35

Understanding Who Qualifies to Refinance a VA Loan

| Date post: | 20-Jul-2015 |

| Category: |

Investor Relations |

| Upload: | kay-frenzer-zeeh |

| View: | 168 times |

| Download: | 1 times |

Understanding Who Qualifies to Refinance a VA Loan

The U.S. Veterans Affairs

Administration has helped

provide home loans for veterans

since 1944.

The program allows both veterans

and active duty service members to

get affordable mortgages that the

VA guarantees to be repaid to

lenders.

The program has been expanded to

include refinancing these loans, and

certain qualifications apply.

Use of VA Loan Eligibility

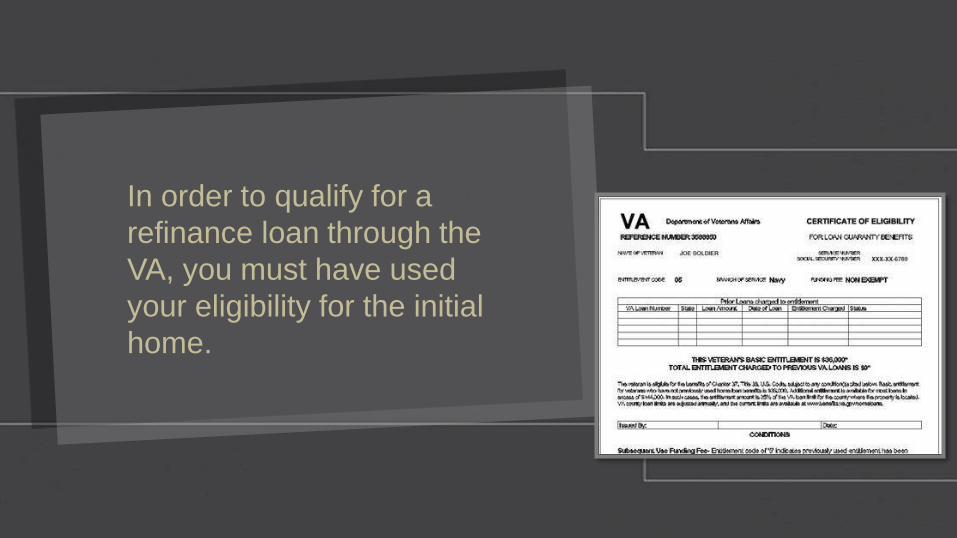

In order to qualify for a

refinance loan through the

VA, you must have used

your eligibility for the initial

home.

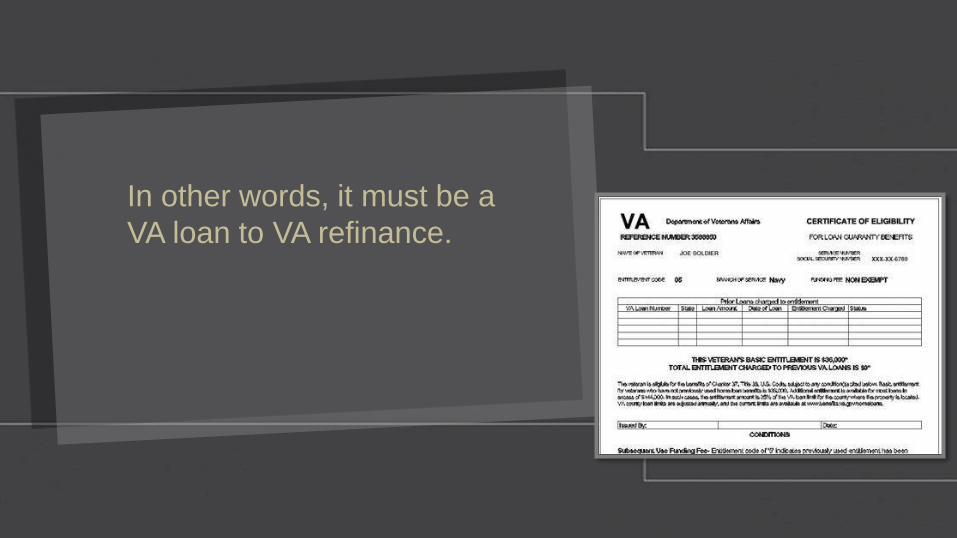

In other words, it must be a

VA loan to VA refinance.

