexisting By-Laws 290.196, 290.197,290.198, 290.199 and 290.202 of notincorporating provisions on legal services inthe By-Laws as legal services can only beprovided by advocates and solicitors who areadmitted pursuant to the Legal Profession Act1976. Members of MIA who are notadmitted as advocates and solicitors cannot

provide legal services.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 20/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

20

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

financial statement treatment.

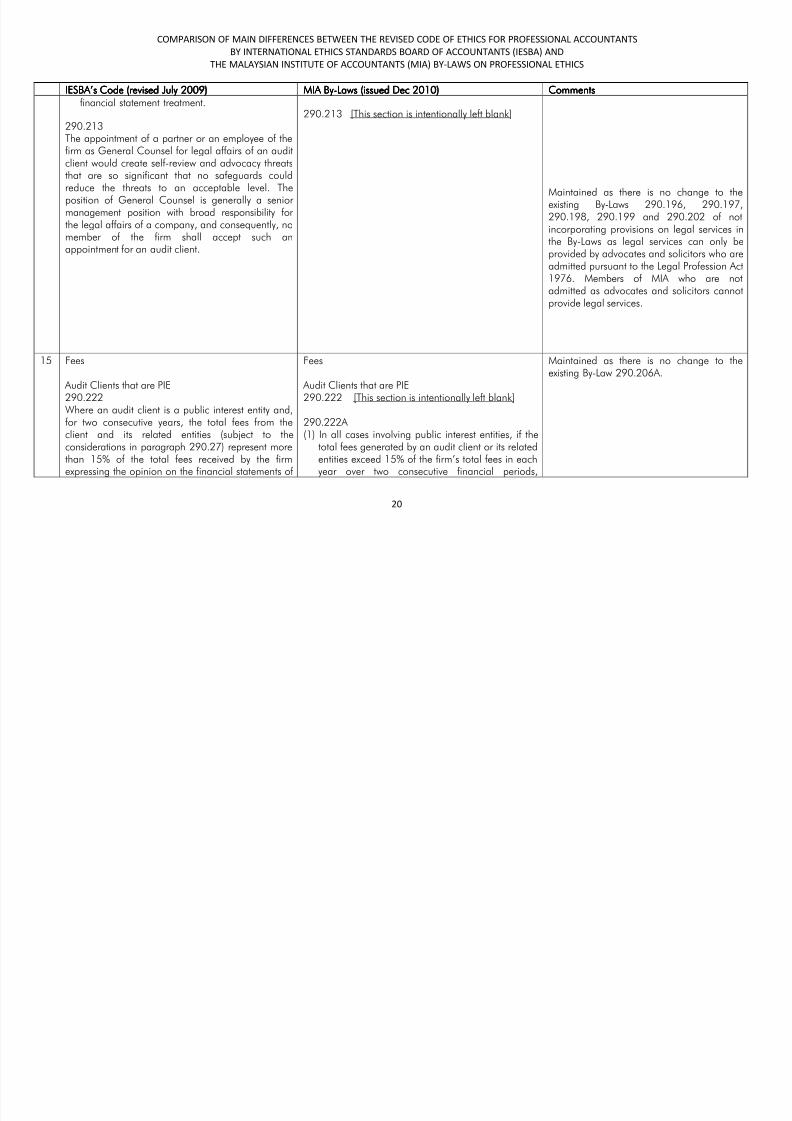

290.213The appointment of a partner or an employee of thefirm as General Counsel for legal affairs of an auditclient would create self-review and advocacy threatsthat are so significant that no safeguards couldreduce the threats to an acceptable level. The

position of General Counsel is generally a senior management position with broad responsibility for the legal affairs of a company, and consequently, nomember of the firm shall accept such anappointment for an audit client.

290.213 [This section is intentionally left blank]

Maintained as there is no change to theexisting By-Laws 290.196, 290.197,290.198, 290.199 and 290.202 of notincorporating provisions on legal services inthe By-Laws as legal services can only beprovided by advocates and solicitors who areadmitted pursuant to the Legal Profession Act1976. Members of MIA who are notadmitted as advocates and solicitors cannotprovide legal services.

15 Fees

Audit Clients that are PIE

290.222Where an audit client is a public interest entity and,for two consecutive years, the total fees from theclient and its related entities (subject to theconsiderations in paragraph 290.27) represent morethan 15% of the total fees received by the firmexpressing the opinion on the financial statements of

Fees

Audit Clients that are PIE

290.222 [This section is intentionally left blank]

290.222A (1) In all cases involving public interest entities, if the

total fees generated by an audit client or its relatedentities exceed 15% of the firm’s total fees in eachyear over two consecutive financial periods,

Maintained as there is no change to theexisting By-Law 290.206A.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 21/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

