“Pick Stocks, Not Markets” The Importance of Bottom-Up Investing in Emerging Markets Goldman Sachs Asset Management Brussels, March 9 th , 2016 FOR PROFESSIONAL INVESTORS USE ONLY. NOT FOR DISTRIBUTION TO GENERAL PUBLIC Trends & Morningstar Investment Summit 2016

Transcript

“Pick Stocks, Not Markets”

The Importance of Bottom-Up Investing in Emerging Markets

Goldman Sachs Asset Management

Brussels, March 9th, 2016

FOR PROFESSIONAL INVESTORS USE ONLY. NOT FOR DISTRIBUTION TO GENERAL PUBLIC

Trends & Morningstar Investment Summit 2016

2

Executive Summary

Source: GSAM, as of Mar-2016

We believe

Inefficiency at the stock level in EM creates tremendous alpha

opportunity

Outsized returns are generated by investing in sound businesses at

substantial discounts to intrinsic value

II

III

Challenges related to growth, divergence and index composition have

created uncertainty for investors I

The recent challenge for EM investors

4

A declining growth premium has challenged investor

perception of Emerging Markets

Source: IMF, World Economic Outlook Database, Oct-15.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

Downward growth trend disguises increased divergence in

growth cycles post-crisis

Source: Goldman Sachs, as of Oct-15.Countries shown represent the five largest emerging market economies, by nominal GDP.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

Please see additional disclosures.

0

3

6

9

12

15

2002 2003 2004 2005 2006 2007

Rea

l GD

P G

row

th (

yoy

- %

)

Brazil China India Russia South Korea Average

-5

0

5

10

15

2010 2011 2012 2013 2014 2015

Rea

l GD

P G

row

th (

yoy

- %

)

Pre-crisis – more homogenous growth patterns Post crisis – greater divergence in growth

6

Dominance of SOEs and ‘success stories of the 2000s’ in

traditional EM benchmarks has created additional uncertainty

1 Source: Datastream, MSCI, UBS Estimates. Data as of 30 September 2014. 2 Source: Datastream , MSCI, GSAM calculations. Data shown for respective MSCI indices, as of Oct-15.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

Please see additional disclosures.

SOE % of country market cap1 Trailing 12m earnings growth2

0

100

200

300

400

500

600

2003 2005 2007 2009 2011 2013 2015

Tra

iling 1

2m

earn

ings –

Index,

100=

Mar-

03

Energy Materials EM

How should investors approach the EM opportunity?

