80

Union Properties Public Joint Stock Company and its subsidiaries Consolidated financial statements 31 December 2018

Union Properties Public Joint Stock Company and its subsidiaries

Consolidated financial statements 31 December 2018

Union Properties Public Joint Stock Company and its subsidiaries Consolidated financial statements 31 December 2018 Contents Page(s) Directors’ report ......................................................................................................................................... 1 Independent auditor’s report ............................................................................................................. 2-10 Consolidated statement of profit or loss and other comprehensive income ......................................... 11 Consolidated statement of financial position .......................................................................................... 12 Consolidated statement of cash flows.................................................................................................... .13 Consolidated statement of changes in equity ......................................................................................... 14 Notes to the consolidated financial statements.............................................................................. 15 – 78

11

Union Properties Public Joint Stock Company and its subsidiaries Consolidated statement of profit or loss and other comprehensive income For the year ended 31 December 2018

2018 2017

Notes AED’000 AED’000

Revenue from contracts with customers 5 500,988 484,607

Net loss on financial instruments at FVTPL 11 (1,787) (1,619)

Gain on disposal of a joint venture 24 125,014 -

Share of profit of equity accounted investees 24 16,380 3,580

Gain/(loss) on valuation of properties, net 9 86,404 (2,075,698)

Finance income 4,102 10,705

Other income 7 119,700 142,557

Direct costs 5 (382,063) (716,218)

Administrative and general expenses 6 (282,251) (157,279)

Finance cost (124,158) (65,855)

Profit/(loss) for the year attributable to the shareholders of

the Company 62,329 (2,375,220)

Other comprehensive income for the year 8 390,011 - Total comprehensive income/(loss) for the year 452,340 (2,375,220)

Basic and diluted earnings per share (AED) 26 0.015 (0.554)

The notes from 1 to 32 form an integral part of these consolidated financial statements.

The independent auditor’s report is set out on the pages 2 to 10.

13

Union Properties Public Joint Stock Company and its subsidiaries

Consolidated statement of cash flows For the year ended 31 December 2018

2018 2017

Notes AED’000 AED’000

Operating activities

Profit/(loss) for the year 62,329 (2,375,220)

Adjustments for:

Depreciation 8 12,928 16,947

(Gain)/loss on fair valuation of investment properties 9 (86,404) 2,075,698

Share of profit of equity accounted investees 24 (16,380) (3,580)

Provision for slow moving inventories - 45,927

Provision for doubtful debts 29 13,264 599

Reversal of development properties provision 12 (9,420) -

Gain on disposal of property, plant and equipment 8 - (589)

Loss on financial instruments at FVTPL 11 1,787 1,619

Gain on disposal of a joint venture (125,014) -

Finance income (4,102) (10,705)

Finance cost 124,158 65,855

Operating loss before working capital changes (26,854) (183,449)

Change in inventories (212) 9,261

Change in contract assets 9,836 22,378

Change in trade and other receivables (52,281) 151,798

Change in due from related parties 11,946 (18,547)

Change in trade and other payables and contract liabilities (16,702) 118,224

Change in due to related parties - (4,386)

Change in development properties 43,622 -

Change in staff terminal benefits - net (5,017) (14,212)

Net cash (used in)/generated from operating activities (35,662) 81,067

Investing activities

Additions to property, plant and equipment 8 (15,990) (19,324)

Additions to investment properties 9 (32,500) (198,906)

Additions to development properties 12 (2,792) -

Purchase of financial instruments at FVTPL 11 (940,233) (111,878)

Proceeds from sale of financial instruments at FVTPL 11 359,422 190,408

Dividend received - 20,000

Proceeds from disposal of a joint venture 500,000 -

Proceeds from disposal of property, plant and equipment - 204

Interest received 4,102 5,771

Change in deposit with banks (31,583) 10,407

Net cash used in investing activities (159,574) (103,318)

Financing activities

Long-term bank loans availed 20 485,110 241,892

Repayment of bank loans 20 (450,873) (95,314)

Interest paid (83,063) (65,256)

Net cash (used in)/generated from financing activities (48,826) 81,322 Net (decrease)/increase in cash and cash equivalents (244,062) 59,071 Cash and cash equivalents at the beginning of the year 67,488 8,417 Cash and cash equivalents at the end of the year 16(a) (176,574) 67,488

The notes from 1 to 32 form an integral part of these consolidated financial statements.

The independent auditor’s report is set out on the pages 2 to 10.

14

Union Properties Public Joint Stock Company and its subsidiaries Consolidated statement of changes in equity For the year ended 31 December 2018

Share

capital

Statutory

reserve

General

reserve

Asset

revaluation

surplus

(Accumlated

losses)/retained

earnings Total

AED’000 AED’000 AED’000 AED’000 AED’000 AED’000

At 1 January 2017 3,971,796 326,647 313,697 - 417,898 5,030,038

Total comprehensive income for the year - - - - (2,375,220) (2,375,220)

Other equity movements

Issuance of bonus shares (refer note 22) 317,744 - - - (317,744) -

Transfer of general reserve (refer note 23) - - (313,697) - 313,697 -

At 31 December 2017 4,289,540 326,647 - - (1,961,369) 2,654,818

At 1 January 2018 4,289,540 326,647 - - (1,961,369) 2,654,818

Total comprehensive income for the year - - - 390,011 62,329 452,340

Other equity movements

Transfer to statutory reserve (refer note 23) - 6,233 - - (6,233) -

At 31 December 2018 4,289,540 332,880 - 390,011 (1,905,273) 3,107,158

The notes from 1 to 32 form an integral part of these consolidated financial statements.

The independent auditor’s report is set out on the pages 2 to 10.

15

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements

1 LEGAL STATUS AND PRINCIPAL ACTIVITIES

Union Properties Public Joint Stock Company (“the Company”) was incorporated on 28 October 1993 as a public joint stock company by a United Arab Emirates Ministerial decree. The Company’s registered office address is P.O. Box 24649, Dubai, United Arab Emirates (“UAE”).

The principal activities of the Company are investment in and development of properties, the management and maintenance of owned properties including the operation of cold stores, the undertaking of property related services on behalf of other parties (including related parties) and acting as the holding company of its subsidiaries and investing in other entities as set out in note 2.1.

The Company and its subsidiaries are collectively referred to as “the Group”.

2 BASIS OF PREPARATION

2.1 Statement of compliance

The consolidated financial statements of the Group have been prepared in accordance with the International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (IASB) and the requirements of the UAE Federal Law No. (2) of 2015.

2.2 Basis of measurement

The consolidated financial statements of the Group have been prepared on the historical cost convention basis except for investment properties and investments at fair value through profit or loss that have been measured at fair value. 2.3 Comparative information The consolidated financial statements provide comparative information in respect of the previous period. In addition, the Group presents an additional statement of financial position at the beginning of the preceding period when there is a retrospective application of an accounting policy, a retrospective restatement, or a reclassification of items in the consolidated financial statements. An additional consolidated statement of financial position as at 1 January 2017 was not presented in these consolidated financial statements, given that the effect of the retrospective application of accounting policies as a result of the adoption of new accounting standards was not significant (note 3.2).

