23

Transfer Pricing – Risk and Opportunities David Slemmer, CohnReznick New York, New York June 6, 2014

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | muriel-todd |

| View: | 217 times |

| Download: | 2 times |

Transfer Pricing – Risk and Opportunities

David Slemmer, CohnReznickNew York, New York

June 6, 2014

Transfer Pricing – Risk and Opportunities

Agenda

• Introduction• Intellectual property• Tax planning opportunities – IP migration• Full risk distribution to stripped risk distribution• How do multinationals effectively manage these risks?• Questions

Transfer Pricing – Risk and Opportunities

• Transfer pricing refers to the way that multinationals price all transactions (goods, services, royalties, interest, etc.) between related entities.

• Transfer pricing is a primary concern for tax authorities that want a fair share of tax revenue and for multinationals that want a true measure of their profit driving activities.

• Intercompany transactions need to be priced on an “arm’s length” basis and multinational taxpayers are faced with significant compliance obligations and penalties to ensure compliance with this principle.

Introduction

Transfer Pricing – Risk and Opportunities

• Given that 70-80% of the value of a multinational corporation is considered to lie in its intangible assets, it is no surprise that the OECD and tax authorities globally are particularly focused on this aspect of transfer pricing (i.e., IP, royalties, etc.)

• The potential risks can include disallowance of tax deductions for license fee/royalty payments paid to related parties, arguments for significant exit taxes where IP is moved between group entities and claims for increased profitability in local distributors due to the presence of local marketing intangibles.

Introduction (cont’d)

Transfer Pricing – Risk and Opportunities

• As an indication of what impact this can have, the largest transfer pricing adjustment in history was imposed by the U.S. IRS on pharmaceutical company GlaxoSmithKline (GSK paid the IRS more than $3.0 billion, and abandoned its claim seeking a refund of nearly $2.0 billion in overpaid income taxes.) – There was a dispute between the IRS and HMRC in the UK regarding

whether the product intangibles or the marketing intangibles were the key driver of the success and profitability of a particular drug.

– Such differences of opinion are one of the many challenges of transfer pricing for intangibles and will be a critical feature of transfer pricing disputes going forward.

Introduction (cont’d)

Transfer Pricing – Risk and Opportunities

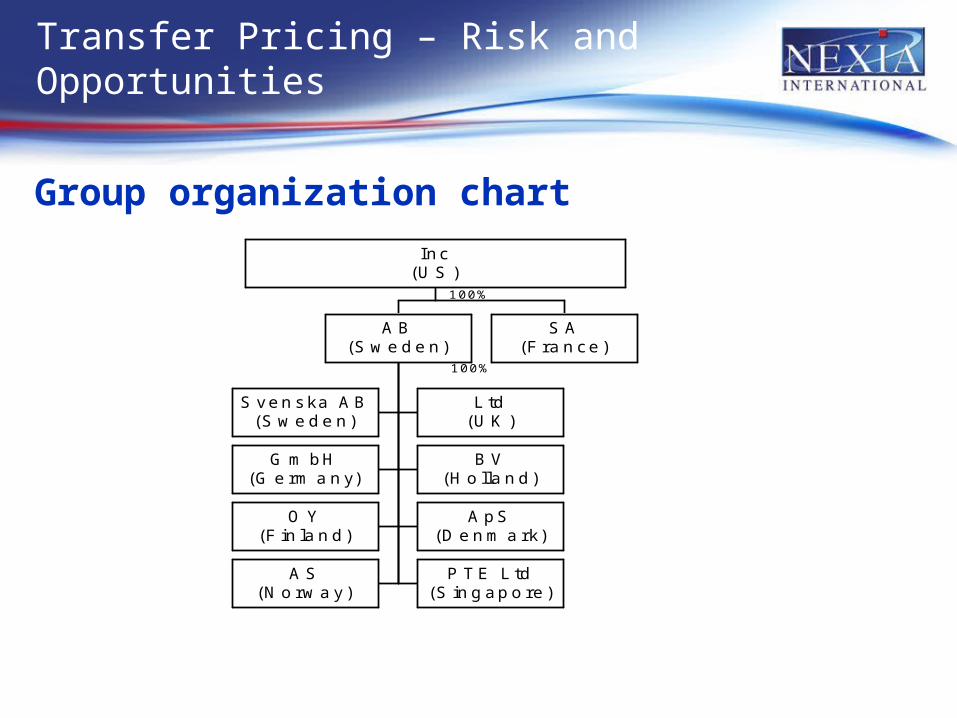

• US parent company ("Inc") is engaged in software development and consultancy in the field of business communication solutions.

• Inc has subsidiaries in Europe and Asia-Pacific.• Inc owns valuable brand name and software consulting

methodology.• Swedish subsidiary ("AB") is engaged in software publishing and

sale.• Other European subsidiaries ("consulting subsidiaries") engaged

in software consultancy and software sale.

