UNIT-9 Accounting for Receivable & Inventory The term receivable refers to the amounts due from individuals and companies. Receivables are claims that are expected to be collected in cash. Receivable are important because they represent one of a company's most liquid assets. For many companies receivable are also one of the largest assets. Ques. What are the receivable? Ans. Receivables are claims that are expected to be collected in cash. Ques. why are receivable important? 1

Transcript

1

UNIT-9Accounting for Receivable & Inventory

The term receivable refers to the amounts due from individuals and companies. Receivables are claims that are expected to be collected in cash. Receivable are important because they represent one of a company's most liquid assets. For many companies receivable are also one of the largest assets.Ques. What are the receivable?Ans. Receivables are claims that are expected to be collected in cash.Ques. why are receivable important?

2

Ans. Receivable are important because they represent one of a company's most liquid assets.

Kinds of ReceivableReceivables are classified as –

1.Account Receivable 2. Note Receivable3.Other Receivable Account Receivable Money which is owed to a company by a customer for the

products and services provided on credit. This is often treated as a current asset on a balance sheet.

A specific sale is generally only treated as an accounting receivable after the customer is sent an invoice.

In brief account receivable are amounts customers owe-

3

On account. They result from the sale of goods and services.

Ques. What are the different kinds of receivable?Ans. There are three kinds of receivable namely- 1.Account Receivable 2. Note Receivable3.Other ReceivableQues. What is meant by account receivable?Ans. Account Receivable is the amount customers owe on

account and that is the result from the sale of goods and services.

4

Note ReceivableA note receivable is a written promise to receive a

specific amount of cash from another party on one or more future dates. This is treated as an asset by the holder of the note. The payee is the party who receives payment under the term of the note and the maker is the party obliged to send funds to the payee.

Ques. What is note receivable?Ans. A note receivable is a written promise to receive a

specific amount of cash from another party on one or more future dates.

Ques. Is note receivable an asset or liability in the hand of holder?

Ans. Note Receivable is an asset in the hand of holder.

5

Ques. Is note receivable an asset or liability in hand of maker ?Ans. Note Receivable is a liability in the hand of maker. Other ReceivablesOther receivables include non-trade receivables such as interest

receivable ,loan to company's officers , advances to employees and income taxes refundable.

These do not generally result from the operation of the business. Therefore, they are generally classified and reported as separate items in the balance sheet.

Ques. What do you know about other receivables?Ans. Various form of non- trade receivable are called other

receivable. For example interest receivable ,loan to company's officers , advances to employees and income taxes refundable etc.

6

Accounting Issues Associated With Account ReceivableThere are three accounting issues associated with

forward. A service organisation records a receivable when it performs service on account. A merchandiser

records account receivable at the time of sale of merchandise on account. When goods are sold the following entry is recorded.