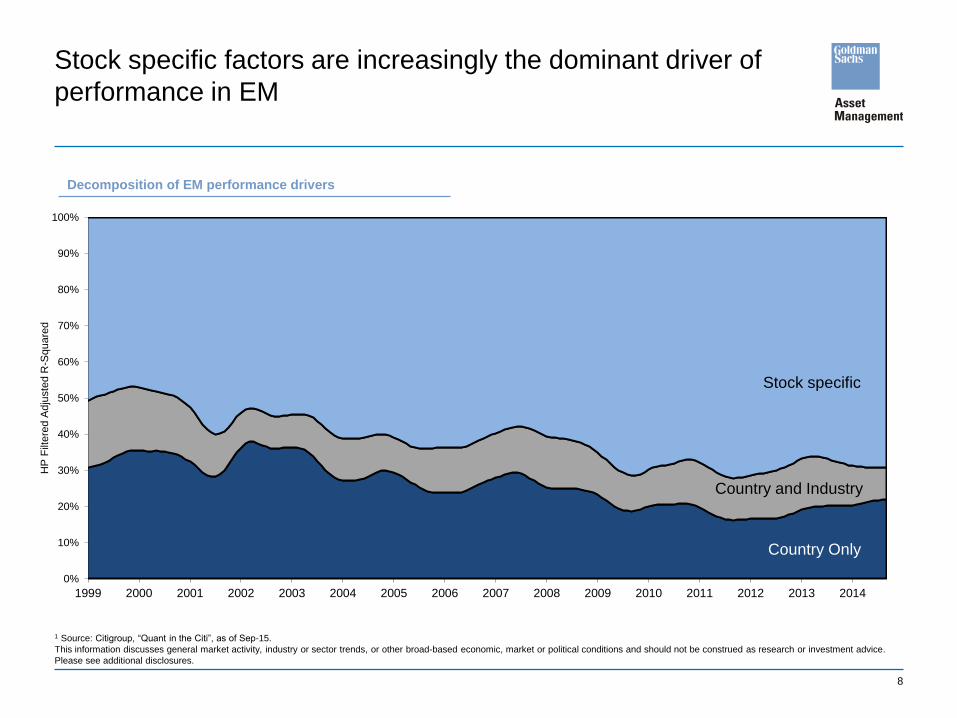

8

Stock specific factors are increasingly the dominant driver of

performance in EM

1 Source: Citigroup, “Quant in the Citi”, as of Sep-15.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

Inefficiency at the stock level in EM creates tremendous alpha

opportunity

1 Source: Goldman Sachs Portfolio Strategy Research, “The EM flow outlook for H2 2013”, 04-Aug-2013. 2 Source: GSAM. For informational purposes only.

Past performance does not guarantee future results, which may vary.

Dispersion in stock level returns1

90th percentile vs 10th percentile

22%

41%

63%

100%

155%

10%

19%

30%

45%

65%

0%

20%

40%

60%

80%

100%

120%

140%

160%

1 month 3 month 6 month 12 month 24 month

Sto

ck r

etu

rn d

isp

ers

ion

(9

0th

vs 1

0th

pe

rce

ntile

)

Emerging Markets

Developed Markets

Funnel of opportunity2 Small and mid cap space can offer attractive upside

Our approach: “Pick companies, not countries”

11

Outsized returns are earned over time by investing in sound

businesses at substantial discount to intrinsic value

Source: GSAM. For illustrative purposes only

Industry

Business

Management

What We Evaluate

Business

Value Flow Analysis

Discounted Cash Flow

Sum of Parts

Relative Valuation

Valuation Approach

Valuation

12

Attributes influencing portfolio exposure: Importance of

sustainability of returns

As of Dec-15. Source: FactSet. Portfolio holdings may not be representative of current or future investments. The securities discussed may not represent all of the portfolio's holdings and may represent only

a small percentage of the portfolio holdings. Future portfolio holdings may not be profitable. For illustrative purposes only. There can be no assurance that the same or similar results to those presented

above can or will be achieved.

People, Philosophy, Process and Portfolio Construction

Exchanges Telecoms

Environment

Largely monopolistic businesses insulated from competitive

pressures

Capital light businesses; cash conversion close to 100%

Intense competition, multiple players

Environment heavily influenced by regulation

Implications

Sustainable return over time

Invest in largely underdeveloped capital markets that should

expand over time

Regulatory uncertainty

Competition has led to low pricing power and less sustainable

returns

Outcome Higher structural allocation to exchanges Lower structural allocation to telecoms

