NCSL’s Legislative Conference Transforming Medicaid Lessons from Pioneering States Deborah Bachrach August 20, 2014 1 Drivers of Reform 2 Health Care Cost Growth 0 500 1000 1500 2000 2500 3000 1960 1970 1980 1990 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 National Health Expenditures (in billions) National Health Expenditures from 1960-2012 Source: Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group; U.S. Department of Commerce, Bureau of Economic Analysis; and U.S. Bureau of the Census, http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends- and-Reports/NationalHealthExpendData/Downloads/tables.pdf In fiscal 2011, before implementation of the ACA’s Medicaid expansion, Medicaid comprised over 23 percent of total state expenditures.

Transcript

NCSL’s Legislative Conference

Transforming Medicaid Lessons from Pioneering States

Deborah Bachrach

August 20, 2014

1

Drivers of Reform

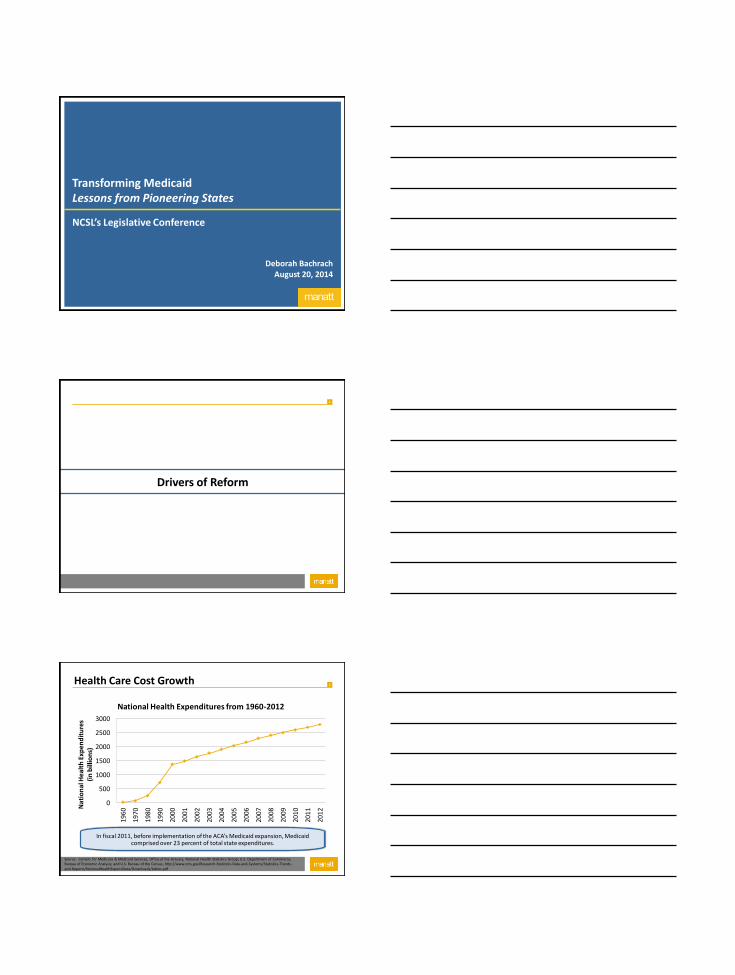

2 Health Care Cost Growth

0

500

1000

1500

2000

2500

3000

196

0

197

0

198

0

199

0

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2 Nat

ion

al H

ealt

h E

xpen

dit

ure

s

(in

bill

ion

s)

National Health Expenditures from 1960-2012

Source: Centers for Medicare & Medicaid Services, Office of the Actuary, National Health Statistics Group; U.S. Department of Commerce, Bureau of Economic Analysis; and U.S. Bureau of the Census, http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/tables.pdf

In fiscal 2011, before implementation of the ACA’s Medicaid expansion, Medicaid comprised over 23 percent of total state expenditures.

