32

Global Energy Trends and it’s Impact on European Petrochemicals Dusseldorf Mar 11, 2015

Global Energy Trends and it’s Impact on European Petrochemicals

Dusseldorf Mar 11, 2015

01 Large uncertainties in evolution of global crude oil market –

balance of US Light Tight Oil (LTO) production and global

demand evolution will dictate outcomes in the mid-term

Crude oil summary

Crude oil

Oil & Gas industry has rarely seen magnitude and pace of change as in previous 2-3

years; as a result, huge uncertainty in crude industry outlook

Little agreement among various industry players/experts as to crude price outlook

– Bulls – Crude prices will keep going up (Barclays)

– Bears – Increased oil production could take crude to $70-90/bbl (IHS CERA, Citibank)

– Middle of road – Oil production will increase, but not sure of impact on crude prices

(McKinsey, Goldman)

However, few dynamics likely to continue to play a role

– Marginal global supply is currently around $90/bbl, which could be “equilibrium crude

price”

– Fiscal earnings pressures on OPEC countries require $90+ crude oil price

– Downward pressure by Light Tight Oil (LTO) to below $90

3

Recent steep decline in global crude oil price – what happened?

0

20

40

60

80

100

120

140

Jan-1990 Jan-2010 Jan-1995 Jan-2015 Jan-2005 Jan-2000

• Crude oil prices plunged 60% since June ‘14, due to a ~1MMBPD oversupply in 2H '14

Global liquids supply grew YoY 2.0 MMBPD, primarily from US tight oil, Libya and Iraq

Simultaneously, demand growth slowed to 0.9 MMBPD driven by weak Chinese and European economies

• Crude prices reacted violently as OPEC declined to intervene

Through 2014 Saudi reduced its global selling prices to maintain share in the face of a crowded market...

...and on 27th Nov, OPEC decided to maintain production quota at 30 MMBPD

• In recent decades, oil price recoveries have varied widely

This decline was catalysed by both supply and demand-side factors

The pace and shape of recovery will thus depend upon multiple parallel supply and demand changes

• But where could prices go in the meantime?

There is a de-facto floor around $35-40 where we reach cash lifting costs for a significant slice of production

Marginal economics should, in the longer-term, demand prices around $90 or more

Brent Crude Price $/bbl

Source: EIA; BCG 4

Oil price declines similar in duration, but recoveries vary a lot

20

30

40

50

60

70

80

90

100

Days

1150 1100 1050 1000 950 900 850 800 750 700 650 600 550 500 450 400 350 300 250 200 150 100 50 0

Dec 2008

Mar 1986 Mar 1998 Jan 2007 Dec 1998

Oil price declines / recoveries since 1986

Jan 2014

(Ongoing)

Decline (Days)

Recovery (Days)

82 Mar 1986

Mar 1998

Dec 1998

Jan 2007

Dec 2008

1184

165 535

72 107

164 232

163

Jan 2014 193

1. Days given is to the next historically high price peak which equals 78.1% recovery ($113.39 on 29 April 2011 from a pre-decline price of $145.16 on 14 July 2008) - All prices are WTI Source: EIA, BCG Analysis

1 70% 100%

280

371

28

31

1018 764

5

SOURCE: EIA; Deutsche Bank; ShaleGas.com; USGS; NPC; company announcements; McKinsey

