79

TRADING PLACES TRADING PLACES Presented by: Mr Richard Leech – Executive Director CB Richard Ellis Vietnam August 11th, 2010

TRADING PLACESTRADING PLACES

Presented by:Mr Richard Leech – Executive DirectorCB Richard Ellis VietnamAugust 11th, 2010

CB Richard Ellis | Page 2

WET MARKETWET MARKET

CB Richard Ellis | Page 3

NEW SHOPPING CENTERNEW SHOPPING CENTER

Shopping is the purpose of life……it drives change!

CB Richard Ellis | Page 4

Shopping center

ParkingTraditional Market

Shopping center

Parking

Traditional Market

Shopping centerShopping center

Traditional Market

THE MIXTURETHE MIXTURE

A COMBINATION OF A COMBINATION OF

WET MARKET &WET MARKET &

SHOPPING CENTERSHOPPING CENTER

Parking

EMERGING TRENDS

CRITICAL SUCCESS FACTORS

RECENT CASE STUDIES

DEVELOPER DECISIONS

CB Richard Ellis | Page 6

Benefit from some GREAT locations:In central/great locations for retailOld/traditional retail areas with existing footfallHigh density population with regular variety of customers and income groupsHigh trading density (size of units/sale per square meter)Convenient access

Mixing business with pleasure

&

EMERGING TRENDS EMERGING TRENDS –– THE REBIRTH OF THE WET MARKETTHE REBIRTH OF THE WET MARKET

CB Richard Ellis | Page 7

EMERGING TRENDS EMERGING TRENDS –– THE REBIRTH OF THE WET MARKETTHE REBIRTH OF THE WET MARKET

Revitalization:The rebirth of traditional markets will take the form of modern and well-organized retail concepts (temperature control/fresh air, improved health and hygiene, better fire safety, health and security conditions, organized merchandising,..)

Mixing business with pleasure

CB Richard Ellis | Page 8

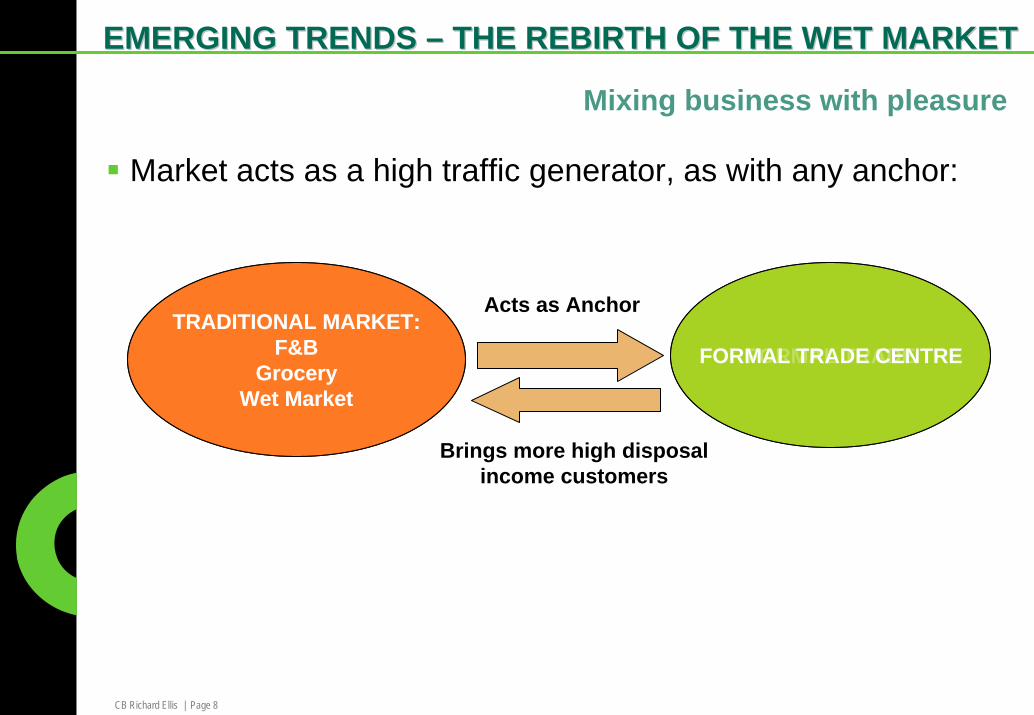

EMERGING TRENDS EMERGING TRENDS –– THE REBIRTH OF THE WET MARKETTHE REBIRTH OF THE WET MARKET

Market acts as a high traffic generator, as with any anchor:

Mixing business with pleasure

TRADITIONAL MARKET:F&B

GroceryWet Market

Acts as Anchor

FORMAL TRADETRADITIONAL MARKET:

F&BGrocery

Wet Market

FORMAL TRADE CENTRE

Brings more high disposal income customers

CB Richard Ellis | Page 9

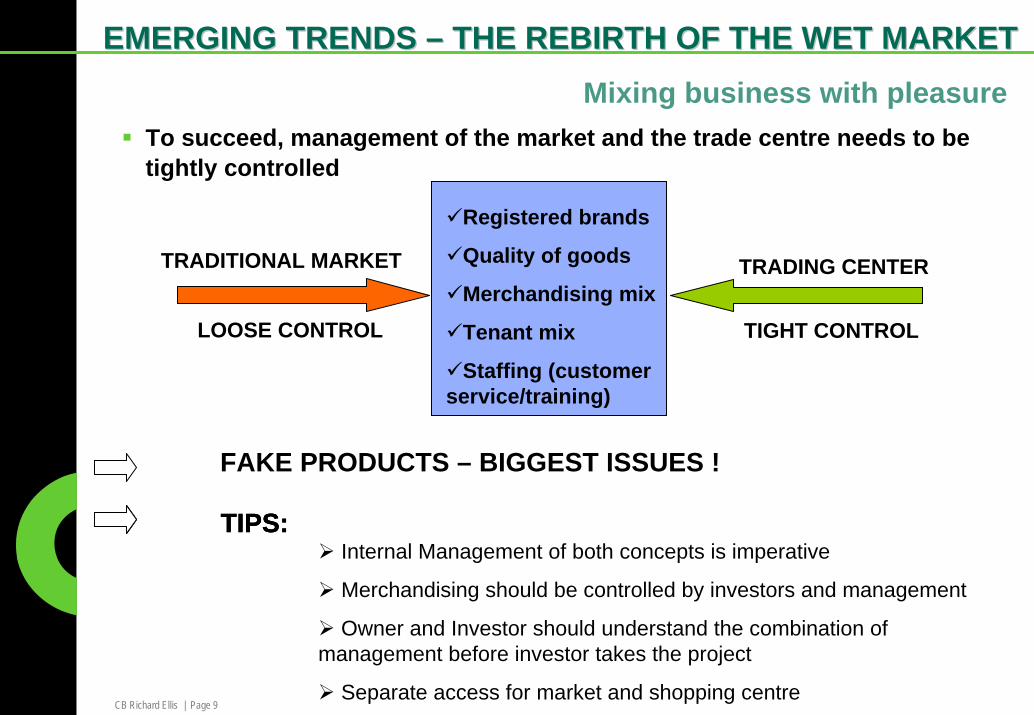

EMERGING TRENDS EMERGING TRENDS –– THE REBIRTH OF THE WET MARKETTHE REBIRTH OF THE WET MARKET

To succeed, management of the market and the trade centre needs to be tightly controlled

Registered brands

Quality of goods

Merchandising mix

Tenant mix

Staffing (customer service/training)

Mixing business with pleasure

TRADITIONAL MARKET TRADING CENTER

LOOSE CONTROL TIGHT CONTROL

TIPS:Internal Management of both concepts is imperative

Merchandising should be controlled by investors and management

Owner and Investor should understand the combination of management before investor takes the project

Separate access for market and shopping centre

FAKE PRODUCTS – BIGGEST ISSUES !

TIPS:TIPS:

CB Richard Ellis | Page 10

EMERGING TRENDS EMERGING TRENDS –– MULTIPLEX CINEMAS AND ENTERTAINMENTMULTIPLEX CINEMAS AND ENTERTAINMENT

Foot traffic…….and their importance to the success of the centre

Multiplex cinemas and entertainment centre’s are attracting thousands of additional feet.

Increasing foot traffic

Creates the opportunity for other space users, particularly food and beverage to increase their turnover from these mid to high income spenders.

CB Richard Ellis | Page 11

EMERGING TRENDS EMERGING TRENDS –– MULTIPLEX CINEMAS AND ENTERTAINMENTMULTIPLEX CINEMAS AND ENTERTAINMENT

Trading hours…….and their importance to the success of the centre

The trading hours of the centre are extended to serve the needs of the cinema and

entertainment goers creating more opportunities amongst other space users to increase

revenue.

Advertising

Customers, especially young people are paying more attention to movie

advertisements or kinds of entertainment.

Results in advertising support for the whole shopping centre

CB Richard Ellis | Page 12

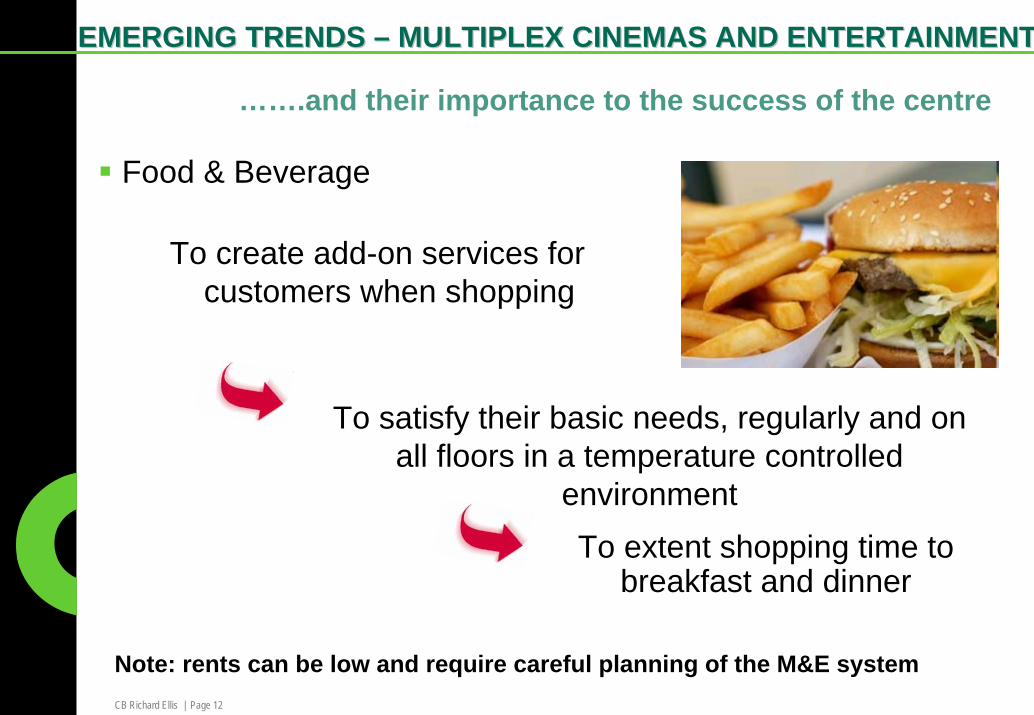

Food & Beverage

EMERGING TRENDS EMERGING TRENDS –– MULTIPLEX CINEMAS AND ENTERTAINMENTMULTIPLEX CINEMAS AND ENTERTAINMENT

…….and their importance to the success of the centre

To create add-on services for customers when shopping

To satisfy their basic needs, regularly and on all floors in a temperature controlled

environmentTo extent shopping time to

breakfast and dinner

Note: rents can be low and require careful planning of the M&E system

CB Richard Ellis | Page 13

…….and their importance to the success of the centre

With a lack of outside entertainment options, a young, urbanized and sizable population, the mall will

become the new town centre, and the entertainment is the spice.