A new Certificate of Eligibility is

not required. Your previous

Certificate of Eligibility serves as

proof of the use of your

entitlement.

Loan Limits

VA refinance loans are

subject to certain loan limits

as defined by the program.

These limits cap the amount of

liability for repayment required by

the program. Each county

determines the amount of loan

limit.

Generally, lenders will approve up

to four times the basic entitlement

amount of $36,000 for a home

loan, without a down payment.

Funding Fee

A funding fee is required for all

those who apply for loans through

the VA Guaranteed Loan

Program.

Payment of the fee is required at

closing on the loan. You can

either pay the funding fee in cash

or roll it into the financing of the

property.

Funding fees can range from 0.5

percent to 3.3 percent. Funding fees

for the second use of your eligibility

are generally higher than the first

use.

Certain veterans with disabilities and

surviving spouses are not required to

pay a funding fee.

Interest Rate Reduction

Refinance Loan

The program allows

refinancing up to 100 percent

of the home’s value.

Although credit checks and new

appraisals are not required under

the program, lenders may impose

these requirements under their

own rules.

Unlike a VA Purchase Loan, you

do not have to certify that you will

occupy the home. You must only

certify that you have previously

occupied it.

The IRRRL program cannot be

used to pay off a second

mortgage. Generally, the second

mortgage must be approved.

Your current mortgage payments

must be up to date, with no more

than one 30-day late payment

within the past year.

Cash-Out Refinance Loan

If you wish to take cash out of

your home for medical costs,

children’s college or home

improvement costs, the VA offers

a Cash-Out Refinancing Program

that allows you to use your equity

to finance these major expenses.

The above qualifications apply

similarly for these loans.

You may also refinance as much

as 100 percent of the value of the

property. Unlike the IRRL loan, a

credit report, income verification

and property appraisal are

required.

You must also certify that you will

occupy the home being

refinanced.

Certain costs associated with

refinancing can increase the

cost of the loan to a greater

amount than the fair market

value of the property.

These costs can include state

and local taxes, discount

points and other closing

costs.

Applicants for refinancing

should always take these

additional costs into account

when determining if

refinancing their VA loan is a

favorable idea.

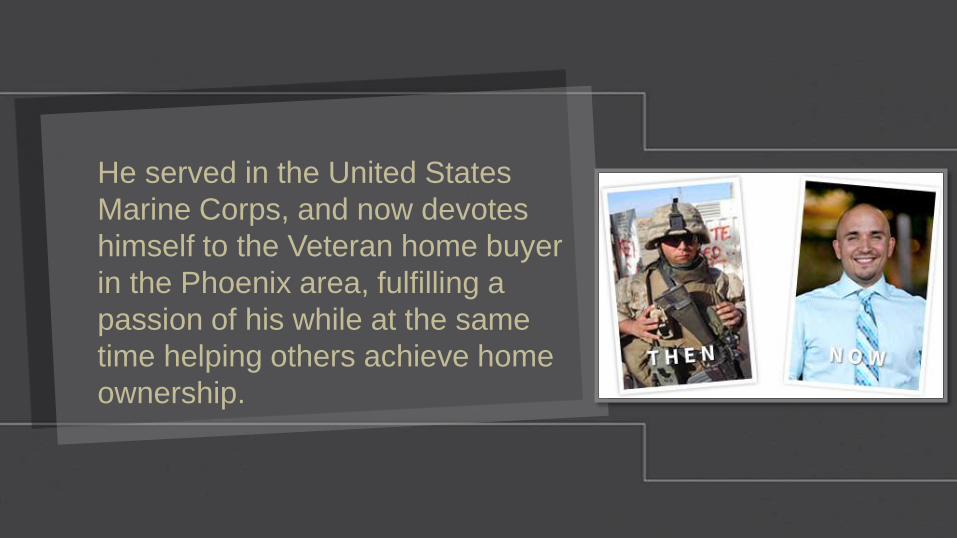

He served in the United States

Marine Corps, and now devotes

himself to the Veteran home buyer

in the Phoenix area, fulfilling a

passion of his while at the same

time helping others achieve home

ownership.

Be a proud homeowner today.

For more details call

480-351-5904 or visit the site

www.valoansforvets.co

m

VA Loans for Vets

7702 E. Doubletree Ranch Road,

Suite 220

Scottsdale, AZ 85258

Phone: (480) 351-5904

Email: [email protected]