Page 1

LondonHouston

SingaporeMoscow

DubaiNew York

CalgarySantiago

Rio de JaneiroBeijing

ShanghaiTokyo

SydneyAstana

KievCape Town

RigaSan Francisco

Washington

Market Reporting

ConsultingEvents

Trends and Opportunities in Specialty FertilizerNew Orleans

Blake Hurtik & Lauren WilliamsonNovember 2017 for TFI Outlook

Page 2

• One of the world’s leading PRAs, Argus is a team of more than 900 staff members in 20 global offices

• Publishing more than 11,000 daily spot and forward price assessments, plus market intelligence for world commodities markets

• Coverage includes:◦ Energy◦ Fertilizers◦ Petrochemicals◦ Metals

• Services◦ Price reporting and indexation◦ Consulting◦ Conferences

• Indexation examples◦ US crude oil◦ US and European refined products ◦ US and European natural gas◦ NGLs◦ US and European environmental markets

The Argus view

Copyright © 2017 Argus Media group. All rights reserved.

Page 3

Micronutrients Forum on 22 January ‐ Delegates will benefit from all the agronomic and commercial insight needed to leverage their position in this growing market.A dedicated track of presentations focused on Innovation and R&D ‐ Examine developments in soil analysis, crop requirements and new fertilizer blends to meet regional demand

Page 4

Copyright © 2017 Argus Media group. All rights reserved.

Other

Water Soluble

Enhanced Efficiency

Technical Grades

Blends, Secondary, Micro

Bulk N, P, K

Topics covered

• Drivers• Enhanced Efficiency• Specialty Blends• Company Case Studies • Future

Low volume, high margin

High volume, low margin

Page 5

Copyright © 2017 Argus Media group. All rights reserved.

Drivers: Resource management, ag profitability, population

Subsidy control

RegulationGHG concerns

Algal BloomsHuman nutritionYield increase

Water scarcity

Irrigated Fields

Unpredictable Weather

BMPs , 4R, new laws

Population growth

Manage costs

Page 6

Copyright © 2017 Argus Media group. All rights reserved.

N Nutrient Uptake Efficiency Routes

Controlled Release (CRF)

Coated with physical barrier to prolong

breakdown

Polymer, resins, hydrogels, wax

Sulfur, other mineral based coatings

Stabilized Nitrogen Fertilizer (SNF)

Impregnated granule or surface coated to delay nitrification, volatilization

Urease inhibitors reduce volatilization, N loss to

NH3

NBPT, 2‐NPT, NPPT, PPD, triazone,

Nitrification inhibitors delay bacterial action of converting to nitrate N, N

loss to leaching

DCD, DMPP, nitrapyrin, ATS

Slow Release Nitrogen (SRN)

Chemical chain lengthened to slow

release

UF, IBDU, MU, CDU

Enhanced efficiency N

N loss is commonly~30% to leaching

and ~10% to nitrification

Page 7

Copyright © 2017 Argus Media group. All rights reserved.

