14

WINNING IN THE DISRUPTION ERA FOR COMMUNICATIONS SERVICE PROVIDERS TRASH THE RULEBOOK BORIS MAURER TM Forum Digital Transformation World - May 2018 #NewAppliedNow

WINNING IN THE DISRUPTION ERA FOR COMMUNICATIONS SERVICE PROVIDERS

TRASH THE RULEBOOK

BORIS MAURER

TM Forum

Digital Transformation World -

May 2018 #NewAppliedNow

Copyright © 2018 Accenture. All rights reserved. 2

(67.0%)

(20 .0%)

(15.0%)

(12.3%)(10 .9%)(10 .2%)

(8.3%)

(2.2%)(0 .7%)

2.8%3.2%3.5%

6.3%8.6%9.7%10 .8%

15.0%23.2%24.1%

(23.4%)(20 .6%)

(15.8%)

(14.2%)(13.0%)

(7.6%)(5.8%)(5.0%)

(2.8%)

(0 .3%)

(61.8%)(51.6%)

(46.6%)(29.1%)

(18.3%)

(8.4%)

(2.9%)

Ø -10.2%

Telstra

MTN

BT

VEONKDDI

Vodafone

Swisscom

Deutsche TelekomLiberty

Iliad SA

NTT

Bharti Airtel

Orange

China Mobile

Telia

China Telecom

Hellenic

Telephone and Data Systems

Comcast

Singapore Telecom

CenturyLink

TELUS

KT Corp

Telefónica

SK Telecom

Telenor

SoftBank

PTTTelecom Italia

AT&T

Verizon

WindstreamBCE

América MóvilEmirates Telecom

KPN

Future Value Change =[(avg 2015-2017 FV) - (avg 2013-2015 FV)] / [2012-2017 avg Invested Capital]

