Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org Carolyn April, Sr. Director, Industry Analysis CompTIA June 2016 Trends in Managed Services: The Art & Science of the MSP Business Carolyn April Sr. Director, Industry Analysis CompTIA

Transcript

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

Carolyn April, Sr. Director, Industry Analysis

CompTIA

June 2016

Trends in Managed Services: The Art & Science of the MSP Business

Carolyn AprilSr. Director, Industry AnalysisCompTIA

On Tap Today

Why Managed Services?

Internal Operations

Strategic Planning

Wrap Up & Q&A

2

65%

33%

2% By the numbers…

• 77% of the smallest

channel firms (2-9 employees) described themselves as “skilled experts” at managed services, compared to roughly 6 in 10 respondents from larger firms.

Self-Assessment of Managed Services Capabilities Today

Early On/Too Soon to Tell

Skilled Expert

Competent/Getting Better

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

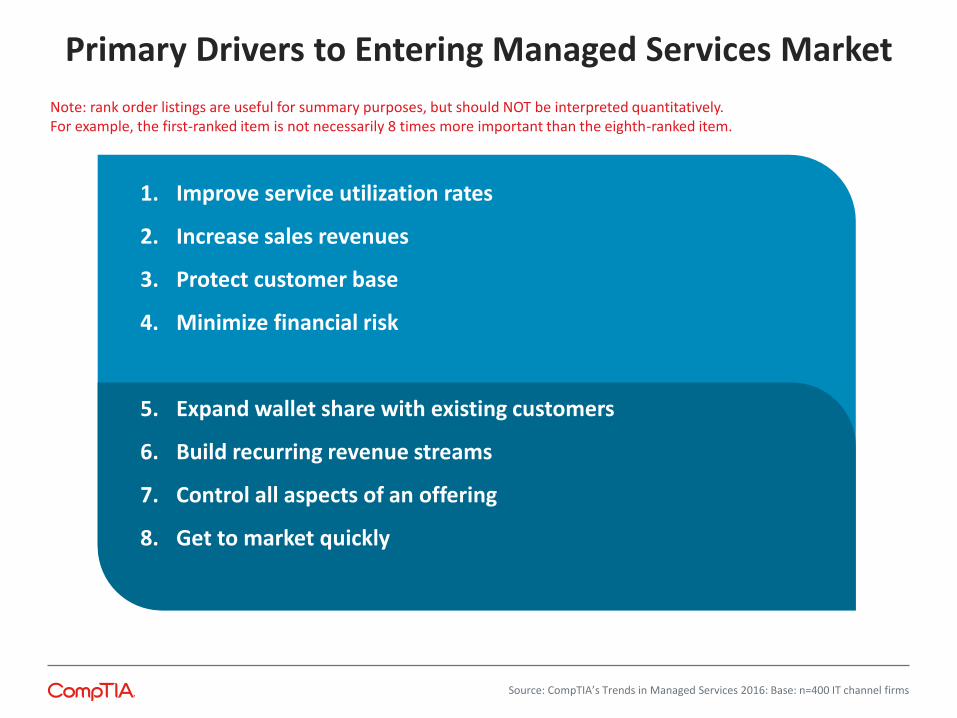

Primary Drivers to Entering Managed Services Market

1. Improve service utilization rates

2. Increase sales revenues

3. Protect customer base

4. Minimize financial risk

5. Expand wallet share with existing customers

6. Build recurring revenue streams

7. Control all aspects of an offering

8. Get to market quickly

Note: rank order listings are useful for summary purposes, but should NOT be interpreted quantitatively. For example, the first-ranked item is not necessarily 8 times more important than the eighth-ranked item.

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

Channel Business Lines: Which Two Drive Most Revenue?

IT Solutions/Projects

44% rank this LOB as

top revenue generator. 12% rank it No. 2

Managed Services

29% rank this LOB

as top revenue generator. 21%

rank it No. 2

Top LOB by company size:• Small firms: 31% • Medium firms: 25% • Large firms: 34%

Top LOB by company size• Small firms: 31% • Medium firms: 43% • Large firms: 61%

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

Expectations for Managed Services Business Next Two Years

4%

36%

61%

1%

52%

47%

4%

44%

52%

Flat growth: Remains at currentlevels

Medium growth: Comprisingincreasing part of revenue (50% or

more)

High growth: Comprising majority ofrevenue (75% or more)

Large

Medium

Small

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

Small firms Medium firms

Large firms

Product sales( hardware, software,peripherals)

31% 20% 36%

One-off project-centric work 39% 39% 14%

Pure consulting services 18% 27% 26%

Other (e.g. referrals, extended warranties, etc.

