31

Martyn Begbour, Executive Director & Desk Head South & South West An Introduction to UBS Wealth Management

| Date post: | 14-Jul-2015 |

| Category: |

Business |

| Upload: | maria-yaroslavskaya |

| View: | 203 times |

| Download: | 1 times |

Martyn Begbour, Executive Director &

Desk Head South & South West

An Introduction to UBS

Wealth Management

1

Career background

HSBC undertaking a variety of roles inc.

• Head of Marketing & Business Development, Private Clients

• Senior Manager, Investment Products, HSBC International, Jersey

Coutts & Co Private Bank

• Client Partner

UBS Wealth Management

• Desk Head, South & South West

UBS – Wealth Management at the core

UBS is one of the

world’s leading

financial firms

We are present in all

major financial

centers and employ

about 60,000 people

in over 50 countries

Wealth

ManagementWealth Management

Americas

Global Asset

Management

Provides superior

investment advice

and solutions for

private clients

Sophisticated

investment process

and research

Present in over 40

countries, including

Switzerland

Offers advice-based

solutions through

financial advisors

Integrated set of

products and

services designed

to address the

needs of individuals

and families

Large scale asset

manager

Well-diversified

businesses across

regions, capabilities

and distribution

channels

Offers investment

capabilities across

all major traditional

and alternative

asset classes for

private clients,

financial

intermediaries and

institutional

investors

Offers research,

equities, foreign

exchange, precious

metals and tailored

fixed income

services

Provides advisory

services, financial

solutions and

access to capital

markets for

corporate,

institutional and

wealth management

clients

Investment Bank

Financial strength

3

1,936

1,353999

173 30.5

2,017

0

500

1000

1500

2000

Bank of

America

UBS¹ Credit Suisse JPMorgan Barclays² RBS3Credit ratings as of 20.10.14, unless otherwise indicated

Source: UBS AG1 Source: Company websites

Wealth management invested assets as at Q2 2014 (CHF bn)

1 Assets include Wealth Management and Wealth Management Americas2 Figures as at 31.03.143 Figures as at 31.07.14

Source: Company reportingData as at end Q3 2014 unless otherwise indicated.Figures will be updated on the next publication of UBS's results (28 October 2014 for Q3 2014)

Long term credit ratings S&P's Moody's Fitch

UBS AG A A2 A

Credit Suisse Group AG A- (P)A2 A

HSBC Holdings Plc A+ Aa3 AA-

JPMorgan Chase & Co A A3 A+

Bank of America Corp A- Baa2 A

Barclays Plc A- (P)A3 A

Citigroup Inc A- Baa2 A

Royal Bank of Scotland Group Plc1 Baa2 BBB+ A

Lloyds Banking Group Plc1 A A1 A

BIS Basel III common equity tier 1 ratio as at 28.10.14(%) – fully

applied*

* UBS and Credit Suisse - BIS Basel III framework came into effect on 01.01.13, for other banks,

ratios shown represent pro-forma Basel 3 estimates as disclosed by the companies.2 As at 31.03.2014

Source: Company data and broker reports. Date as of 30.06.14 unless otherwise indicated.

Figures will be updated on the next publication of UBS's results (10 February 2015 for Q4 2014)

*- indicates rating is under review for a possible downgrade

*+ indicates rating is under review for a possible upgrade

9.5 9.510.6 9.8 9.6

10.8

13.7

0

2

4

6

8

10

12

UB

S

Cre

dit

Su

isse

Ban

k o

f

Am

eri

ca

Cit

igro

up

JPM

org

an

Barc

lays

²

HSB

C²

UBS Wealth Management in the UK

An established presence in the UK since 1999

– Around 850 employees1

– More than 200 Client Advisors1

Serving over 15,000 clients across the UK

Over 100 Investment Products and Service professionals1,

including wealth planning specialists focused on delivering

UK tax-effective solutions**

Dedicated teams to support clients with specific needs

including family offices, charities, intermediaries,

professionals and executives

One of the Top 5 UK wealth managers by invested assets2

Recognised as the best private bank in the UK and No 1 in

the UK for High Net Worth II ($10m to $30m) and Family

Office services3

Jersey (St. Helier)

London

Birmingham

Manchester

Newcastle

Edinburgh

1 As at 28.10.14. All figures rounded.

2 Source: PAM Insight Ltd, 2014

3 Source: Euromoney Private Banking Survey 2014

Source: UBS Wealth Management

** UBS does not provide tax advice

Figures will be updated on the next publication of UBS's quarterly results (10 February

2015 for Q4 2014)

A network of regional offices and teams* to

ensure fast and reliable access to our

specialists

Leeds

*Team of 4 Client Advisors covering South and West of Britain

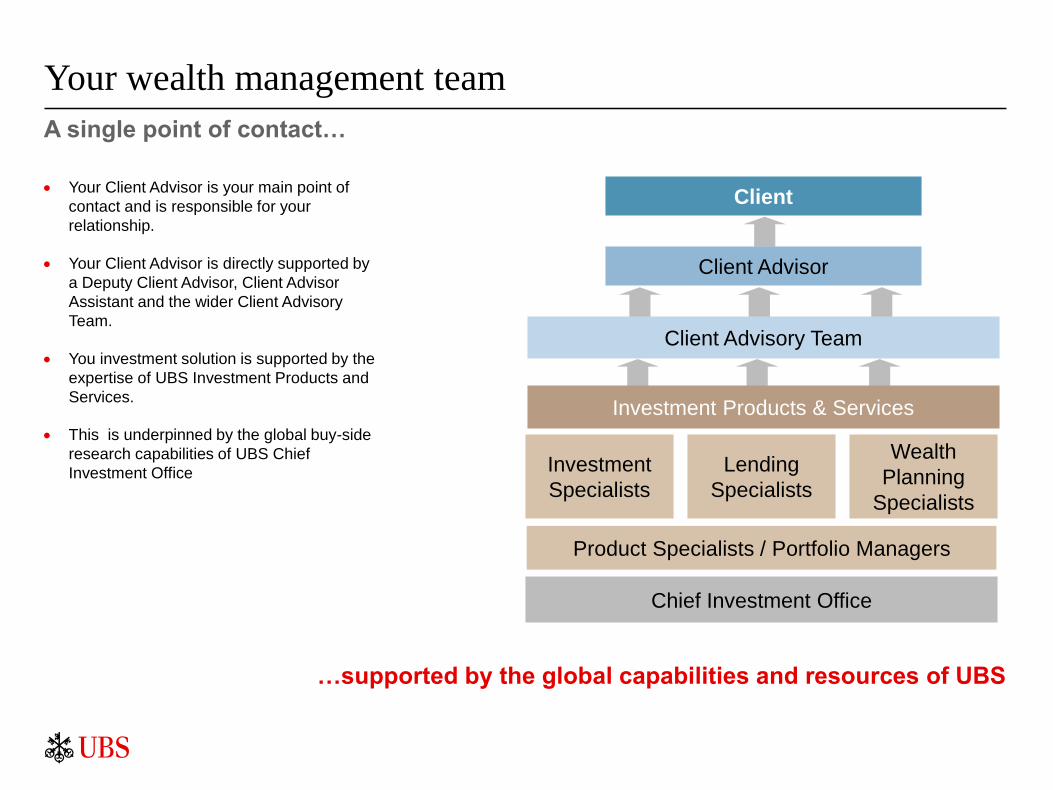

Your wealth management team

Your Client Advisor is your main point of

contact and is responsible for your

relationship.

Your Client Advisor is directly supported by

a Deputy Client Advisor, Client Advisor

Assistant and the wider Client Advisory

Team.

You investment solution is supported by the

expertise of UBS Investment Products and

Services.

This is underpinned by the global buy-side

research capabilities of UBS Chief

Investment Office

Client

…supported by the global capabilities and resources of UBS

A single point of contact…

Client Advisor

Product Specialists / Portfolio Managers

Investment

Specialists

Lending

Specialists

Wealth

Planning

Specialists

Chief Investment Office

Client Advisory Team

Investment Products & Services

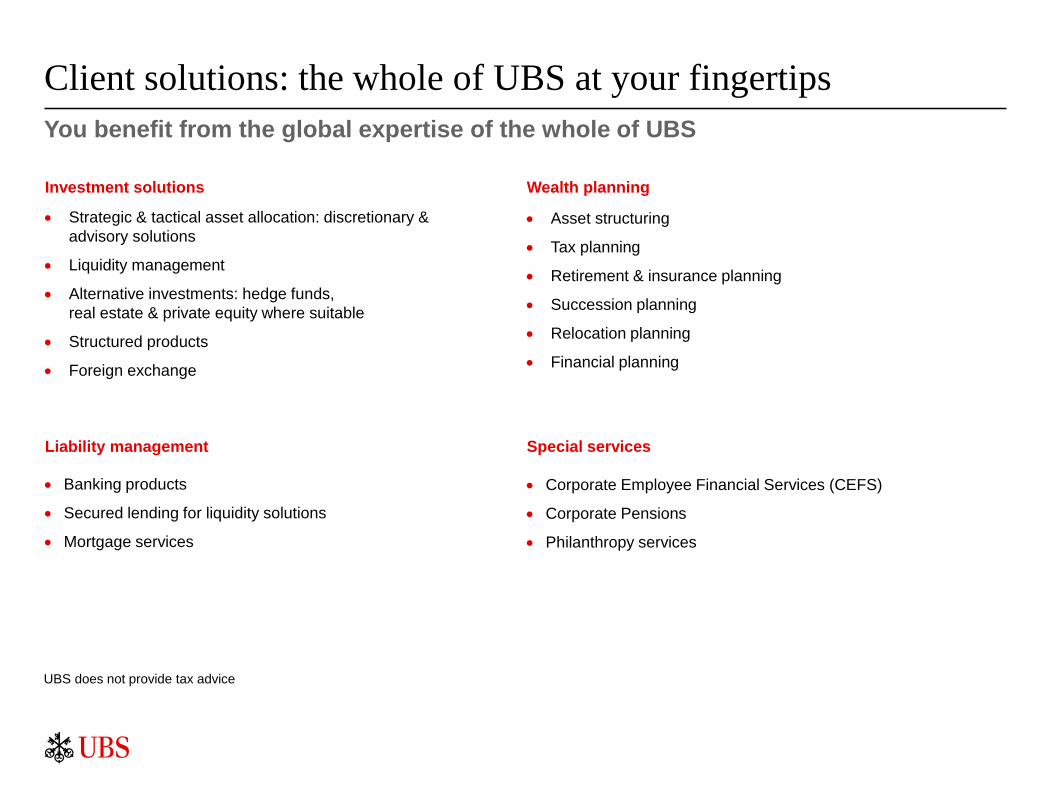

Client solutions: the whole of UBS at your fingertips

Asset structuring

Tax planning

Retirement & insurance planning

Succession planning

Relocation planning

Financial planning

Strategic & tactical asset allocation: discretionary &

advisory solutions

Liquidity management

Alternative investments: hedge funds,

real estate & private equity where suitable

Structured products

Foreign exchange

You benefit from the global expertise of the whole of UBS

Corporate Employee Financial Services (CEFS)