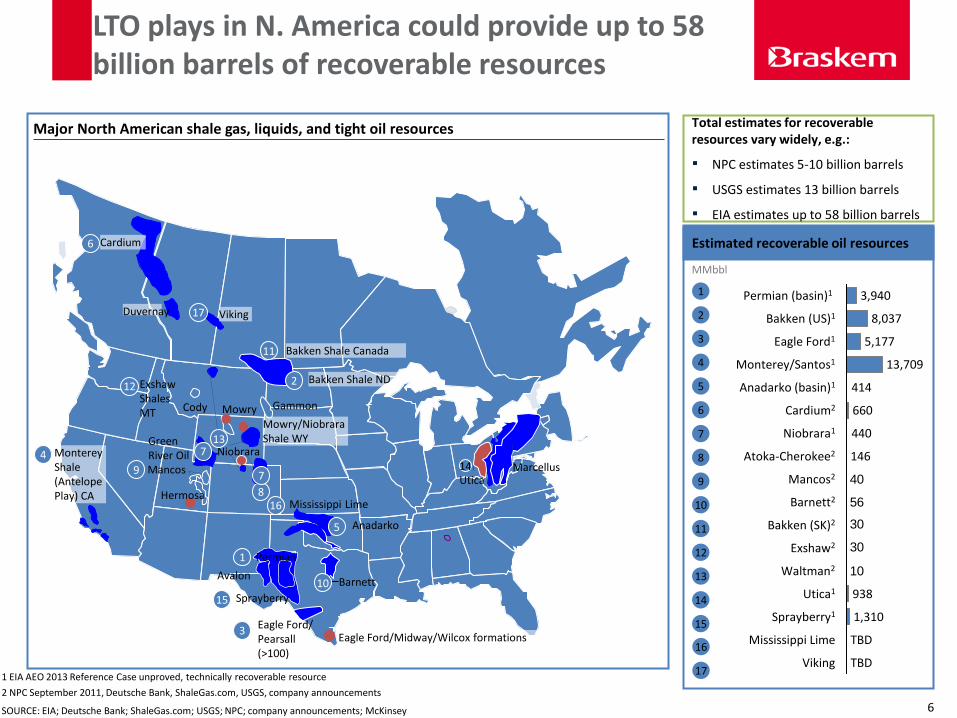

LTO plays in N. America could provide up to 58 billion barrels of recoverable resources

Major North American shale gas, liquids, and tight oil resources

16

12

11

10

9

8

7

6

5

4

3

2

1

MMbbl

13

14

15

17

Estimated recoverable oil resources

Total estimates for recoverable resources vary widely, e.g.:

▪ NPC estimates 5-10 billion barrels

▪ USGS estimates 13 billion barrels

▪ EIA estimates up to 58 billion barrels

Niobrara

Cody Mowry Gammon

Barnett

Eagle Ford/ Pearsall (>100)

