1. Accountancy- preparation of balance sheets 2. Assessment of economic viability, 3. Inventory control, 4. Decision making, 5. Expected costs, 6. Planning and production control, 7. Quality control, 8. Marketing, advertisement 9. Industrial relations, wages and incentive, 10. Sales and purchases, 11. Preparation of financial reports, accounts and stores studies. UNIT -III

Transcript

1. Accountancy- preparation of balance sheets 2. Assessment of economic viability, 3. Inventory control, 4. Decision making, 5. Expected costs, 6. Planning and production control, 7. Quality control, 8. Marketing, advertisement 9. Industrial relations, wages and incentive, 10. Sales and purchases, 11. Preparation of financial reports, accounts and stores

studies.

UNIT -III

• UNIT -IV 1. Project planning and control: 2. The financial functions, 3. Cost of capital approach in project planning and

control. 4. Economic evaluation, 5. Risk analysis, 6. Capital expenditures, 7. Policies and practices in public enterprises. 8. Profit planning and programming, 9. Planning cash flow, 10. Capital expenditure and operations. 11. Control of financial flows, control and

communication.

RISK Analysis

– Definition of business risk

– Causes

– Techniques of risk analysis

– Classification/Types

– Business risk

– Production risk

– Financial risk

– Social risk

– Market risk

– risk of the loss of firm’s assets

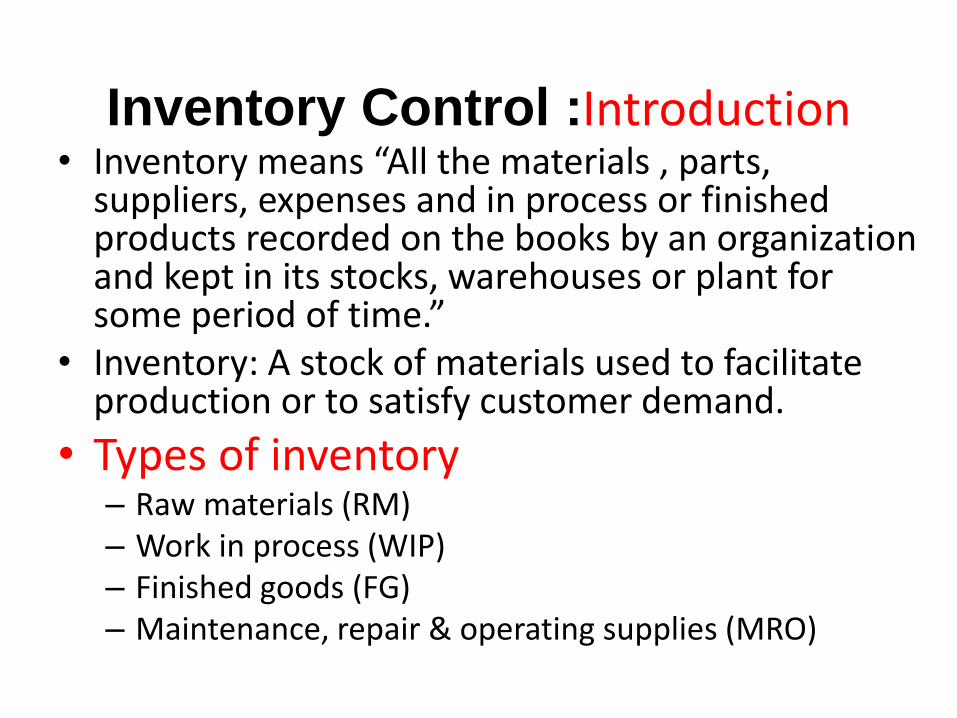

Inventory Control :Introduction • Inventory means “All the materials , parts,

suppliers, expenses and in process or finished products recorded on the books by an organization and kept in its stocks, warehouses or plant for some period of time.”

• Inventory: A stock of materials used to facilitate production or to satisfy customer demand.

• Types of inventory – Raw materials (RM) – Work in process (WIP) – Finished goods (FG) – Maintenance, repair & operating supplies (MRO)

4/17/2015 XIDAS, INVENTORY CONTROL 5

Definition of inventory control

Inventory control is the technique of maintaining the size of the inventory at some desired level keeping in view the best economic interest of an organization.

A Material-Flow Process

Work in

process

Work in

process

Work in

process

Finished

goods

Raw

Materials Vendors Customer

Productive Process

Purpose/need for inventory • Transaction motive

– Reasons for Transaction motive • Economies of scale • Specialization • Permits purchase and transportation economies

• Precautionary motive – Reasons for Precautionary motive

• Inventory as a buffer • Hedge against price changes • Protects against fluctuations in demand and lead time uncertainties

• Speculative Motive (to earn extra profit) • To improve customer’s goodwill and improve customer

service • Better use of men, machines and material; • Protection against fluctuations in output; • Control of stock volume; • Control of stock distribution.

Classification of inventory

• On the basis of nature of material

– Direct material Inventories

– Indirect material Inventories

• On the basis of uses of material

Direct material Inventories

• Production Inventories (raw material , Parts and Components)

• In-process Inventories

• Finished goods Inventories

• Indirect material Inventories

• MRO (Maintenance, Repair and Operating)Inventories

• Consumable Inventories

On the basis of uses of material • Transaction Inventory

• Precautionary Inventory

• Speculative Inventory

• Anticipation Inventory

• Cycle Inventory

Various levels of Inventory

1.Minimum inventory Level:

2.Maximum inventory Level

3. Re-order or Ordering inventory Level

4. Average inventory Level

5. Danger inventory Level

Optimum level of inventory • Rate of inventory turnover

• Type of product • Market structure • Economies of production • Costs • Financial position of the firm • Inventory policy and Attitude of

management

Process of Inventory Control

• State-I: process of purchasing material or ordering

• State-II: Inventory storing procedure

• State-III: Process of issue of material

Techniques of Inventory control • A-B-C

• H-M-L (High-Med-Low)