7

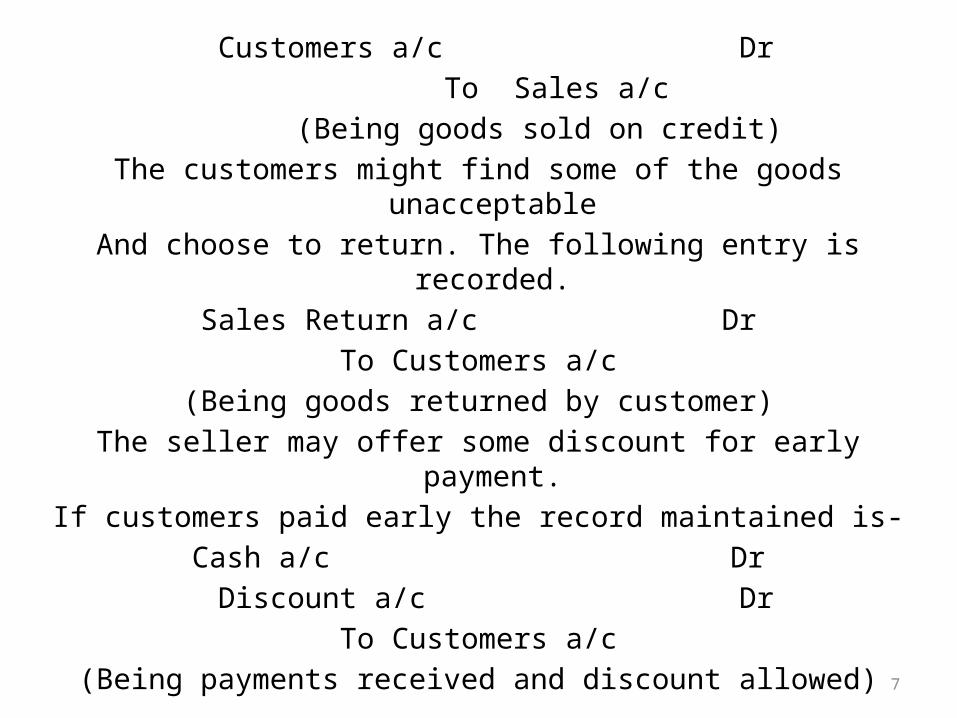

Customers a/c Dr To Sales a/c

(Being goods sold on credit)The customers might find some of the goods unacceptable

And choose to return. The following entry is recorded.Sales Return a/c Dr

To Customers a/c(Being goods returned by customer)

The seller may offer some discount for early payment.If customers paid early the record maintained is-

Cash a/c Dr Discount a/c Dr

To Customers a/c(Being payments received and discount allowed)

8

Valuing Accounts ReceivableSome times amount due from customers are not receivable due

to different reasons. These uncollectibleamount is called bad-debts.Two methods are used in accounting for uncollectible accounts

i.e. (1) the direct write - off method and (2) the allowance method. Direct write - off Method for Uncollectible AccountsUnder this method the uncollectible amount is transferredTo bad – debts account and write-off by following entry. Bad-Debts a/c Dr To Customer’s a/c ( Being bad-debts provided for)

9

Allowance Method for Uncollectible AccountsUnder the allowance method if a specific customer’s

account receivable is identified as uncollectible, it is written-off by removing the amount from account receivable/ debtors by passing the following entry.

Allowance for Bad-Debts a/c Dr To Customer’s a/c Disposing of Accounts ReceivableThe financial accounting term disposition of accounts

receivable is used to describe several approaches company can take to accelerate the receipt of cash from customers/receivables. The two most common methods

Include factoring and assignment, whereby the company

10

transfer receivables to another party in exchange for cash.The companies sell receivables for two major reasons. FirstThey may be the only reasonable sources of cash. When

money is tight, companies may not be able to borrow money in the usual credit markets, or if money is available, the cost of borrowing may be prohibitive.

A second reason for selling receivable is that billing andCollection are often time consuming and costly. It is often easier for a businessman to sell the receivables to another party with expertise in billing and collection matter.

11

Note ReceivablesThe basic issues in an accounting for notes receivable are

the same as those for accounts receivable: 1. Recognising Notes Receivable 2. Valuing Notes Receivable 3. Disposing of Notes Receivable Recognising Notes ReceivableThe company records the note receivable at its face value,

the amount shown on the face of the note. No interest is reported when the note is accepted, because the

revenue recognition principles does not recognise revenue untill the performance obligation is satisfied. Interest is earned(accrued) as time passes. If a company-

12

Lends money using a note, the following entry is recorded. Note Receivable a/c Dr To Cash a/c (Being loan given by issuing a note receivable) Valuing Notes ReceivableCompanies have two methods available to them for valuing

notes receivable i.e. allowance method and direct write off method. These are explained below-

The Allowance MethodThis method establishes a contra asset account allowancefor doubt full debt account or bad debts provision that has the effect of reducing the balance for account receivable.The amount for bad debt provision can be computed in-