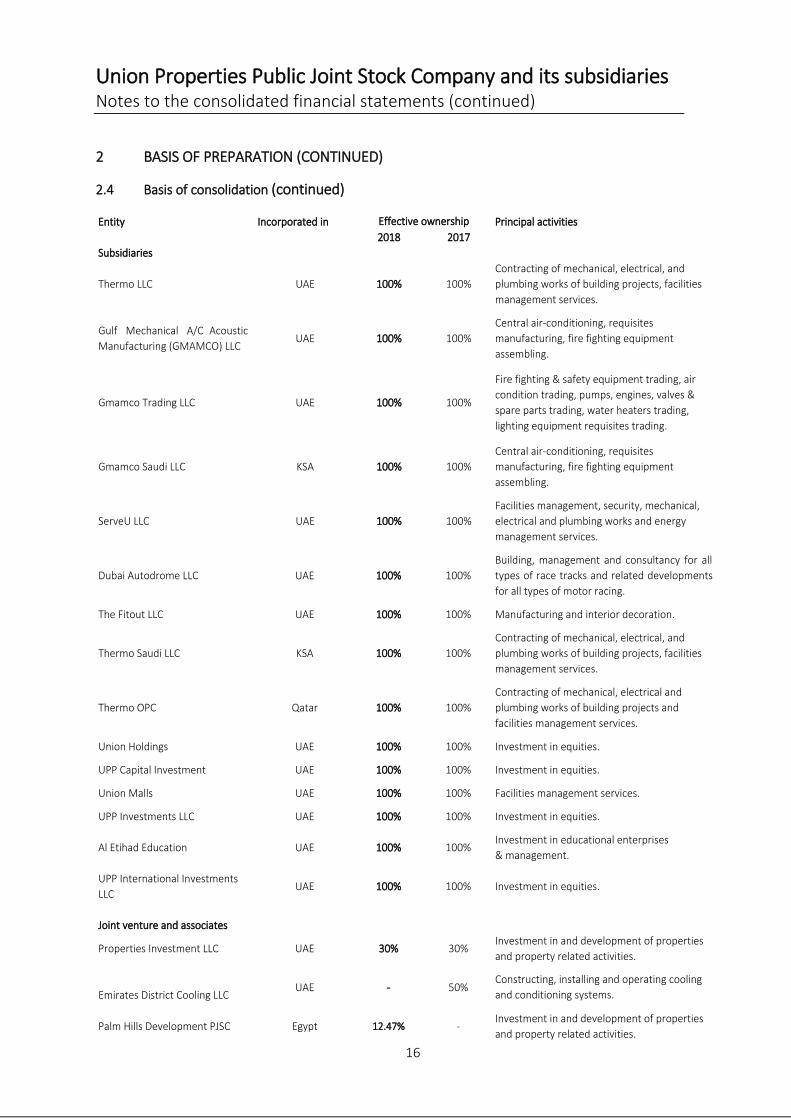

2.4 Basis of consolidation

These consolidated financial statements comprise the financial statements of the Company and its subsidiaries at 31 December 2018, as set out below:

16

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

2 BASIS OF PREPARATION (CONTINUED)

2.4 Basis of consolidation (continued)

Entity Incorporated in Principal activities

2018 2017

Subsidiaries

Thermo LLC UAE 100% 100%

Contracting of mechanical, electrical, and

plumbing works of building projects, facilities

management services.

Gulf Mechanical A/C Acoustic

Manufacturing (GMAMCO) LLCUAE 100% 100%

Central air-conditioning, requisites

manufacturing, fire fighting equipment

assembling.

Gmamco Trading LLC UAE 100% 100%

Fire fighting & safety equipment trading, air

condition trading, pumps, engines, valves &

spare parts trading, water heaters trading,

lighting equipment requisites trading.

Gmamco Saudi LLC KSA 100% 100%

Central air-conditioning, requisites

manufacturing, fire fighting equipment

assembling.

ServeU LLC UAE 100% 100%

Facilities management, security, mechanical,

electrical and plumbing works and energy

management services.

Dubai Autodrome LLC UAE 100% 100%

Building, management and consultancy for all

types of race tracks and related developments

for all types of motor racing.

The Fitout LLC UAE 100% 100% Manufacturing and interior decoration.

Thermo Saudi LLC KSA 100% 100%

Contracting of mechanical, electrical, and

plumbing works of building projects, facilities

management services.

Thermo OPC Qatar 100% 100%

Contracting of mechanical, electrical and

plumbing works of building projects and

facilities management services.

Union Holdings UAE 100% 100% Investment in equities.

UPP Capital Investment UAE 100% 100% Investment in equities.

Union Malls UAE 100% 100% Facilities management services.

UPP Investments LLC UAE 100% 100% Investment in equities.

Al Etihad Education UAE 100% 100%Investment in educational enterprises

& management.

UPP International Investments

LLCUAE 100% 100% Investment in equities.

Joint venture and associates

Properties Investment LLC UAE 30% 30%Investment in and development of properties

and property related activities.

Emirates District Cooling LLCUAE - 50%

Constructing, installing and operating cooling

and conditioning systems.

Palm Hills Development PJSC Egypt 12.47% -Investment in and development of properties

and property related activities.

Effective ownership

17

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

2 BASIS OF PREPARATION (CONTINUED)

2.4 Basis of consolidation (continued)

Subsidiaries

Subsidiaries are entities controlled by the Group. The Group controls an investee when it is exposed to, or has rights to, variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. The financial statements of subsidiaries are included in the consolidated financial statements from the date on which control commences until the date on which control ceases.

Transactions eliminated on consolidation

Intra-group balances and transactions, and any unrealised income and expenses arising from intra-group transactions, are eliminated in full in preparing these consolidated financial statements. 2.5 Functional and presentation currency

The consolidated financial statements are presented in United Arab Emirates Dirhams (“AED”), which is the Group’s functional currency. All amounts have been rounded to the nearest thousand (“AED’000”), except when otherwise indicated. 2.6 Use of estimates and judgements

In preparing these consolidated financial statements, management has made judgements, estimates and assumptions that affect the application of the Group’s accounting policies and the reported amounts of assets, liabilities, income and expenses.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to estimates are recognised prospectively.

In particular, information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the consolidated financial statements are described in note 30. 2.7 Fair Value Measurement

The Group measures certain financial instruments such as financial assets at FVTPL, and certain non-financial assets such as investment properties, at fair value at each reporting date. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The fair value measurement is based on the presumption that the transaction to sell the asset or transfer the liability takes place either:

• In the principal market for the asset or liability; or

• In the absence of a principal market, in the most advantageous market for the asset or liability

The principal or the most advantageous market must be accessible by the Group. The fair value of an asset or a liability is measured using the assumptions that market participants would use when pricing the asset or liability, assuming that market participants act in their economic best interest.

18

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

2 BASIS OF PREPARATION (CONTINUED)

2.7 Fair Value Measurement (continued) A fair value measurement of a non-financial asset takes into account a market participant's ability to generate economic benefits by using the asset in its highest and best use or by selling it to another market participant that would use the asset in its highest and best use. The Group uses valuation techniques that are appropriate in the circumstances and for which sufficient data are available to measure fair value, maximising the use of relevant observable inputs and minimising the use of unobservable inputs. All assets and liabilities for which fair value is measured or disclosed in the consolidated financial statements are categorised within the fair value hierarchy, described as follows, based on the lowest level input that is significant to the fair value measurement as a whole:

• Level 1: quoted (unadjusted) market prices in active markets for identical assets or liabilities.

