62

Investor Day 2022 Strategy November 16, 2018

Investor Day

2022 Strategy

November 16, 2018

2

Forward Looking Statements

This presentation contains forward-looking statements, that should be considered as good faith

estimates. Such statements are subject to risks and uncertainties outside of Viña Concha y Toro’s

control that could cause Viña Concha y Toro’s actual results to differ materially from those set forth

in the forward-looking statements. These risks factors include but are not limited to the risks factors

in Item 3 - “Key Information – Risk Factors” in the 20-F Annual Report, and in those described in

Viña Concha y Toro’s Financial Statements, Note 5 (“Gestión de Riesgos Financieros”). Forward-

looking statements speak only as of the date they are delivered, Viña Concha y Toro undertake no

obligation to publicly update or revise them considering developments which differ from those

anticipated.

3

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

4

2018 harvest - Chile

Following two low-volume vintages, 2018 harvested volume increased 36% in Chile.

915

1,046

1,255 1,282

990

1,287

1,014 949

1,290

0

200

400

600

800

1.000

1.200

1.400

2010 2011 2012 2013 2014 2015 2016 2017 2018

Chile Harvest - (MM liters)

Source: SAG

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

5

2018 harvest - Argentina

In Argentina, the harvested volume increased 31% in 2018.

2,539

2,807

2,174

2,786 2,587

2,338

1,704

1,922

2,516

0

500

1.000

1.500

2.000

2.500

3.000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Argentina Harvest – (th. tons)

Source: INV

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

6

2018 harvest - USA

Estimates for California vintage point to a 5% increase in the harvested volume (4.2 millions of tons)

3.589 3.347

4.018 4.246

3.894 3.705

4.031 4.014 4.200

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

2010 2011 2012 2013 2014 2015 2016 2017 2018 E

USA vintage – thousand tons.

Source: Ciatti

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

7

Global wine production

• Global wine production in 2018 is estimated at 282 Mhl, an increase of 12%.

• Strong rebound of main producers:

Italy (+14%), France (+27%), and Spain (+26%).

266

262

281 280

267

258

267

300

282 284

268 269

272

264

268

258

292

270

275

269

251

282

200

220

240

260

280

300

320

Mil

lio

ns

of

HL

Source: OIV

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

100

83

98 100

77

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

110,0

2014 2015 2016 2017 2018

ba

se 1

00

: 2

01

4

Internal grape price (own production)

8

Chile - Price trends for main varieties

Premium Cabernet Sauvignon

100 107

119 142

133

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

2014 2015 2016 2017 2018

ba

se 1

00

: 2

01

4

External grape price

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

100

88

110 104

83

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2014 2015 2016 2017 2018

ba

se 1

00

: 2

01

4

Internal grape price (own production)

100

83 95

167

209

0,0

50,0

100,0

150,0

200,0

250,0

2014 2015 2016 2017 2018

ba

se 1

00

: 2

01

4

External grape price

9

Chile - Price trends for main varieties

Generic Cabernet Sauvignon

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

10

Chile - Share of own production and external grape sourcing

2018 harvest

Own

production

50%

External

50%

Own

production

30%

External

70%

Premium grapes Generic grapes

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

11

Argentina - Price trends for main varieties

Premium Malbec

100,0

148.5 154.4

163.9

88,6

0

20

40

60

80

100

120

140

160

180

2014 2015 2016 2017 2018

Internal grape cost

100.0 93.1

137.8

233.2 172,0

0

50

100

150

200

250

2014 2015 2016 2017 2018

External grape price

Base year: 2014, in USD, f/x as of 04/30 of every year

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

12

Argentina - Price trends for main varieties

Generic Malbec Blend

100.0

105.8

99.7

58.9

69,9

0

20

40

60

80

100

120

2014 2015 2016 2017 2018

Internal grape price

100.0 99.5

151.2

251.2

212.1

0

50

100

150

200

250

300

2014 2015 2016 2017 2018

External grape price

Base year: 2014, in USD, f/x as of 04/30 of every year.

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

13

Argentina - Share of own production and external grape sourcing

External

51%

Own

production

49%

External

46%

Own

production

54%

2018 harvest

Premium grapes Blend - Generic grapes

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

14

Conclusions

• Premium inventory stocks have recovered strongly.

• A decrease in the price of wine was foreseen during 2018, thus, not all of the needs projected (in

terms of grapes) were vinified.

• 2018 harvest: One of the best if not the greatest in terms of quality, in Chile and Argentina.