EMERGING TRENDS EMERGING TRENDS –– MULTIPLEX CINEMAS AND ENTERTAINMENTMULTIPLEX CINEMAS AND ENTERTAINMENT

CB Richard Ellis | Page 14

CB Richard Ellis | Page 15

SUCCESS AND FAILURESUCCESS AND FAILURECritical success factors of a shopping center

Hardware design

• Lay-out: try to avoid secondary corridors, and dead-ends

regular race-track design in a rectangular mall has proved

successful.

• Accessibility: infrastructure (road, public transportation,…)

• Design the shopping centre before construction, not during or

after.Software planning:

• Tenant mix: research, propose and select the tenants that best

match not only with the shopping center’s market positioning but

also reflect the demands of the target customers.

• Target market: identify by researching population demographics,

consumption demand and living habits.

Planning in advance of a shopping center

CB Richard Ellis | Page 16

SUCCESS AND FAILURESUCCESS AND FAILURE

Critical success factors of a shopping centreLeasing Strategy – Marketing

Effective marketing campaigns

Create a strong image and reputation in the minds of the prospect tenants and consumers

Create more local and international leasing opportunities

Success of the shopping centre

CB Richard Ellis | Page 17

SUCCESS AND FAILURESUCCESS AND FAILURE

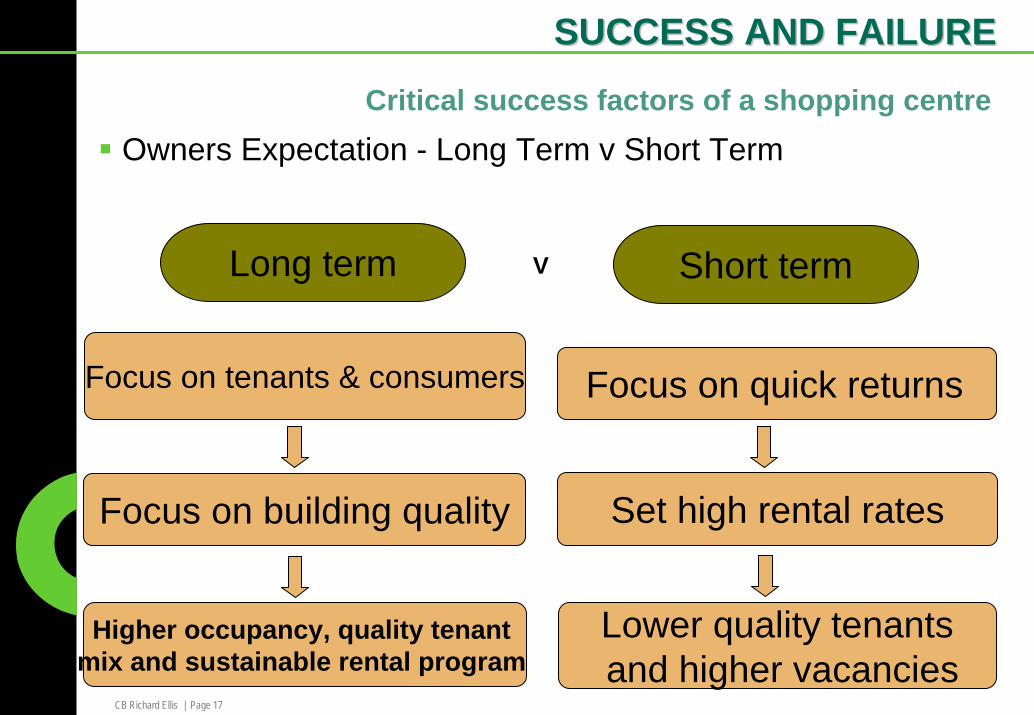

Critical success factors of a shopping centreOwners Expectation - Long Term v Short Term

Focus on tenants & consumers

Long term Short term

Focus on building quality

Higher occupancy, quality tenant mix and sustainable rental program

Focus on quick returns

Set high rental rates

Lower quality tenantsand higher vacancies

V

CB Richard Ellis | Page 18

SUCCESS AND FAILURESUCCESS AND FAILURECritical success factors of a shopping centre

Retail Management – incl. promotions/serviceSpecific, active retail management plays a vital role in the success of the centre.Ongoing advertising & promotions plan will generate more feet and an exciting and compelling retail space. Maintaining high standards of service will contribute to the long term success of the centre.

CB Richard Ellis | Page 19

FROM THE NORTH

TO THE SOUTH

CB Richard Ellis | Page 20

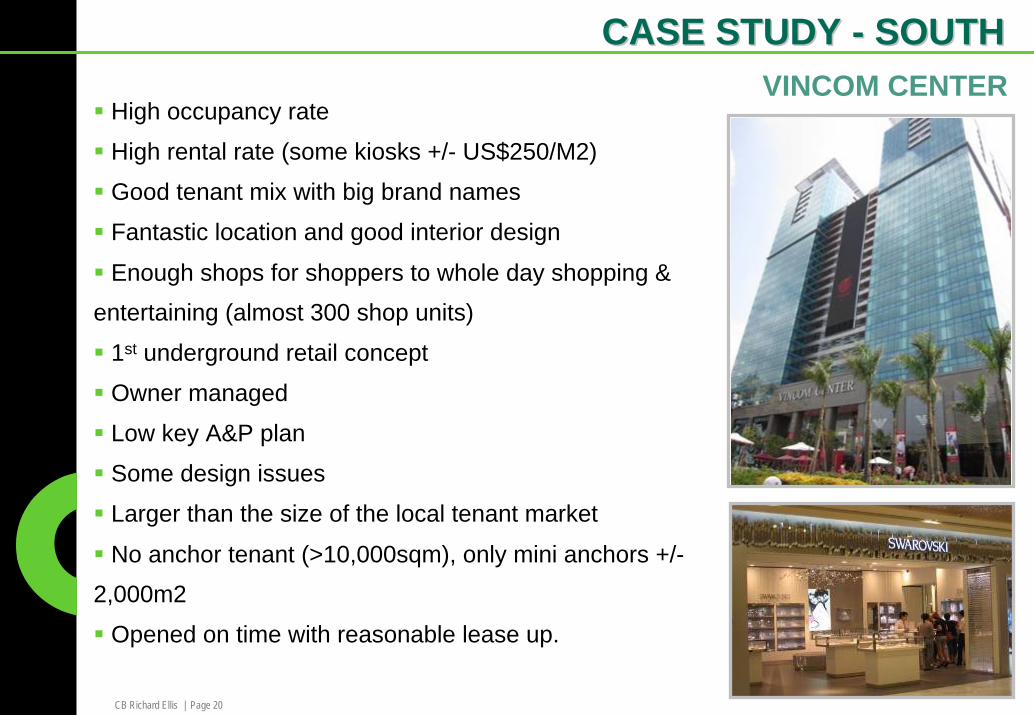

CASE STUDY CASE STUDY -- SOUTHSOUTH

High occupancy rate

High rental rate (some kiosks +/- US$250/M2)

Good tenant mix with big brand names

Fantastic location and good interior design

Enough shops for shoppers to whole day shopping & entertaining (almost 300 shop units)

1st underground retail concept

Owner managed

Low key A&P plan

Some design issues

Larger than the size of the local tenant market

No anchor tenant (>10,000sqm), only mini anchors +/-2,000m2

Opened on time with reasonable lease up.

VINCOM CENTER

CB Richard Ellis | Page 21

Good quality complex (Hotel – Office – Retail)

Decentralized location (west-new CBD)

No anchor (although Big C, almost opposite acts as an anchor)

New concept of food court on 5th level

Owner managed but with international management consultancy

High number of small shopsOpened, on time, but then partly closed again to

complete fitting out, will re-open in August 2010Reasonable interior design and layout.

CASE STUDY CASE STUDY -- NORTHNORTHGRAND PLAZA

CB Richard Ellis | Page 22

DEVELOPERDEVELOPER’’S DECISIONSS DECISIONS

…… and what keeps them awake at night

CB Richard Ellis | Page 23

DEVELOPERDEVELOPER’’S DECISIONSS DECISIONS…….and what keeps them awake at night

SINGLE ANCHOR versus MULTIPLE TENANTSRent – Gross area basisUpfront Commitment Management & operationsLease termHandover conditionMarketing – Project branding

CB Richard Ellis | Page 24

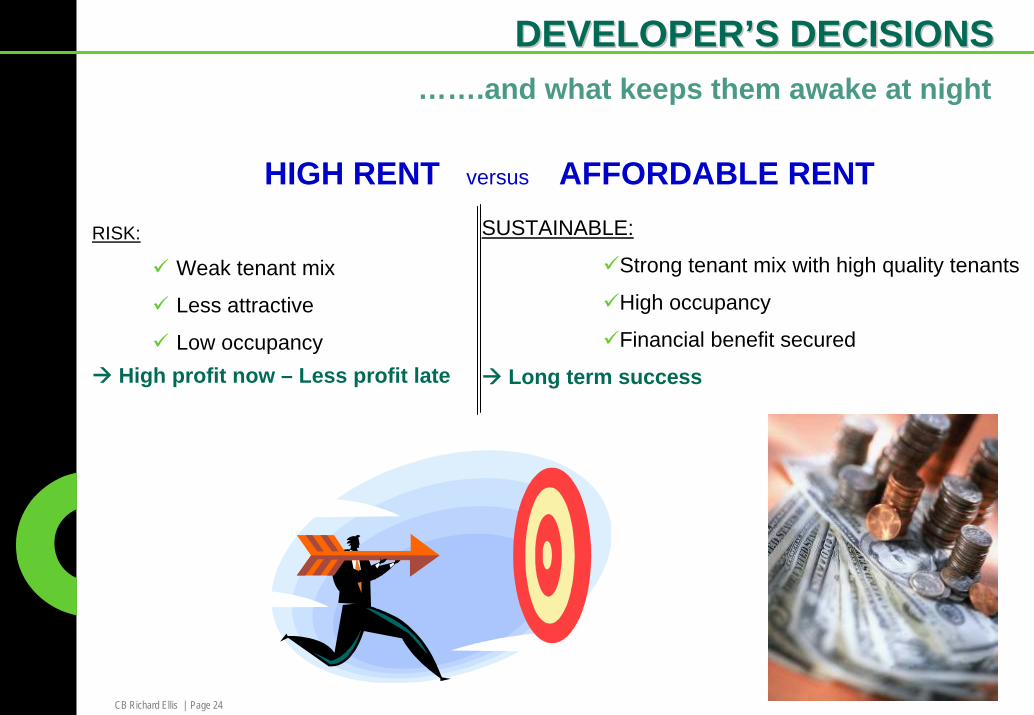

HIGH RENT versus AFFORDABLE RENTRISK:

Weak tenant mix

Less attractive

Low occupancyHigh profit now – Less profit late

SUSTAINABLE:

Strong tenant mix with high quality tenants

High occupancy

Financial benefit secured

Long term success

DEVELOPERDEVELOPER’’S DECISIONSS DECISIONS…….and what keeps them awake at night

CB Richard Ellis | Page 25

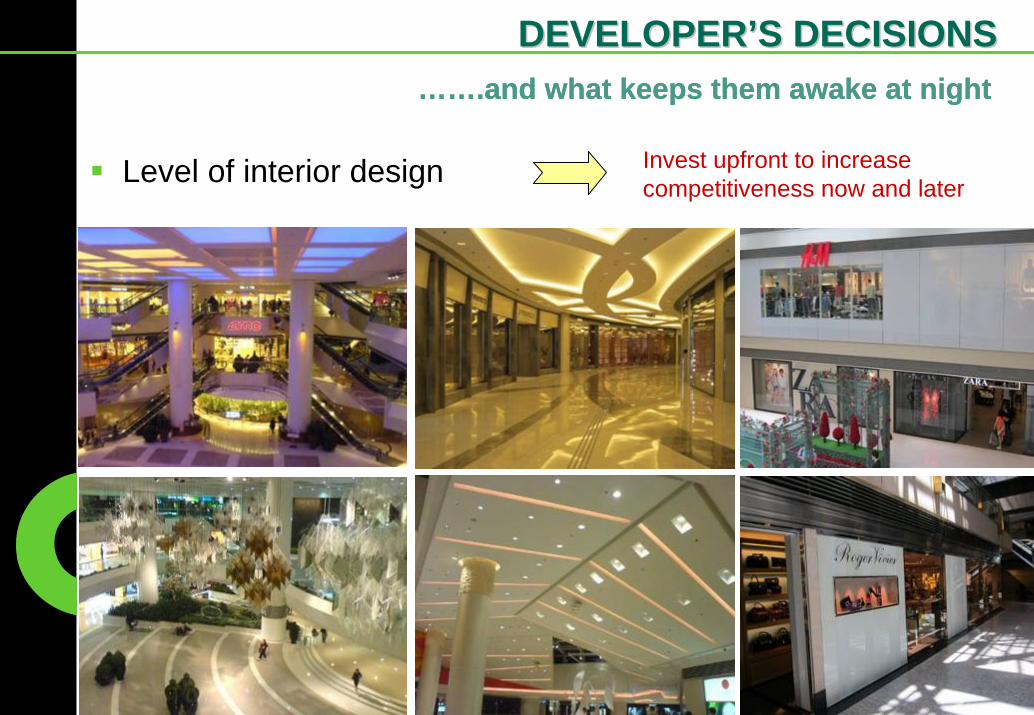

Level of interior design

…….and what keeps them awake at night

Invest upfront to increase competitiveness now and later

DEVELOPERDEVELOPER’’S DECISIONSS DECISIONS…….and what keeps them awake at night

CB Richard Ellis | Page 26

Landlord handover condition (ceiling, floor, shop fronts, etc)

