Tripping Over Transfer Pricing Regulations in India by Mihir Naniwadekar and T.P. Janani Reprinted from Tax Notes Int’l, September 16, 2013, p. 1127 Volume 71, Number 12 September 16, 2013 (C) Tax Analysts 2013. All rights reserved. Tax Analysts does not claim copyright in any public domain or third party content.

Transcript

Tripping Over Transfer PricingRegulations in India

by Mihir Naniwadekar and T.P. Janani

Reprinted from Tax Notes Int’l, September 16, 2013, p. 1127

Volume 71, Number 12 September 16, 2013

(C)

TaxA

nalysts2013.A

llrightsreserved.

TaxA

nalystsdoes

notclaim

copyrightin

anypublic

domain

orthird

partycontent.

Tripping Over Transfer Pricing Regulations in Indiaby Mihir Naniwadekar and T.P. Janani

The amount locked up in litigation in direct tax casesin India on September 30, 2012, was INR 1.002

trillion (about $15.4 billion).1 The transfer pricing adjust-ments made in 2012-2013 alone were INR 700 billion(about $10.8 billion).2 In the recent past, a large majorityof direct tax disputes have been decided initially in favorof the tax authorities but later in favor of the taxpayer atappellate levels in tribunals and courts.3 The taxpayer isrequired to deposit the whole or a significant portion ofthe disputed amount before pursuing appellate proceed-ings, and any refund of deposits on reversal of the judg-ment appealed against must be made with 6 percent in-terest per annum. Therefore, the tax authorities areleading the Indian government into a debt trap.

Much of the analysis of transfer pricing litigation inIndia has concentrated on the adoption of the right

method for determining the arm’s-length price (ALP).This article attempts to explore issues beyond those ques-tions, particularly the issues at the very root of the regu-lation — the extent to which the transfer pricing regula-tions are fair, just, and reasonable (according to article214 read with article 2655 of the Constitution of India).

Transfer pricing regulations are provisions to deter-mine income arising from transactions carried outbetween associated enterprises such that the incomewould be equivalent to the income that would havearisen had the enterprises not been associated. Theobjective of the determination is to prevent artificialprofit shifting to enterprises situated in jurisdictionswith relatively lower tax rates or that are otherwisetaxed at lower rates by virtue of exemptions, specialdeductions, setoff of losses carried forward fromprevious years, and so forth.

In 2001 transfer pricing regulations were introducedin India in an amendment to the Income Tax Act,1961. The following table captures some of the impor-tant provisions of the transfer pricing regulations(along with comparison of the position in other coun-tries whenever possible), the analysis of which is vitalto understanding whether the Indian transfer pricingprovisions are fair, just, and reasonable.

1‘‘Enough: Govt May Choose to Draw the Line on Tax Liti-gation With Firms,’’ The Indian Express (Apr. 25, 2013), availableat http://www.indianexpress.com/news/enough-govt-may-choose-to-draw-the-line-on-tax-litigation-with-firms/1107372/0.

2 Ministry of Finance, ‘‘Tax Evasion by Foreign Companies,’’Press Information Bureau, Government of India (Aug. 30, 2013),available at http://pib.nic.in/newsite/erelease.aspx?relid=99349.

3In 2011-2012, in appeals cases filed by the taxpayer at thetribunal, High Court and Supreme Court level, 36 percent, 38percent, and 33 percent, respectively, have been decided whollyin favor of the taxpayer, compared to 35 percent, 36 percent, and14 percent, respectively (that is, slightly less), decided wholly infavor of the tax authorities. For the same period, in case of ap-peals filed by the tax authorities, only 19 percent, 20 percent,and 10 percent, respectively, were decided wholly in favor of thetax authorities, compared to 52 percent, 62 percent, and 39 per-cent, respectively (almost triple), decided wholly in favor of thetaxpayer (Report of the Standing Committee on Finance on De-mand for Grants (2013-2014) of the Ministry of Finance (De-partment of Revenue), dated Apr. 16, 2013).