Intellectual property holding companies - example

Transfer Pricing – Risk and Opportunities

Group organization chart

100%

100%

S ven ska A B(S w e d e n)

L td(U K )

G m bH(G e rm a n y)

B V(H o lla n d)

O Y(F in la n d)

A pS(D e n m a rk)

A S(N o rw a y )

P T E L td(S in g ap o re)

A B(S w e d e n)

S A(F ra n ce)

Inc(U S )

Transfer Pricing – Risk and Opportunities

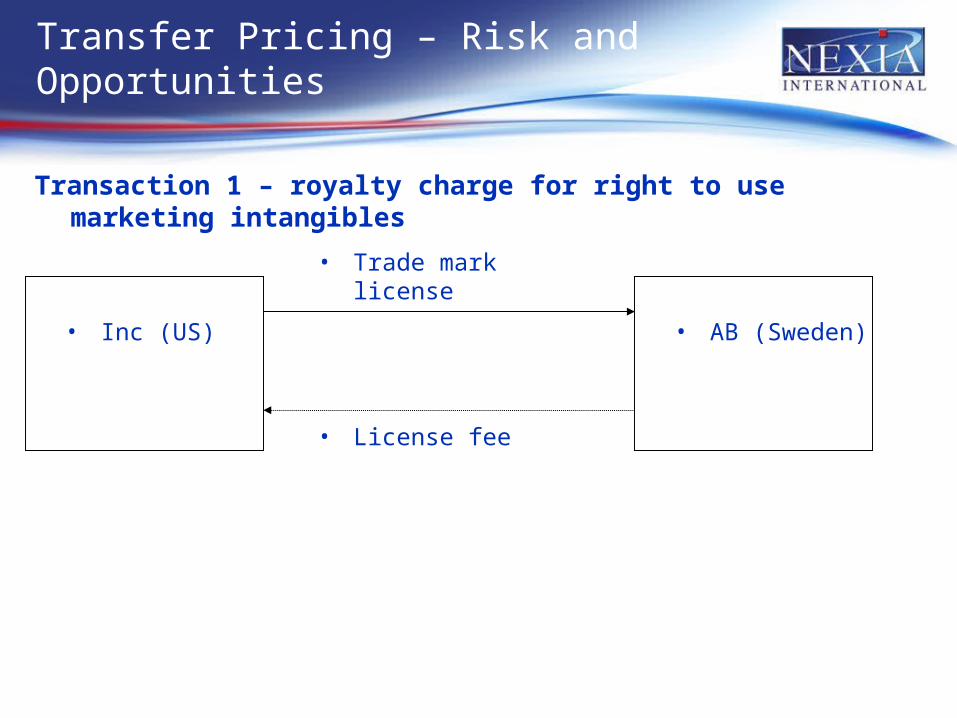

• Inc has extended to AB the right to use its trade name and trademark ("marketing intangibles") in order for AB to license its own software products to its subsidiaries, under Inc's brand name.

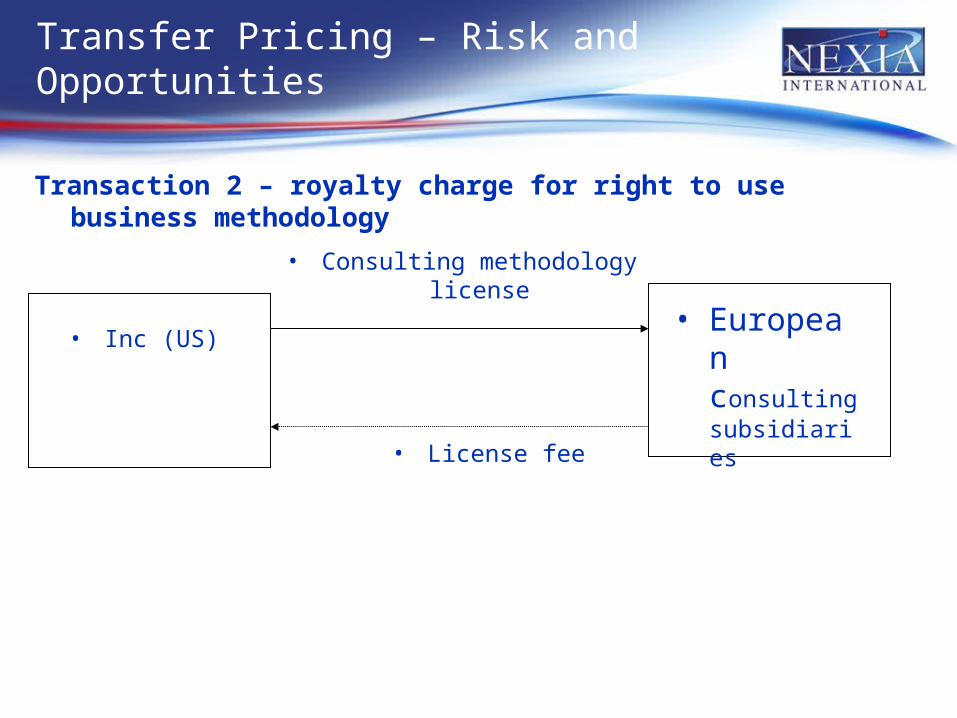

• Inc has extended to its European consulting subsidiaries the right to use its consulting methodology to provide software consultancy services to customers.

