THIS DISCLOSURE STATEMENT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT. THE FILING AND DISSEMINATION OF THIS DISCLOSURE STATEMENT SHOULD NOT BE CONSTRUED AS A SOLICITATION OF ACCEPTANCES OF THE PLAN, NOR SHOULD THE INFORMATION CONTAINED HEREIN BE RELIED UPON FOR ANY OTHER PURPOSE UNTIL THIS DISCLOSURE STATEMENT HAS BEEN APPROVED BY THE BANKRUPTCY COURT PURSUANT TO SECTION 1125 OF THE BANKRUPTCY CODE. UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - x In re: DELTA AIR LINES, INC., et al., Debtors. : : : : : : : - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - x Chapter 11 Case No. 05-17923 (ASH) (Jointly Administered) DISCLOSURE STATEMENT FOR DEBTORS JOINT PLAN OF REORGANIZATION UNDER CHAPTER 11 OF THE BANKRUPTCY CODE DAVIS POLK & WARDWELL 450 Lexington Avenue New York, New York 10017 Telephone: (212) 450-4000 Fax: (212) 450-6539 John Fouhey (JF 9006) Marshall S. Huebner (MH 7800) Benjamin S. Kaminetzky (BK 7741) Timothy Graulich (TG 0046) Damian S. Schaible (DS 7427) Attorneys for Debtors and Debtors in Possession Dated: December 19, 2006

Transcript

THIS DISCLOSURE STATEMENT HAS NOT YET BEEN APPROVED BY THE BANKRUPTCY COURT. THE FILING AND DISSEMINATION OF THIS DISCLOSURE STATEMENT SHOULD NOT BE CONSTRUED AS A SOLICITATION OF ACCEPTANCES OF THE PLAN, NOR SHOULD THE INFORMATION CONTAINED HEREIN BE RELIED UPON FOR ANY OTHER PURPOSE UNTIL THIS DISCLOSURE STATEMENT HAS BEEN APPROVED BY THE BANKRUPTCY COURT PURSUANT TO SECTION 1125 OF THE BANKRUPTCY CODE.

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK

REORGANIZATION UNDER CHAPTER 11 OF THE BANKRUPTCY CODE

DAVIS POLK & WARDWELL 450 Lexington Avenue New York, New York 10017 Telephone: (212) 450-4000 Fax: (212) 450-6539 John Fouhey (JF 9006) Marshall S. Huebner (MH 7800) Benjamin S. Kaminetzky (BK 7741) Timothy Graulich (TG 0046) Damian S. Schaible (DS 7427) Attorneys for Debtors

and Debtors in Possession

Dated: December 19, 2006

THIS DISCLOSURE STATEMENT CONTAINS A SUMMARY OF CERTAIN

PROVISIONS OF THE DEBTORS

PLAN OF REORGANIZATION AND CERTAIN OTHER

DOCUMENTS AND FINANCIAL INFORMATION. THE INFORMATION INCLUDED HEREIN IS FOR PURPOSES OF SOLICITING ACCEPTANCES OF THE PLAN AND SHOULD NOT BE RELIED UPON FOR ANY PURPOSE OTHER THAN TO DETERMINE HOW AND WHETHER TO VOTE ON THE PLAN. THE DEBTORS BELIEVE THAT THESE SUMMARIES ARE FAIR AND ACCURATE. THE SUMMARIES OF THE FINANCIAL INFORMATION AND THE DOCUMENTS THAT ARE ATTACHED HERETO OR INCORPORATED BY REFERENCE HEREIN ARE QUALIFIED IN THEIR ENTIRETY BY REFERENCE TO SUCH INFORMATION AND DOCUMENTS. IN THE EVENT OF ANY INCONSISTENCY OR DISCREPANCY BETWEEN A DESCRIPTION IN THIS DISCLOSURE STATEMENT AND THE TERMS AND PROVISIONS OF THE PLAN OR THE OTHER DOCUMENTS AND FINANCIAL INFORMATION INCORPORATED HEREIN BY REFERENCE, THE PLAN OR THE OTHER DOCUMENTS AND FINANCIAL INFORMATION, AS THE CASE MAY BE, SHALL GOVERN FOR ALL PURPOSES.

THE STATEMENTS AND FINANCIAL INFORMATION CONTAINED HEREIN HAVE BEEN MADE AS OF THE DATE HEREOF UNLESS OTHERWISE SPECIFIED. HOLDERS OF CLAIMS AND INTERESTS REVIEWING THIS DISCLOSURE STATEMENT SHOULD NOT INFER AT THE TIME OF SUCH REVIEW THAT THERE HAVE BEEN NO CHANGES IN THE FACTS SET FORTH HEREIN SINCE THE DATE HEREOF. EACH HOLDER OF A CLAIM OR INTEREST ENTITLED TO VOTE ON THE PLAN SHOULD CAREFULLY REVIEW THE PLAN AND THIS DISCLOSURE STATEMENT IN THEIR ENTIRETY BEFORE CASTING A BALLOT. THIS DISCLOSURE STATEMENT DOES NOT CONSTITUTE LEGAL, BUSINESS, FINANCIAL OR TAX ADVICE. ANY PERSONS DESIRING ANY SUCH ADVICE OR OTHER ADVICE SHOULD CONSULT WITH THEIR OWN ADVISORS.

ALTHOUGH THE DEBTORS HAVE ATTEMPTED TO ENSURE THE ACCURACY OF THE FINANCIAL INFORMATION PROVIDED IN THIS DISCLOSURE STATEMENT, EXCEPT WHERE SPECIFICALLY NOTED, THE FINANCIAL INFORMATION CONTAINED IN OR INCORPORATED BY REFERENCE INTO THIS DISCLOSURE STATEMENT HAS NOT BEEN AUDITED.