Case study: Exchanges and Telecoms

11.4%

0.2% 0.2%

6.7%

0%

2%

4%

6%

8%

10%

12%

Weig

ht

Portfolio MSCI EM

13

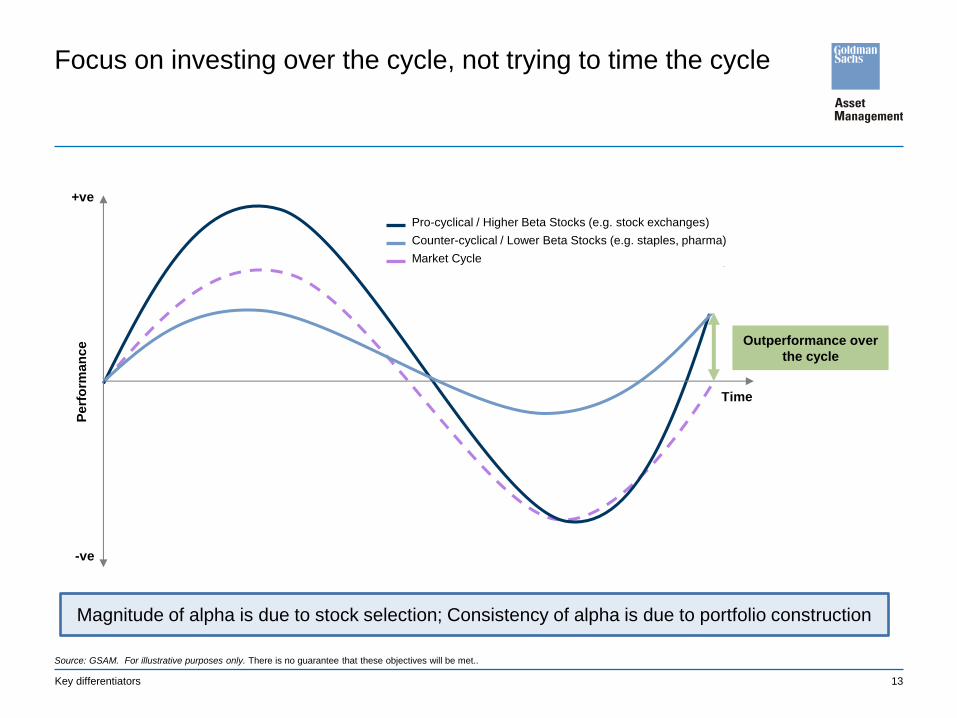

Focus on investing over the cycle, not trying to time the cycle

Source: GSAM. For illustrative purposes only. There is no guarantee that these objectives will be met..

Magnitude of alpha is due to stock selection; Consistency of alpha is due to portfolio construction

14

We believe a balanced, bottom-up driven portfolio can lead to

consistent alpha irrespective of market environment

1 As of Dec-15. Shown since restructure (01-Jul-13). Returns are shown for the institutional accumulation share class, net of fees. 2 As of Dec-15. Shown since restructure (01-Jul-13) Returns are shown for the institutional accumulation

share class, net of fees. Both shown since 01-Jul-2013 when Prashant Khemka was asked to become CIO of Emerging Markets Equity. Past performance does not guarantee future results, which may vary. The performance data

does not take account of the commissions and costs incurred on the issue and redemption of units.

Key differentiators

Case study: Alpha generation over the cycle2

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Jun-13 Dec-13 Jun-14 Dec-14 Jun-15 Dec-15

Portfolio Cumulative Excess Return (net, %)

MSCI EM Cumulative Return (%)

Average Quarterly Performance in Different Market Environments1

Up Markets Overall Down Markets

Outperformed 10 out

of 10 quarters

Average Alpha: +199

bps

Outperformed 6 out of

6 up quarters

Average Alpha: +257

bps

Outperformed 4 out of

4 down quarters

Average Alpha: +112

bps

5.5%

1.1%

-5.5%

3.0%

-0.9%

-6.6%

Portfolio Quarterly Average Return (net)

MSCI EM Quarterly Average Return

15

GSAM Emerging Markets fund performance overview As of 31-Jan-16

As of Jan-16. Returns are shown for the institutional accumulation share class, net of fees. Past performance does not guarantee future results, which may vary. The performance data does not take

account of the commissions and costs incurred on the issue and redemption of units. For illustrative purposes only. There can be no assurance that the same or similar results to those presented

above can or will be achieved.