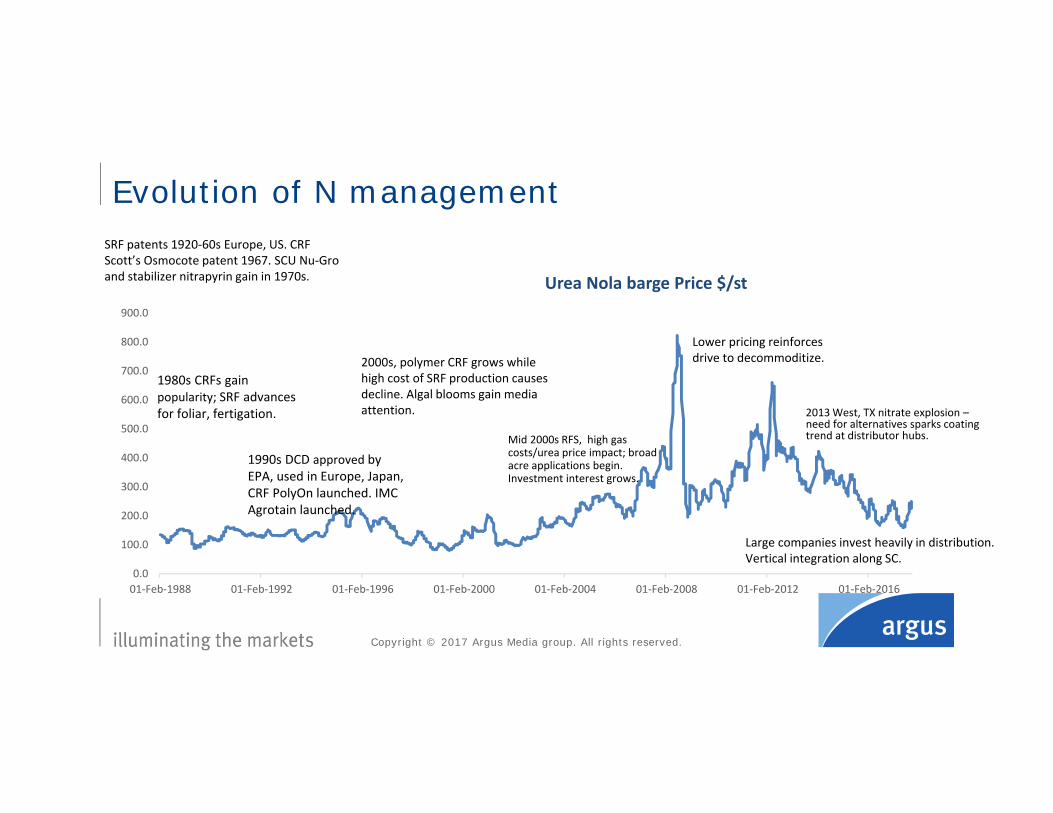

Evolution of N management

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

01‐Feb‐1988 01‐Feb‐1992 01‐Feb‐1996 01‐Feb‐2000 01‐Feb‐2004 01‐Feb‐2008 01‐Feb‐2012 01‐Feb‐2016

Urea Nola barge Price $/st

2000s, polymer CRF grows while high cost of SRF production causes decline. Algal blooms gain media attention.

SRF patents 1920‐60s Europe, US. CRF Scott’s Osmocote patent 1967. SCU Nu‐Groand stabilizer nitrapyrin gain in 1970s.

1980s CRFs gain popularity; SRF advances for foliar, fertigation.

1990s DCD approved by EPA, used in Europe, Japan, CRF PolyOn launched. IMC Agrotain launched.

Mid 2000s RFS, high gas costs/urea price impact; broad acre applications begin. Investment interest grows.

2013 West, TX nitrate explosion –need for alternatives sparks coating trend at distributor hubs.

Lower pricing reinforces drive to decommoditize.

Large companies invest heavily in distribution. Vertical integration along SC.

Page 8

Copyright © 2017 Argus Media group. All rights reserved.

Huge growth in 15 years, but adoption tied to logistics

0

1

2

3

4

5

6

7

8

2000 2016

Global Demand estimates in mn t

SNF CRF SRN

15

60

0

10

20

30

40

50

60

70

80

90

100

2000 2016

Demand (%) by Sector

Professional Consumer General Ag

Strong crop profitability= drive for increased yield

Low crop profitability = drive for cost reductions

Page 9

Copyright © 2017 Argus Media group. All rights reserved.

• N savings must be higher than the price premium for the product

• In Europe, take $/unit N value of nitrate and capture difference to $/unit N value of urea

• Freight from production point for homogenized products can distort and fragment pricing

• Time lag with underlying commodity price movements creates exposure

• Huge variations in contracts, price formulas, particularly between specialty crops vs cash crops

Pricing challenges for heterogeneous products

0

2

4

6

8

10

12

2013 2014 2015 2016 2017

Theoretical Interior US Distribution Hub Pricing

Urea $/unitAN $/unitSurface coat inhibitorStabilizedPCU

Page 10

Copyright © 2017 Argus Media group. All rights reserved.