THE FINANCIAL PROJECTIONS PROVIDED IN THIS DISCLOSURE STATEMENT HAVE BEEN PREPARED BY THE MANAGEMENT OF THE DEBTORS AND THEIR FINANCIAL ADVISORS. THESE FINANCIAL PROJECTIONS, WHILE PRESENTED WITH NUMERICAL SPECIFICITY, ARE NECESSARILY BASED ON A VARIETY OF ESTIMATES AND ASSUMPTIONS THAT, ALTHOUGH CONSIDERED REASONABLE BY MANAGEMENT, MAY NOT BE REALIZED AND ARE INHERENTLY SUBJECT TO SIGNIFICANT BUSINESS, ECONOMIC, COMPETITIVE, INDUSTRY, REGULATORY, MARKET AND FINANCIAL UNCERTAINTIES AND CONTINGENCIES, MANY OF WHICH ARE BEYOND THE DEBTORS

CONTROL. THE DEBTORS CAUTION THAT NO REPRESENTATIONS CAN BE MADE AS TO THE ACCURACY OF THESE FINANCIAL PROJECTIONS OR THE ABILITY TO ACHIEVE THE PROJECTED

ii

RESULTS. SOME ASSUMPTIONS INEVITABLY WILL NOT MATERIALIZE. FURTHER, EVENTS AND CIRCUMSTANCES OCCURRING SUBSEQUENT TO THE DATE ON WHICH THESE FINANCIAL PROJECTIONS WERE PREPARED MAY BE DIFFERENT FROM THOSE ASSUMED AND/OR MAY HAVE BEEN UNANTICIPATED, AND THUS THE OCCURRENCE OF THESE EVENTS MAY AFFECT FINANCIAL RESULTS IN A MATERIALLY ADVERSE OR MATERIALLY BENEFICIAL MANNER. THE FINANCIAL PROJECTIONS, THEREFORE, MAY NOT BE RELIED UPON AS A GUARANTEE OR OTHER ASSURANCE OF THE ACTUAL RESULTS THAT WILL OCCUR.

NO PARTY IS AUTHORIZED TO GIVE ANY INFORMATION WITH RESPECT TO THE PLAN OTHER THAN THAT WHICH IS CONTAINED IN THIS DISCLOSURE STATEMENT. NO REPRESENTATIONS CONCERNING THE DEBTORS OR THE VALUE OF THEIR PROPERTY HAVE BEEN AUTHORIZED BY THE DEBTORS OTHER THAN AS SET FORTH IN THIS DISCLOSURE STATEMENT. ANY INFORMATION, REPRESENTATIONS OR INDUCEMENTS MADE TO OBTAIN AN ACCEPTANCE OF THE PLAN OTHER THAN, OR INCONSISTENT WITH, THE INFORMATION CONTAINED HEREIN AND IN THE PLAN SHOULD NOT BE RELIED UPON BY ANY HOLDER OF A CLAIM OR INTEREST.

WITH RESPECT TO CONTESTED MATTERS, ADVERSARY PROCEEDINGS AND OTHER PENDING, THREATENED OR POTENTIAL LITIGATION OR ACTIONS, THIS DISCLOSURE STATEMENT DOES NOT CONSTITUTE AND MAY NOT BE CONSTRUED AS AN ADMISSION OF FACT, LIABILITY, STIPULATION OR WAIVER, BUT RATHER AS A STATEMENT MADE IN SETTLEMENT NEGOTIATIONS.

THE SECURITIES DESCRIBED HEREIN WILL BE ISSUED WITHOUT REGISTRATION UNDER THE UNITED STATES SECURITIES ACT OF 1933, AS AMENDED, OR ANY SIMILAR FEDERAL, STATE OR LOCAL LAW, IN RELIANCE ON THE EXEMPTIONS SET FORTH IN SECTION 1145 OF THE BANKRUPTCY CODE.

THIS DISCLOSURE STATEMENT HAS NOT BEEN APPROVED OR DISAPPROVED BY THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION, NOR HAS THE COMMISSION PASSED UPON THE ACCURACY OR ADEQUACY OF THE STATEMENTS CONTAINED HEREIN.

SEE ARTICLE 8 OF THIS DISCLOSURE STATEMENT, ENTITLED CERTAIN FACTORS TO BE CONSIDERED PRIOR TO VOTING,

FOR A DISCUSSION OF CERTAIN CONSIDERATIONS IN CONNECTION WITH A DECISION BY A HOLDER OF AN IMPAIRED CLAIM TO ACCEPT THE PLAN.

iii

SUMMARY OF THE PLAN

The following summary is qualified in its entirety by the more detailed information contained in the Plan and elsewhere in this Disclosure Statement. Capitalized terms used but not otherwise defined herein have the meanings given to such terms in the Plan; provided, however, that any capitalized term used herein that is not defined herein or in the Plan, but is defined in the Bankruptcy Code or the Bankruptcy Rules, shall have the meaning ascribed to that term in the Bankruptcy Code or the Bankruptcy Rules.

Delta Air Lines is a major air carrier that provides scheduled air transportation for passengers and cargo throughout the United States and around the world. Delta offers customers service to more destinations than any global airline, with Delta and Delta Connection carrier service to 303 destinations in 52 countries. With more than 50 new international routes added to its network since 2005, Delta is the fastest growing international airline in the United States and is a leader across the Atlantic with flights to 31 trans-Atlantic destinations. Delta offers more than 400 weekly flights to 56 destinations in Latin America and the Caribbean. Delta is a founding member of the SkyTeam international alliance ( SkyTeam ), a global airline alliance that provides customers with extensive worldwide destinations, flights and services. Including its SkyTeam and worldwide codeshare partners, Delta offers flights to 459 worldwide destinations in 97 countries.

This Disclosure Statement is being furnished by the Debtors as proponents of the Debtors

Joint Plan of Reorganization Under Chapter 11 of the Bankruptcy Code, a copy of which is attached hereto as Appendix A, pursuant to section 1125 of the Bankruptcy Code and in connection with the solicitation of votes for the acceptance or rejection of the Plan.

This Disclosure Statement describes certain aspects of the Plan, including an analysis of the treatment of holders of Claims against, and Interests in, the Debtors and the securities to be issued under the Plan, and also contains a discussion of the Debtors

history, businesses, properties and operations, projections for those operations and risk factors associated with the businesses and the Plan.