Avalon

Anadarko

Mancos Utica

Monterey Shale (Antelope Play) CA

Eagle Ford/Midway/Wilcox formations 3

14

6

12 Exshaw Shales MT

11 Bakken Shale Canada

2 Bakken Shale ND

8

13

4

1

Sprayberry

Permian

5

Mississippi Lime

Mowry/Niobrara Shale WY

7

Green River Oil

Cardium

Duvernay Viking

7

10

15

16

17

Hermosa

Marcellus 9

10

30

30

56

40

8,037

Bakken (SK)2

Niobrara1

Monterey/Santos1

660

Exshaw2

Eagle Ford1 5,177

440

Atoka-Cherokee2

Bakken (US)1

Permian (basin)1

146

Cardium2

Anadarko (basin)1

Mississippi Lime

Sprayberry1

3,940

Viking

938

Waltman2

Utica1

Mancos2

13,709

Barnett2

414

1,310

TBD

TBD 1 EIA AEO 2013 Reference Case unproved, technically recoverable resource

2 NPC September 2011, Deutsche Bank, ShaleGas.com, USGS, company announcements

6

797371655932

80727066625958575450424234

968572

494637

106100

6889

575644

0

50

100

150

Bak

ken

- N

ort

her

n E

xten

sio

n

Gra

nit

e W

ash

- H

emp

hill

Gra

nit

e W

ash

- R

ob

erts

Eagl

e Fo

rd -

Wes

t O

il

Bak

ken

- S

ou

ther

n E

xten

sio

n

Cle

vela

nd

Bak

ken

- W

este

rn E

xten

sio

n

DJ

Nio

bra

ra -

EO

G

Bak

ken

- B

aile

y

Mis

s Li

me

Hz

SK B

akke

n -

Ver

y Po

or

to P

oo

r

Bak

ken

- E

ast

Nes

son

Gra

nit

e W

ash

- W

hee

ler

Bak

ken

- F

BIR

Bak

ken

- N

esso

n A

nti

clin

e

Bo

ne

Spri

ng

- Sh

elf

Slo

pe

Spra

ber

ry W

olf

ber

ry -

Bas

in C

en

Bak

ken

- E

lm C

ou

lee

SK B

akke

n -

Bila

ts

Gra

nit

e W

ash

- W

ash

ita

Eagl

e Fo

rd -

Eas

t O

il

DJ

Nio

bra

ra -

Oth

er

Spra

ber

ry W

olf

ber

ry -

W F

lan

k

Bak

ken

- S

anis

h P

arsh

all

SK B

akke

n -

Fai

r to

Go

od

Eagl

e Fo

rd -

Eas

t C

on

dy

Eagl

e Fo

rd -

Wes

t C

on

dy

PR

B N

iob

rara

- H

igh

Eagl

e Fo

rd -

Eas

t W

et G

as

Bo

ne

Spri

ng

- B

asin

Cen

ter

Eagl

e Fo

rd -

Wes

t W

et G

as

SK B

akke

n -

VG

to

Exc

elle

nt

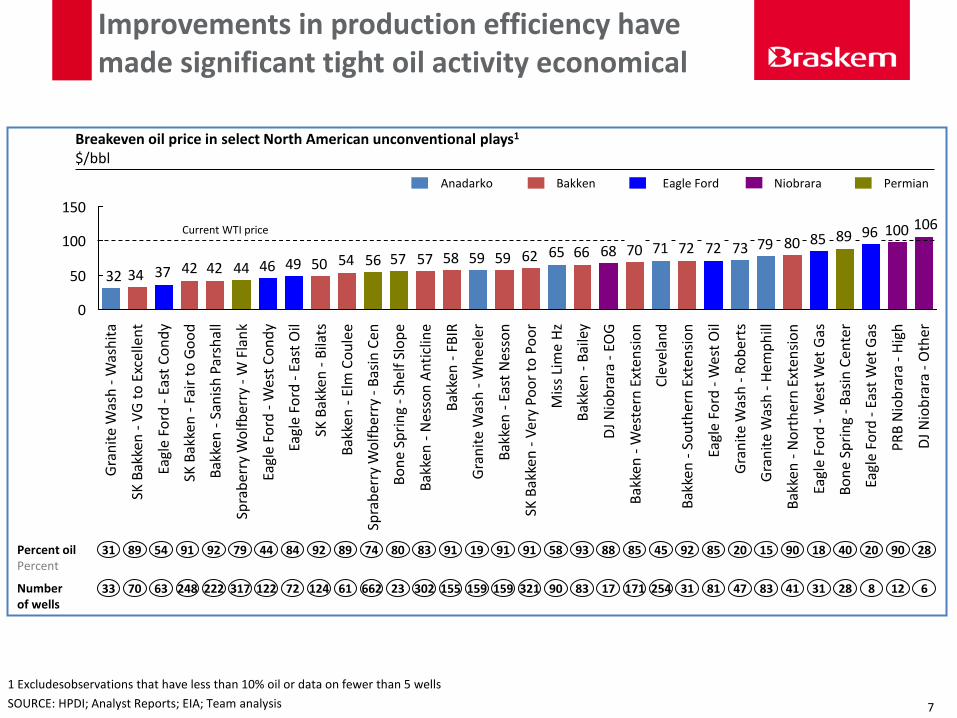

Breakeven oil price in select North American unconventional plays1

$/bbl

31 Percent oil Percent

89 54 91 92 79 44 84 92 89 74 80 83 91 19 91 91 58 93 88 85 45 92 85 20 15 90 18 40 20 90 28

33 Number of wells

70 63 248 222 317 122 72 124 61 662 23 302 155 159 159 321 90 83 17 171 254 31 81 47 83 41 31 28 8 12 6

Anadarko Bakken Eagle Ford Niobrara Permian

1 Excludesobservations that have less than 10% oil or data on fewer than 5 wells

SOURCE: HPDI; Analyst Reports; EIA; Team analysis

Current WTI price

Improvements in production efficiency have made significant tight oil activity economical

7

2020 Estimate

Wide range of estimates for LTO production in the US

Based on known projects Other

Oil production from LTO plays, Mbd

5.3

4.44.24.0

2.01.8

Energy Insights

8.9

5.6

Belfer

Center

6.6

4.2

Bentek EIA

4.7

2.2

2.8

IHS Wood-

mac

IEA Rystad

Energy

Current

SOURCE: Rystad; Belfer Center; Bentek; Bernstein Research; McKinsey; EIA AEO2013; IEA MTOMR 2013

High Case

Base Case (EI: Constant Activity)

Low Case (EI: Resource Constrained)

8

SOURCE: Energy Insights

Liquids supply1-demand2 by scenario

Mbd

Lo

ose

nin

g

Su

pp

ly

Low

economic

growth

Medium

economic

growth

High

economic

growth

Demand

Constrained

Co

ns

tra

ine

d

120

100

0

4.3

2520152010

120

100

0

5.9

202520152010

120

100

0

2.4

202520152010Made by Energy Insights. Released May

2013.

