19

Transfer Pricing – New Guidelines Webinar | Wednesday, 3 March 2021

Transfer Pricing – New Guidelines

Webinar | Wednesday, 3 March 2021

2© 2021 Deloitte Ireland LLP. All rights reserved.

Today’s presenters:

Wilco Froneman Gerard Feeney Kevin Norton Markella Karakalpaki

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 3

Agenda for today

Debt Capacity

TP Documentation include:

TP Exemptions

Q&A

Overview

4© 2021 Deloitte Ireland LLP. All rights reserved.

Overview

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 5

Transfer Pricing Guidelines - Part 35A-01-01

© 2020 Deloitte & Touche (M.E.) All rightsreserved.

5

Table of Contents

1 Overview 6

2 Key definitions 8

3 Meaning of “associated” 10

4 Basic rules on transfer pricing 12

5 Principles for construing rules in accordance with OECD Guidelines 18

6 Modification of basic rules on transfer pricing for arrangements between

qualifying relevant persons 19

7 Small or medium-sized enterprise 26

8 Transfer pricing documentation requirements 28

9 Elimination of double counting 40

10 Interaction with capital allowances provisions 42

11 Interaction with provisions dealing with chargeable gains 48

12 Approach to Monitoring Compliance 55

6© 2021 Deloitte Ireland LLP. All rights reserved.

Debt Capacity

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 7

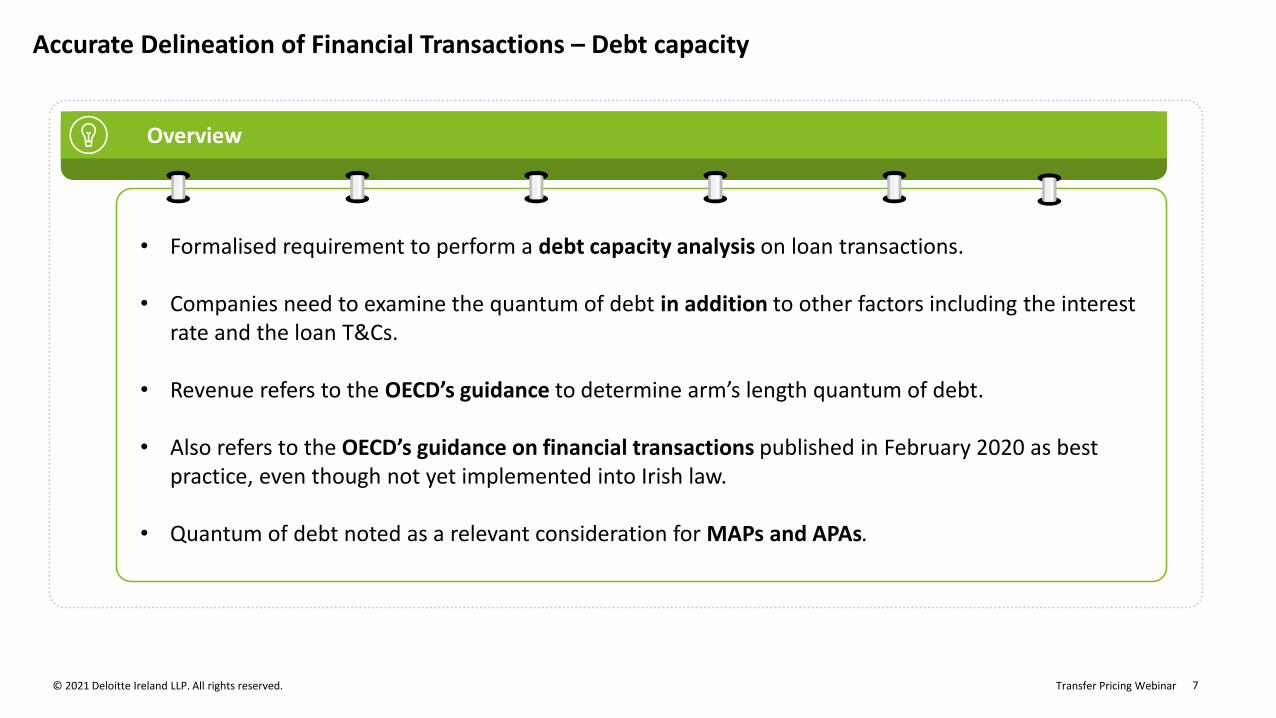

Accurate Delineation of Financial Transactions – Debt capacity

Overview

• Formalised requirement to perform a debt capacity analysis on loan transactions.