Corporate Pensions

Philanthropy services

Banking products

Secured lending for liquidity solutions

Mortgage services

Investment solutions Wealth planning

Liability management Special services

UBS does not provide tax advice

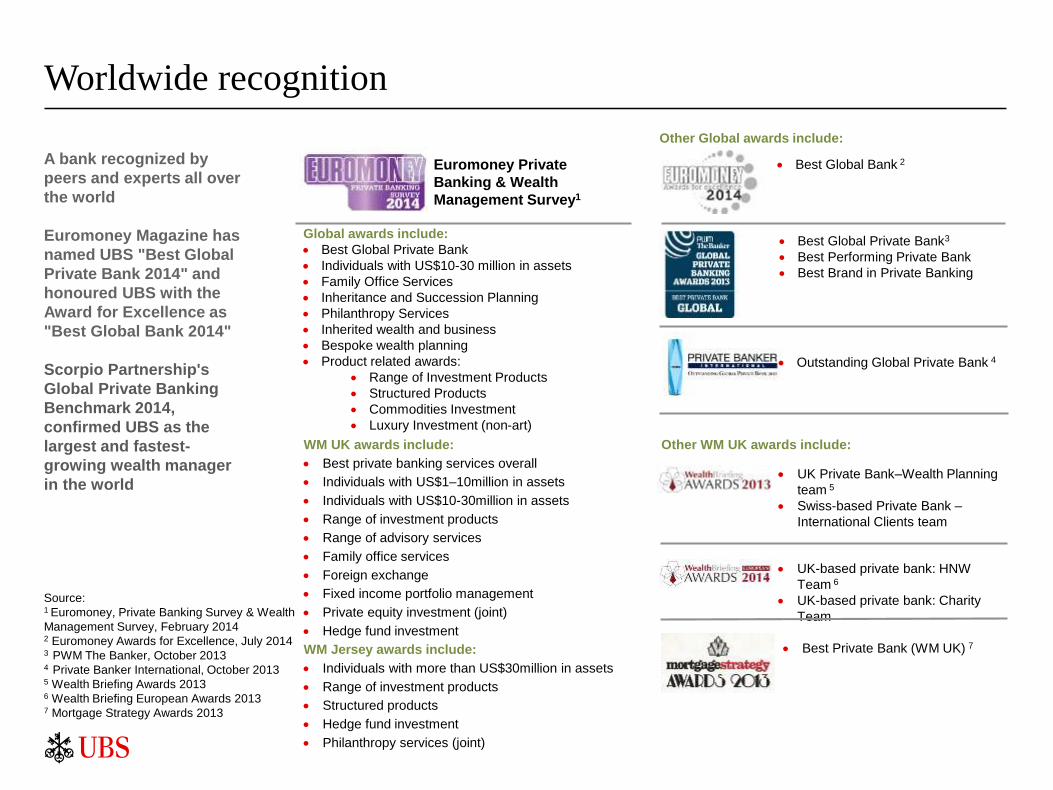

Worldwide recognition

A bank recognized by

peers and experts all over

the world

Euromoney Magazine has

named UBS "Best Global

Private Bank 2014" and

honoured UBS with the

Award for Excellence as

"Best Global Bank 2014"

Scorpio Partnership's

Global Private Banking

Benchmark 2014,

confirmed UBS as the

largest and fastest-

growing wealth manager

in the world

Euromoney Private

Banking & Wealth

Management Survey1

Global awards include:

Best Global Private Bank

Individuals with US$10-30 million in assets

Family Office Services

Inheritance and Succession Planning

Philanthropy Services

Inherited wealth and business

Bespoke wealth planning

Product related awards:

Range of Investment Products

Structured Products

Commodities Investment

Luxury Investment (non-art)

Best Global Private Bank3

Best Performing Private Bank

Best Brand in Private Banking

Outstanding Global Private Bank 4

WM UK awards include:

Best private banking services overall

Individuals with US$1–10million in assets

Individuals with US$10-30million in assets

Range of investment products

Range of advisory services

Family office services

Foreign exchange

Fixed income portfolio management

Private equity investment (joint)

Hedge fund investment

WM Jersey awards include:

Individuals with more than US$30million in assets

Range of investment products

Structured products

Hedge fund investment

Philanthropy services (joint)

Best Global Bank 2

Best Private Bank (WM UK) 7

UK Private Bank–Wealth Planning

team 5

Swiss-based Private Bank –

International Clients team

UK-based private bank: HNW

Team 6

UK-based private bank: Charity

Team

Source: 1 Euromoney, Private Banking Survey & Wealth

Management Survey, February 20142 Euromoney Awards for Excellence, July 20143 PWM The Banker, October 20134 Private Banker International, October 20135 Wealth Briefing Awards 20136 Wealth Briefing European Awards 20137 Mortgage Strategy Awards 2013

Other Global awards include:

Other WM UK awards include:

8

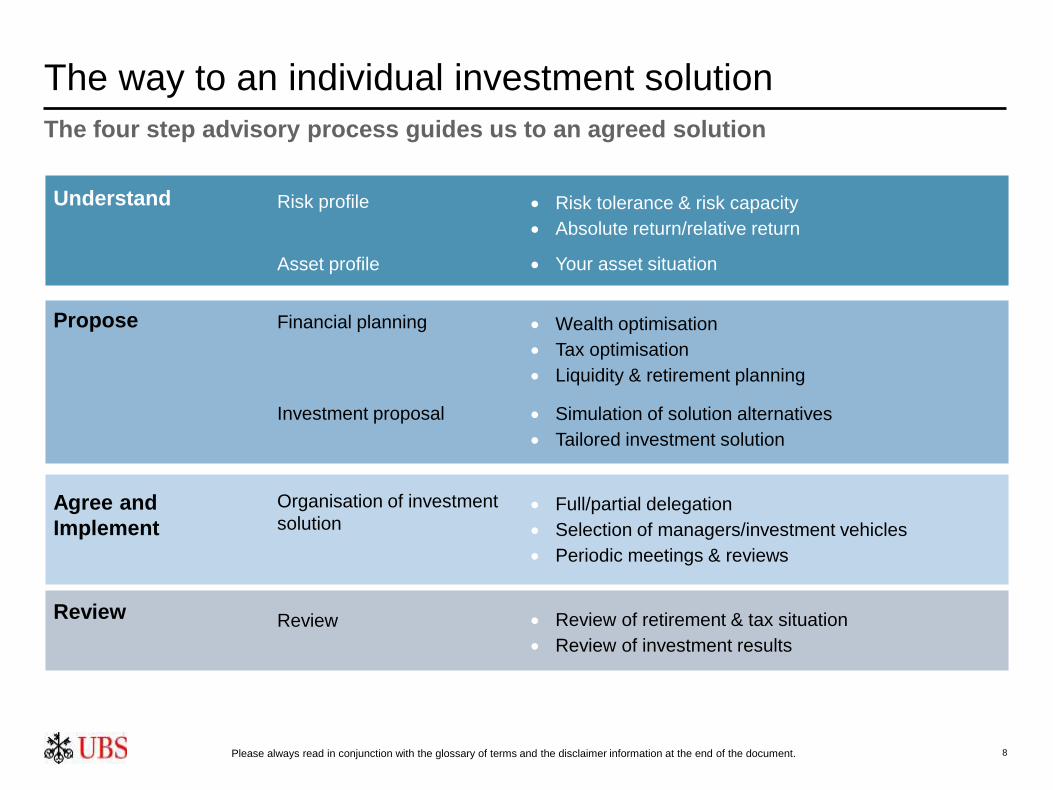

The way to an individual investment solution

Asset profile

Risk profile

Your asset situation

Risk tolerance & risk capacity

Absolute return/relative return

Financial planning

Investment proposal

Wealth optimisation

Tax optimisation

Liquidity & retirement planning

Simulation of solution alternatives

Tailored investment solution

Organisation of investment

solution Full/partial delegation

Selection of managers/investment vehicles

Periodic meetings & reviews

Review Review of retirement & tax situation

Review of investment results

Understand

Propose

Agree and

Implement

Review

The four step advisory process guides us to an agreed solution

Please always read in conjunction with the glossary of terms and the disclaimer information at the end of the document.