Institutional share class, net of fees 1 Year 3 Years 5 Years

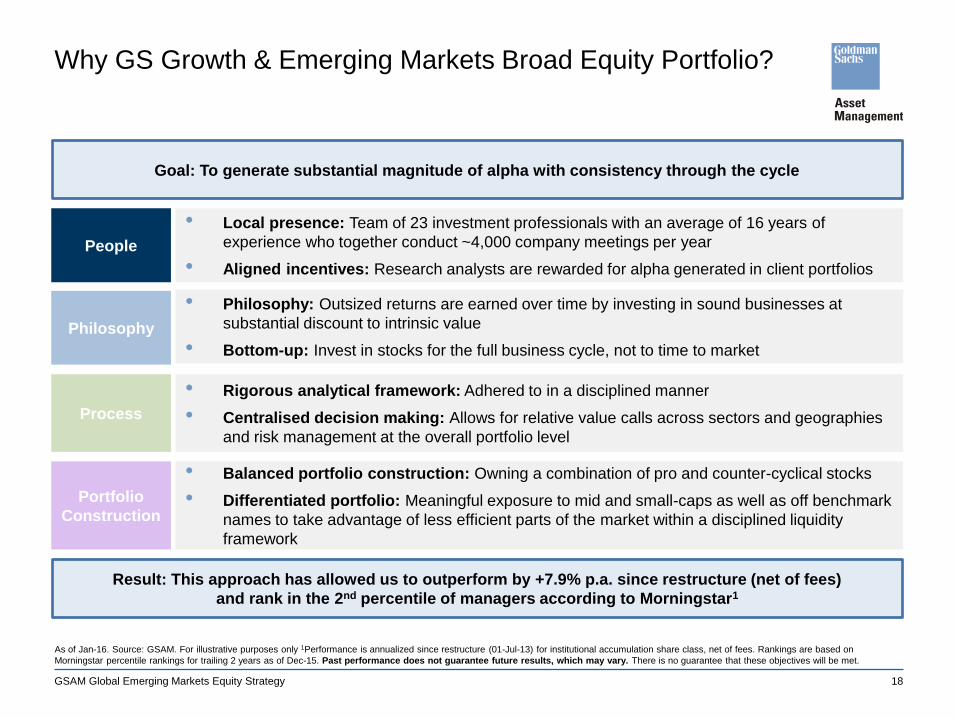

Goal: To generate substantial magnitude of alpha with consistency through the cycle

Result: This approach has allowed us to outperform by +7.9% p.a. since restructure (net of fees)

and rank in the 2nd percentile of managers according to Morningstar1

GSAM Global Emerging Markets Equity Strategy

As of Jan-16. Source: GSAM. For illustrative purposes only 1Performance is annualized since restructure (01-Jul-13) for institutional accumulation share class, net of fees. Rankings are based on

Morningstar percentile rankings for trailing 2 years as of Dec-15. Past performance does not guarantee future results, which may vary. There is no guarantee that these objectives will be met.

• Balanced portfolio construction: Owning a combination of pro and counter-cyclical stocks

• Differentiated portfolio: Meaningful exposure to mid and small-caps as well as off benchmark

names to take advantage of less efficient parts of the market within a disciplined liquidity

framework

• Rigorous analytical framework: Adhered to in a disciplined manner

• Centralised decision making: Allows for relative value calls across sectors and geographies

and risk management at the overall portfolio level

• Philosophy: Outsized returns are earned over time by investing in sound businesses at

