22

“Un-baking the Insurance Cake” Seeing Insurance for the trucking and logistics industry from a different point of view

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | dwight-scott |

| View: | 214 times |

| Download: | 0 times |

“Un-baking the Insurance Cake”Seeing Insurance for the trucking and logistics industry from a different point of view

Topics for discussion Do you view your insurance as a commodity or a

specialty product? What does a “good” insurance placement mean to you? Let’s look at the parts of the cake?

The decoration The icing The top layer The middle layer The bottom layer

Questions you want to ask at your next renewal?

Commodity or Specialty?

Would you buy “brain surgery” from the lowest bidder?Should you buy insurance from the lowest bidder?Why do insurance companies “bid” on accounts?

What does “good” Insurance Mean?

“I am paying $6,000 per unit I’m happy” “My loss ratio is 30% I should get a reduction” “I had a “big” claim my insurer took only a modest

increase” “My broker “went to market” and I got a cheaper

quote” “My broker reduced his commission which got me a

better price”

Some things I wonder about… What does $6,000 per unit premium mean? What does a 30% loss ratio mean? Why do insurers think they have to increase your

premium after you had a claim? Why do insurers “quote” on new business based from a

“submission”?

Let’s “un-bake” bake that cake!!

Disclaimer!!!

Richard asked me for a catchy presentation title on short notice. I picked the “cake” thing and now I am stuck with it. -- you will now be subjected to a series of “cake” clichés -

Please address all complaints to Richard

A Chocolate Layer CakeDecoration

Icing

Top Layer

Middle Layer

Bottom Layer

Sales

Insurer Services

Excess Layer

Working Layer

Burn Layer

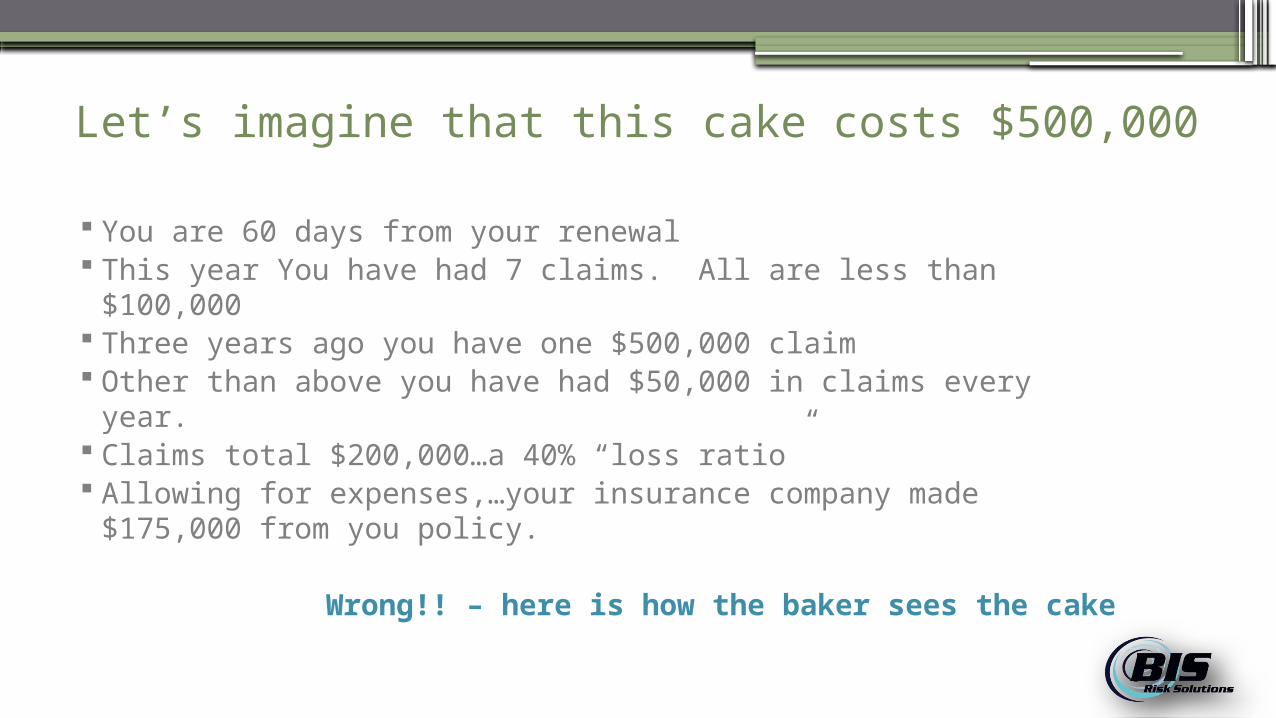

Let’s imagine that this cake costs $500,000

You are 60 days from your renewal This year You have had 7 claims. All are less than $100,000 Three years ago you have one $500,000 claim Other than above you have had $50,000 in claims every

year. Claims total $200,000…a 40% “loss ratio” Allowing for expenses,…your insurance company made