9

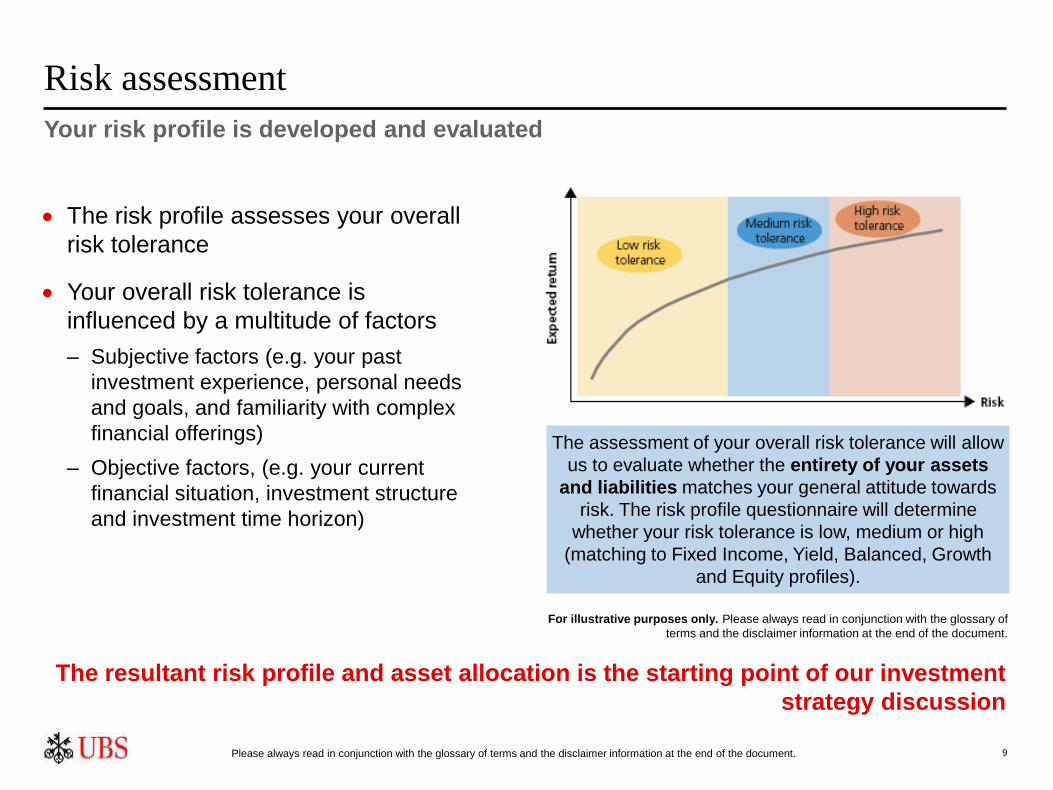

The resultant risk profile and asset allocation is the starting point of our investment

strategy discussion

The risk profile assesses your overall

risk tolerance

Your overall risk tolerance is

influenced by a multitude of factors

– Subjective factors (e.g. your past

investment experience, personal needs

and goals, and familiarity with complex

financial offerings)

– Objective factors, (e.g. your current

financial situation, investment structure

and investment time horizon)

The assessment of your overall risk tolerance will allow

us to evaluate whether the entirety of your assets

and liabilities matches your general attitude towards

risk. The risk profile questionnaire will determine

whether your risk tolerance is low, medium or high

(matching to Fixed Income, Yield, Balanced, Growth

and Equity profiles).

Risk assessment

Your risk profile is developed and evaluated

For illustrative purposes only. Please always read in conjunction with the glossary of

terms and the disclaimer information at the end of the document.

Please always read in conjunction with the glossary of terms and the disclaimer information at the end of the document.

10

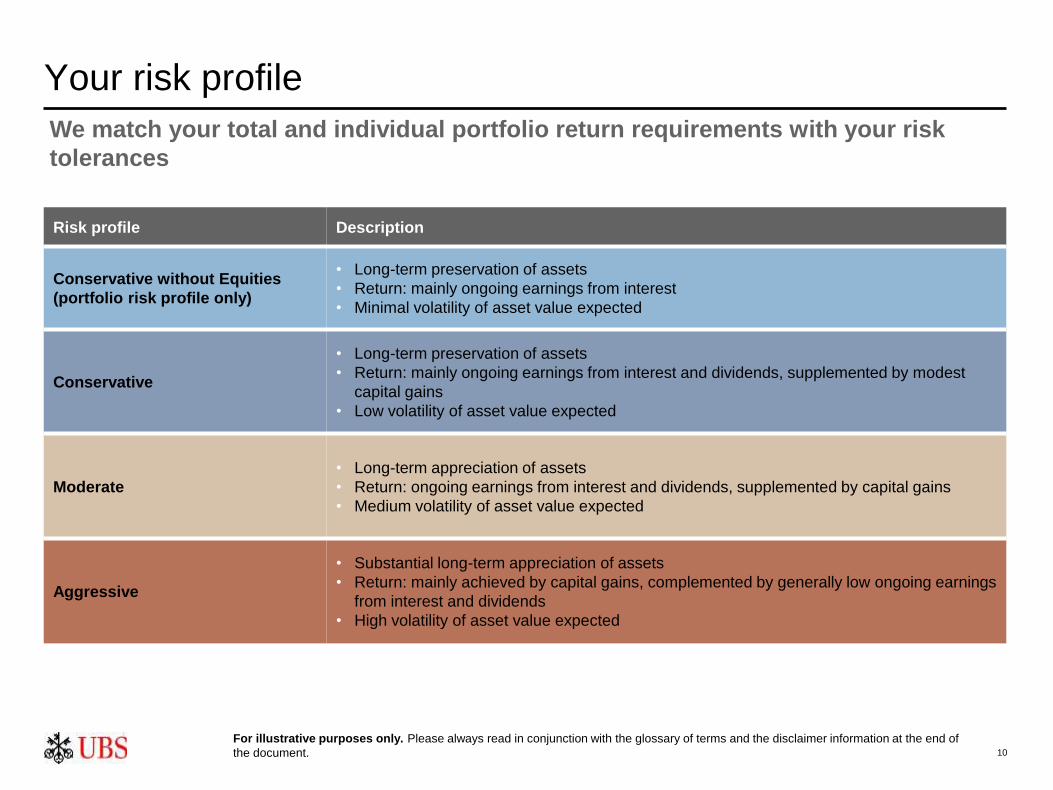

Risk profile Description

Conservative without Equities

(portfolio risk profile only)

• Long-term preservation of assets

• Return: mainly ongoing earnings from interest

• Minimal volatility of asset value expected

Conservative

• Long-term preservation of assets

• Return: mainly ongoing earnings from interest and dividends, supplemented by modest

capital gains

• Low volatility of asset value expected

Moderate

• Long-term appreciation of assets

• Return: ongoing earnings from interest and dividends, supplemented by capital gains

• Medium volatility of asset value expected

Aggressive

• Substantial long-term appreciation of assets

• Return: mainly achieved by capital gains, complemented by generally low ongoing earnings

from interest and dividends

• High volatility of asset value expected

Your risk profile

We match your total and individual portfolio return requirements with your risk

tolerances

For illustrative purposes only. Please always read in conjunction with the glossary of terms and the disclaimer information at the end of

the document.

11

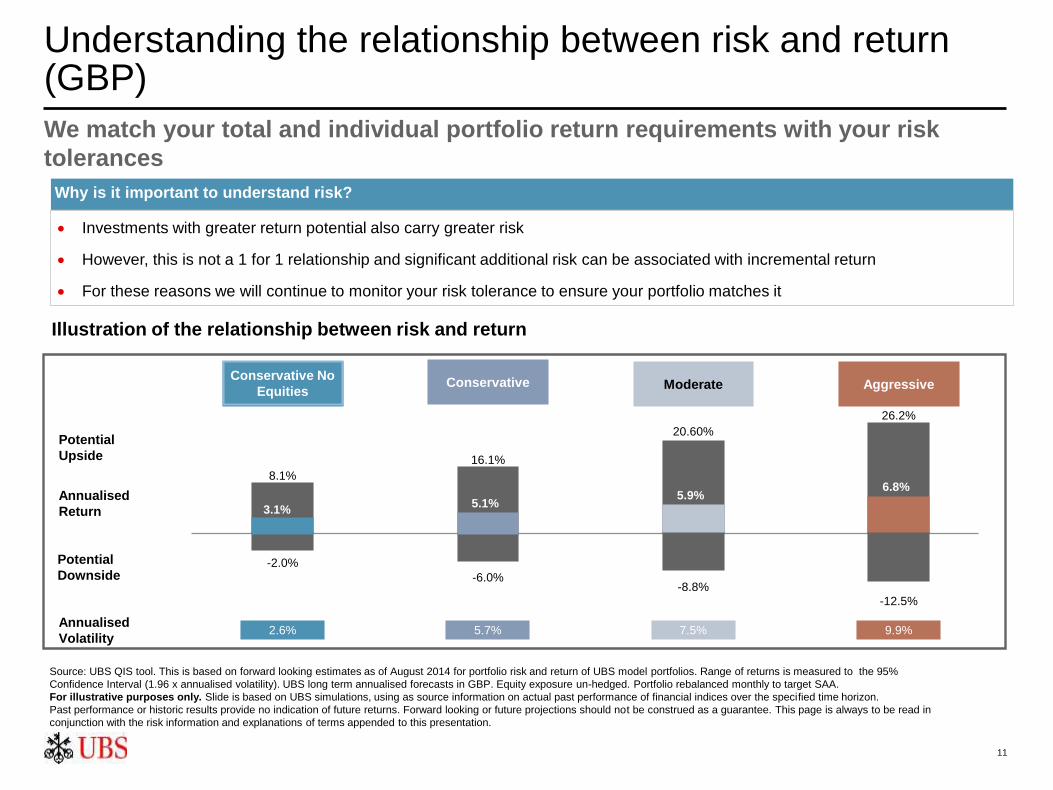

Understanding the relationship between risk and return (GBP)

We match your total and individual portfolio return requirements with your risk

tolerances

Illustration of the relationship between risk and return

Potential

Upside

Potential

Downside

Annualised

Return

Annualised

Volatility5.7%

16.1%

-6.0%

5.1%

Conservative

7.5%

20.60%

-8.8%

5.9%

Moderate

9.9%

26.2%

-12.5%

6.8%

AggressiveConservative No

Equities

2.6%

8.1%

-2.0%

3.1%

Conservative No

Equities

Source: UBS QIS tool. This is based on forward looking estimates as of August 2014 for portfolio risk and return of UBS model portfolios. Range of returns is measured to the 95%

Confidence Interval (1.96 x annualised volatility). UBS long term annualised forecasts in GBP. Equity exposure un-hedged. Portfolio rebalanced monthly to target SAA.