1% 3% 3%

Other areas remain status quo 3% 5% 8%

All of the above 7% 5% 13%

Which Revenue Lines Decline as Managed Services Grows?

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

Managed Services’ Portfolios Cut Wide Swath

Managed Services Currently Offer

Plan to Offer

Security (firewall management)

74% 24%

Server management 74% 24%

Storage 72% 27%

Network management/monitor

71% 28%

Desktop management 70% 28%

Business continuity/DR 70% 28%

Backup as a service 69% 28%

Software management (patch) 69% 29%

Database management 68% 30%

Help desk 67% 31%

Email 67% 29%

Virtual desktop 66% 30%

Managed print services 65% 32%

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

28%

59%

3%

10%

Increase overall

Staysame

Mix bagDecrease overall

Services mix in the next year will…

MSP Approach to Offering Cloud-based Services

54%

44%

3%

Strategic part of MSPcatalog

Supported at customers'request

Not part of MSP catalog

Source: CompTIA’s Trends in Managed Services 2016: Base: n=400 IT channel firms

Internal Operations

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

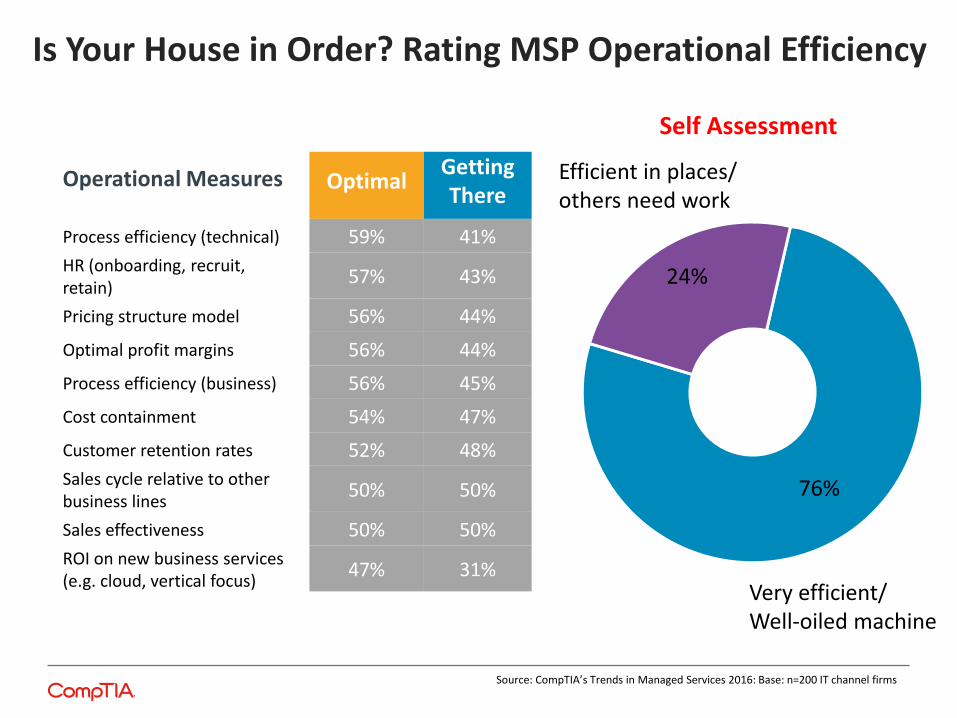

Is Your House in Order? Rating MSP Operational Efficiency

Operational Measures OptimalGetting There

Process efficiency (technical) 59% 41%

HR (onboarding, recruit, retain)

57% 43%

Pricing structure model 56% 44%

Optimal profit margins 56% 44%

Process efficiency (business) 56% 45%

Cost containment 54% 47%

Customer retention rates 52% 48%

Sales cycle relative to other business lines

50% 50%

Sales effectiveness 50% 50%

ROI on new business services (e.g. cloud, vertical focus)