$175,000 from you policy.

Wrong!! – here is how the baker sees the cake

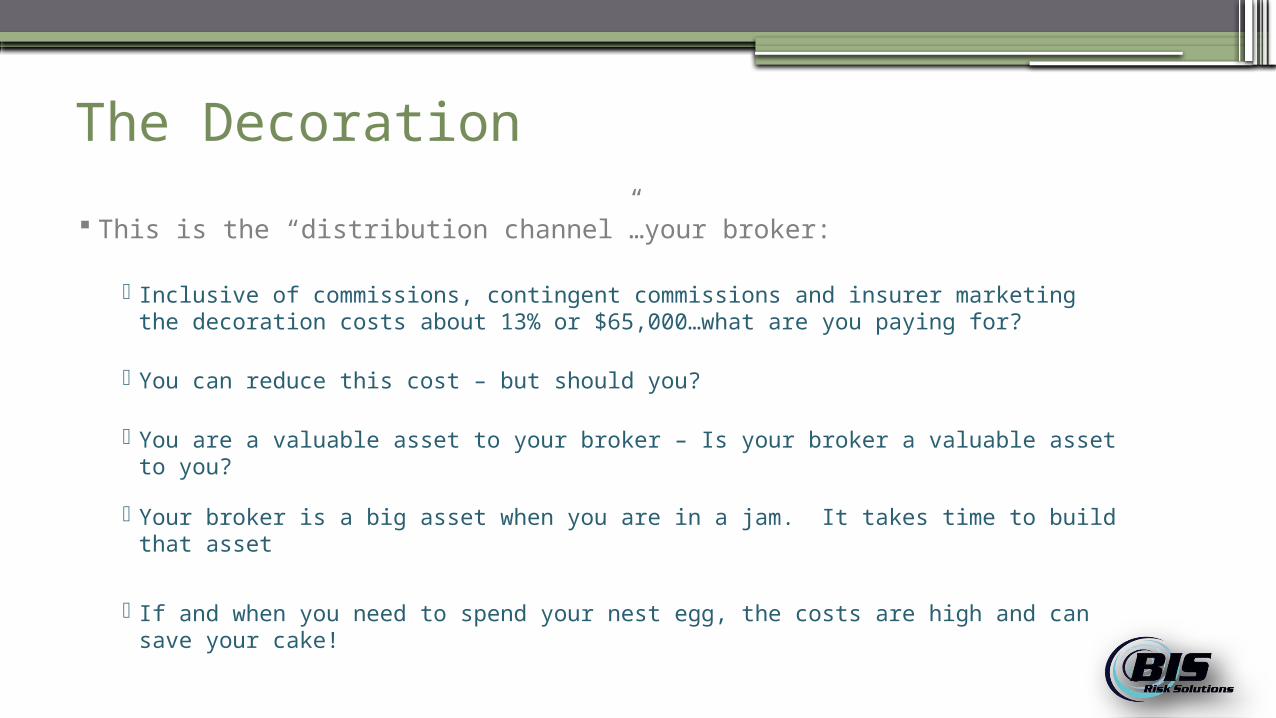

The Decoration

This is the “distribution channel”…your broker:

Inclusive of commissions, contingent commissions and insurer marketing the decoration costs about 13% or $65,000…what are you paying for?

You can reduce this cost – but should you?

You are a valuable asset to your broker – Is your broker a valuable asset to you?

Your broker is a big asset when you are in a jam. It takes time to build that asset

If and when you need to spend your nest egg, the costs are high and can save your cake!