For illustrative purposes only. Slide is based on UBS simulations, using as source information on actual past performance of financial indices over the specified time horizon.

Past performance or historic results provide no indication of future returns. Forward looking or future projections should not be construed as a guarantee. This page is always to be read in

conjunction with the risk information and explanations of terms appended to this presentation.

Investments with greater return potential also carry greater risk

However, this is not a 1 for 1 relationship and significant additional risk can be associated with incremental return

For these reasons we will continue to monitor your risk tolerance to ensure your portfolio matches it

Why is it important to understand risk?

12

Asset allocation

Asset classes and asset allocation

Diversification

– History shows that not all asset classes move in the same direction at the same time

Risk management

– Some assets have proven to be “riskier” than others in the past

– The selected asset allocation should be matched to your perceived risk tolerance

Avoid market timing

– If an investor could predict which asset classes would do best in a specific time period there

would be no need for asset allocation

An asset class is a broad category of investments that exhibit similar sensitivities to market

conditions

Strategic asset allocation determines efficient allocations of these broad categories to suit your

investment time horizon and risk tolerance

Why is it important to have a strategic asset allocation?

Please always read in conjunction with the glossary of terms and the disclaimer information at the end of the document.

13

Diversification is critical

Diversification and a

dynamic, market-

driven investment

process are key

When analysing

historical annual

returns on various

asset classes,

differences in annual

returns become very

clear

Liquidity Real estateBonds Hedge fundsEquities Commodities

Historical annual returns of selected asset classes

2002 – 2012

Highest

return

Lowest

return

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

The best-performing asset classes change over time

For illustrative purposes only. Past performance is not an indication of future returns. Markets are subject to change and returns may vary. The above asset

classes, asset allocation and investment instruments are indicative only and can be changed at any time at UBS’ discretion. Please always read in

conjunction with the glossary of terms and the disclaimer information at the end of the document. Source: UNS Quantitative Investment Solutions.

14

Portfolio diversification

Our mandates are well diversified

and are designed to capture an optimal asset blend

Traditional asset mix Typical UBS solution

Bonds

Equities

Liquidity

Real Estate Funds

Private Equity

Sector Equity Funds

Active Equity Funds

Hedge Funds

Single Global Equities

Single Bond Holdings

Regional Equity Funds

Commodities

For illustrative purposes only. Please always read in conjunction with the glossary of terms and the disclaimer information at the end of

the document.

Corporate Bond Funds

Investment Grade Bond Funds

Liquidity

15

Open architecture – our philosophy

Why is open architecture important?

– No one investment house consistently outperforms in all asset classes

– A collection of specialists is better positioned to meet and exceed your investment goals

Flexibility and objectivity of selection:

– Our mission is to identify and secure access to the best investment management talent in

each asset class

– We are impartial to solutions offered in-house or by third parties

– We have long track-record of selecting leading managers globally

– We have significant assets invested with third party managers, giving us vast economies of

scale representing over 470 approved funds as at Dec 2010

selecting leading third party managers and funds to use in combination with our in-

house portfolio management capabilities

UBS and its subsidiaries are significant players in 'open architecture'

Please always read in conjunction with the glossary of terms and the disclaimer information at the end of the document.

Investment process

We aim to generate excess return from two complimentary sources

16

Chief Investment

Office

Investment

Management

Tactical Asset Allocation Security Selection

Bonds EquityHedge

FundsCash FX

Active

Funds

Passive

FundsEquities

Fixed

Income

Hedge

Funds

Wealth Management

Investment Bank

Asset Management

Your Portfolio

Please always read in conjunction with the glossary of terms and the risk information at the end of this presentation

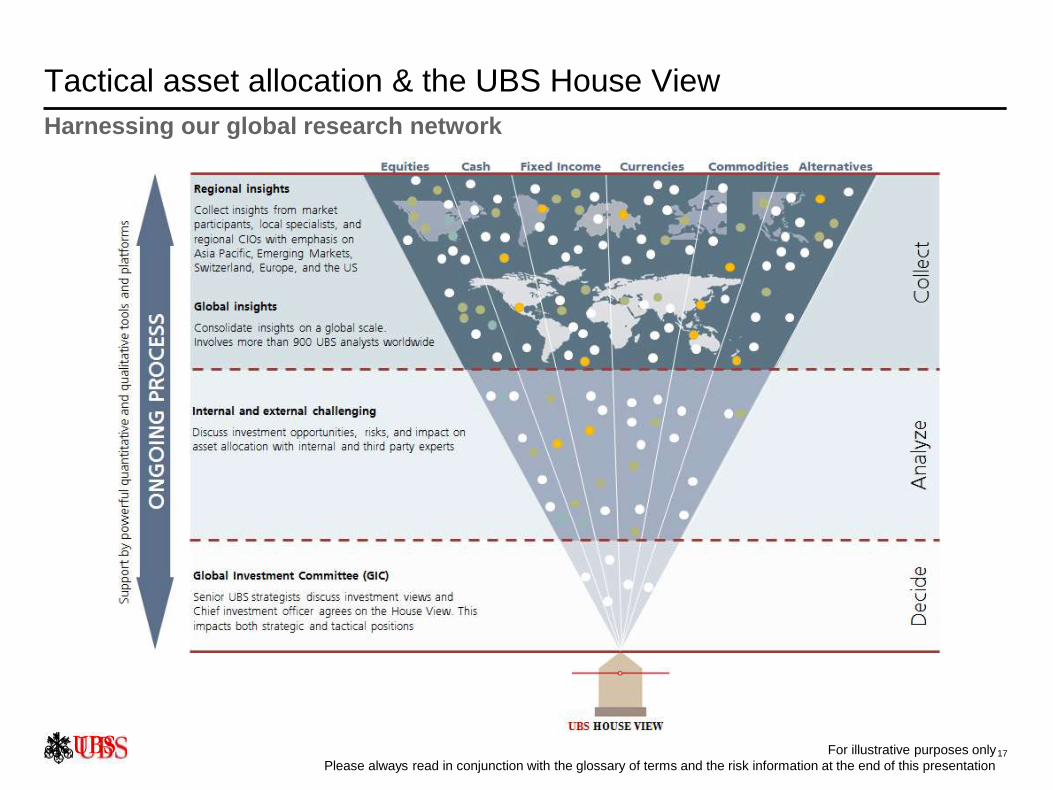

Tactical asset allocation & the UBS House View

Harnessing our global research network

17For illustrative purposes only

Please always read in conjunction with the glossary of terms and the risk information at the end of this presentation

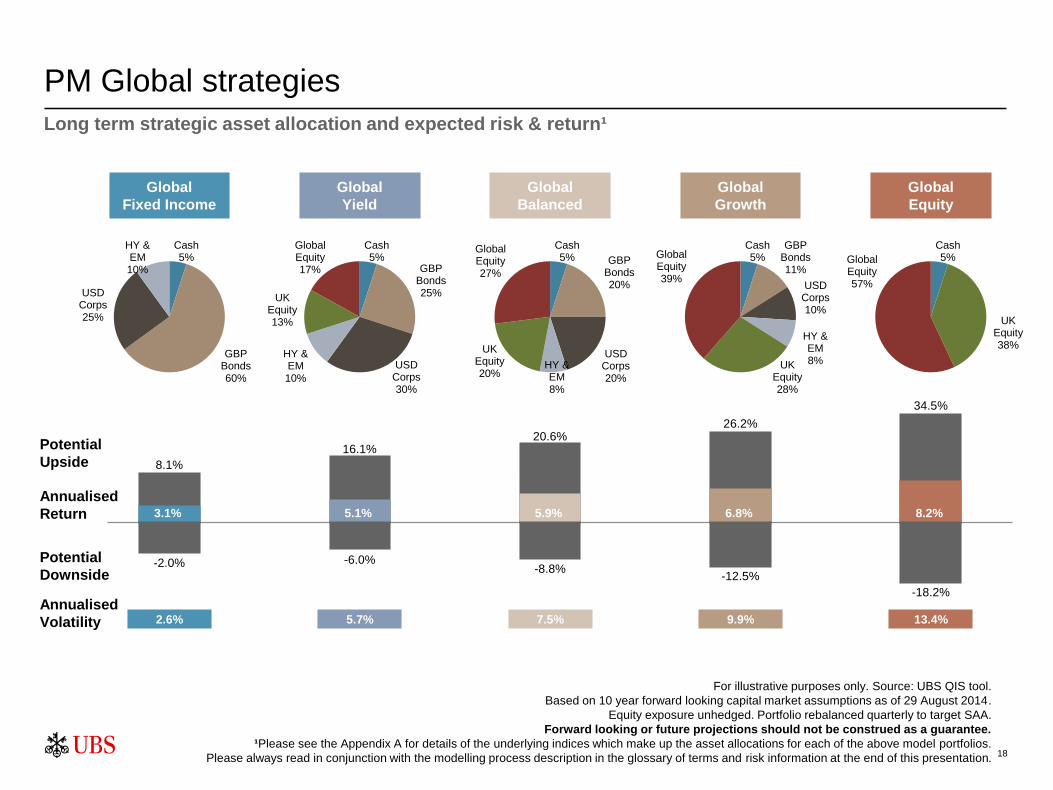

PM Global strategies

Long term strategic asset allocation and expected risk & return¹

Potential

Upside

Potential

Downside

Annualised

Return

Annualised

Volatility

Cash5%

GBP Bonds60%

USD Corps25%

HY & EM10%

2.6%

8.1%

-2.0%

Global

Fixed Income

3.1%

Cash5%

GBP Bonds25%

USD Corps30%

HY & EM10%

UK Equity13%

Global Equity17%

5.7%

16.1%

-6.0%

Global

Yield

5.1%

Cash5% GBP

Bonds20%

USD Corps20%

HY & EM8%

UK Equity20%

Global Equity27%

7.5%

20.6%

-8.8%

Global

Balanced

5.9%

Cash5%

UK Equity38%

Global Equity57%

13.4%

34.5%

-18.2%

Global

Equity

8.2%

Cash5%

GBP Bonds11%

USD Corps10%

HY & EM8%UK

Equity28%

Global Equity39%

9.9%

26.2%

-12.5%

Global

Growth

6.8%

18

For illustrative purposes only. Source: UBS QIS tool.

Based on 10 year forward looking capital market assumptions as of 29 August 2014.

Equity exposure unhedged. Portfolio rebalanced quarterly to target SAA.

Forward looking or future projections should not be construed as a guarantee.

¹Please see the Appendix A for details of the underlying indices which make up the asset allocations for each of the above model portfolios.

Please always read in conjunction with the modelling process description in the glossary of terms and risk information at the end of this presentation.

Portfolio structuring

Strategic cash advice

20

Issues/Background

Safety is your basic need: To keep what you have,

to react to unforeseen events

Cash makes you feel safe: Cash is a safe haven,

and is available at short notice

But Cash has its price: low yield

Aren’t you missing something?

Solutions

UBS can help you find out:

(1) How much you really want to keep in cash

(2) How to structure the solution addressing your

cash needs

(3) Which further opportunities exist that suit you

Benefits

+ You know that you keep the right amount in cash

+ You know you have done the right thing with the rest

Solutions

Stay in cash: safe and liquid

With daily liquidity: Current Account, Fiduciary Call, Call Deposits, MM

Certificates, Libor Accrual Certificate

For longer tenors: Fiduciary Fix, Fixed Term Deposits, Money Market

Funds or Structured Notes (e.g., Trend Accrual Bill, higher risk with higher

yield opportunities)

Create opportunities

Understand your investment goals

Look for investments that fit your needs

Überschuss-

liquidität

Iron Reserve For asset

portfolio

Consumption

cash

Excess

liquidity

Gathered cash

accounts

money market

investments

The rest,

excess liquidity!

To buy & sell

securities, wait

for market

opportunities

For critical

eventualities,

”to sleep well”

To pay daily

bills, for

planned

purchases

UBS Cash Analysis

Notes: For illustrative purposes only.

21

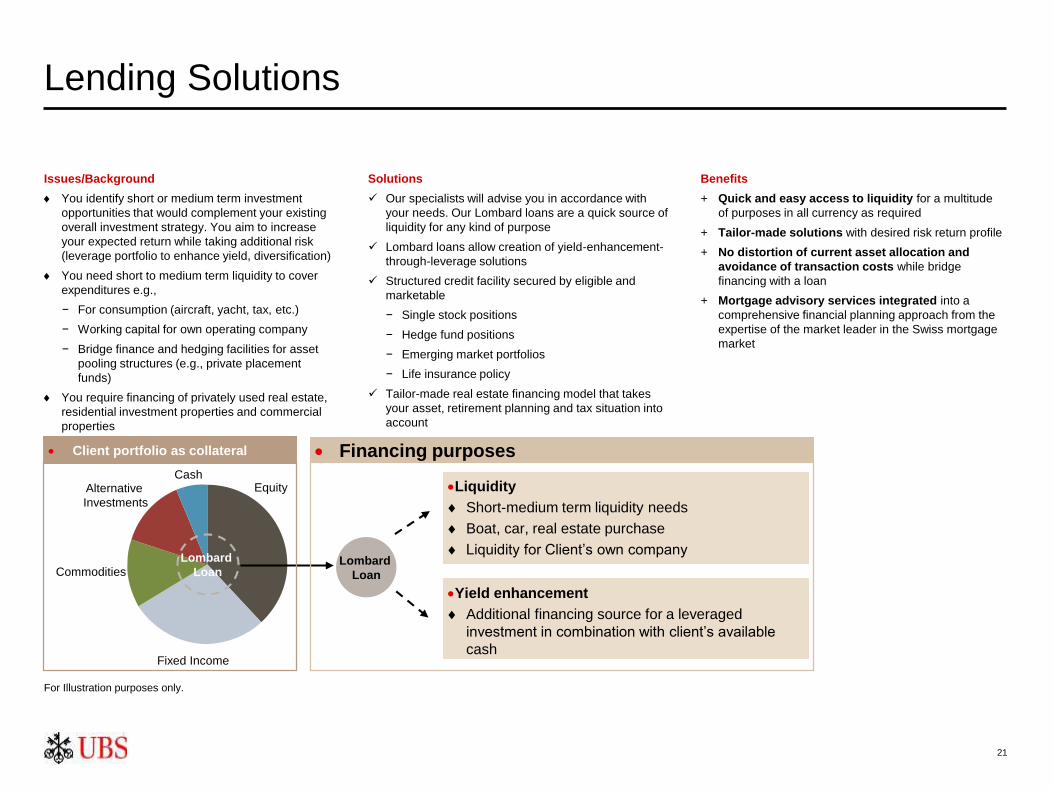

Lending Solutions

For Illustration purposes only.

Issues/Background

You identify short or medium term investment

opportunities that would complement your existing

overall investment strategy. You aim to increase

your expected return while taking additional risk

(leverage portfolio to enhance yield, diversification)

You need short to medium term liquidity to cover

expenditures e.g.,

− For consumption (aircraft, yacht, tax, etc.)

− Working capital for own operating company

− Bridge finance and hedging facilities for asset

pooling structures (e.g., private placement

funds)

You require financing of privately used real estate,

residential investment properties and commercial

properties

Solutions

Our specialists will advise you in accordance with

your needs. Our Lombard loans are a quick source of

liquidity for any kind of purpose

Lombard loans allow creation of yield-enhancement-

through-leverage solutions

Structured credit facility secured by eligible and

marketable

− Single stock positions

− Hedge fund positions

− Emerging market portfolios

− Life insurance policy

Tailor-made real estate financing model that takes

your asset, retirement planning and tax situation into

account

Benefits

+ Quick and easy access to liquidity for a multitude

of purposes in all currency as required

+ Tailor-made solutions with desired risk return profile

+ No distortion of current asset allocation and

avoidance of transaction costs while bridge

financing with a loan

+ Mortgage advisory services integrated into a

comprehensive financial planning approach from the

expertise of the market leader in the Swiss mortgage

market

Lombard

Loan

CashEquity

Fixed Income

Commodities

Alternative

Investments

Liquidity

Short-medium term liquidity needs

Boat, car, real estate purchase

Liquidity for Client’s own company

Yield enhancement

Additional financing source for a leveraged

investment in combination with client’s available

cash

Client portfolio as collateral Financing purposes

Lombard

Loan

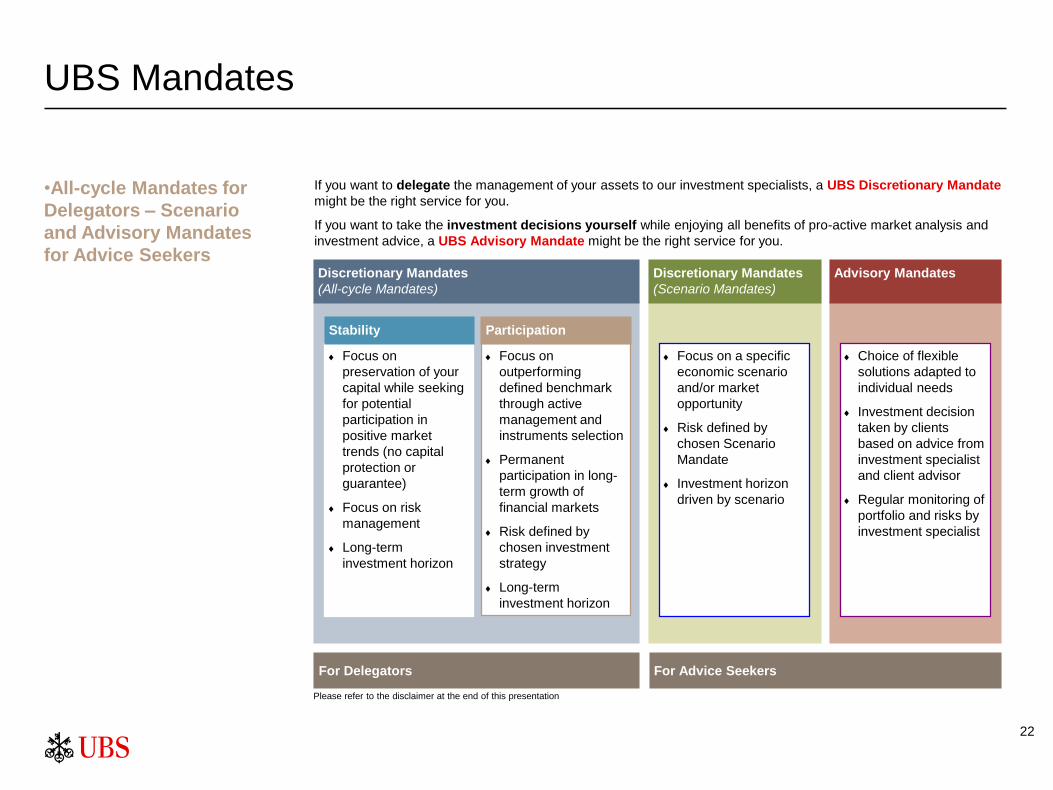

UBS Mandates

22

•All-cycle Mandates for

Delegators – Scenario

and Advisory Mandates

for Advice Seekers

If you want to delegate the management of your assets to our investment specialists, a UBS Discretionary Mandate

might be the right service for you.

If you want to take the investment decisions yourself while enjoying all benefits of pro-active market analysis and

investment advice, a UBS Advisory Mandate might be the right service for you.

Focus on

preservation of your

capital while seeking

for potential

participation in

positive market

trends (no capital

protection or

guarantee)

Focus on risk

management

Long-term

investment horizon

Focus on

outperforming

defined benchmark

through active

management and

instruments selection

Permanent

participation in long-

term growth of

financial markets

Risk defined by

chosen investment

strategy

Long-term

investment horizon

Stability Participation

Discretionary Mandates

(All-cycle Mandates)

Discretionary Mandates

(Scenario Mandates)

Focus on a specific

economic scenario

and/or market

opportunity

Risk defined by

chosen Scenario

Mandate

Investment horizon

driven by scenario

Advisory Mandates

Choice of flexible

solutions adapted to

individual needs

Investment decision

taken by clients

based on advice from

investment specialist

and client advisor

Regular monitoring of

portfolio and risks by

investment specialist

For Delegators For Advice Seekers

Please refer to the disclaimer at the end of this presentation

23

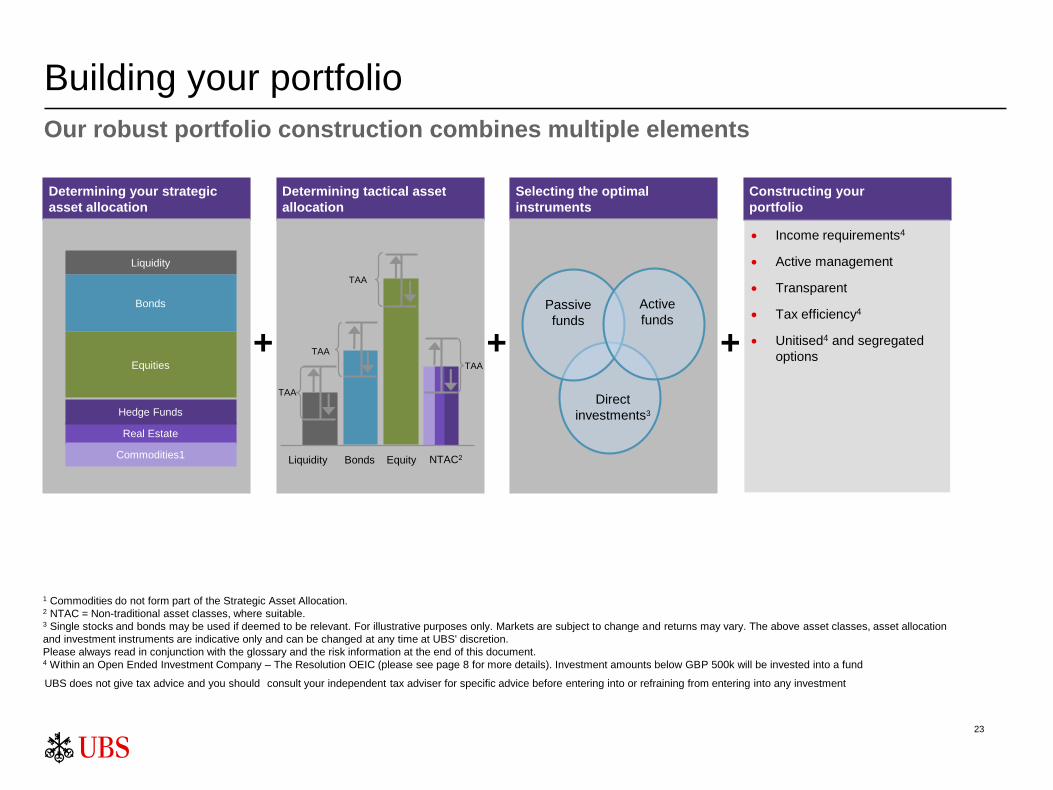

Building your portfolio

Our robust portfolio construction combines multiple elements

1 Commodities do not form part of the Strategic Asset Allocation. 2 NTAC = Non-traditional asset classes, where suitable. 3 Single stocks and bonds may be used if deemed to be relevant. For illustrative purposes only. Markets are subject to change and returns may vary. The above asset classes, asset allocation

and investment instruments are indicative only and can be changed at any time at UBS' discretion.

Please always read in conjunction with the glossary and the risk information at the end of this document.4 Within an Open Ended Investment Company – The Resolution OEIC (please see page 8 for more details). Investment amounts below GBP 500k will be invested into a fund

Selecting the optimal

instruments

Constructing your

portfolio

Determining your strategic

asset allocation

Determining tactical asset

allocation

Income requirements4

Active management

Transparent

Tax efficiency4

Unitised4 and segregated

options

Liquidity

Equities

Real Estate

Hedge Funds

Commodities1

Bonds

+ + +

Liquidity Bonds Equity NTAC2

TAA

TAA

TAA

TAA

Direct

investments3

Passive

funds

Active

funds

UBS does not give tax advice and you should consult your independent tax adviser for specific advice before entering into or refraining from entering into any investment

Portfolio structure

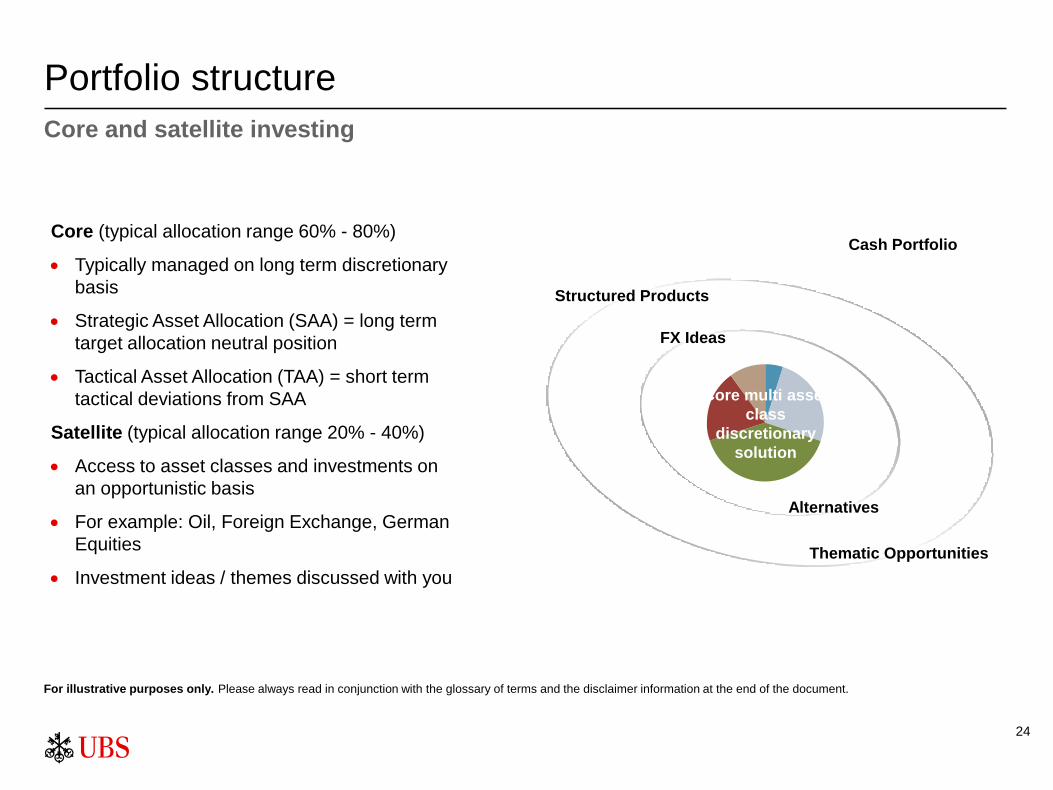

24

Core and satellite investing

Core (typical allocation range 60% - 80%)

Typically managed on long term discretionary

basis

Strategic Asset Allocation (SAA) = long term

target allocation neutral position

Tactical Asset Allocation (TAA) = short term

tactical deviations from SAA

Satellite (typical allocation range 20% - 40%)

Access to asset classes and investments on

an opportunistic basis

For example: Oil, Foreign Exchange, German

Equities

Investment ideas / themes discussed with you

Core / Satellite Objectives Illustrative Strategy

Core multi asset

class

discretionary

solution

FX Ideas

Structured Products

Thematic Opportunities

Alternatives

Cash Portfolio

For illustrative purposes only. Please always read in conjunction with the glossary of terms and the disclaimer information at the end of the document.