• Level 2: Valuation techniques for which the lowest level input that is significant to the fair value measurement is directly or indirectly observable

• Level 3: Valuation techniques for which the lowest level input that is significant to the fair value measurement is unobservable

If the inputs used to measure the fair value of an asset or liability might be categorised in different levels of the fair value hierarchy, then the fair value measurement is categorised in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement.

For assets and liabilities that are recognised in the consolidated financial statements at fair value on a recurring basis, the Group determines whether transfers have occurred between levels in the hierarchy by re-assessing categorisation (based on the lowest level input that is significant to the fair value measurement as a whole) at the end of each reporting period.

The Group has an established control framework with respect to the measurement of fair values. This includes a management team that has overall responsibility for overseeing all significant fair value measurements, including Level 3 fair values. The management team regularly reviews significant unobservable inputs and valuation adjustments. External valuers are involved for valuation of significant assets, such as investment properties. If third party is used to measure fair values, the management team discusses with the valuer the valuation techniques and inputs to use and assesses the evidence obtained from the third party to support the conclusion that such valuations meet the requirements of IFRS, including the level in the fair value hierarchy in which such valuations should be classified.

19

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

2 BASIS OF PREPARATION (CONTINUED) 2.8 Financial Commitments

The Group’s loans and borrowings as at 31 December 2018 amounted to AED 1,776 million (AED 1,545 million of bank loans and AED 231 million of bank overdrafts). Furthermore, the Group has net current liabilities of AED 1,599 million as at the reporting date.

The management has analysed the Group’s liquidity position over a period of 12 months from the reporting date. Based on the Group’s available funding facilities, forecasted cash inflows from operations, contractual loan maturities, debt service costs, estimated and committed capital expenditure, and liquid investments management has not identified a material uncertainty that may cast significant doubt about the Group’s ability to continue as a going concern or to meet its future obligations.

The Board of Directors has reviewed the Group’s cash flow projections and concluded that the Group will be able to meet its commitments as they fall due in the foreseeable future.

3 SIGNIFICANT ACCOUNTING POLICIES

3.1 Summary of significant accounting policies Associates and joint ventures

Associates are those entities over which the Group has significant influence. Significant influence is the power to participate in the financial and operating policy decisions of the investee, but is not control or joint control over those policies. A joint venture is a type of joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the joint venture. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control. The considerations made in determining significant influence or joint control are similar to those necessary to determine control over subsidiaries. The Group’s investment in its associates and joint venture are accounted for using the equity method.

Under the equity method, the investment in an associate or a joint venture is initially recognised at cost. The carrying amount of the investment is adjusted to recognise changes in the Group’s share of net assets of the associate or joint venture since the acquisition date. Goodwill relating to the associate or joint venture is included in the carrying amount of the investment and is not tested for impairment separately. The statement of profit or loss reflects the Group’s share of the results of operations of the associates and joint venture. Unrealised gains and losses resulting from transactions between the Group and the associate or joint venture are eliminated to the extent of the interest in the associates or joint venture. The aggregate of the Group’s share of profit or loss of an associate and a joint venture is shown on the face of the consolidated statement of profit or loss outside operating profit and represents profit or loss after tax and non-controlling interests in the subsidiaries of the associate or joint venture.

20

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.1 Summary of significant accounting policies (continued) Associates and joint ventures (continued) The financial statements of the associate or joint venture are prepared for the same reporting period as the Group. When necessary, adjustments are made to bring the accounting policies in line with those of the Group. After application of the equity method, the Group determines whether it is necessary to recognise an impairment loss on its investment in its associate or joint venture. At each reporting date, the Group determines whether there is objective evidence that the investment in the associate or joint venture is impaired. If there is such evidence, the Group calculates the amount of impairment as the difference between the recoverable amount of the associate or joint venture and its carrying value, and then recognises the loss within ‘Share of profit of associates and a joint venture’ in the consolidated statement of profit or loss. Upon loss of significant influence over the associate or joint control over the joint venture, the Group measures and recognises any retained investment at its fair value. Any difference between the carrying amount of the associate or joint venture upon loss of significant influence or joint control and the fair value of the retained investment and proceeds from disposal is recognised in profit or loss. Current versus non-current classification The Group presents assets and liabilities in the consolidated statement of financial position based on current/non-current classification. An asset is current when it is:

• Expected to be realised or intended to be sold or consumed in the normal operating cycle

• Held primarily for the purpose of trading

• Expected to be realised within twelve months after the reporting period or

• Cash or cash equivalent unless restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period

All other assets are classified as non-current. A liability is current when:

• It is expected to be settled in the normal operating cycle

• It is held primarily for the purpose of trading

• It is due to be settled within twelve months after the reporting period or

• There is no unconditional right to defer the settlement of the liability for at least twelve months after the reporting period

The Group classifies all other liabilities as non-current.

21

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.1 Summary of significant accounting policies (continued) Revenue from contracts with customers

The Group is in the business of development, sale and leasing of properties as well as involved in manufacturing, contracting, trading and services activities. Revenue from contracts with customers is recognised when control of the goods or services are transferred to the customer at an amount that reflects the consideration to which the Group expects to be entitled in exchange for those goods or services. The Group has generally concluded that it is the principal in its revenue arrangements, because it typically controls the goods or services before transferring them to the customer. The disclosures of significant accounting judgements, estimates and assumptions relating to revenue from contracts with customers are provided in Note 30. Trading activities

Revenue from sale of goods is recognised at the point in time when control of the asset is transferred to the customer, generally on delivery of the goods. The normal credit term is 30 to 90 days upon delivery.

Contracting activities Revenue from contracts for mechanical, electrical and plumbing works as well as from interior architecture is recognised over time using an input method (note 3) to measure progress towards complete satisfaction of the service, because the customer simultaneously receives and consumes the benefits provided by the Group. The Group considers whether there are other promises in the contract that are separate performance obligations to which a portion of the transaction price needs to be allocated (e.g., delivery, installation, warranties etc.). In determining the transaction price, the Group considers the effects of variable consideration, the existence of significant financing components, noncash consideration, and consideration payable to the customer (if any). Variable consideration If the consideration in a contract includes a variable amount, the Group estimates the amount of consideration to which it will be entitled in exchange for transferring the goods to the customer. The variable consideration is estimated at contract inception and constrained until it is highly probable that a significant revenue reversal in the amount of cumulative revenue recognised will not occur when the associated uncertainty with the variable consideration is subsequently resolved. Contracts with customers specify that the Group is liable to pay penalty or for liquidated damages if certain conditions specified in the contract are not met for reasons not attributable to the customer. This penalty amount may vary for different contracts and/or customers. When the Group identifies the existence of variable consideration, it will estimate the amount of the consideration at contract inception by using the expected value approach and recognise a liability for the expected future losses.

