22

Instructor: Dr. Zhu Zinan Email: [email protected] Office: BIZ1 #7‐24 ACC3602 Managerial Planning and Control Semester II, AY 2014/15

Instructor: Dr. Zhu ZinanEmail: [email protected]

Office: BIZ1 #7‐24

ACC3602

Managerial Planning and Control

Semester II, AY 2014/15

Lecture 3 Transfer Pricing

Relevant Chapters:• Merchant and Van der Stede, Management Control Systems:

Performance Measurement, Evaluation, and Incentives, Chapter 7

Learning Objectives:1. What is transfer pricing and its purposes2. Transfer pricing alternatives3. A general guideline for transfer‐pricing situations4. Multinational transfer pricing and tax considerations

2

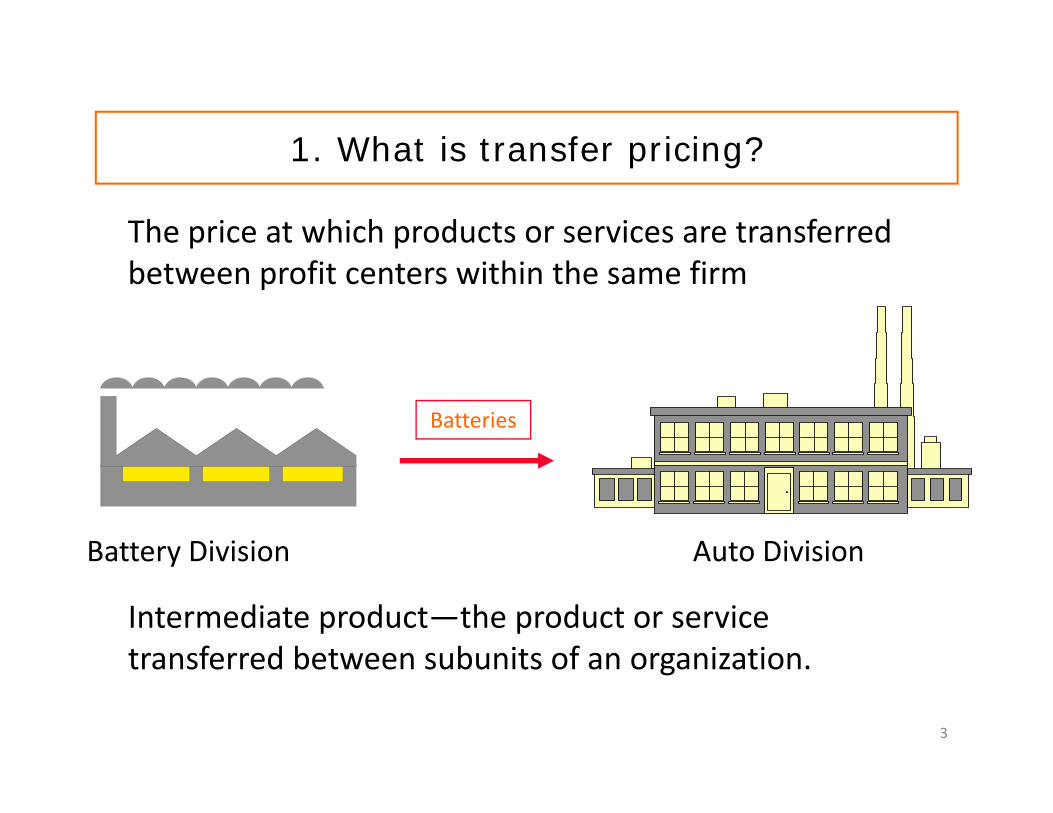

The price at which products or services are transferred between profit centers within the same firm

Battery Division Auto Division

Batteries

3

1. What is transfer pricing?

Intermediate product—the product or service transferred between subunits of an organization.