CSP Future Value Erosion 2012-2017

0

200

400

600

800

1,000

1,200

1,400

2012 2013 2014 2015 2016

Disruptive investments in options to ensure high future value

Current valueFuture value

Disruptor Future Value Accretion 2012-2016

En

terp

rise

Va

lue

$B

Source : Company reports, Accenture Analysis

INVESTOR OPTIMISM HAS WANED WHILE DISRUPTORS HAVE SEIZED THE FUTURE

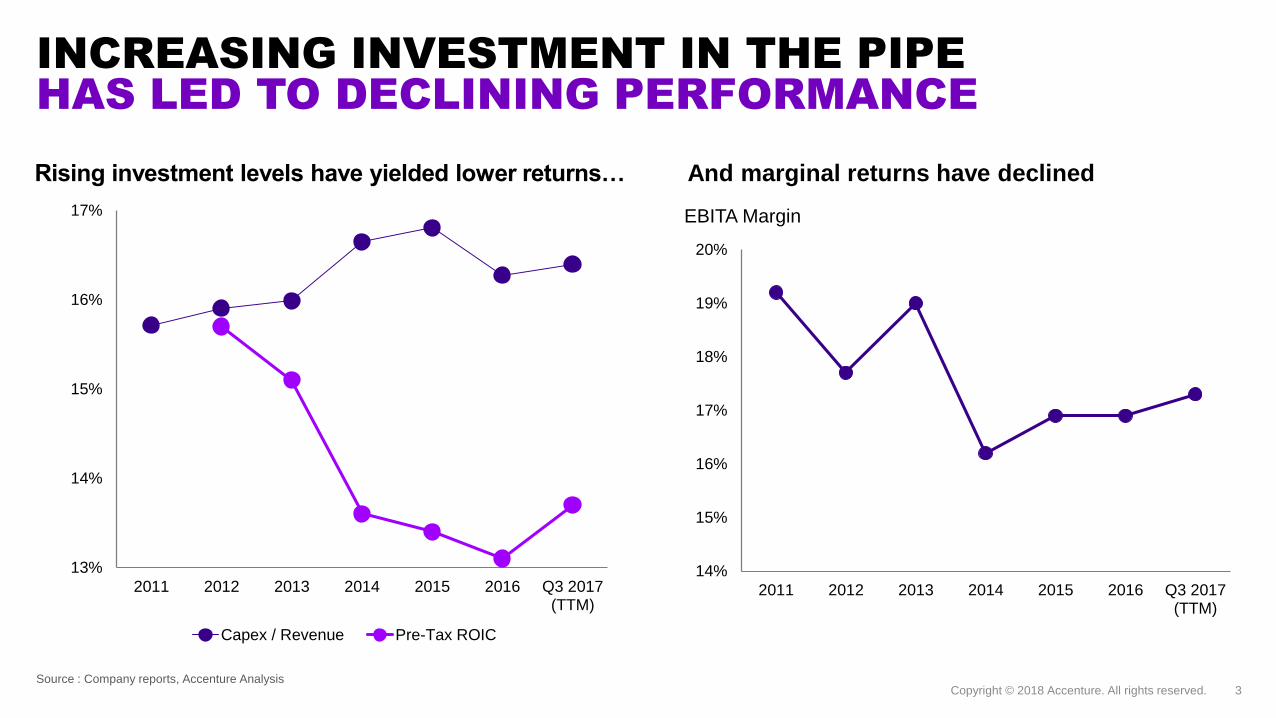

INCREASING INVESTMENT IN THE PIPE HAS LED TO DECLINING PERFORMANCE

Copyright © 2018 Accenture. All rights reserved. 3

14%

15%

16%

17%

18%

19%

20%

2011 2012 2013 2014 2015 2016 Q3 2017(TTM)

EBITA Margin

Rising investment levels have yielded lower returns… And marginal returns have declined

13%

14%

15%

16%

17%

2011 2012 2013 2014 2015 2016 Q3 2017(TTM)

Capex / Revenue Pre-Tax ROIC

Source : Company reports, Accenture Analysis

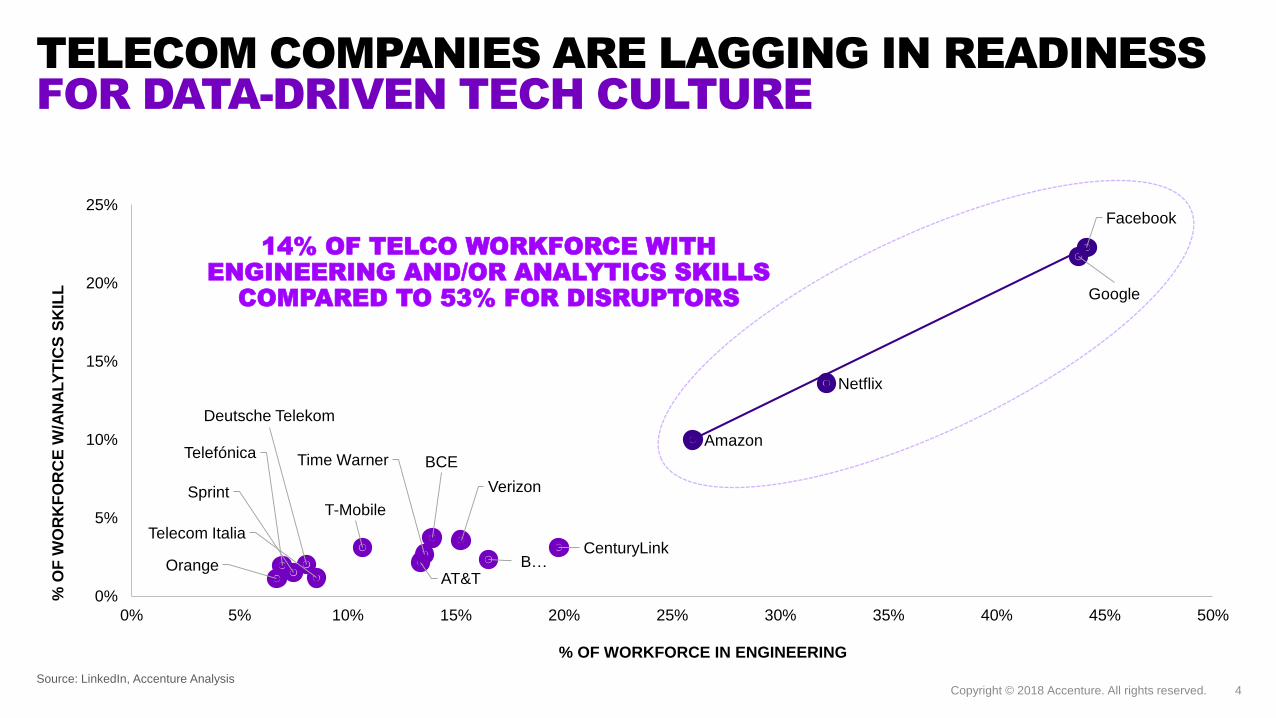

TELECOM COMPANIES ARE LAGGING IN READINESS FOR DATA-DRIVEN TECH CULTURE

Copyright © 2018 Accenture. All rights reserved. 4Source: LinkedIn, Accenture Analysis