“I can’t remember such a good year in terms of

wine volume or quality. The wines are very

fruity, expressive and long, and they are easy to

drink. This 2018 harvest has achieved great

wines”.

Marcelo Papa Technical Director Viña Concha y Toro

“It was a typical harvest in Mendoza, with

excellent health and quality. Volume came

in above our expectations.”

Germán Di Césare Chief Winemaker Trivento.

I n v e s t o r D a y - 2 0 1 8

h a r v e s t

15

Conclusions

• Wine prices in 2018 year-to-date, in equivalent terms to grape prices:

• Generic Cabernet Sauvignon: -31%

• Sauvignon Blanc: -34%

• 2019 vintage outlook :

Normal conditions up to date, downward trend for grape prices.

I n v e s t o r

D a y

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

17

Trends in the global industry

• Premiumization trend is observed in most markets.

• Wine consumption is not growing significantly in any relevant market.

• China has entered in a stage of lower dynamism and growing “realism” in distribution

channels.

• Strong penetration of “discounters” to the detriment of larger retail chains. A phenomena

with higher intensity in Europe.

• Partnerships among marketers aimed to succeed in the penetration of fine wines category.

I n v e s t o r

D a y

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

19

Restructuring process – Support areas

1. Supply chain optimization in Chile local market

- Closure of branches: from 13 in 2016 to 8 in 2018

- Estimated annual net savings (full year): $1,100 million

2. Wine making process optimization

- Reduced number of owned cellars: from 13 to 11 in 2018

- Reduced number of leased cellars: from 5 to 3 in 2018

- Increased winemaking capacity of cellars: +20%

- Estimated annual net savings (full year): $1,630 million

3. Closure of Lo Espejo plant

- Reduced number of bottling plants: from 3 to 2 in 2018 (in Santiago)

- Estimated annual net savings (full year): $5,000 million

4. Rationalization of organizational structure in Chile

- Estimated annual net savings (full year): $4,800 million

I n v e s t o r

D a y

5. Important increase in productivity from higher share of clonal selections

• Productivity of vineyards planted with clonal selections is 27% higher than in massal selections

• 2017-18: Clonal selections share: 29% and massal selections share: 71%

20

Restructuring process – Support areas

Clonal selections - Evolution of share in production

29% 27%

15% 13%

21% 17%

clonal

massal

I n v e s t o r

D a y

21

Restructuring process – Estimated savings

(Ch$ million) 2017 2018 2019 Full Year

Efficiencies and synergies

from program 4,383 10,466 17,656 18,802

Severance payments,

consultancies (3,153) (6,141) (1,668)

Net savings 1,230 4,325 15,989 18,802

I n v e s t o r

D a y

22

Restructuring process – Previous estimates for savings

Differences in estimated net savings for 2018 and 2019 are explained by higher consultancies and

severance expenses.

(Ch$ million) 2017 2018 2019 Full Year

Efficiencies and synergies

from program 4,383 10,466 17,656 18,802

Severance payments,

consultancies (3,153) (4,460) (1,298)

Net savings 1,230 6,006 16,358 18,802

I n v e s t o r

D a y

23

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

New commercial strategy

We seek to lead the global wine industry through a consumer-centric focus,

oriented to the development of premium brands, delivering a higher value to

our customers, through a simple, agile, and sustainable productive model.

24

We have carried out significant adjustments in the commercial area in order to face

the new strategy.

I n v e s t o r

D a y

Low

Po

tenti

al

Relevance

1. Casillero del Diablo

1. 1000 Stories

2. Adorada

3. Bonterra

4. CdD Devil’s Collection

5. CdD Reserva Privada

6. CdD Reserva Especial

7. Cono Sur 20 Barrels

8. Cono Sur Bicicleta

1. Anthony’s Hill

2. Cold Water Creek

3. Cono Sur Orgánico

4. Sunrise

5. Tocornal

6. Tocornal CS

7. Tocornal Trivento

8. Trio

1. Clos de Pirque

2. Exportación

3. Fetzer

4. Frontera

5. Isla Negra

6. Maipo Entry Level

(Mi Pueblo y Classic)

7. Reservado

Brand matrix

High

9. Cono Sur Reserva Esp.

10. Diablo

11. Don Melchor

12. Jacked

13. Marques de Casa Concha

14. Trivento Golden

15. Trivento Private Reserve

16. Trivento Reserve

I n v e s t o r

D a y

Brand matrix

26

– Portfolio rationalization: Exit from 82 brand out of 304.