• X-Y-Z

• V-E-D (vital/essensial/desirable)

• F-S-N (fast/slow/non-moving)

• S-D-E (scarce/ diffcult /easy)

• G-O-L-F (govt/open/local/foreign)

• S-0-S (seasonal/ off seasonal)

Selective Inventory Control System

Title Basis Main Use

A-B-C Value of Consumption To control- raw material/ w.i.p/

components

H-M-L (High-Med-

Low)

Unit price of the material Mainly to control purchase

X-Y-Z Value of items in storage To review the inventories & their

uses at scheduled intervals

V-E-D (vital/essen/

desirable

Criticality of the component To determine stock levels of spare

parts

F-S-N

(fast/slow/non-

moving)

Consumption pattern of the

component

To control obsolescence

S-D-E

(scarce/diff/easy)

Problems faced in

procurement

Lead-time analysis & purchasing

strategy

G-O-L-F

(govt/open/local/for

eign)

Source of materials Procurement strategies

S-0-S (seasonal/ off

seasonal)

Nature of supplies Procurement stocking strategies

for seasonal items like agricultural

EOQ Model (basic) Economic Order Quantity

EOQ Assumptions

• Known & constant demand

• Known & constant lead time

• Instantaneous receipt of material

• No quantity discounts

• Only order (setup) cost & holding cost

• No stockouts

EOQ Model

Order Quantity

Annual Cost

Order Quantity

Annual Cost

Holding Cost

EOQ Model

Order Quantity

Annual Cost

Holding Cost

Order (Setup) Cost

EOQ Model

Order Quantity

Annual Cost

Holding Cost

Total Cost Curve

Order (Setup) Cost

EOQ Model

Order Quantity

Annual Cost

Holding Cost

Total Cost Curve

Order (Setup) Cost

Optimal Order Quantity (Q*)

EOQ Model

H

SDEOQ

2

D = Annual demand (units) S = Cost of placing order (Rs.) C = price per unit (Rs.) I = Holding cost (Rs.) of each unit H = Total Holding cost (Rs.) = I x C

Economic Order Quantity

Optimal Order Quantity

Expected Number Orders

Expected Time Between OrdersWorking Days / Year

Working Days / Year

QD S

H

ND

Q

TN

dD

ROP d L

*

*

2

D = Demand per year

S = Setup (order) cost per order

H = Holding (carrying) cost

d = Demand per day

L = Lead time in days

EOQ Example

You’re a buyer for SaveMart.

SaveMart needs 1000 coffee makers per year. The cost of each coffee maker is Rs.78. Ordering cost is Rs.100 per order. Carrying cost is 40% of per unit cost. Lead time is 5 days. SaveMart is open 365 days/yr.

What is the optimal order quantity & ROP?

SaveMart EOQ

H

SDEOQ

2

20.31$

100$10002EOQ

D = 1000 S = Rs.100 C = Rs. 78 I = 40% H = C x I H = Rs.31.20

EOQ = 80 coffeemakers

SaveMart ROP

ROP = demand over lead time = daily demand x lead time (days) = d x l D = annual demand = 1000 Days / year = 365 Daily demand = 1000 / 365 = 2.74 Lead time = 5 days

ROP = 2.74 x 5 = 13.7 => 14

Avg. CS = OQ / 2 = 80 / 2 = 40 coffeemakers = 40 x Rs.78 = Rs.3,120 Inv. CC = Rs.3,120 x 40% = Rs.1,248 Note: unrelated to reorder point

SaveMart Average (Cycle Stock) Inventory

Marketing Concepts

Marketing concepts are the philosophies, beliefs or attitudes adopted by companies or marketers in relation to market their product. Some say they are consumer oriented, some say they value their customers and some say customers are their kings. Various types of marketing concepts: A. Traditional Concepts B. Modern Concepts 1. Exchange concept 1. Marketing concept 2. Production concept 2. Societal concept 3. Product concept 3.Holistic marketing concept 4. Selling concept

Types of Marketing Concepts

Traditional Concepts • Exchange Concept: The Exchange concept holds that the

exchange of a product between the seller and the buyer is the central idea of marketing.

• Production Concept: The production concept holds that the consumer prefer the goods which are easily available at lower prices. Therefore, it is necessary to produce in large quantities at lower costs.

• Product Concept: It is a belief of the management that consumers favour the products of superior quality, better performance and innovative features. Therefore, successful marketing requires continuous product planning and development and improvement in quality standards.

• Selling Concept: This concept assumes that consumers will

not buy goods voluntarily unless the seller undertakes a large

scale selling and promotional efforts.

Modern Concepts • Marketing Concept: This is the modern concept of marketing

or marketing philosophy. This concept holds that the primary

task of a business firm is to study the needs, desires and the

preferences of the potential consumers and produce goods

which are actually needed by the consumers. When an

organisation practices the marketing concept, all it’s activities

are directed to satisfy the consumer.

• Social Concepts: According to this concept, the task of

management is to identify and satisfy consumer wants, in

conformity with social interests. Firms should not only

consider consumer wants and profits but also society interests

while making their marketing decision.

• Holistic Marketing Concept: Holistic marketing concept is a

new marketing concept. Holistic marketing recognizes that

“everything matters” with marketing- and that a broad,

integrated perspective is often necessary. There are four

components of holistic marketing concept. They are…

• Relationship marketing

• Integrated marketing

• Internal marketing

• Social responsibility marketing

Factory Existing products

Selling and promotion

Profits through sales volume

Target market

Integrated marketing

Profits through customer

satisfaction

Customer needs

Starting point

Focus Means Ends

(b) The marketing concept

(a) The selling concept

Features of Modern Marketing Concepts

• Modern marketing is consumer oriented.