Amazon

Netflix

AT&T

Verizon

Telefónica

Deutsche Telekom

Time Warner

Orange

Telecom Italia

T-Mobile

B…

Sprint

CenturyLink

BCE

0%

5%

10%

15%

20%

25%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

% O

F W

OR

KF

OR

CE

W/A

NA

LY

TIC

S S

KIL

L

% OF WORKFORCE IN ENGINEERING

14% OF TELCO WORKFORCE WITH ENGINEERING AND/OR ANALYTICS SKILLS

COMPARED TO 53% FOR DISRUPTORS

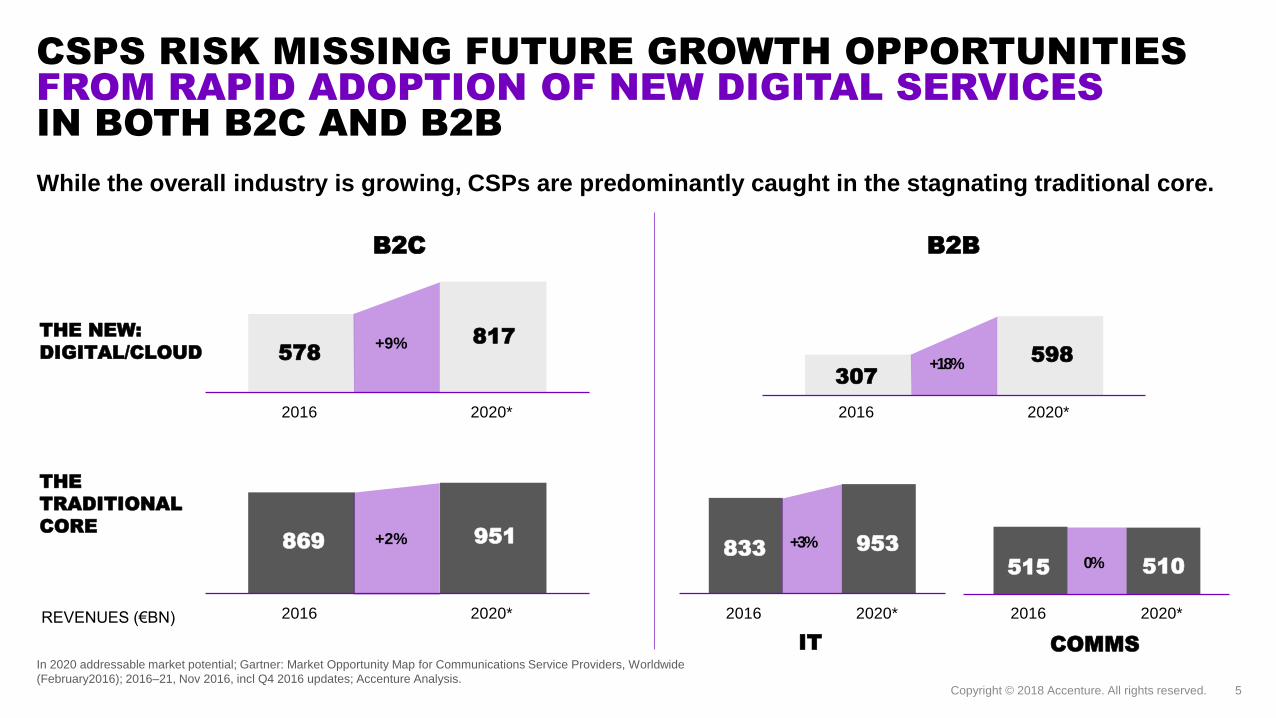

CSPS RISK MISSING FUTURE GROWTH OPPORTUNITIES FROM RAPID ADOPTION OF NEW DIGITAL SERVICES IN BOTH B2C AND B2B

Copyright © 2018 Accenture. All rights reserved. 5

While the overall industry is growing, CSPs are predominantly caught in the stagnating traditional core.

578817

2020*2016

307598

2020*2016

869 951

2020*2016

833 953

2020*2016

515 510

2020*2016

THE

TRADITIONAL

CORE

THE NEW:

DIGITAL/CLOUD

IT COMMS

B2BB2C

In 2020 addressable market potential; Gartner: Market Opportunity Map for Communications Service Providers, Worldwide

(February2016); 2016–21, Nov 2016, incl Q4 2016 updates; Accenture Analysis.