4Article 21 reads: ‘‘Protection of Life and Personal Liberty:No person shall be deprived of his life or personal liberty exceptaccording to procedure established by law’’; in Maneka Gandhi v.Union of India (AIR 1978 SC 597), the Supreme Court of Indiaheld that the procedure prescribed by ‘‘law’’ referred to in article21 should be one that is fair, just, and reasonable.

5Article 265 reads: ‘‘Taxes not to be imposed save by author-ity of law: No tax shall be levied or collected except by authorityof law.’’

Mihir Naniwadekar and T.P. Janani are associates with Nishith Desai in Mumbai.

TAX NOTES INTERNATIONAL SEPTEMBER 16, 2013 • 1127

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Background Position in India Contrasting Position in Other ProminentJurisdictions

a) Burden of Proof

Many countries with transfer pricingregulations have made it mandatory forassociated enterprises to prepare and submitdocumentation on the determination of ALPin respect of the various transactions theyenter into among themselves.

Leaving apart such documentation, countriesdiffer with respect to whether they impose theburden of proof on the taxpayer or the taxofficials so as to arrive at an ALP which isdifferent from the one reflected in thedocumentation submitted by the taxpayer.

The concerned tax official merely has to forman opinion that the ALP determined by thetaxpayer is not in accordance with statutoryprovisions, or that the information used forcomputation thereof is not reliable/correct(instead of having to substantiate the same).

It is the taxpayer who has to show why theALP suggested by the tax official is notcorrect.

While it has been judicially interpreteda thatonce a taxpayer presents a reasonableargument and evidence to suggest that itstransfer pricing was at arm’s length, theburden of proof shifts to the tax officials toestablish why the taxpayer’s transfer pricingwas not at arm’s length, the tax officials,particularly lower level officials, reject thetaxpayer’s determination of ALP as a matterof routine without assigning reasons and shiftthe burden of proof to the taxpayer by askingthe taxpayer to show cause as to why thedetermination made by the tax officialsshould not be adopted.

The harshness of the imposition of suchburden of proof on the taxpayer becomesmore prominent when seen in light of:

(i) judicial interpretationb that absence ofmotive to avoid tax or to shift profitsoutside India is not a defense againstapplicability of the transfer pricingprovisions; and

(ii) the difficulty in treating transfer pricingregulations as charging provisionsc (comparedwith mere rules of evidence, for theapplication of which requires some realevidence of tax evasion).

U.K. — If the taxpayer’s transfer pricingposition is reasonable and well documented,the tax authorities will have to demonstratethat it is wrong before an adjustment can beimposed.

Australia — If the tax office’s view of therelevant ALP is materially different to thatadopted by the taxpayer, a position paper isissued by the Australian Taxation Office(ATO) setting out the basis for the ATO’sdetermination. The taxpayer has anopportunity to respond to the position paperbefore the ATO makes a final decision.

Japan — The tax authorities bear the burden ofproof for the allegation that the transfer pricingmethod applied by the tax authorities accordswith one of the methods provided for underJapanese tax law.

U.S. — While the taxpayer has to bear theburden of proof in showing both that the taxauthorities’ determination of ALP is arbitrary,capricious, and unreasonable, and that theALP determined by it is accurate, the taxauthorities are required to provide thetaxpayer with an explanation as to how theiradjustment was determined.

b) Reciprocity — Whether Both Upward and Downward Adjustments Are Made?

Where tax officials determine the ALP withrespect to a transaction (different from theone determined by the taxpayer) and make anadjustment with respect to the income of oneof the associated enterprises to thetransaction, there could be double taxation ofsuch additional income if a correspondingadjustment (or downward adjustment) is notmade with respect to the income of the otherassociated enterprise(s).

In cases where tax is required be deducted atsource according to the Indian Income TaxAct, 1961, by way of a withholding/similarprocedure and an upward adjustment is madein case of the payer, downward adjustment is notpermissible in case of the payee.

U.S. and U.K. — When an ALP adjustmentis made, the corresponding downwardadjustment is also allowed.

South Africa — When an ALP adjustment ismade, the corresponding downwardadjustment is also allowed, if the enterprise inquestion is resident in a jurisdiction with whichSouth Africa has a tax treaty.