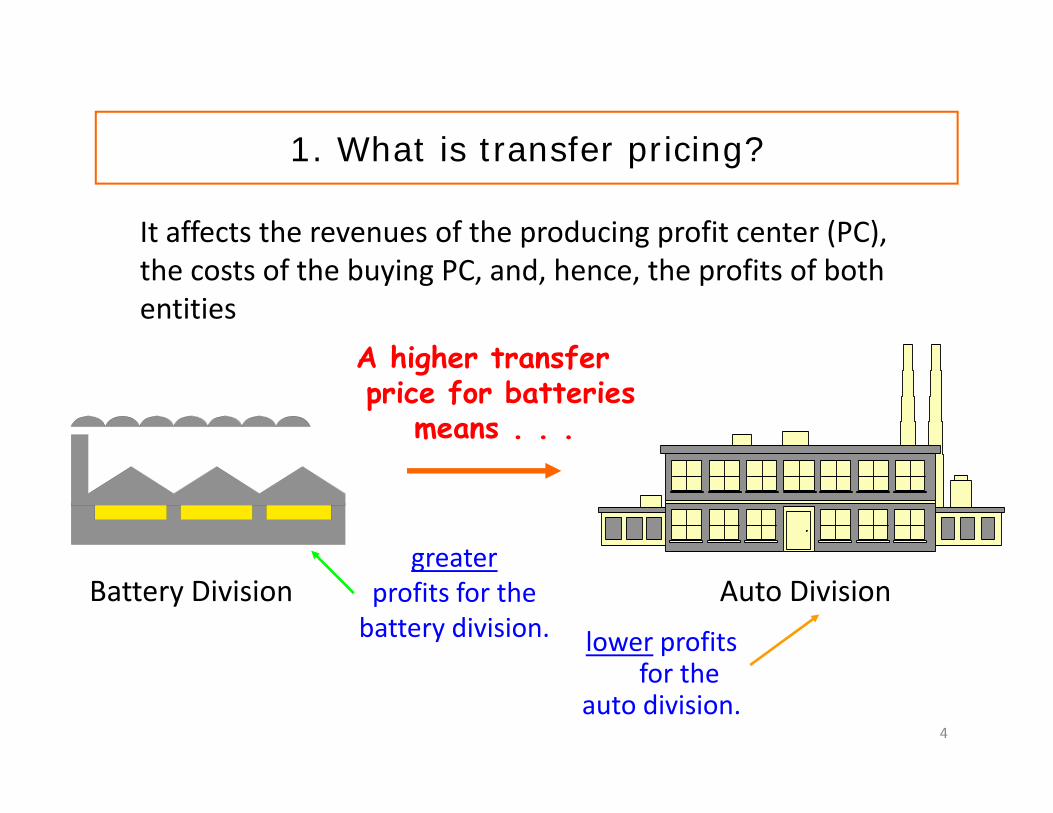

It affects the revenues of the producing profit center (PC),the costs of the buying PC, and, hence, the profits of both entities

A higher transferprice for batteries

means . . .

greaterprofits for thebattery division.

Auto DivisionBattery Divisionlower profits

for theauto division.

4

1. What is transfer pricing?

1. What is transfer pricing?

• Purposes– Focus managers’ attention on the performance of their own

subunits and provide information for evaluating PC performance

– Plan and coordinate the actions of different subunits to maximize the company’s income as a whole

– Purposely move profits between company entities/locations

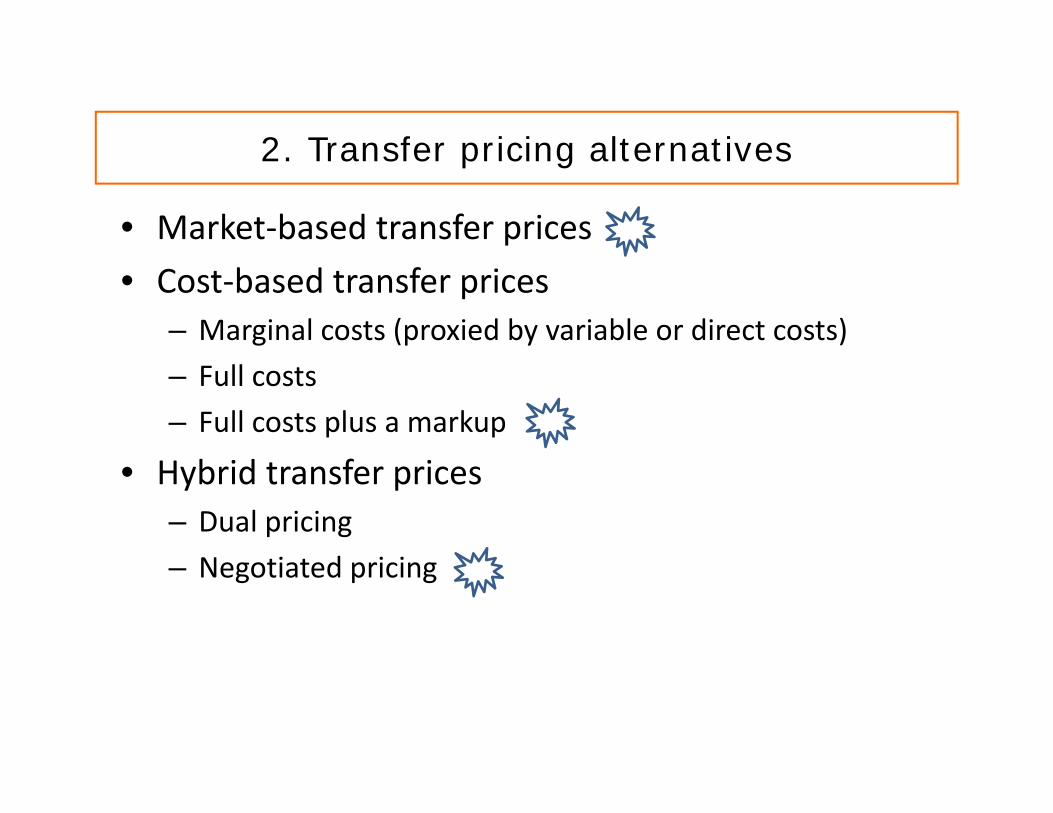

2. Transfer pricing alternatives

• Market‐based transfer prices• Cost‐based transfer prices

– Marginal costs (proxied by variable or direct costs)– Full costs– Full costs plus a markup