REVENUES (€BN)

+9%

+2%

+18%

+3%

0%

PICK YOUR PLAYNetwork Innovator, Ecosystem

Player? We believe there are four

scenarios emerging for CSPs to scale new growth models.

Copyright © 2018 Accenture. All rights reserved.#NewAppliedNow

TELCO EVOLUTION INTO ECO-SYSTEM ORCHESTRATORS

Copyright © 2018 Accenture. All rights reserved. 7

MULTI-SIDED PLATFORM

MODEL

CONNECTED INDUSTRY

ORCHESTRATOR

VERTICALLY INTEGRATED

SERVICE PROVIDER

DIGITAL MOBILE

ONLY ATTACKER

Establish cloud-platform business

enriched by OTT/industry partners

Monetizing core with digital services and

customer interactions

Monetizing core with differentiated

services / content bundles

Managing intelligent, open,

self-service digital networks

SCENARIO DESCRIPTION

CUSTOMER BASED ECO

SYSTEM PLAY

INFRASTRUCTURE-BASED

NETWORK PLAY

CO

NT

INU

UM

OF

OP

TIO

NS

LONG TERM PLAY

LONG TERM PLAY

SC

AL

E T

HE

NE

W

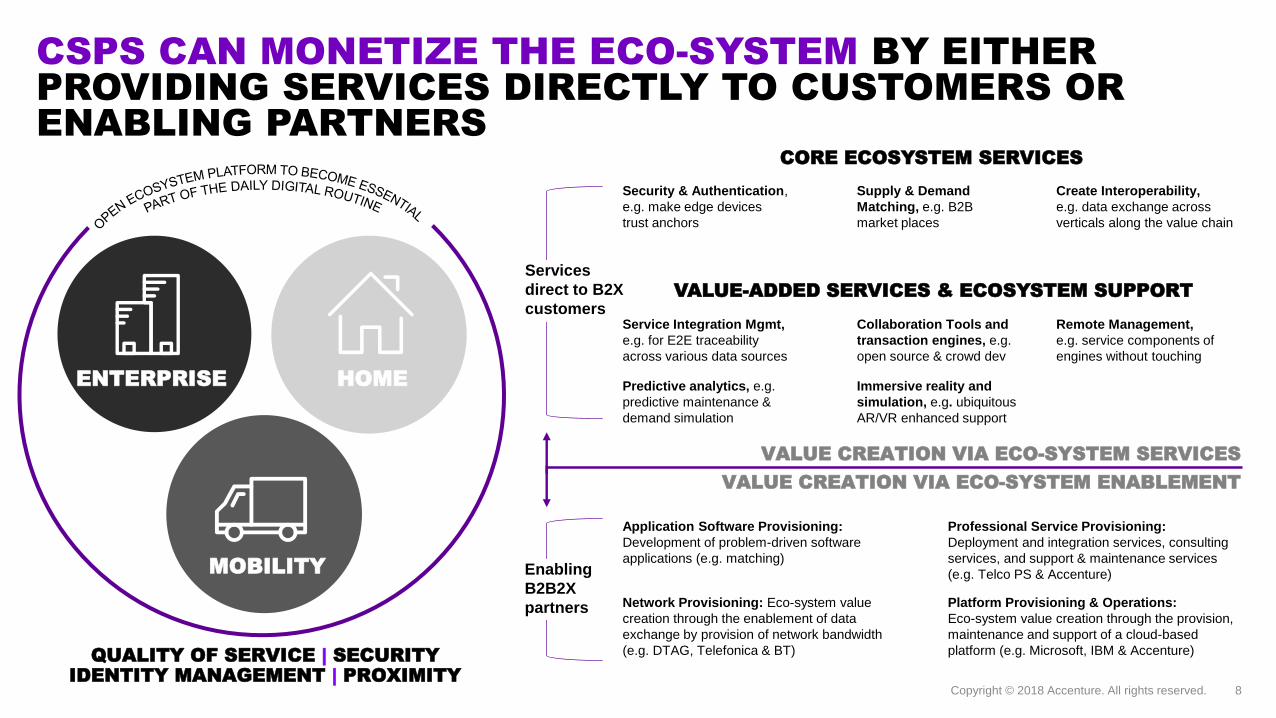

CSPS CAN MONETIZE THE ECO-SYSTEM BY EITHER PROVIDING SERVICES DIRECTLY TO CUSTOMERS OR ENABLING PARTNERS

Copyright © 2018 Accenture. All rights reserved. 8

QUALITY OF SERVICE | SECURITY IDENTITY MANAGEMENT | PROXIMITY

ENTERPRISE

VALUE CREATION VIA ECO-SYSTEM ENABLEMENT

VALUE CREATION VIA ECO-SYSTEM SERVICES

CORE ECOSYSTEM SERVICES

Security & Authentication,

e.g. make edge devices

trust anchors

VALUE-ADDED SERVICES & ECOSYSTEM SUPPORT

Supply & Demand

Matching, e.g. B2B