13

two ways-1. By receiving each individual debt and deciding whether it is doubtful(a specific provision)2. By providing for a fixed percentage of total debts. The Direct Write off MethodThis method is simpler than allowance method, in that it allows for one simple entry to reduce account receivableto its net realisable value The entry would consists- Bad Debts a/c Dr To A/R (customers) a/c

14

Disposing of Notes Receivable Notes may held to their maturity date, at which time the

face value plus accrued interest is due. In some situationthe maker of note defaults and the payee must make an Appropriate adjustment. Honour of Account/ Notes ReceivableWhen the payment is made on due date is called the

honour of account/notes receivable. On the collection of money the following record is maintained.

Cash a/c Dr To Note Receivable a/c To Interest a/c (Being note receivable honour with interest)

15

Dishonour of Account/ Notes ReceivableWhen the payment is not made on due date, is called the dishonour. A dishonoured note receivable is no longer

negotiable. However the payee still has a claim againstthe maker of the note for both the note and the interest.Ques. What is honour of receivable?Ans. When amount of account receivable/notes

receivable is paid on due date is called honour of accounts or honour of notes receivable .

Ques. What is dishonour of account?Ans. When amount of account receivable/notes

receivable is not paid on due date is called dihonour of accounts or dihonour of notes receivable .

16

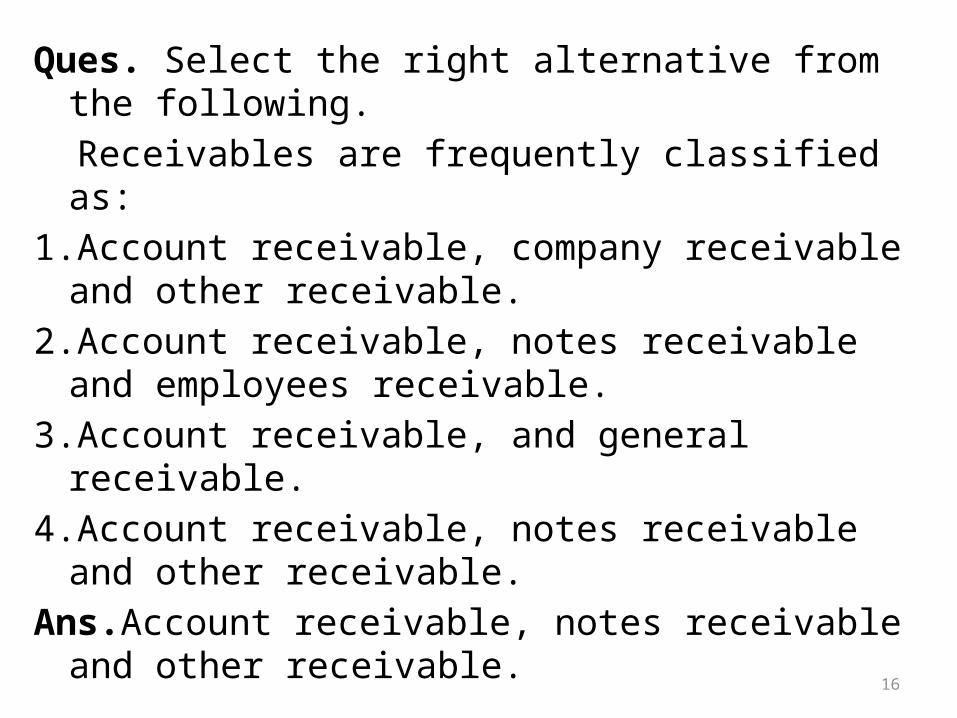

Ques. Select the right alternative from the following. Receivables are frequently classified as:1.Account receivable, company receivable and other

receivable.2.Account receivable, notes receivable and employees

receivable.3.Account receivable, and general receivable.4.Account receivable, notes receivable and other

receivable.Ans.Account receivable, notes receivable and other

receivable.

