37

Mergers & Acquisitions Restructuring & Cooperative Strategies Unit 11 Lecture by Prof.Rajat Shuvro Bakshi

Mergers & Acquisitions Restructuring &

Cooperative Strategies

Unit 11

Lecture by Prof.Rajat Shuvro Bakshi

The Strategic Management Process

Mission Objectives

ExternalAnalysis

InternalAnalysis

StrategicChoice

StrategyImplementation

CompetitiveAdvantage

Corporate LevelStrategy

Which Businessesto Enter?

• Vertical Integration

• Diversification

• Strategic Alliances

Mode of Entry?

• Mergers & Acquisitions

Logic of Corporate Level Strategy Applies

• Corporate Level Strategy Should Create Value

– Such that the value of the corporate whole increases

– Such that businesses forming the corporate whole are worth more than they would be under independent owners

– That equity holders cannot create through portfolio investment

Mergers & Acquisitions Defined(1 of 3)

Mergers Acquisitions

• two firms are combined ona relatively co-equal basis

• one firm buys anotherfirm

• the words are often used interchangeably eventhough they mean something very different

• merger sounds more amicable, less threatening

Mergers & Acquisitions Defined(2 of 3)

• parent stocks are usuallyretired and new stock issued

• name may be one of the parents’ or a combination

• can be a controllingshare, a majority, or all of the target firm’sstock

• can be friendly orhostile

Mergers Acquisitions

• usually done througha tender offer

• one of the parents usuallyemerges as the dominantmanagement

Mergers & Acquisitions Defined(3 of 3)

Types of M&A Activity

Vertical

Horizontal

Product Extension

Market Extension

Conglomerate

» suppliers or customers

» competitors

» complementary products

» complementary markets

» everything else

Related

Unrelated

Do Mergers and Acquisitions Create Value(1 of 4)

The Logic

Unrelated M&A Activity

• there would be no expectation of value creationdue to the lack of synergies between businesses

• there might be value creation due to efficienciesfrom an internal capital market

• there might be value creation due to the exploitationof a conglomerate discount

• a corporate raider who buys and restructures firms

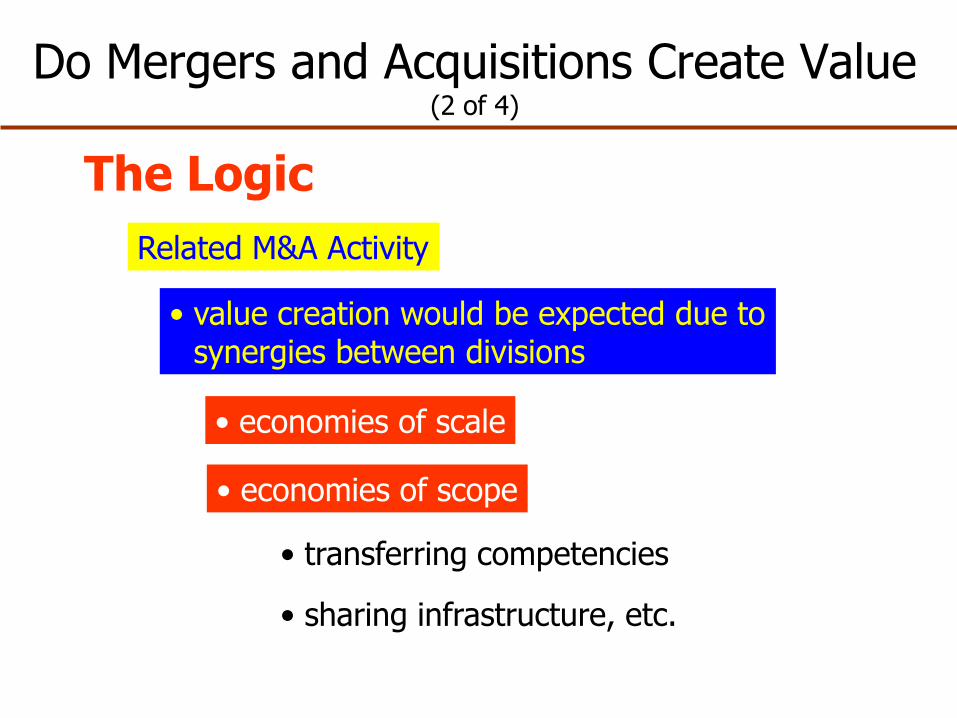

Do Mergers and Acquisitions Create Value(2 of 4)

The Logic

Related M&A Activity

• value creation would be expected due tosynergies between divisions

• economies of scale

• economies of scope

• transferring competencies

• sharing infrastructure, etc.