market places

Create Interoperability,

e.g. data exchange across

verticals along the value chain

Service Integration Mgmt,

e.g. for E2E traceability

across various data sources

Collaboration Tools and

transaction engines, e.g.

open source & crowd dev

Remote Management,

e.g. service components of

engines without touching

Predictive analytics, e.g.

predictive maintenance &

demand simulation

Immersive reality and

simulation, e.g. ubiquitous

AR/VR enhanced support

Services

direct to B2X

customers

Application Software Provisioning:

Development of problem-driven software

applications (e.g. matching)

Network Provisioning: Eco-system value

creation through the enablement of data

exchange by provision of network bandwidth

(e.g. DTAG, Telefonica & BT)

Professional Service Provisioning:

Deployment and integration services, consulting

services, and support & maintenance services

(e.g. Telco PS & Accenture)

Platform Provisioning & Operations:

Eco-system value creation through the provision,

maintenance and support of a cloud-based

platform (e.g. Microsoft, IBM & Accenture)

Enabling

B2B2X

partners

MOBILITY

HOME

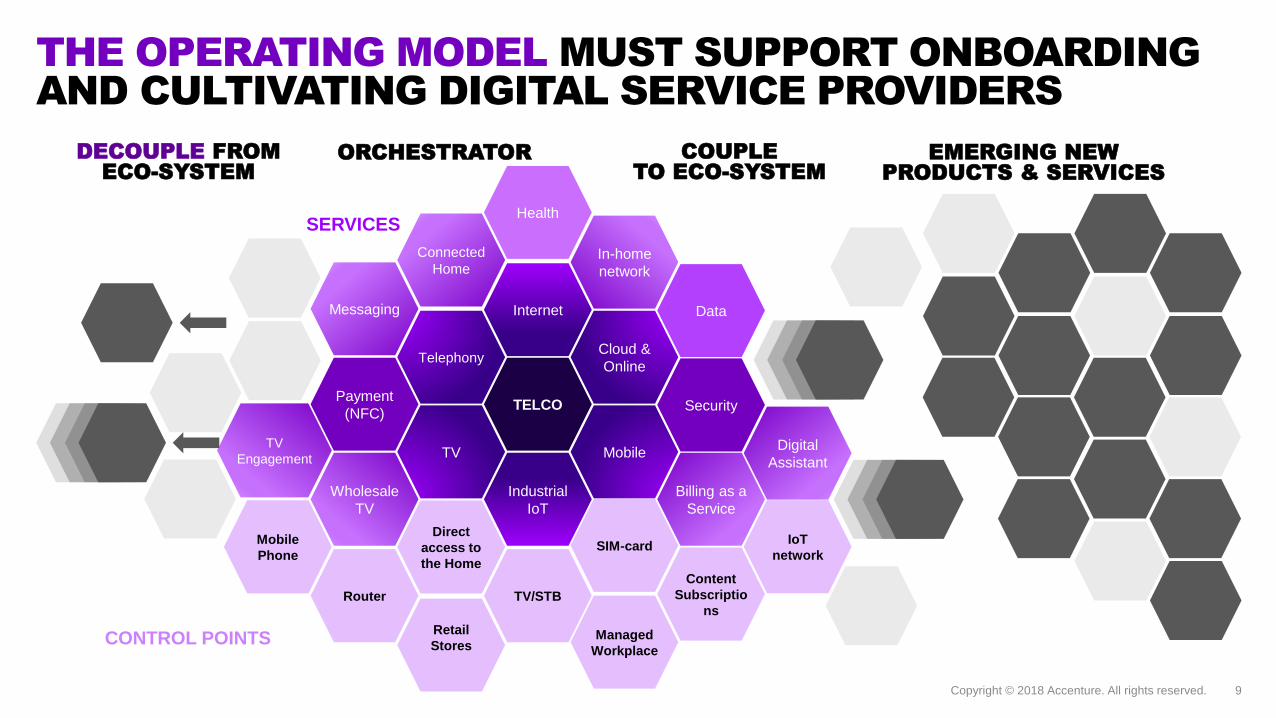

THE OPERATING MODEL MUST SUPPORT ONBOARDING AND CULTIVATING DIGITAL SERVICE PROVIDERS

Telephony

Internet

TELCO

Cloud &

Online

Data

Security

TV

Engagement

Industrial

IoT

Billing as a

Service

Messaging

Payment

(NFC)