22

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.1 Summary of significant accounting policies (continued) Revenue from contracts with customers (continued) Contracting activities (continued) Contract modifications Variation orders or modifications to original contracts are common to the Group considering the long-term contracting nature of business. The terms for variation orders are defined in each contract. Generally, variations are priced by reference to the per unit rates agreed in the contract and the revised quantities required for the completion of the contract. In accordance with IFRS 15, the Group will account for a modification through a cumulative catch-up adjustment if the goods or services in the modification are not distinct and are part of a single performance obligation that is only partially satisfied when the contract is modified. Alternatively, the Group will account for a contract modification as a separate contract if the scope of contract increases due to addition of distinct goods or services and price of the contract increases by an amount that reflects the Group’s standalone selling prices. Warranty obligations The Group provides its customers warranty against defects arising from normal and/or expected usage and maintenance for a period of 1 year from the date of taking over certificates. Management assessed that 1 year warranty for defects are considered as an assurance type warranty as this warranty is necessary to ensure that the delivered products/services are as specified in the contract for a minimum period. There is no separate performance obligation for this warranty. The extended warranty which is given by the Group for a period longer than required by the normal practice, is usually for the purpose of detecting errors or defects in the work performed and is necessary to provide assurance that the goods or services comply with the agreed upon specifications, and accordingly, such warranties are treated as assurance type warranty. Otherwise, and in rare cases, such warranty will be treated as a service type warranty and thus will be considered as a separate performance obligation. Where warranty is considered as an assurance type warranty, the Group accrues for the cost of satisfying the warranty liability on the basis of historical experiences in accordance with the provisions of IAS 37. Facility management, maintenance and motor racing services Revenue from services are satisfied over time, because the customer simultaneously receives and consumes the benefits provided by the Group, on a fixed contract basis or using an input method to measure progress towards complete satisfaction of the service. Sponsorship fees related to motor racing events are recognised in the period in which the related event is held.

Rental income

Rental income from investment properties is recognised as revenue on a straight-line basis over the term of the lease. Lease incentives granted are recognised as an integral part of the total rental income, over the term of the lease.

23

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.1 Summary of significant accounting policies (continued) Revenue from contracts with customers (continued) Revenue from sale of development properties

The Group satisfies a performance obligation and recognises revenue from sale of properties over time, if one of the following criteria is met:

• The customer simultaneously receives and consumes the benefits provided by the Group’s performance as the Group performs; or

• The Group’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced; or

• The Group’s performance does not create an asset with an alternative use to the Group and the entity has an enforceable right to payment for performance completed to date.

For performance obligations where one of the above conditions are not met, revenue from the sale of properties is recognised at the point in time at which the performance obligation is satisfied. Contract balances

Contract assets A contract asset is the right to consideration in exchange for goods or services transferred to the customer. If the Group performs by transferring goods or services to a customer before the customer pays consideration or before payment is due, a contract asset is recognised for the earned consideration that is conditional. Trade receivables A receivable represents the Group’s right to an amount of consideration that is unconditional (i.e., only the passage of time is required before payment of the consideration is due). Refer to accounting policies of financial assets under the section Financial instruments – initial recognition and subsequent measurement. Contract liabilities A contract liability is the obligation to transfer goods or services to a customer for which the Group has received consideration (or an amount of consideration is due) from the customer. If a customer pays consideration before the Group transfers goods or services to the customer, a contract liability is recognised when the payment is made or the payment is due (whichever is earlier). Contract liabilities are recognised as revenue when the Group performs under the contract.

Cost to obtain a contract The Group has elected to apply the optional practical expedient for costs to obtain a contract which allows the Group to immediately expense such costs (included in cost of sales) because the amortisation period of the asset that the Group otherwise would have used is one year or less.

Contract costs Contract costs comprise direct contract costs and other costs relating to the contracting activity in general and which can be allocated to contracts. In addition, contract costs include other costs that are specifically chargeable to the customer under the terms of the contracts.

24

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued) Value added tax

Expenses and assets are recognised net of the amount of value added tax, except:

• When the value added tax incurred on a purchase of assets or services is not recoverable from the taxation authority, in which case, the value added tax is recognised as part of the cost of acquisition of the asset or as part of the expense item, as applicable

• When receivables and payables are stated with the amount of value added tax included The net amount of value added tax recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the consolidated financial statements.

Foreign currency transactions

Transactions denominated in foreign currencies are initially recorded in the functional currency by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency using the closing rate. The foreign currency gain or loss on monetary items is the difference between amortised cost in the functional currency at the beginning of the period, adjusted for effective interest and payments during the period, and the amortised cost in foreign currency translated at the exchange rate at the end of the reporting period. All foreign currency differences are recognised in the profit or loss. Finance income and expense

Finance income comprises interest income on fixed deposits and changes in the fair value of financial assets at fair value through profit or loss. Interest income is recognised as it accrues in the profit or loss using the effective interest method.

Finance expense comprises interest expense on bank borrowings, changes in the fair value of financial assets at fair value through profit or loss and impairment losses recognised on financial assets. All borrowing costs, except to the extent that they are capitalised in accordance with the paragraph below, are recognised in the profit or loss using the effective interest method.

Borrowing costs directly attributable to the acquisition or construction of qualifying asset are capitalised as part of the cost of that asset. The capitalisation of borrowing costs commences from the date of incurring of expenditure related to the asset and ceases when substantially all the activities necessary to prepare the qualifying asset for its intended use is complete. Borrowing costs relating to the period after acquisition or construction are expensed.

25

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Property, plant and equipment and depreciation

Recognition and measurement

Other than land, items of property, plant and equipment are measured at cost less accumulated depreciation (refer below) and accumulated impairment losses (refer accounting policy on impairment), if any. Cost includes expenditure that is directly attributable to the acquisition of the asset. When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment. The cost of self constructed assets includes the cost of materials, direct labour and an appropriate proportion of overheads.