• Hybrid transfer prices– Dual pricing– Negotiated pricing

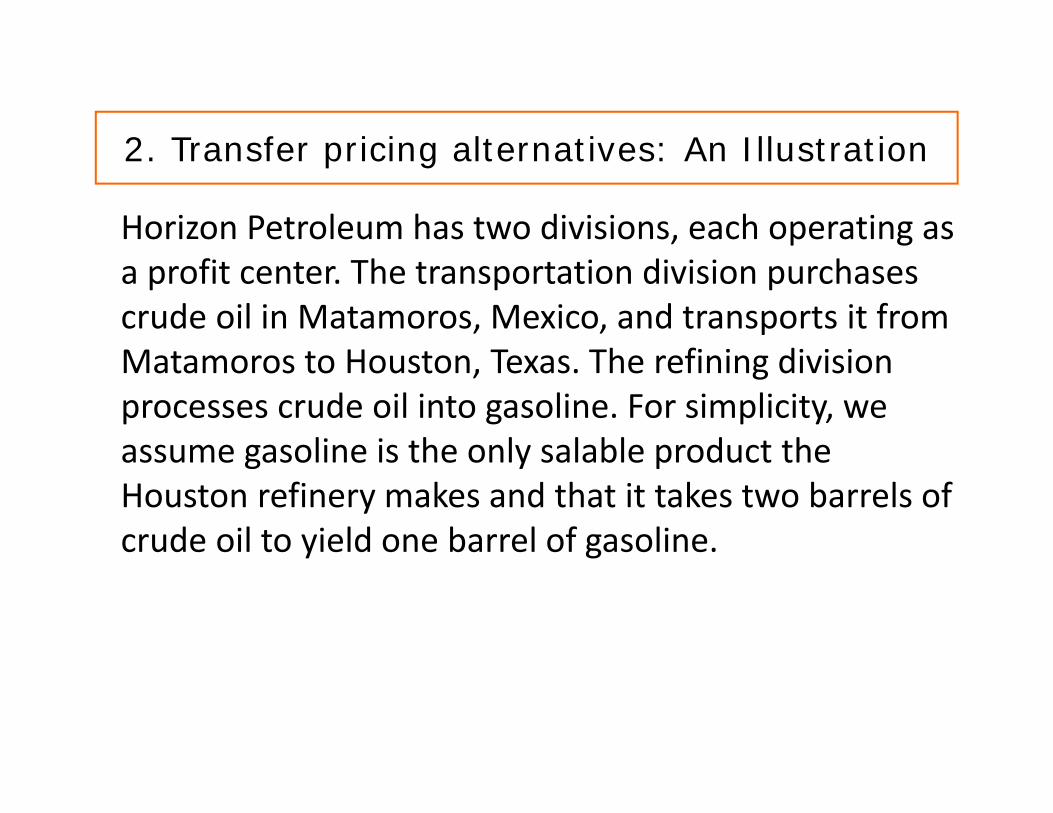

2. Transfer pricing alternatives: An Illustration

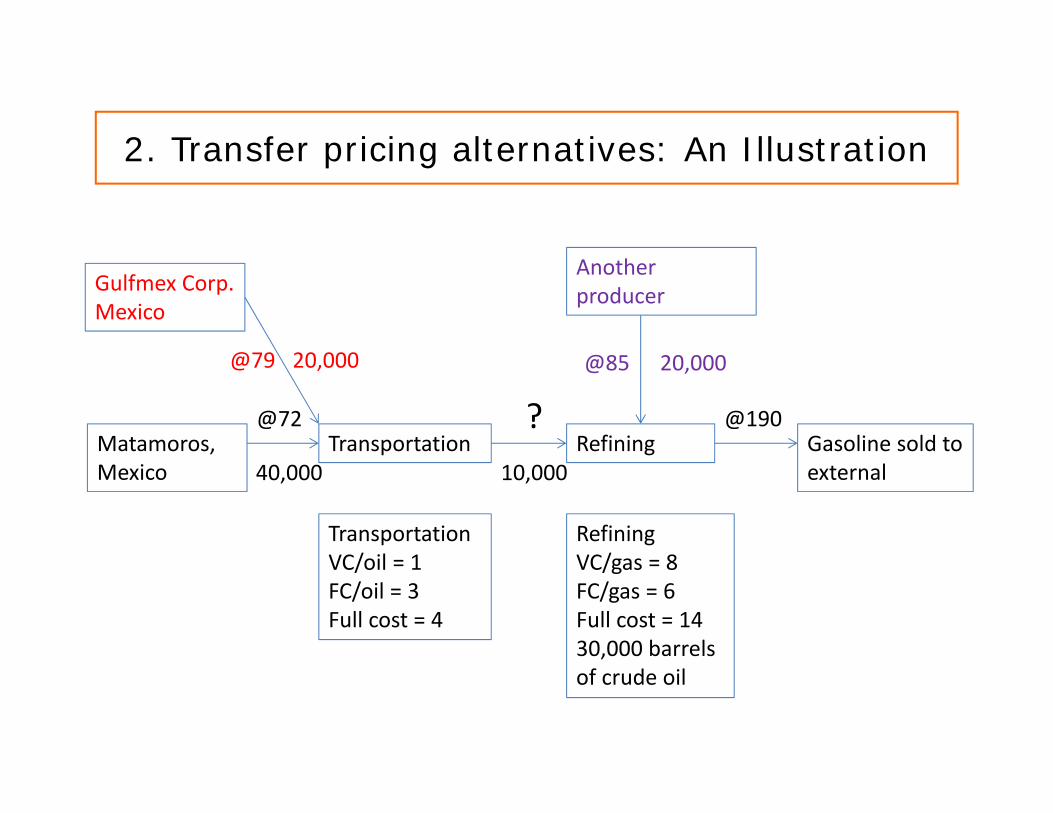

Horizon Petroleum has two divisions, each operating as a profit center. The transportation division purchases crude oil in Matamoros, Mexico, and transports it from Matamoros to Houston, Texas. The refining division processes crude oil into gasoline. For simplicity, we assume gasoline is the only salable product the Houston refinery makes and that it takes two barrels of crude oil to yield one barrel of gasoline.