Canada — The tax officials allowcorresponding adjustments in accordance withthe provisions of the relevant tax treaty, subject tothe tax officials being satisfied that theprimary adjustment made by the treatypartner’s tax officials is in order.

PRACTITIONERS’ CORNER

1128 • SEPTEMBER 16, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Background Position in India Contrasting Position in Other ProminentJurisdictions

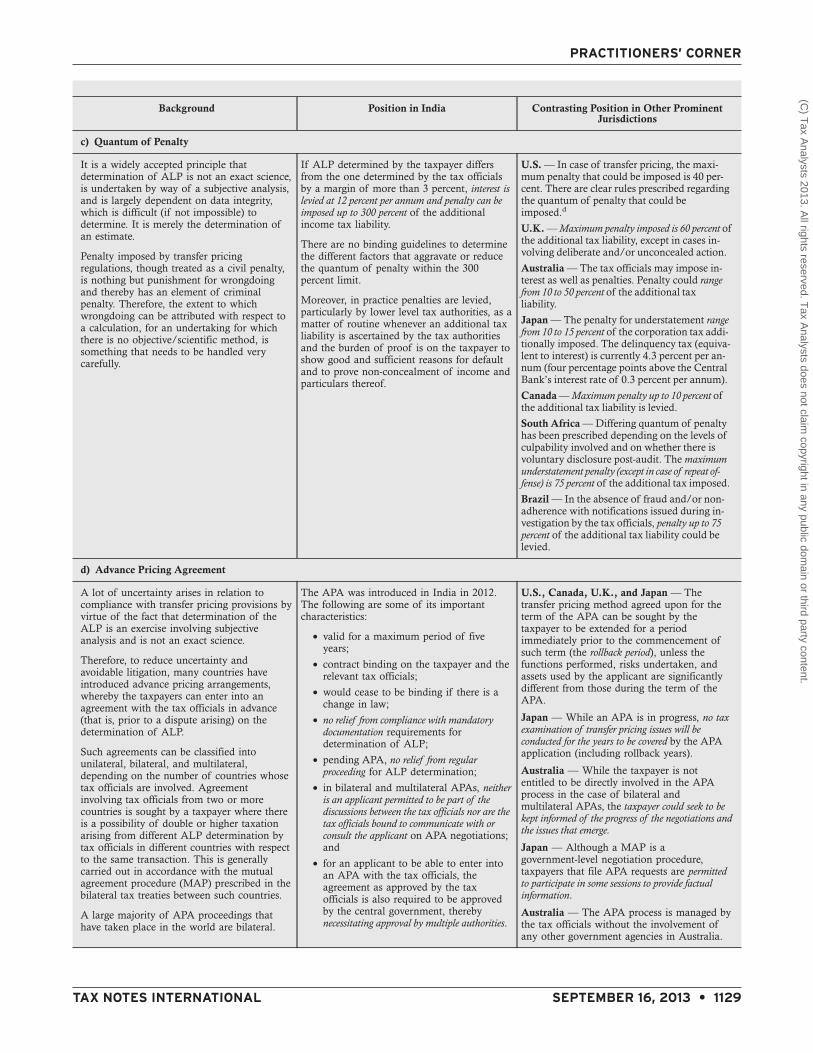

c) Quantum of Penalty

It is a widely accepted principle thatdetermination of ALP is not an exact science,is undertaken by way of a subjective analysis,and is largely dependent on data integrity,which is difficult (if not impossible) todetermine. It is merely the determination ofan estimate.

Penalty imposed by transfer pricingregulations, though treated as a civil penalty,is nothing but punishment for wrongdoingand thereby has an element of criminalpenalty. Therefore, the extent to whichwrongdoing can be attributed with respect toa calculation, for an undertaking for whichthere is no objective/scientific method, issomething that needs to be handled verycarefully.

If ALP determined by the taxpayer differsfrom the one determined by the tax officialsby a margin of more than 3 percent, interest islevied at 12 percent per annum and penalty can beimposed up to 300 percent of the additionalincome tax liability.

There are no binding guidelines to determinethe different factors that aggravate or reducethe quantum of penalty within the 300percent limit.