• Companies need to examine the quantum of debt in addition to other factors including the interest rate and the loan T&Cs.

• Revenue refers to the OECD’s guidance to determine arm’s length quantum of debt.

• Also refers to the OECD’s guidance on financial transactions published in February 2020 as best practice, even though not yet implemented into Irish law.

• Quantum of debt noted as a relevant consideration for MAPs and APAs.

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 8

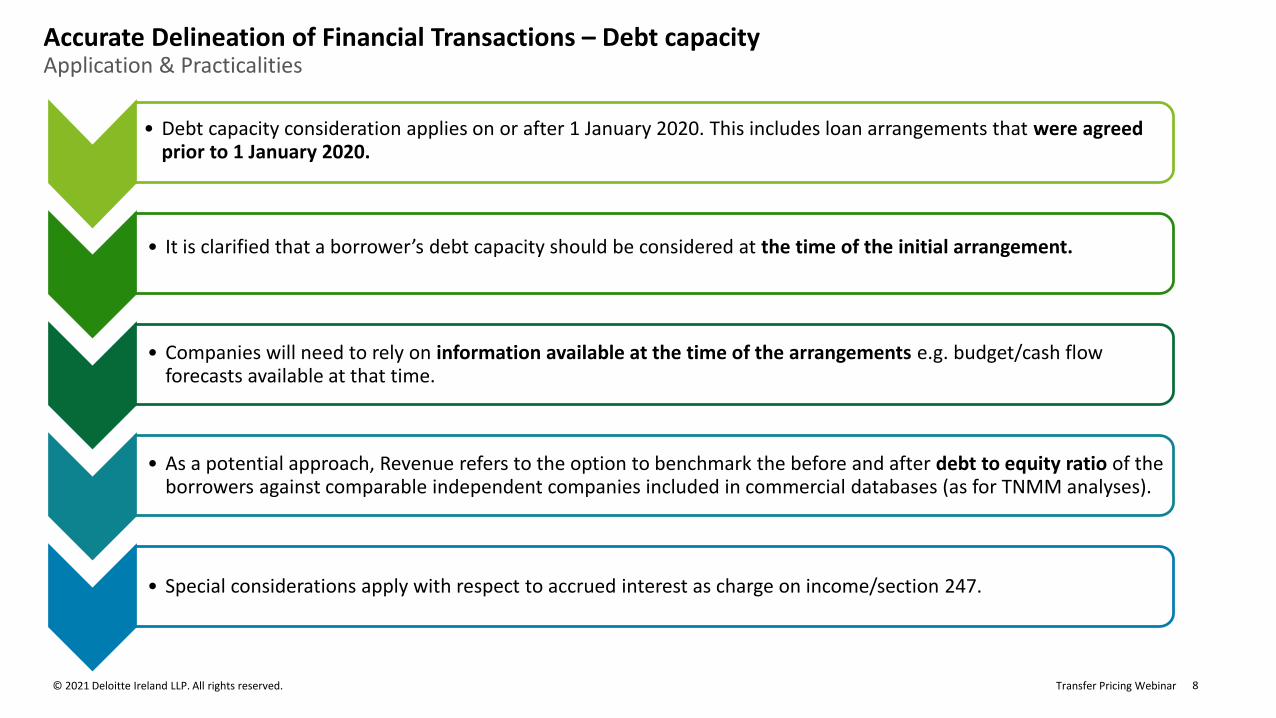

Accurate Delineation of Financial Transactions – Debt capacity Application & Practicalities

• Debt capacity consideration applies on or after 1 January 2020. This includes loan arrangements that were agreed prior to 1 January 2020.

• It is clarified that a borrower’s debt capacity should be considered at the time of the initial arrangement.

• Companies will need to rely on information available at the time of the arrangements e.g. budget/cash flow forecasts available at that time.

• As a potential approach, Revenue refers to the option to benchmark the before and after debt to equity ratio of the borrowers against comparable independent companies included in commercial databases (as for TNMM analyses).

• Special considerations apply with respect to accrued interest as charge on income/section 247.