17

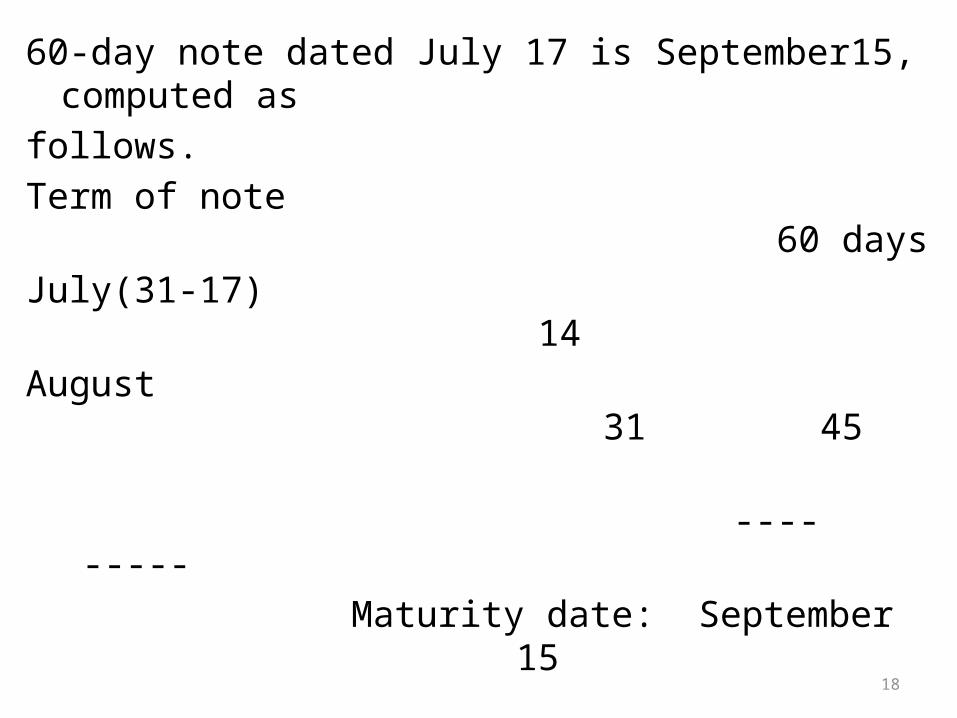

Determining the Maturity DateWhen the life of note is expressed in terms of months, one Can find the date when it matures by counting the monthsfrom the date of issue. For example, the maturity date of athree-month note dated May 1 is August 1. A note drawn on the last day of a month matures on the last day of a Subsequent month. This is, a July 31 note due in two monthsmatures on September 30.When the due date is stated in terms of days, one need to Count the exact number of days to determine the maturity date. In counting, omit the date the note is issued but Include the due date. For example, the maturity date of a -

18

60-day note dated July 17 is September15, computed asfollows.Term of note 60 daysJuly(31-17) 14 August 31 45 ---- ----- Maturity date: September 15

19

Accounting for InventoryThe raw materials, work-in-process goods and completely

finished goods that are considered to be the portion of a business's assets that are ready or will be ready for sale. Inventory represents one of the most important assets that most businesses possess, because the turnover of inventory represents one of the primary sources of revenue generation and subsequent earnings for the company's shareholders/owners.

20

Possessing a high amount of inventory for long periods of time is not usually good for a business because of inventory storage, obsolescence and spoilage costs. However, possessing too little inventory isn't good either, because the business runs the risk of share losing out on potential sales and potential market as well.

21

Purpose of InventoryThe purpose of an inventory system is to keep track

of what you have in your small store, large office or product development factory. If you know what you have available for sale or to build products, you can easily satisfy the needs of your customers when they contact you to buy your products. The inventory system informs you when you need to purchase more products or supplies.