Moreover, in practice penalties are levied,particularly by lower level tax authorities, as amatter of routine whenever an additional taxliability is ascertained by the tax authoritiesand the burden of proof is on the taxpayer toshow good and sufficient reasons for defaultand to prove non-concealment of income andparticulars thereof.

U.S. — In case of transfer pricing, the maxi-mum penalty that could be imposed is 40 per-cent. There are clear rules prescribed regardingthe quantum of penalty that could beimposed.d

U.K. — Maximum penalty imposed is 60 percent ofthe additional tax liability, except in cases in-volving deliberate and/or unconcealed action.

Australia — The tax officials may impose in-terest as well as penalties. Penalty could rangefrom 10 to 50 percent of the additional taxliability.

Japan — The penalty for understatement rangefrom 10 to 15 percent of the corporation tax addi-tionally imposed. The delinquency tax (equiva-lent to interest) is currently 4.3 percent per an-num (four percentage points above the CentralBank’s interest rate of 0.3 percent per annum).

Canada — Maximum penalty up to 10 percent ofthe additional tax liability is levied.

South Africa — Differing quantum of penaltyhas been prescribed depending on the levels ofculpability involved and on whether there isvoluntary disclosure post-audit. The maximumunderstatement penalty (except in case of repeat of-fense) is 75 percent of the additional tax imposed.

Brazil — In the absence of fraud and/or non-adherence with notifications issued during in-vestigation by the tax officials, penalty up to 75percent of the additional tax liability could belevied.

d) Advance Pricing Agreement

A lot of uncertainty arises in relation tocompliance with transfer pricing provisions byvirtue of the fact that determination of theALP is an exercise involving subjectiveanalysis and is not an exact science.

Therefore, to reduce uncertainty andavoidable litigation, many countries haveintroduced advance pricing arrangements,whereby the taxpayers can enter into anagreement with the tax officials in advance(that is, prior to a dispute arising) on thedetermination of ALP.

Such agreements can be classified intounilateral, bilateral, and multilateral,depending on the number of countries whosetax officials are involved. Agreementinvolving tax officials from two or morecountries is sought by a taxpayer where thereis a possibility of double or higher taxationarising from different ALP determination bytax officials in different countries with respectto the same transaction. This is generallycarried out in accordance with the mutualagreement procedure (MAP) prescribed in thebilateral tax treaties between such countries.

A large majority of APA proceedings thathave taken place in the world are bilateral.

The APA was introduced in India in 2012.The following are some of its importantcharacteristics:

• valid for a maximum period of fiveyears;

• contract binding on the taxpayer and therelevant tax officials;

• would cease to be binding if there is achange in law;

• no relief from compliance with mandatorydocumentation requirements fordetermination of ALP;

• pending APA, no relief from regularproceeding for ALP determination;

• in bilateral and multilateral APAs, neitheris an applicant permitted to be part of thediscussions between the tax officials nor are thetax officials bound to communicate with orconsult the applicant on APA negotiations;and

• for an applicant to be able to enter intoan APA with the tax officials, theagreement as approved by the taxofficials is also required to be approvedby the central government, therebynecessitating approval by multiple authorities.

U.S., Canada, U.K., and Japan — Thetransfer pricing method agreed upon for theterm of the APA can be sought by thetaxpayer to be extended for a periodimmediately prior to the commencement ofsuch term (the rollback period), unless thefunctions performed, risks undertaken, andassets used by the applicant are significantlydifferent from those during the term of theAPA.

Japan — While an APA is in progress, no taxexamination of transfer pricing issues will beconducted for the years to be covered by the APAapplication (including rollback years).

Australia — While the taxpayer is notentitled to be directly involved in the APAprocess in the case of bilateral andmultilateral APAs, the taxpayer could seek to bekept informed of the progress of the negotiations andthe issues that emerge.

Japan — Although a MAP is agovernment-level negotiation procedure,taxpayers that file APA requests are permittedto participate in some sessions to provide factualinformation.

Australia — The APA process is managed bythe tax officials without the involvement ofany other government agencies in Australia.