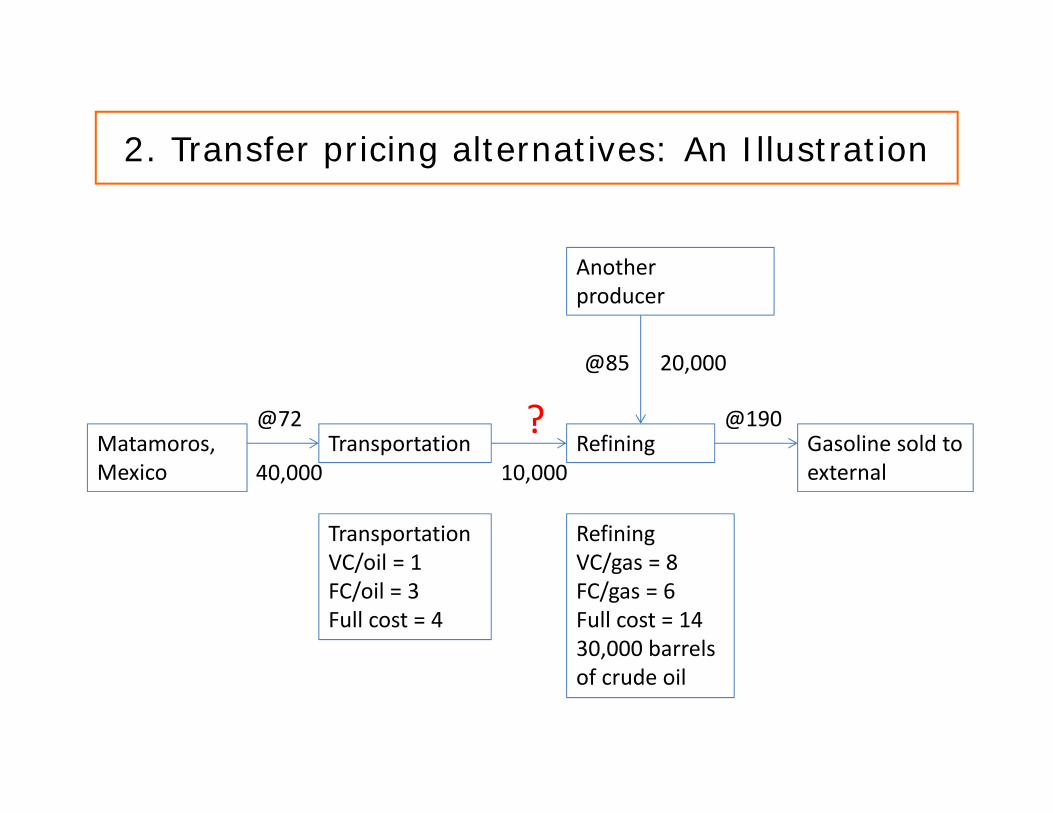

2. Transfer pricing alternatives: An Illustration

Transportation Refining Gasoline sold to external

TransportationVC/oil = 1FC/oil = 3Full cost = 4

RefiningVC/gas = 8FC/gas = 6Full cost = 1430,000 barrels of crude oil

Matamoros, Mexico

Another producer

@72

40,000 10,000

@85 20,000

@190?

2. Transfer pricing alternatives: Market-based TP

• Top management chooses to use the price of similar product or service that is publicly available. Sources of prices include trade associations, competitors, and so on.