THIS DISCLOSURE STATEMENT CONTAINS A SUMMARY OF THE STRUCTURE OF, CLASSIFICATION AND TREATMENT OF CLAIMS AND INTERESTS IN, AND IMPLEMENTATION OF, THE PLAN. IT IS QUALIFIED IN ITS ENTIRETY BY REFERENCE TO THE PLAN WHICH ACCOMPANIES THIS DISCLOSURE STATEMENT AND TO THE SCHEDULES ATTACHED THERETO OR REFERRED TO THEREIN.

A. The Plan

The Plan contemplates the reorganization of the Debtors and the resolution of all outstanding Claims against and Interests in the Debtors. Subject to the specific provisions set forth in the Plan, all of the pre-petition obligations owed to holders of Unsecured Claims of any of the Debtors will, as a general matter, be converted into New Delta Common Stock to be

iv

issued by Reorganized Delta. Moreover, the holders of Old Stock or of rights or Claims arising in connection therewith will receive no distribution on account of these Claims or Interests, which will be cancelled. Administrative Claims, Priority Tax Claims, Other Priority Claims, Secured Aircraft Claims and Other Secured Claims are Unimpaired under the Plan, which means, in general, that the Plan will leave their legal, equitable and contractual rights unaltered.

The Plan is premised upon the limited and separate consolidation of (i) the Estates of the Delta Debtors with one another and (ii) the Estates of the Comair Debtors with one another, each such consolidation to be effected solely for purposes of actions associated with the Confirmation of the Plan and the occurrence of the Effective Date, including voting, Confirmation and distribution. If one or both Plan Consolidations are not approved by the Bankruptcy Court, the Claims and Interests against and in the Delta Debtors and Comair Debtors may be classified, treated and voted as specified in Section 2.4 of the Plan.

B. Treatment of Claims and Interests Under the Plan

1. Administrative and Priority Tax Claims

An Administrative Claim is a Claim for payment of an administrative expense of a kind specified in section 503(b) of the Bankruptcy Code and entitled to priority pursuant to section 507(a)(1) of the Bankruptcy Code. Administrative Claims include, but are not limited, to Amex Post-Petition Facility Claims, DIP Facility Claims, Other Administrative Claims and Professional Fee Claims.

A Priority Tax Claim is an unsecured Claim of a governmental unit entitled to priority pursuant to section 507(a)(8) of the Bankruptcy Code or specified under section 502(i) of the Bankruptcy Code.

Under the Plan, the Debtors will pay Administrative Claims in full. Priority Tax Claims will be paid in full on a deferred basis, with interest accrued from the Effective Date.

2. Other Claims and Interests

The Plan divides all other Claims against, and all Interests in, the Debtors into various Classes. The following table summarizes the classification of Claims and Interests under the Plan, the treatment of each such Class, the projected recovery under the Plan, if any, for each Class and whether or not each Class is entitled to vote. Note that the classifications and distributions set forth in the table remain subject to change, as further described in Section 17.1 of the Plan.

v

Summary of Classification and Treatment of Claims and Interests in the Delta Debtors

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

1 Other Priority Claims against the Delta Debtors

Payment in full in Cash; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

2 Secured Aircraft Claims against the Delta Debtors

Payment in full in Cash; Reinstatement of the legal, equitable and contractual rights of the holder of such Claim; payment of the proceeds of the sale or disposition of the Collateral securing such Claim to the extent of the value of the holder s secured interest in such Collateral; return of Collateral securing such Claim; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

vi

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

3 Other Secured Claims against the Delta Debtors

Payment in full in Cash; Reinstatement of the legal, equitable and contractual rights of the holder of such Claim; payment of the proceeds of the sale or disposition of the Collateral securing such Claim to the extent of the value of the holder s secured interest in such Collateral; return of Collateral securing such Claim; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

4 General Unsecured Claims against the Delta Debtors

New Delta Common Stock equal to pro rata share of Delta Unsecured Allocation. Opportunity to participate in New Equity Investment Rights Offering.

63 - 80%

Impaired Entitled to Vote

5 Non-Convenience Class Retiree Claims1 against Delta

New Delta Common Stock equal to pro rata share of Delta Unsecured Allocation; or, if elected on Ballot, Cash proceeds from sale of pro rata share of Delta Unsecured Allocation.