• It begins and ends with Consumers.

• It precedes & succeeds production.

• It is competition oriented.

• Its strategy is target marketing

• The distribution policy under modern marketing is direct marketing and direct selling.

• Modern marketing relies on information.

• It emphasizes mutuality of benefit.

• Business networks.

• Emphasis on retaining customers

• Marketing on the net.

• Shifting from international to borderless world marketing.

• Innovation.

• Business Process Outsourcing.

• Branding shifting values.

Operational Model for Implementing the Philosophy of the

Marketing Concept is the:

• Marketing Mix - A mixture of several ideas and plans followed by a marketing representative to promote a particular product or brand is called marketing mix.

• Several concepts and ideas combined together to formulate final strategies helpful in making a brand popular amongst the masses form marketing mix.

The Marketing Mix Consists of Four Basic Strategic Variables

The role of marketing management is to mix or blend these four strategic

variables in such a way as to meet the needs of THE TARGET MARKET

Product Price Promotion Place

Target Market

Product

• Goods manufactured by organizations for the end-users are called products.

• Products can be of two types - Tangible Product and Intangible Product (Services)

• An individual can see, touch and feel tangible products as compared to intangible products.

• A product in a market place is something which a seller sells to the buyers in exchange of money.

Price

• The money which a buyer pays for a product is called as price of the product. The price of a product is indirectly proportional to its availability in the market. Lesser its availability, more would be its price and vice a versa.

• Retail stores which stock unique products (not available at any other store) quote a higher price from the buyers.

Place

Place refers to the location where the products are available and can be sold or purchased. Buyers can purchase products either from physical markets or from virtual markets. In a physical market, buyers and sellers can physically meet and interact with each other whereas in a virtual market buyers and sellers meet through internet.

Promotion

Promotion refers to the various strategies and ideas implemented by the marketers to make the end - users aware of their brand. Like:

• Advertising. • Word of mouth Lately three more P’s have been added to the marketing mix. They are

as follows: • Packaging- Attractive, transport, sale & exchange. • People- to whom and through whom goods are being sold. • Public relations- increase awareness through public relations (Customers,

Govt., employees, retailers, wholesalers, press, ) • Politics- (should go in accordance with rules & regulations made by law

makers.)

Marketing Mix

Target Market

Product Product Variety Quality Design Features Brand name Packaging Size Services Warranties Returns

Price List price Discounts Allowances Payment period Credit terms

Promotion Sales promotion Advertising Sales force Public relations Direct marketing

Place Channels Coverage Assortments Locations Inventory Transport

4C’s

Customer

Solution

Cost

(to customer) Convenience Communication

Utility/Importance of Marketing Mix

• Helps in understanding important tasks of marketing.

• Important tool of marketing programme.

• It promotes better utilisation of limited resources.

• Facilitates the meeting of different requirements of customers.

• It provides customer satisfaction.

• It helps in goal achievement.

• It facilitates communication.

• It helps in establishing relations with customers.

• It helps in developing new products.

MARKETING MANAGEMENT

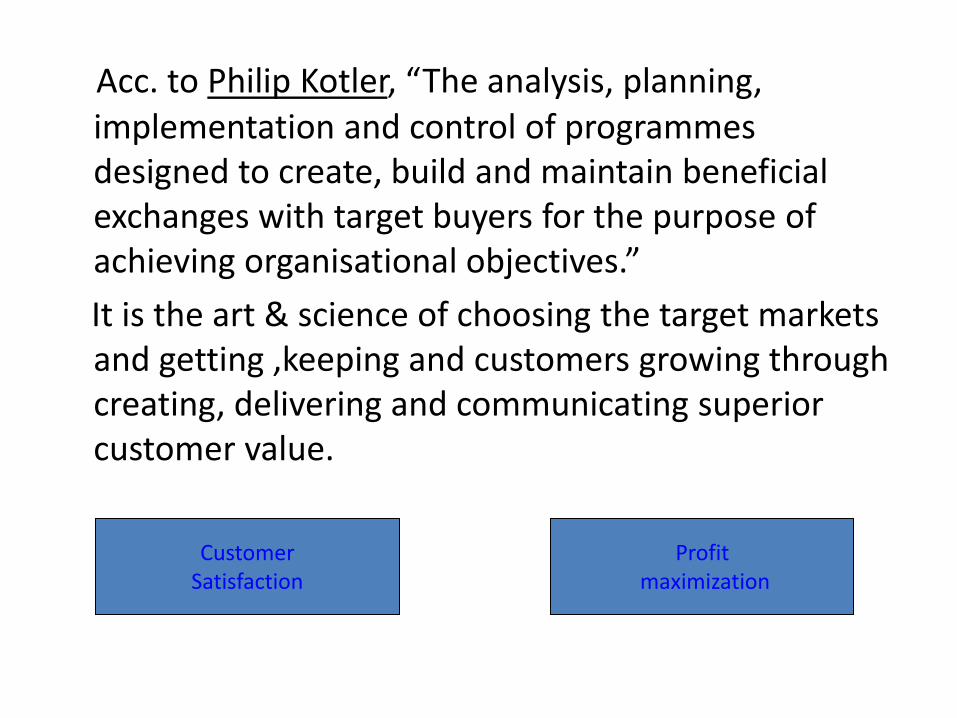

Acc. to Philip Kotler, “The analysis, planning, implementation and control of programmes designed to create, build and maintain beneficial exchanges with target buyers for the purpose of achieving organisational objectives.”

It is the art & science of choosing the target markets and getting ,keeping and customers growing through creating, delivering and communicating superior customer value.