• Actual price, which is charged to external customers, listed price of a similar product, or the price a competitor is offering (bid price)– Deviations can be allowed that reflect differences between internal and

external sales: e.g., savings in marketing, selling, and collecting costs; differences in quality standards, special features, or special services provided

• The selling division may elect to transfer or to continue to sell to the outside.

• Managers of both the selling and buying PC will make decisions that are optimal from a corporate perspective, and reports of their performances will provide good information for evaluation purposes.

2. Transfer pricing alternatives: Marginal cost TP

• Usually proxied by variable or direct costs

• It provides poor information for evaluation purposes• The selling PC incurs a loss• The profits of the buying PC are overstated

• Rarely used in practice• Variation: Marginal cost + lump‐sum fee

• The marginal cost of the transfer remains visible• The selling PC can recover its fixed cost and a profit margin through the lump‐sum fee

• Problem: must predetermine the lump‐sum fee based on an estimate of the capacity that each internal customer will require in the forthcoming period.

2. Transfer pricing alternatives: Full cost TP

• Popular in practice• Relatively easy to implement

– Firms have cost systems in place to calculate the full cost of production

– But, full costs rarely reflect actual, current costs of producing the products because of financial accounting conventions (e.g., depreciation) and arbitrary overhead cost allocations

• There is no incentive for the selling PC to transfer internally since there is no profit margin

• The profit of the selling PC is understated

2. Transfer pricing alternatives: Full cost plus a markup

• It provides a measure of long‐run viability.• It allows the selling PC to earn a profit on internally transferred products/services

• It also provides a crude approximation of the market price in cases where no competitive external market price exists. Such transfer prices, however, are not (quite) responsive to market conditions.

• Say “105% of full cost”

2. Transfer pricing alternatives: An Illustration

Transportation Refining Gasoline sold to external

TransportationVC/oil = 1FC/oil = 3Full cost = 4

RefiningVC/gas = 8FC/gas = 6Full cost = 1430,000 barrels of crude oil

Matamoros, Mexico

Another producer

@72

40,000 10,000

@85 20,000

@190?

Gulfmex Corp.Mexico

@79 20,000

2. Transfer pricing alternatives: Dual-rate TP

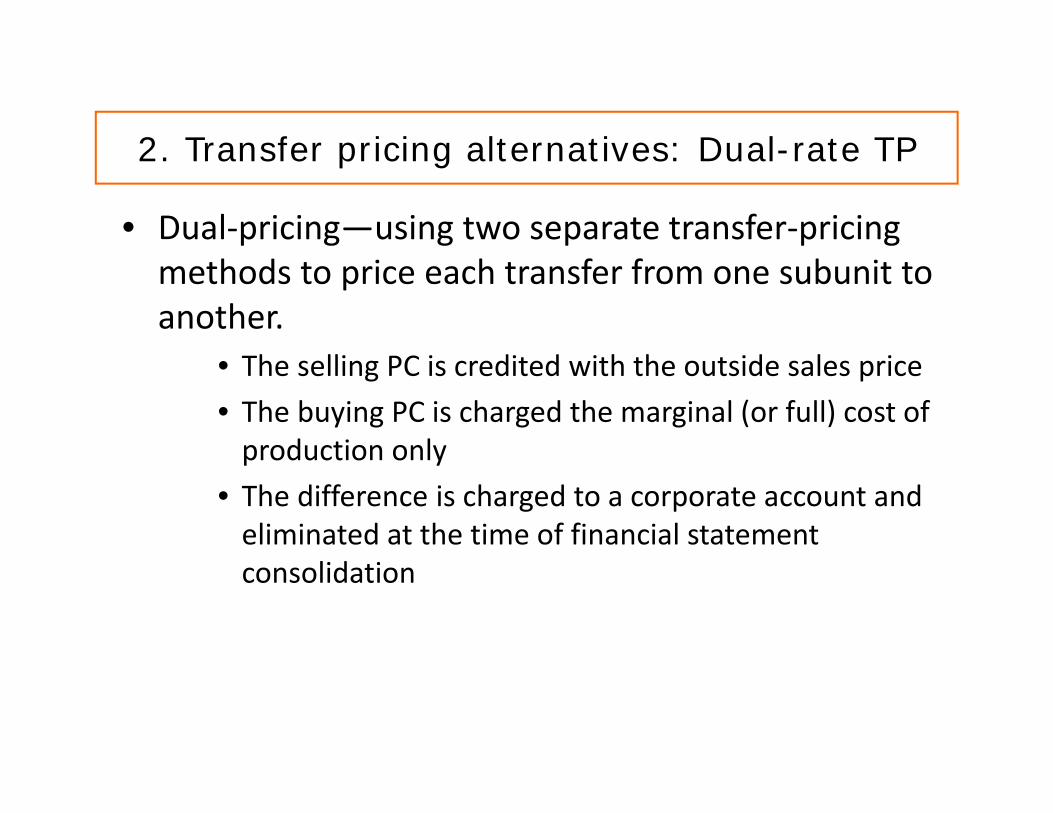

• Dual‐pricing—using two separate transfer‐pricing methods to price each transfer from one subunit to another.