A busy decade of investment - PE’s next goal?Year Year

Agrium buys Pursell tech $75mn 2006 Hanfeng Evergreen sells plants on financial difficulties

2014

Chisso, Asahi, Mitsubishi form JCAM (invest new PCF Taiwan plant 2016)

2009 Koch buys Agrium Advanced Tech; (Yara buys Brazil distributor Galvani stake)

2014

Koch buys Agrotain $94mn (and buys UK dist Bunn, incorporates MU from GP)

2011 Koch licenses N‐tegration technologyYara buys Agrium USWC upgrade facilities

2015

K+S sells Compo (est 1956) to PE 2011 Solvay partners with EcoAgro (est 2014) 2015

Gavilon exclusive distributor Arborite in US, Mexico 2011 Kingenta buys Ekompany (est 2010) and portion of Compo – other division sold to PE

2016

ICL buys division of Scotts $270mn 2011 Stamicarbon invests $6mn in Pursell Agri Tech 2017

EuroChem buys BASF Entec technology (also buys US dist BenTrei in 2015 and Brazil Tocantins 2016)

2012 Yara invests in UAS production in Sliuskill 2017

PE firm establishes Verdesian Life Sciences (also acquires Specialty Fert Products 2015)

2012 Koch Enid Super U expansion 2017

Page 11

Copyright © 2017 Argus Media group. All rights reserved.

Product life cycle – first mover advantage?

R&D Growth Maturity

Profits

Decline

Fend off competitors in growth phase with legal action to protect patents.

Exploit cost efficiencies. Differentiation via integrated solutions, service models and branding.

Extend maturing phase with new patents, renewals.

Manage PLC toward generics via licensing.

Expanding market share begins to commoditize the product.

Page 12

Copyright © 2017 Argus Media group. All rights reserved.

Opportunities: vary depending on market position

TECH COMPANIESlicense to

manufacturers or retailers

PROOF OF CONCEPTUniversity studies,

government legitimization via regulation and BMP

certification

RETAIL/DISTRIBUTIONpartners to facilitate supply chain control,

direct sales

BRAND AND PACKAGING

for local brands + niche markets

WHOLESALE PARTNERS

for bin space (if substituting bulk

product)

EQUIPMENT SALES

at distributor /retail level. Rapid “DEMAND THEN DEPLOY” model.

TECH SALES TEAMrequired to convince partners, especially further down chain

TRADITIONAL MANUFACTURER create/acquire tech, license out,

form JVs

ADDITIVE PRODUCERS sell direct to distributors, retailers

Heavy marketing & branding required

“INTEGRATED SERVICE MODEL” with tech tools

tools to incentivize

CONTAINER EXPORTS

bulk exports with liquid additives

Page 13

Copyright © 2017 Argus Media group. All rights reserved.

Limitations: US farmer profitability improving but still low

$0

$1

$2

$3

$4

$5

$6

$7

$8

$0

$20

$40

$60

$80

$100

$120

$140

$160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net farm income Nat cash farm income Avg farm corn price, right

$/bushelbillions

Page 14

Copyright © 2017 Argus Media group. All rights reserved.

Micronutrients not immune to macro pricing

150

200

250

300

350

400

450

500

550

600

Jul-

12

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-

13

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep

-15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-

16

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-

17

Sep

-17

Granular urea fob Nola DAP fob Nola MOP fob Nola

$/st

Page 15

Copyright © 2017 Argus Media group. All rights reserved.

• Key micronutrients◦ Sulfur◦ Magnesium◦ Zinc◦ Boron◦ Manganese◦ Copper◦ Iron◦ Calcium

Micronutrient and secondary demand

-

1

2

3

4

5

6

7

8

9

mn

shor

t to

ns

‐ USDA,

Page 16

Copyright © 2017 Argus Media group. All rights reserved.

So what do specialty blends look like?

Page 17

Copyright © 2017 Argus Media group. All rights reserved.