Customer Satisfaction

Profit maximization

COST &

COST ELEMENTS

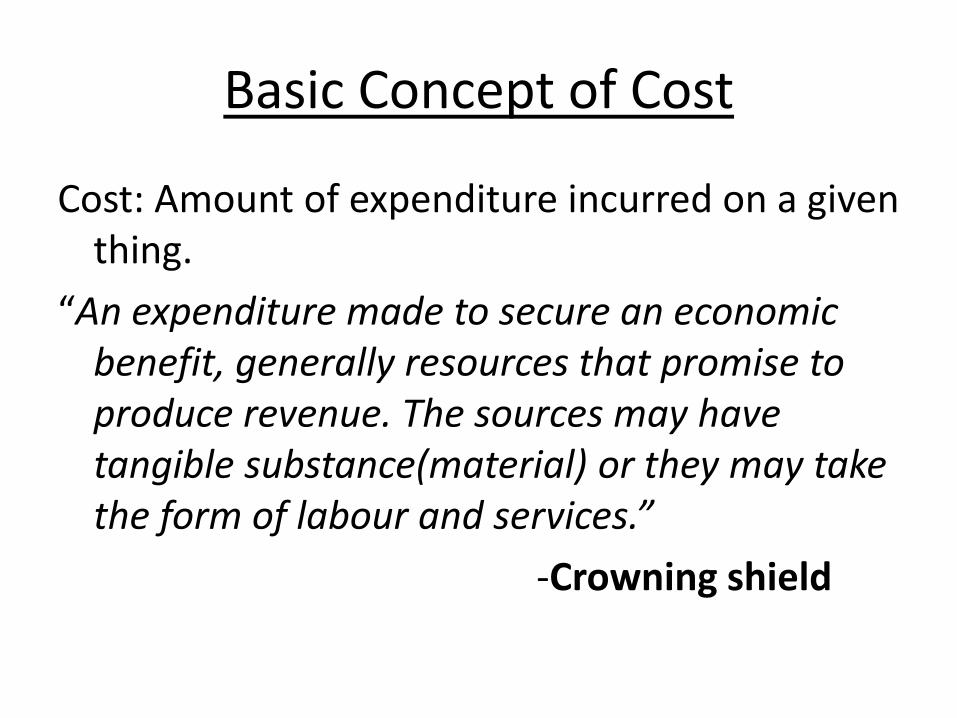

Basic Concept of Cost

Cost: Amount of expenditure incurred on a given thing.

“An expenditure made to secure an economic benefit, generally resources that promise to produce revenue. The sources may have tangible substance(material) or they may take the form of labour and services.”

-Crowning shield

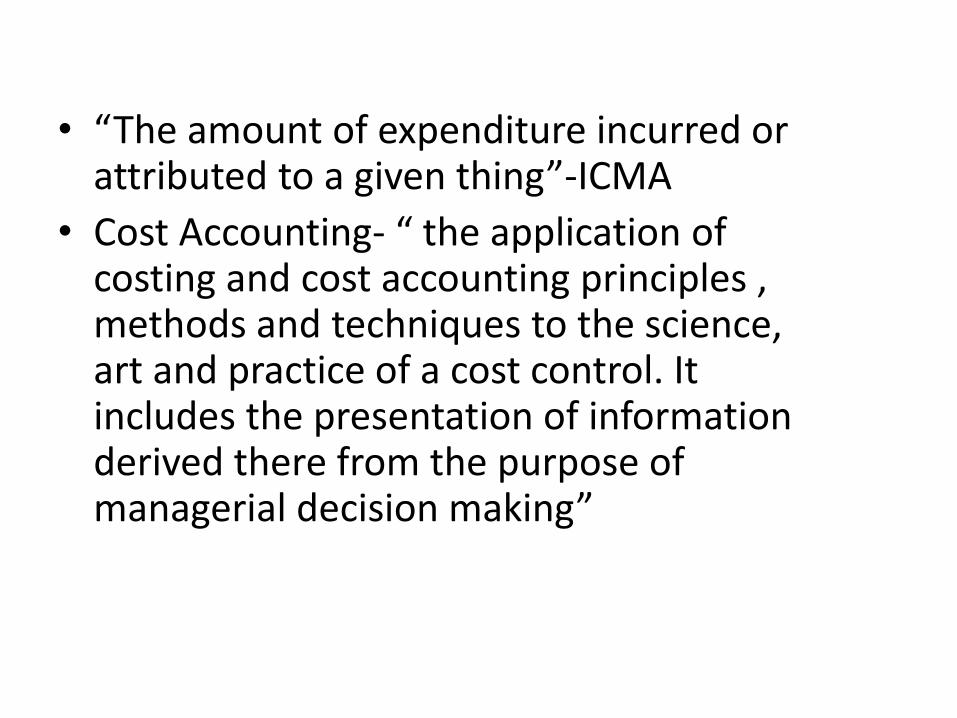

• “The amount of expenditure incurred or attributed to a given thing”-ICMA

• Cost Accounting- “ the application of costing and cost accounting principles , methods and techniques to the science, art and practice of a cost control. It includes the presentation of information derived there from the purpose of managerial decision making”