Wholesale

TV

TV Mobile

Health

Connected

HomeIn-home

network

Digital

Assistant

Retail

Stores

Content

Subscriptio

nsRouter

SIM-cardDirect

access to

the Home

Mobile

Phone

Managed

Workplace

TV/STB

IoT

network

SERVICES

CONTROL POINTS

COUPLETO ECO-SYSTEM

DECOUPLE FROMECO-SYSTEM

ORCHESTRATOR EMERGING NEWPRODUCTS & SERVICES

Copyright © 2018 Accenture. All rights reserved. 9

POLICY-DRIVEN NETWORKING & MEC ALLOW CSP’S TO CONQUER CRITICAL CONTROL POINTS

Copyright © 2018 Accenture. All rights reserved. 10

REGIONAL NETWORKS / COLO / ETHERNET BACKBONECORPORATE OFFICES

MobileNetwork

MOBILE NETWORKS

Regional Network

MPLS / IP VPN/SD - WAN

Broadband / Internet

LTE

PRIVATE CLOUD

PUBLIC CLOUD

IOT

EDGE COMPUTING

Managed LAN

Managed Wi-Fi

CLOUD

Key Policy Alignment Points –CSP specific

Key Policy Alignment Points –Enterprise on prem workloads

Key Policy Alignment Points –Enterprise off prem workloads

TECHNOLOGY REVOLUTION WITH 5G DRIVEN BY DATA IN A DISTRIBUTED CLOUD TOPOLOGY

Copyright © 2018 Accenture. All rights reserved. 11

14%

0% 20% 40% 60% 80% 100%

23%

69%BUSINESSES

CONSUMERS

GOVERNMENT

Most Important Somewhat Important Neutral

Not Very Important Least Important

10%

75%

2017 2022

X7.5

New capabilities required in distributed computing

architectures, remote management and edge security

% OF ENTERPRISE-GENERATED DATA

processed outside traditional data center or cloud

TELCOS INCREMENTAL REVENUE POTENTIAL

from 5G

Source: GSMA, Global Mobile Trends 2017, September 2017

PAST FUTUREPRESENT

Services and Connectivity strictly

bundled through a closed Network

Technology

Limited competition, strongly

dominated by Network Incumbents

High barriers for new entrants

Connectivity

Marketplace

OTT players compete with Telcos to

sell content/digital services over the

IP Layer. Limited/zero cooperation

with operators

Operators strategies not well defined,

struggling to define how compete on

services, while monetizing the physical

network asset

Services

Transaction

Based

Operators newly a key actor of the digital

marketplace providing:

• Premium infrastructure (Network Slicing, MEC)

• Common platform/enablers for Industry X.0

Enhance cooperation with partners through the

Telco open-platform:

• Content/Media (OTT players)

• Home service providers (home automation,

home security etc.)

• Public administrations (e-Health, Smart

cities etc.)

• Industry X.0 vertical partners

Hard-Bundle of

Services and

Connectivity

Connectivity

Fixed Fee

(Connectivity)

Pay-per-Use

(Services) Fixed

Fee

VALUE CREATION IS EVOLVING FROM COMPETITION WITH OTT TO A COMPLEMENTARY MODEL

Copyright © 2018 Accenture. All rights reserved. 12

Copyright © 2018 Accenture. All rights reserved. 13

Service Service

Fee

FROMstand alone, one-product

service provider

TOone to many, diversified communication

services enriched with eco-system

originated offers

Service Access

Recurring charges (per service

and contract commitment)

Number of transactions

Value per transaction

Service Service

Fee

Partner

Ecosystem

Marketplace

Key Value

Elements

CREATING MARKET VALUE IS SHIFTINGTO A TRANSACTION BASED REVENUE MODEL

STEPFORWARDIt’s time to lead or lose.

Copyright © 2018 Accenture. All rights reserved.

#NewAppliedNow