The intangibles involved

Transfer Pricing – Risk and Opportunities

Case for payment of two royalty charges to Inc from:• AB for the right to use the marketing intangibles; and• European consulting subsidiaries for the right to use Inc's

consulting methodology.

Proposed royalty charges

Transfer Pricing – Risk and Opportunities

Transaction 1 – royalty charge for right to use marketing intangibles

• Inc (US) • AB (Sweden)

• Trade mark license

• License fee

Transfer Pricing – Risk and Opportunities

Transaction 2 – royalty charge for right to use business methodology

• European consulting subsidiaries

• Consulting methodologylicense

• License fee

• Inc (US)

Transfer Pricing – Risk and Opportunities

External Comparable Uncontrolled Price (“CUP”) analysis • Conduct research for external comparable trademark licenses • Conduct research for external comparable business

methodology licenses

Arm’s length approach

Transfer Pricing – Risk and Opportunities

• This focus on intangibles represents an opportunity for taxpayers to identify what their intangibles are, where they are located and whether they can be managed more efficiently and effectively from an operational perspective in a centralized business model.

• Centralizing the ownership and management of intangible assets in a low tax jurisdiction, such as Hong Kong or Singapore, where this is supported by genuine economic substance and decision-making, may enable a multinational group to achieve significant reductions in effective tax rates while better managing overall transfer pricing risk (Be aware of treaty networks).

But these intangibles are in high tax location

Transfer Pricing – Risk and Opportunities

• Goals of IP migration– Reduce effective tax rate by earning profits from IP in a

lower taxed jurisdiction– Move existing rights at an appropriate transfer price– Do no harm to the IP legal ownership

Tax planning opportunities – IP migration

Transfer Pricing – Risk and Opportunities

• Why consider IP migration in a down economy?– Current and future value of existing IP has likely gone

down under a variety of methodologies– Creates opportunity for the ultimate turn-around

(assuming it comes!)

Tax planning opportunities – IP migration

Transfer Pricing – Risk and Opportunities

• Cost sharing agreement (U.S.)• Licensing model

– With contract R&D services– With marketing intangibles– Sale

Options for structuring an IP migration

Transfer Pricing – Risk and Opportunities

• Cost sharing if each participant has non-routine IP to contribute at the outset

• If that is not the case, licensing/contract R&D model is best• Remember to think about valuation opportunities (Call Ed!)• Appetite for risk/ risk management

What should you consider?

Transfer Pricing – Risk and Opportunities

Company goal:• To adapt to changes in global markets. • Belief that this is not efficient.

– Change from full risk distribution to stripped risk distribution• improve cash flow• achieve economies of scale • bring about other operational/ structural efficiencies

Full risk distribution to stripped risk distribution

Transfer Pricing – Risk and Opportunities

• responsible for completing sales calls to potential customers• take customer orders• have an ability to discount prices • take title to the goods they sell• take responsibility for forecasting and scheduling inventory shipments• hold inventory• bear accounts receivable, inventory, market, and product (with exception of

manufacturers' production liability) risks• bear costs of intellectual property protection• undertake some strategic marketing activities• perform many customer services• their primary intangibles are customer lists and brand awareness developed by the

distributor through its strategic marketing activities• remuneration is based on margin on sales of products.

Full risk distributor characteristics

Transfer Pricing – Risk and Opportunities

• responsible for completing sales calls to potential customers• may take customer orders• limited ability to discount prices • take flash title to the goods they sell• do not take responsibility for forecasting and scheduling inventory shipments• hold no inventory• bear accounts receivable risk• no inventory, market and product risks• do not bear costs of intellectual property protection• undertake no marketing activities• perform limited customer services• their only intangibles are customer lists and customer relationships• remuneration is based on margin on sales of products.

Stripped risk distributor characteristics

Transfer Pricing – Risk and Opportunities

• Database research for limited risk distributors (not easily done)• Conversion file with brief overview of reasons

• Board minutes• Background paper• Business case for conversion• Functional analysis• New transfer pricing agreements are critical• Financial details and projections

• Tax compliance and local tax inspector considerations

Potential implementation issues

Transfer Pricing – Risk and Opportunities

• Review royalties and license fees for product, process or marketing intangibles to ensure there is a clear benefit received from the payment and that the rate applied can be demonstrated to be arm’s length if and when questioned by one of the affected tax authorities;

• When designing or reviewing a transfer pricing system, give particular attention to where the key intangible-generating activities are located, as these may give rise to higher profit expectations in future; and

• Consider the impact of the transfer pricing rules and potential exit taxes when undertaking any form of business restructuring involving movement of functions or assets within a group.

How do multinationals effectively manage these risks?

Transfer Pricing – Risk and Opportunities

© 2014 Nexia International Limited. All rights reserved. The trade marks NEXIA INTERNATIONAL, NEXIA and the NEXIA logo are owned by Nexia International Limited. Nexia International and its member firms are not part of a worldwide partnership.Member firms of Nexia International are independently owned and operated. Nexia International does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its members.

Questions