25

! " February 1, 2018 ULI Cleveland

! "

February 1, 2018 ULI Cleveland

# REAL ESTATE FORECASTS FROM OTHERS o MULTIFAMILY o COMMERCIAL o RETAIL o INDUSTRIAL

# RESULTS OF ULI TRENDS SURVEY

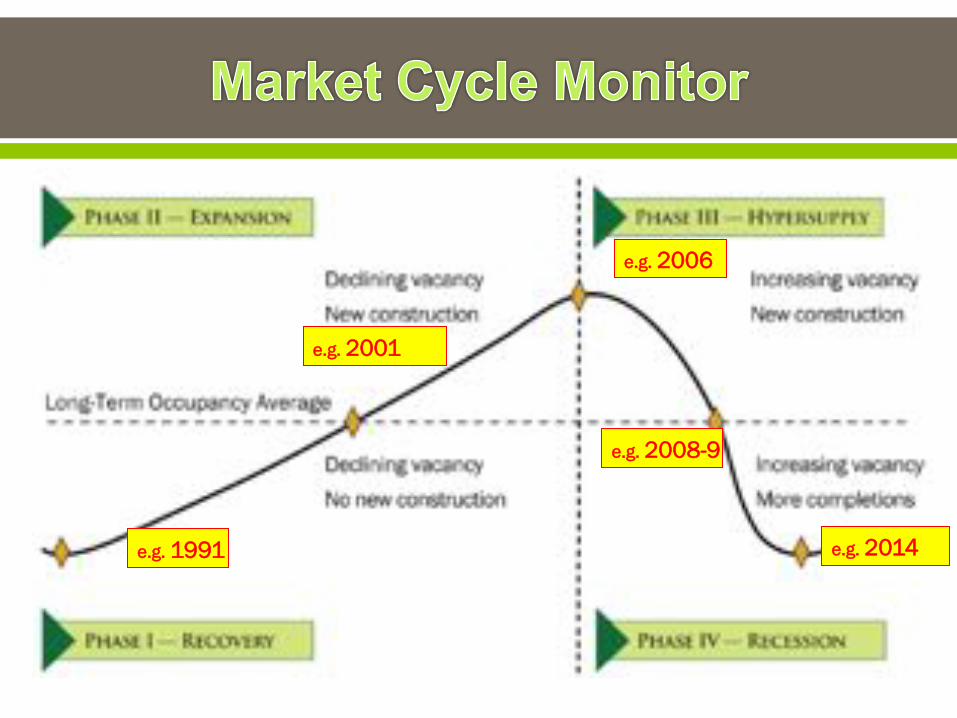

! Longer view: since @1970; recessions in 1974 (oil shock) 1979-1981 (more oil and stagflation ) 1982 (double dip); 1986-1989 (real estate only – tax code driven); 1991 (economic exhaustion) and 2001 (9-11)

! Expansion from 2002 until 2007-2008 recession (Financial rules and liquidity driven, FNMA, FMC, AIG)

! 7 recessions in 47 years=A recession every 6.6 years.