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 9

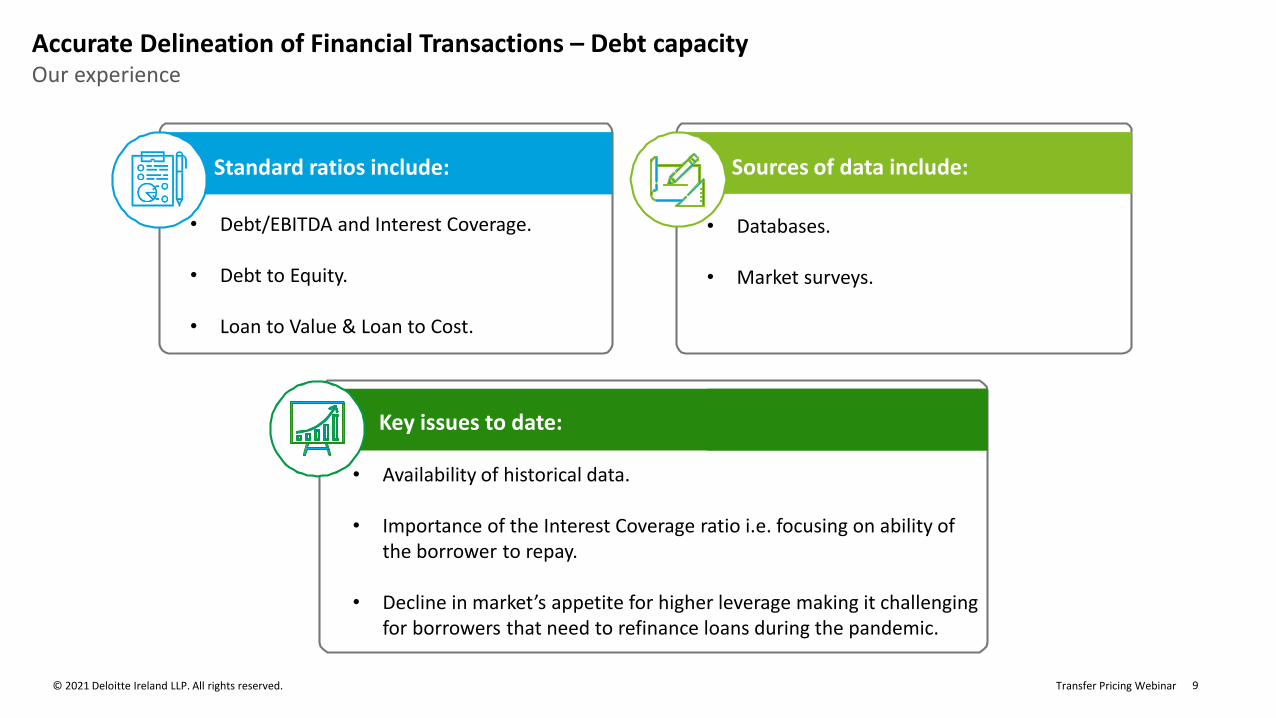

• Debt/EBITDA and Interest Coverage.

• Debt to Equity.

• Loan to Value & Loan to Cost.

• Standard ratios include:

• Databases.

• Market surveys.

Sources of data include:

Accurate Delineation of Financial Transactions – Debt capacityOur experience

• Availability of historical data.

• Importance of the Interest Coverage ratio i.e. focusing on ability of the borrower to repay.

• Decline in market’s appetite for higher leverage making it challenging for borrowers that need to refinance loans during the pandemic.

Key issues to date:

10© 2021 Deloitte Ireland LLP. All rights reserved.