substantial discount to intrinsic value

• Bottom-up: Invest in stocks for the full business cycle, not to time to market

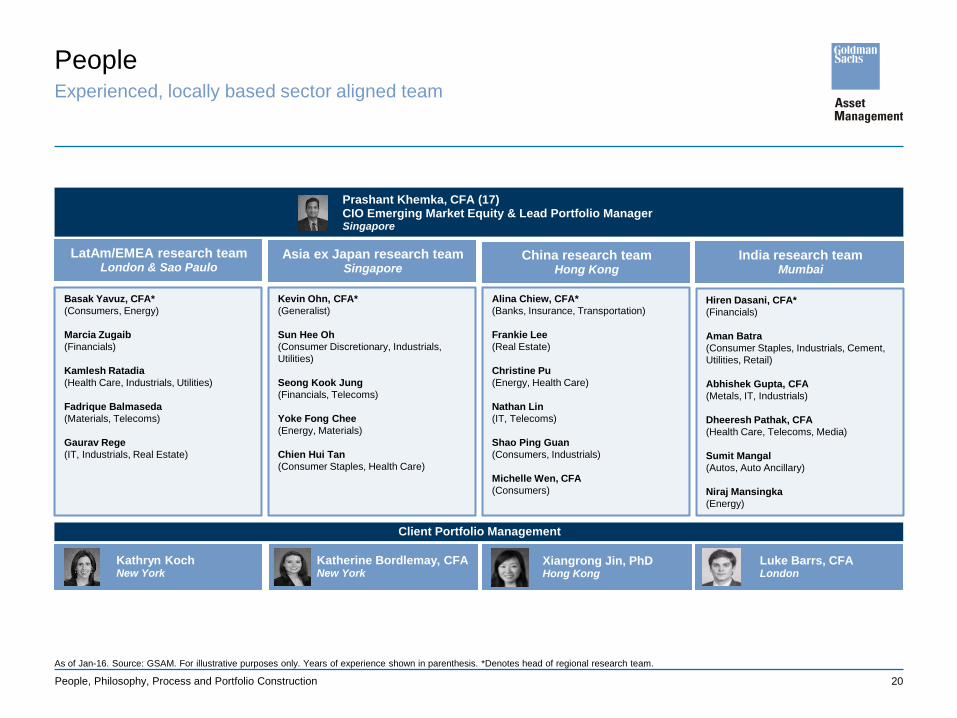

• Local presence: Team of 23 investment professionals with an average of 16 years of

experience who together conduct ~4,000 company meetings per year

• Aligned incentives: Research analysts are rewarded for alpha generated in client portfolios

Note: Holdings are subject to change and should not be construed as research or investment advice. Past performance does not guarantee future results, which may vary. There is no guarantee that

these objectives will be met. Targets are subject to change and are current as of the date of this presentation. Targets are objectives and do not provide any assurance as to future results.

As of Sep-15. 1 Strategy AUM as of Oct-15. 2 Performance is net of fees, annualized since 1-Jul-2013 which is when Prashant Khemka became CIO of Emerging Markets Equity.

Prashant is the CIO of Emerging Markets Equity, overseeing the portfolio management and investment research for the firm's Emerging Markets Equity accounts.

Prashant is the lead portfolio manager of GSAM’s Emerging Markets Equity, BRIC Equity and India Offshore Equity strategies. Prior to assuming this role, Prashant

spent seven years in Mumbai as head of the India Equity Research team. Prashant joined GSAM in May 2000 as a member of the US Growth Equity team, first as a

research analyst, then as a portfolio manager and then as a senior portfolio manager and co-chair of the Investment Committee. Prior to joining Goldman Sachs,

Prashant was an assistant portfolio manager in the Fundamental strategies group at State Street Global Advisors. He graduated with honors from Bombay University

with a BE in Mechanical Engineering and received his MBA in Finance from the Owen Graduate School of Management at Vanderbilt University, receiving the Matt

Wiggington leadership award for outstanding performance in finance. Prashant was awarded the Chartered Financial Analyst (CFA) designation in 2001 and is a fellow

of The Aspen Institute, India.

Kevin Ohn, CFA

Managing Director; Head of Asia ex-Japan Equity – Singapore

Kevin is the head of Asia ex-Japan Equity and lead portfolio manager of GSAM’s Asia ex-Japan Equity strategies. Prior to assuming this role, Kevin was the head of the

Korea Equity team in Seoul. Kevin joined GSAM in January 2007 from Allianz Global Investors, Seoul, where he spent four years as the Head of Equity Research and

then as the Chief Investment Officer of the Equity business, responsible for supervising equity investment, research and client service support, and managing corporate

governance and institutional mandates. Prior to working at Allianz Global Investors, he held positions as Head of Research at Hannuri Investment Securities, Equity

Analyst and Deputy Head of Research at Salomon Smith Barney, Senior Equity Analyst at Credit Lyonnais Securities and Equity Analyst at Daishin Securities. Kevin has

been covering the telecommunications, utilities, construction, and construction material sectors since 1987. He received an MBA in Finance and Accounting from the

Anderson Graduate School of Management at UCLA in 1993 and a BA in Economics from Sung Kyun Kwan University in 1988. Kevin was awarded the Chartered

Financial Analyst (CFA) designation in 1999.