! Since 1999=average cycle: 2 recessions in 17 years

! It’s been 9 years since beginning of last recession

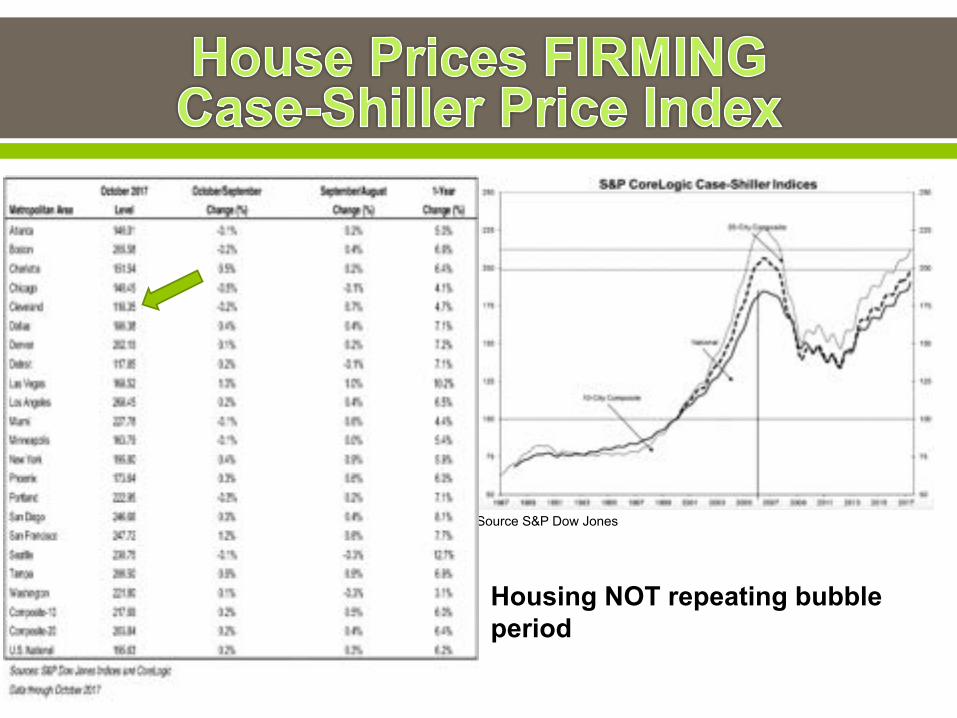

! Housing construction leads us out of a recession: NOT!