TP Documentation

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 11

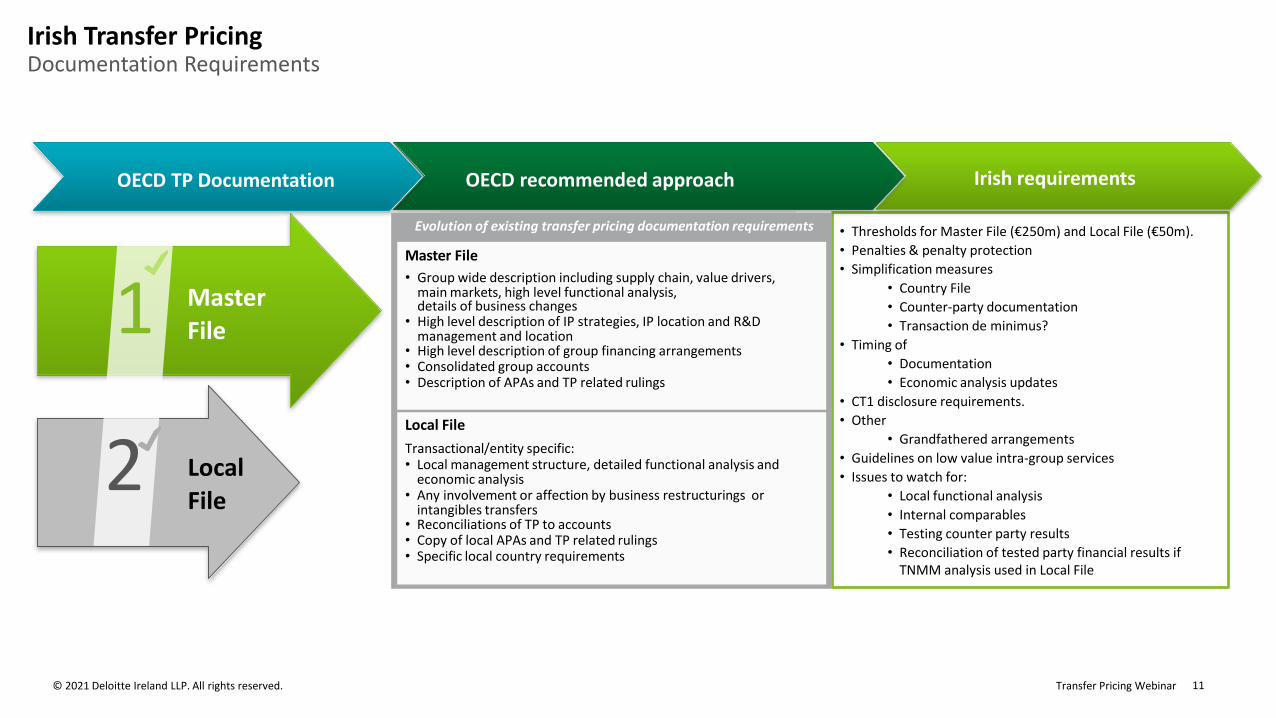

1

2

MasterFile

LocalFile

• Thresholds for Master File (€250m) and Local File (€50m).

• Penalties & penalty protection

• Simplification measures

• Country File

• Counter-party documentation

• Transaction de minimus?

• Timing of

• Documentation

• Economic analysis updates

• CT1 disclosure requirements.

• Other

• Grandfathered arrangements

• Guidelines on low value intra-group services

• Issues to watch for:

• Local functional analysis

• Internal comparables

• Testing counter party results

• Reconciliation of tested party financial results if TNMM analysis used in Local File

Irish requirementsOECD recommended approachOECD TP Documentation

Evolution of existing transfer pricing documentation requirements

Master File

• Group wide description including supply chain, value drivers, main markets, high level functional analysis,details of business changes

• High level description of IP strategies, IP location and R&D management and location

• High level description of group financing arrangements• Consolidated group accounts• Description of APAs and TP related rulings

Local File

Transactional/entity specific:• Local management structure, detailed functional analysis and

economic analysis• Any involvement or affection by business restructurings or

intangibles transfers• Reconciliations of TP to accounts• Copy of local APAs and TP related rulings• Specific local country requirements

Irish Transfer Pricing Documentation Requirements

12© 2021 Deloitte Ireland LLP. All rights reserved.