PRACTITIONERS’ CORNER

TAX NOTES INTERNATIONAL SEPTEMBER 16, 2013 • 1129

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Background Position in India Contrasting Position in Other ProminentJurisdictions

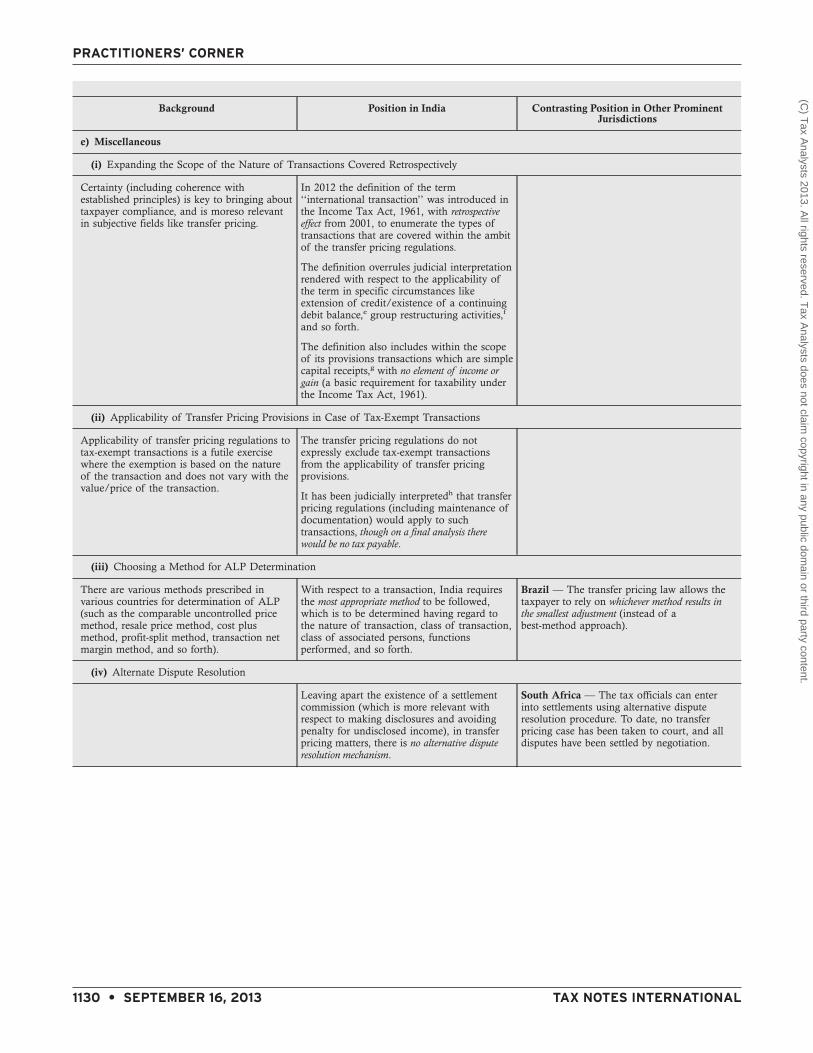

e) Miscellaneous

(i) Expanding the Scope of the Nature of Transactions Covered Retrospectively

Certainty (including coherence withestablished principles) is key to bringing abouttaxpayer compliance, and is moreso relevantin subjective fields like transfer pricing.

In 2012 the definition of the term‘‘international transaction’’ was introduced inthe Income Tax Act, 1961, with retrospectiveeffect from 2001, to enumerate the types oftransactions that are covered within the ambitof the transfer pricing regulations.

The definition overrules judicial interpretationrendered with respect to the applicability ofthe term in specific circumstances likeextension of credit/existence of a continuingdebit balance,e group restructuring activities,f

and so forth.

The definition also includes within the scopeof its provisions transactions which are simplecapital receipts,g with no element of income orgain (a basic requirement for taxability underthe Income Tax Act, 1961).

(ii) Applicability of Transfer Pricing Provisions in Case of Tax-Exempt Transactions

Applicability of transfer pricing regulations totax-exempt transactions is a futile exercisewhere the exemption is based on the natureof the transaction and does not vary with thevalue/price of the transaction.

The transfer pricing regulations do notexpressly exclude tax-exempt transactionsfrom the applicability of transfer pricingprovisions.