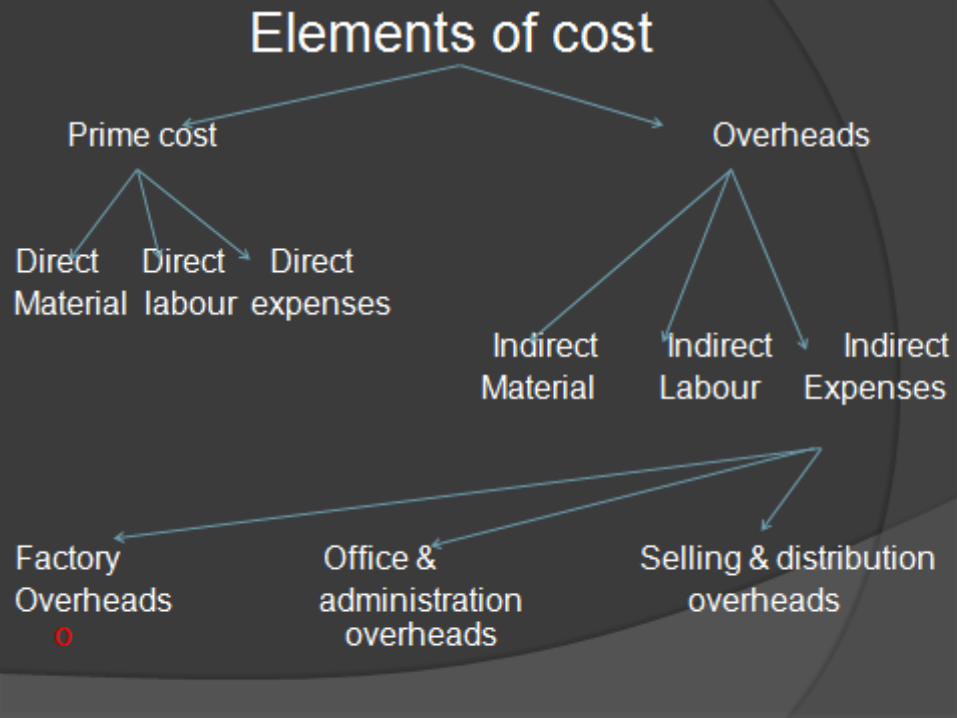

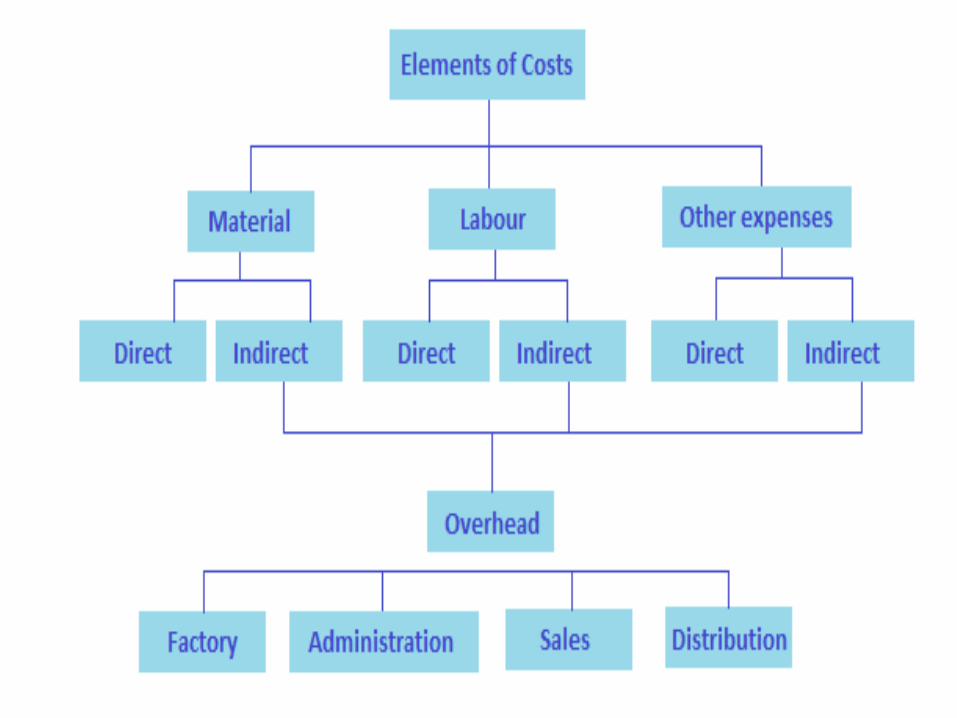

Elements of cost

1.Material

2.Labour

3.Expenses

1(a)Direct material:

• All type of raw material issued

• Raw material purchased

• Transferred from one cost centre to another cost centre

• Primary packing material

1(b) Indirect material cost:

• Stores used in maintenance of machinery ,building etc

• Opportunity cost-Value of benefit sacrificed in favor of an alternative course of action

Cost of capital

• The cost of capital is a term used in the field of financial investment to refer to the cost of a company's funds (both debt and equity), or, from an investor's point of view "the shareholder's required return on a portfolio company's existing securities"

• ]It is used to evaluate new projects of a company.

• It is the minimum return that investors expect for providing capital to the company, thus setting a benchmark that a new project has to meet.

DEFINITION

“ Cost of capital is the minimum required rate of earning or the cut off rate for capital expenditure.”

Soloman Ezra

Importance of the concept of cost of capital

(i) Designing the optimal Capital structure

(ii) Assisting in investment decisions

(iii) Helpful in evaluation of expansion projects

(iv) Rational allocation of national resources

Capital expenditures

• Capital expenditures (CAPEX or capex) are expenditures altering the future of the business. A capital expenditure is incurred when a business spends money either to buy fixed assets or to add to the value of an existing fixed asset with a useful life extending beyond the taxable year.

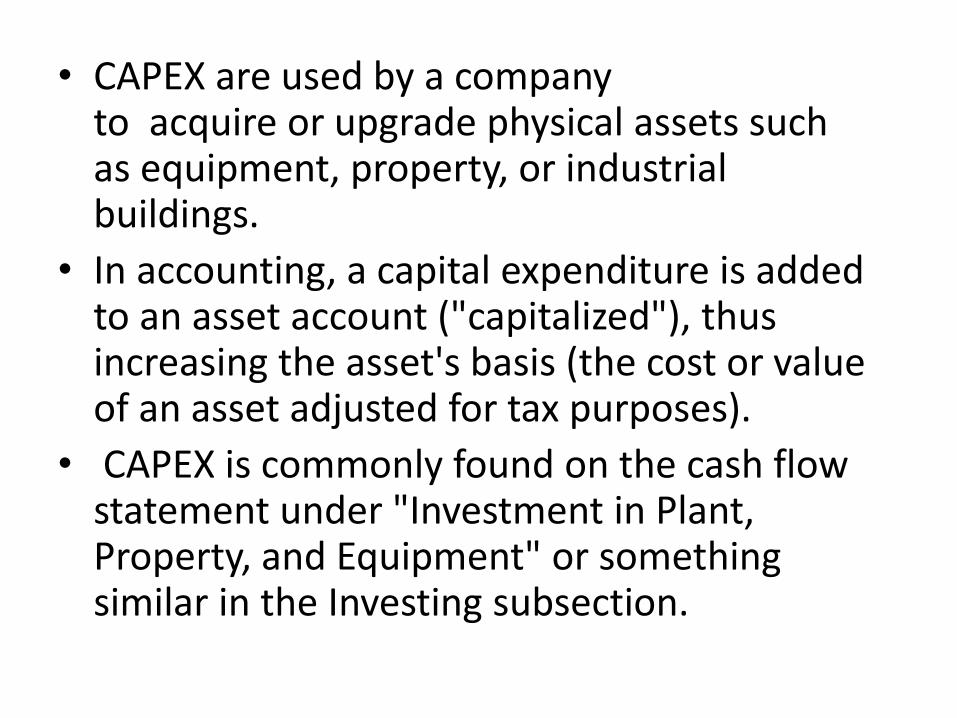

• CAPEX are used by a company to acquire or upgrade physical assets such as equipment, property, or industrial buildings.

• In accounting, a capital expenditure is added to an asset account ("capitalized"), thus increasing the asset's basis (the cost or value of an asset adjusted for tax purposes).

• CAPEX is commonly found on the cash flow statement under "Investment in Plant, Property, and Equipment" or something similar in the Investing subsection.

68

Budgeting

* INTRODUCTION

* TYPES * METHODS

Capital Budgeting

69

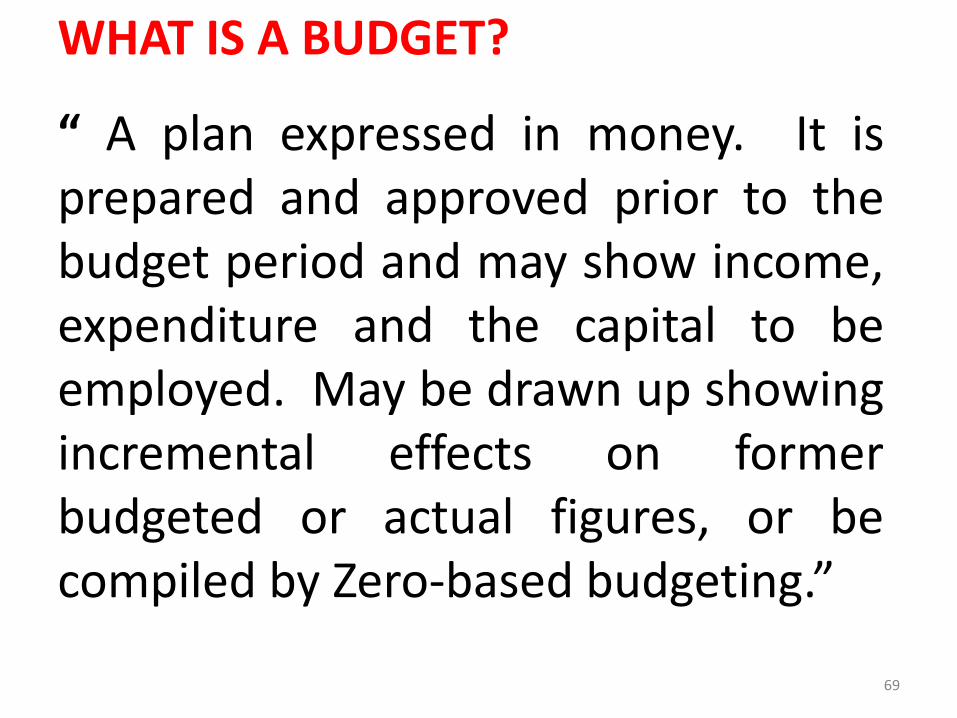

WHAT IS A BUDGET?

“ A plan expressed in money. It is prepared and approved prior to the budget period and may show income, expenditure and the capital to be employed. May be drawn up showing incremental effects on former budgeted or actual figures, or be compiled by Zero-based budgeting.”

70

CLASSIFICATION OF BUDGETS

ACCORDING TO ACCORDING TO ACCORDING TO TIME FUNCTION FLEXIBILITY

1. Long term budget 1. Sales budget 1. Fixed budget 2. Short term budget 2. Production budget 2. Flexible budget 3. Current budget 3. Cost of Production budget 4. Rolling budget 4. Purchase budget 5. Personnel budget 6. R & D budget 7. Capital Expenditure budget 8. Cash budget 9. Master budget

71

1. SALES BUDGET:

Sales budget is the most important budget based on which all the other budgets are built up. This budget is a forecast of quantities

and values of sales to be achieved in a budget period.

2. PRODUCTION BUDGET:

Production budget involves planning the level of production which in turn involves the answer to the following questions:

a. What is to be produced?

b. When is it to be produced?

c. How is it to be produced?

d. Where is it to be produced?

72

3. COST OF PRODUCTION BUDGET:

This budget is an estimate of cost of output planned for a budget period and may be classified into –

• Material Cost Budget

• Labour Cost Budget

• Overhead Cost Budget

4. PURCHASE BUDGET:

This budget provides information about the materials to be acquired from the market during the budget period.

73

5. PERSONNEL BUDGET:

This budget gives an estimate of the requirements of direct labour essential to meet the production target.

This budget may be classified into –

a. Labour requirement budget

b. Labour recruitment budget

6. RESEARCH AND DEVELOPMENT BUDGET:

This budget provides an estimate of expenditure to be incurred on R & D during the budget period.

A R&D budget is prepared taking into consideration the research projects in hand and new R & D projects to be taken up.

74

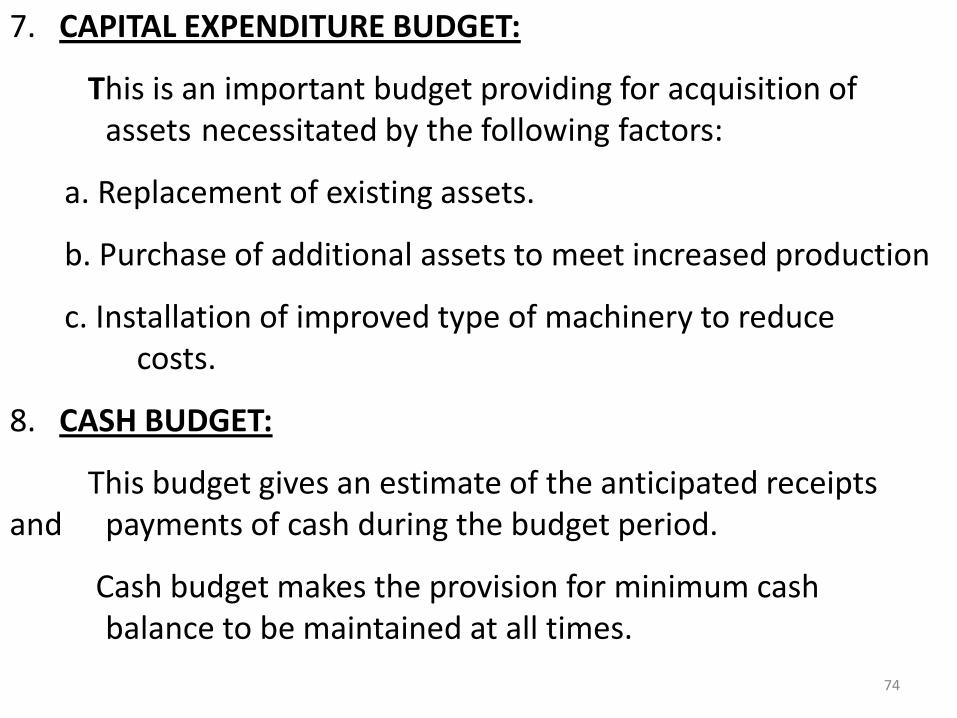

7. CAPITAL EXPENDITURE BUDGET:

This is an important budget providing for acquisition of assets necessitated by the following factors:

a. Replacement of existing assets.

b. Purchase of additional assets to meet increased production

c. Installation of improved type of machinery to reduce costs.

8. CASH BUDGET:

This budget gives an estimate of the anticipated receipts and payments of cash during the budget period.

Cash budget makes the provision for minimum cash balance to be maintained at all times.

75

9. MASTER BUDGET:

CIMA defines this budget as “ The summary budget incorporating its component functional budget and which is finally approved, adopted and employed”.

Thus master budget is a summary of all functional budgets in capsule form available in one report.

10. FIXED BUDGET:

This is defined as a budget which is designed to remain unchanged irrespective of the volume of output or turnover attained.

This budget will, therefore, be useful only when the actual level of activity corresponds to the budgeted level of activity.

76

11. FLEXIBLE BUDGET:

CIMA defines this budget as one “ which, by recognising the difference in behaviour between fixed and variable costs in relation to fluctuations in output, turnover or other variable factors such as number of employees, is designed to change appropriately with such fluctuations”.

12. PERFORMANCE BUDGETING:

These days budgets are established in such a way so that each item of expenditure is related to specific responsibility centre and is closely linked with the performance of that standard.

77

78

CAPITAL BUDGETING

Capital budgeting is a decision situation where large funds are committed (invested) in the initial stages of the project and the returns are expected over a long period of time. These decisions are related to allocation of investible funds to different long-term assets.

Capital budgeting is a continuous process and it is carried out by different functional areas of management such as production, marketing, engineering, financial management etc.

79

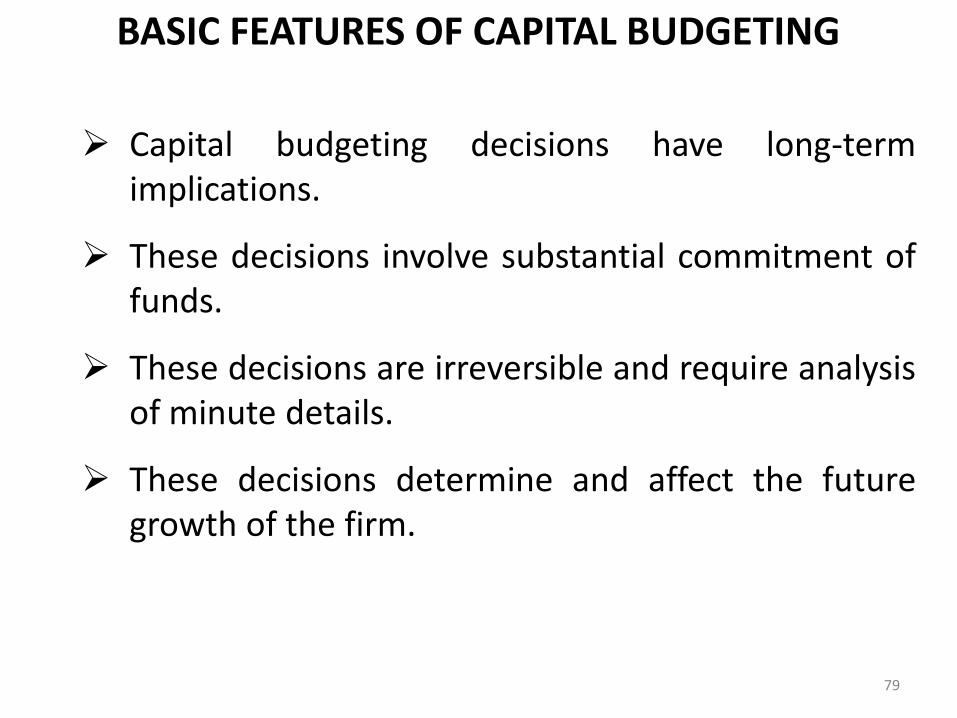

BASIC FEATURES OF CAPITAL BUDGETING

Capital budgeting decisions have long-term implications.