3

“Triple Aim”

Better Care

Better Health Lower Costs

Triple Aim

4 Medicaid Expansion

Medicaid is broken; Reform

comes first

Payment and Delivery Reform

Expansion States Non Expansion States

Expansion requires reform; reform

requires expansion

5

Reform Strategies

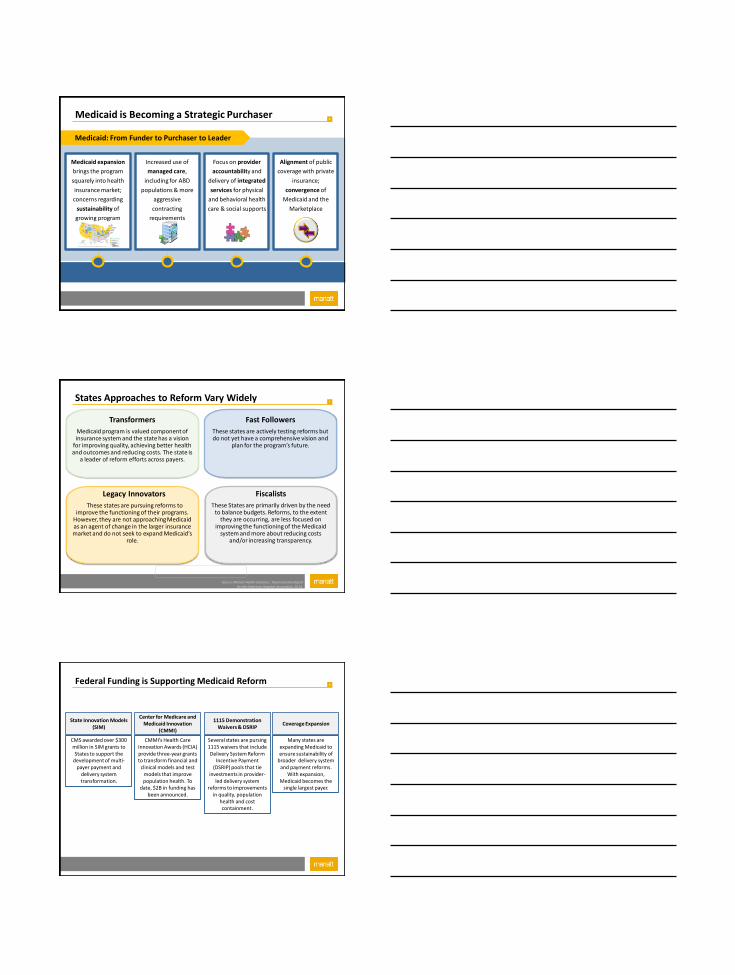

6 Medicaid is Becoming a Strategic Purchaser

Medicaid expansion

brings the program

squarely into health

insurance market;

concerns regarding

sustainability of

growing program

surface

Medicaid: From Funder to Purchaser to Leader

Increased use of

managed care,

including for ABD

populations & more

aggressive

contracting

requirements

Focus on provider

accountability and

delivery of integrated

services for physical

and behavioral health

care & social supports

Alignment of public

coverage with private

insurance;