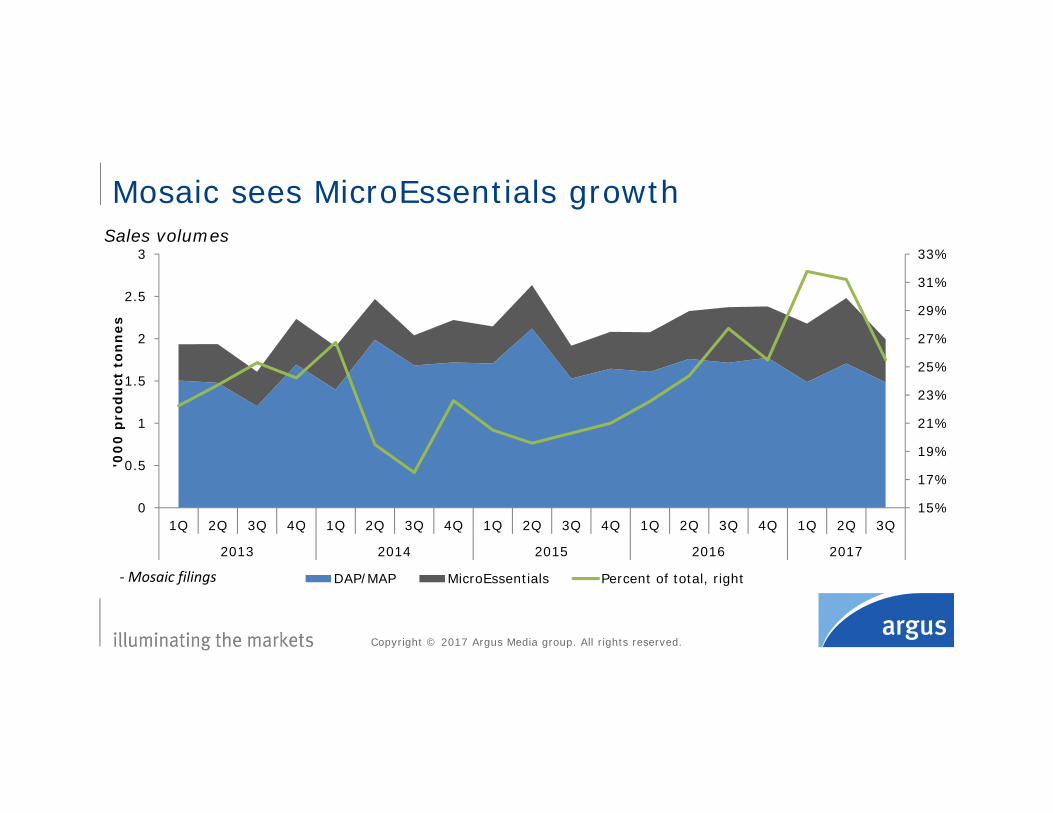

• Mosaic introduces MicroEssentials, expands capacity by 1.2mn t/yr to 3.5mn t/yr — 30pc of total capacity

• Morocco’s OCP offers range of enhanced phosphates targeting African market◦ Licenses Shell Thiogro technology to add sulfur to finished