Basak Yavuz, CFA

Executive Director; Head of EEMEA/LatAm Equity – London

Basak is the lead portfolio manager of the GSAM Growth Markets strategy and the lead portfolio manager of our N11 Equity Strategy. She is also the head of the

EEMEA/LatAm Equity team, and covers the Consumer and Materials sectors. Basak joined Goldman Sachs Asset Management in September 2011 from HSBC Global

Asset Management, where she spent three and a half years as a portfolio manager for frontier markets, focusing on Eastern Europe and Asia. During this time, Basak

also had primary research responsibility for commodities in the Middle East and North Africa. Prior to joining HSBC, Basak was a research analyst at Alliance Bernstein

in London from 2001 to 2008, with research responsibility for the Materials sector in EMEA. She began her career at Alliance Capital in Istanbul, where she worked from

1997 to 2001. Basak has BA (Hons) degrees in Management and Economics from the Bosphorus University in Istanbul and was awarded the Chartered Financial

Analyst (CFA) designation in 2001.

Appendix

22

Profiles of Professionals

Alina Chiew, CFA

Managing Director; Head of Greater China Equity – Hong Kong

Alina manages Goldman Sachs Asset Management (GSAM) Equity Strategies in Greater China, a role she assumed in Hong Kong in 2010. She joined Goldman Sachs

in Shanghai in 2006 as an executive director in GSAM and assumed the role of chief representative for the Goldman Sachs Shanghai representative office in 2007. Alina

was named managing director in 2009. Prior to joining the firm, Alina was head of research at CITIC Frontier China Research in Shanghai from 2004 to 2006. Before

that, she was head of Singapore Research and a member of the Asian Banks team at Morgan Stanley from 2000 to 2004. From 1995 to 2000, she worked as an equity

analyst at Merrill Lynch and Crosby Research, where she covered Malaysian financial institutions. Alina also worked at the Central Bank of Malaysia in the Regulation

Department from 1990 to 1995, focusing primarily on banking policy formulation.

Hiren Dasani, CFA

Executive Director; Head of India Equity Research Team – Mumbai

Hiren is the head of the GSAM India Equity Research team and lead portfolio manager of GSAM’s India Onshore Equity strategy. He also has primary research

responsibility for the Financials sector within India. Hiren joined the GSAM India Equity Research team in January 2007 from SSKI Securities, where he spent a year

working as a sell-side Research Analyst covering the Indian banking and Financial Services sector. Prior to that, he spent a year at Prudential ICICI as a Credit and

Economy Analyst and Assistant Fixed Income Fund Manager, and three years at UTI Bank in Corporate Credit. Prior to attending business school, he worked at Dorf

Ketal Chemicals, a specialist chemical company, for two years. Hiren received a PGDM in Finance and Marketing from the Indian Institute of Management, Kozhikode in

2001 and a Bachelor of Engineering (Chemical) from the M.S. University of Baroda in 1997. He was awarded the Chartered Financial Analyst (CFA) designation in 2008.

Luke Barrs, CFA

Executive Director; Fundamental Equity Client Portfolio Management – London

Luke Barrs is an Emerging Markets specialist at Goldman Sachs Asset Management. In this role he is focused on helping clients gain appropriate access to emerging

markets, as well as assisting with their strategic asset allocation decision making process. As part of his role, Luke worked closely with Jim O’Neill – creator of the BRIC,

N-11 and Growth Markets concepts – and the Office of the Chairman within GSAM, helping launch GSAM's Growth Markets and N-11 Equity strategies. Luke continues

to act as client portfolio manager in GSAM's Fundamental Equity team, responsible for their Global Emerging Markets, N-11, India and Income related equity strategies.

Prior to joining Goldman Sachs Asset Management he received a first-class B.A. (Hons) in Economics & Management from Exeter College, University of Oxford. He was

awarded the Chartered Financial Analyst (CFA) designation in 2013.

Appendix

23

Additional Notes

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO

SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might

be relevant.

This document has been issued by Goldman Sachs International, authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Offering Documents

This material is provided at your request for informational purposes only and does not constitute a solicitation in any jurisdiction in which such a solicitation is unlawful or to any person to whom it is unlawful.