The Decoration

How to build that your broker as an asset: Their value as an asset lies in their access to markets

in a pinch You may never need this value but it is good

Insurance Their value to you is the value they bring to the

market…know what that is Pay them a competitive rate

The Icing

These are your insurer services:• Underwriting• Claims• Loss control• Finance• Actuarial

The icing costs roughly 17% or $85,000 – what are you paying for?

The Icing

Is your Insurer a partner or a vendor? Have you met your underwriter? Does loss control “Analyze Risk” or “Integrated” Is your adjuster the “next available operator” – or

“pre-disposed” to your business? How does your insurer compete and compare as a

financial institution? What is your insurer’s point of view where pricing

ought to be and where the market supports?

The Top Layer of the Cake

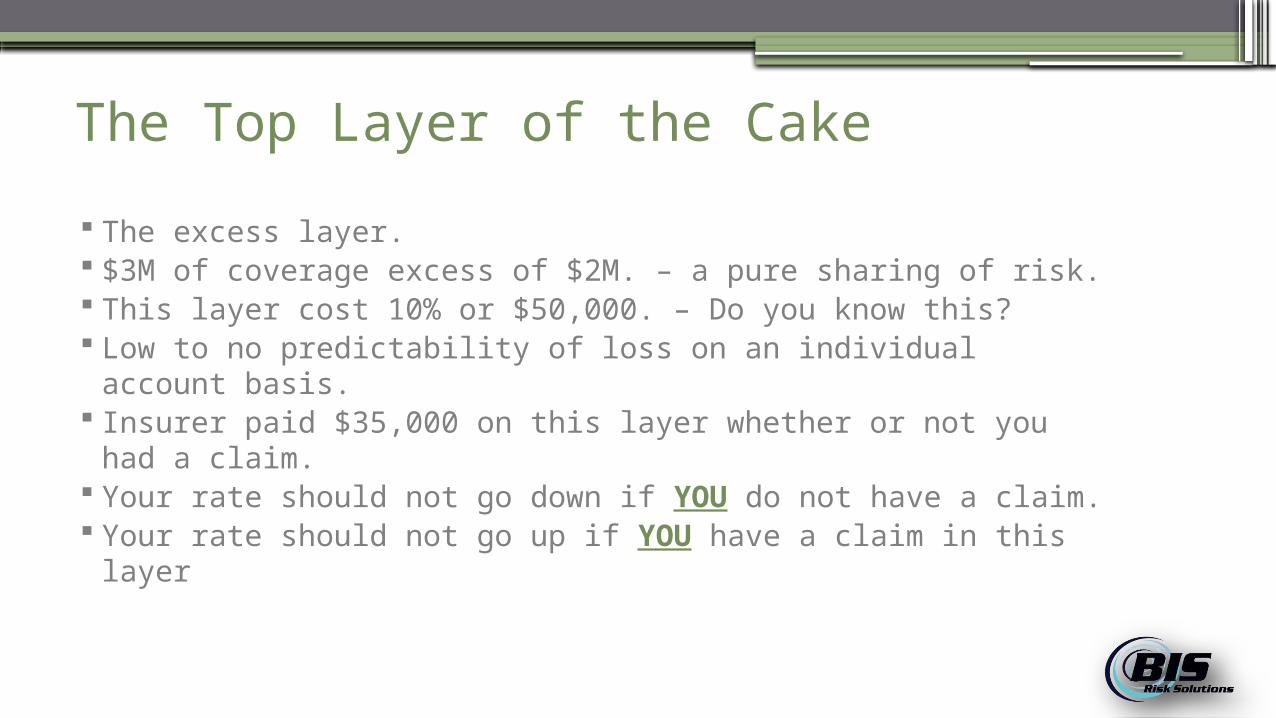

The excess layer. $3M of coverage excess of $2M. – a pure sharing of risk. This layer cost 10% or $50,000. – Do you know this? Low to no predictability of loss on an individual account

basis. Insurer paid $35,000 on this layer whether or not you had a

claim. Your rate should not go down if YOU do not have a claim. Your rate should not go up if YOU have a claim in this layer

The Top Layer of the Cake

You should be paying rate based on how this layer performs in the insurance market -and-

How you compare against your peers.