22

Inventory SystemInventory systems are tracking systems that inform you of

the amount of raw materials, supplies or final products you have readily available. The inventory system is updated each time you sell an item or use raw materials to create a product, so you know what you have available for the following day or week. This type of system also allows you to order products in advance, so you have everything you need at all times.

There are basically two inventory systems followed by business concerns.1. Periodic Inventory System2. Perpetual Inventory System

23

Periodic Inventory SystemIt is a system of inventory in which updates are made on a

periodic basis. In a periodic inventory system no effort is made to keep

up-to-date records of either the inventory or the cost of goods sold. Instead, these amounts are determined only periodically - usually at the end of each year. This physical count determines the amount of inventory appearing in the balance sheet. The cost of goods sold for the entire year then is determined by a short computation.

24

Perpetual Inventory System System of inventory control in which the number of units of

any inventory item (and the total value of inventory) on any day can be obtained from the stock records. In this method (1) all additions (purchases) and withdrawals (sales or consumption) are recorded in inventory cards as they occur to provide a running balance of quantity and cost of items, (2) a certain number of items are counted every day (or week or month) so that, by the year end, every item has been actually (physically) counted at least once. If there is any mismatch (due to human error, leakage, pilferage, loss) between the physical quantity and the quantity shown in inventory cards, the records are adjusted accordingly. It is also called the continuous inventory method.

25

Classifying InventoryClassification of inventory depends on whether the firm is amerchandiser or a manufacturer. On this basis inventorycan be classify as – 1. Merchandising Company Inventory 2.Manufacturing Company Inventory Merchandising Company Inventory Merchandising Company merchandisers need only one Inventory classification i.e. merchandising inventory. (Different items make up the total inventory)

26

Manufacturing Company InventoryManufacturers usually classify inventory into three

categories- 1.Finished goods inventory 2.Work in progress 3. Raw materials. Determining Inventory QuantitiesNo matter whether they are using periodic or perpetual inventory system, all companies need to determine invent- ory quantities at the end of the accounting period. If using a perpetual system, companies take a physical inventoryfor the following reasons:

27

1. To check the accuracy of their perpetual inventory records.

2. To determine the amount of inventory lost due to wasted raw materials, shoplifting, or employee theft.

Companies using a periodic inventory system take a physical inventory for two different

purposes: to determine the inventory on hand at the balance sheet date, and to determine the cost of

goods sold for the period.Ques. Why do the companies determine the inventory?Ans. The companies determine the inventory due to the following reasons:

28

1. To check the accuracy of their perpetual inventory records.

2. To determine the amount of inventory lost due to wasted raw materials, shoplifting, or employee theft.

Inventory CostingInventory is accounted for at cost. Cost includes all Expenditures necessary to acquire goods and place them in a condition ready for sale. After a company hasdetermined the quantity of units of inventory, it appliesunit costs to the quantities to compute the total cost ofthe inventory and the cost of the goods sold. There arethree methods for the inventory costing.

29

1. First in, first – out (FIFO)2. Last in, first- out (LIFO)3. Average- cost First in, first – out (FIFO) The first in, first – out (FIFO) method assumes that the earlier goods purchased are first to be sold. FIFO oftenparallels the actual physical flow of merchandise. That is,it generally is good business practice to sell the oldest unitfirst. Under the FIFO method, therefore , the costs of theearliest goods purchased are the first to be recognised indetermining cost of goods sold.

30

Ques. Explain FIFO.Ans. The first in, first – out (FIFO) method assumes that the earlier goods purchased are first to be sold. FIFO oftenparallels the actual physical flow of merchandise. That is,it generally is good business practice to sell the oldest unitfirst. Under the FIFO method, therefore , the costs of theearliest goods purchased are the first to be recognised indetermining cost of goods sold.