Exemptions

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 13

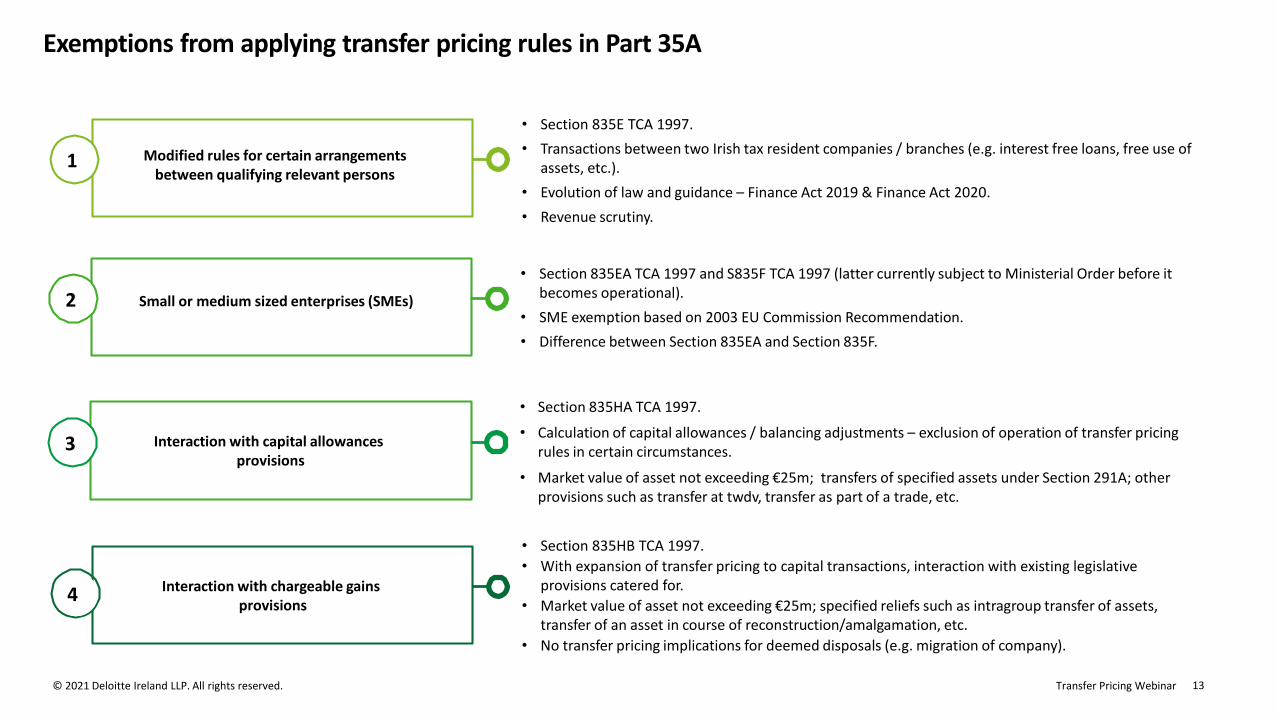

Exemptions from applying transfer pricing rules in Part 35A

• Section 835EA TCA 1997 and S835F TCA 1997 (latter currently subject to Ministerial Order before it becomes operational).

• SME exemption based on 2003 EU Commission Recommendation.

• Difference between Section 835EA and Section 835F.

2

• Section 835HA TCA 1997.

• Calculation of capital allowances / balancing adjustments – exclusion of operation of transfer pricing rules in certain circumstances.

• Market value of asset not exceeding €25m; transfers of specified assets under Section 291A; other provisions such as transfer at twdv, transfer as part of a trade, etc.

3

• Section 835HB TCA 1997.

• With expansion of transfer pricing to capital transactions, interaction with existing legislative provisions catered for.

• Market value of asset not exceeding €25m; specified reliefs such as intragroup transfer of assets, transfer of an asset in course of reconstruction/amalgamation, etc.

• No transfer pricing implications for deemed disposals (e.g. migration of company).

4

© 2020 Deloitte & Touche (M.E.) All rightsreserved.

13

Small or medium sized enterprises (SMEs)

• Section 835E TCA 1997.

• Transactions between two Irish tax resident companies / branches (e.g. interest free loans, free use of assets, etc.).

• Evolution of law and guidance – Finance Act 2019 & Finance Act 2020.

• Revenue scrutiny.