Homebuilding in the U.S. has traditionally led the country out of recessions

Expect slow recovery as housing supply and demand re-equilibrate

Source S&P Dow Jones

Housing NOT repeating bubble period

BUT DEFAULTS HAVE LESSENED PEOPLES’ DESIRE TO OWN A HOME, EVEN IF THEIR CREDIT HAS BEEN FIXED

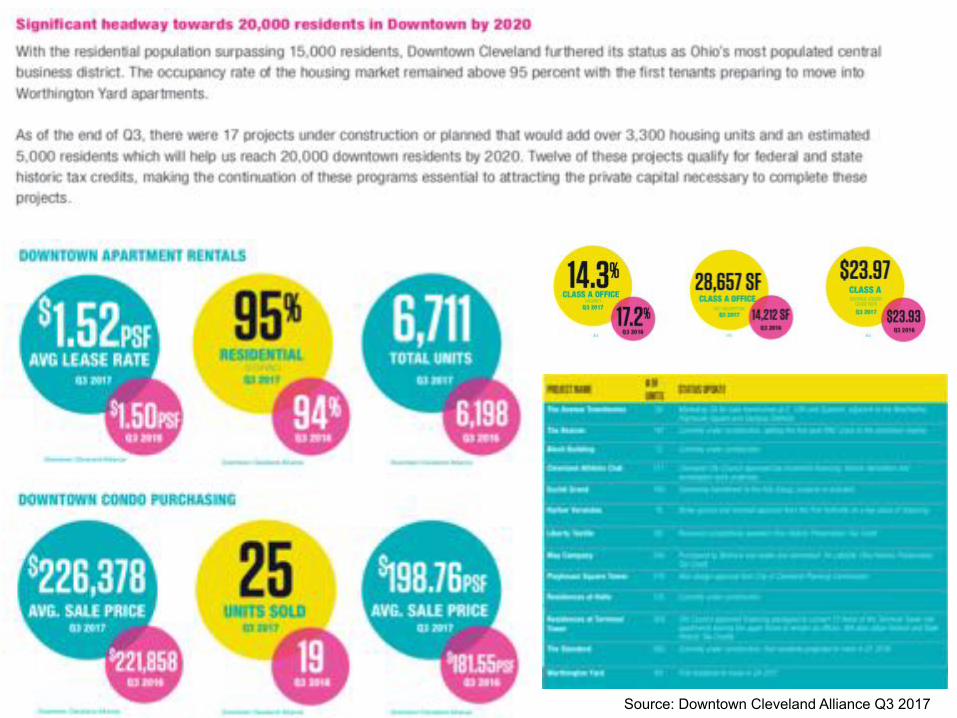

Source: Downtown Cleveland Alliance Q3 2017

e.g. 2001

e.g. 2006

e.g. 2008-9

e.g. 2014 e.g. 1991

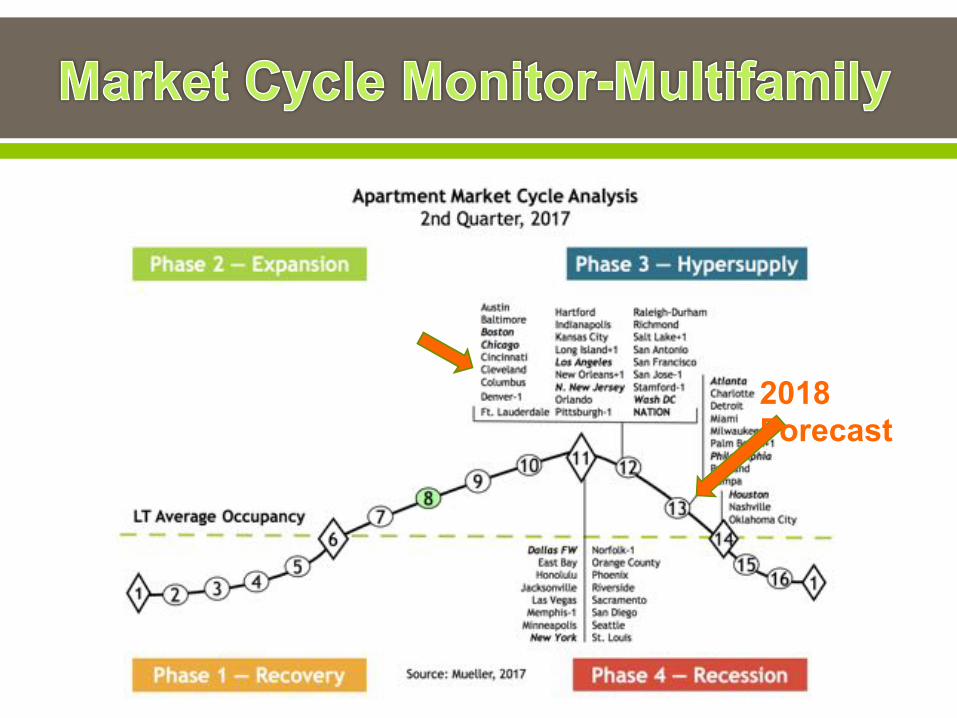

2018 Forecast

EXECUTIVE SUMMARY

Prepared by Robert Simons, Ph.D. Alexandra Malkin

Levin College of Urban Affairs Cleveland State University

Prepared for ULI Cleveland February, 2018

# Takes the pulse of the region’s real estate market, including capital markets, various property types, and geographic submarkets.

# Survey complements the national PWC/Urban Land Institute’s Emerging Trends in Real Estate, adding in-depth local perspective.

# In September, 2017, ULI Cleveland distributed a link to an online survey to its e-mail contact list. The survey was available online between September 20 and October 25, 2017 and 77 non-random responses were collected, a response rate of about 9%. Additionally, 16 in-person interviews were conducted with key local experts from the private and public sectors across a range of professional disciplines, in particular real estate development, management, finance, and planning.

# Generally, the Cleveland and Northeast Ohio RE market is good ,and consensus is about the same next year.

# Respondents expect to see a good profitability in real estate businesses in 2018, especially in multifamily, with a focus on townhomes

# The most important financial issues for real estate investment and development in 2018 will be: o job, income and wage growth, follow closely by o interest rates, inflation, and o state and local budget problems.

# The top potential needs for land development are o more economic growth (a greater demand for real estate), o infrastructure, more workforce for construction and skilled trades, and o better transportation.