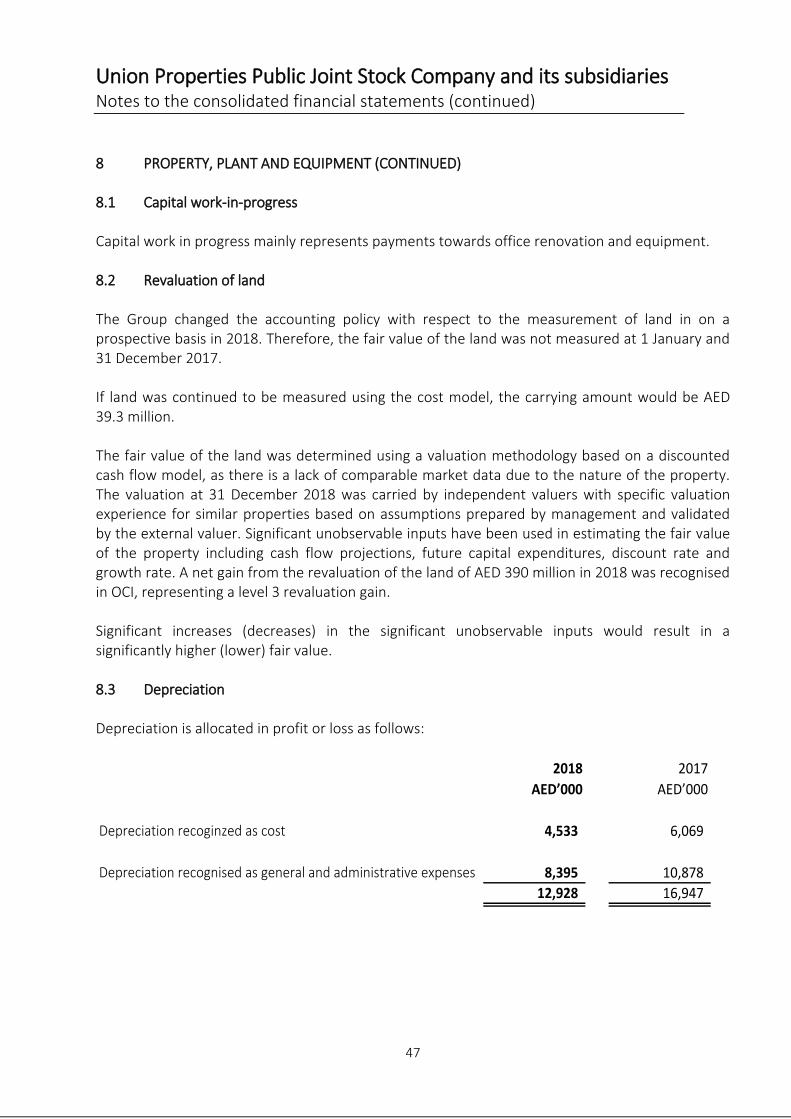

At 31 December 2018, land is measured at fair value less accumulated impairment losses recognised after the date of revaluation (2017: land is measured at cost less accumulated impairment losses). Valuation is performed with sufficient frequency to ensure that the carrying amount of a revalued asset does not differ materially from its fair value.

A revaluation surplus is recorded in OCI and credited to the asset revaluation surplus in equity. However, to the extent that it reverses a revaluation deficit of the same asset previously recognised in profit or loss, the increase is recognised in profit and loss. A revaluation deficit is recognised in the consolidated statement of profit or loss, except to the extent that it offsets an existing surplus on the same asset recognised in the asset revaluation surplus.

Any gain or loss on disposal of an item of property, plant and equipment is recognised in profit or loss. Depreciation

Depreciation is recognised in the profit or loss on a straight-line basis over the estimated useful life of each part of an item of property, plant and equipment. Land is not depreciated. The estimated useful lives for the current and comparative periods are as follows:

Assets Number of years

Buildings and leasehold improvements 3 to 20

Plant and machinery 5 to 10

Furniture, fixtures and office equipments 2 to 4

Motor vehicles 4

Equipment and tools 2 to 3

The depreciation method, useful lives and residual values are reassessed at the reporting date.

Capital work-in-progress

Capital work-in-progress is stated at cost less accumulated impairment losses (refer accounting policy on impairment), if any, until the construction is complete. Upon completion of construction, the cost of such asset together with the cost directly attributable to construction (including borrowing costs and land rent capitalised) are transferred to the respective class of assets. No depreciation is charged on capital work-in-progress.

26

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.1 Summary of significant accounting policies (continued) Investment properties

Recognition

Land and buildings owned by the Group for the purposes of generating rental income or capital appreciation or both are classified as investment properties. Properties that are being constructed or developed for future use as investment properties are also classified as investment properties. Where the Group provides ancillary services to the occupants of a property, it treats such a property as an investment property if the services are a relatively insignificant component of the arrangement as a whole.

When the Group begins to redevelop an existing investment property for continued future use as an investment property, the property remains as an investment property, which is measured based on fair value model and is not reclassified as development property during the redevelopment with respect to as an investment property.

Measurement

Investment properties are initially measured at cost, including related transaction costs. Subsequent to initial recognition, investment properties are stated at fair value, which reflects market conditions at the reporting date. Any gain or loss arising from a change in fair value is recognised in the profit or loss. Fair values are determined based on a semi-annual valuation performed by an accredited external independent valuer applying a valuation model recommended by the International Valuation Standards Committee

Where the fair value of an investment property under development is not reliably determinable, such property is measured at cost until the earlier of the date construction is completed and the date at which fair value becomes reliably measurable.

Transfer from development properties to investment properties

Certain properties held for sale under inventory are transferred from development properties to investment properties when those properties are either released for rental or for capital appreciation or both. The properties held for sale under development properties are transferred to investment properties at cost. Subsequent to initial recognition, such properties are valued at fair value in accordance with the measurement policy for investment properties.

Transfer from investment properties to development properties

When the use of investment properties changes to held for sale, the respective properties are transferred from investment properties to development properties at their fair values on the date of transfer, which becomes its deemed cost for subsequent accounting.

Derecognition

Investment properties are derecognised either when they have been disposed of (i.e., at the date the recipient obtains control) or when they are permanently withdrawn from use and no future economic benefit is expected from their disposal. The difference between the net disposal proceeds and the carrying amount of the asset is recognised in profit or loss in the period of derecognition. The amount of consideration to be included in the gain or loss arising from the derecognition of investment property is determined in accordance with the requirements for determining the transaction price in IFRS 15.

27

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Financial instruments – initial recognition and subsequent measurement A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

i) Financial assets

Initial recognition and measurement Financial assets are classified, at initial recognition, as subsequently measured at amortised cost, fair value through other comprehensive income (OCI), or fair value through profit or loss. The classification of financial assets at initial recognition depends on the financial asset’s contractual cash flow characteristics and the Group’s business model for managing them. With the exception of trade receivables that do not contain a significant financing component or for which the Group has applied the practical expedient, the Group initially measures a financial asset at its fair value plus, in the case of a financial asset not at fair value through profit or loss, transaction costs. Trade receivables that do not contain a significant financing component or for which the Group has applied the practical expedient are measured at the transaction price determined under IFRS 15. Refer to the accounting policies in section Revenue from contracts with customers. In order for a financial asset to be classified and measured at amortised cost or fair value through OCI, it needs to give rise to cash flows that are ‘solely payments of principal and interest (SPPI)’ on the principal amount outstanding. This assessment is referred to as the SPPI test and is performed at an instrument level. The Group’s business model for managing financial assets refers to how it manages its financial assets in order to generate cash flows. The business model determines whether cash flows will result from collecting contractual cash flows, selling the financial assets, or both. Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the market place (regular way trades) are recognised on the trade date, i.e., the date that the Group commits to purchase or sell the asset.

Subsequent measurement Financial assets at amortised cost (debt instruments) The Group measures financial assets at amortised cost if both of the following conditions are met: • The financial asset is held within a business model with the objective to hold financial assets in order to

collect contractual cash flows; and • The contractual terms of the financial asset give rise on specified dates to cash flows that are solely

payments of principal and interest on the principal amount outstanding Financial assets at amortised cost are subsequently measured using the effective interest rate (EIR) method and are subject to impairment. Gains and losses are recognised in profit or loss when the asset is derecognised, modified or impaired. The Group’s financial assets at amortised cost includes trade receivables, retentions receivable, contract assets, rent receivable and due from related parties.