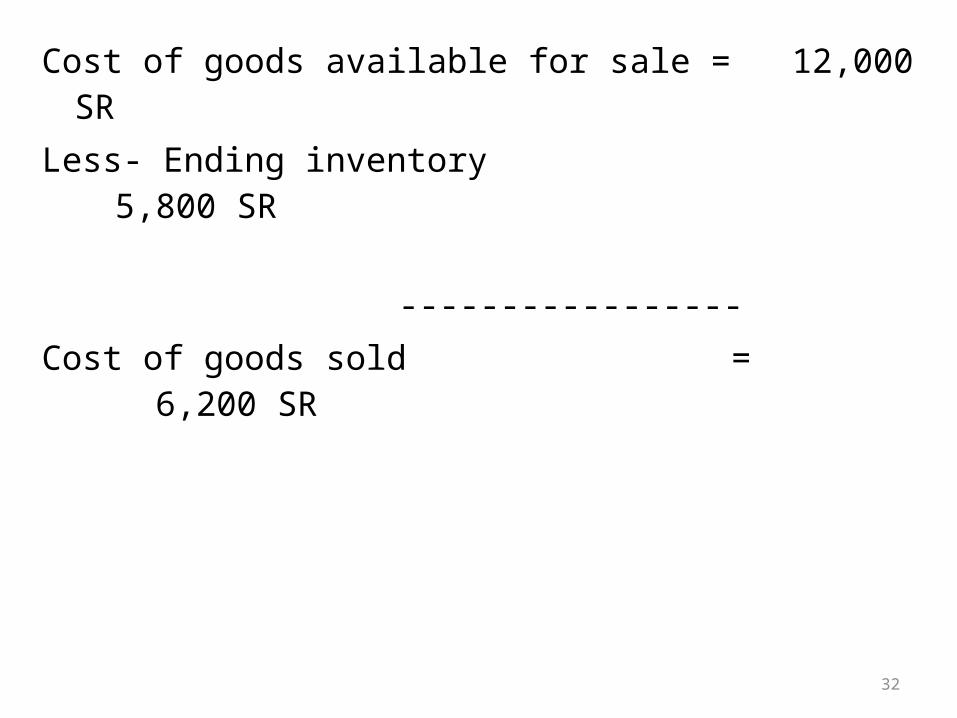

Illustration given below shows the allocation of costof goods available for sale at Houston Electronics under FIFO

Cost of goods available for sale = 12,000 SRLess- Ending inventory 5,800 SR -----------------Cost of goods sold = 6,200 SR