1 Global Liquids supply capacity including crude, condensates, NGLs, refinery gains, bio-fuels and spare capacity 2 Liquids demand is demand for all petroleum products and bio-fuel substitution

Loosening

Unconventionals

boom

Limited to

conventionals

▪ Supply and demand based on current trends

▪ Oil prices stabilize at $90-100/barrel

▪ Significant growth of supply in US LTO ▪ Slowing demand due to continued low

economic growth ▪ Oil price of around $60-70/barrel

▪ Steady liquids demand growth ▪ “Constrained supply” from setbacks in

unconventional and deep water basins ▪ Oil price of around $120-140/barrel

Key developments

With more uncertainty on demand and supply than before, three scenarios could materialize

Reference

Re

fere

nc

e

$90-100 /barrel

$60-70 /barrel

$120-140 /barrel

Demand2 Supply1 x Spare capacity

Long-term

trends plus

some new

sources

9

02 N. America likely to enjoy low natural gas prices in the mid-

to-long term; chemicals and energy intensive manufacturing

will benefit

Natural gas summary

Large proven reserves of natural gas from current shale gas fields in N.America

Natural gas will also be produced from Tight Oil plays

LNG exports unlikely to be significant, and even if so, not expected to be big impact on

NG pricing

Largely, agreement that long-term N. America NG prices will be at $3-5/mmbtu

Price range does not reflect good growth of LTO which has associated gas

Asia uses large amounts of fuel oil for power and heat, so gas price likely to be linked to

crude oil ($15/mmbtu range)

EU gas price will likely be below fuel oil due to ability to develop more resource, but still

in the $8/mmbtu range

Natural

Gas

11

SOURCE: EIA; Deutsche Bank; Shale Gas.com; USGS; NPC; Company announcements; McKinsey analysis

Tremendous growth of shale gas resources in N. America over past decade

L48 gas resources

Tcf

~100 years

of natural gas

available

xx Resource to production ratio (years)

54 57

583535

2012

2,688

1,072

178

228

1,210

2010

2,203

986

185

234

797

2007

1,309

963

109 202

2003

928

190

Conven-

tional

+122%

CBM

Tight

gas

Shale

gas

1,211

98 111

Major US shale gas and liquids resources

Exploration

Developing

Producing (Tcf resources)

Cody

Mowry Gammon

Excello-

Mulky

Marcellus (256)

Devonian

Chattanooga

Conasauga

Floyd-Neal Haynesville/

Bossier (251)

Woodford/

Caney

Barnett

(118)

Eagle Ford/Pearsall (>100)

Woodford (42)

Bend

Pierre Lewis

Hermosa

Mancos

Hilliard-

Baxter-

Mancos

Antrim Utica

Horn River Shale (40)

Montney (152)

Granite Wash Fayetteville (20)