28

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Financial instruments – initial recognition and subsequent measurement (continued) i) Financial assets (continued)

Subsequent measurement (continued)

Financial assets at fair value through profit or loss Financial assets at fair value through profit or loss include financial assets held for trading, financial assets designated upon initial recognition at fair value through profit or loss, or financial assets mandatorily required to be measured at fair value. Financial assets are classified as held for trading if they are acquired for the purpose of selling or repurchasing in the near term. Derivatives, including separated embedded derivatives, are also classified as held for trading unless they are designated as effective hedging instruments. Financial assets with cash flows that are not solely payments of principal and interest are classified and measured at fair value through profit or loss, irrespective of the business model. Notwithstanding the criteria for debt instruments to be classified at amortised cost or at fair value through OCI, as described above, debt instruments may be designated at fair value through profit or loss on initial recognition if doing so eliminates, or significantly reduces, an accounting mismatch. Financial assets at fair value through profit or loss are carried in the consolidated statement of financial position at fair value with net changes in fair value recognised in the consolidated statement of income. Derecognition A financial asset (or, where applicable, a part of a financial asset or part of a group of similar financial assets) is primarily derecognised (i.e., removed from the Group’s consolidated statement of financial position) when: • The rights to receive cash flows from the asset have expired; or • The Group has transferred its rights to receive cash flows from the asset or has assumed an obligation

to pay the received cash flows in full without material delay to a third party under a ‘pass-through’ arrangement; and either (a) the Group has transferred substantially all the risks and rewards of the asset, or (b) the Group has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

When the Group has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, it evaluates if, and to what extent, it has retained the risks and rewards of ownership. When it has neither transferred nor retained substantially all of the risks and rewards of the asset, nor transferred control of the asset, the Group continues to recognise the transferred asset to the extent of its continuing involvement. In that case, the Group also recognises an associated liability. The transferred asset and the associated liability are measured on a basis that reflects the rights and obligations that the Group has retained. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Group could be required to repay.

29

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Financial instruments – initial recognition and subsequent measurement (continued) i) Financial assets (continued) Impairment of financial assets

The Group recognises an allowance for expected credit losses (ECLs) for all debt instruments not held at fair value through profit or loss. ECLs are based on the difference between the contractual cash flows due in accordance with the contract and all the cash flows that the Group expects to receive, discounted at an approximation of the original effective interest rate. The expected cash flows will include cash flows from the sale of collateral held or other credit enhancements that are integral to the contractual terms. ECLs are recognised in two stages. For credit exposures for which there has not been a significant increase in credit risk since initial recognition, ECLs are provided for credit losses that result from default events that are possible within the next 12-months (a 12-month ECL). For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses expected over the remaining life of the exposure, irrespective of the timing of the default (a lifetime ECL). For trade receivables and contract assets, including receivables from sale of real estate properties that contain a significant financing component, the Group applies a simplified approach in calculating ECLs. Therefore, the Group does not track changes in credit risk, but instead recognises a loss allowance based on lifetime ECLs at each reporting date. The Group has established a provision matrix that is based on its historical credit loss experience, adjusted for forward-looking factors specific to the debtors and the economic environment. A financial asset is written off when there is no reasonable expectation of recovering the contractual cash flows. ii) Financial liabilities Initial recognition and measurement Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. All financial liabilities are recognised initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs. The Group’s financial liabilities include trade and other payables, loans and borrowings including bank overdrafts, and contingent consideration at fair value through profit or loss.

30

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Financial instruments – initial recognition and subsequent measurement (continued) ii) Financial liabilities (continued) Subsequent measurement The measurement of financial liabilities depends on their classification, as described below: Trade and other payables Liabilities are recognised for amounts to be paid in the future for goods or services received, whether billed by the supplier or not. Trade and other payables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method. Loans and borrowings After initial recognition, interest-bearing loans and borrowings are subsequently measured at amortised cost using the EIR method. Gains and losses are recognised in profit or loss when the liabilities are derecognised as well as through the EIR amortisation process. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included as finance costs in the statement of profit or loss. Derecognition A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognised in the statement of profit or loss. iii) Offsetting of financial instruments Financial assets and financial liabilities are offset and the net amount is reported in the consolidated statement of financial position if there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, to realise the assets and settle the liabilities simultaneously.

Cash and cash equivalents

Cash and cash equivalents comprise cash in hand and at bank in current and deposit accounts (having a maturity of three months or less and excluding deposits held under lien). Bank overdrafts that are repayable on demand and bills discounted having a maturity of three months or less form an integral part of the Group’s cash management and are included as a component of cash and cash equivalents for the purpose of the statement of cash flows.

31

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued)

Impairment of non-financial assets

The Group assesses, at each reporting date, whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Group estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or CGUs fair value less costs to sell and its value in use. Recoverable amount is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. When the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. In determining fair value less costs to sell, recent market transactions are taken into account. If no such transactions can be identified, an appropriate valuation model is used. These calculations are corroborated by valuation multiples, quoted share prices for publicly traded companies or other available fair value indicators. The Group bases its impairment calculation on detailed budgets and forecast calculations, which are prepared separately for each of the Group’s CGUs to which the individual assets are allocated. These budgets and forecast calculations generally cover a period of one to five years. For longer periods, a long-term growth rate is calculated and applied to project future cash flows after the fifth year. Impairment losses are recognised in the consolidated statement of other comprehensive income in expense categories consistent with the function of the impaired asset. For assets excluding goodwill, an assessment is made at each reporting date to determine whether there is an indication that previously recognised impairment losses no longer exist or have decreased. If such indication exists, the Group estimates the asset’s or CGU’s recoverable amount. A previously recognised impairment loss is reversed only if there has been a change in the assumptions used to determine the asset’s recoverable amount since the last impairment loss was recognised. The reversal is limited so that the carrying amount of the asset does not exceed its recoverable amount, nor exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the consolidated statement of other comprehensive income unless the asset is carried at a revalued amount, in which case, the reversal is treated as a revaluation increase. Inventories

Inventories are valued at the lower of cost and net realisable value.

Properties held for sale

Properties held for sale are classified as inventories and stated at the lower of cost and net realisable value. Cost includes the aggregate cost of development, borrowing costs capitalised and other direct expenses. Net realisable value is estimated by the management, taking into account the expected price which can be ultimately achieved, based on prevailing market conditions.

32

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued) Inventories (continued) Properties held for sale (continued) The amount of any write down of properties under development for sale is recognised as an expense in the period the write down or loss occurs. The amount of any reversal of any write down arising from an increase in net realisable value is recognised in profit or loss in the period in which the increase occurs.

Other inventories

The cost of other inventories is based on the first-in-first-out method and includes expenditure incurred in acquiring inventories and bringing them to their existing location and condition. Net realisable value is the estimated selling price in the ordinary course of business less the estimated costs of completion and selling expenses.

Provision

A provision is recognised in the consolidated statement of financial position when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable that an outflow of economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation.

Provision for contract maintenance

Provision for contract maintenance is recognised when the underlying contract enters the maintenance period. The provision is made on a case-by-case basis for each job where the maintenance period has commenced and is based on historical maintenance cost data and an assessment of all possible outcomes against their associated probabilities.