25

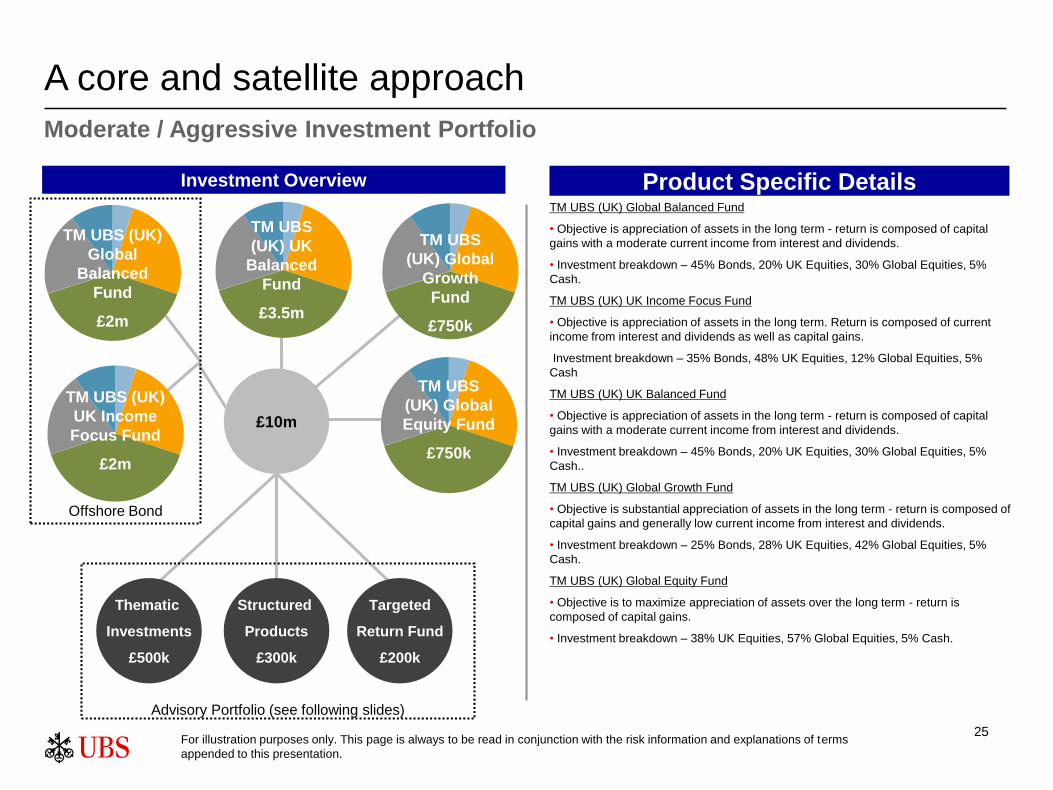

A core and satellite approach

Product Specific Details

For illustration purposes only. This page is always to be read in conjunction with the risk information and explanations of terms

appended to this presentation.

Moderate / Aggressive Investment Portfolio

Structured

Products

£300k

£10m

Investment Overview

TM UBS (UK) Global Balanced Fund

• Objective is appreciation of assets in the long term - return is composed of capital

gains with a moderate current income from interest and dividends.

• Investment breakdown – 45% Bonds, 20% UK Equities, 30% Global Equities, 5%

Cash.

TM UBS (UK) UK Income Focus Fund

• Objective is appreciation of assets in the long term. Return is composed of current

income from interest and dividends as well as capital gains.

Investment breakdown – 35% Bonds, 48% UK Equities, 12% Global Equities, 5%

Cash

TM UBS (UK) UK Balanced Fund

• Objective is appreciation of assets in the long term - return is composed of capital

gains with a moderate current income from interest and dividends.

• Investment breakdown – 45% Bonds, 20% UK Equities, 30% Global Equities, 5%

Cash..

TM UBS (UK) Global Growth Fund

• Objective is substantial appreciation of assets in the long term - return is composed of

capital gains and generally low current income from interest and dividends.

• Investment breakdown – 25% Bonds, 28% UK Equities, 42% Global Equities, 5%

Cash.

TM UBS (UK) Global Equity Fund

• Objective is to maximize appreciation of assets over the long term - return is

composed of capital gains.

• Investment breakdown – 38% UK Equities, 57% Global Equities, 5% Cash.

Discretionary

portfolios x 2

(Fixed Income

& Global

Yield)

£

Discretionary

portfolios x 2

(Fixed Income

TM UBS (UK)

UK Income

Focus Fund

£2m

TM UBS (UK)

Global

Balanced

Fund

£2m

Offshore Bond

TM UBS

(UK) Global

Equity Fund

£750k

TM UBS

(UK) Global

Growth

Fund

£750k

Thematic

Investments

£500k

Targeted

Return Fund

£200k

Advisory Portfolio (see following slides)

TM UBS

(UK) UK

Balanced

Fund

£3.5m

26

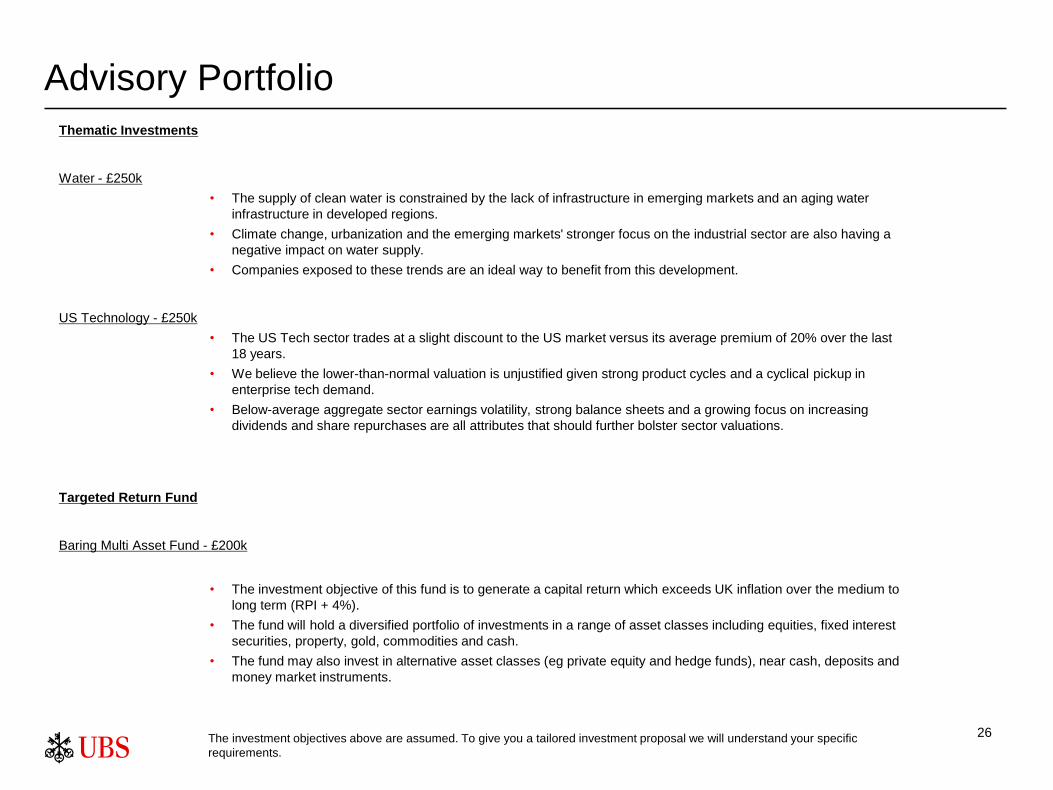

Advisory Portfolio

The investment objectives above are assumed. To give you a tailored investment proposal we will understand your specific

requirements.

Thematic Investments

Water - £250k

• The supply of clean water is constrained by the lack of infrastructure in emerging markets and an aging water

infrastructure in developed regions.

• Climate change, urbanization and the emerging markets' stronger focus on the industrial sector are also having a

negative impact on water supply.

• Companies exposed to these trends are an ideal way to benefit from this development.

US Technology - £250k

• The US Tech sector trades at a slight discount to the US market versus its average premium of 20% over the last

18 years.

• We believe the lower-than-normal valuation is unjustified given strong product cycles and a cyclical pickup in

enterprise tech demand.

• Below-average aggregate sector earnings volatility, strong balance sheets and a growing focus on increasing

dividends and share repurchases are all attributes that should further bolster sector valuations.

Targeted Return Fund

Baring Multi Asset Fund - £200k

• The investment objective of this fund is to generate a capital return which exceeds UK inflation over the medium to

long term (RPI + 4%).

• The fund will hold a diversified portfolio of investments in a range of asset classes including equities, fixed interest

securities, property, gold, commodities and cash.

• The fund may also invest in alternative asset classes (eg private equity and hedge funds), near cash, deposits and

money market instruments.

27

Advisory Portfolio

The investment objectives above are assumed. To give you a tailored investment proposal we will understand your specific

requirements.

Structured Products

UBS 4 Year Step Down linked to US and Canadian Equities - £150k

• Linked to S&P 500 and TSX 60 (Toronto Stock Exchange).

• Autocall levels 100% of strikes year 1, 95% year 2, 90% year 3 and 85% year 4.

• Current indicative coupon 8.5% per annum.

• 65% European capital protection barrier.

• Note subject to capital gains tax.

• Issued by UBS AG, Jersey.

Goldman Sachs 4 Year Defensive Autocallable Note Linked to UK, US and European Equities - £150k

• Linked to FTSE 100, S&P 500 and Eurostoxx 50.

• Autocall levels 100% of strikes year 1-3, 60% in year 4.

• Current indicative coupon 8.5% per annum.

• 60% European capital protection barrier.

• Note subject to capital gains tax.

• Issued by Goldman, Sachs & Co. Wertpapier GmBH, Frankfurt, Germany.

Glossary of terms (1 of 2)

Alpha: excess return over a benchmark.

Alternative Investments: are non-traditional investments which do not fall within the traditional asset classes such as equities, bonds or money market products.

Alternative investments include hedge funds, private equity, real estate and commodities and are often referred to as non-traditional asset classes (NTAC). Such

investments might have higher levels of risk than traditional investments, including (but not limited to), higher volatility, illiquidity, complexity and a lack of

transparency.

Annualised Return is a compound annual growth rate.

Asset Allocation: composition of a portfolio by currency and asset class.

Benchmark: reference parameter (e.g. a share index or a portfolio of indices) to compare the performance of a portfolio. A benchmark that is an index is also called

a reference index.

Corporate Bonds: combination of higher duration risk (1-10 year maturity) and credit risk (BBB rated and above) makes this our highest yielding bond investment

strategy.

Customised: mix of single line bond strategies (Conservative, Short-dated Corporates and Corporate) along with fund selection across Investment grade, High

Yield and Emerging markets.

EMMA: emerging markets, which may offer higher levels of risk and return than more developed investment markets.

Equity Risk Premia: The additional return an investor expects to compensate for the additional risk associated with investing in equities as opposed to investing in a

riskless asset (typically investment grade government bonds).

Expected Return Estimates: Using statistical methods, UBS estimates long-term average risk/return figures for all major asset classes and their behaviour in given

model portfolios. Investors should note that these figures are derived from estimated long-term asset class performances and do not account for the content of

individual portfolios nor of the performance of individual securities or active management. Active management may result in higher or lower future performance.