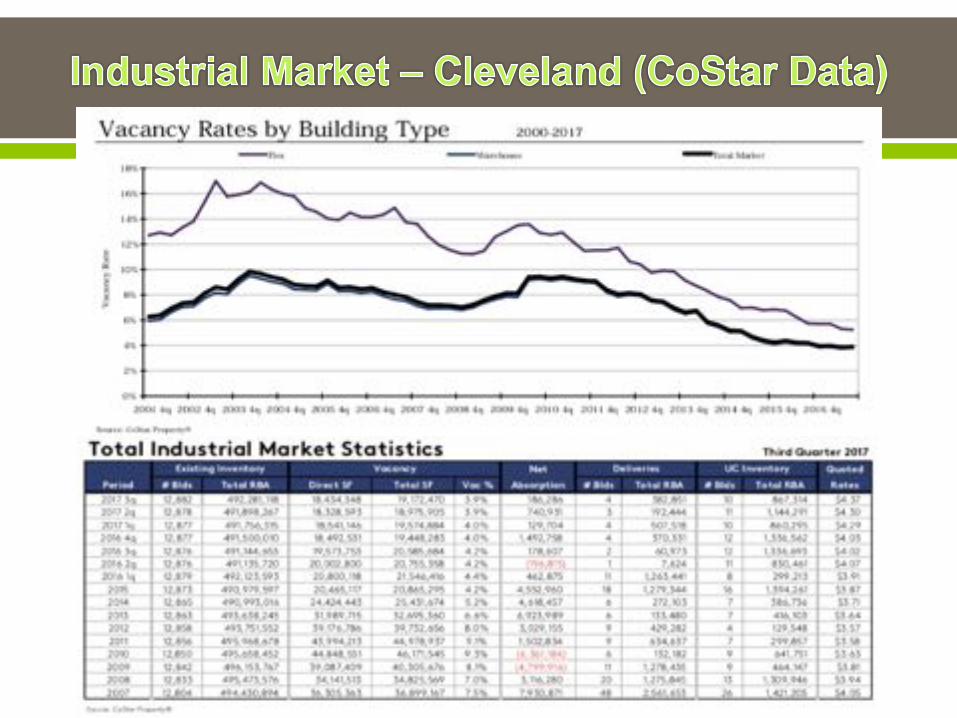

# Residential rental and office sectors are still strong, even with a little decline, especially in residential-rental. The industrial and distribution sector has increased in percentage growth compared to last year.

# The majority of respondents (68%) feel the real estate capital markets through 2018 are in balance, and half the respondents felt that some increase (34%) is expected in the availability of equity capital.

0%#

20%#

40%#

60%#

80%#

ACTIVE'SECTORS,'201402017'CHANGES'

2014#2015#2016#2017#

# Compared with last years’ survey, it is evident that respondents agree that the apartment sector and the residential for-sale sector have been growing. However, respondents expressed concern that there has been too much focus on high-end rental units.

# Respondents agree that the office sector has been in a steady recovery/growth stage.

# The industrial sector has picked up significantly compared to last year.

# The general view is that most of the markets are currently moving from a recovery/growth stage to growth stage potential, while retail continues on a declining trend with regional malls in advanced decline.

# Hospitals lead the growth of the institutional/public sector, with higher education following close behind. Such institutions are investing in the market, which contributes to the jump from last year.

# Hottest submarkets with good-excellent prospects continue to be University Circle and Downtown Cleveland.

# All respondents regard the economic health of the region as vital to continued growth

0#

2#

4#

6#

8#

10#

12#

14#

16#

Peak' Early'Decline' Advanced'Decline' Bottomed'Out' Recovery/Growth' Growth'

Number'of'Respondents'

CURRENT'STAGE'OF'REAL'ESTATE'CYCLE0APARTMENT'(N=25029)'

All#Apartments# Luxury#Apartments# Moderate#Apartments# Tax#Credit#Apartments# Student#Housing#

0#

2#

4#

6#

8#

10#

12#

14#

16#

Peak' Early'Decline' Advanced'Decline' Bottomed'Out' Recovery/Growth' Growth'

Number'of'Respondents'

CURRENT'STAGE'OF'REAL'ESTATE'CYCLE0RETAIL'(N=23025)'

All#Retail# Regional#Malls# Power#Centers# Neighborhood/Community#Shopping#Centers#

0"

4"

8"

12"

16"