21

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

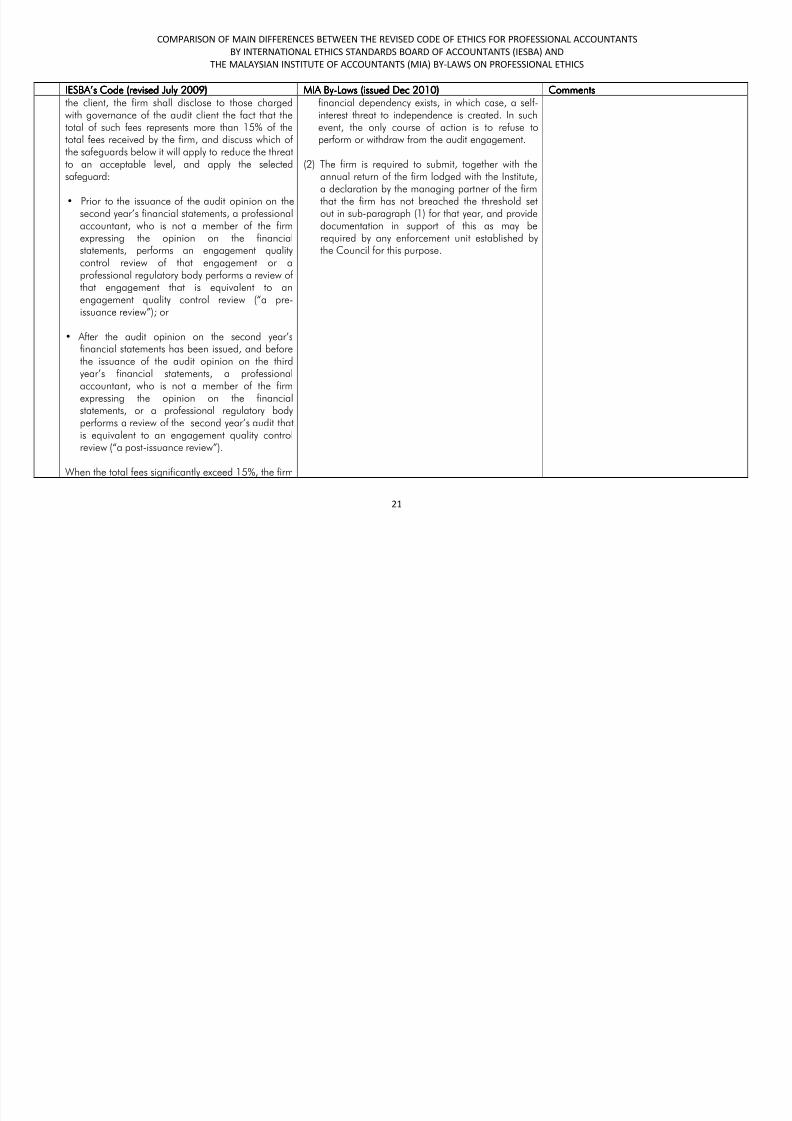

the client, the firm shall disclose to those chargedwith governance of the audit client the fact that thetotal of such fees represents more than 15% of thetotal fees received by the firm, and discuss which of the safeguards below it will apply to reduce the threatto an acceptable level, and apply the selectedsafeguard:

• Prior to the issuance of the audit opinion on thesecond year’s financial statements, a professionalaccountant, who is not a member of the firmexpressing the opinion on the financialstatements, performs an engagement qualitycontrol review of that engagement or aprofessional regulatory body performs a review of that engagement that is equivalent to an

engagement quality control review (“a pre-issuance review”); or

• After the audit opinion on the second year’sfinancial statements has been issued, and beforethe issuance of the audit opinion on the thirdyear’s financial statements, a professionalaccountant, who is not a member of the firm

expressing the opinion on the financialstatements, or a professional regulatory bodyperforms a review of the second year’s audit thatis equivalent to an engagement quality controlreview (“a post-issuance review”).

When the total fees significantly exceed 15%, the firm

financial dependency exists, in which case, a self-interest threat to independence is created. In suchevent, the only course of action is to refuse toperform or withdraw from the audit engagement.

(2) The firm is required to submit, together with theannual return of the firm lodged with the Institute,a declaration by the managing partner of the firm

that the firm has not breached the threshold setout in sub-paragraph (1) for that year, and providedocumentation in support of this as may berequired by any enforcement unit established bythe Council for this purpose.

8/3/2019 Tracking Modifications to IESBA Code

http://slidepdf.com/reader/full/tracking-modifications-to-iesba-code 22/22

COMPARISON OF MAIN DIFFERENCES BETWEEN THE REVISED CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTS

BY INTERNATIONAL ETHICS STANDARDS BOARD OF ACCOUNTANTS (IESBA) AND

THE MALAYSIAN INSTITUTE OF ACCOUNTANTS (MIA) BY-LAWS ON PROFESSIONAL ETHICS

22

IESBA’s CodeIESBA’s CodeIESBA’s CodeIESBA’s Code (revised July 2009)(revised July 2009)(revised July 2009)(revised July 2009) MIA ByMIA ByMIA ByMIA By----LawsLawsLawsLaws (issued Dec 2010)(issued Dec 2010)(issued Dec 2010)(issued Dec 2010) CommentsCommentsCommentsComments

shall determine whether the significance of the threatis such that a post-issuance review would not reducethe threat to an acceptable level and, therefore, apre issuance review is required. In suchcircumstances a pre-issuance review shall beperformed.

Thereafter, when the fees continue to exceed 15%

each year, the disclosure to and discussion withthose charged with governance shall occur and oneof the above safeguards shall be applied. If the feessignificantly exceed 15%, the firm shall determinewhether the significance of the threat is such that apost-issuance review would not reduce the threat toan acceptable level and, therefore, a pre-issuancereview is required. In such circumstances a pre-

issuance review shall be performed.

Note: By-Laws 290.113, 290.118 and 290.171 in the revised By-Laws on Professional Ethics does not include the phrase ‘Subject to the provision of

any written law’ as a statement in the Explanatory Foreword explains that the statutory provisions and laws in Malaysia shall prevail over the By-Laws .

Members are advised that this is nonononot at at at a changechangechangechange to the existing By-Laws. It is implied throughout the By-Laws where applicable that the statutory provisions

and laws in Malaysia shall prevail over the By-Laws.