1 Modified rules for certain arrangements between qualifying relevant persons

Interaction with capital allowancesprovisions

Interaction with chargeable gainsprovisions

4

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 14

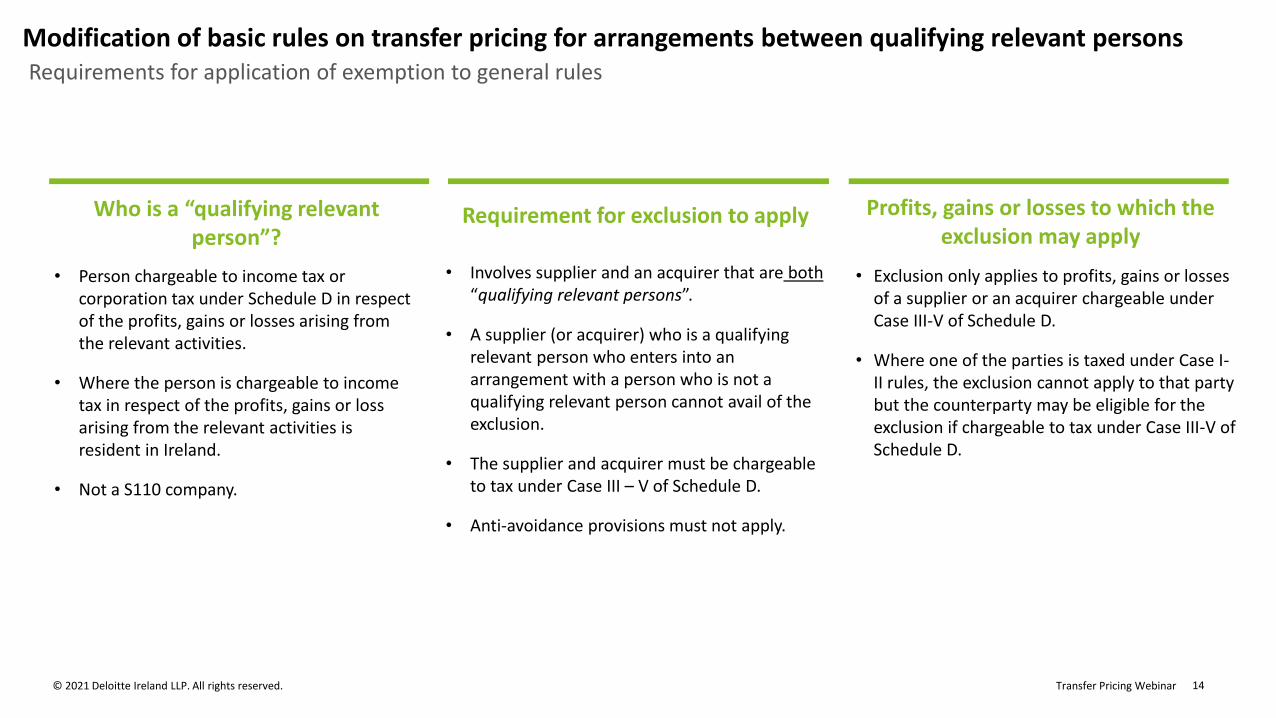

Requirements for application of exemption to general rules

Modification of basic rules on transfer pricing for arrangements between qualifying relevant persons

Who is a “qualifying relevant person”?

• Person chargeable to income tax or corporation tax under Schedule D in respect of the profits, gains or losses arising from the relevant activities.

• Where the person is chargeable to income tax in respect of the profits, gains or loss arising from the relevant activities is resident in Ireland.

• Not a S110 company.

• Involves supplier and an acquirer that are both “qualifying relevant persons”.

• A supplier (or acquirer) who is a qualifying relevant person who enters into an arrangement with a person who is not a qualifying relevant person cannot avail of the exclusion.

• The supplier and acquirer must be chargeable to tax under Case III – V of Schedule D.

• Anti-avoidance provisions must not apply.

• Exclusion only applies to profits, gains or losses of a supplier or an acquirer chargeable under Case III-V of Schedule D.

• Where one of the parties is taxed under Case I-II rules, the exclusion cannot apply to that party but the counterparty may be eligible for the exclusion if chargeable to tax under Case III-V of Schedule D.