Not ready on timeLack of uniformity

Maximize income from rental

More planning in advance

More time for tenants

High quality tenants

Stringent fitting out regulations

High occupancy with competitive rent

DEVELOPERDEVELOPER’’S DECISIONSS DECISIONS…….and what keeps them awake at night

LESS FROM LANDLORD

MATURE MARKET NEEDS:

HCMC RETAIL MARKET OVERVIEW

CB Richard Ellis | Page 28

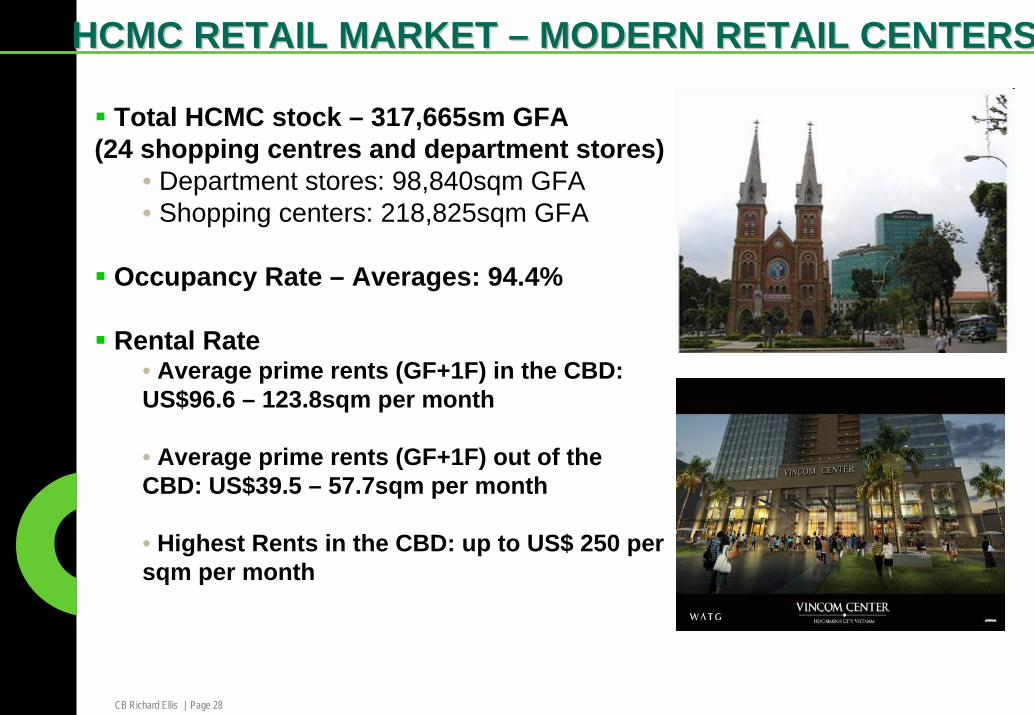

HCMC RETAIL MARKET HCMC RETAIL MARKET –– MODERN RETAIL CENTERSMODERN RETAIL CENTERS

Total HCMC stock – 317,665sm GFA (24 shopping centres and department stores)

• Department stores: 98,840sqm GFA• Shopping centers: 218,825sqm GFA

Occupancy Rate – Averages: 94.4%

Rental Rate• Average prime rents (GF+1F) in the CBD:US$96.6 – 123.8sqm per month

• Average prime rents (GF+1F) out of the CBD: US$39.5 – 57.7sqm per month

• Highest Rents in the CBD: up to US$ 250 per sqm per month

CB Richard Ellis | Page 29

HCMC CURRENT RETAIL SUPPLY HCMC CURRENT RETAIL SUPPLY –– MAJOR PROJECTSMAJOR PROJECTS

CB Richard Ellis | Page 30

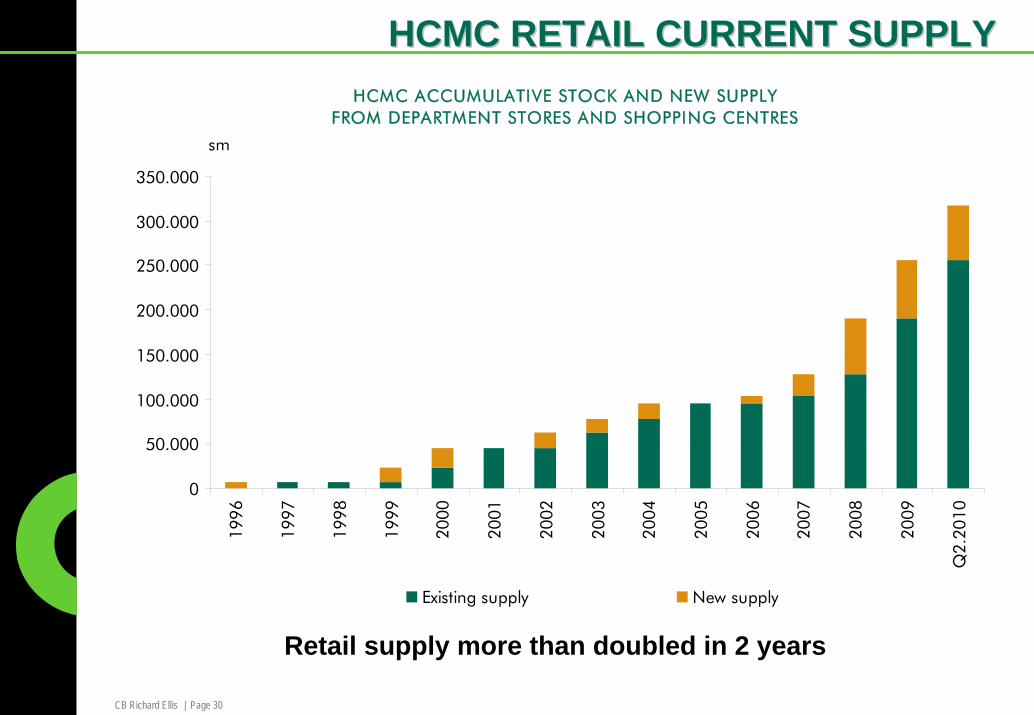

HCMC RETAIL CURRENT SUPPLYHCMC RETAIL CURRENT SUPPLY

Retail supply more than doubled in 2 years

HCMC ACCUMULATIVE STOCK AND NEW SUPPLY FROM DEPARTMENT STORES AND SHOPPING CENTRES

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Q2.

2010

sm

Existing supply New supply

CB Richard Ellis | Page 31

Current Market

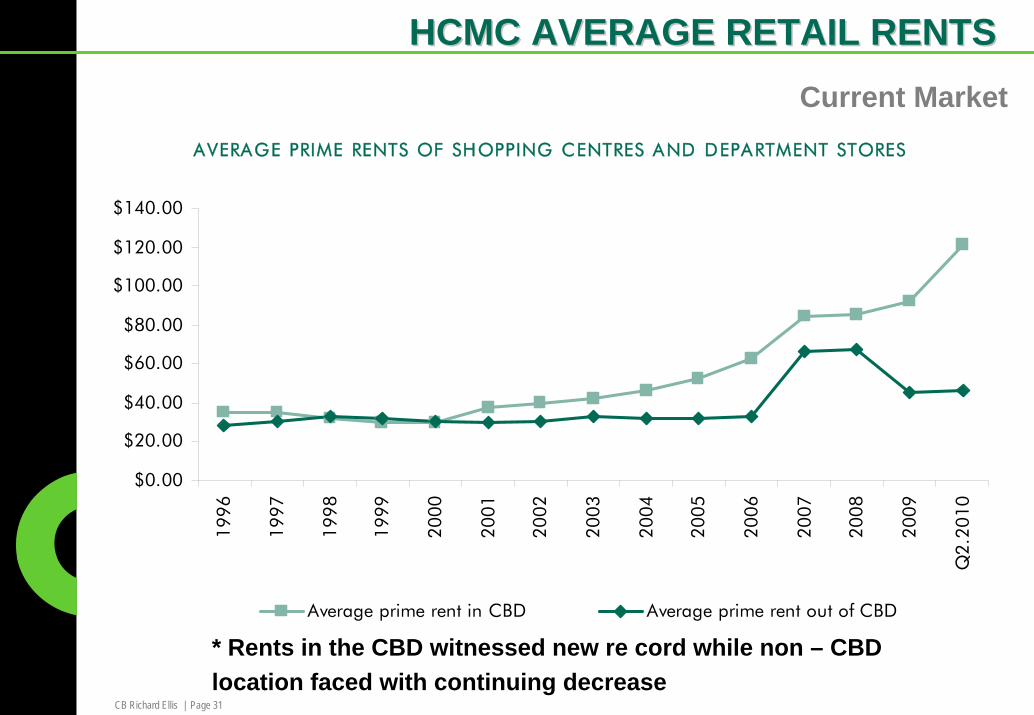

HCMC AVERAGE RETAIL RENTSHCMC AVERAGE RETAIL RENTS

AVERAGE PRIME RENTS OF SHOPPING CENTRES AND DEPARTMENT STORES

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.0019

96

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Q2.