Do Mergers and Acquisitions Create Value(3 of 4)

The Empirical Evidence

• this reflects the market’s assessment of theexpected value of the merger or acquisition

• these studies look at what happens to the priceof both the acquirer’s stock and the target’s stock

• thus, we can see who is capturing any expectedvalue that may be created

Research is based on stock market reaction to the announcement of M&A activity

Do Mergers and Acquisitions Create Value(4 of 4)

The Empirical Evidence

AcquiringFirms

TargetFirms

M&A Activity creates value, on average, as follows:

• no value created • value increases byabout 25%

• related M&A activity creates more value thanunrelated M&A activity

M&A activity creates value, but target firms capture it

Why Is M&A Activity So Prevalent?(1 of 3)

If managers know that acquiring firms do notcapture any value from M&A’s, why do theycontinue to merge and acquire?

Survival

Free CashFlow

• cash generating, normal return investment

• avoid competitive disadvantage

• avoid scale disadvantages

Why Is M&A Activity So Prevalent?(2 of 3)

If managers know that acquiring firms do notcapture any value from M&A’s, why do theycontinue to merge and acquire?

AgencyProblems

ManagerialHubris

• managers benefit from increases in size

• managers benefit from diversification

• managers believe they can beat the odds

Why Is M&A Activity So Prevalent?(3 of 3)

If managers know that acquiring firms do notcapture any value from M&A’s, why do theycontinue to merge and acquire?

Above NormalProfits

• proposed M&A activity may satisfythe logic of corporate level strategy

• managers may see economies thatthe market can’t see

• some M&A activity does generateabove normal profits (expected andoperational over the long run)

Specific Advantages of Mergers & Acquisitions

• Reducing competition

• Getting access to proprietary products or services

• Gaining access to new products of services

• Gaining access to new products and markets

• Access to technical expertise

• Access to an established brand name

• Economies of scale

• Diversification of business risk

Specific Disadvantage of Mergers & Acquisitions

• Incompatibility of top management

• Clash of corporate cultures

• Operational problems

• Increased business complexity

• Loss of organizational flexibility

• Antitrust implications

Mergers and AcquisitionsCompleting the Acquisition of Another Firm

Step 1 Step 2

Step 4

Step 9Step 8Step 7

Step 5

Step 3

Step 6

Meet with the top management team of the acquisition

target

Assess the mood of the acquisition

target

Identify sources of financing for the

transaction

Continue negotiations

Make an offer to purchase if

acceptable terms are available

Negotiate a non-compete agreement

with the key employees of the

target firm that will be retained

Retain an attorney to prepare

documents for closing

Meet as soon as possible with all

affected employees

Implement the plan for the acquired

firm

Competitive Advantage(1 of 6)

Yes, if managers’ abilities meet VRIO criteria

Can an M&A strategy generate sustainedcompetitive advantage?