Profits, gains or losses to which the exclusion may apply

Requirement for exclusion to apply

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 15

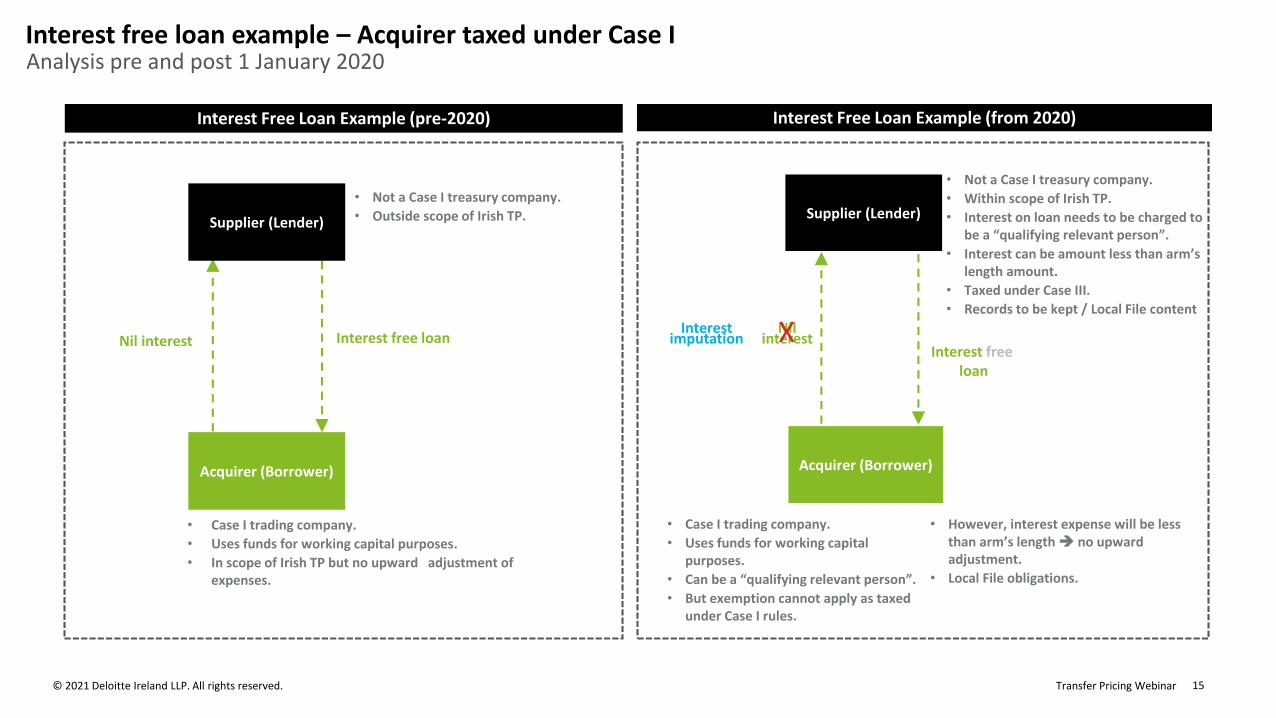

Interest free loan example – Acquirer taxed under Case I

Interest Free Loan Example (pre-2020)

Interest free loanNil interest

• Case I trading company.

• Uses funds for working capital purposes.

• In scope of Irish TP but no upward adjustment of expenses.

Acquirer (Borrower)

Supplier (Lender)

• Not a Case I treasury company.

• Outside scope of Irish TP.

Interest Free Loan Example (from 2020)

Interest freeloan

Nil interest

• Case I trading company.

• Uses funds for working capital purposes.

• Can be a “qualifying relevant person”.

• But exemption cannot apply as taxed under Case I rules.

• However, interest expense will be less than arm’s length no upward adjustment.

• Local File obligations.

Acquirer (Borrower)

Supplier (Lender)

• Not a Case I treasury company.

• Within scope of Irish TP.

• Interest on loan needs to be charged to be a “qualifying relevant person”.

• Interest can be amount less than arm’s length amount.

• Taxed under Case III.