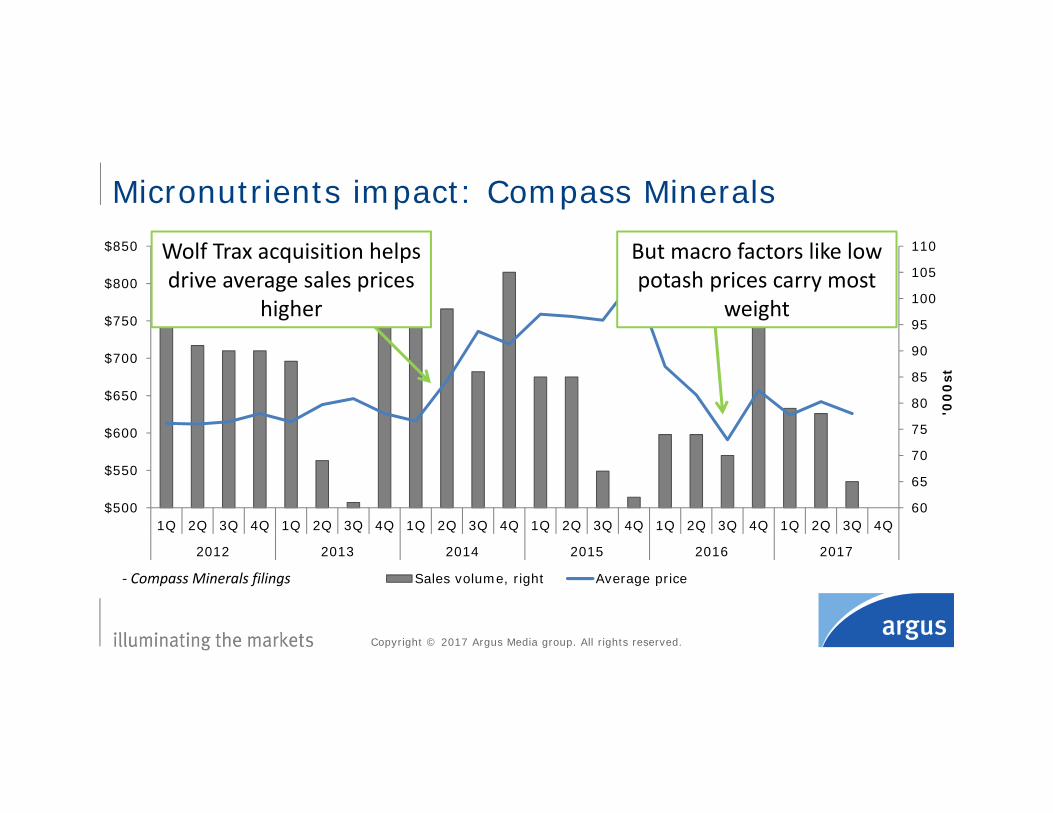

phosphates• Compass Minerals buys Wolf Trax in 2014• ICL converts UK potash mine to focus on polyhalite; Sirius

Minerals begins construction of 10mn t/yr polyhalite mine in UK

Majors go micro

Page 18

Copyright © 2017 Argus Media group. All rights reserved.

Mosaic sees MicroEssentials growth

15%

17%

19%

21%

23%

25%

27%

29%

31%

33%

0

0.5

1

1.5

2

2.5

3

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2013 2014 2015 2016 2017

'00

0 p

rod

uct

ton

nes

DAP/MAP MicroEssentials Percent of total, right

Sales volumes

‐ Mosaic filings

Page 19

Copyright © 2017 Argus Media group. All rights reserved.

Micronutrients impact: Compass Minerals

60

65

70

75

80

85

90

95

100

105

110

$500

$550

$600

$650

$700

$750

$800

$850

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2012 2013 2014 2015 2016 2017

'00

0st

Sales volume, right Average price‐ Compass Minerals filings

Wolf Trax acquisition helps drive average sales prices

higher

But macro factors like low potash prices carry most

weight

Page 20

Copyright © 2017 Argus Media group. All rights reserved.

The risk of commodification: Intrepid Potash

$150

$200

$250

$300

$350

$400

$450

$500

0

50

100

150

200

250

300

350

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2012 2013 2014 2015 2016 2017

Pro

du

ctio

n '0

00

st

MOP Trio MOP sales price, right Trio sales price, right‐ Intrepid filings

Page 21

Copyright © 2017 Argus Media group. All rights reserved.

Key takeaways

Next trends?

Fertigation, WSFs, adjuvant/surfactant

improvements

P management espin foliar, solubles

“Core” technology

Seed inoculation –rhizobia researchBiostimulants

Biofertilizer (but interaction with finished blends)

Nanotechnology

• Drivers supporting specialty products to remain constant for the foreseeable future

• Limitations tie to traditional agricultural risks and fundamentals

•• Different companies have made

different market entries, with mixed results

• More specialties in the mainstream now leave room for the next wave of niche products – but adoption takes time, proof of concept key

Page 22

LondonHoustonSingaporeMoscowDubaiNew YorkCalgarySantiagoRio de JaneiroBeijingShanghaiTokyoSydneyAstanaKievCape TownRigaSan FranciscoWashington

Page 23

Stay Connected

@ArgusMedia Argus-media

+Argusmediaplus argusmediavideo

Copyright notice Copyright © 2017 Argus Media group. All rights reserved. All intellectual property rights in this presentation and the information herein are the exclusive property of Argus and and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, by reading this presentation you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus.

Trademark notice ARGUS, the ARGUS logo, ARGUS MEDIA, ARGUS DIRECT, ARGUS OPEN MARKETS, AOM, FMB, DEWITT, JIM JORDAN & ASSOCIATES, JJ&A, FUNDALYTICS, METAL-PAGES, METALPRICES.COM, Argus publication titles and Argus index names are trademarks of Argus Media group.

Disclaimer All data and other information presented (the “Data”) are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, adequacy, timeliness, or completeness of the Data or fitness for any particular purpose. Argus shall not be liable for any loss or damage arising from any party’s reliance on the Data and disclaims any and all liability related to or arising out of use of the Data to the full extent permissible by law.

Blake Hurtik, editor North American FertilizerLauren Williamson, SVP Fertilizer

Email:Phone:Office:Web:

[email protected] +1 713-968-0000Londonwww.argusmedia.com/fertilizer/

![[01] Feb 2015 - Church & Village Newsletter](https://static.documents.pub/doc/80x56/568caabd1a28ab186da2c531/01-feb-2015-church-village-newsletter.jpg)