63 - 80%

Impaired Entitled to Vote

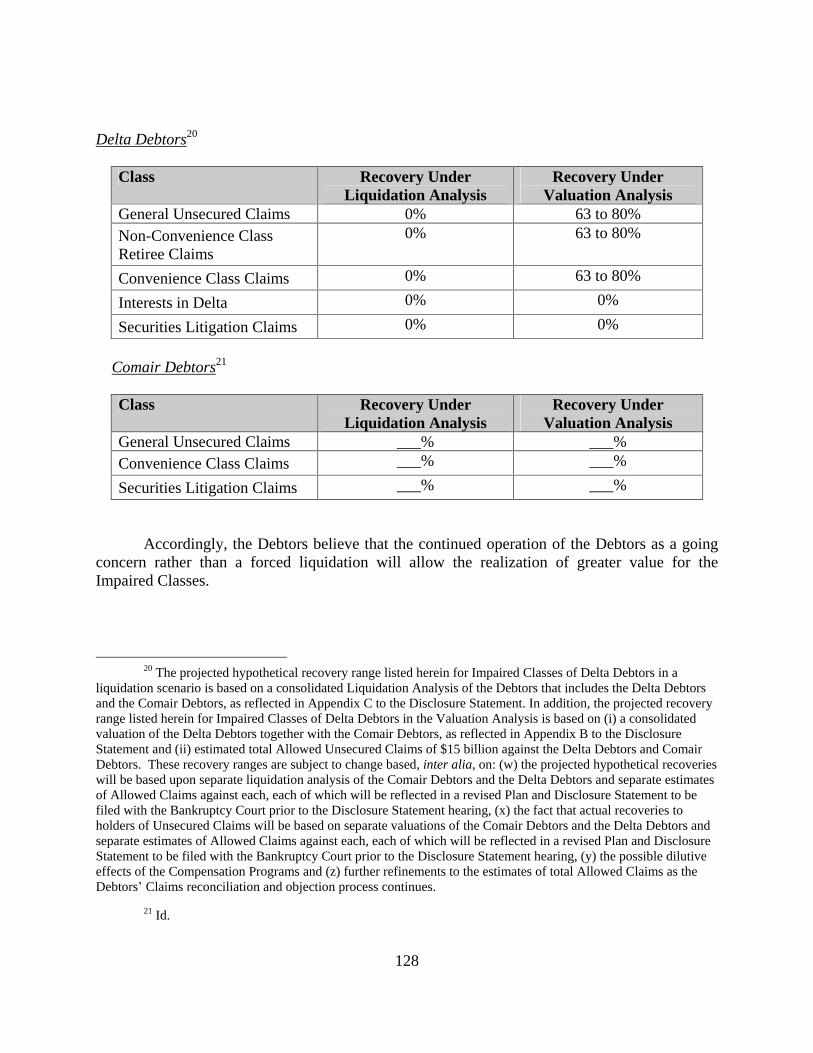

The projected recovery range listed herein for Delta Class 4, Delta Class 5 and Delta Class 6 is based on (i) a consolidated valuation of the Delta Debtors together with the Comair Debtors, as reflected in Appendix B to the Disclosure Statement and (ii) estimated total Allowed Unsecured Claims of $15 billion against the Delta Debtors and Comair Debtors. This recovery range is subject to change based, inter alia, on: (x) the fact that actual recoveries to holders of Unsecured Claims will be based on separate valuations of the Comair Debtors and the Delta Debtors and separate estimates of Allowed Claims against each, each of which will be reflected in a revised Plan and Disclosure Statement to be filed with the Bankruptcy Court prior to the Disclosure Statement hearing, (y) the possible dilutive effects of the Compensation Programs and (z) further refinements to the estimates of total Allowed Claims as the Debtors Claims reconciliation and objection process continues.

1 A Non-Convenience Class Retiree Claim is a Claim against Delta in an amount that is greater than $2,000 but less than or equal to $100,000 arising from (i) the modification of retiree health or welfare benefits as ( continued)

vii

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

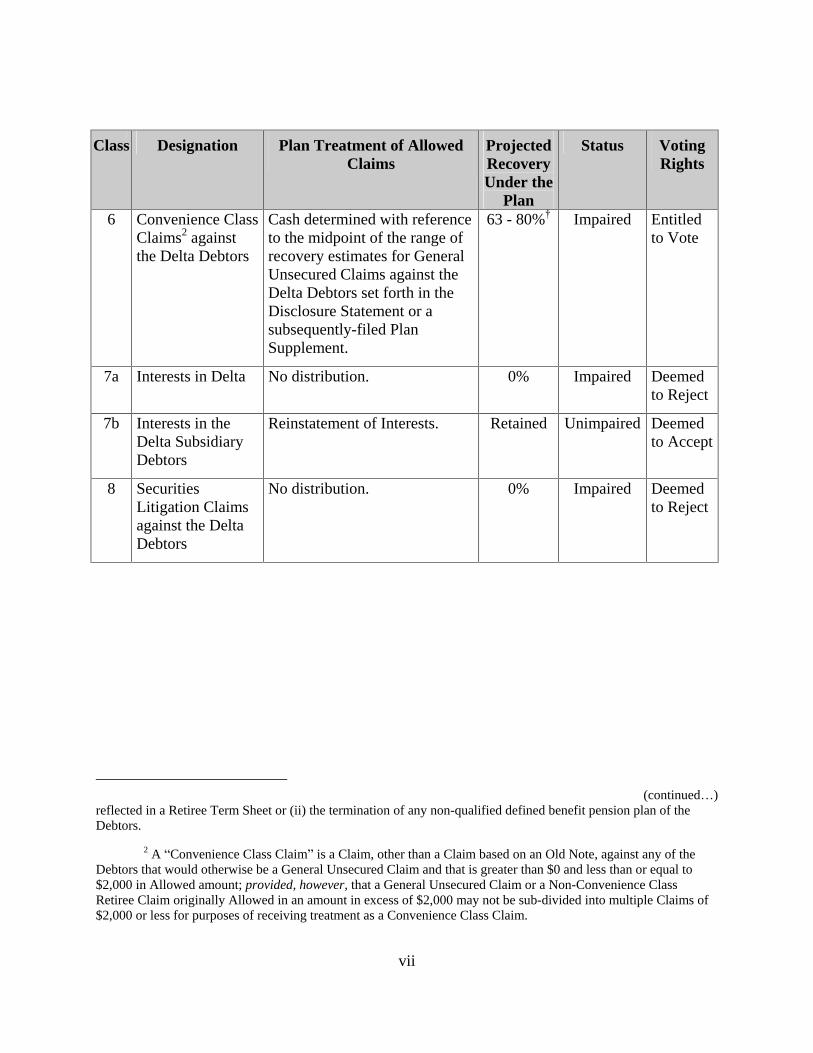

6 Convenience Class Claims2 against the Delta Debtors

Cash determined with reference to the midpoint of the range of recovery estimates for General Unsecured Claims against the Delta Debtors set forth in the Disclosure Statement or a subsequently-filed Plan Supplement.

63 - 80%

Impaired Entitled

to Vote

7a Interests in Delta No distribution. 0% Impaired Deemed to Reject

7b Interests in the Delta Subsidiary Debtors

Reinstatement of Interests. Retained Unimpaired

Deemed to Accept

8 Securities Litigation Claims against the Delta Debtors

No distribution. 0% Impaired Deemed to Reject

(continued ) reflected in a Retiree Term Sheet or (ii) the termination of any non-qualified defined benefit pension plan of the Debtors.

2 A Convenience Class Claim is a Claim, other than a Claim based on an Old Note, against any of the Debtors that would otherwise be a General Unsecured Claim and that is greater than $0 and less than or equal to $2,000 in Allowed amount; provided, however, that a General Unsecured Claim or a Non-Convenience Class Retiree Claim originally Allowed in an amount in excess of $2,000 may not be sub-divided into multiple Claims of $2,000 or less for purposes of receiving treatment as a Convenience Class Claim.

viii

Summary of Classification and Treatment of Claims and Interests in the Comair Debtors

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

1 Other Priority Claims against the Comair Debtors

Payment in full in Cash; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

2 Secured Aircraft Claims against the Comair Debtors

Payment in full in Cash; Reinstatement of the legal, equitable and contractual rights of the holder of such Claim; payment of the proceeds of the sale or disposition of the Collateral securing such Claim to the extent of the value of the holder s secured interest in such Collateral; return of Collateral securing such Claim; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

ix

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

3 Other Secured Claims against the Comair Debtors

Payment in full in Cash; Reinstatement of the legal, equitable and contractual rights of the holder of such Claim; payment of the proceeds of the sale or disposition of the Collateral securing such Claim to the extent of the value of the holder s secured interest in such Collateral; return of Collateral securing such Claim; or other treatment that will render the Claim Unimpaired.

100% Unimpaired

Deemed to Accept

4 General Unsecured Claims against the Comair Debtors

New Delta Common Stock equal to pro rata share of Comair Unsecured Allocation. Opportunity to participate in New Equity Investment Rights Offering.

__-__%

Impaired Entitled to Vote

5 Convenience Class Claims3 against the Comair Debtors

Cash determined with reference to the midpoint of the range of recovery estimates for General Unsecured Claims against the Comair Debtors set forth in the Disclosure Statement or a subsequently-filed Plan Supplement.

__-__%

Impaired Entitled to Vote

The projected recovery range for Comair Class 4 and Comair Class 5 will be included in a revised Plan and Disclosure Statement to be filed with the Bankruptcy Court prior to the Disclosure Statement hearing and will be based on a separate valuation of the Comair Debtors and a separate estimate of Allowed Claims against the Comair Debtors. The projected recovery range for holders of Unsecured Claims against the Comair Debtors may well differ substantially from (i) the projected recovery range listed above for Delta Class 4, Delta Class 5 and Delta Class 6 and/or (ii) any subsequently revised projected recovery range for Unsecured Claims against the Delta Debtors.

3 A Convenience Class Claim is a Claim, other than a Claim based on an Old Note, against any of the Debtors that would otherwise be a General Unsecured Claim and that is greater than $0 and less than or equal to $2,000 in Allowed amount; provided, however, that a General Unsecured Claim or a Non-Convenience Class ( continued)

x

Class

Designation Plan Treatment of Allowed

Claims Projected Recovery Under the

Plan

Status Voting Rights

6 Interests in the Comair Debtors

Reinstatement of Interests. Retained Unimpaired

Deemed to Accept

7 Securities Litigation Claims against the Comair Debtors

No distribution. 0% Impaired Deemed to Reject

In accordance with and giving effect to the provisions of section 1124(1) of the Bankruptcy Code, Intercompany Claims are Unimpaired by the Plan. However, the Debtors, in their sole discretion, retain the right to eliminate or adjust any Intercompany Claims as of the Effective Date by offset, cancellation, distribution or contribution of Claims or otherwise.

C. Claims Estimates

The projected recoveries set forth in the Plan are based on certain assumptions, including the Debtors

estimates of the Claims that will eventually be Allowed in various Classes. The following table sets forth information on Claims filed in the Debtors

cases, Claims disallowed to date and Claims that the Debtors estimate will eventually be Allowed. There is no guarantee that the ultimate amount of each of such categories of Claims will conform to the estimates set forth below.

(continued ) Retiree Claim originally Allowed in an amount in excess of $2,000 may not be sub-divided into multiple Claims of $2,000 or less for purposes of receiving treatment as a Convenience Class Claim.

xi

Class

Designation Claims Filed /

Scheduled Claims

Disallowed (to Date)4

Total Allowed Claims

(estimate)5

Other Administrative Claims against the Debtors

$236,129,152 $59,330,378 $___

Priority Tax Claims against the Debtors6

$57,675,400,206 $39,521,556 $___

The Delta Debtors

1 Other Priority Claims against the Delta Debtors

$610,190,819 $219,527,421 $___

2 Secured Aircraft Claims against the Delta Debtors

$5,799,700,055 0 $___

3 Other Secured Claims against the Delta Debtors

$6,691,794,709 $117,318,863 $___

4 The general bar date for filing Claims was August 21, 2006, at which time the Debtors began the process of analyzing and reconciling the filed Claims. The Debtors believe that many of the Claims filed in the Chapter 11 Cases are invalid, untimely, duplicative and/or overstated, and are in the process of objecting to such Claims. The amounts in this column represent the amounts the Bankruptcy Court has disallowed to date in each of the various Classes. In addition to these amounts, Delta has filed additional omnibus objections to disallow or reduce Claims by an additional aggregate amount of approximately $264 million, which objections are pending before the Bankruptcy Court. Because the process of analyzing and objecting to Claims is ongoing and is only at the beginning stages, the amount of Disallowed Claims may increase significantly in the future.

5 The Debtors currently estimate that at the conclusion of the Claims objection, reconciliation and resolution process, the aggregate amount of Allowed Claims in each class will be approximately as indicated in this column.

The Debtors estimates of the Claims that will eventually be Allowed against the Delta Debtors and against the Comair Debtors will be included in a revised Plan and Disclosure Statement to be filed with the Bankruptcy Court prior to the Disclosure Statement hearing.

6 As discussed in more detail in footnote 16, supra, the filed Priority Tax Claims include approximately $57.5 billion of Claims filed by the IRS, of which approximately $27.6 billion are duplicate claims. The Debtors are in discussion with the IRS to settle these open periods and expect that the actual amounts owed, if any, will be substantially less than the average and aggregate value of the filed Claims.

xii

Class

Designation Claims Filed /

Scheduled Claims

Disallowed (to Date)4

Total Allowed Claims

(estimate)5

4-6 Unsecured Claims against the Delta Debtors

$13,027,064,164 $281,045,333 $___

The Comair Debtors

1 Other Priority Claims against the Comair Debtors

$194,689,137 0 $___

2 Secured Aircraft Claims against the Comair Debtors

$1,145,829,751 0 $___

3 Other Secured Claims against the Comair Debtors

$31,699,276 $62,834 $___

4-5 Total Unsecured Claims against the Comair Debtors7

$1,379,608,133 $32,153,039 $___

D. Recommendation

After careful review of their current business operations, their prospects as ongoing business enterprises and the estimated recoveries of Creditors in various liquidation scenarios, the Debtors have concluded that the recovery of holders of Allowed Claims will be maximized by the Debtors

continued operation as a going concern. The Debtors believe that their businesses and assets have significant value that would not be realized in a liquidation scenario, either in whole or in substantial part, and that the value of the Debtors

Estates is considerably greater as a going concern than if they were liquidated. See Article 6 herein, Statutory Requirements for Confirmation of the Plan.

The Debtors believe that the Plan provides the best recoveries possible for the Debtors

Creditors and strongly recommend that, if you are entitled to vote, you vote to accept the Plan. The Debtors also believe that any alternative to Confirmation of the Plan, such as liquidation,

7 Holders of Unsecured Claims against the Comair Debtors will receive the New Delta Common Stock that Reorganized Delta will issue to such holders pursuant to Section 4.3 of the Plan. In exchange, the Interests in the Comair Debtors will be Reinstated for the ultimate benefit of Reorganized Delta.

xiii

partial sale of assets or any attempt by another party in interest to file a plan, would result in lower recoveries for stakeholders, as well as significant delays, litigation and costs.

THE DEBTORS BELIEVE THAT THE PLAN PROVIDES THE BEST RECOVERIES POSSIBLE FOR THE HOLDERS OF CLAIMS AGAINST EACH OF THE DEBTORS AND THUS RECOMMEND THAT YOU VOTE TO ACCEPT

THE PLAN.

PLAN VOTING INSTRUCTIONS AND PROCEDURES

A. Notice to Holders of Claims

This Disclosure Statement is being transmitted to certain Creditors for the purpose of soliciting votes on the Plan and to others for informational purposes. The purpose of this Disclosure Statement is to provide adequate information to enable holders of Claims that are entitled to vote on the Plan to make a reasonably informed decision with respect to the Plan prior to exercising their right to vote to accept or reject the Plan.

By the Approval Order entered on ______________, the Bankruptcy Court approved this Disclosure Statement as containing information of a kind and in sufficient and adequate detail to enable holders of Claims that are entitled to vote on the Plan to make an informed judgment with respect to acceptance or rejection of the Plan. THE BANKRUPTCY COURT S APPROVAL OF THIS DISCLOSURE STATEMENT DOES NOT CONSTITUTE EITHER A GUARANTEE OF THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED HEREIN OR AN ENDORSEMENT OF THE PLAN BY THE BANKRUPTCY COURT.

ALL HOLDERS OF CLAIMS ARE ENCOURAGED TO READ THIS DISCLOSURE STATEMENT, ITS APPENDICES AND ALL PLAN SUPPLEMENTS FILED PRIOR TO THE VOTING DEADLINE CAREFULLY AND IN THEIR ENTIRETY BEFORE DECIDING TO VOTE EITHER TO ACCEPT OR TO REJECT THE PLAN. This Disclosure Statement contains important information about the Plan, considerations pertinent to acceptance or rejection of the Plan and developments concerning the Chapter 11 Cases.

THIS DISCLOSURE STATEMENT AND THE OTHER MATERIALS INCLUDED IN THE SOLICITATION PACKAGE ARE THE ONLY DOCUMENTS AUTHORIZED BY THE BANKRUPTCY COURT TO BE USED IN CONNECTION WITH THE SOLICITATION OF VOTES ON THE PLAN. No solicitation of votes may be made except after distribution of this Disclosure Statement.

CERTAIN OF THE INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT IS BY ITS NATURE FORWARD-LOOKING AND CONTAINS ESTIMATES, ASSUMPTIONS AND PROJECTIONS THAT MAY BE MATERIALLY DIFFERENT FROM ACTUAL, FUTURE RESULTS. This Disclosure Statement contains projections of future performance as set forth in Appendix D attached hereto. Other events may occur subsequent to the date hereof that may have a material impact on the information contained in this Disclosure

xiv

Statement. Except as expressly stated, neither the Debtors nor the Reorganized Debtors intend to update the Financial Projections for the purposes hereof. Thus, the Financial Projections will not reflect the impact of any subsequent events not already accounted for in the assumptions underlying the Financial Projections. Further, the Debtors do not anticipate that any amendments or supplements to this Disclosure Statement will be distributed to reflect such occurrences. Accordingly, the delivery of this Disclosure Statement does not imply that the information herein is correct or complete as of any time subsequent to the date hereof.

EXCEPT WHERE SPECIFICALLY NOTED, THE FINANCIAL INFORMATION CONTAINED HEREIN HAS NOT BEEN AUDITED BY A CERTIFIED PUBLIC ACCOUNTANT AND HAS NOT BEEN PREPARED IN ACCORDANCE WITH GENERALLY ACCEPTED ACCOUNTING PRINCIPLES.

B. Who is Entitled to Vote on the Plan?

In general, a holder of a Claim or Interest may vote to accept or reject a plan of reorganization if (i) no party in interest has objected to such Claim or Interest (or the Claim or Interest has been Allowed subsequent to any objection or estimated for voting purposes), (ii) the Claim or Interest is Impaired by the plan and (iii) the holder of such Claim or Interest will receive or retain property under the plan on account of such Claim or Interest. The holders of Claims in the following Classes are entitled to vote on the Plan:

Delta and Comair Class 4 (General Unsecured Claims)

Delta Class 5 (Non-Convenience Class Retiree Claims against Delta)

Delta Class 6 and Comair Class 5 (Convenience Class Claims)

In general, if a Claim or Interest is Unimpaired under a plan, section 1126(f) of the Bankruptcy Code deems the holder of such Claim or Interest to have accepted the plan and thus the holders of Claims in such Unimpaired Classes are not entitled to vote on the plan. Because the following Classes are Unimpaired under the Plan, the holders of Claims in these Classes are not entitled to vote:

Delta and Comair Class 1 (Other Priority Claims)

Delta and Comair Class 2 (Secured Aircraft Claims)

Delta and Comair Class 3 (Other Secured Claims)

Delta Class 7b (Interests in the Delta Subsidiary Debtors)

Comair Class 6 (Interests in the Comair Debtors)