• The selling PC is credited with the outside sales price• The buying PC is charged the marginal (or full) cost of production only

• The difference is charged to a corporate account and eliminated at the time of financial statement consolidation

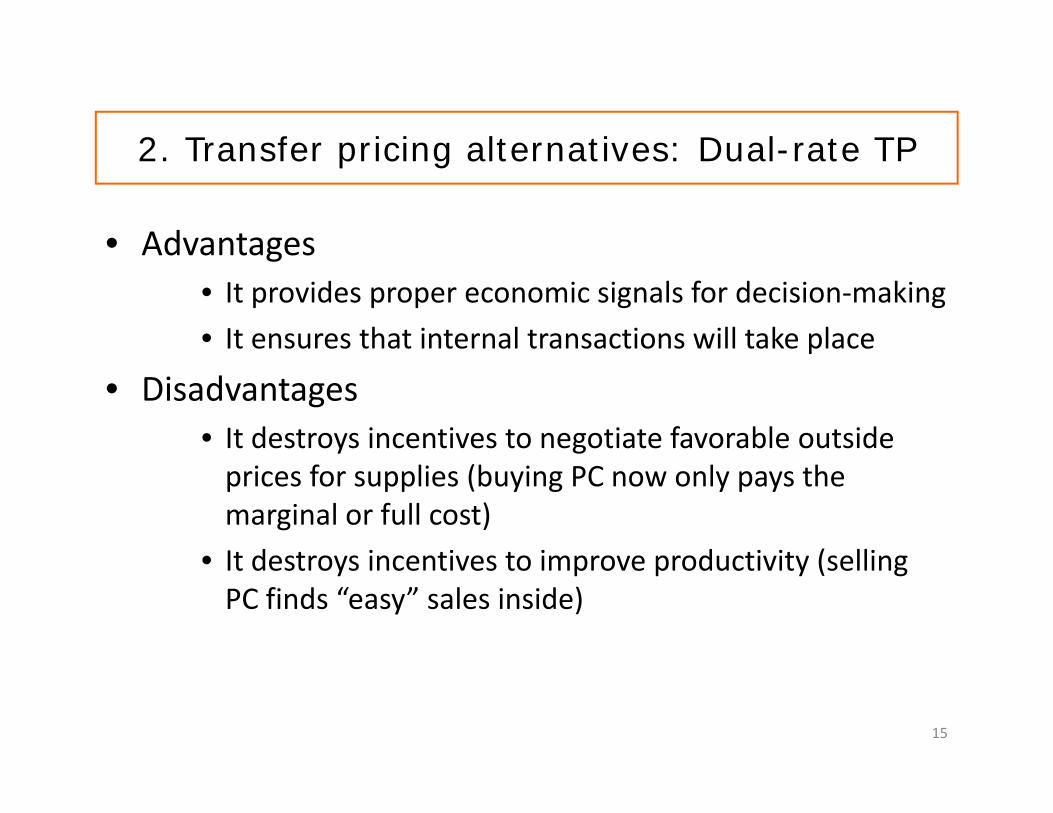

• Advantages• It provides proper economic signals for decision‐making• It ensures that internal transactions will take place

• Disadvantages• It destroys incentives to negotiate favorable outside prices for supplies (buying PC now only pays the marginal or full cost)

• It destroys incentives to improve productivity (selling PC finds “easy” sales inside)