What is your insurer’s underwriting profit is in this layer

What is your insurer’s investment profit is in this layer

The Middle Layer

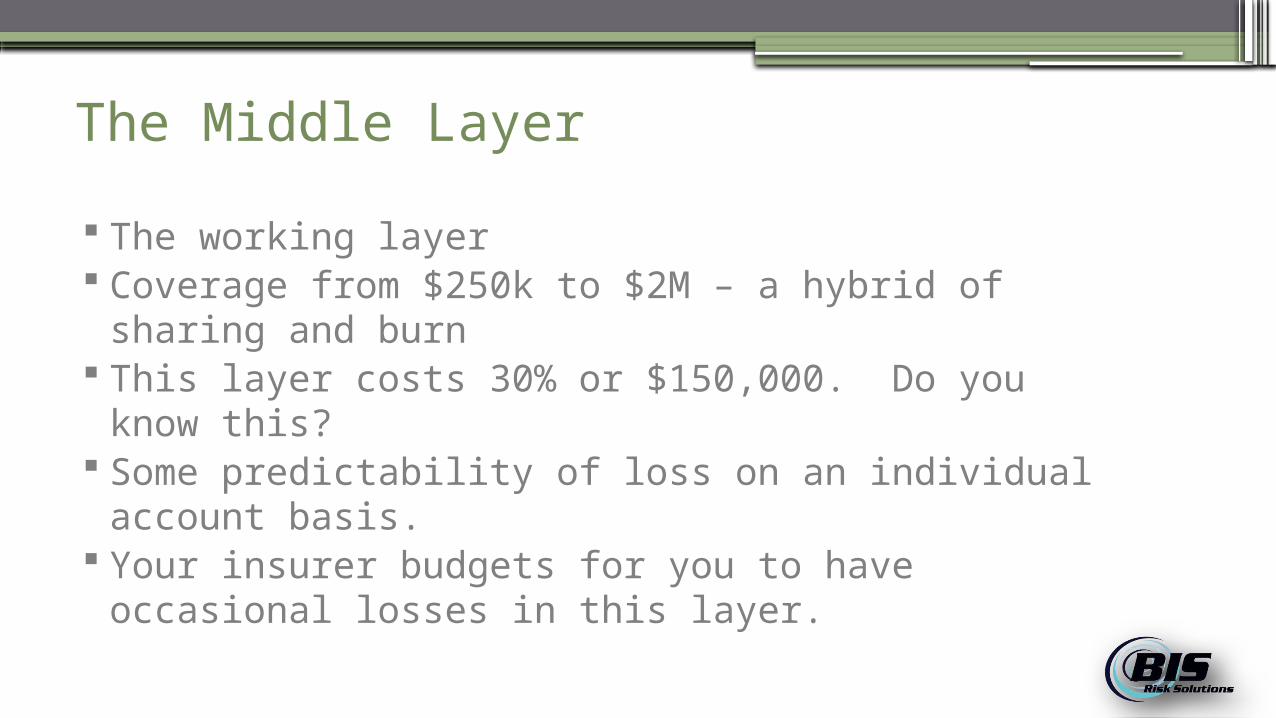

The working layer Coverage from $250k to $2M – a hybrid of sharing

and burn This layer costs 30% or $150,000. Do you know this? Some predictability of loss on an individual account

basis. Your insurer budgets for you to have occasional

losses in this layer.

The Middle Layer

To gauge your performance in this layer (Layman’s terms)

70% of the premium ($105,000) should be allocated to loss 50% of that ($52,500) is pure risk sharing….spent before you

start. How has your account performed over the past 5 years on

the other 50%. i.e. one loss $500,000 loss in past five years:

$250,000 allocated to middle layer Divide by 5 is $50,000 per year. Annual underwriting profit on this year of $2,500

The Bottom Layer

The burn layer – the foundation – “centre of the universe layer” Coverage from $0 to $250,000 – purely based on YOUR results:

Upper level can vary This layer (in YOUR case) cost $165,000 – You should really know

this Layer pricing based on YOUR LOSS PICK

Your insurer’s prediction of what YOU WILL incur Working and Excess Layers are built from your pick Frequency – not Severity – is what should keep you up at

night

The Bottom Layer

Insurers use loss and exposure history and apply development factors

You incurred $200,000 in losses in the first 10 months. Your insurer believes that this will grow to $474,800…will it?