– Special focus on Casillero del Diablo brand (PRINCIPAL).

– Investments in brands with the highest potential from our 3 origins (INVEST).

– Commercial and marketing focus on new brands development to support a

high growth.

Implications:

I n v e s t o r

D a y

Market matrix: Specialized commercial areas

27

Commercial offices: 14 - Distributors: 352 - Markets + 130

I n v e s t o r

D a y

Independent distribution for Viña Cono Sur y Almaviva

28

Viña Cono Sur:

125 distributors

Presence in 84 countries

Viña Almaviva:

Distribution through Negociants de Bordeaux

I n v e s t o r

D a y

29

2018: Year of implantation of the new commercial model

• Long process, not free from internal difficulties: Cultural change.

• External difficulties: Brand portfolio redefinition and reorientation.

• Creation of a new unit for marketing excellence, analytics and market intelligence (CEMAI).

Develops analysis and reports to facilitate information on insights and trends.

• Strengthening of innovation and product development areas.

I n v e s t o r

D a y

New Products - Chile

I n v e s t o r

D a y

New Products - Chile

I n v e s t o r

D a y

32

New Products - Chile

I n v e s t o r

D a y

New Products - Argentina

I n v e s t o r

D a y

New Products - USA

I n v e s t o r

D a y

35

Following this complete revision,

realignment, and new vision:

We have a new company,

a new way of working

I n v e s t o r

D a y

36

A New Company

• Deep restructuring of the senior executive team in Chile.

• A new culture definition, based on :

– Forward-looking approach

– High level of expertise – with external advisory

– Management leadership

– Communication and teamwork promotion

• A simplified company at all levels and areas. High impact on costs and on agility.

• A transformed and new commercial business model.

• Commitment of the company's entire workforce: clear and traceable KPI’s.

• Greater innovation, entrepreneurial mindset of the senior executive team, and openness to change.

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

38

Fetzer-Excelsior merger

1. Further consolidation of distributors and retailers. After the last merger, RNDC /

Breakthru, # 1 & #2 will have 60% market share.

Top US Wine Distributors

Integration Sales (billion)

1 Souther Glazer`s Wine & Spirits 2016 US$ 16.5

2 RNDC & Breakthru 2018 US$ 12.0

3 Young`s Market Co. US$ 3.0

2013 2014 2015 2016 2017

Volume USA

(th. cases) 2,811 2,938 3,083 2,951 2,570

YoY variation -6% 5% 3% -3% -13%

60% market share

2. Low performance of Excelsior.

3. The merger is a step taken after achieving a greater level of expertise by Fetzer

commercial and support teams.

I n v e s t o r

D a y

39

Fetzer-Excelsior merger

• Cost savings from consolidation of sales force and SG&A absorption

Investmente US$ 40,5 mm

Annual savings US$ 9,0 mm

Increment marketing

expenses US$ 4,0 mm

Ahorros netos US$ 5,0 million

Fuerza Venta Nº people Merger

Excelsior 50 90

Fetzer 66

SKU’s Nº Merger

Excelsior 121 440

Fetzer 319

• Consolidation of sales force as of July 1, 2018, a year of adjustments and portfolio integration

• 2019: year of expected sales expansion from innovations and larger marketing expenses

40

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

41

3Q18 operating profit

(Ch$ million) 3Q18 3Q17 Var%

Sales 155,021 153,728 0.8%

Gross profit 50,946 51,193 (0.5%)

Gross margin 32.9% 33.3% (40 bp)

SG&A (39,033) (36,461) 7.1%

SG&A / sales (25.2%) (23.7%) (150 bp)

Other Income/Expenses 5,543 160 3374.2%

Operating profit 17,457 14,891 17.2%

Operating margin 11.3% 9.7% 160 bp

I n v e s t o r D a y – R e s u l t a d o s 3 Q 2 0 1 8

42

3Q18 non-recurring items

*.

(Ch$ million) 3Q18 3Q17

Restructuring

Costs 846 499

Expenses 1,483 1,037

Restructuring costs + expenses 2,329 1,536

Revaluation 50% Excelsior 6,218 0

I n v e s t o r

D a y

43

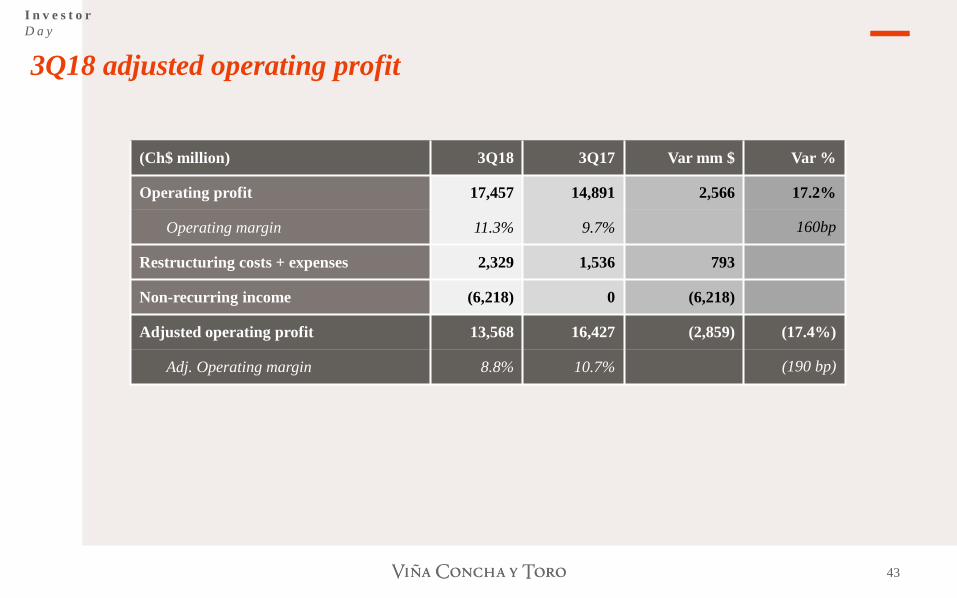

3Q18 adjusted operating profit

*.

(Ch$ million) 3Q18 3Q17 Var mm $ Var %

Operating profit 17,457 14,891 2,566 17.2%

Operating margin 11.3% 9.7% 160bp

Restructuring costs + expenses 2,329 1,536 793

Non-recurring income (6,218) 0 (6,218)

Adjusted operating profit 13,568 16,427 (2,859) (17.4%)

Adj. Operating margin 8.8% 10.7% (190 bp)

I n v e s t o r

D a y

44

3Q18 results – Impact from lower sales volume

Main reasons:

1. Portfolio Rationalization: Exit from 82 out of 304 brands.

2. Volume decline concentrated in non-priority brands:

• Brands in the matrix: -3.6% YoY. Protect and Watch explain 81% of the

decline

• Brands out of the matrix: -15.3% YoY

I n v e s t o r

D a y

45

3Q18 results – Impact from lower sales volume

3. Integration of Excelsior in Fetzer from July 1st, 2018. Large adjustment in the quarter.

• Decline in shipments to USA: -19.2%

4. Fewer business days in September 2018

Bottled exports from Chile (var. 2018/17)

• Jan –mar : -1.4%

•Apr – Jun : -2.2%

• Jul – sept : -9.0%

•September : -26.5%

- Decreases in shipments mainly in direct exports, not at distribution subsidiaries..

5. End of distribution contracts for Diageo and Cusqueña: Decline of $3,098 million

I n v e s t o r

D a y

46

3Q18 non-operating profit

(Ch$ million) 3Q18 3Q17 Var %

Net financial expenses (3,047) (2,584) 17.9%

Exchange differences 2,182 3,791 (42.4%)

Share of profit associates, JV 2,471 2,905 (14.9%)

Non-operating profit 1,606 4,112 (60.9%)

I n v e s t o r

D a y

47

3Q18 affiliates results

(Ch$ million) 3Q18 3Q17 Var %

Industria Corchera 99 169 (41.3%)

Viña Almaviva S.A. 2,546 2,128 19.6%

Others (174) 609 (128.5%)

Share of profit of associates, JV 2,471 2,905 (14.9%)

I n v e s t o r

D a y

48

3Q18 results

(Ch$ million) 3Q18 3Q17 Var %

Sales 155,021 153,728 0.8%

Gross profit 50,946 51,193 (0.5%)

Gross margin 32.9% 33.3% (40 bp)

Operating profit 17,457 14,891 17.2%

Operating margin 11.3% 9.7% 160 bp

Non-operating profit 1,606 4,112 (60.9%)

Net profit 17,582 14,642 20.1%

Net margin 11.3% 9.5% 180 bp

EBITDA 24,626 21,003 17.3%

EBITDA margin 15.9% 13.7% 220 bp

I n v e s t o r

D a y

49

3Q18 Fetzer Vineyards results - individual

(Ch$ million) 3Q18 3Q17 Var %

Sales 19,771 17,884 10.6%

Operating profit 1,877 896 109.5%

Operating margin 9.5% 5.0% 450 bp

I n v e s t o r

D a y

50

3Q18 Trivento results - individual

(Ch$ million) 3Q18 3Q17 Var %

Sales 8,013 9,923 (19.2%)

Operating profit 370 938 (60.6%)

Exchange differences 1,962 379 417.7%

Adjusted operating profit 2,332 1,317 77.1%

Adjusted operating margin 29.1% 13.3% 1,580 bp

I n v e s t o r

D a y

51

9M18 Results

(Ch$ million) 9M18 9M17 Var %

Sales 430,754 434,125 (0.8%)

Gross profit 139,798 142,992 (2.2%)

Gross margin 32.5% 32.9% (50 pb)

Operating profit 41,805 39,541 5.7%

Operating margin 9.7% 9.1% 60 pb

Non-operating profit 4,057 334 1114.6%

Net profit 37,580 29,983 25.3%

Net margin 8.7% 6.9% 180 pb

EBITDA 60,108 56,466 6.5%

EBITDA margin 14.0% 13.0% 90 pb

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

53

THE COMPANY INCORPORATES INITIATIVES THAT FOSTER A

BALANCED ADMINISTRATION OF ECONOMIC, ENVIRONMENTAL

AND SOCIAL FACTORS THROUGHOUT THE PRODUCTIVE

PROCESS.

RATIONAL USE OF NATURAL RESOURCES

ENVIRONMENTAL RESPONSIBILITY

COMMITMENT WITH PEOPLE AND

COMMUNITIES

Sustainability

I n v e s t o r

D a y

SOCIAL PRACTICES

CARBON FOOTPRINT Measured since 2007

WATER FOOTPRINT Measured since 2010

RENEWABLE ENERGY

NATIVE FOREST

54

Sustainability

• Eco-glass lightweight bottle used in 99% of portfolio • Carbon footprint certificated by Carbon Trust • 30% reduction of carbon footprint since 2012

• 100% drip irrigation in own vineyards • Water footprint 40% below global industry average

• 65% energy sourcing from clean energy, making progress in certification of energy footprint. Goal: 100% of energy sourcing in 2020

• Compliant with Business Social Compliance Initiative (BSCI) standards • Certificated by Wines of Chile National Sustainability Code • Ruggie Framework Analysis of UN Guiding Principles on Business and

Human Rights

• 3.372 hectares of native forest under conservation plans. 100% of forests with biodiversity inventories

• 2020 Sustainability strategy aligned with United Nations SDG (sustainable development goals)

SUSTAINABILITY STRATEGY

DOW JONES SUSTAINABILITY INDEX

• Top 10 - Global Beverages Ranking - Viña Concha y Toro (4 years in a row)

TRACK RECORD

I n v e s t o r

D a y

Agenda

1. 2018 harvest

2. Global wine industry trends

3. Restructuring process – Support areas

4. Restructuring process – Commercial area

5. Fetzer – Excelsior merger

6. 3Q18 results

7. Sustainability

8. Real Estate business

I n v e s t o r

D a y

56

Real Estate business

• Our Real Estate subsidiary has continued to make progress in feasibility studies and approvals for

our properties in order to maximize their value.

• Progress according to the current phase within Real Estate timelines.

• Projects with the highest degree of advance are La Cisterna y Tocornal.

• In paralell, we have made progress in the divestment of former distribution facilities, with a total

surface of 53,645 m2 and estimated value of UF 200,000, to be executed in 12-24 months.

I n v e s t o r

D a y

57

Real Estate business – La Cisterna ( 50% ownership share)

Location:

La Cisterna, RM

Land area:

10,070 m2

Real Estate project:

apartments.

Project duration:

8 years

Est. land market value w/feasibility:

UF 19/m2

Estimated value of land and project:

UF 48.5/m2

Estimated starting date of construction:

April 2020

I n v e s t o r

D a y

58

Real Estate business – Fundo Tocornal

N

TOCORNAL

Location:

Puente Alto, RM

Land area:

43.57 Ha.

Real Estate project:

Houses

Project duration:

10 years

Est. land market value w/feasibility:

UF 1.8/m2

Estimated value of land and project:

UF 4.5 /m2

Estimated starting date of construction:

December 2021

I n v e s t o r

D a y

Important recognitions

to the company’s portfolio

Investor Day

2022 Strategy

November 16, 2018