2010

Average prime rent in CBD Average prime rent out of CBD

* Rents in the CBD witnessed new re cord while non – CBD location faced with continuing decrease

CB Richard Ellis | Page 32

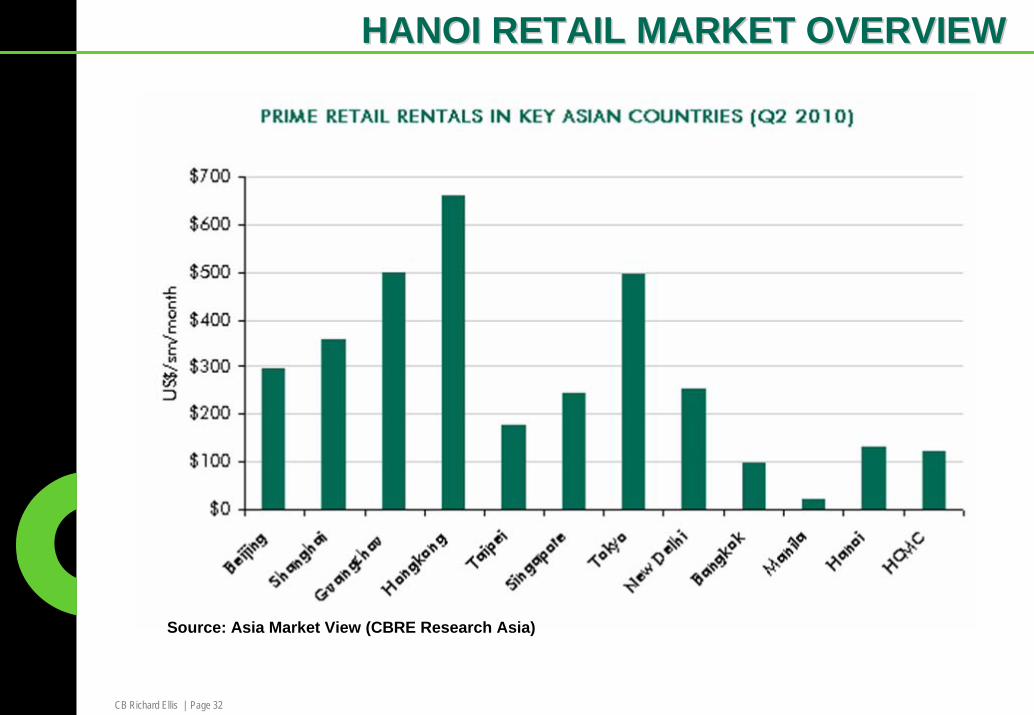

HANOI RETAIL MARKET OVERVIEWHANOI RETAIL MARKET OVERVIEW

Source: Asia Market View (CBRE Research Asia)

CB Richard Ellis | Page 33

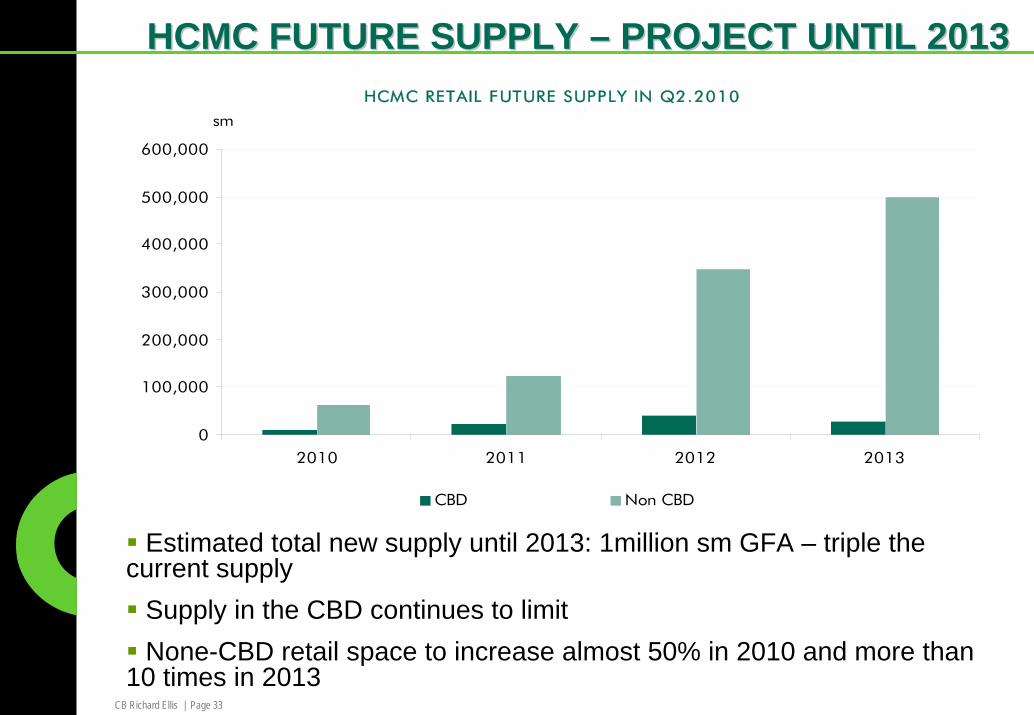

HCMC FUTURE SUPPLY HCMC FUTURE SUPPLY –– PROJECT UNTIL 2013PROJECT UNTIL 2013HCMC RETAIL FUTURE SUPPLY IN Q2.2010

0

100,000

200,000

300,000

400,000

500,000

600,000

2010 2011 2012 2013

sm

CBD Non CBD

Estimated total new supply until 2013: 1million sm GFA – triple the current supply

Supply in the CBD continues to limitNone-CBD retail space to increase almost 50% in 2010 and more than

10 times in 2013

CB Richard Ellis | Page 34

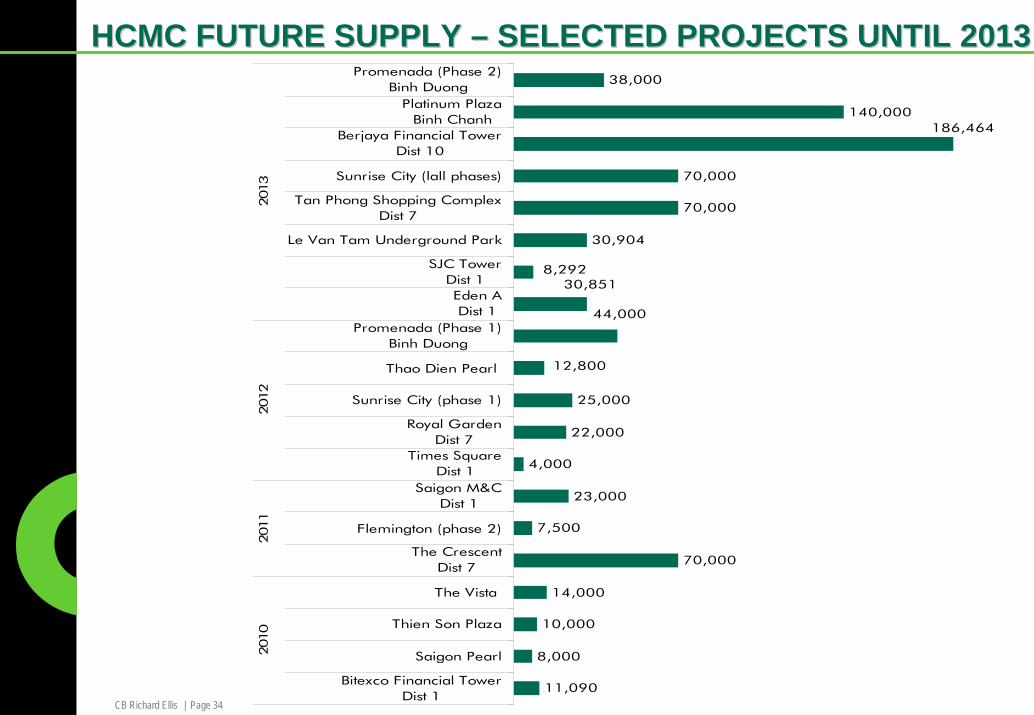

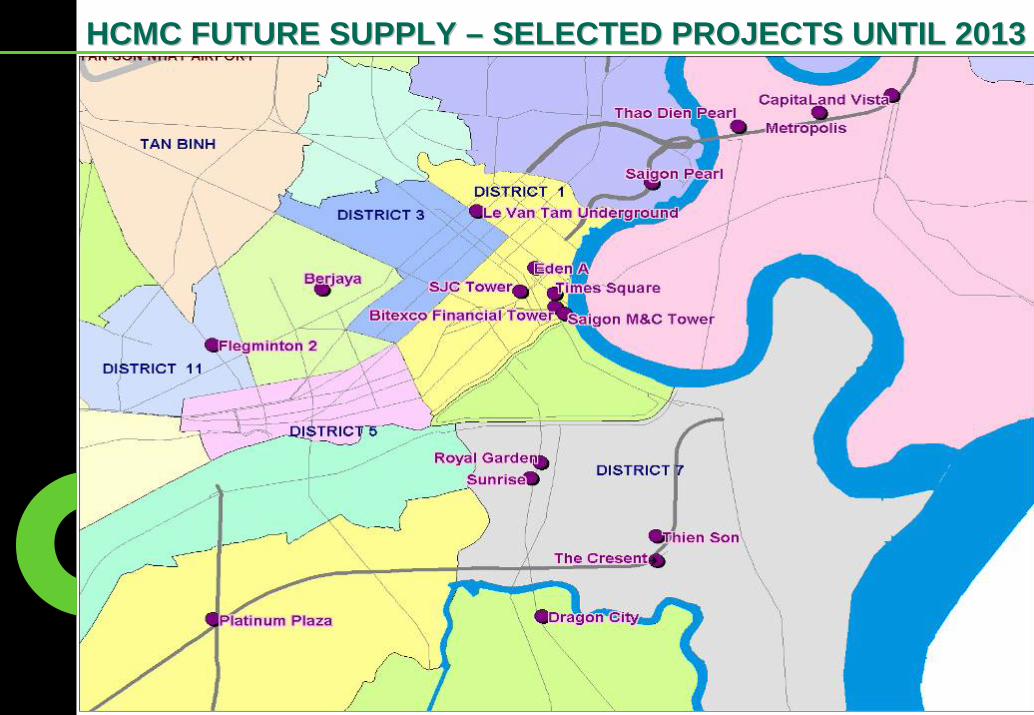

HCMC FUTURE SUPPLY HCMC FUTURE SUPPLY –– SELECTED PROJECTS UNTIL 2013SELECTED PROJECTS UNTIL 2013

11,090

8,000

10,000

14,000

70,000

7,500

23,000

4,000

22,000

25,000

30,904

70,000

70,000

140,000

38,000

12,800

30,8518,292

44,000

186,464

Bitexco Financial TowerDist 1

Saigon Pearl

Thien Son Plaza

The Vista

The CrescentDist 7

Flemington (phase 2)

Saigon M&CDist 1

Times SquareDist 1

Royal GardenDist 7

Sunrise City (phase 1)

Thao Dien Pearl

Promenada (Phase 1)Binh Duong

Eden ADist 1

SJC TowerDist 1

Le Van Tam Underground Park

Tan Phong Shopping ComplexDist 7

Sunrise City (lall phases)

Berjaya Financial TowerDist 10

Platinum PlazaBinh Chanh

Promenada (Phase 2)Binh Duong

2010

2011

2012

2013

CB Richard Ellis | Page 35

HCMC FUTURE SUPPLY HCMC FUTURE SUPPLY –– SELECTED PROJECTS UNTIL 2013SELECTED PROJECTS UNTIL 2013

CB Richard Ellis | Page 36

BITEXCO FINANCIAL TOWER

HCMC FUTURE RETAIL SUPPLY HCMC FUTURE RETAIL SUPPLY -- 20102010

Location: 1 Ho Tung Mau, Dist 1, HCMC

Developer: BitexcoLand

Concept: Grade A Office & Retail

Retail: 11,000sqm NLA – inc 3 upper levels

Attraction: Iconic landmark in HCMC

Opening: October 2010

CB Richard Ellis | Page 37

Location: Le Dai Hanh, Dist. 11

Developer: Pau Jar Group (Taiwan)

Retail GFA: 7,500sqm (5 levels)

Concept: Retail F&B & Office Services

Expected Completion: Q1, 2011

Status: Under construction

THE FLEMINGTON – PHASE 2

HCMC FUTURE RETAIL SUPPLY HCMC FUTURE RETAIL SUPPLY -- 20112011

CB Richard Ellis | Page 38

Location: District 2 HCMC (4-6 km from CBD)

Developer: VN Capital land Group

Retail NLA: 5,000sqm

Status: Advanced construction

Completion: Q2, 2011

HCMC HCMC –– NEW RETAIL SUPPLY NEW RETAIL SUPPLY -- 20112011

THE VISTA

CB Richard Ellis | Page 39

HCMC HCMC –– NEW RETAIL SUPPLY NEW RETAIL SUPPLY -- 20112011

Location: Dual frontage Nguyen Hue & Dong Khoi, D1

Developer: Times Square (VN) Investment Joint Stock

Co.

Retail NLA: 4,000sqm

Concept: world-class tower, mixed use development

including luxury shopping, office space & high-end

hotel.