It only contains selected information with regards to the fund and does not constitute an offer to buy shares in the fund. Prior to an investment, prospective investors should carefully read the latest Key

Investor Information Document (KIID) as well as the offering documentation, including but not limited to the fund’s prospectus which contains inter alia a comprehensive disclosure of applicable risks. The

relevant articles of association, prospectus, supplement, KIID and latest annual/semi-annual report are available free of charge from the fund’s paying and information agent and/or from your financial

adviser.

Distribution of Shares

Shares of the fund may not be registered for public distribution in a number of jurisdictions (including but not limited to any Latin American, African or Asian countries). Therefore, the shares of the fund must

not be marketed or offered in or to residents of any such jurisdictions unless such marketing or offering is made in compliance with applicable exemptions for the private placement of collective investment

schemes and other applicable jurisdictional rules and regulations.

Investment Advice and Potential Loss

Financial advisers generally suggest a diversified portfolio of investments. The fund described herein does not represent a diversified investment by itself. This material must not be construed as investment

or tax advice. Prospective investors should consult their financial and tax adviser before investing in order to determine whether an investment would be suitable for them.

An investor should only invest if he/she has the necessary financial resources to bear a complete loss of this investment.

Swing Pricing

Please note that the fund operates a swing pricing policy. Investors should be aware that from time to time this may result in the fund performing differently compared to the reference benchmark based

solely on the effect of swing pricing rather than price developments of underlying instruments.

The strategy may include the use of derivatives. Derivatives often involve a high degree of financial risk because a relatively small movement in the price of the underlying security or benchmark may result

in a disproportionately large movement in the price of the derivative and are not suitable for all investors. No representation regarding the suitability of these instruments and strategies for a particular

investor is made.

Emerging markets securities may be less liquid and more volatile and are subject to a number of additional risks, including but not limited to currency fluctuations and political instability.

Portfolio holdings may not be representative of current or future investments. The securities discussed do not represent all of the portfolio's holdings and may represent only a small percentage of the

strategy’s portfolio holdings. Future portfolio holdings may not be profitable.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss

of principal may occur.

Appendix

24

Additional Notes (cont’d)

Appendix

Economic and market forecasts presented herein reflect our judgment as of the date of this presentation and are subject to change without notice. These forecasts do not take into account the specific

investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be reflected here. These forecasts are subject to high levels of

uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative of a broad range of possible outcomes. These forecasts are estimated, based on

assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Goldman Sachs has no obligation to provide updates or changes to these

forecasts. Case studies and examples are for illustrative purposes only.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent

verification, the accuracy and completeness of all information available from public sources.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are current as of the date of this

presentation and may be subject to change, they should not be construed as investment advice

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

This material has been prepared by GSAM and is not financial research nor a product of Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of

law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from

those of Goldman Sachs Global Investment Research or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or

selling any securities. This information may not be current and GSAM has no obligation to provide any updates or changes.

A Goldman Sachs affiliate (the “Manager”) relies (or expects to rely) on Rule 4.13(a)(3) under the U.S. Commodity Exchange Act, as amended (the “Rule 4.13(a)(3) Exemption”) with respect to the GS

Growth & Emerging Markets Broad Equity portfolio (the “Fund”) based on satisfaction of the criteria for the Rule 4.13(a)(3) Exemption set forth therein. Therefore, the Manager is not required to deliver

certain CFTC-compliant disclosure documents and certified annual reports to investors in the Fund. In order to rely on the Rule 4.13(a)(3) Exemption, the Fund may only engage in a limited amount of

commodity interest transactions, which includes transactions involving futures contracts and swaps.

Index Benchmarks

Indices are unmanaged. The figures for the index reflect the reinvestment of all income or dividends, as applicable, but do not reflect the deduction of any fees or expenses which would reduce returns.

Investors cannot invest directly in indices.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the Investment Manager believes, in part based on industry

practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein. The exclusion of “failed” or closed hedge funds may mean that each index overstates

the performance of hedge funds generally.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the portfolio will achieve

similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects appropriate risk and return features, portfolio

characteristics may deviate from those of the benchmark.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer,