36

United Power Company SAOG Financial statements for the year ended 31 December 2016

United Power Company SAOG

Financial statements for the year ended

31 December 2016

United Power Company SAOG

Financial statements for the year ended31 December 2016

Contents Page

Administration and contact details 1

Independent auditor's report 2-5

Statement of financial position 6

Statement of profit or loss and other comprehensive income 7

Statement of changes in shareholders' equity 8

Statement of cash flows 9

Notes to the financial statements 10 – 34

United Power Company SAOG

Administration and contact details as at 31 December 2016

Commercial registration number 1460366

Board of Directors Mr. Murtadha Ahmed Sultan - Chairman

Mr. Bandar Ahmed Allaf - Vice-Chairman

Mr. Abdullah Mohammed Al Ma'mari - Director

Mr. Grahame Laurence Farquhar - Director

Mr. Ryan Zanin - Director

Mr. Fabrizio Bocciardi - Director

Mr. Yaseen Hassan Ali Abdullatif - Director

Mr. Hamad Lal Baksh Al Baloushi - Director

Mr. Sami Yahya hamad Al-Dughaishi - Director

Mr. Zoher Karachiwala - Director & CEO

Audit Committee Mr. Yaseen Hassan Ali Abdullatif - Chairman

Mr. Grahame Laurence Farquhar - Member

Mr. Ryan Zanin - Member

Executive management Mr. Zoher Karachiwala - Chief Executive Officer

Mr. Guillaume Baudet - Company Secretary

Mr. Sreenath Hebbar - Chief Technical Officer

Mr. Mirdas Al Rawahi - Chief Financial Officer

Mr. Jamal Al Bloushi - Administration Manager

Registered office PO Box 147

Postal Code 134

Jawharat Al Shatti

Sultanate of Oman

Bankers Bank Muscat

Ahli Bank

HSBC Bank Oman

Auditors BDO

Suites 601 & 602

Penthouse, Beach One Bldg.

Way Number 2601, Shatti Al Qurum

PO Box 1176, PC 112, Ruwi

Sultanate of Oman

1

Tel: +968 2495 5100 Suite No. 601 & 602

Fax: +968 2464 9030 Pent House, Beach One Bldg

www.bdo.com.om Way No. 2601, Shatti Al Qurum

PO Box 1176, Ruwi, PC 112

Sultanate of Oman

Independent auditor's report to the shareholders of

United Power Company SAOG

Qualified Opinion

Basis for Qualified Opinion

Accountants and Auditors License No. SMH/13/2015, Financial Advisory License No. SMA/69/2015, Commercial Registration No. 1222681

We have audited the financial statements of United Power Company SAOG ("the Company"), which

comprise the statement of financial position as at 31 December 2016, the statement of profit and loss and

other comprehensive of income, the statement of changes in shareholders' equity and the statement of

cash flows for the year then ended, and notes to the financial statements, including a summary of

significant accounting policies.

In our opinion, except for the effect of the matter described in the Basis for Qualified Opinion section of

our report, the accompanying financial statements present fairly, in all material respects, a true and fair

view of the financial position of the Company as at 31 December 2016, and its financial performance and

its cash flows for the year then ended in accordance with International Financial Reporting Standards

(IFRSs).

The Company has been established to undertake a project primarily to Build, Own, Operate and Transfer

(“BOOT”) a power station in the Sultanate of Oman in the year 1995. IFRIC 12 'Service Concession

Agreements' issued in the year 2006, was applicable from the year 2008 to the Company's financial

statements. According to IFRIC 12, such a project falls within its ambit and requires the Company to

recognise revenue for the construction and operation phases in accordance with IAS 11 and IAS 18,

respectively. Accordingly, the Company should have recognised a financial asset for the fixed charge of

the revenue component and an intangible asset for the variable part. Further, the Company should have

derecognised the property, plant and equipment. However, the Company has reported revenue and

property, plant and equipment in its financial statements in accordance with the Power Purchase

Agreement (PPA) entered into with Oman Power and Water Procurement Co. SAOG (OPWPC) and the then

applicable accounting standards. This constitutes a departure from International Financial Reporting

Standards after introduction of IFRIC 12. Had the Company adopted IFRIC 12, the property, plant and

equipment reflected in the statement of financial position at 31 December 2016 of RO 3.80 million would

have to be fully de-recognised, the retained earnings of the Company would have to be increased by RO

6.98 million, a financial asset recognised amounting to RO 10.78 million and an intangible asset recognised

of RO 0.4 million.

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities

under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial

Statements section of our report. We are independent of the Company in accordance with the ethical

requirements that are relevant to our audit of the financial statements in accordance with the "Code of

Ethics for Professional Accountants ("IESBA Code") issued by International Ethics Standards Board for

Accoountants", and have fulfilled our other responsibilities in accordance with its requirements. We

believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

qualified audit opinion.

BDO Jawad Habib LLC, an Omani registered limited liability company, is a member of BDO International Limited, a UK company limited by guarantee, and

forms part of the international BDO network of Independent member firms.

BDO is the brand name for BDO International network and for each of the BDO Member Firms .

2

Independent auditor's report to the shareholders of

United Power Company SAOG (continued)

Key audit matters

Management override of controls

Other matters

Other information

Our procedures included testing of segregation of duties, testing of controls over the authorisation and

processing of journal entries, other adjustments to the financial statements, testing of significant

transactions that are outside the normal course of business or that otherwise appear to be unusual and

reviewed management judgments in making significant accounting estimates in the current year’s financial

statements.

The financial statements of the Company for the year ended 31 December 2015 were audited by another

auditor, who expressed an unqualified opinion on those financial statements in their opinion dated 23

February 2016. However, they had added an emphasis of matter paragraph over the revenue recognition

for the non-adoption of IFRIC 12 'Service Concession Agreements', and which continues to have relevance

in the audit of financial statements for the year ended 31 December 2016 as mentioned in the Basis for

Qualified Opinion section of our report.

Management is responsible for the other information. The other information comprises the information

included in the annual report but does not include the financial statements and our auditor's report

thereon. Our opinion on the financial statements does not cover the other information and we do not

express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information

and, in doing so, consider whether the other information is materially inconsistent with the financial

statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If,

based on the work we have performed, we conclude that there is a material misstatement of this other

information, we are required to report that fact. We have nothing to report in this regard.

Management in any organisation is in a unique position to perpetrate fraud because of its ability to directly

or indirectly manipulate accounting records and prepare fraudulent financial statements by overriding

controls that otherwise appear to be operating effectively. When considering management’s philosophy

and operating style, we considered the risk of management override of controls and how Those Charged

With Governance consider the potential for management override of controls or other inappropriate

influence over the financial reporting process.

Key audit matters are those matters that, in our professional judgment, were of most significance in our

audit of the financial statements of the current period. These matters were addressed in the context of

our audit of the financial statements as a whole, and in forming our opinion thereon and we do not provide

a separate opinion on these matters. In addition to the matter described in the Basis for Qualified Opinion

section of our report, we have determined the matters described below to be the key audit matters to be

communicated in our report.

3

Independent auditor's report to the shareholders of

United Power Company SAOG (continued)

Auditor’s responsibilities for the audit of the financial statements

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates

and related disclosures made by management.

Conclude on the appropriateness of management’s use of the going concern basis of accounting and based

on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that

may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a

material uncertainty exists, we are required to draw attention in our auditor’s report to the related

disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our

conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However,

future events or conditions may cause the Company to cease to continue as a going concern.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness

of the Company’s internal control.

Responsibilities of management and Those Charged with Governance for the financial statements

The management is responsible for the preparation and fair presentation of these financial statements in

accordance with International Financial Reporting Standards, and for such internal control as management

determines is necessary to enable the preparation of financial statements that are free from material

misstatement, whether due to fraud or error.

In preparing the financial statements, the management is responsible for assessing the Company’s ability

to continue as a going concern, disclosing, as applicable, matters related to going concern and using the

going concern basis of accounting unless management either intends to liquidate the Company or to cease

operations, or have no realistic alternative but to do so.

Those Charged With Governance are responsible for overseeing the Company’s financial reporting process.

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are

free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that

includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an

audit conducted in accordance with ISAs will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are considered material if, individually or in the

aggregate, they could reasonably be expected to influence the economic decisions of users taken on the

basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional

skepticism throughout the audit. We also:

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud

or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is

sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material

misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve

collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

4

Independent auditor's report to the shareholders of

United Power Company SAOG (continued)

Auditor’s responsibilities for the audit of the financial statements (continued)

Report on other legal and regulatory requirements

Muscat Bipin Kapur

Date: Partner

Further, as required by the Commercial Companies Law 1974, as amended, of the Sultanate of Oman and

the Rules and Guidelines on Disclosure issued by the Capital Market Authority, we report that:

(1) we have obtained all the information we considered necessary for the purpose of our audit;

(2) the Company has maintained proper books of account and the financial statements are in agreement

therewith; and

(3) the financial information included in the Directors' report is consistent with the books of account of the

Company.

In addition, we report that, nothing has come to our attention which causes us to believe that the

Company has breached any of the applicable provisions of the Commercial Companies Law 1974, as

amended, of the Sultanate of Oman and the Rules and Guidelines on Disclosure issued by the Capital

Market Authority, which would materially affect its activities, or its financial position as at 31 December

2016.

Evaluate the overall presentation, structure and content of the financial statements, including the

disclosures, and whether the financial statements represent the underlying transactions and events in a

manner that achieves fair presentation.

We communicate with Those Charged With Governance regarding, among other matters, the planned scope

and timing of the audit and significant audit findings, including any significant deficiencies in internal

control that we identify during our audit.

We also provide Those Charged With Governance with a statement that we have complied with relevant

ethical requirements regarding independence, and to communicate with them all relationships and other

matters that may reasonably be thought to bear on our independence, and where applicable, related

safeguards.

From the matters communicated with Those Charged With Governance, we determine those matters that

were of most significance in the audit of the financial statements of the current period and are therefore

the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes

public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter

should not be communicated in our report because the adverse consequences of doing so would reasonably

be expected to outweigh the public interest benefits of such communication.

5

United Power Company SAOG

Statement of financial position as at 31 December 2016

Notes 31 December 31 December

2016 2015

RO'000 RO'000

ASSETS

Non-current assets

Property, plant and equipment 6 3,821 7,663

Total non-current assets 3,821 7,663

Current assets

Inventories 7 259 259

Trade and other receivables 8 1,471 1,986

Cash and bank balances 9 172 80

Total current assets 1,902 2,325

Total assets 5,723 9,988

EQUITY AND LIABILITIES

Capital and reserves

Share capital 10 2,000 2,000

Legal reserve 11 667 667

Retained earnings 1,051 1,164

Total capital and reserves 3,718 3,831

Non-current liabilities

Employees' terminal benefits 15 13

Deferred tax liability 13 147 554

Total non-current liabilities 162 567

Current liabilities

Trade and other payables 14 597 780

Taxation 13 746 810

Short-term borrowings 15 500 4,000

Total current liabilities 1,843 5,590

Total equity and liabilities 5,723 9,988

Net assets per share (OMR) 21 1.859 1.916

Chairman Vice - Chairman

These financial statements, as set out on pages 6 to 34, were approved and authorised for issue by the Board

of Directors on 9 February 2017 and signed on their behalf by:

6

United Power Company SAOG

Year ended Year ended

31 December 31 December

Notes 2016 2015

RO'000 RO'000

Income

Revenue 17 10,033 10,811

Other income 18 - 117

10,033 10,928

Expenses

General and administrative expenses 19 (5,021) (5,161)

Depreciation 6 (3,878) (4,458)

Finance costs 20 (67) (95)

(8,966) (9,714)

Profit before tax for the year 1,067 1,214

Income tax expense 13 (125) (143)

942 1,071

Basic earnings per share 22 0.471 0.286

Statement of profit or loss and other comprehensive income for the year ended

31 December 2016

Net profit after tax for and total

comprehensive income for the year

7

United Power Company SAOG

Statement of changes in shareholders' equity for the year ended 31 December 2016

Notes Share

capital

Legal

reserve

Retained

earnings Total

RO'000 RO'000 RO'000 RO'000

At 31 December 2014 5,000 1,667 1,677 8,344

Reduction in share capital (3,000) - - (3,000)

- - 1,071 1,071

11 - (1,000) 1,000 -

Final dividend for the year 2014 - - (1,584) (1,584)

Interim dividend for the year 2015 - - (1,000) (1,000)

At 31 December 2015 2,000 667 1,164 3,831

- - 942 942

Final dividend for the year 2015 12 - - (1,055) (1,055)

At 31 December 2016 2,000 667 1,051 3,718

Net profit after tax for and total

comprehensive income for the year

Transferred from legal reserve to retained

earnings

Net profit after tax for and total

comprehensive income for the year

8

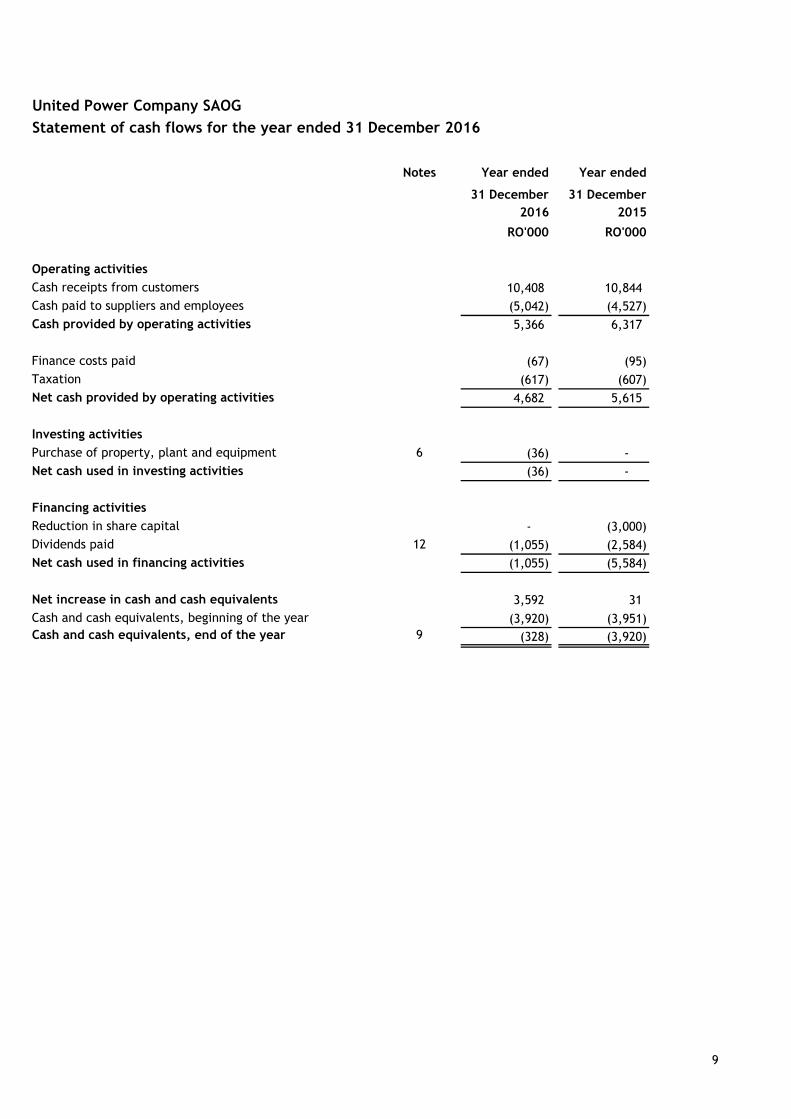

United Power Company SAOG

Statement of cash flows for the year ended 31 December 2016

Notes Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Operating activities

Cash receipts from customers 10,408 10,844

Cash paid to suppliers and employees (5,042) (4,527)

Cash provided by operating activities 5,366 6,317

Finance costs paid (67) (95)

Taxation (617) (607)

Net cash provided by operating activities 4,682 5,615

Investing activities

Purchase of property, plant and equipment 6 (36) -

Net cash used in investing activities (36) -

Financing activities

Reduction in share capital - (3,000)

Dividends paid 12 (1,055) (2,584)

Net cash used in financing activities (1,055) (5,584)

Net increase in cash and cash equivalents 3,592 31

Cash and cash equivalents, beginning of the year (3,920) (3,951)

Cash and cash equivalents, end of the year 9 (328) (3,920)

9

United Power Company SAOG

1 Legal status and activities

The financial statements were approved for issue by the Board of Directors on 9 February 2017.

2 Significant agreements

The Company has entered into the following significant agreements:

(i)

(ii)

All the property, plant and equipment of the Company is to be transferred at RO 1 to the Government

automatically at the end of the Project Life, which, in accordance with Supplemental Agreements for

the Expansion Project, expires on 30 April 2020. (At the end of the Project Life, the value of the shares

of the Company will become nil.)

The original duration of the Company was for a period of twenty-five years commencing from 9 January

1995 being the date of its registration in the Commercial Register of the Ministry of Commerce and

Industry (‘MOCI’). At an Extra-ordinary General Meeting held on 17 January 2000, the duration of the

Company was increased by five years thereby revising the duration of the Company to thirty years ("the

Project Life") commencing from 9 January 1995. The MOCI approved the extension to the Company’s

life on 11 October 2000.

Effective 1 May 2005, the rights and obligations of the Ministry of Housing, Electricity and Water under

the Power Purchase Agreement (‘PPA’) was novated to the Oman Power and Water Procurement

Company SAOC (‘OPWPC') in accordance with the arrangements described in the Master Novation

Agreement signed on 8 October 2005. All the financial obligations of the OPWPC under the Project

Agreements are secured under the guarantee issued by the Ministry of Finance, Government of Oman,

which has come into force on execution of the Novation Agreements. The PPA contains embedded

derivatives in the pricing formulae that compute the variable capacity charge rate and energy charge

rate for Phase 1 and Phase 2. The percentages of the variable capacity charge rate and energy charge

rate for Phase 1 and Phase 2 is adjusted to reflect changes in United States Consumer Price Index (CPI)

and the Omani Consumer Price Index assuming an exchange rate pegged to the United States Dollar

(‘USD’).

Agreements with the Government for project implementation, power purchase and land lease for Phase

1 (‘Project Agreements’) were entered into on 27 June 1994 by the United Power Group (‘the Group’)

comprising some of the Founder Shareholders. Under a Novation Agreement entered into by the

Company with the Group, the Company assumed all rights, duties, liabilities and obligations of the

Group pursuant to the Project Agreements.

Notes to the financial statements for the year ended 31 December 2016

The Company's principal place of business is located at Nizwa, Sultanate of Oman.

United Power Company SAOG (‘the Company’) was registered as a public joint stock company in the

Sultanate of Oman on 9 January 1995. The Company has been established to undertake a project

primarily to Build, Own, Operate and Transfer (“BOOT”) to the Government of the Sultanate of Oman

(‘the Government’) a power station at Manah, and to build, own and transfer (“BOT”) to the

Government, interconnection and transmission facilities. The Company is also permitted to undertake

activities related to the expansion of its primary objective. Accordingly, the Company implemented the

Phase II-Expansion Project (‘the Expansion Project’) during the year ended 31 December 2000.

10

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

2 Significant agreements (continued)

(iii)

(iv)

(v)

(vi)

All parties acknowledged that whicle the ITF was owned by UPC, it was being operated by Oman

Electricity Transmission Company SAOC ("OETC") in respect to its transmission components and by

Mazoon Electricity Company ("MEC") in respect to its distribution components, each as per their

licensed activities.

UPC and OPWP (in accordance with its right under the novation agreement), have decided to transfer

the interconnection and transmission facility to OETC and MEC, whereby OETC will receive the

Transmission Assets and MEC will receive the Distribution Assets.

As envisaged in the PPA, the fully depreciated ITF assets were to be transferred for consideration of RO

1. Accordingly, on 1 December 2016, all of the above parties executed the "Interconnection and

Transfer Facility Agreement", to complete this process.

The Company has entered into an Operations and Maintenance Agreement with Suez Tractebel

Operation and Maintenance Oman (“STOMO”), a company owned by Kahrabel FZE (Engie) (70%) and

Sogex LLC (30%).

The Company has entered into a Management Agreement (‘the Management Agreement’) with Power

Development Company LLC (‘PDC’), a related party, to provide full management and administrative

services to the Company. From 1 January 2009, the base fee has been fixed at RO 601,842 (USD 1.561

million, being the indexed base fee for 2008 converted to Omani Rials at the exchange rate prevailing

on 31 December 2008) and is indexed annually based on the Sultanate of Oman CPI published by the

Ministry of National Economy. The Company is also liable to pay a management fee of USD 400,000 (RO

154,200) for each calendar year in respect of Phase II of the plant (‘the Expansion Project’). No

indexation is applicable on the Expansion Project fee. In addition to the management fee, the Company

also pays to PDC, all proper costs and expenses which are incurred by PDC in rendering the above

services.

Pursuant to the Project Agreements, the Company had, on 19 December 1999, entered into

Supplemental and Addendum Agreements with the Government for the expansion of the power

generation facilities. The above agreements have been amended and the duration of all the agreements

has now been extended up to 30 April 2020.

The Government of the Sultanate of Oman represented by the former Ministry of Electricity and Water

and United Power SAOG ("UPC") had entered into a Power Purchase Agreement dated 27 June 1994

("PPA"), a supplemental agreement to the PPA dated 19 December 1994 and an addendum agreement to

the PPA dated 19 December 1999 by which UPC constructed, owned and operated the project

comprising the plant and the Interconnection and Transmission Facilities ("ITF") and by the end of the

initial term transfer the Project to the former Ministry of Electricity and Water ("MEW").

Following the Sultani Decree No. 78/2004 promulgating the law for the regulation and privatisation of

the electricity and water sector (as amended), a novation agreement dated 8 October 2005 was signed

between former Ministry of Housing, Electricity and Water ("MHEW") and UPC and OPWP whereby the

rights and obligation of the MEW under the Manah Project Agreement were novated to OPWP.

11

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

2 Significant agreements (continued)

3 Basis of preparation

Statement of compliance

Functional currencies

Basis of presentation

As per the terms of the PPA, UPC has fully received the fixed capacity fees relating to ITF from

Commercial Operation Date to 14 Deptember 2016 (completion of 20 years of Phase 1) and therefore

there was no financial loss/gain arising on tranfer of ITF assets.

During 2004, the Company reached settlement with the MHEW ('OPWPC') regarding the commencement

of Phase 1 term life of twenty years effective 14 September 1996 instead of 15 October 1996. The

effect of this change and resolution of other matters was taken into account in the financial year ended

31 December 2004.

The financial statements are prepared under historical cost convention. These financial statements

have been prepared on the basis that the Company commenced full generation and distribution of

electricity on 15 October 1996. All costs incurred during the construction period of the project were

capitalized on 15 October 1996.

The financial statements have been prepared in accordance with International Financial Reporting

Standards (“IFRS”) issued by the International Accounting Standards Board (IASB), interpretations issued

by the International Financial Reporting Interpretation Committee (IFRIC) and the relevant

requirements of the Commercial Companies Law 1974, as amended, of the Sultanate of Oman and the

relevant disclosure requirements for licensed companies issued by the Capital Market Authority (CMA).

The financial statements are presented in Omani Rials, rounded off to the nearest thousand, which is

the functional and reporting currency for the financial statements.

The Company commenced partial generation of electricity on 31 May 1996. On 15 October 1996, the

entire construction of the power station and transmission facilities was completed and from that date

the Company commenced full generation of electricity. The Ministry of Housing, Electricity and Water

(“MHEW”) had initially determined 1 January 1997 as the “Commercial Operation Date’ and had issued

the Commercial Completion Certificate on that date.

Under the Supplemental and Addendum Agreement to the PPA (‘Supplemental Agreement’), the

operation date for the Expansion Project was 1 May 2000. The MHEW (‘OPWPC’) issued an interim

completion certificate for the first unit of the Expansion Project on 29 April 2000. The interim

completion certificate for the second unit of the Expansion Project as well as the commercial

operations certificate for the Expansion Project was issued by the OPWPC on 19 May 2000. Accordingly,

19 May 2000 has been determined as the “Commercial Operation date’ for the Expansion Project. The

Company has billed the MHEW ('OPWPC') from the respective completion dates for the two units of the

Expansion Project in accordance with the Supplemental Agreement.

12

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

3 Basis of preparation (continued)

4 Adoption of new and revised IFRS

• Depreciation on property, plant and equipment has been booked on a straight-line basis at rates

prescribed in the above mentioned agreement.

The tariff for electricity generated and supplied to OPWPC has been structured in the Project

Agreements in such a way that the tariff rates were significantly higher during the initial years as

compared to the later period of the Project Life. The tariff for electricity to be generated and supplied

from the Expansion Project under the Supplemental Agreement has been structured so that the tariff is

more uniformly received over the Project Life.

Improvements/amendments to IFRS/IAS 2012/2014 cycle

Improvements/amendments to IFRS/IAS issued in 2012/2014 cycle contained numerous amendments to

IFRS that the IASB considers non-urgent but necessary. ‘Improvements to IFRS’ comprise amendments

that result in accounting changes to presentation, recognition or measurement purposes, as well as

terminology or editorial amendments related to a variety of individual IFRS standards. The amendments

are effective for the Company’s annual audited financial statements beginning on or after 1 January

2016 and subsequent periods with earlier adoption permitted.

Accordingly, while the combined tariff revenue for the Company after the first eight years of

operations will significantly reduce, the annual depreciation charges will remain constant. Accordingly,

the net profits available for appropriation to the shareholders has been significantly higher during the

first half compared to the second half of the Project life. Although it is not possible to accurately

determine the effect on profits if revenue recognised was matched with the depreciation charge, the

Company is expected to continue to earn net profits.

In terms of the PPA signed in 1994 between the Company and the Government, the Company was given

the right to build, own, operate and transfer a power plant and build, own and transfer interconnection

and transmission facilities, to the Government.

IFRIC 12 ‘Service Concession Arrangements’ which was effective for annual periods commencing on or

after 1 January 2008 gives guidance on the accounting by operators for public-to-private service

concession arrangements. However, since inception of the Company in the year 1995, the financial

statements of the Company have disclosed that:

The Company’s gas turbines, interconnection and transmission facilities, balance of plant, plant spares

and plant buildings and ancillaries are being depreciated on a straight-line basis in accordance with

their expected useful lives and with the Project Agreements.

• The Company has recognised the ‘revenue’ based on the agreed tariff prescribed under the PPA

between the Government and the Company.

• The tariff has been agreed based on covenants of financing agreements, which includes a

prescribed repayment profile, debt coverage ratios and other security features.

13

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

4 Adoption of new and revised IFRS (continued)

Standards, amendments and interpretations effective and adopted in the year 2016

Title

IAS 1 Presentation of Financial Statements 1 January 2016

IAS 16 Property, Plant and Equipment 1 January 2016

Title

IAS 19 Employee Benefits 1 January 2016

IAS 27 Separate Financial Statements 1 January 2016

IAS 28 Investments in Associates and Joint Ventures 1 January 2016

IAS 34 Interim Financial Reporting 1 January 2016

IAS 38 Intangible Assets 1 January 2016

IAS 41 Agriculture 1 January 2016

IFRS 7 Non-current Assets Held for Sale and Discontinued Operations 1 January 2016

IFRS 7 Financial Instruments – Disclosures 1 January 2016

IFRS 10 Consolidated Financial Statements 1 January 2016

IFRS 11 Joint Arrangements 1 January 2016

IFRS 12 Disclosure of Interests in Other Entities 1 January 2016

IFRS 14 Regulatory Deferral Accounts 1 January 2016

Standards, amendments and interpretations issued but not yet effective in the year 2016

Title

IFRS 9 Financial Instruments 1 January 2018

IFRS 15 Revenue from Contracts with Customers 1 January 2018

IFRS 16 Leases 1 January 2019

Standards, amendments and interpretations issued and effective in the year 2016 but not relevant

Effective for annual periods

beginning on or after

The following new standards, amendments to existing standards and interpretations to published

standards are mandatory for accounting periods beginning on or after 1 January 2016 or subsequent

periods, but are not relevant to the Company’s operations:

Standard or

Interpretation

Effective for annual periods

beginning on or after

The following new/amended accounting standards and interpretations have been issued, but are not

mandatory for the year ended 31 December 2016. They have not been adopted in preparing the

financial statements for the year ended 31 December 2016, but may affect the Company in the period

of initial application. In all cases, the Company intends to apply these standards from the application

date as indicated in the table below.

Standard or

Interpretation

Effective for annual periods

beginning on or after

The following new standards, amendment to existing standards or interpretations to published

standards are mandatory for the first time for the financial year beginning 1 January 2016 and have

been adopted in the preparation of the financial statements:

Standard or

Interpretation

14

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

4 Adoption of new and revised IFRS (continued)

Early adoption of amendments or standards in the year 2016

The Company did not early-adopt any new or amended standards in the year ended 31 December 2016.

The Company is assessig the impact on the operational results of the Company for the year ended 31

December 2016 had the Company early adopted any of the above standards applicable to the Company.

Standards, amendments and interpretations issued but not yet effective in the year 2016

(continued)

IFRS 9, ‘Financial Instruments’ has an effective date for accounting periods beginning on or after 1

January 2018 now that it has been finalised. IFRS 9 outlines the recognition, measurement and

derecognition of financial assets and financial liabilities, the impairment of financial assets and hedge

accounting. Financial assets are to be measured at amortised cost, fair value through profit and loss or

fair value through other comprehensive income, with an irrevocable option on initial recognition to

recognise some equity financial assets at fair value through other comprehensive income. The

impairment model in IFRS 9 moves to one that is based on expected credit losses rather than the IAS 39

incurred loss model. The derecognition principles of IAS 39, ‘Financial Instruments: Recognition and

Measurement’ have been transferred to IFRS 9. The hedge accounting requirements have been

liberalised from that allowed previously. The requirements are based on whether an economic hedge is

in existence, with less restriction about proving whether a relationship will be effective than current

requirements.

IFRS 15, ‘Revenue from Contracts with Customers’ issued in May 2014 establishes principles for

reporting useful information to users of financial statements about the nature, amount, timing and

uncertainty of revenue and cash flows arising from an entity’s contracts with customers. IFRS 15

supersedes IAS 11 ‘Construction Contracts’, IAS 18 ‘Revenue’ and related IFRICs 13, 15 and 18, and SIC-

31. IFRS 15 is applicable for annual periods beginning on or after 1 January 2018. The standard is based

on a 5 step approach to recognise revenue and also provides specific principles to apply, when there is

a contract modification, accounting for contract costs and accounting for refunds and warranties. On

application of the standard, the disclosures are likely to increase.

IFRS 16 issued in January 2016 provides a single lessee accounting model, requiring lessees to recognise

assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has

a low value. Lessors continue to classify leases as operating or finance, with lessor accounting

substantially unchanged from IAS 17. IFRS 16 is effective from 1 January 2019.

15

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

5 Summary of significant accounting policies

(a) Property, plant and equipment

Description Years

Gas turbines 20

Balance of plant 20

Plant spares 8

Interconnection and transmission facilities 18 to 20

Plant buildings and ancillaries 25

Other assets - furniture, office equipment and motor vehicles 4

(b) Capital work-in-progress

(c) Impairment of assets

Financial assets

Repairs and renewals are charged to the statement of profit or loss and other comprehensive income

when the expenditure is incurred.

Capital work-in-progress is stated at cost including capital advances incurred upto the date of the

statement of financial position and is not depreciated. When commissioned, capital work-in-progress is

transferred to the appropriate property, plant and equipment and depreciated in accordance with the

Company's policy.

A summary of the significant accounting policies adopted in the preparation of these financial

statements is set out below. These policies have been adopted for all the years presented, unless

stated otherwise.

At the end of each reporting period, the management assesses if there is any objective evidence

indicating impairment of financial assets carried at cost or non-collectability of receivables. An

impairment loss, if any, arrived at as a difference between the carrying amount and the recoverable

amount, is recognised in the statement of profit or loss and other comprehensive income. The

recoverable amount represents the present value of expected future cash flows discounted at the

original effective interest rate. Cash flows relating to short-term receivables are not discounted.

Depreciation is charged to the statement of profit or loss and other comprehensive income on a straight-

line basis over the estimated useful lives of items of property, plant and equipment. The estimated

useful economic lives are as follows:

Items of property, plant and equipment are stated at cost less accumulated depreciation and

impairment losses. Following initial recognition at cost, expenditure incurred to replace a component

of an item of property, plant and equipment which increases the future economic benefits embodied in

the item of property, plant and equipment is capitalised. All other expenditures are recognised in the

statement of profit or loss and other comprehensive income as an expense as incurred.

Items of property, plant and equipment are derecognised upon disposal or when no future economic

benefit is expected to arise from the continued use of the asset. Any gains or losses arising on de-

recognition of the asset is included in the statement of profit or loss and other comprehensive income

in the year the item is derecognised.

16

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

5 Summary of significant accounting policies (continued)

(c) Impairment of assets (continued)

Non-financial assets

(d)

(e)

(f)

(g) Cash and cash equivalents

(h)

(i) Provisions

Trade payables

Trade payables are recognised for amounts to be paid for goods and services received, whether or not

billed to the Company. Trade payables are initially measured at their fair values and subsequently

measured at amortised cost, using the effective interest method.

Dividends

Dividends are recognised as a liability in the period in which they are declared.The Board of Directors

recommends to the shareholders the dividend to be paid out of the Company’s profits. The Directors

take into account appropriate parameters including the requirements of the Commercial Companies

Law 1974, as amended, while recommending dividend.

A provision is recognised in the statement of financial position when the Company has a legal or

constructive obligation as a result of a past event, and it is probable that an outflow of economic

benefits will be required to settle the obligation.

Trade and other receivables originated by the Company are measured at cost. An allowance for credit

losses of trade and other receivables is established when there is objective evidence that the Company

will not be able to collect the amounts due. When a trade or other receivable is uncollectible, it is

written-off against the allowance account for credit losses.

At the end of each reporting period, the management assesses if there is any indication of impairment

of non-financial assets. If an indication exists, the management estimates the recoverable amount of

the asset and recognises an impairment loss in the statement of profit or loss and other comprehensive

income. The management also assesses if there is any indication that an impairment loss recognised in

prior years no longer exists or has reduced. The resultant impairment loss or reversals are recognised

immediately in the statement of profit or loss and other comprehensive income.

Inventories

For the purposes of the statement of cash flows, cash and cash equivalents consist of bank balances

and cash, net of short-term bank borrowings.

Trade and other receivables

Inventories comprise of fuel oil and other spares and are stated at the lower of cost and net realisable

value. The cost of inventories is based on first-in-first-out basis and comprises expenditure incurred in

the normal course of business in bringing inventories to their present location and condition. Net

realisable value is the estimate of the selling price in the ordinary course of business. Where necessary,

provision is made for obsolete, slow-moving and defective inventories.

17

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

5 Summary of significant accounting policies (continued)

(j) Employees' terminal benefits

(k) Revenue

(l) Other income

Other income is accounted for on the accruals basis, unless collectibility is in doubt.

(m)

(n) Foreign currencies

(o) Directors’ remuneration

In respect of Omani employees, contributions are made in accordance with the Oman Social Insurance

Law and recognised as an expense in the statement of profit or loss and other comprehensive income as

incurred.

For non-Omani employees, provision is made for amounts payable under the Oman Labour Law, based

on the employees’ accumulated periods of service at the statement of financial position date. This

provision is classified as a non-current liability.

Leases where the lessor retains substantially all the risks and benefits of ownership of the asset are

classified as operating leases. Operating lease payments are recognised as an expense in the statement

of profit or loss and other comprehensive income on a straight-line basis over the lease term.

Operating leases

The Company follows the Commercial Companies Law 1974, as amended, and other latest relevant

directives issued by the CMA, with regards to determining the amount to be paid as Directors’

remuneration. Directors’ remuneration is charged to the statement of profit or loss and other

comprehensive income in the year to which they relate.

Revenue comprises tariffs for fixed capacity charges for transmission facilities and turbines, variable

capacity charges and energy charges. Tariffs are calculated in accordance with the Project Agreements.

No revenue is recognised if there are significant uncertainties regarding recovery of the consideration

due and associated costs. Tariff revenue has been accounted net of gas fuel costs, which are borne by

the Government of the Sultanate of Oman.

Transactions denominated in foreign currencies are translated to Omani Rial at the foreign exchange

rates prevailing at the date of the transaction. Monetary assets and liabilities denominated in foreign

currencies at the end of the reporting period are translated to Omani Rial at the foreign exchange rates

prevailing at that date. Foreign exchange differences arising on translation are recognised in the

statement of profit or loss and other comprehensive income.

18

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

5 Summary of significant accounting policies (continued)

(p)

(q)

(r) Critical accounting judgments and key source of estimation uncertainity

All financial liabilities are initially measured at fair value and are subsequently measured at amortised

cost. A financial liability is derecognised when the obligation under the liability is discharged or

cancelled or expires. Where an existing financial liability is replaced by another from the same lender

on substantially different terms, or the terms of an existing liability are substantially modified, such an

exchange or modification is treated as a derecognition of the original liability and the recognition of a

new liability, and the difference in the respective carrying amounts is recognised in statement or profit

or loss and other comprehensive income.

The carrying amount of deferred income tax assets are reviewed at each reporting date and reduced to

the extent that it is no longer probable that sufficient taxable profit will be available to allow all or

part of the deferred income tax asset to be utilised.

Taxation is provided in accordance with Omani fiscal regulations.Taxation for the year comprises

current and deferred tax. Current tax is the expected tax payable on the taxable income for the year,

using tax-rates enacted or substantially enacted at the end of the reporting period.

Deferred income tax is provided on all temporary differences at the reporting date between the tax

bases of assets and liablities and their carrying amounts. Deferred income tax assets and liabilities are

measured at the tax rates that are expected to apply in the period when the asset is realised or the

liability is settled, based on tax laws that have been enacted at thereporting date. Deferred income tax

assets are recognised for all deductible temporary differences, carry-forward of unused tax credits and

unused tax losses, to the extent that it is probable that taxable profit will be available, against which

the deductible temporary differences and the carry-forward of unused tax credits and unused tax losses

can be utilised.

Income tax

Preparation of financial statements in accordance with IFRS requires the Company’s management to

make estimates and assumptions that affect the reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the financial statements, and the reported

amounts of revenue and expenses during the reporting period. The determination of estimates requires

judgments which are based on historical experience, current and expected economic conditions, and all

other available information. Actual results could differ from those estimates.

Financial liabilities

19

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

5 Summary of significant accounting policies (continued)

Economic useful lives of property, plant and equipment

Provisions

Going concern

Contingencies

The Company also creates a provision for obsolete and slow-moving inventories. Estimates of net

realisable value of inventories are based on the most reliable evidence available at the time the

estimates are made. These estimates take into consideration fluctuations of price or cost directly

relating to events occurring subsequent to the statement of financial position date to the extent that

such events confirm conditions existing at the end of the reporting period.

The most significant areas requiring the use of management estimates and assumptions in the financial

statements relate to:

An assessment is made at each statement of financial position date to determine whether there is

objective evidence that specific financial assets may be impaired. An estimate of the collectible

amount of trade receivables is made when the collection of the full amount is no longer probable. For

individually significant amounts, this estimate is performed on an individual basis. Amounts which are

not significant, but which are past due, are individually assessed collectively and a provision is applied

according to the length of time the receivable is past due, based on historical recovery rates. Any

difference between the amount actually collected in future periods and the amounts expected is

recognised in the statement of profit or loss and other comprehensive income.

The Company's property, plant and equipment are depreciated on a straight-line basis over their

economic useful lives. Economic useful lives of property, plant and equipment are reviewed by

management periodically. Estimation of economic useful lives is based on management’s assessment of

various factors such as the operating cycles, the maintenance programs and normal wear and tear using

its best estimates.

The management of the Company reviews the financial position of the Company on a periodical basis

and assesses the requirement of any additional funding to meet the working capital requirements and

estimated funds required to meet the liabilities as and when they become due. In addition, the

shareholders of the Company ensure that they provide adequate financial support to funding the

requirements to the Company to ensure the going concern status of the Company.

By their nature, contingencies will only be resolved when one or more future events occur or fail to

occur. The assessment of such contingencies inherently involves the exercise of significant judgment

and estimates of the outcome of future events.

20

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

6 Property, plant and equipment

(a) The movement in property, plant and equipment is as set out below:

2016

Cost

At 31 December 2015 18,945 26,386 5,391 49,994 7,453 128 - 108,297

Additions during the year - - - - 15 - 21 36

Transferred during the year - - - (49,994) - - - (49,994)

At 31 December 2016 18,945 26,386 5,391 - 7,468 128 21 58,339

Accumulated depreciation

At 31 December 2015 18,313 22,440 5,104 47,936 6,714 127 - 100,634

Charge for the year 173 1,263 231 2,058 153 - - 3,878

Transferred during the year - - - (49,994) - - - (49,994)

At 31 December 2016 18,486 23,703 5,335 - 6,867 127 - 54,518

Net book amount

At 31 December 2016 459 2,683 56 - 601 1 21 3,821

Gas

turbines

Plant

spares

Interconnection

and transmission

facilities

Total

RO'000

Plant buildings

and ancillaries

Other

assets

Balance

of plant

Capital

work-in-

progress

In accordance with the PPA, interconnection and transmission facilities ("ITF") have been transferred to the Government of the Sultanate of Oman with effect

from 1 December 2016 as per note 2 (vi).

21

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

6 Property, plant and equipment (continued)

2015

Cost

18,945 26,386 5,391 49,994 7,453 128 108,297

Accumulated depreciation

At 31 December 2015 18,114 21,062 4,871 45,440 6,563 126 96,176

Charge for the year 199 1,378 233 2,496 151 1 4,458

At 31 December 2015 18,313 22,440 5,104 47,936 6,714 127 100,634

Net book amount

At 31 December 2015 632 3,946 287 2,058 739 1 7,663

Plant

spares

Plant buildings

and ancillaries

Other

assets

At 31 December 2014 and at

31 December 2015

Gas

turbines

Total

RO'000

Interconnection

and transmission

facilities

Balance

of plant

22

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

7 Inventories 31 December 31 December

2016 2015

RO'000 RO'000

Liquid fuel 259 259

Spares 63 63

322 322

Provision for obsolescence (63) (63)

259 259

8 Trade and other receivables 31 December 31 December

2016 2015

RO'000 RO'000

Trade receivables 1,475 1,850

Less: provision for impaired trade receivables (93) (93)

1,382 1,757

Prepayments and other receivables 89 229

1,471 1,986

31 December 31 December

2016 2015

RO'000 RO'000

Up to 3 months 1,382 1,757

Trade receivables are from OPWPC, the only customer of the Company.

The carrying amounts of the Company’s trade receivables are primarily denominated in Omani Rial.

The Company, in accordance with the Project Agreements, is required to maintain a base stock of liquid fuel

to be used in case of interruption of gas fuel. Spares stock is maintained for the gas turbines and is held for

emergencies.

Trade receivables from the OPWPC amounting to RO 1.382 million (2015 – RO 1.757 million) are neither past

due nor impaired.

The ageing analysis of unimpaired trade receivables is as follows:

The maximum exposure to credit risk at the reporting date is the fair value of each class of receivable

mentioned above. The trade receivables are secured by a guarantee from the Ministry of Finance.

23

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

9 Cash and cash equivalents

31 December 31 December

2016 2015

RO'000 RO'000

Current account balances with banks 172 80

172 80

Less: short-term bank borrowings (500) (4,000)

The current account balances with banks are non-interest bearing. (328) (3,920)

10 Share capital

Authorised share capital

Issued and fully paid-up share capital

Total Paid Paid

RO ’000 % in-cash in-kind

RO ’000 RO ’000

Preference shares 1,200 60 162 1,038

Ordinary shares 800 40 800 -

2,000 100 962 1,038

Number of % to % to

preference preference total

31 December 2016 shares shares shares

Mannah Power Co Limited 762,552 63.55 38.13

Ministry of Defence, Pension Fund 109,360 9.11 5.47

M GEC (Oman) Holdings Limited 328,078 27.34 16.40

Fractions from capital reduction 10 - -

1,200,000 100 60

For the purposes of the statement of cash flows, cash and cash

equivalents comprise the following:

At 31 December 2016 and 31 December 2015, the Company’s authorised share capital comprised of

15,965,760 ordinary shares and 23,948,640 preference shares of RO 1 each.

At the end of the reporting period, the details of the significant preference shareholders and the percentage

of their shareholding in the Company is as follows:

At 31 December 2016, the Company’s issued and paid-up share capital consists of 2,000,000 shares of RO 1

each (2015: 2,000,000 shares of RO 1 each) analysed as follows:

Preference shareholders have the right to two votes per share at any general meeting of the Company and

are entitled to a dividend of up to 5% of the net profit of the Company prior to and in addition to any

dividend to the holders of ordinary shares. The holders of ordinary shares have the right to one vote per share

at any general meeting of the Company.

24

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

10 Share capital (continued)

Number of % to % to

preference preference total

31 December 2015 shares shares shares

Mena Infrastructure Investments Limited 762,552 63.55 38.13

Ministry of Defence, Pension Fund 109,360 9.11 5.47

M GEC (Oman) Holdings Limited 328,078 27.34 16.40

Fractions from capital reduction 10 - -

1,200,000 100 60

None of the ordinary shareholders own more than 10% of the Company’s share capital (2015 – none).

11 Legal reserve

12 Dividends paid and proposed

(a)

(b)

13 Income tax

(a) Current tax

Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Statement of profit or loss and other comprehensive income

Tax charge (net)

Current tax charge 533 617

Deferred tax credit (408) (474)

125 143

Provision for income tax has been made after giving due consideration to adjustments for potential

allowances and disallowances.

In accordance with Article 106 of the Commercial Companies Law 1974, as amended, of the Sultanate of

Oman, 10% of the Company’s net profit for the year is to be transferred to a non-distributable legal reserve

until the amount of the legal reserve becomes equal to one-third of the Company’s issued share capital.

During the year ended 31 December 2016, no transfer has been made as the legal reserve has reached the

statutory minimum of one-third of the capital (2015: RO Nil).

During the year, dividend to preference shareholders of RO 0.545 per share amounting to RO 0.654 million

and dividend to ordinary shareholders of RO 0.500 per share amounting to RO 0.400 million for the year 2015

was approved in the Annual General Meeting held on 22 March 2016 and paid subsequently.

During the year, an amount of RO 417,877 pertaining to the years 2015 unclaimed dividends have been

transferred to the Investors’ Trust Fund of the CMA.

25

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

13 Income tax (continued)

31 December 31 December

2016 2015

RO'000 RO'000

Statement of financial position

Current liability

Current year 533 617

Prior years 213 193

746 810

Deferred tax liability 147 554

Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Profit before tax 1,067 1,214

Taxation on accounting profit at applicable rates 125 142

Add tax effect of:

Depreciation on property, plant and equipment 408 474

Other expenses disallowed for tax purpose - 1

533 617

(b) Status of tax assessments

The reconciliation of taxation on the accounting profit with the current taxation charge for the year is as

follows:

The Company is subject to income tax in accordance with the income tax law of the Sultanate of Oman at the

tax rate of 12% on taxable profits in excess of RO 30,000. The taxation assessments for the years 2011 to

2015 have not been finalised by the Secretariat General for Taxation (SGT). The Management believes that

the tax assessed, if any, for the unassessed tax years would not be material to the financial position as at the

31 December 2016.

26

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

13 Income tax (continued)

(c) Deferred tax

Total

RO '000 RO '000 RO '000

31 December 2016

At 31 December 2015 573 (19) 554

Recognised in the statement of profit or loss

and other comprehensive income (408) - (408)

At 31 December 2016 165 (19) 147

Total

RO '000 RO '000 RO '000

31 December 2015

At 31 December 2014 1,047 (19) 1,028

Recognised in the statement of profit or loss

and other comprehensive income (474) - (474)

At 31 December 2015 573 (19) 554

14 Trade and other payables 31 December 31 December

2016 2015

RO'000 RO'000

Trade payables 179 468

Accruals and other payables 376 237

Directors’ remuneration payable 42 75

597 780

Trade payables are generally settled within 60 to 90 days of the suppliers' invoice date.

Property,

plant and

equipment

The contractual maturity date for trade payables is due within 12 months from the statement of financial

position date.

The deferred tax liability and the deferred tax charge (net) in the statement of profit or loss and other

comprehensive income are attributable to the following items:

Provision for

obsolete

inventories

and impaired

trade

receivables

Provision for

obsolete

inventories

and impaired

trade

receivables

Property,

plant and

equipment

27

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

15 Short-term bank borrowings 31 December 31 December

2016 2015

RO'000 RO'000

Short-term borrowings 500 4,000

16 Related party transactions and balances

Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Management fees 897 896

Shared office overheads 471 464

Directors’ remuneration and attendance fees 45 91

Key management personnel remuneration - 11

17 Revenue Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Revenue from Phase 1 3,958 4,523

Revenue from Phase 2 6,075 6,288

10,033 10,811

18 Other income Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Penalty income from STOMO - 96

Others - 21

- 117

The Company, in the ordinary course of business, deals with parties, which fall within the definition of

‘related parties’ as contained in International Accounting Standard Number 24. The management believes

that such transactions are not materially different from those that could be obtained from unrelated parties.

Significant transactions during

the period with related parties

are as follows:

Short term bank borrowings are from local commercial banks which carry interest ranging between 2.25% and

3.5% per annum (2015 – between 1.85% and 2.5% per annum). The borrowings are revolving facilities with a

maximum period of 6 months during the availability period. The borrowing facilities contain certain

restrictive covenants that are common for such arrangements.

28

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

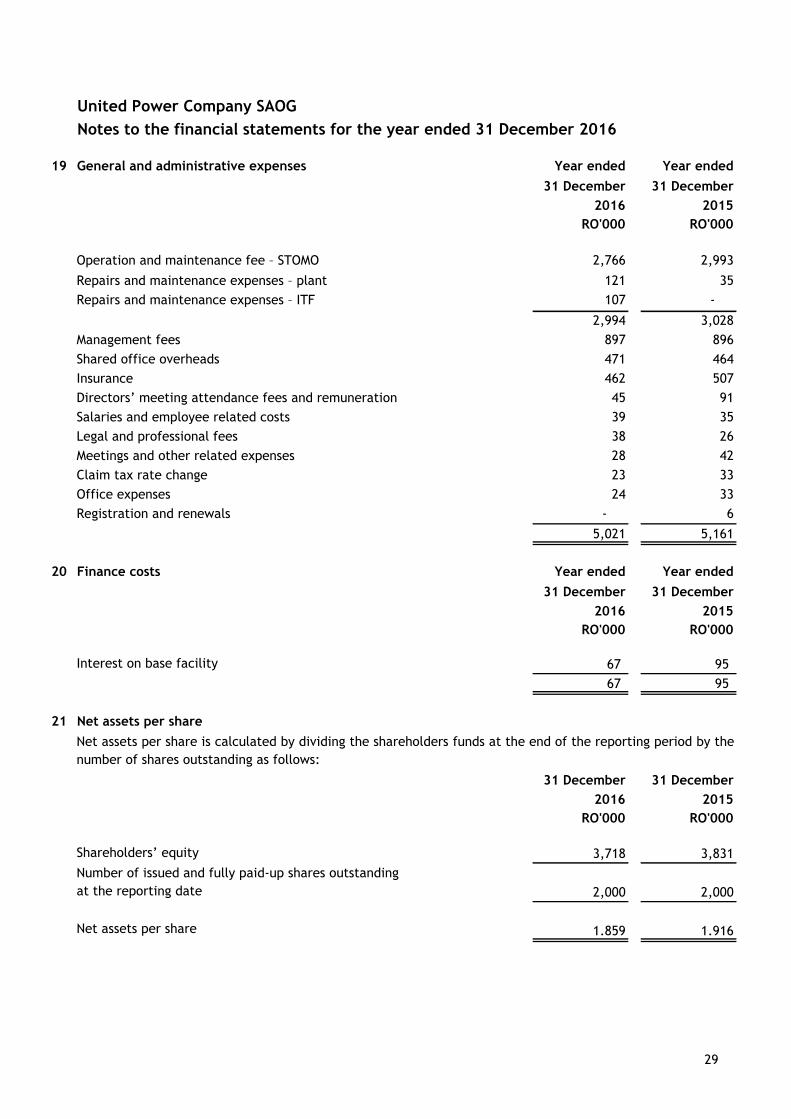

19 General and administrative expenses Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Operation and maintenance fee – STOMO 2,766 2,993

Repairs and maintenance expenses – plant 121 35

Repairs and maintenance expenses – ITF 107 -

2,994 3,028

Management fees 897 896

Shared office overheads 471 464

Insurance 462 507

Directors’ meeting attendance fees and remuneration 45 91

Salaries and employee related costs 39 35

Legal and professional fees 38 26

Meetings and other related expenses 28 42

Claim tax rate change 23 33

Office expenses 24 33

Registration and renewals - 6

5,021 5,161

20 Finance costs Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Interest on base facility 67 95

67 95

21 Net assets per share

31 December 31 December

2016 2015

RO'000 RO'000

Shareholders’ equity 3,718 3,831

2,000 2,000

Net assets per share 1.859 1.916

Net assets per share is calculated by dividing the shareholders funds at the end of the reporting period by the

number of shares outstanding as follows:

Number of issued and fully paid-up shares outstanding

at the reporting date

29

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

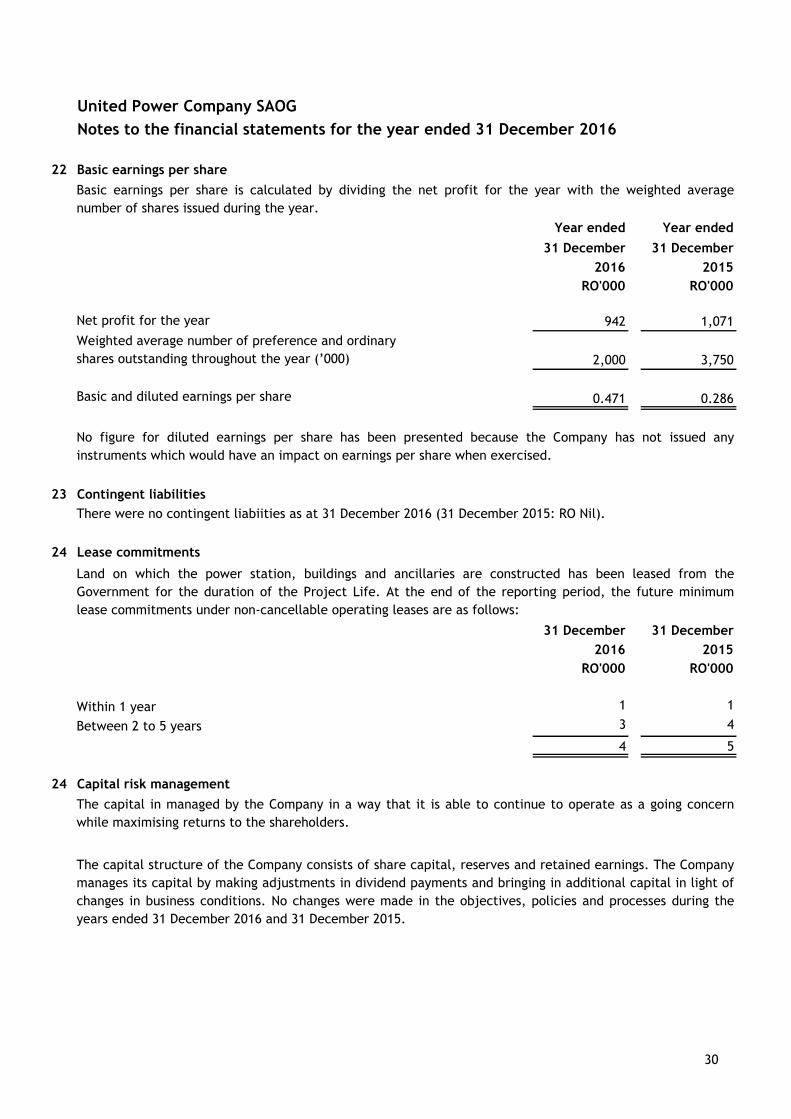

22 Basic earnings per share

Year ended Year ended

31 December 31 December

2016 2015

RO'000 RO'000

Net profit for the year 942 1,071

2,000 3,750

Basic and diluted earnings per share 0.471 0.286

23 Contingent liabilities

There were no contingent liabiities as at 31 December 2016 (31 December 2015: RO Nil).

24 Lease commitments

31 December 31 December

2016 2015

RO'000 RO'000

Within 1 year 1 1

Between 2 to 5 years 3 4

4 5

24 Capital risk management

The capital in managed by the Company in a way that it is able to continue to operate as a going concern

while maximising returns to the shareholders.

The capital structure of the Company consists of share capital, reserves and retained earnings. The Company

manages its capital by making adjustments in dividend payments and bringing in additional capital in light of

changes in business conditions. No changes were made in the objectives, policies and processes during the

years ended 31 December 2016 and 31 December 2015.

No figure for diluted earnings per share has been presented because the Company has not issued any

instruments which would have an impact on earnings per share when exercised.

Land on which the power station, buildings and ancillaries are constructed has been leased from the

Government for the duration of the Project Life. At the end of the reporting period, the future minimum

lease commitments under non-cancellable operating leases are as follows:

Weighted average number of preference and ordinary

shares outstanding throughout the year (’000)

Basic earnings per share is calculated by dividing the net profit for the year with the weighted average

number of shares issued during the year.

30

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

25 Financial assets and liabilities and risk management

(a) Financial assets and liabilities

(b)

(c)

31 December 31 December

2016 2015

RO'000 RO'000

Trade and other payables 597 780

Taxation 746 810

Short-term bank borrowings 500 4,000

Less: cash and bank balances (172) (80)

Net debt 1,671 5,510

2,000 2,000

667 667

1,051 1,164

3,718 3,831

5,389 9,341

Gearing ratio 0.31 0.59

Risk management is carried out by the Finance Department of the Company under the guidance of the senior

management and Board of Directors. The senior management and Board of Directors provide significant

guidance for overall risk management covering specific areas such as credit risk, interest rate risk, foreign

exchange risk and investment of excess liquidity.

The primary objective if the Company's capital management is to ensure that it maintains a healthy capital

ratio in order to support its business and maximise shareholders' value.

Financial assets and liabilities carried on the statement of financial position include cash and bank balances,

trade and other receivables, short-term bank borrowings and trade and other payables. The particular

recognition methods adopted are disclosed in the individual policy statements associated with each item.

The Company monitors capital using a gearing ratio, which is net debt divided by total capital plus net debt.

The Company includes within net debt, trade and other payables and short-term bank borrowings less cash

and bank balances. Capital includes share capital, reserves and retained earnings.

Total capital and net debt

Legal reserve

Total capital

Retained earnings

Risk management

Capital management

Share capital

31

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

25 Financial assets and liabilities and risk management (continued)

(a) Market risk

(i) Foreign exchange risk

As the Company has no exposure to investments, it does not have the risk of fluctuation in prices.

(b)

The Company’s short term borrowings are on fixed rate basis. Accordingly, the Company is not exposed to

interest rate risk due to fluctuation in market interest rate. The Management manages its exposure to

interest rate risk on short term borrowings by ensuring that they are as far as possible on a fixed rate basis.

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate

because of changes in interest rates.

(ii) Interest rate risk

In addition, the Company's activities expose it to a variety of financial risks: market risk (including currency

rate risk, interest rate risk and price risk), credit risk and liquidity risk.

The Company is exposed to foreign exchange risk arising from various currency exposures. Significant portion

of revenues and major operating costs are denominated in OMR and indexed to the USD / OMR exchange

rates. The balance operating costs denominated in USD are covered by the fact that OMR is pegged to the

USD and has remained unchanged since 1986. As these currencies are pegged against the Omani Rial, the

Management does not believe that the Company is exposed to any material currency risk.

Foreign exchange risk is the risk that the fair value or future cash flows of a financial instrument will

fluctuate because of a changes in foreign exchange rates.

Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument

fails to meet its contractual obligations, and arises principally from the Company’s receivables. At the end of

the year, the entire trade receivable was from a government owned company (OPWPC). The management

considers the credit risk associated with the trade receivables to be very low because the receivables are

from the Government. Furthermore, the cash is placed in reputable banks, which minimise the credit risk.

The carrying value of accounts and other receivables approximate their fair values due to the short-term

nature of those receivables.

Price risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of

changes in market prices (other than those arising from interest rate risk or currency risk), whether those

changes are caused by factors specific to the individual financial instrument or its issuer, or factors affecting

all similar financial instruments traded in the market.

(iii) Price risk

Credit risk

32

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

25 Financial assets and liabilities and risk management (continued)

(b)

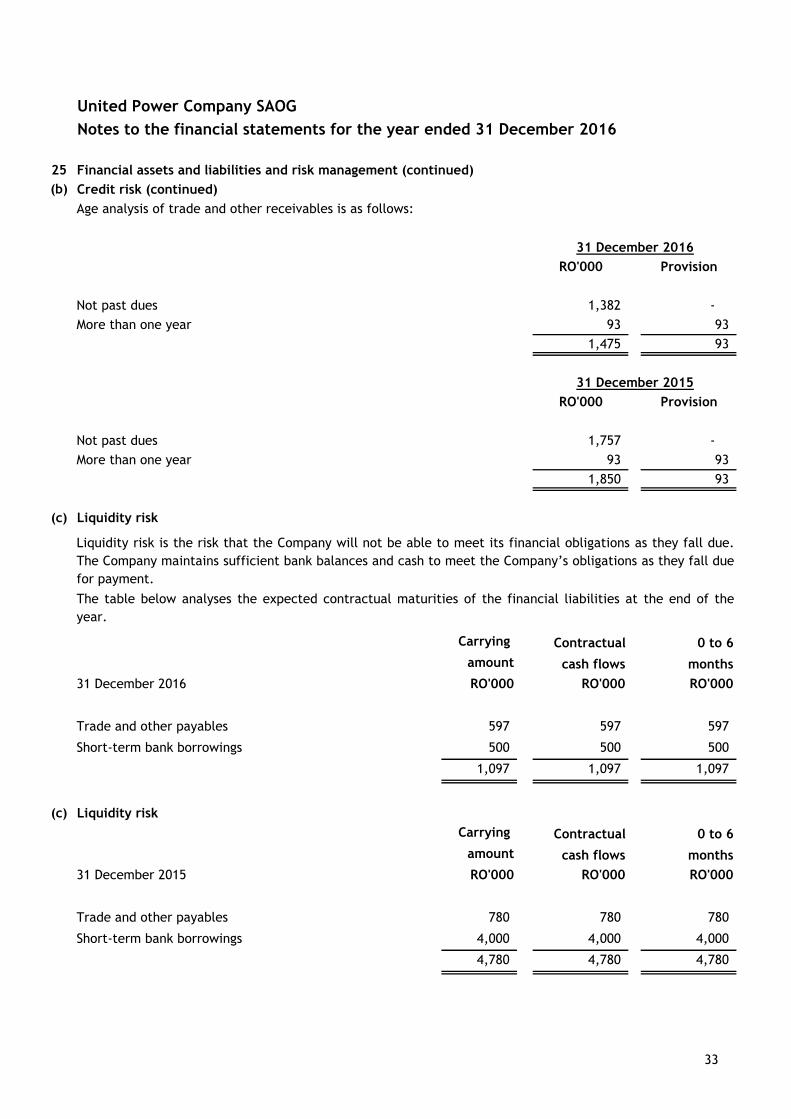

Age analysis of trade and other receivables is as follows:

RO'000 Provision

Not past dues 1,382 -

More than one year 93 93

1,475 93

RO'000 Provision

Not past dues 1,757 -

More than one year 93 93

1,850 93

(c)

Carrying Contractual 0 to 6

amount cash flows months

31 December 2016 RO'000 RO'000 RO'000

Trade and other payables 597 597 597

Short-term bank borrowings 500 500 500

1,097 1,097 1,097

(c)

Carrying Contractual 0 to 6

amount cash flows months

31 December 2015 RO'000 RO'000 RO'000

Trade and other payables 780 780 780

Short-term bank borrowings 4,000 4,000 4,000

4,780 4,780 4,780

Liquidity risk

Credit risk (continued)

Liquidity risk

The table below analyses the expected contractual maturities of the financial liabilities at the end of the

year.

31 December 2016

Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they fall due.

The Company maintains sufficient bank balances and cash to meet the Company’s obligations as they fall due

for payment.

31 December 2015

33

United Power Company SAOG

Notes to the financial statements for the year ended 31 December 2016

26 Capital commitments

27 Subsequent events

28 Comparative figures

There were no events occurring subsequent to 31 December 2016 and before the date of the report that are

expected to have a significant impact on these financial statements.

Certain comparative figures for the previous year have been reclassified, wherever necessary, in order to

conform with the presentation adopted in the current year. Such reclassifications do not affect previously

reported net profit or shareholders' equity.

Outstanding capital commitments as at 31 December 2016 amounted to RO 97 thousand (31 December 2015:

Rial Nil).

34