convergence of

Medicaid and the

Marketplace

7

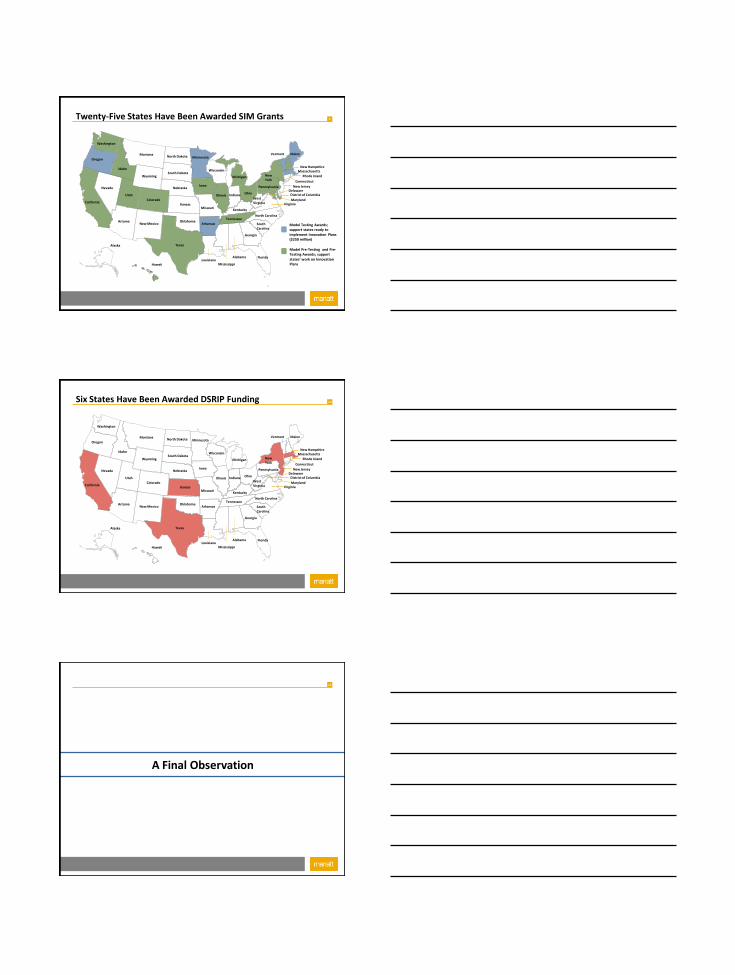

Fast Followers

These states are actively testing reforms but do not yet have a comprehensive vision and

plan for the program’s future.

Legacy Innovators

These states are pursuing reforms to improve the functioning of their programs.

However, they are not approaching Medicaid as an agent of change in the larger insurance market and do not seek to expand Medicaid’s

role.

Fiscalists

These States are primarily driven by the need to balance budgets. Reforms, to the extent

they are occurring, are less focused on improving the functioning of the Medicaid

system and more about reducing costs and/or increasing transparency.

Transformers

Medicaid program is valued component of insurance system and the state has a vision

for improving quality, achieving better health and outcomes and reducing costs. The state is

a leader of reform efforts across payers.

States Approaches to Reform Vary Widely

Source: Manatt Health Solutions. Taxonomy Developed for the American Hospital Association, 2014.

8

CMMI’s Health Care Innovation Awards (HCIA) provide three-year grants to transform financial and

clinical models and test models that improve population health. To

date, $2B in funding has been announced.

CMS awarded over $300 million in SIM grants to States to support the

development of multi-payer payment and

delivery system transformation.

State Innovation Models (SIM)

Center for Medicare and Medicaid Innovation

(CMMI)

Several states are pursing 1115 waivers that include Delivery System Reform

Incentive Payment (DSRIP) pools that tie

investments in provider-led delivery system

reforms to improvements in quality, population

health and cost containment.

1115 Demonstration Waivers & DSRIP

Many states are expanding Medicaid to ensure sustainability of

broader delivery system and payment reforms.

With expansion, Medicaid becomes the

single largest payer.

Coverage Expansion

Federal Funding is Supporting Medicaid Reform

9 Twenty-Five States Have Been Awarded SIM Grants

Alaska

Hawaii

Michigan

California

Nevada

Oregon

Arizona

Utah

Idaho

Montana

Wyoming

Colorado

New Mexico

Nebraska

Maine Vermont

New York

North Carolina

Georgia

South Carolina

Florida Alabama

Mississippi Louisiana

Texas

Pennsylvania

Wisconsin

Minnesota North Dakota

Ohio

West Virginia

South Dakota

Arkansas

Missouri

Iowa

Illinois Indiana

Tennessee

Kentucky

Delaware New Jersey

Connecticut

Massachusetts New Hampshire

Virginia Maryland

Rhode Island

District of Columbia

Kansas

Oklahoma Model Testing Awards; support states ready to implement Innovation Plans ($250 million)

Model Pre-Testing and Pre-Testing Awards; support states’ work on Innovation Plans

Washington

10 Six States Have Been Awarded DSRIP Funding

Alaska

Hawaii

Michigan

California

Nevada

Oregon

Arizona

Utah

Idaho

Montana

Wyoming

Colorado

New Mexico

Nebraska

Maine Vermont

New York

North Carolina

Georgia

South Carolina

Florida Alabama

Mississippi Louisiana

Texas

Pennsylvania

Wisconsin

Minnesota North Dakota

Ohio

West Virginia

South Dakota

Arkansas

Missouri

Iowa

Illinois Indiana

Tennessee

Kentucky

Delaware New Jersey

Connecticut

Massachusetts New Hampshire

Virginia Maryland

Rhode Island

District of Columbia

Kansas

Oklahoma

Washington

11

A Final Observation

12

From Medicaid to All-Payer Reform Attributes of Successful State Transformation Initiatives