New

Albany

12

SOURCE: EIA; HPDI; McKinsey analysis

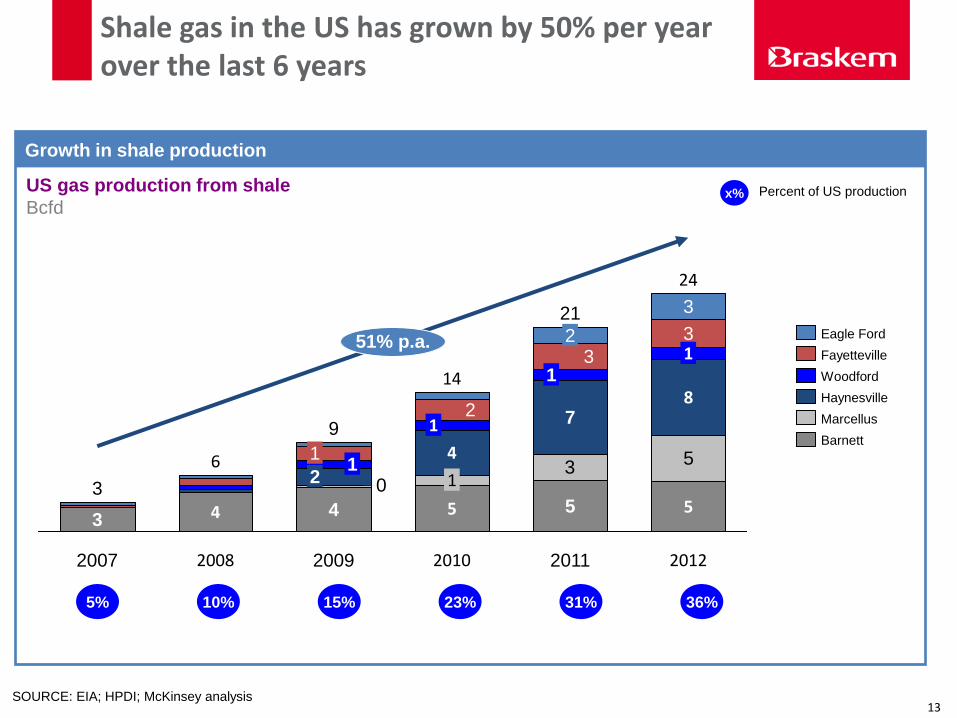

Growth in shale production

35

0

2012

24

5

8

1 3

3

2011

21

5

7

1 3

2

2010

14

51% p.a.

5

1

4

1 2

2009

9

4

2 1

1

2008

6

4

2007

3

3

Barnett

Marcellus

Haynesville

Woodford

Fayetteville

Eagle Ford

US gas production from shale

Bcfd

5% 15% 31%

x% Percent of US production

Shale gas in the US has grown by 50% per year over the last 6 years

10% 23% 36%

13

SOURCE: EIA; HPDI; McKinsey analysis

Growth in supply has led to a sharp decline in US natural gas prices – this is expected to continue

Decline in US natural gas prices

$ / MMBtu

US gas tightness Gas supply shortage leads to high prices correlated with residual fuel

Shale gas development Technology has unlocked development of previously unrecoverable or uneconomic shale gas resources in North America

0

2

4

6

8

10

12

14

16

18

20

2009 2013 2012 2011 2010 2006 2008 2007

LNG import to Japan NBP (UK) Henry Hub (US)

14

1 Excludes finding and land costs 2 Associated gas plays and predominantly oil basins excluded from this chart

SOURCE: HPDI, Woodmac, Rystad, Industry reports, EIA, McKinsey

1,000

8

200

4

2

0

1,700 1,600 1,500 800 700 600 500 900

6

400 300 100 0

16

14

12

10

1,300 1,200 1,100 1,400

Technically Recoverable resources2

Tcf

Full cost Breakeven for gas basins1 2

$/MMbtu

Conventional

CBM

Tight

Shale

Substantial resources in the $5/MMBtu range, setting a “ceiling” for US gas prices

2011 Prod. = 24 TCF

~30 yrs of resources below $4/MMbtu

40+ yrs of resources below $6/MMbtu

15

03 Low cost feedstock in N. America will impact global dynamics

of ethylene and propylene; W. Europe continues to remain at

disadvantaged position

Petrochemical summary

US ethylene-PE producers are second lowest cost producers in the world (next to the Middle East), and

can build new capacity even for export markets

The outlook of this continuing advantage has led to several announcements of expansions, debottlenecks

and new-builds of ethylene-PE capacity – current crude oil situation could temper investment outlook

Global PE prices will be set by the full cost of a new China naphtha cracker, while US and European

prices will be linked to this via netbacks

Global propylene demand growth will need to be met by on-purpose propylene – most likely routes are

PDH, metathesis, and coal/methanol routes in China

Lightening of cracker feedstock, cracker rationalilztion, accompanied by refinery utilization decrease and

potential refinery shutdowns could result in reduced propylene supply going forward

Unclear how increased propylene derivative demand in W. and C&E Europe will be met; derivative

demand in Asia and N. America will need to be met by on-purpose capacity (PDH is preferred route)

N. America on-purpose propylene could be competitive in the mid to long-term, which is causing several

regional and international players to consider investments in N. America PDH

Unlike ethylene-PE, economics favor building on-purpose propylene in each region compared to shipping

propylene or the derivatives (Europe could be the exception)

Petro-

chemicals

17

150,000

1,500

1,000

500

0

100,000 50,000 0

Global ethylene (and PE) prices are driven by marginal naphtha crackers; W. Europe at high end

SOURCE: Tecnon, ICIS, IHS, McKinsey cost curve models

Effective capacity1, kta

Demand: 131 kta

Cash cost

$/tonne

Global ethylene cost curve (plant gate) – 2012 capacities,Q4/2012 prices and cash costs2