These decisions involve substantial commitment of funds.

These decisions are irreversible and require analysis of minute details.

These decisions determine and affect the future growth of the firm.

80

CAPITAL BUDGETING

DECISION INVOLVES

THREE STEPS

1. Estimation of costs and benefits of a proposal or of each alternative.

2. Estimation of the required rate of return, i.e., the cost of capital

3. Selection and applying the decision criterion.

81

1. ESTIMATION OF CASH FLOWS

The costs and benefits for a capital budgeting decision situation are measured in terms of cash flows.

An important point is that all cash flows are considered on after tax basis. The rule is that all financial decisions are subservient to tax laws.

The cash flow from the project are compared with the cost of acquiring the project.

82

2. DECISION CRITERIA

TECHNIQUES OF EVALUATION

Traditional or Time-adjusted or

Non-discounting Discounted cash flows

1. Payback period 1. Net Present Value

2. Accounting Rate of 2. Profitability Index

Return 3. Internal Rate of Return

Factors Influencing Capital Budgeting

• Availability of funds • Structure of capital • Taxation Policy • Government Policy • Lending Policies of Financial Institutions • Immediate need of the Project • Earnings • Capital Return • Economic Value of the Project • Working Capital • Accounting Practice • Trend of Earning • Risk of the business • Forecast of the market • Political unrest • Geographical Condition • Exchange Rate of Currency

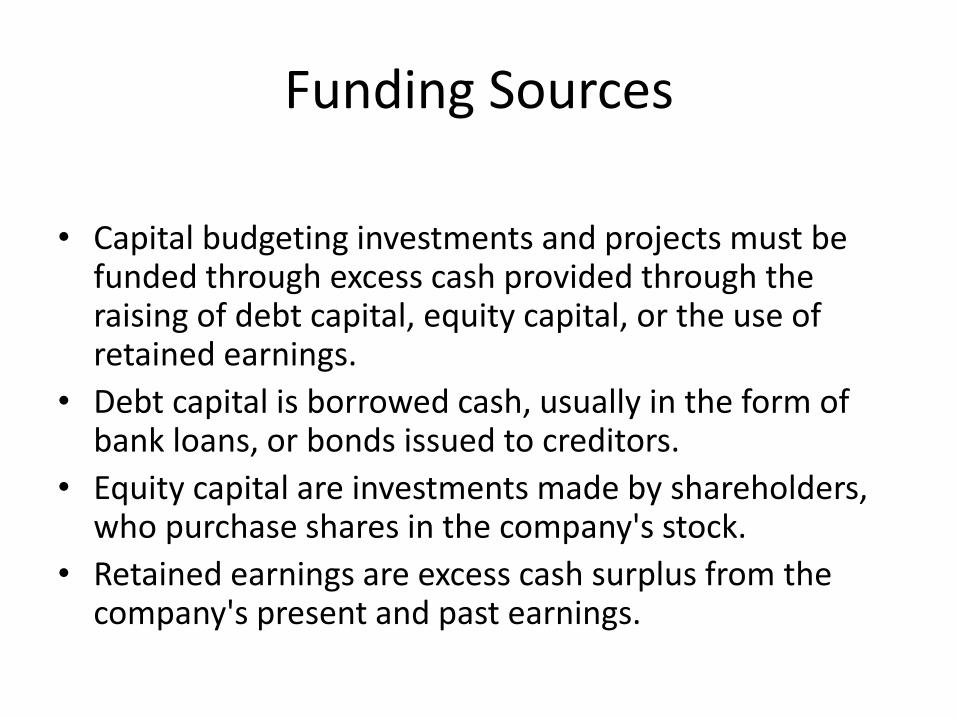

Funding Sources

• Capital budgeting investments and projects must be funded through excess cash provided through the raising of debt capital, equity capital, or the use of retained earnings.

• Debt capital is borrowed cash, usually in the form of bank loans, or bonds issued to creditors.

• Equity capital are investments made by shareholders, who purchase shares in the company's stock.

• Retained earnings are excess cash surplus from the company's present and past earnings.

Cash flow • Forecasting Cash Flows in a Start-up or Small

Business: • Why Cash flow is important? • Cash flow is a dynamic and unpredictable part

of life for a start-up or small business• • Cash flow problems are the main reason why a

new business fails• • Regular and reliable cash flow forecasting can

address many of the problems • Cash is king – it is the lifeblood of a business• • If a business runs out of cash it will almost

certainly fail• • Few start-ups have unlimited finance – cash is

limited, so it needs to be managed carefully

Main kinds of cash flows • Cash inflows or Cash outflows • sales Payments to suppliers • Receipts from trade debtors • Wages and salaries Setting • Sale of fixed assets the business up assets • Payments for fixed Interest on bank balances • Tax on profits Grants • Day-to-day trading • Interest on loans & overdrafts • Dividends paid to Loans from bank • Growth shareholders • Share capital invested • Repayment of loans

• Advanced warning of cash shortages•

• Make sure that the business can afford to pay suppliers and employees•

• Spot problems with customer payments•

• As an important part of financial control•

• Provide reassurance to investors and lenders that the business is being managed properly