Operating lease payments

Group as a lessee Leases of assets under which the lessor effectively retains all the risks and rewards of ownership are classified as operating leases. Payments made under operating leases are recognised in the profit or loss on a straight-line basis over the term of the lease. Lease incentives allowed by the lessor are recognised in the profit or loss as an integral part of the total lease payments made. Group as a lessor Leases in which the Group does not transfer substantially all the risks and rewards of ownership of an asset are classified as operating leases. Rental income arising is accounted for on a straight-line basis over the lease terms and is included in revenue in the statement of profit or loss due to its operating nature. Initial direct costs incurred in negotiating and arranging an operating lease are added to the carrying amount of the leased asset and recognised over the lease term on the same basis as rental income. Contingent rents are recognised as revenue in the period in which they are earned.

33

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.1 Summary of significant accounting policies (continued) Earnings per share

The Group presents basic and diluted earnings per share (“EPS”) data for its ordinary shares. Basic earnings per share is calculated by dividing the profit or loss attributable to ordinary shareholders of the Group by the weighted average number of ordinary shares outstanding during the period. Diluted earnings per share is determined by adjusting the profit or loss attributable to ordinary shareholders and the weighted average number of ordinary shares outstanding for the effects of all dilutive potential ordinary shares.

Segment reporting

An operating segment is a component of the Group that engages in business activities from which it may earn revenues and incur expenses, including revenues and expenses that relate to transactions with any of the Group’s other components. The results of the operating segments are reviewed regularly by the Board of Directors to make decisions about resources to be allocated to the segment and to assess its performance, and for which discrete financial information is available.

Segment results, assets and liabilities include items directly attributable to a segment as well as those that can be allocated on a reasonable basis.

Segment capital expenditure is the total cost incurred during the year to acquire property, plant and equipment, costs incurred for purchase of investment properties or redevelopment of existing investment properties and costs incurred towards development of properties which are either intended to be sold or transferred to investment properties. 3.2 Changes in accounting policies and disclosures Revaluation of land under property, plant and equipment The Group re-assessed its accounting for property, plant and equipment with respect to measurement of land under property, plant and equipment after initial recognition. The Group had previously measured land under property, plant and equipment using the cost model whereby, after initial recognition of the asset classified as property, plant and equipment, the asset was carried at cost less accumulated impairment losses. In the last quarter of 2018, the Group elected to change the method of accounting for land classified as property, plant and equipment, as the Group believes that the revaluation model provides more relevant information to the users of its consolidated financial statements. In addition, available valuation techniques provide reliable estimates of land’s fair value. The Group applied the revaluation model prospectively. After initial recognition, land is measured at fair value at the date of the revaluation less any subsequent accumulated impairment losses. As a result of the change in the accounting policy, a revaluation adjustment of AED 390 million was recorded in OCI.

34

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.2 Changes in accounting policies and disclosures (continued) New and amended standards and interpretations The Group applied for the first time certain standards and amendments, which are effective for annual periods beginning on or after 1 January 2018. The Group has not early adopted any other standard, interpretation or amendment that has been issued but is not yet effective. Although these new standards and amendments applied for the first time in 2018, they did not have a material impact on the annual consolidated financial statements of the Group. The nature and the impact of each new standard or amendment is described below:

IFRS 9 Financial Instruments

IFRS 9 Financial Instruments replaces IAS 39 Financial Instruments: Recognition and Measurement for annual periods beginning on or after 1 January 2018, bringing together all three aspects of the accounting for financial instruments: classification and measurement; impairment; and hedge accounting.

The Group applied IFRS 9 retrospectively, with the initial application date of 1 January 2018 and adjusting the comparative information for the period beginning 1 January 2017. However, the adoption of IFRS 9 did not have any impact on the Group’s consolidated financial statements, and accordingly, the comparative information was not restated.

Classification – financial assets

Under IFRS 9, debt instruments are subsequently measured at fair value through profit or loss, amortised cost, or fair value through OCI. The classification is based on two criteria: the Group’s business model for managing the assets; and whether the instruments’ contractual cash flows represent ‘solely payments of principal and interest’ on the principal amount outstanding. The assessment of the Group’s business model was made as of the date of initial application, 1 January 2018. The assessment of whether contractual cash flows on debt instruments are solely comprised of principal and interest was made based on the facts and circumstances as at the initial recognition of the assets. The classification and measurement requirements of IFRS 9 did not have a significant impact on the Group. The Group continued measuring at fair value all financial assets previously held at fair value under IAS 39. Trade receivables and other current financial assets classified as Loans and receivables as at 31 December 2017 are held to collect contractual cash flows and give rise to cash flows representing solely payments of principal and interest. These are now classified and measured as Debt instruments at amortised cost. The Group has not designated any financial liabilities as at fair value through profit or loss. There are no changes in classification and measurement for the Group’s financial liabilities.

35

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.2 Changes in accounting policies and disclosures (continued) New and amended standards and interpretations (continued) IFRS 9 Financial Instruments (continued)

Impairment

The adoption of IFRS 9 has fundamentally changed the Group’s accounting for impairment losses for financial assets by replacing IAS 39’s incurred loss approach with a forward-looking expected credit loss (ECL) approach. IFRS 9 requires the Group to recognise an allowance for ECLs for all debt instruments not held at fair value through profit or loss and contract assets.

Upon the adoption of IFRS 9, management performed an impairment loss assessment on the Group’s Trade and other receivables as at 1 January and 31 December 2017. However, the adoption of IFRS 9 did not result in any additional impairment losses to be recognised on the Group’s Trade and other receivables prior to the application date. IFRS 15 Revenue from Contracts with Customers

IFRS 15 supersedes IAS 11 Construction Contracts, IAS 18 Revenue and related Interpretations and it applies, with limited exceptions, to all revenue arising from contracts with its customers. IFRS 15 establishes a five-step model to account for revenue arising from contracts with customers and requires that revenue be recognised at an amount that reflects the consideration to which an entity expects to be entitled in exchange for transferring goods or services to a customer.

IFRS 15 requires entities to exercise judgement, taking into consideration all of the relevant facts and circumstances when applying each step of the model to contracts with their customers. The standard also specifies the accounting for the incremental costs of obtaining a contract and the costs directly related to fulfilling a contract. In addition, the standard requires extensive disclosures.

The Group adopted IFRS 15 using the full retrospective method of adoption. However, the effect of the adoption of IFRS 15 on the Group’s consolidated financial statements was limited to reclassification of certain items in the consolidated statement of financial position with no effect on the previously reported profit and net assets of the Group. In the consolidated statement of financial position, ‘Contract work in progress’ and ‘Deposits and advances’ have been categorised as ‘Contract assets’ and ‘Contract liabilities’, respectively, under IFRS 15, with no changes in the previously reported amounts, except for an amount of AED 5.6 million that was reclassified from Contract liabilities to Trade and other payables representing deposits received from customers without a corresponding performance obligation. The change did not have any impact on OCI or the consolidated statement of cash flows for the year ended 31 December 2017.

36

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

3.2 Changes in accounting policies and disclosures (continued) New and amended standards and interpretations (continued)

IFRIC Interpretation 22 Foreign Currency Transactions and Advance Considerations The Interpretation clarifies that, in determining the spot exchange rate to use on initial recognition of the related asset, expense or income (or part of it) on the derecognition of a non-monetary asset or non-monetary liability relating to advance consideration, the date of the transaction is the date on which an entity initially recognises the non-monetary asset or non-monetary liability arising from the advance consideration. If there are multiple payments or receipts in advance, then the entity must determine the date of the transactions for each payment or receipt of advance consideration. This Interpretation does not have any impact on the Group’s consolidated financial statements.

Amendments to IAS 40 Transfers of Investment Property The amendments clarify when an entity should transfer property, including property under construction or development into, or out of investment property. The amendments state that a change in use occurs when the property meets, or ceases to meet, the definition of investment property and there is evidence of the change in use. A mere change in management’s intentions for the use of a property does not provide evidence of a change in use. These amendments did not have any impact on the Group’s consolidated financial statements given that all transfers from/to investment properties are based on evidence of the change in use.

Amendments to IFRS 2 Classification and Measurement of Share-based Payment Transactions The IASB issued amendments to IFRS 2 Share-based Payment that address three main areas: the effects of vesting conditions on the measurement of a cash-settled share-based payment transaction; the classification of a share-based payment transaction with net settlement features for withholding tax obligations; and accounting where a modification to the terms and conditions of a share-based payment transaction changes its classification from cash settled to equity settled. On adoption, entities are required to apply the amendments without restating prior periods, but retrospective application is permitted if elected for all three amendments and other criteria are met. These amendments are not relevant to the Group.

Amendments to IFRS 4 Applying IFRS 9 Financial Instruments with IFRS 4 Insurance Contracts The amendments address concerns arising from implementing the new financial instruments standard, IFRS 9, before implementing IFRS 17 Insurance Contracts, which replaces IFRS 4. The amendments introduce two options for entities issuing insurance contracts: a temporary exemption from applying IFRS 9 and an overlay approach. These amendments are not relevant to the Group.

Amendments to IAS 28 Investments in Associates and Joint Ventures - Clarification that measuring investees at fair value through profit or loss is an investment-by-investment choice The amendments clarify that an entity that is a venture capital organisation, or other qualifying entity, may elect, at initial recognition on an investment-by-investment basis, to measure its investments in associates and joint ventures at fair value through profit or loss. If an entity that is not itself an investment entity, has an interest in an associate or joint venture that is an investment entity, then it may, when applying the equity method, elect to retain the fair value measurement applied by that investment entity associate or joint venture to the investment entity associate’s or joint venture’s interests in subsidiaries. This election is made separately for each investment entity associate or joint venture, at the later of the date on which: (a) the investment entity associate or joint venture is initially recognised; (b) the associate or joint venture becomes an investment entity; and (c) the investment entity associate or joint venture first becomes a parent. These amendments do not have any impact on the Group’s consolidated financial statements.

37

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued)

3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.2 Changes in accounting policies and disclosures (continued) New and amended standards and interpretations (continued) Amendments to IFRS 1 First-time Adoption of International Financial Reporting Standards - Deletion of short- term exemptions for first-time adopters Short-term exemptions in paragraphs E3–E7 of IFRS 1 were deleted because they have now served their intended purpose. These amendments do not have any impact on the Group’s consolidated financial statements. Standards issued but not yet effective The standards and interpretations that are issued, but not yet effective, up to the date of issuance of the Group’s consolidated financial statements are disclosed below. The Group intends to adopt these standards, if applicable, when they become effective. IFRS 16 Leases IFRS 16 was issued in January 2016 and it replaces IAS 17 Leases, IFRIC 4 Determining whether an Arrangement contains a Lease, SIC-15 Operating Leases-Incentives and SIC-27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease. IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases and requires lessees to account for all leases under a single on-balance sheet model similar to the accounting for finance leases under IAS 17. The standard includes two recognition exemptions for lessees – leases of ’low-value’ assets (e.g., personal computers) and short-term leases (i.e., leases with a lease term of 12 months or less). At the commencement date of a lease, a lessee will recognise a liability to make lease payments (i.e., the lease liability) and an asset representing the right to use the underlying asset during the lease term (i.e., the right-of-use asset). Lessees will be required to separately recognise the interest expense on the lease liability and the depreciation expense on the right-of-use asset. Lessees will be also required to remeasure the lease liability upon the occurrence of certain events (e.g., a change in the lease term, a change in future lease payments resulting from a change in an index or rate used to determine those payments). The lessee will generally recognise the amount of the remeasurement of the lease liability as an adjustment to the right-of-use asset. Lessor accounting under IFRS 16 is substantially unchanged from today’s accounting under IAS 17. Lessors will continue to classify all leases using the same classification principle as in IAS 17 and distinguish between two types of leases: operating and finance leases. IFRS 16, which is effective for annual periods beginning on or after 1 January 2019, requires lessees and lessors to make more extensive disclosures than under IAS 17. Transition to IFRS 16 The Group plans to adopt IFRS 16 retrospectively with the cumulative effect of initially applying IFRS 16, if any, recognised as an adjustment to the opening balance of retained earnings.

38

Union Properties Public Joint Stock Company and its subsidiaries

Notes to the consolidated financial statements (continued) 3 SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) 3.2 Changes in accounting policies and disclosures (continued) Standards issued but not yet effective (continued) IFRS 16 Leases (continued) Transition to IFRS 16 (continued) The Group will elect to use the exemptions proposed by the standard on lease contracts for which the lease terms ends within 12 months as of the date of initial application, and lease contracts for which the underlying asset is of low value. The Group is in the process of finalizing the analysis of the impact of IFRS 16 at the date of issuance of these consolidated financial statements, and is planning to make use of one or more of the practical expedients allowed by the standard. In summary, the application of IFRS 16 is not expected to have a material impact on the Group’s consolidated financial statements given that the Group’s significant lease contracts are short-term in nature and the Group conducts its business operations primarily through owned properties. Other amendments and improvements The following amendments and improvements are not expected to have any significant impact on the Group’s consolidated financial statements when they become effective:

• IFRIC Interpretation 23 Uncertainty over Income Tax Treatments: effective for annual periods beginning on or after 1 January 2019

• Prepayment Features with Negative Compensation - Amendments to IFRS 9: effective for annual periods beginning on or after 1 January 2019

• Long-term Interests in Associates and Joint Ventures - Amendments to IAS 28: effective for annual periods beginning on or after 1 January 2019

• Plan Amendment, Curtailment or Settlement - Amendments to IAS 19: effective for annual periods beginning on or after 1 January 2019

• AIP IFRS 3 Business Combinations - Previously held Interests in a joint operation: effective for annual periods beginning on or after 1 January 2019

• AIP IFRS 11 Joint Arrangements - Previously held Interests in a joint operation: effective for annual periods beginning on or after 1 January 2019

• AIP IAS 12 Income Taxes - Income tax consequences of payments on financial instruments classified as equity: effective f or annual periods beginning on or after 1 January 2019

• AIP IAS 23 Borrowing Costs - Borrowing costs eligible for capitalisation: effective for annual periods beginning on or after 1 January 2019

• The Conceptual Framework for Financial Reporting: effective for annual periods beginning on or after 1 January 2020