Unless stated, transaction costs and portfolio fees are not included and these will reduce future performance accordingly. They indicate the statistically most likely

performance from a range of possible outcomes and investors should not base their investment decision solely on the estimates above. Estimated annual

performance and annual risk are not reliable indicators of future performance and future risk. Estimates are based on our current assessment of financial markets

and are therefore subject to change. Short-term performance can deviate substantially from these estimates.

GBP Bonds: Sterling denominated bonds rated AA+ or better with maturities of up to 10 years.

28

Glossary of terms (2 of 2)

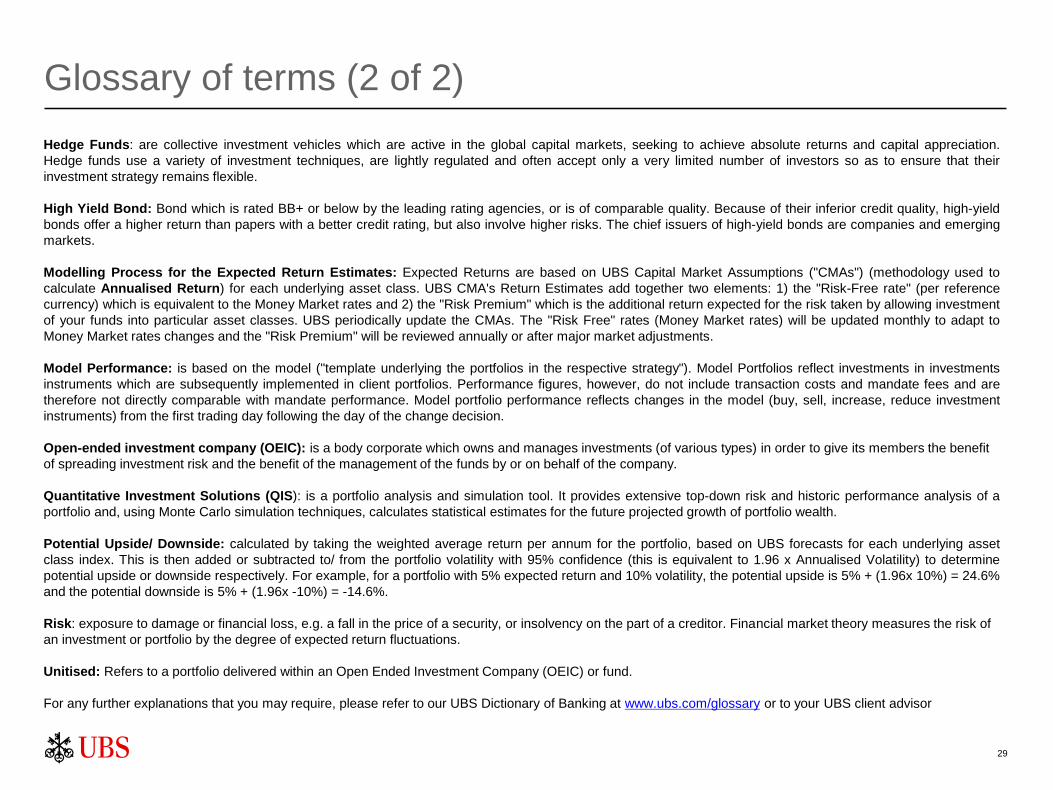

Hedge Funds: are collective investment vehicles which are active in the global capital markets, seeking to achieve absolute returns and capital appreciation.

Hedge funds use a variety of investment techniques, are lightly regulated and often accept only a very limited number of investors so as to ensure that their

investment strategy remains flexible.

High Yield Bond: Bond which is rated BB+ or below by the leading rating agencies, or is of comparable quality. Because of their inferior credit quality, high-yield

bonds offer a higher return than papers with a better credit rating, but also involve higher risks. The chief issuers of high-yield bonds are companies and emerging

markets.

Modelling Process for the Expected Return Estimates: Expected Returns are based on UBS Capital Market Assumptions ("CMAs") (methodology used to

calculate Annualised Return) for each underlying asset class. UBS CMA's Return Estimates add together two elements: 1) the "Risk-Free rate" (per reference

currency) which is equivalent to the Money Market rates and 2) the "Risk Premium" which is the additional return expected for the risk taken by allowing investment

of your funds into particular asset classes. UBS periodically update the CMAs. The "Risk Free" rates (Money Market rates) will be updated monthly to adapt to

Money Market rates changes and the "Risk Premium" will be reviewed annually or after major market adjustments.

Model Performance: is based on the model ("template underlying the portfolios in the respective strategy"). Model Portfolios reflect investments in investments

instruments which are subsequently implemented in client portfolios. Performance figures, however, do not include transaction costs and mandate fees and are

therefore not directly comparable with mandate performance. Model portfolio performance reflects changes in the model (buy, sell, increase, reduce investment

instruments) from the first trading day following the day of the change decision.

Open-ended investment company (OEIC): is a body corporate which owns and manages investments (of various types) in order to give its members the benefit

of spreading investment risk and the benefit of the management of the funds by or on behalf of the company.

Quantitative Investment Solutions (QIS): is a portfolio analysis and simulation tool. It provides extensive top-down risk and historic performance analysis of a

portfolio and, using Monte Carlo simulation techniques, calculates statistical estimates for the future projected growth of portfolio wealth.

Potential Upside/ Downside: calculated by taking the weighted average return per annum for the portfolio, based on UBS forecasts for each underlying asset

class index. This is then added or subtracted to/ from the portfolio volatility with 95% confidence (this is equivalent to 1.96 x Annualised Volatility) to determine

potential upside or downside respectively. For example, for a portfolio with 5% expected return and 10% volatility, the potential upside is 5% + (1.96x 10%) = 24.6%

and the potential downside is 5% + (1.96x -10%) = -14.6%.

Risk: exposure to damage or financial loss, e.g. a fall in the price of a security, or insolvency on the part of a creditor. Financial market theory measures the risk of

an investment or portfolio by the degree of expected return fluctuations.

Unitised: Refers to a portfolio delivered within an Open Ended Investment Company (OEIC) or fund.

For any further explanations that you may require, please refer to our UBS Dictionary of Banking at www.ubs.com/glossary or to your UBS client advisor

29

DisclaimerThis document is issued by UBS Wealth Management, a division of UBS AG which is authorised and regulated by the Financial Market Supervisory Authority inSwitzerland. In the United Kingdom, UBS AG is authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authorityand limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from uson request. Where products or services are provided from outside the UK, they will not be covered by the UK regulatory regime or the Financial ServicesCompensation Scheme.

UBS AG, Jersey Branch is authorised and regulated by the Jersey Financial Services Commission for the conduct of banking, funds and investment business.Where services are provided from outside Jersey, they will not be covered by the Jersey regulatory regime. UBS AG, Jersey Branch and UBS AG, London Branch(which is registered as a branch in England and Wales Branch No. BR004507) are both branches of UBS AG a public company limited by shares, incorporated inSwitzerland whose registered offices are at Aeschenvorstadt 1, CH-4051 Basel and Bahnhofstrasse 45, CH 8001 Zurich. UBS AG, Jersey Branch's principal placebusiness is P.O. Box 350, 24 Union Street, St Helier, Jersey JE4 8UJ.

This presentation has been prepared solely for information purposes and is based upon opinions which reflect our current views but which may be liable to change,and upon sources believed to be reliable. It is for your information only and is not intended as a recommendation, an offer, or a solicitation of an offer, to buy or sellany investment or other specific product. Although all information and opinions expressed in this document were obtained from sources believed to be reliable andin good faith, no representation or warranty, express or implied, is made as to its accuracy or completeness. All information and opinions as well as any pricesindicated are subject to change without notice and the asset classes, the asset allocation and the investment instruments are only indicative.

In accordance with the Financial Conduct Authority requirements, we should point out that with regard to any investments mentioned, values may fall as well as riseand you may not get back the original amount invested. It should be noted that past performance is not a reliable indication of future returns.

At any time UBS AG ("UBS") and other companies in the UBS group (or employees thereof) may have a long or short position, or deal as principal or agent, inrelevant securities or provide advisory or other services to the issuer of relevant securities or to a company connected with an issuer. Some investments may not bereadily realisable since the market in the securities is illiquid and therefore valuing the investment and identifying the risk to which you are exposed may be difficultto quantify. Futures and options trading as well as alternative investments are considered risky. Some investments may be subject to sudden and large falls in valueand on realisation you may receive back less than you invested or may be required to pay more. Changes in FX rates may have an adverse effect on the price,value or income of an investment. Furthermore, performance information may be based on simulations and/or be for illustration only. We would recommend that youtake financial and/or legal advice as to the implications of investing in any of the products mentioned herein, including tax matters. Alternative investment funds areunregulated collective investment schemes under the UK regulations. As such, they have their own specific risks. They may only be proposed to private clients forwhom they are suitable.

When investing in the TM UBS (UK) fund range clients are purchasing the discretionary portfolio management service of UBS WM UK. The discretionary service isavailable in both a fund structure and a segregated portfolio format. The TM UBS (UK) fund range is an Open-Ended Investment Company (OEIC). In respect ofthe TM UBS (UK) fund range, UBS Wealth Management is acting as the Investment Manager and Thesis Unit Trust Management Limited is acting as theAuthorised Corporate Director (ACD). The ACD is the corporate body and authorised person given powers and duties under FCA regulations to operate an OEIC.UBS Wealth Management and Thesis Unit Trust Management Limited are authorised and regulated by the Financial Conduct Authority (FCA).

UBS does not provide tax advice. This document may not be reproduced or copies circulated without prior authority of UBS. This document is not intended fordistribution into the US and / or to US persons or in jurisdictions where its distribution by us would be restricted.

© UBS 2014. The key symbol and UBS are registered and/or unregistered trademarks of UBS. All rights reserved.

30