15

2. Transfer pricing alternatives: Dual-rate TP

2. Transfer pricing alternatives: Negotiated TP

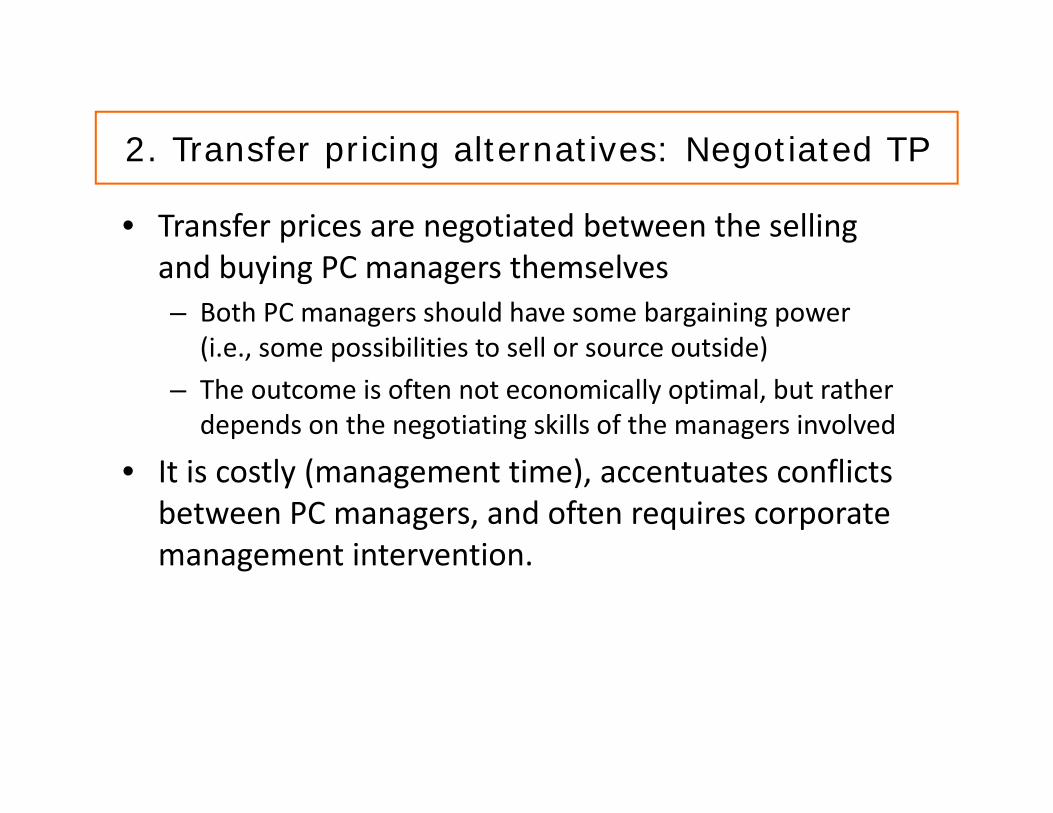

• Transfer prices are negotiated between the selling and buying PC managers themselves– Both PC managers should have some bargaining power

(i.e., some possibilities to sell or source outside)– The outcome is often not economically optimal, but rather

depends on the negotiating skills of the managers involved

• It is costly (management time), accentuates conflicts between PC managers, and often requires corporate management intervention.

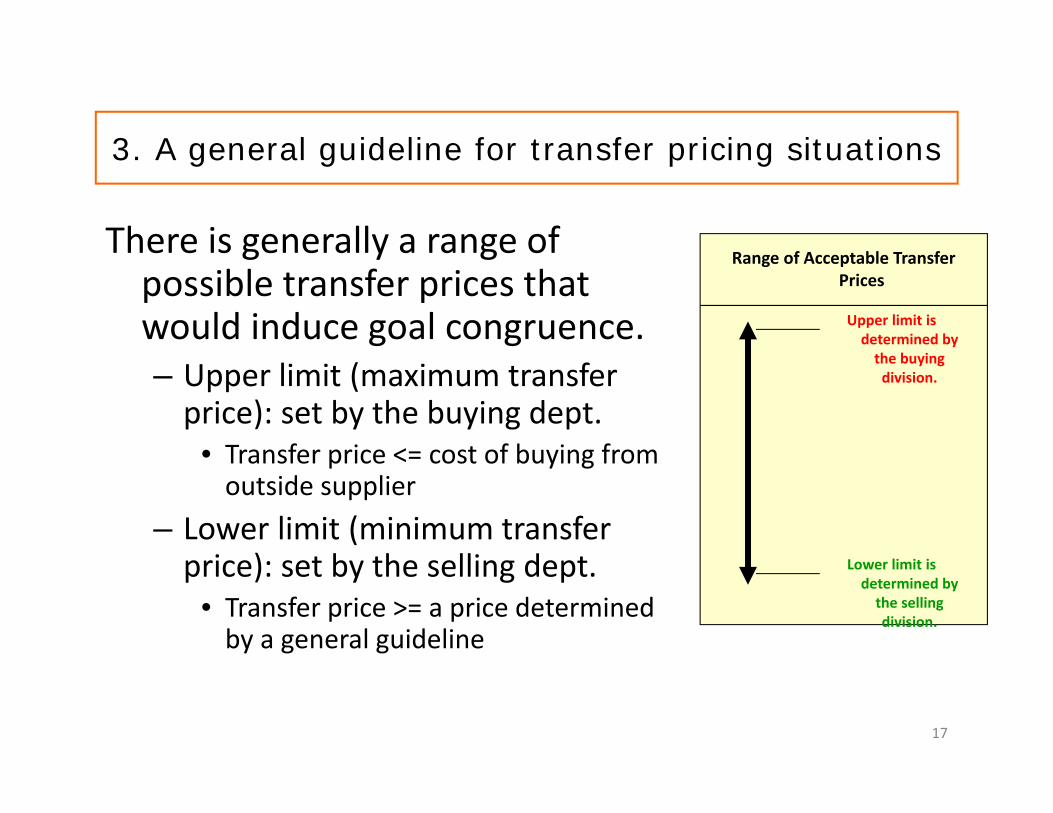

There is generally a range of possible transfer prices that would induce goal congruence. – Upper limit (maximum transfer price): set by the buying dept.

• Transfer price <= cost of buying from outside supplier

– Lower limit (minimum transfer price): set by the selling dept.

• Transfer price >= a price determined by a general guideline

Upper limit is determined by the buying division.

Lower limit is determined by the selling division.