In general, if the holder of an Impaired Claim or Impaired Interest will not receive any distribution under a plan in respect of such Claim or Interest, section 1126(g) of the Bankruptcy Code deems the holder of such Claim or Interest to have rejected the plan, and thus the holders of Claims in such Classes are not entitled to vote on the plan. The holders of Claims and Interests in the following Classes are conclusively presumed to have rejected the Plan and are therefore not entitled to vote:

xv

Delta Class 7a (Interests in Delta)

Delta Class 8 and Comair Class 7 (Securities Litigation Claims)

C. General Voting Procedures and the Voting Deadline

On _______________, the Bankruptcy Court entered the Approval Order, which, among other things, approved this Disclosure Statement, set voting procedures and scheduled the hearing on Confirmation of the Plan. A copy of the Confirmation Hearing Notice is enclosed with this Disclosure Statement. The Confirmation Hearing Notice sets forth in detail, among other things, the voting deadlines and objection deadlines with respect to the Plan. The Confirmation Hearing Notice and the instructions attached to the Ballot should be read in connection with this Section of this Disclosure Statement.

If you are entitled to vote, after carefully reviewing the Plan, this Disclosure Statement and the detailed instructions accompanying your Ballot(s), please indicate your acceptance or rejection of the Plan by checking the appropriate box on the enclosed Ballot(s). Please complete and sign your original Ballot(s) (copies with non-original signatures will not be accepted) and return it/them in the envelope provided. You must provide all of the information requested by the appropriate Ballot(s). Failure to do so may result in the disqualification of your vote on such Ballot(s).

Each Ballot has been coded to reflect the Class of Claims it represents. Accordingly, in voting to accept or reject the Plan, you must use only the coded Ballot(s) sent to you with this Disclosure Statement.

The Debtors have retained Bankruptcy Services, LLC as their Solicitation Agent to assist in the voting process. If you have any questions concerning the procedure for voting your Claim, the packet of materials that you have received or the amount of your Claim, or if you wish to obtain (at no charge) a hard copy of the Plan, this Disclosure Statement or any appendices or exhibits to such documents, please contact Bankruptcy Services, LLC at (310) 838-8020 or (866) 686-8702 (toll free).

IN ORDER FOR YOUR VOTE TO BE COUNTED, YOUR BALLOT MUST BE PROPERLY COMPLETED AS SET FORTH ABOVE AND IN ACCORDANCE WITH THE VOTING INSTRUCTIONS ON THE BALLOT AND ACTUALLY RECEIVED

NO LATER THAN ___________ AT ____ P.M. (PREVAILING EASTERN TIME) (THE VOTING DEADLINE ) BY THE SOLICITATION AGENT, AS FOLLOWS:

xvi

If by U.S. Mail:

If by courier/hand delivery:

Delta Air Lines, Inc. Ballot Processing Grand Central Station P.O. Box 5295 New York, NY 10163-5014

Delta Air Lines, Inc. Ballot Processing Bankruptcy Services LLC/Financial Balloting Group 757 Third Avenue, 3rd floor New York, NY 10017

BALLOTS RECEIVED AFTER THE VOTING DEADLINE WILL NOT BE COUNTED. BALLOTS SHOULD NOT BE DELIVERED DIRECTLY TO THE DEBTORS, THE BANKRUPTCY COURT, THE CREDITORS

COMMITTEE, COUNSEL TO THE DEBTORS OR THE CREDITORS

COMMITTEE OR ANYONE OTHER THAN BANKRUPTCY SERVICES, LLC.

D. Confirmation Hearing and Deadline for Objections to Confirmation

Pursuant to section 1128 of the Bankruptcy Code and Bankruptcy Rule 3017(c), the Bankruptcy Court has scheduled the Confirmation Hearing for ________________, at ____ _.m. (prevailing Eastern time) before the Honorable Adlai S. Hardin, Jr., United States Bankruptcy Judge, at the United States Bankruptcy Court for the Southern District of New York, [300 Quarropas Street, White Plains, New York 10601]. The Confirmation Hearing may be adjourned from time to time by the Bankruptcy Court without further notice except for a notice filed on the Bankruptcy Court s docket and/or an announcement of the adjournment date made at the Confirmation Hearing or at any subsequently adjourned Confirmation Hearing.

The Bankruptcy Court has directed that objections to Confirmation and proposed modifications to the Plan, if any, must (i) be in writing, (ii) conform to the Bankruptcy Rules, (iii) state the name and address of the objecting party and the amount and nature of the Claim or Interest of such party, (iv) state with particularity the basis and nature of any objection to the Plan and (v) be filed, together with proof of service, with the Court in accordance with the Court s Case Management Order and served so as to be actually RECEIVED on or before 4:00 p.m. (prevailing Eastern time) on _______, 2007 by:

1. The United States Bankruptcy Court for the Southern District of New York, 300 Quarropas Street, White Plains, NY 10601-4140, Attn: The Honorable Adlai S. Hardin, Jr.;

2. Attorneys for the Debtors, Davis Polk & Wardwell, 450 Lexington Avenue, New York, NY 10017, Attn: Marshall S. Huebner, Esq.;

3. Conflicts counsel to the Debtors, Stroock & Stroock & Lavan LLP, 180 Maiden Lane, New York, NY 10038, Attn: Lawrence M. Handelsman, Esq.;

4. Aircraft counsel to the Debtors, Debevoise & Plimpton LLP, 919 Third Avenue, New York, NY 10022, Attn: Richard F. Hahn, Esq.;

xvii

5. The Office of the United States Trustee for the Southern District of New York, 33 Whitehall Street, Suite 2100, New York, NY 10004, Attn: Greg M. Zipes, Esq.;

Madison Avenue, New York, NY 10022, Attn: Daniel H. Golden, Esq., Lisa G. Beckerman, Esq. and David H. Botter, Esq.;

7. The Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549, Attn: Michael A. Berman;

8. The Securities and Exchange Commission, 3 World Financial Center, New York, NY 10281, Attn: Nathan Fuchs;

9. The Internal Revenue Service, 290 Broadway, New York, NY 10008, Attn: Sid Brown;

10. Bankruptcy Services LLC, 757 Third Avenue, New York, NY 10017, Attn: Robert Saraceni; and

11. Each of the Non-ECF Service Parties (as defined in the Case Management Order), a list of which is available on the Debtors

case information website - www.deltadocket.com.