Status: under construction

Completion: Q4, 2011

TIMES SQUARE

CB Richard Ellis | Page 40

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20112011Location: Phu My Hung City

Developer: Phu My Hung Corporation

Construction site: 112,000sqm (6 floors & 3 basements)

Retail GFA: Eventually over 70,000sqm over several phases

• supermarket: 6,000sqm

• entertainment: 3,000sqm (including 8 cinema rooms)

Status: Under construction

Completion: Phased opening between Sept 10 and Oct 11

CRESCENT MALL

CB Richard Ellis | Page 41

Location: Binh Duong

Developer: ECC Invest / GuocoLand

Adjacent to VSIP and Song Be Golf Course

GFA: 82,000sqm - 4 floors

Concept: “More Than Just Shopping”, a vibrant

lifestyle destination for residents of HCMC, Binh

Duong and other neighboring provinces.

Status: construction commenced Nov 2007

Expected Completion:

• Phase 1: Q3/2011

• Phase 2: Q4/2012

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20112011PROMENADA @ CANARY

CB Richard Ellis | Page 42

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20112011

Location: Intersection of triangle (Ham Nghi -Ton

Duc Thang – Chuong Duong streets), Dist.1 - HCMC

Developer: Saigon M&C

Retail GFA: 23,000sqm

Concept: Mixed use development: residential, office

and shopping center

• Retail podium: 6 floors (23,000sqm)

• Office components: 34 floors (49,000sqm)

• Residential components: 133 condo

Status: Under construction

Completion: 2011

SAIGON M&C TOWER

CB Richard Ellis | Page 43

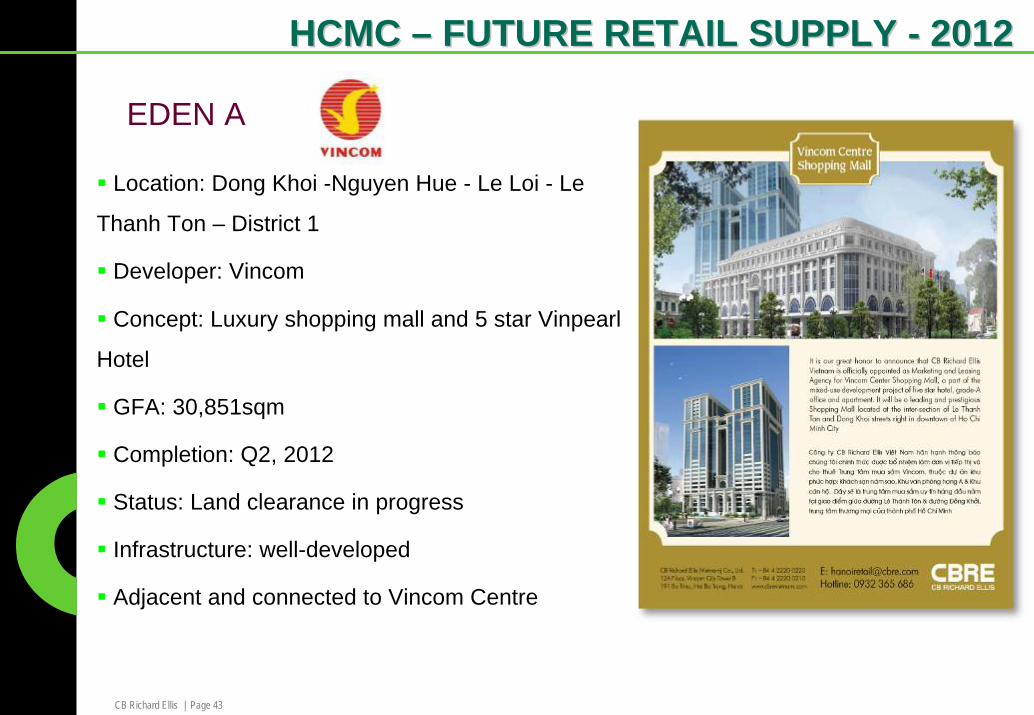

Location: Dong Khoi -Nguyen Hue - Le Loi - Le

Thanh Ton – District 1

Developer: Vincom

Concept: Luxury shopping mall and 5 star Vinpearl

Hotel

GFA: 30,851sqm

Completion: Q2, 2012

Status: Land clearance in progress

Infrastructure: well-developed

Adjacent and connected to Vincom Centre

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012

EDEN A

CB Richard Ellis | Page 44

Location: Nguyen Van Linh, 7 Dist.

Developer: JV of Saigon Co-op (SCID); Samco; Mapletree

Invst. (Singapore)

Total land area: 4.4ha

Concept: office, retail and apartment

Retail GFA: 70,000sqm

Apartment GFA: 60,000sqm

Office GFA: 100,000sqm

Expected completion: 2012

TAN PHONG SHOPPING COMPLEXHCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012

CB Richard Ellis | Page 45

Location: Nguyen Huu Tho, Dist 7 – HCMC

Developer: Novaland (Nova Real Estate Joint Stock Co.)

Concept: high-rise complex incl. retail, trade centre, apartments

GFA: 52 ha

Retail GFA: 25,000sqm (Phase 1)

70,000spm (all phases)

Status: Under construction

Completion: Q4 2012 (Phase 1)

SUNRISE CITY

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012

CB Richard Ellis | Page 46

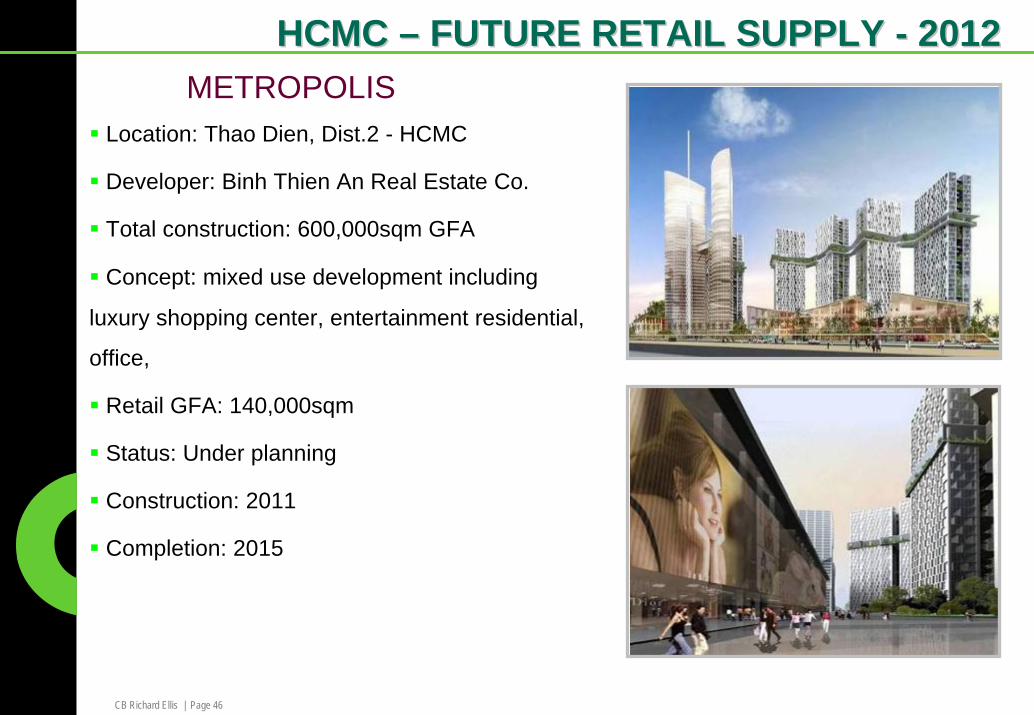

Location: Thao Dien, Dist.2 - HCMC

Developer: Binh Thien An Real Estate Co.

Total construction: 600,000sqm GFA

Concept: mixed use development including

luxury shopping center, entertainment residential,

office,

Retail GFA: 140,000sqm

Status: Under planning

Construction: 2011

Completion: 2015

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012METROPOLIS

CB Richard Ellis | Page 47

Location: An Phu Ward, Dist. 2

Developer: Keppel Land

Site GFA: 64 ha – 25 minutes from CBD

Concept : “healthy lifestyle” residential township

(with 3,500 condo) and 14 ha for sport facilities

(to be developed over 10 years)

Status: Under planning review

Completion: 2012 onward

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012SPORTS CITY

CB Richard Ellis | Page 48

Location: 12 Quoc Huong street - Thao Dien ward - District 2 HCMC

Developer: SSG Group

Concept: Complex of luxury shopping center and apartment

Site GFA: 12,800sqm

Construction GFA: 90,000sqm

GFA Retail: 18,500sqm on 4 floors

Status: Under planning review

Completion: Q4 - 2012

THAO DIEN PEARL

HCMC HCMC –– FUTURE RETAIL SUPPLY FUTURE RETAIL SUPPLY -- 20122012

Infrastructure: Attached to proposed

light rail system

CB Richard Ellis | Page 49

Location: Le Hong Phong, Dist.10

Developer: Berjaya (Malaysia)

GFA: 186,464sqm

Status: Under planning

Completion: 2013

Infrastructure: well developed

HCMC HCMC –– NEW RETAIL SUPPLY NEW RETAIL SUPPLY -- 20132013

SAIGON FINANCIAL CENTER

CB Richard Ellis | Page 50

HCMC FUTURE RETAIL SUPPLYHCMC FUTURE RETAIL SUPPLY

Location: 600A Dien Bien Phu street, Ward 22,

Binh Thanh Dist, Ho Chi Minh city

Developer: Daewon – Thu Duc Housing

Development Corporation

Concept: 2 towers of 36 storeys, retail center,

office building and apartment complex

Retail GFA: 20,000sqm

CANTAVIL AN PHU – PHASE 2

Attraction: Impressive landmark

development at the gate of HCMC,

promising to provide luxury modern urban,

comfortable living environment and

international standards offices and shopping

center

Opening: TBC

CB Richard Ellis | Page 51

HCMC FUTURE RETAIL SUPPLYHCMC FUTURE RETAIL SUPPLY

Location: 92 Nguyen Huu Canh, Binh Thanh Dist.

Developer: Vietnam Land SSG

Concept: Residential and retail podium

Residential: 1,500 apartments

Retail GFA: 8,000sqm (2 levels)

Status: Under construction

Completion: Dec 2010/Early 2011

SAIGON PEARL

HANOI RETAIL MARKET OVERVIEW

CB Richard Ellis | Page 53

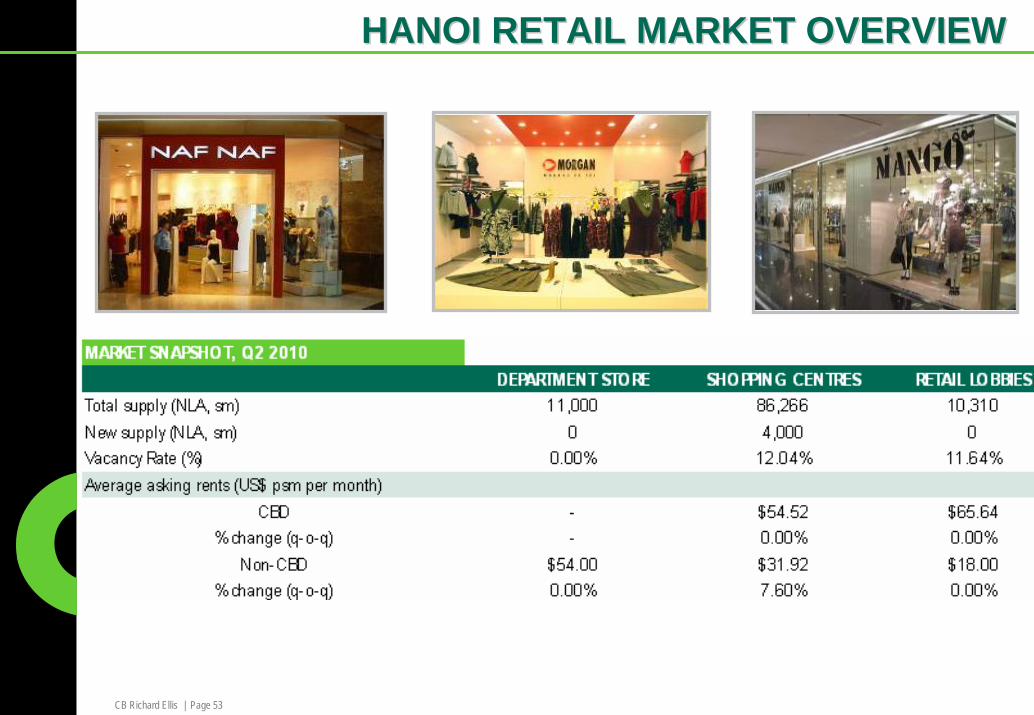

HANOI RETAIL MARKET OVERVIEWHANOI RETAIL MARKET OVERVIEW

CB Richard Ellis | Page 54

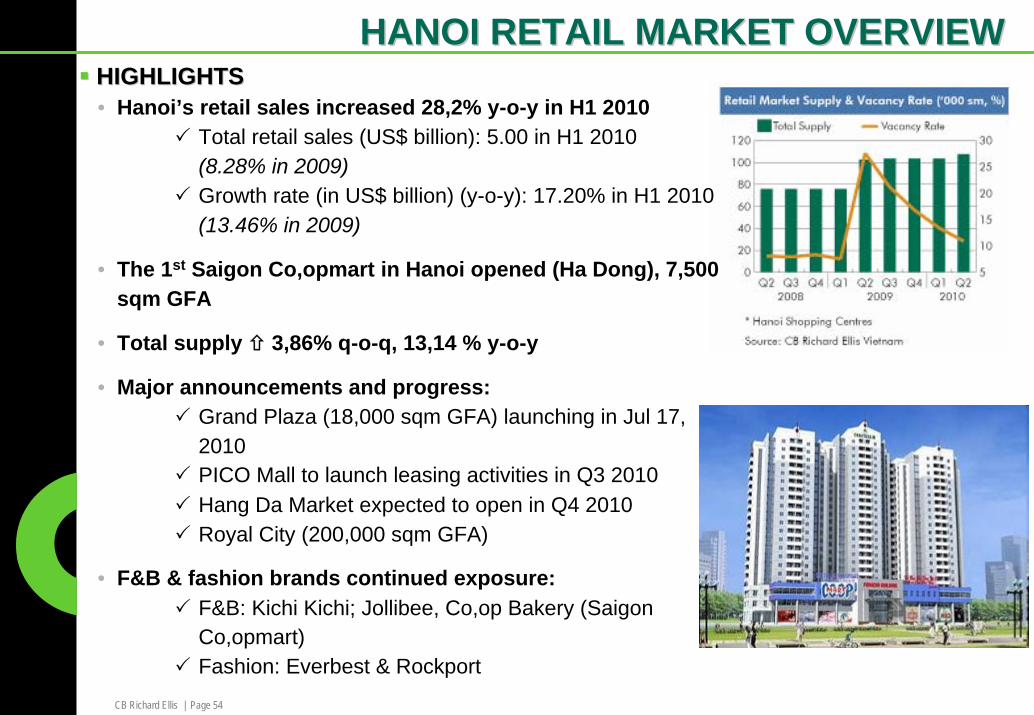

HANOI RETAIL MARKET OVERVIEWHANOI RETAIL MARKET OVERVIEWHIGHLIGHTSHIGHLIGHTS• Hanoi’s retail sales increased 28,2% y-o-y in H1 2010

Total retail sales (US$ billion): 5.00 in H1 2010 (8.28% in 2009)Growth rate (in US$ billion) (y-o-y): 17.20% in H1 2010 (13.46% in 2009)

• The 1st Saigon Co,opmart in Hanoi opened (Ha Dong), 7,500 sqm GFA

• Total supply 3,86% q-o-q, 13,14 % y-o-y

• Major announcements and progress:Grand Plaza (18,000 sqm GFA) launching in Jul 17, 2010PICO Mall to launch leasing activities in Q3 2010Hang Da Market expected to open in Q4 2010Royal City (200,000 sqm GFA)

• F&B & fashion brands continued exposure:F&B: Kichi Kichi; Jollibee, Co,op Bakery (Saigon Co,opmart)Fashion: Everbest & Rockport

CB Richard Ellis | Page 55

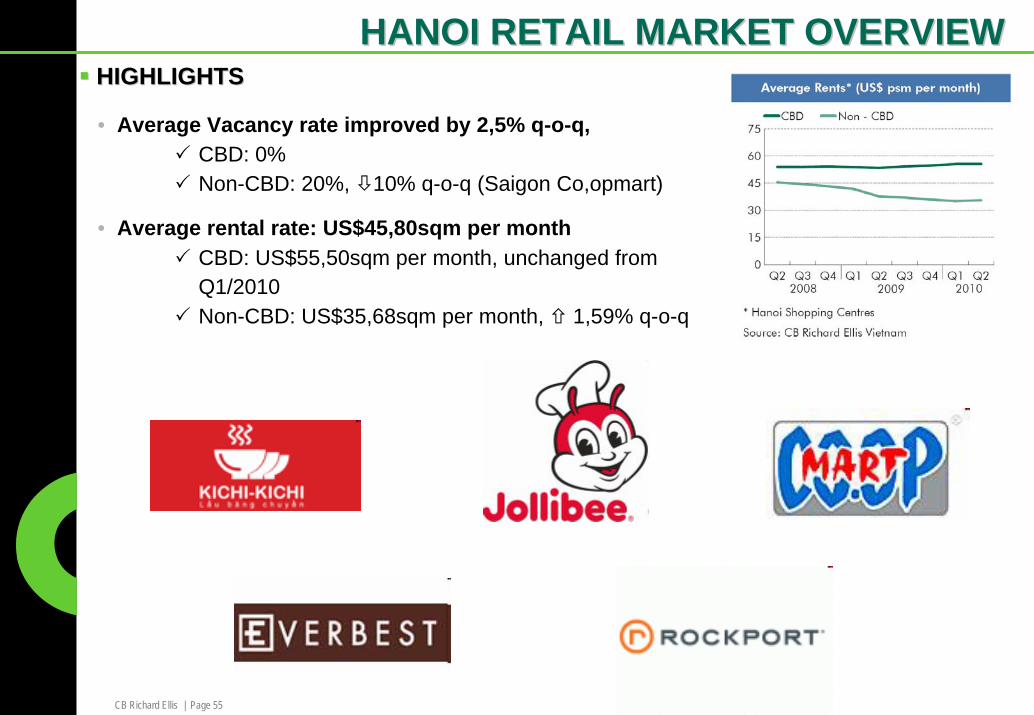

HANOI RETAIL MARKET OVERVIEWHANOI RETAIL MARKET OVERVIEWHIGHLIGHTSHIGHLIGHTS

• Average Vacancy rate improved by 2,5% q-o-q, CBD: 0%Non-CBD: 20%, 10% q-o-q (Saigon Co,opmart)

• Average rental rate: US$45,80sqm per monthCBD: US$55,50sqm per month, unchanged from Q1/2010Non-CBD: US$35,68sqm per month, 1,59% q-o-q

CB Richard Ellis | Page 56

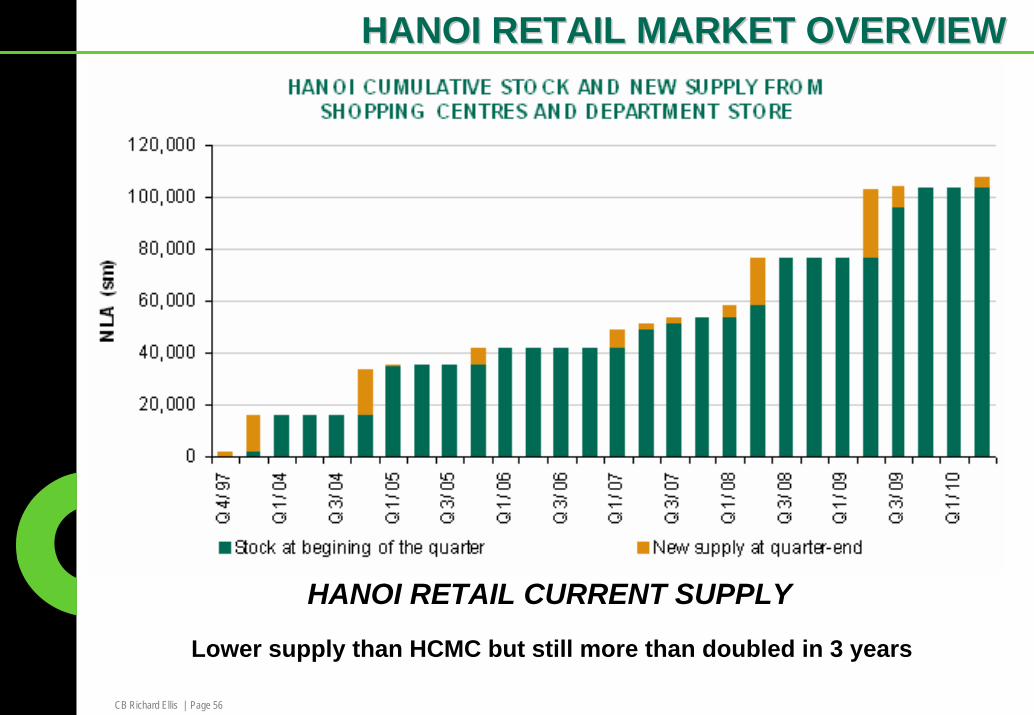

HANOI RETAIL MARKET OVERVIEWHANOI RETAIL MARKET OVERVIEW

HANOI RETAIL CURRENT SUPPLY

Lower supply than HCMC but still more than doubled in 3 years

CB Richard Ellis | Page 57

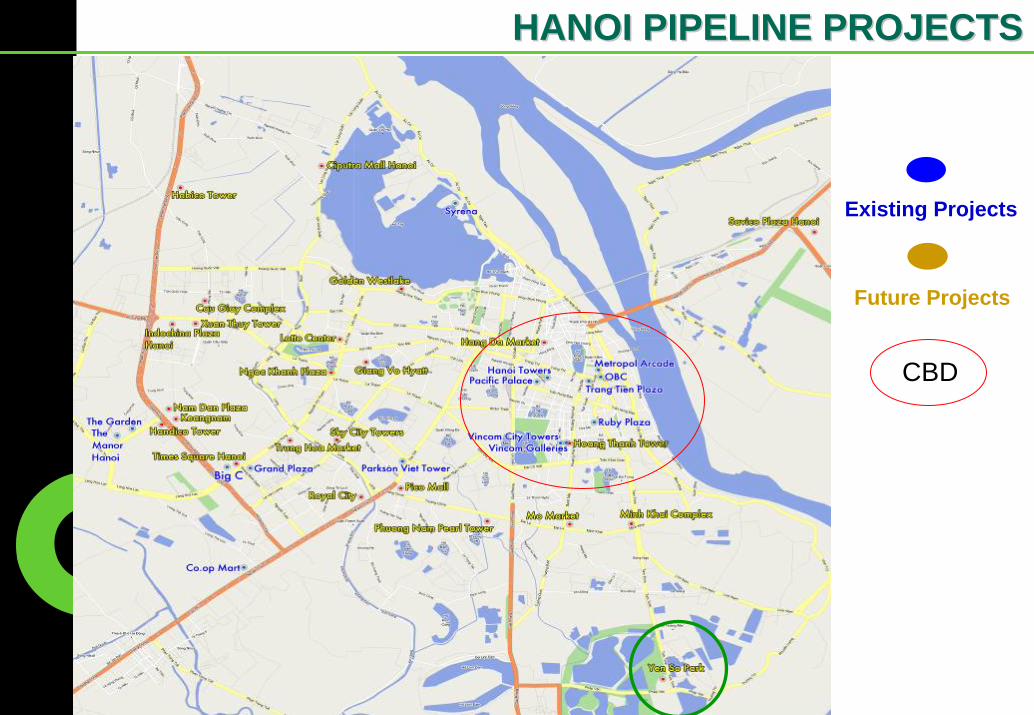

HANOI PIPELINE PROJECTSHANOI PIPELINE PROJECTS

Existing Projects

Future Projects

CBD

CB Richard Ellis | Page 58

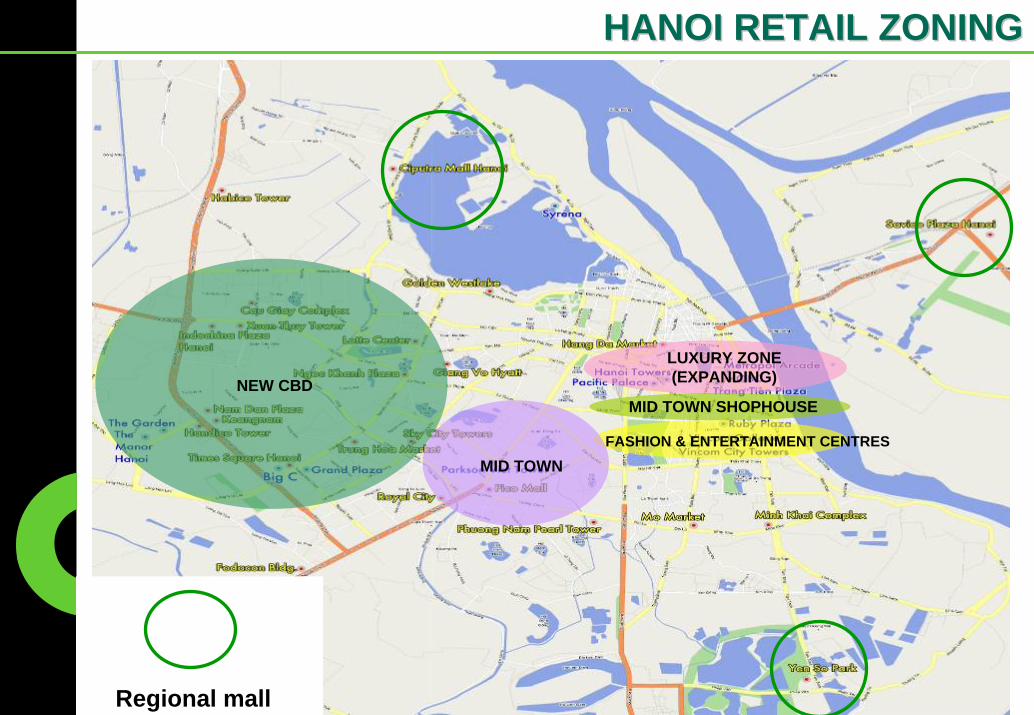

HANOI RETAIL ZONINGHANOI RETAIL ZONING

LUXURY ZONE (EXPANDING)

MID TOWN SHOPHOUSE

FASHION & ENTERTAINMENT CENTRES

NEW CBD

MID TOWN

Regional mall

CB Richard Ellis | Page 59

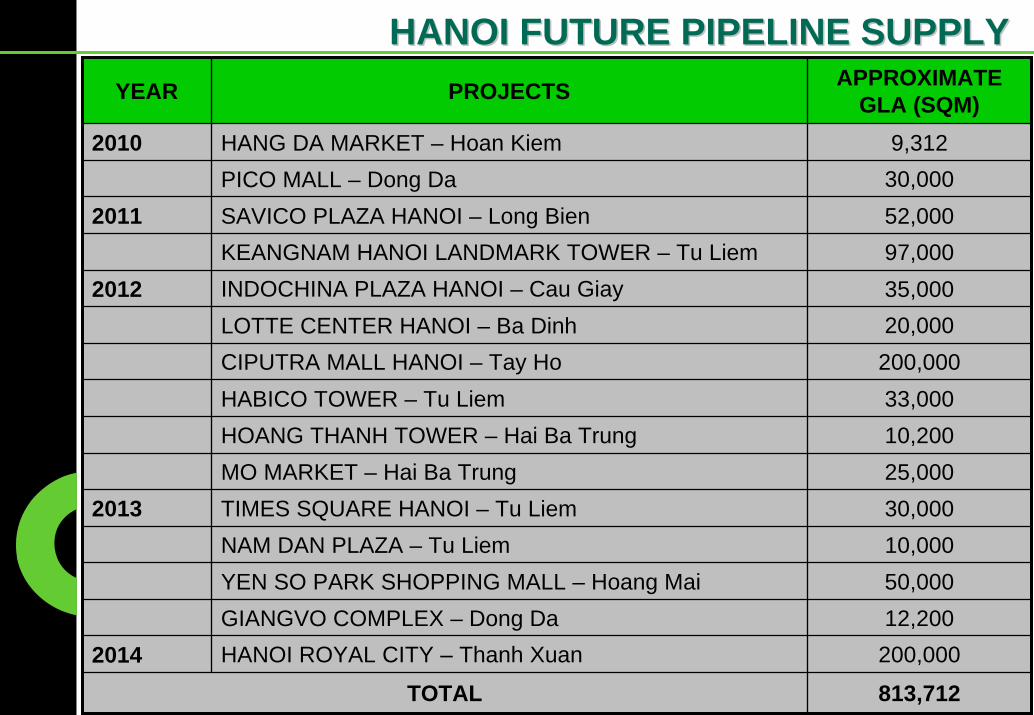

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYYEAR PROJECTS APPROXIMATE

GLA (SQM)2010 HANG DA MARKET – Hoan Kiem

PICO MALL – Dong DaSAVICO PLAZA HANOI – Long BienKEANGNAM HANOI LANDMARK TOWER – Tu LiemINDOCHINA PLAZA HANOI – Cau GiayLOTTE CENTER HANOI – Ba DinhCIPUTRA MALL HANOI – Tay HoHABICO TOWER – Tu Liem 33,000HOANG THANH TOWER – Hai Ba Trung 10,200MO MARKET – Hai Ba Trung 25,000TIMES SQUARE HANOI – Tu LiemNAM DAN PLAZA – Tu LiemYEN SO PARK SHOPPING MALL – Hoang MaiGIANGVO COMPLEX – Dong Da

2014 HANOI ROYAL CITY – Thanh Xuan 200,000

TOTAL 813,712

9,31230,00052,00097,00035,00020,000

200,000

30,00010,000

2011

50,000

2012

12,200

2013

CB Richard Ellis | Page 60

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYHANG DA MARKET

Location: Hang Da Market, Cua Dong, Hoan

Kiem Dist., Hanoi

Developer: Hang Da Commercial Joint-

Stock Company

Investor (F2nd – 4th - 6,600.00sqm): Quan

Nhan Joint-Stock Company

Concept: 05 floors including

traditional market and modern

shopping center.

Total GFA: 9,312.00sqm

Total basement area:

7,556.00sqm (02 floors)

Expected completion: Q4, 2010

Outstanding features: Location

CB Richard Ellis | Page 61

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYPICO MALL

Location: 229 Tay Son Road, Dong Da District,

Developer: Military Petrochemical JSC.

Investor in retail podium: Pico JSC

25 levels (office towers) & 27 levels (2 apartment

towers)

Project concept: Mixed-use Condo & Commercial

Total GFA: 150,000sqm

Retail GFA: 30,000sqm

Office GFA: 33,000sqm

Apartments sold: 314 units

Parking: 2 basements + external parking

Expected Completion: Q4, 2010

Outstanding features: Interior design

CB Richard Ellis | Page 62

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

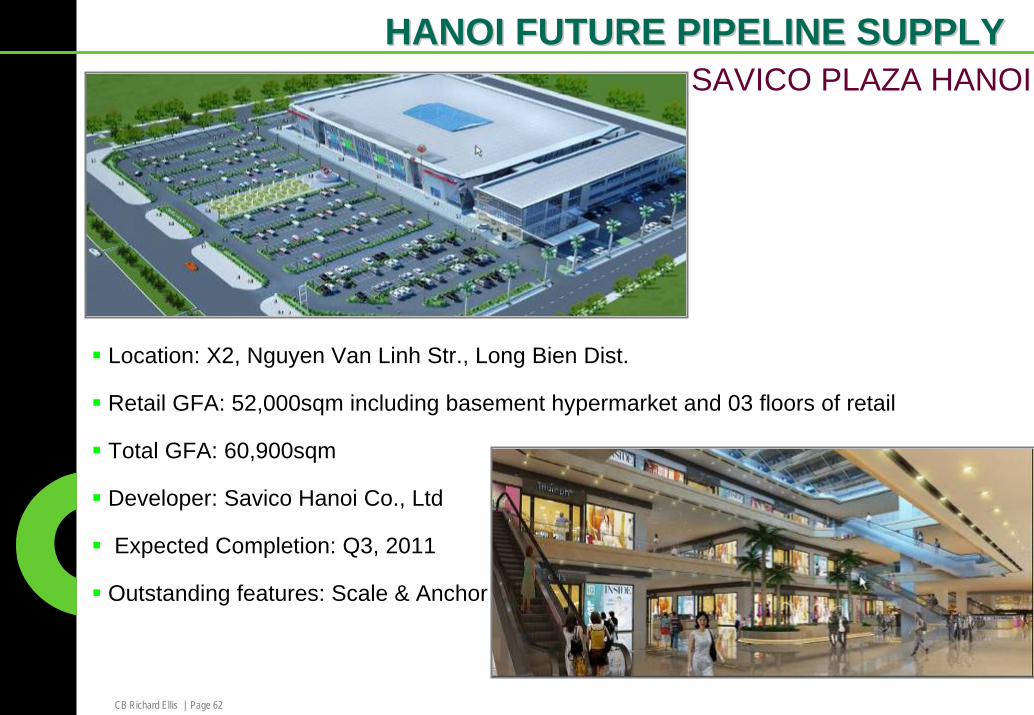

Location: X2, Nguyen Van Linh Str., Long Bien Dist.

Retail GFA: 52,000sqm including basement hypermarket and 03 floors of retail

Total GFA: 60,900sqm

Developer: Savico Hanoi Co., Ltd

Expected Completion: Q3, 2011

Outstanding features: Scale & Anchor

SAVICO PLAZA HANOI

CB Richard Ellis | Page 63

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYKEANGNAM HANOI LANDMARK TOWER

Location: Pham Hung Road, Tu Liem Dist., Hanoi

Developer: Keangnam Vina One member Co,.Ltd

Concept: Hotel, Apartments, Office and Retail

Total GFA: 608,298sqm

Total retail GFA: 97,275sqm

Total hotel GFA: 63,644sqm

Total office GFA: 181,518sqm

Total apartments GFA: 265,861sqm

Expected retail completion: August, 2011

CB Richard Ellis | Page 64

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

Location: Xuan Thuy, Cau Giay Dist.

Developer: IndochinaLand

Luxury Apartments, Office & Retail

Total GFA: 124,489sqm

Retail GFA: 35,000sqm

Ground Breaking: Q4, 2008

Completion: Q4/11

Outstanding features: Central Plaza

INDOCHINA PLAZA HANOI

CB Richard Ellis | Page 65

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

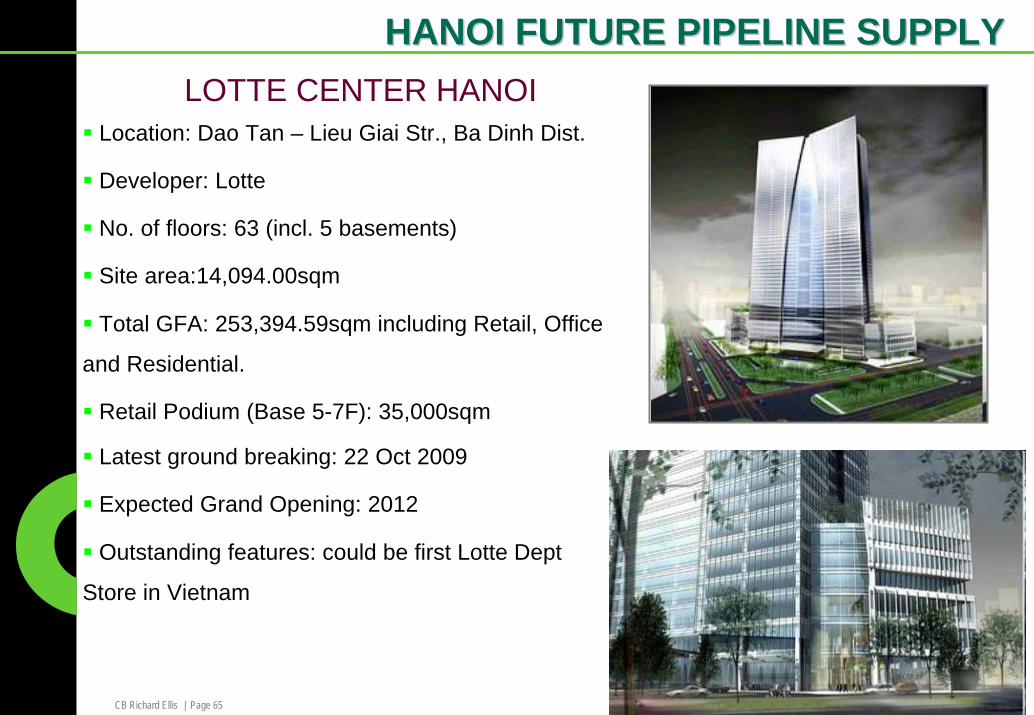

Location: Dao Tan – Lieu Giai Str., Ba Dinh Dist.