33

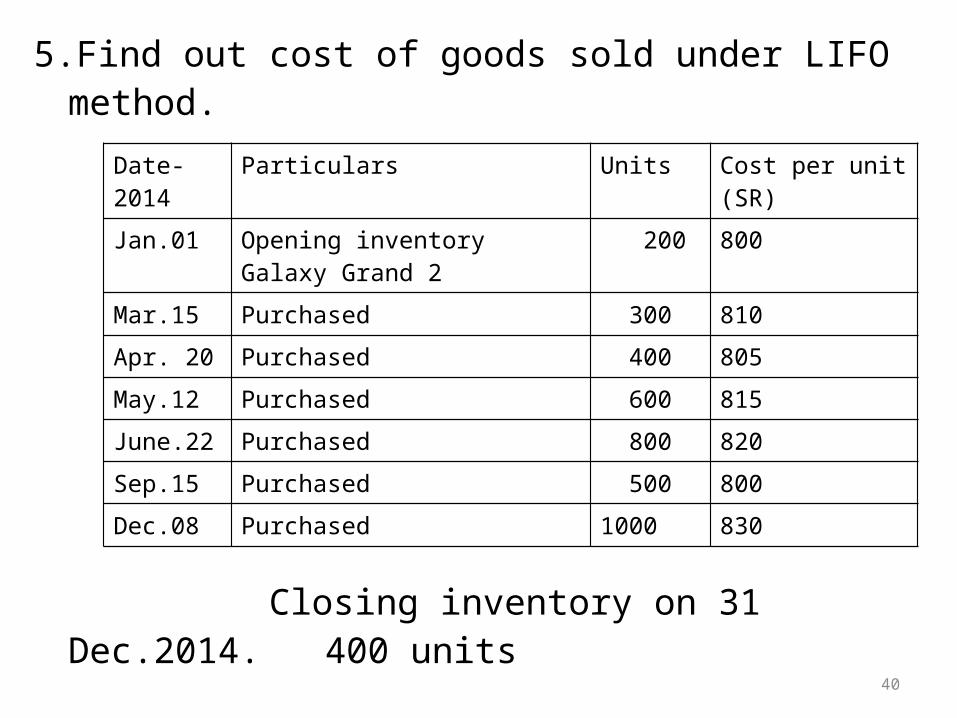

Last-In, First-Out (LIFO) MethodLast-In, First-Out is one of the common techniques used in the valuation of inventory on hand at the end of a period and the cost of goods sold during the period. LIFO assumes that goods which made their way to inventory (after purchase, manufacture etc.) later are sold first and those which are manufactured or acquired early are sold last. Thus LIFO assigns the cost of newer inventory to cost of goods sold and cost of older inventory to ending inventory account. This method is exactly opposite to first-in, first-out method.

34

Ques. Explain LIFO.Ans. Last-In, First-Out is one of the common techniques used in the valuation of inventory on hand at the end of a period and the cost of goods sold during the period. LIFO assumes that goods which made their way to inventory (after purchase, manufacture etc.) later are sold first and those which are manufactured or acquired early are sold last.

35

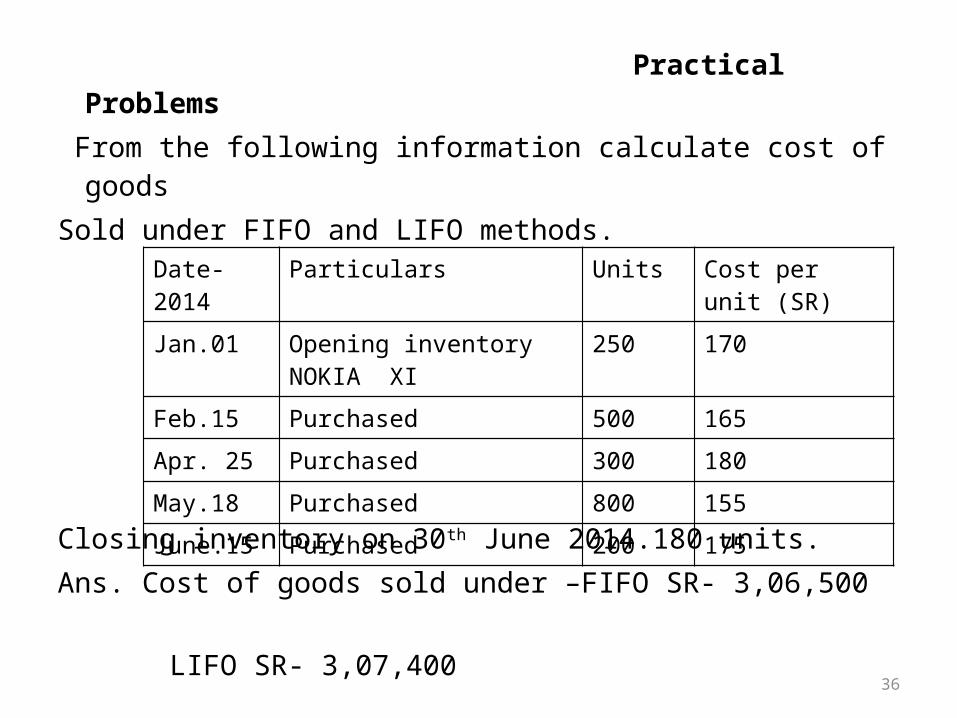

Illustration given below shows the allocation of costof goods available for sale at Houston Electronics under LIFO