It has been judicially interpretedh that transferpricing regulations (including maintenance ofdocumentation) would apply to suchtransactions, though on a final analysis therewould be no tax payable.

(iii) Choosing a Method for ALP Determination

There are various methods prescribed invarious countries for determination of ALP(such as the comparable uncontrolled pricemethod, resale price method, cost plusmethod, profit-split method, transaction netmargin method, and so forth).

With respect to a transaction, India requiresthe most appropriate method to be followed,which is to be determined having regard tothe nature of transaction, class of transaction,class of associated persons, functionsperformed, and so forth.

Brazil — The transfer pricing law allows thetaxpayer to rely on whichever method results inthe smallest adjustment (instead of abest-method approach).

(iv) Alternate Dispute Resolution

Leaving apart the existence of a settlementcommission (which is more relevant withrespect to making disclosures and avoidingpenalty for undisclosed income), in transferpricing matters, there is no alternative disputeresolution mechanism.

South Africa — The tax officials can enterinto settlements using alternative disputeresolution procedure. To date, no transferpricing case has been taken to court, and alldisputes have been settled by negotiation.

PRACTITIONERS’ CORNER

1130 • SEPTEMBER 16, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

While courts in India may be slow in striking downfiscal provisions for violation of fundamental rights,clearly they would be determinative factors in develop-ing or hampering local and international investor confi-dence, which at the moment appears to be at an all-

time low and cannot be corrected by adopting quickfixes targeting only the symptoms of structural faultlines. Transfer pricing is relatively new in India and itis not too late to make the difficult choices withoutincurring too much transitional cost. ◆

Background Position in India Contrasting Position in Other ProminentJurisdictions

(v) Taxpayer Rights

There is no clear-cut/comprehensiverecognition of taxpayer rights.

Australia — It has a taxpayers’ charter, whichis a policy guide to provide information totaxpayers on their legal rights.i Although thecharter is not legally binding, taxpayers have alegitimate expectation that it will be followed.

aDeputy Commissioner of Income Tax v. Indo American Jewellery Ltd., [2010] 41 SOT 1 (Mum); Dresser-Rand India (P.) Ltd. v. Additional Commissioner ofIncome-tax, [2011] 13 taxmann.com 82 (Mum); Aztec Software & Technology Services Ltd. v. Assistant Commissioner of Income Tax, [2007] 107 ITD141 (Bang).bCoca Cola India Inc. v. Assistant Commissioner of Income Tax, 309 ITR 194 (P&H); Aztec Software and Technology Service Ltd. v. Assistant Commissionerof Income Tax, [2007] 294 ITR 32 (Bang); Assistant Commissioner of Income Tax v. MSS India, ITA No. 393/PN/07.cUnder the Income Tax Act, 1961, tax is only chargeable on income that is either accrued/received in India or deemed to have been accruedor received in India (as against income that ought to have accrued in India).d For example, a penalty of up to 20 percent and 40 percent could be imposed only if the ALP determined by the tax authorities is more thantwofold and fourfold or less than one-half and one-quarter, respectively, of the determination by the taxpayer. Further, the total adjustmentmust also be beyond certain absolute and relative thresholds.ePatni Computer Systems v. Deputy Commissioner of Income Tax, [2011] 16 ITR 533 (Pune); Nimbus Communications Limited v. Assistant Commissionerof Income Tax, ITA No. 6597/Mum/09.fDana Corporation v. Director of Income Tax, [2010] 321 ITR 178 (AAR).gAn instance of application of this provision is the recent issue of a draft assessment order to Shell India Markets Private Limited adding INR150 billion to the taxable income of the company by alleging underpricing in relation to issue of shares to an overseas group entity.hIn re Castleton Investment Limited, [2012] 348 ITR 537 (AAR).iTaxpayers’ rights include the right to be treated fairly and reasonably by the tax officials; to be presumed to be telling the truth unless theiractions indicate otherwise; to have their privacy respected and the confidentiality of documentation maintained; and to obtain professionaladvice and representation.

PRACTITIONERS’ CORNER

TAX NOTES INTERNATIONAL SEPTEMBER 16, 2013 • 1131

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom