23

| Date post: | 24-May-2018 |

| Category: |

Documents |

| Upload: | truongminh |

| View: | 216 times |

| Download: | 2 times |

Turkish Flat Steel

Ersun ÖZDEMİREL

BORÇELİK ÇELİK SAN. TİC. A.Ş.

Forward-Looking Statement

Statements in this presentation describing either macro economic and relevant steel industry

parameters or the Borçelik Çelik Sanayii Ticaret A.Ş.’s (“Company” or “Borçelik”) objectives, financial

and non-financial projections, estimates, expectations along with their underlying assumptions may be

in the form of “forward looking statements” within the meaning of applicable securities laws and

regulations. Forward-looking statements might be identified by the words “believe”, “expect”,

“anticipate”, “target” or similar expressions. Although Company’s management believes that the

expectations reflected in such forward-looking statements are reasonable, readers are cautioned that

forward-looking information and statements are subject to numerous risks and uncertainties, many of

which are difficult to predict and generally beyond the control of Company. Actual results could differ

materially from those expressed or implied. Important factors that could make a difference to the

Company’s operations include, among others, economic conditions affecting demand, supply and price

conditions in the domestic and overseas markets in which Company conducts business transactions,

changes in Government regulations, tax laws and other incidental factors.

AGENDA

• Borçelik

• Turkish Steel Industry

• Turkish Flat Steel Market

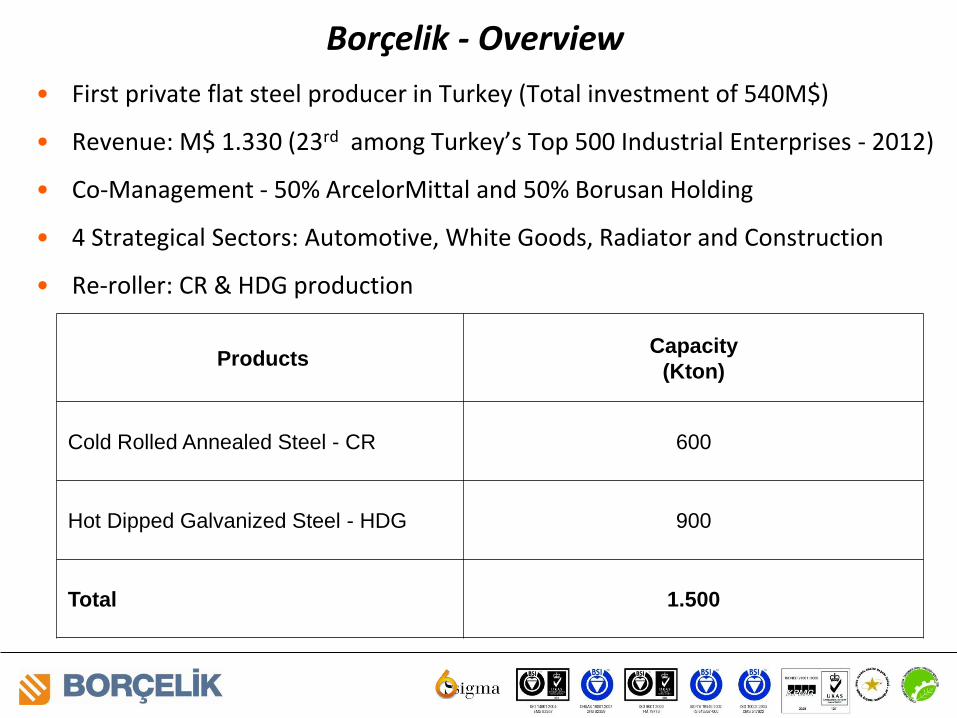

• First private flat steel producer in Turkey (Total investment of 540M$)

• Revenue: M$ 1.330 (23rd among Turkey’s Top 500 Industrial Enterprises - 2012)

• Co-Management - 50% ArcelorMittal and 50% Borusan Holding

• 4 Strategical Sectors: Automotive, White Goods, Radiator and Construction

• Re-roller: CR & HDG production

Borçelik - Overview

Products Capacity

(Kton)

Cold Rolled Annealed Steel - CR 600

Hot Dipped Galvanized Steel - HDG 900

Total 1.500

Borçelik - Location

Situated near Gemlik,

20 km away from Bursa city

200 km away from Istanbul.

Borusan Port logistic advantage,

Container and bulk shipment options.

Borusan Holding

World’s biggest steel producer

• Global and widespread operation…

• Strategic investments to raw materials

(coal, iron ore)…

0

100

ArcelorMittalTurkey

88

36

2012 Steel Production (mio ton)

World steel production in 2012 was 1,518 million tons.

Germany 43 mio ton (7th), Turkey 36 mio ton (8th),

ArcelorMittal

AGENDA

• Borçelik

• Turkish Steel Industry

• Turkish Flat Steel Market

Turkey 8th biggest producer in the world (2nd in EU after Germany)

Turkish Steel Industry

Rank Country 2012 2011

% change-

12/11

1. China 716.540 695.000 3,1

2. Japan 107.460 107.601 -0,1

3. United States 88.598 86.398 2,5

4. India 76.720 73.590 4,3

5. Russia 70.608 68.852 2,5

6. South Korea 69.345 68.519 1,2

7. Germany 42.661 44.284 -3,7

8. Turkey 35.885 34.107 5,2

9. Brazil 34.682 35.221 -1,5

10. Ukraine 32.911 35.332 -6,9

TOTAL WORLD 1.518.289 1.500.442 1,2

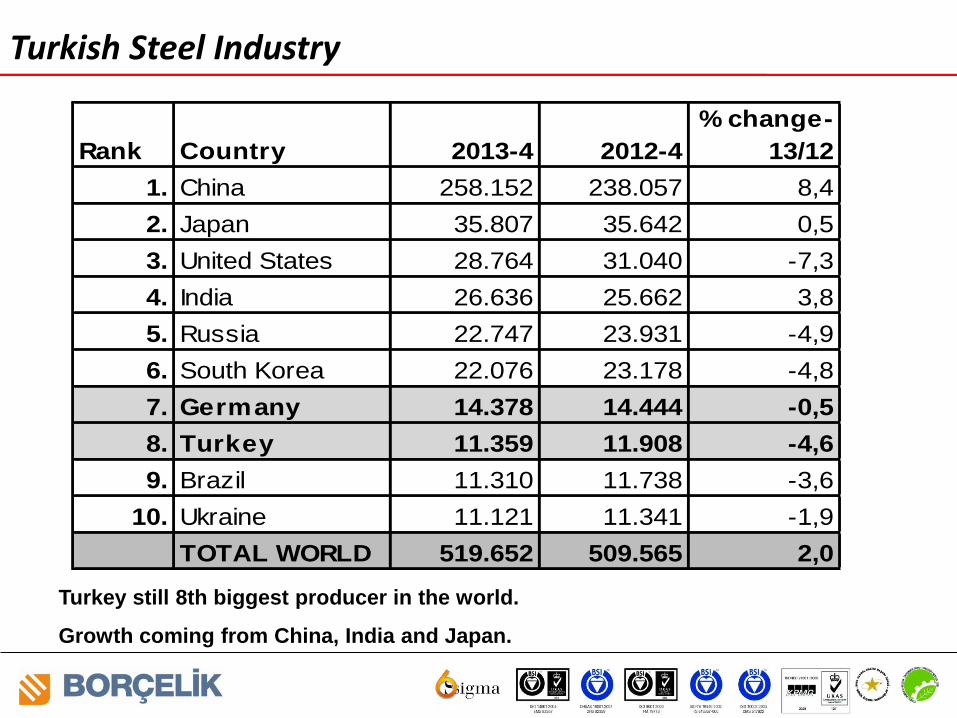

Turkey still 8th biggest producer in the world.

Growth coming from China, India and Japan.

Turkish Steel Industry

Rank Country 2013-4 2012-4

% change-

13/12

1. China 258.152 238.057 8,4

2. Japan 35.807 35.642 0,5

3. United States 28.764 31.040 -7,3

4. India 26.636 25.662 3,8

5. Russia 22.747 23.931 -4,9

6. South Korea 22.076 23.178 -4,8

7. Germany 14.378 14.444 -0,5

8. Turkey 11.359 11.908 -4,6

9. Brazil 11.310 11.738 -3,6

10. Ukraine 11.121 11.341 -1,9

TOTAL WORLD 519.652 509.565 2,0

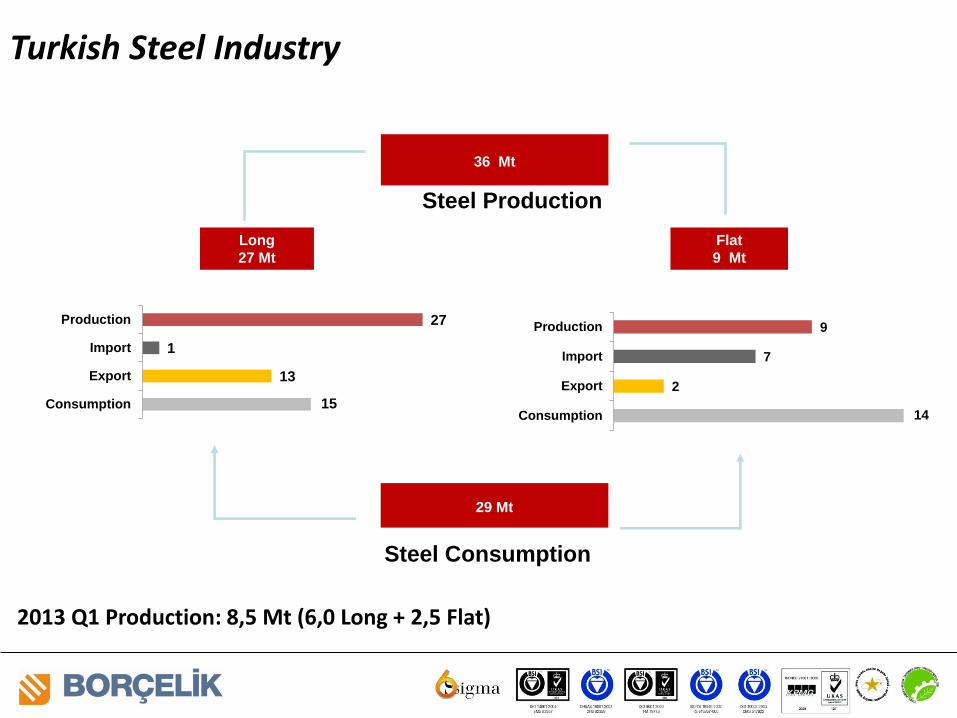

Turkish Steel Industry

29 Mt

Steel Consumption

36 Mt

Flat

9 Mt

Long

27 Mt

15

13

1

27

Consumption

Export

Import

Production

14

2

7

9

Consumption

Export

Import

Production

Steel Production

2013 Q1 Production: 8,5 Mt (6,0 Long + 2,5 Flat)

Turkish Steel Industry

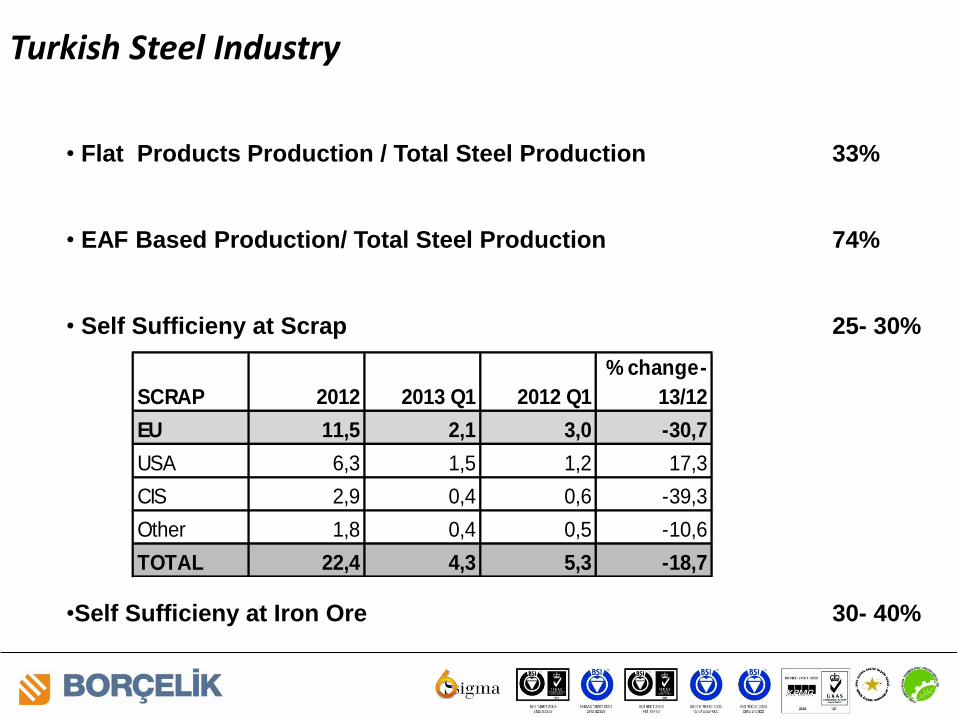

• Flat Products Production / Total Steel Production 33%

• EAF Based Production/ Total Steel Production 74%

• Self Sufficieny at Scrap 25- 30%

•Self Sufficieny at Iron Ore 30- 40%

Turkish Steel Industry

SCRAP 2012 2013 Q1 2012 Q1

% change-

13/12

EU 11,5 2,1 3,0 -30,7

USA 6,3 1,5 1,2 17,3

CIS 2,9 0,4 0,6 -39,3

Other 1,8 0,4 0,5 -10,6

TOTAL 22,4 4,3 5,3 -18,7

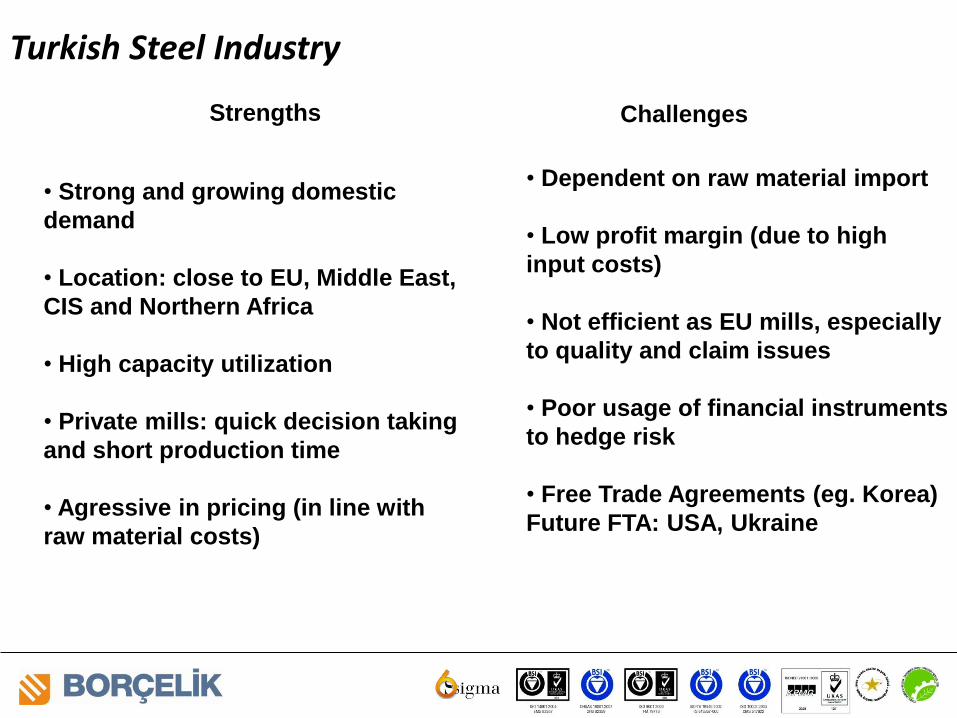

• Strong and growing domestic

demand

• Location: close to EU, Middle East,

CIS and Northern Africa

• High capacity utilization

• Private mills: quick decision taking

and short production time

• Agressive in pricing (in line with

raw material costs)

Turkish Steel Industry

Strengths Challenges

• Dependent on raw material import

• Low profit margin (due to high

input costs)

• Not efficient as EU mills, especially

to quality and claim issues

• Poor usage of financial instruments

to hedge risk

• Free Trade Agreements (eg. Korea)

Future FTA: USA, Ukraine

AGENDA

• Borçelik

• Turkish Steel Industry

• Turkish Flat Steel Market

Turkish Flat Steel Market

Share of local production in flat steel consumption is increasing:

2008 28%

2012 66%

Mton Production Import Export Consumption

2012 9,0 6,4 1,9 13,6

2011 9,1 6,4 2,3 13,2

Difference 0% 0% -19% 3%

Source : Turkish Statistical Institute -TUIK & DCUD

Turkish Flat Steel Market

Mton Production Import Export Consumption

2013 Q1 2,5 1,8 0,7 3,6

2012 Q1 2,3 1,5 0,4 3,4

Difference 9% 21% 73% 6%

Source : Turkish Statistical Institute -TUIK & DCUD

Difference -7% 6% -11% -2%

Long products affected total production tonnage (-4,6% in 2013-4)

Source : TUIK, Company press releases and Borçelik estimation

Mton

Turkish HRC Market - 2012

Mton

Source : TUIK, Company press releases and Borçelik estimation

Turkish CR Market - 2012

Mton

Source : TUIK, Company press releases and Borçelik estimation

Turkish HDG Market - 2012

Kton

Source : TUIK, Company press releases and Borçelik estimation

Turkish CCC Market - 2012

• Turkey’s flat steel production capacity increased during last couple years.

• However, capacity increases are in commercial grades production.

• Still nearly half of the flat steel consumption has to be met by imports;

especially for value-added grades for automotive and consumer goods.

• Nearly 50% of flat steel imported from EU region.

• EU and CIS countries account for 85% of Turkey’s flat steel imports.

• In total trade, Turkey has big deficit to EU & CIS countries in flat steel trade.

• Eurozone GDP shrank by 0,2% in 2013-Q1, the sixth concecutive decline.

Germany avoided falling back into recession with growth of 0,1%.

• Capacity surplus and Ilva’s seized products will continue to affect EU market.

• China has the potential to distort world steel markets both in terms of surplus

capacity and price policies applied to export markets.

Summary

Q & A