Range of Acceptable Transfer Prices

17

3. A general guideline for transfer pricing situations

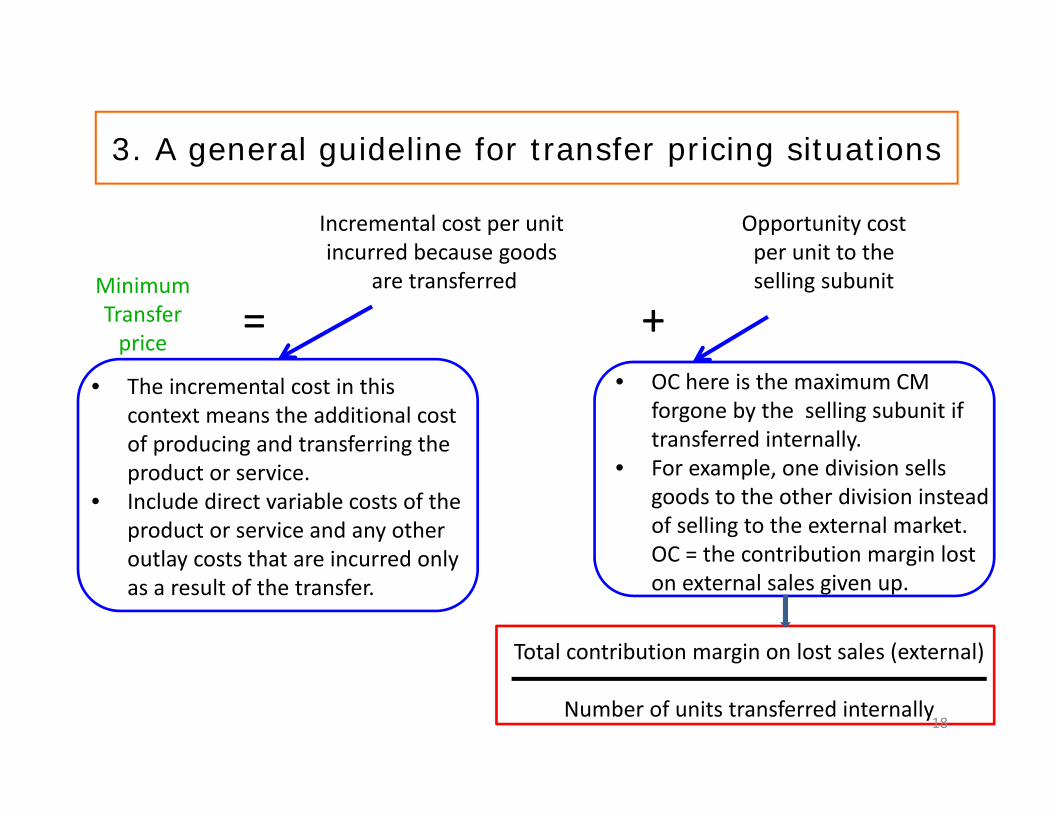

MinimumTransferprice

Incremental cost per unit incurred because goods

are transferred

Opportunity cost per unit to theselling subunit

= +

Total contribution margin on lost sales (external)

Number of units transferred internally

• OC here is the maximum CM forgone by the selling subunit if transferred internally.

• For example, one division sells goods to the other division instead of selling to the external market. OC = the contribution margin lost on external sales given up.

• The incremental cost in this context means the additional cost of producing and transferring the product or service.

• Include direct variable costs of the product or service and any other outlay costs that are incurred only as a result of the transfer.

18

3. A general guideline for transfer pricing situations

Consider the following scenarios:• A perfect competitive market for the intermediate product exists, and the selling division has no unused capacity.

• The selling division has unused capacity.• No market exists for the intermediate product (i.e., the crude oil transported by Transportation could be used only by Refining and would not be wanted by external parties.)

3. A general guideline for transfer pricing situations

Since tax rates and import duties are different in different countries, companies have incentives to set transfer prices that will: Increase revenues in low‐tax countries.

Increase costs in high‐tax countries.

Reduce cost of goods transferred to high‐import‐duty countries.

E.g., Google transferred revenues from customers in Britain to Google’s European headquarters in Dublin. By paying the low Irish corporate tax rate of 12.5%, Google saved £450 million in UK taxes in 2009 alone.

20

4. Multinational transfer pricing and tax considerations

• When goods or services are transferred between divisions of a company that are located in different countries, the company may have an incentive to set transfer prices to minimize the overall tax exposure of the company. And this incentive may be so strong that it overrides the approaches to setting transfer prices discussed earlier.

• According to a survey by Ernst & Young LLP, “transfer pricing is the top tax issue facing multinational corporations. Of the international tax directors at 582 multinational organizations polled in the survey, 75 percent expect their company to face a transfer‐pricing audit within the next two years.”

• Tax laws vary among countries with regard to flexibility in setting transfer prices. Because of the potential for loss of tax revenue, most countries with relatively high tax rates have laws prohibiting the behavior described in our example.

21

4. Multinational transfer pricing and tax considerations

End of Lecture 3

22