10 22 34 46Dev. Factor 2.374 1.526 1.289 1.153

Months Aged

The Bottom Layer

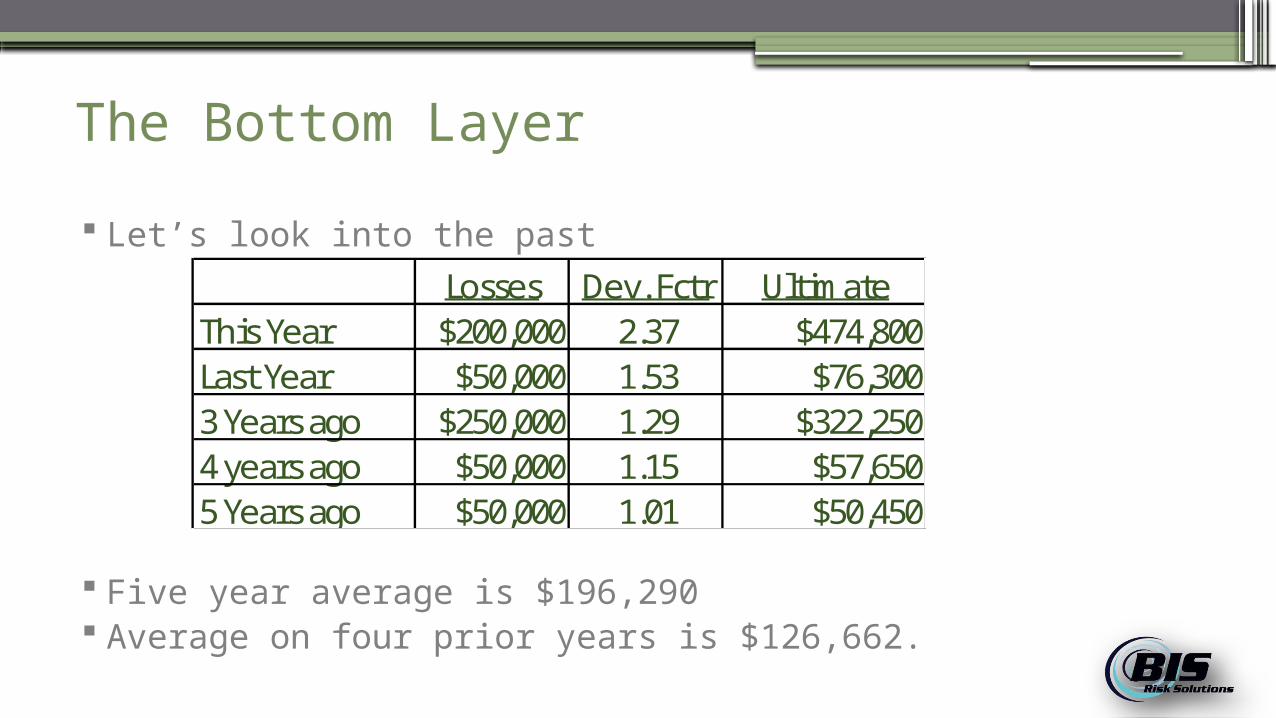

Let’s look into the past

Five year average is $196,290 Average on four prior years is $126,662.

Losses Dev. Fctr UltimateThis Year $200,000 2.37 $474,800Last Year $50,000 1.53 $76,3003 Years ago $250,000 1.29 $322,2504 years ago $50,000 1.15 $57,6505 Years ago $50,000 1.01 $50,450

The Bottom Layer

What is your Loss Pick? What is the upper limit of your Burn Layer? What is the confidence level of that Loss Pick?

If there is a high degree of confidence in the pick….IT IS NOT INSURANCE

IT IS A BUSINESS EXPENSE

Did Your Insurer Make Money

Say Insurer has a 75% loss ratio in Working and Excess Layers…

Premium $500,000Decoration $ 65,000Icing $ 85,000Top Layer $ 37,500Middle Layer $162,500Burn Layer $200,000 (or maybe $474,800?)Underwriting Profit $150,000

InsuranceWith a good understanding “You can have your cake and eat it too!”

![Assorted Baking CupsAssorted Baking Cups - Pastry Pro Cup [NP-2016-09-09].pdf · Assorted Baking CupsAssorted Baking Cups PET Laminated Baking Cup Paper Baking Cup Food grade and](https://static.documents.pub/doc/80x56/5a9dbea27f8b9abd0a8c98bb/assorted-baking-cupsassorted-baking-cups-pastry-cup-np-2016-09-09pdfassorted.jpg)