47% 31%

Source: CompTIA’s Trends in Managed Services 2016: Base: n=200 IT channel firms

76%

24%

Efficient in places/others need work

Very efficient/Well-oiled machine

Self Assessment

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

NoChallenge

Minor Challenge

MajorChallenge

Cost of retraining (technical) 11% 39% 45%

Restructuring sales comp models 11% 47% 42%

Cost of retraining (business) 17% 43% 40%

Automating IT functions 14% 46% 40%

Setting pricing structure 15% 46% 40%

Recruiting/hiring right talent 13% 48% 38%

Operational Challenges in Adopting Managed Services

Source: CompTIA’s Trends in Managed Services 2016: Base: n=200 IT channel firms

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

24%26% 23%

13% 10%

Per device Per user Based on userconsumption

Fixed, recurringfee

Fixed, recurringfee for standard

services

MSP Pricing: The Ongoing Enigma

Source: CompTIA’s Trends in Managed Services 2016: Base: n=200 IT channel firms

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

Employee Retention Remains a Challenge for MSPs

17%

47%

37%

8%

51%

41%

23%

48%

29%

Not a challenge

Minor challenge

Major challenge

Large MSPs

Medium MSPs

Small MSPs

Source: CompTIA’s Trends in Managed Services 2016: Base: n=200 IT channel firms

Leaving the Fold?

80% of MSP

respondents report that at least one of their staff technicians resigned last year to join an end-user organization’s IT department.

Copyright (c) 2014 CompTIA Properties, LLC. All Rights Reserved. | CompTIA.org

Initial Steps Taken to Launch an MSP Practice

27%

38%

48%

49%

49%

53%

56%

63%

Invested in commercial softwareapplications

Retrained technical staff

Obtained credit/access to capital

Restructured sales comp model

Contracted with third-party NOC

Retrained existing sales reps

Invested in building a NOC

Hired new sales reps with MSP experience

Source: CompTIA’s Trends in Managed Services 2016: Base: n=200 IT channel firms

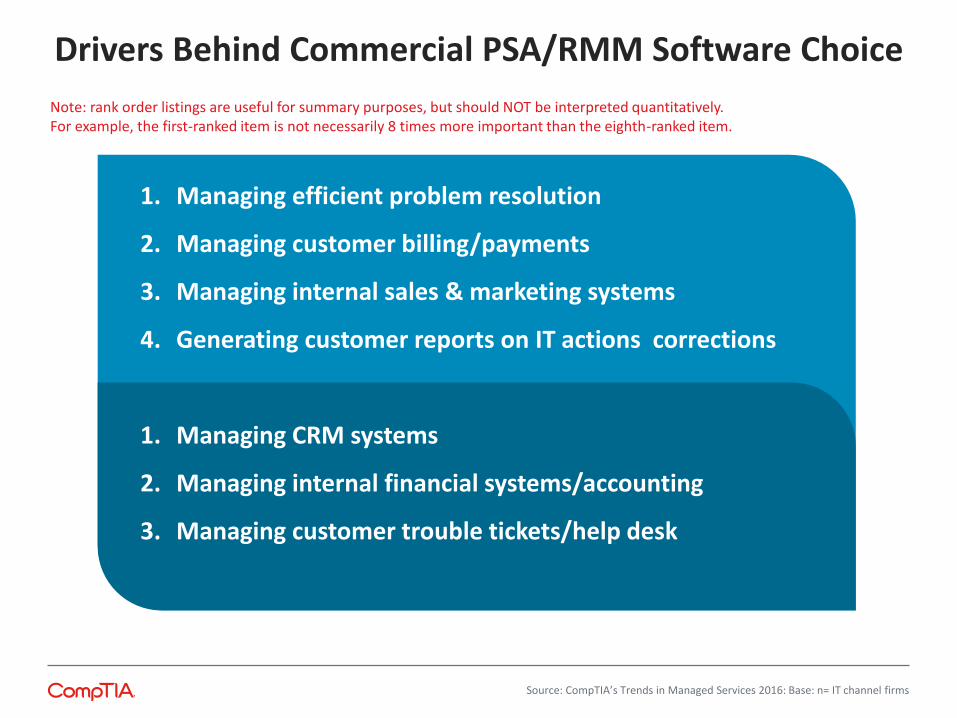

Drivers Behind Commercial PSA/RMM Software Choice

1. Managing efficient problem resolution

2. Managing customer billing/payments

3. Managing internal sales & marketing systems

4. Generating customer reports on IT actions corrections

1. Managing CRM systems

2. Managing internal financial systems/accounting

3. Managing customer trouble tickets/help desk

Note: rank order listings are useful for summary purposes, but should NOT be interpreted quantitatively. For example, the first-ranked item is not necessarily 8 times more important than the eighth-ranked item.

Source: CompTIA’s Trends in Managed Services 2016: Base: n= IT channel firms