Peak' Early'Decline' Advanced'Decline' Bottomed'Out' Recovery/Growth' Growth'

Number'of'Respondents'

CURRENT'STAGE'OF'REAL'ESTATE'CYCLE0OFFICE'(N=30031)'

All#OfKice# Central#City#OfKice# Suburban#OfKice# Medical#OfKice#

0#

2#

4#

6#

8#

10#

12#

14#

16#

18#

Peak' Early'Decline' Advanced'Decline' Bottomed'Out' Recovery/Growth' Growth'

Number'of'Respondents'

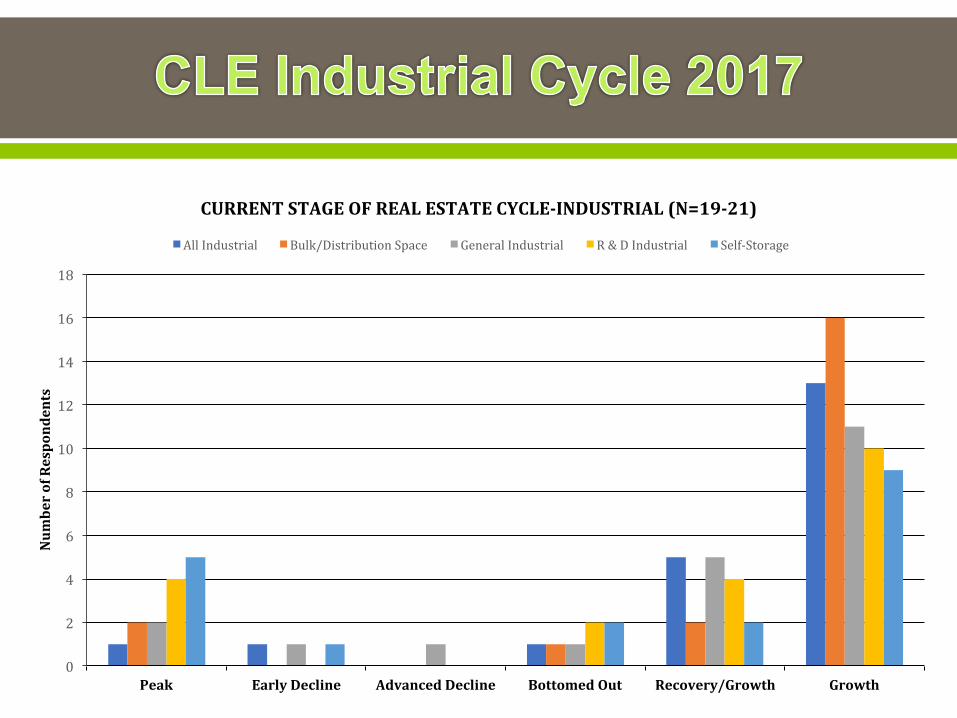

CURRENT'STAGE'OF'REAL'ESTATE'CYCLE0INDUSTRIAL'(N=19021)'

All#Industrial# Bulk/Distribution#Space# General#Industrial# R#&#D#Industrial# SelfSStorage#

1# 2# 3# 4# 5#

ClevelandSEast#

Lorain#County#

Portage#County#

Lake#County#

Geauga#County*#

Cuyahoga#County#South#Central#and#

Cuyahoga#County#Southeastern#

City#of#Akron#

Medina#County#

Summit#County#

Cuyahoga#County#Eastern#Suburbs#

ClevelandSWest#

Downtown#Cleveland#

University#Circle#

ABYSMAL''''''''''''POOR'''''''''''FAIR''''''''''''''GOOD''''''''''EXCELLENT'

2018#2017#

*#No#comparable#data#available#from#2017#

# Executive in Residence at CSU, Levin College # Director of NEOSCC, Vibrant NEO 2040 # Former Planning Director at City of Cleveland

o Civic Vision 2000: 1992 APA National Planning Award for Comprehensive Planning

# Former Director of the Center for Urban and Regional Studies at YSU

# Degrees from Yale College (City Planning & Political Science), Harvard Graduate School of Design (City Planning), & CSU (Bus. Admin.)