China

Asia ex China

Middle East

Western Europe

South America

North America

Only Middle and North America have access to low-cost ethane – other regions use naphtha out of necessity

In Q4, ethane in the US finally reached it’s fuel value, demonstrating the floor on US cracker’s cash cost

Regions outside of the US and Middle East use non-subsidized naphtha and gas oil feeds, which are linked to oil prices

1 Effective capacity assumes 93% of nameplate capacity 2 Plant gate costs; based on prices in US, WE, NEA, SEA, and ME netbacks (S. America costs based primarily on US prices); each cracker’s cost based on estimated feed

mix, scale, and estimated yield efficiency estimate

18

Potential U.S. (lower 48 states) ethane supply (excluding refining)1

NGL-rich shales have driven an increase in ethane production and supply in N. America

+2 x 1000 KTA ethylene plants Current

capacity to consume

Thousand BPD

SOURCE: McKinsey North America Gas Model; government and company reports; Team analysis

If fully developed and recovered, there could be enough new ethane to support 10 million tonnes per year of new ethane capacity

▪ How will ethane supply evolve?

▪ How will ethylene cracker capacity evolve?

▪ What will be supply, demand, and price impact on ethane, ethylene, derivatives, and other cracker-derived products?

0

500

1,000

1,500

2,000

14 12 10 08 06 2004

Woodford

Barnett

Niobrara

Granite Wash

Avalon

2020 18

+85%

Current sources

Eagle Ford

Marcellus

Bakken

16

1 Estimated total supply, but likely only 85% of this will be recovered for petrochemicals as not all gas goes through processing/fractionation

19

20

30

25

35

40

19.2

Odebrecht/Braskem

Shintech Appalachia Resins

Shell

Total Petrochemicals

Williams

PTT & Marubeni

Badlands NGL

2018

1.4

Formosa

Axiall & Lotte Chemical

37.4

Speculative 9.0

Expected 3.4

2018+

8.8

ExxonMobil

Dow Chemical

Chevron Phillips

Total

Under construction

5.8

LBI

2016

0.0

Nova Chemicals

2017

7.1

Aither Chemicals OxyChem/Mexichem Sasol N.A.

2015

1.0

Braskem-Idesa

Base

Under Construction 1.0 4.8 5.8

Expected 2.0 1.4 3.4

Speculative 0.3 8.8 9.0

Total 1.0 0 7.1 1.4 8.8 18.2

North American Ethylene Capacity Additions

Million tonnes per year

N. American ethylene capacity additions

Speculative

Expected

Under construction

Base

20

0

1,000

800

600

400

200

1,200

40 30 20 10 0 40 30 20 10 0

800

600

400

200

1,200

1,000

0

40 30 20 10 0

SOURCE: McKinsey

1 Based on April 2009 prices for feeds and coproducts (except CC4 prices determined by model); outlook demand based on significant recession

Imports

Utilization XX

Domestic demand

Ethylene cost curve (plant gate, 2014, Scenario No. 2) with ethylene derivative trade flow1 USD per metric ton ethylene; million metric tons ethylene equivalents; nameplate ethylene capacities

North America Europe/FSU China

South America Middle East/Africa Non-China Asia

U.S. utilization impacted by lower exports

66% of ME production will be exported

Preference for EU vs. NCA can swing back and forth as relative costs change

93% 75% 93%

63% 93% 93%

26.6

29.4 28.5

22.2

8.0

5.8

0.9

11.9

2.0

5.9

Americas could become an island continent; ME will export primarily to Asia and Europe

21

Global propylene demand will need to be met by on-purpose propylene production

Source: IHS

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

2007 2016 2022 1995 2019 2013 2010 1992 2004 1998 2001

Demand

Global propylene supply and demand outlook million tonnes

Historically, conventional sources of propylene were sufficient to meet demand

~21 million tonnes/yr of new on-purpose capacity will be

needed from 2015 to 2024 – equivalent to 3-4 world-scale

PDH plants every year

• Chemical demand for propylene has grown at 4.5%/year since 1990 versus 3.4%/year supply growth from crackers and FCCs

• Refinery supply has been dictated and limited by gasoline demand growth

• Cracker supply has grown at low rates due to shift to lighter feedstocks in the ME and N. America