2 Managers may be good at doing ‘deals’

1 Managers may be good at recognizing & exploitingpotentially value-creating economies with other firms

3 Managers may be good at both

18

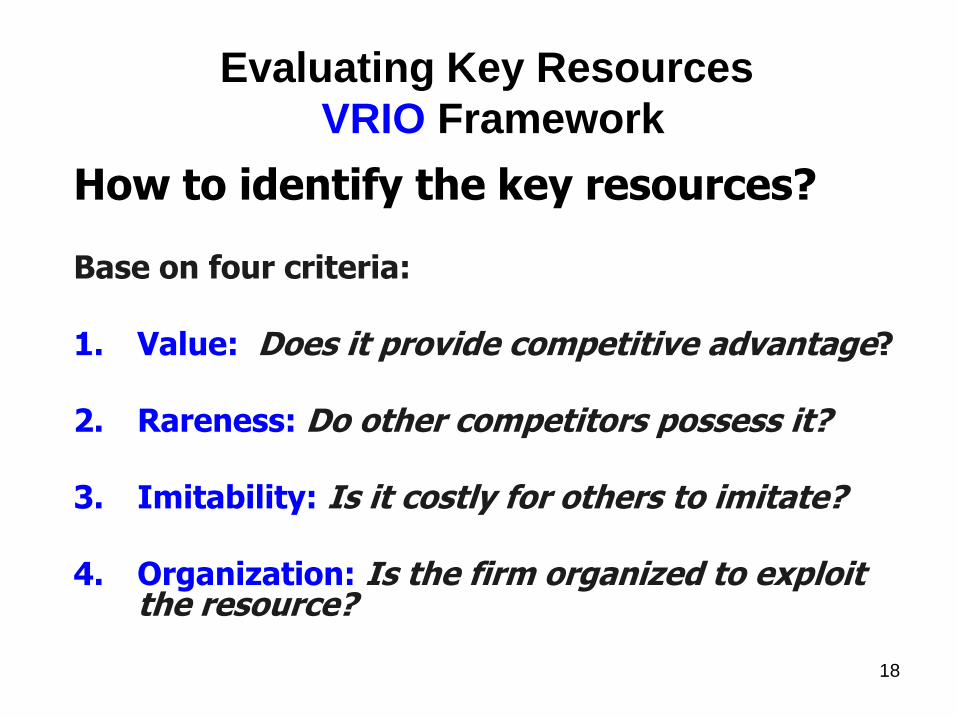

Evaluating Key Resources

VRIO Framework

How to identify the key resources?

Base on four criteria:

1. Value: Does it provide competitive advantage?

2. Rareness: Do other competitors possess it?

3. Imitability: Is it costly for others to imitate?

4. Organization: Is the firm organized to exploit the resource?

Competitive Advantage(2 of 6)

Recognizing and Exploiting Economies of Scope

Private Economies

Firm A

Firm B

Firm C

• Firm C’s recognizedvalue is Rs.120,000

Bidders Target

• Firm A sees valueof Rs.15,000 in Firm C

Competitive Advantage(3 of 6)

Recognizing and Exploiting Economies of Scope

Costly-to-Imitate

Economies

Firm A

Firm B

Firm C

Bidders Target

• if the economy

between A & C

is costly to imitate,

it doesn’t matter

if other firms know

• Firm A can still earn

a Rs.20,000 profit

Competitive Advantage(4 of 6)

Recognizing and Exploiting Economies of Scope

Firm A

Firm B

Firm C

Bidders Target

Unexpected

Economies

• Firm C has a market

value of Rs.100,000

• Firm A buys Firm C

for Rs.100,000

• Firm C turns out to be

worth Rs.120,000Rs.120,000

Competitive Advantage(5 of 6)

Doing the Deal

Bidding Firm’s

Perspective

Search for

Rare Economies

Limit Information

to Other Bidders

Limit Information

to the Target

Avoid Bidding

Wars

Close the

Deal Quickly

Seek Thinly

Traded Markets

Competitive Advantage(6 of 6)

Doing the Deal

Target Firm’s

Perspective

Seek Information

from Bidders

Invite Other Bidders to

Join in Bidding Contest

Delay, But Do Not

Stop the Acquisition

Implementation Issues(1 of 2)

Structure, Control, and Compensation

M&A activity requires responses to these issues:

• m-form structure is typically used

• management controls & compensation policies

are similar to those used in diversification strategies

Managers must decide on the level of integration:

• target firm may remain somewhat autonomous

• target firm may be completely integrated

Implementation Issues(2 of 2)

Cultural Differences

• high levels of integration require greater cultural

blending

• cultural blending may be a matter of:

• combining elements of both cultures

• essentially replacing one culture with the other

• integration may be very costly, often unanticipated

• the ability to integrate efficiently may be a source

of competitive advantage

The fundamental principle of any economic activity is that no man you transact with will lose; then you shall not.