• Records to be kept / Local File content

Interestimputation X

Analysis pre and post 1 January 2020

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 16

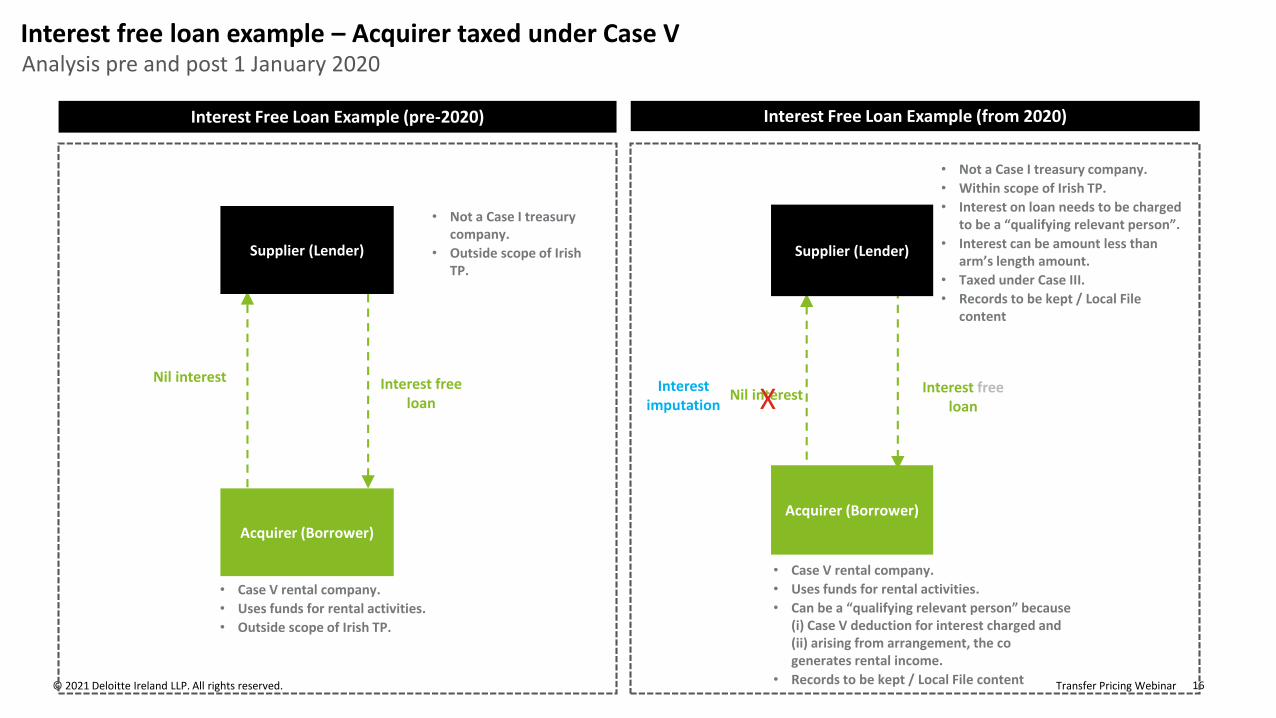

Interest free loan example – Acquirer taxed under Case V

Interest Free Loan Example (pre-2020)

• Case V rental company.

• Uses funds for rental activities.

• Outside scope of Irish TP.

Interest free loan

Nil interest

Acquirer (Borrower)

Supplier (Lender)

• Not a Case I treasury company.

• Outside scope of Irish TP.

Interest Free Loan Example (from 2020)

Interest freeloan

Nil interest

• Case V rental company.

• Uses funds for rental activities.

• Can be a “qualifying relevant person” because (i) Case V deduction for interest charged and (ii) arising from arrangement, the co generates rental income.

• Records to be kept / Local File content

Acquirer (Borrower)

Supplier (Lender)

• Not a Case I treasury company.

• Within scope of Irish TP.

• Interest on loan needs to be charged to be a “qualifying relevant person”.

• Interest can be amount less than arm’s length amount.

• Taxed under Case III.

• Records to be kept / Local File content

Interestimputation X

Analysis pre and post 1 January 2020

Transfer Pricing Webinar © 2021 Deloitte Ireland LLP. All rights reserved. 17

Q&A

Thank you for attending

Important notice

At Deloitte, we make an impact that matters for our clients, our people, our profession, and in the wider society by delivering the solutions and insights they need to address their

most complex business challenges. As the largest global professional services and consulting network, with over 312,000 professionals in more than 150 countries, we bring world-class

capabilities and high-quality services to our clients. In Ireland, Deloitte has over 3,000 people providing audit, tax, consulting, and corporate finance services to public and private

clients spanning multiple industries. Our people have the leadership capabilities, experience and insight to collaborate with clients so they can move forward with confidence.

This publication has been written in general terms and we recommend that you obtain professional advice before acting or refraining from action on any of the contents of this

publication. Deloitte Ireland LLP accepts no liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

Deloitte Ireland LLP is a limited liability partnership registered in Northern Ireland with registered number NC1499 and its registered office at 19 Bedford Street, Belfast BT2 7EJ,

Northern Ireland.

Deloitte Ireland LLP is the Ireland affiliate of Deloitte NSE LLP, a member firm of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”). DTTL and

each of its member firms are legally separate and independent entities. DTTL and Deloitte NSE LLP do not provide services to clients. Please see www.deloitte.com/about to learn more

about our global network of member firms.

© 2021 Deloitte Ireland LLP. All rights reserved.

![OECD Transfer Pricing Guidelines for OECD Transfer Pricing ... · OECD Transfer Pricing Guidelines and the involvement of the business community [DAFFE/CFA/WD(97)11/REV1], adopted](https://static.documents.pub/doc/80x56/5e02ef38d9e2ea2f2040f98f/oecd-transfer-pricing-guidelines-for-oecd-transfer-pricing-oecd-transfer-pricing.jpg)