• Large amounts of on-purpose capacity will be needed to meet demand growth

• Long-term propylene pricing will most likely be set by full cost of on-purpose production – most probable outcome will be a link to PDH economics, with propane driven by crude oil and trade flow relationships

Refining Steam Crackers On-purpose

22

Change in propylene supply, demand1 2013-2024

million tonnes

China is expected to add significant propylene capacity over the next decade

North America

South America

W. Europe

Middle East

Africa

N.E. Asia

S.E. Asia

1. Domestic supply and demand only Source: IHS

China S. Korea

Demand

5.3

Supply

5.2

-0.7 -0.6

Demand Supply

Supply

0.9

Demand

0.9

Supply

0.7 0.4

Demand

Supply

6.3 6.1

Demand

Supply

3.7

Demand

4.0

26.0 26.9

Supply Demand

Demand

26.9 25.6

Supply

0.7 0.7

Demand Supply

23

Europe has seen significant shutdowns of cracker capacity; few more vulnerable assets could close

Company Country Location Age

Ethylene

Capacity (kT) Closing Probability

Included in IHS

balances

Versalis I Gela 1972 245 2008 Completed yes

Total F Carling 240 2009 Completed yes

ExxonMobil UK Fawley 120 2010 Completed yes

Shell & DEA oil D Wesseling 1973 260 2011 Completed yesSyndial I Porto Torres 250 2011 Completed yesVersalis I Priolo 295 2013 Completed yes

FAO B Antwerp 1967 230 2013 Completed yes

Versalis I Porto Marghera 490 2014 No restarted yes

Total F Carling 340 2015 Announced yes

Closed ethylene capacity 2,470 Vunerable assets

Dow NL Terneuzen 1970 535 no

Repsol Sp Sines 250 no

Potential closures 785

Cracker closures (completed and expected)

24 Source: Company announcements

Similarly, there has been refinery capacity rationalization in Europe as well

Source: Argus DeWitt 2014 25

Rationalization could continue in Europe over the next decade

Source: Presentation by Total at Platts European Refining Summit, Sept 2014 26

Perfect storm of events will drive reduction of propylene supply in W. Europe...

27

• Potential rationalization of old/sub-scale crackers in Europe

• Increasing use of propane, replacing naphtha • Investments to use ethane to replace heavier feeds

-900 -1,000 Cracker production of propylene

Source: Braskem analysis

Drivers of change Propylene source Change in C3 supply 2013-2024 kT

• Declining fuel demand in Europe • Increased use of diesel, and decrease of gasoline • Old/small refineries not competitive with fuel imports • Up to 2 million bbl/day of refinery capacity at risk of

closure

-800 -165 Refinery production of propylene

35 On-purpose production of propylene

• Propylene production expected to decrease by 8-13% from current levels • Closure of derivative units to same extent unlikely– large-scale imports of propylene to feed derivative units

are unlikely • As a result, we expect larger imports of derivatives in the mid to long-term

• Two small PDH units operational in W. Europe could see utilization increase

27

…however, other than PP, propylene demand for derivatives production not expected to reduce

1.8

8.0

Propylene Oxide

1.1

0.8

2.2

1.0

7.2

2.0

14.5

0.9

0.7

2.1

13.9

0.8

Polypropylene

2013 2024

Cumene

Other

Acrylic Acid

Acrylonitrile

W. Europe propylene demand 2013-2024

million tonnes

Source: IHS 28

N. America on-purpose propylene expected to be lowest cost supply in the world

29 SOURCE: Braskem Analysis; McKinsey Margin Models; CMAI

Propylene production cost and price1 $/tonne

1,300

1,200

1,100

900

700

+600

NE Asia PDH NE Asia Naphtha W. Europe Naphtha Middle East PDH N. America PDH

1 Estimates based on 2012 costs and prices

29

Potential for additional PDH builds in US

Source: Company announcements

PDH expected capacity KTA

660

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2019

3,072

2018

2,424

2020

3,186

2017

2,157

2016

1,783

2015

1,034

2014

Speculative Dow

Enterprise Existing - Petrologistics / Flint Hills Resources

3 companies have announced their interest in building a PDH: 1. Ascend 2. Williams 3. Formosa

30

Summary

Uncertainties in global energy markets likely to continue

Impact of how energy market evolves could be significant for petrochemicals

Rush for new investments in ME, China and US showing signs of slow down given uncertainty in crude oil markets

European disadvantage in petrochemicals likely to continue, however, survivors

31

Thank you!