Kautilya’s Arthasastra (370 BC)

Adding value through Strategic Alliances(One of the Cooperative Strategies)

Cooperative Strategy

• Cooperative strategy is a strategy in which firms

– work together

– to achieve a shared objective

• Cooperating with other firms is a strategy that

– creates value for a customer

– exceeds the cost of constructing customer

value in other ways

– establishes a favorable position relative to

competition

What makes alliances

succeed?

• Sound strategic footing

– Relation-specific assets

– Knowledge-sharing routines

– Complementary resources and

capabilities

– Effective governance

• Solid, principled implementation

– The eight I’s of successful We’s

Relation-specific assets

• Site specific assets—co-locating plants

– (Sharing Natural Resources, Singrauli Coal

Fields)

• Physical asset specificity—dedicated

machinery

– (NTPC and NPCIL)

• Human asset specificity—learning by

doing

– (Singhreni Coalfields & NTPC)

Knowledge-sharing routines

• Information sharing

• Know-how creation

• Absorptive capacity in the partners

• Who knows what and where

expertise lies

Complementary resources and

capabilities• Strategic complementarity:

– The alliance combines resources and skills

that are more valuable in combination than

individually

– Nestle and Coca-Cola in Japan

• Organizational Complementarity:

– Systems, styles, and cultures compatible

enough to realize joint gains

Effective governance

• Contracts as a basis for alliances

– Allows for 3rd party enforcement

– Difficult to structure for all contingencies

• Self-enforcement

– Mutual investments in ownership or assets

– Trust the key element

– Reputation the wedge

Self enforcement is cheaper and creates more gains

The eight I’s of successful

WE’s1. Individual

Excellence– Both add value

2. Importance– Fits with strategic

objectives

3. Interdependence– Both need each other

4. Investment– Investment signals

commitment

5. Information– Open communication

6. Integration– Shared systems for

smooth operation

7. Institutionalization– Formal relationship

status

8. Integrity– Honorable actions, no

abuse or effort to undermine other

Alliance success factors

• Have a clear strategic purposeAlliances are never an end in themselves – they ought to be tools in service of a business strategy

• Find a fitting partnerThis means a partner with compatible goals and complementary

capabilities

• SpecializeAllocate tasks and responsibilities in the alliances in a way that

enables each party to do what it does best

• Create incentives for cooperationWorking together never happens automatically, particularly not

when partners were former rivals

• Minimize conflicts between partnersThe scope of alliance and of partners’ roles should avoid pitting

one against the other in the market

Alliance success factors(Continued)

• Share informationContinual communication develops trust and also keeps joint

projects on target

• Exchange personnelRegardless of the form of alliance, personal contact and site visits

are essential for maintaining communication and trust

• Operate with long term horizonsMutual forbearance in solving short run conflicts is enhanced by

the expectations of future gains

• Develop multiple joint projectsSuccessful cooperation on one project can help partners weather

the storm in less successful joint projects

• Be flexibleAlliances are open ended, dynamic relationships that need to

evolve in pace with their environment and in pursuit of new

opportunities.

Summary: 3 elements

Executives need:1. to pay more attention to strategy,2. be more rigorous in partner choice,

3. to show more finesse with structural issues.

Are these all equally important?

No. They are subsidiary to each other.

NTPC’s Joint Ventures

NTPCJVs

BF-NTPCEnergy

System Ltd49%

NTPCSAIL

Power Co.Pvt. Ltd

50%

UtilityPowertech

Ltd.50%

NTPCTamilnadu

Energy Co.Ltd50%

RatnagiriGas and

Power Pvt Ltd28.33%

PTC IndiaLtd

5.28%

NTPCAlstom

Power ServicesPvt. Ltd

50%

NTPC BHELPower

Projects Pvt. Ltd

50%

Meija UrjaNigamPvt. Ltd

50%

NTPC SCCLGlobal Ventures

Pvt. Ltd50% Aravalli

Power Co.Pvt. Ltd

50%