Developer: Lotte

No. of floors: 63 (incl. 5 basements)

Site area:14,094.00sqm

Total GFA: 253,394.59sqm including Retail, Office

and Residential.

Retail Podium (Base 5-7F): 35,000sqm

LOTTE CENTER HANOI

Latest ground breaking: 22 Oct 2009

Expected Grand Opening: 2012

Outstanding features: could be first Lotte Dept

Store in Vietnam

CB Richard Ellis | Page 66

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYCIPUTRA MALL HANOI

Location: Lac Long Quan. Tay Ho Dist.

Owner: Citra Westlake

Description: Regional shopping mall

Retail GFA: 200.000sqm (incl. food court.

cinema. department store and hypermarket)

Expected Completion: Q2. 2012

Outstanding features: design and scale

CB Richard Ellis | Page 67

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYHABICO TOWER

Location: 288 Pham Van Dong, Tu Liem, Hanoi (ring road 3,

opposite Metro)

Developer: Habico

Concept: office, retail and condominium

Total GFA: 124,742.73sqm (excluding

area of basements, technical floors and

sky gardens)

Retail GFA: 33,000sqm (1-7F)

Expected Completion: Q2, 2012

CB Richard Ellis | Page 68

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

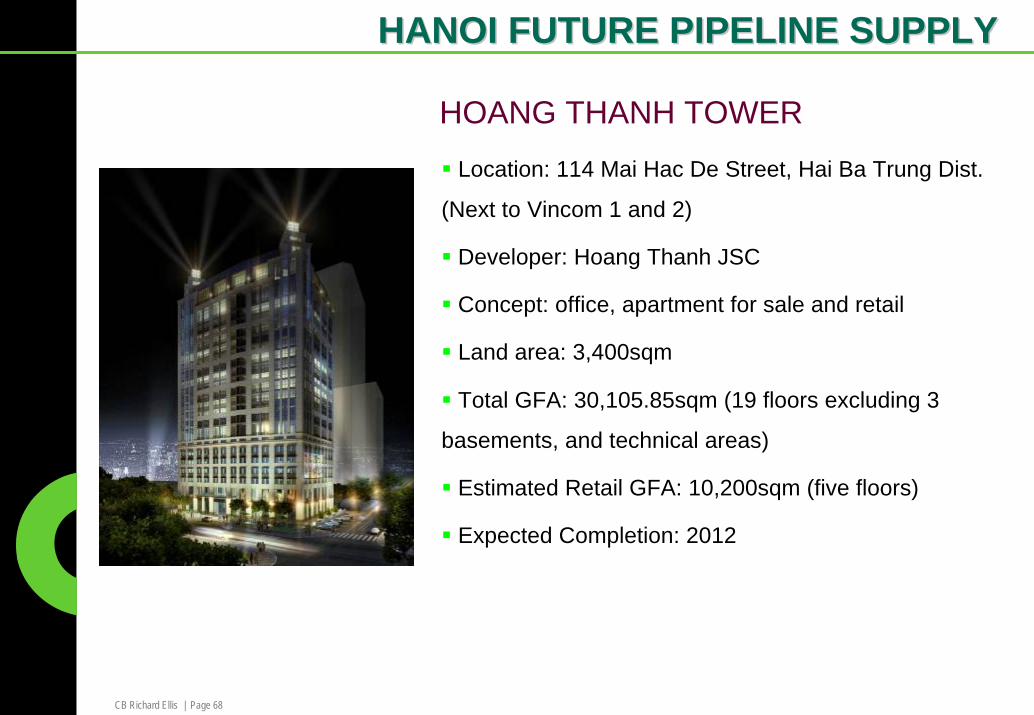

HOANG THANH TOWER

Location: 114 Mai Hac De Street, Hai Ba Trung Dist.

(Next to Vincom 1 and 2)

Developer: Hoang Thanh JSC

Concept: office, apartment for sale and retail

Land area: 3,400sqm

Total GFA: 30,105.85sqm (19 floors excluding 3

basements, and technical areas)

Estimated Retail GFA: 10,200sqm (five floors)

Expected Completion: 2012

CB Richard Ellis | Page 69

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYTIMES SQUARE HANOI

Location: Pham Hung, Tu Liem Dist.

Developer: VinaCapital

Land Area: 4 ha

Five Star Hotel (300 rooms), Grade A Office

(20,000sqm) & Retail (30,000sqm)

Retail GFA: 30,000sqm

Ground Breaking: Dec 2008

Completion: 2013

External design and location

CB Richard Ellis | Page 70

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

Location: Pham Hung Street, Tu Liem Dist.

Owner: PVFC Power Land & Pan Pacific JSC.

Description: 2 towers (40 & 44 levels) of 120,000sqm

GFA Office & 7 storey retail podium

Retail GFA: 10,000sqm

Ground Breaking: Jan 2010

Expected Completion: 2013

Outstanding features: Design

NAM DAN PLAZA

CB Richard Ellis | Page 71

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYYEN SO PARK SHOPPING MALL

Location: Yen So Ward, Hoang Mai Dist.

Owner & Developer: Gamuda Land Group

Description: The Center of all commercial

activities, complimented by the festive retail,

offices, hotels and convention center.

Land Area for retail: 3.85 ha

Proposed Retail NLA: 49,253sqm (4 Storey

Podium)

Completion: 2013

Status: Planning

Outstanding features: Master planned

community

CB Richard Ellis | Page 72

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLY

Location: 15-17 Ngoc Khanh Str., Ba Dinh Dist.

Owner: Pacific Land Limited

Total GFA: 108,777sqm

Retail GFA: 12,200sqm

Project concept: 5-star Hyatt Regency Hotel

(305 rooms), 18-storey Office Tower & Retail

Expected completion: 2013

GIANGVO COMPLEX

(HYATT REGENCY HANOI)

CB Richard Ellis | Page 73

HANOI FUTURE PIPELINE SUPPLYHANOI FUTURE PIPELINE SUPPLYHANOI ROYAL CITY

Location: 74 Nguyen Trai, Thanh Xuan Dist.

Developer: Vincom JSC

Development area of 169,220sqm - A city within a

city with Hotel, schools, condominiums, retail, offices

Retail GFA: 200,000sqm

Ground Breaking: Jan, 2010

Expected Completion: Q4, 2014

DA NANG FUTURE PIPELINE SUPPLY

CB Richard Ellis | Page 75

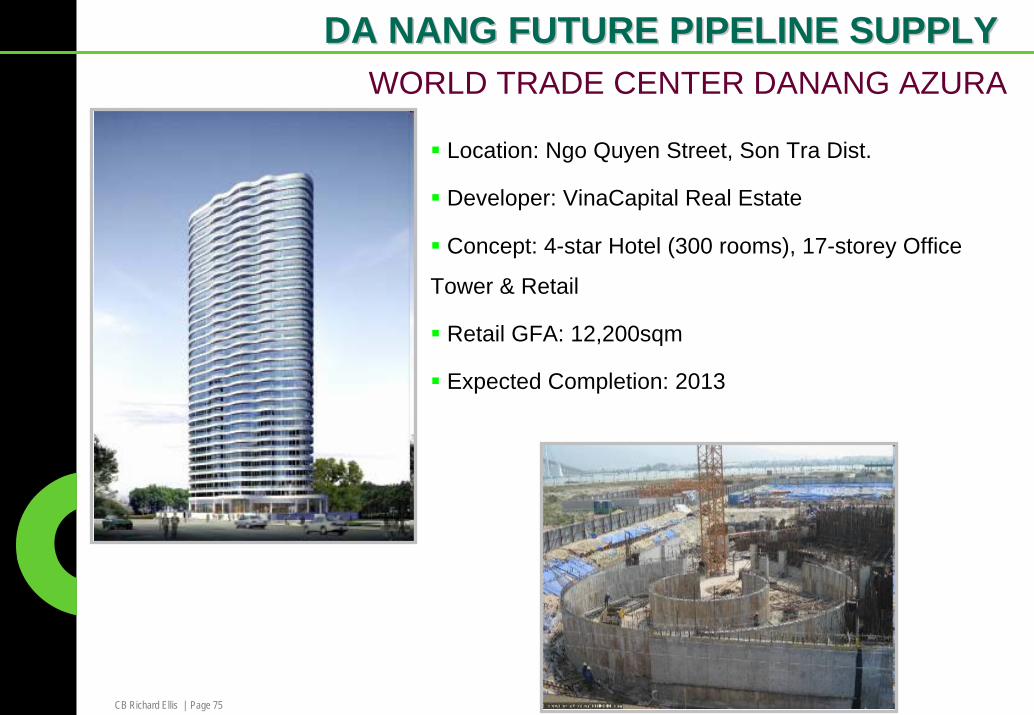

DA NANG FUTURE PIPELINE SUPPLYDA NANG FUTURE PIPELINE SUPPLYWORLD TRADE CENTER DANANG AZURA

Location: Ngo Quyen Street, Son Tra Dist.

Developer: VinaCapital Real Estate

Concept: 4-star Hotel (300 rooms), 17-storey Office

Tower & Retail

Retail GFA: 12,200sqm

Expected Completion: 2013

CB Richard Ellis | Page 76

DA NANG FUTURE PIPELINE SUPPLYDA NANG FUTURE PIPELINE SUPPLYGOLDEN SQUARE COMPLEX

Location: Nguyen Thai Hoc Str, Hai Chau Dist.

Developer: Dong A Land JSC

Concept: 266 Apartments, 5-star Marriot Hotel (200

rooms ), 21-storey Office Tower & 4-storey Retail.

Total land area: 10,664sqm

Retail GFA: 20,000sqm

Expected Completion: Q1, 2012

CB Richard Ellis | Page 77

DA NANG FUTURE PIPELINE SUPPLYDA NANG FUTURE PIPELINE SUPPLYINDOCHINA RIVERSIDE COMPLEXLocation: 74 Bach Dang Str., Hai Chau Dist.

Developer: Indochina Land Limited Company

Project concept: 95 apartments; 10-storey

Office Tower; 3-storey Retail Podium

Total GFA: 33,503sqm (total improvements)

Retail GFA: 4,603sqm

Ground breaking: 2007

CB Richard Ellis | Page 78

BANKERS EVENTBANKERS EVENT

Venue: Sheraton Hotel - HCMCAugust 19th, 201017:30 – 19:30

Hosted by: CB Richard Ellis Vietnam

UPCOMING EVENTSUPCOMING EVENTS

CB Richard Ellis | Page 79

THANK YOU FOR YOUR ATTENTION

Disclaimer: © 2009 CB Richard Ellis, Inc. We obtained the information above from sources we believe to be reliable. However, we have not verified its accuracy and make no guarantee, warranty or representation about it. It is submitted subject to the possibility of errors, omissions, change of price, rental or other conditions, prior sale, lease or financing, or withdrawal without notice. We include projections, opinions, assumptions or estimates for example only, and they may not represent current or future performance of the property. You and your tax and legal advisors should conduct your own investigation of the property and transaction.

www.cbrevietnam.com