xviii

TABLE OF CONTENTS

Page

ARTICLE 1

INTRODUCTION

ARTICLE 2 THE REORGANIZED DEBTORS

Section 2.1 Overview of Business.............................................................................................. 2 Section 2.2 Management and Employee Matters....................................................................... 7 Section 2.3 Emergence Corporate Structure .............................................................................. 9 Section 2.4 Reorganized Capital Structure .............................................................................. 10 Section 2.5 Additional Information and Historical Financials................................................. 12

ARTICLE 3 THE DEBTORS AND EVENTS LEADING UP TO THE CHAPTER 11 CASES

Section 3.1 The Debtors ........................................................................................................... 12 Section 3.2 Pre-Petition Capital Structure of the Debtors........................................................ 14 Section 3.3 Events Leading up to the Chapter 11 Cases.......................................................... 17

ARTICLE 4 THE CHAPTER 11 CASES AND CERTAIN SIGNIFICANT EVENTS AND INITIATIVES

Section 4.1 Overview of Chapter 11 ........................................................................................ 22 Section 4.2 Restructuring Overview ........................................................................................ 22 Section 4.3 Certain Significant Events and Initiatives During the Chapter 11 Cases.............. 25 Section 4.4 US Airways Proposal ............................................................................................ 54

ARTICLE 5 SUMMARY OF THE PLAN OF REORGANIZATION

Section 5.1 Overview of the Plan of Reorganization ............................................................... 59 Section 5.2 Structure of the Plan.............................................................................................. 60 Section 5.3 Classification and Treatment of Claims and Interests........................................... 62 Section 5.4 Implementation of the Plan ................................................................................... 73 Section 5.5 Provisions Governing Distributions ...................................................................... 77 Section 5.6 Filing of Administrative Claims............................................................................ 83 Section 5.7 Disputed Claims .................................................................................................... 84 Section 5.8 Executory Contracts and Unexpired Leases.......................................................... 88 Section 5.9 The Rights Offering .............................................................................................. 96 Section 5.10 Provisions Regarding Corporate Governance of the Reorganized Debtors........ 102

xix

Section 5.11 Effect of Confirmation ........................................................................................ 104 Section 5.12 Conditions Precedent to Confirmation and Effectiveness of the Plan ................ 109 Section 5.13 Modification, Revocation or Withdrawal of the Plan ......................................... 110 Section 5.14 Retention of Jurisdiction by the Bankruptcy Court............................................. 111 Section 5.15 Miscellaneous...................................................................................................... 113

ARTICLE 6 STATUTORY REQUIREMENTS FOR CONFIRMATION OF THE PLAN

Section 6.1 The Confirmation Hearing .................................................................................. 121 Section 6.2 Confirmation Standards ...................................................................................... 122 Section 6.3 Best Interests Test ............................................................................................... 124 Section 6.4 Financial Feasibility ............................................................................................ 129 Section 6.5 Acceptance By Impaired Classes ........................................................................ 130 Section 6.6 Confirmation Without Acceptance By All Impaired Classes ............................. 130

ARTICLE 7 VOTING PROCEDURES

Section 7.1 Who is Entitled to Vote on the Plan? .................................................................. 133 Section 7.2 Solicitation Packages for Voting Classes............................................................ 134 Section 7.3 Solicitation and Solicitation Packages for Non-Voting Classes ......................... 134 Section 7.4 Voting Procedures ............................................................................................... 135 Section 7.5 Releases Under the Plan...................................................................................... 136

ARTICLE 8 CERTAIN FACTORS TO BE CONSIDERED PRIOR TO VOTING

Section 8.1 Certain Bankruptcy Considerations .................................................................... 136 Section 8.2 Factors Affecting the Value of the Securities to be Issued Under the Plan ........ 138 Section 8.3 Risks Relating to the Debtors Business and Financial Condition...................... 143

ARTICLE 9 CERTAIN FEDERAL INCOME TAX CONSEQUENCES

Section 9.1 Certain Federal Income Tax Consequences to the Holders of Claims and Interests ............................................................................................................... 151

Section 9.2 Certain U.S. Federal Income Tax Consequences to Reorganized Debtors......... 156 Section 9.3 Treatment of the Disputed Claims Reserves ....................................................... 160

ARTICLE 10 RECOMMENDATION

xx

Appendices

Appendix A Debtors

Joint Plan of Reorganization Under Chapter 11 of the Bankruptcy Code

Appendix B Valuation Analysis Appendix C Liquidation Analysis Appendix D Financial Projections Appendix E Rights Offering (to be filed separately)

ARTICLE 1

INTRODUCTION

Delta Air Lines, Inc., ASA Holdings, Inc., Comair Holdings, LLC, Comair, Inc., Comair Services, Inc., Crown Rooms, Inc., DAL Aircraft Trading, Inc., DAL Global Services, LLC, DAL Moscow, Inc., Delta AirElite Business Jets, Inc., Delta Benefits Management, Inc., Delta Connection Academy, Inc., Delta Corporate Identity, Inc., Delta Loyalty Management Services, LLC, Delta Technology, LLC, Delta Ventures III, LLC, Epsilon Trading, LLC, Kappa Capital Management, Inc. and Song, LLC submit this Disclosure Statement pursuant to section 1125 of the Bankruptcy Code for use in the solicitation of votes on the Plan, which is attached as Appendix A hereto.

This Disclosure Statement sets forth certain information regarding the Debtors

pre-petition history, significant events that have occurred during the Chapter 11 Cases and the reorganization and anticipated post-reorganization operations and financing of the Reorganized Debtors. This Disclosure Statement also describes the terms and provisions of the Plan, including certain alternatives to the Plan, certain effects of Confirmation of the Plan, certain risk factors associated with the securities to be issued under the Plan and the manner in which distributions will be made under the Plan. In addition, this Disclosure Statement discusses the Confirmation process and the voting procedures that holders of Claims eligible to vote must follow for their votes to be counted.

FOR A SUMMARY OF THE PLAN, PLEASE SEE ARTICLE 5 HEREOF. FOR A DISCUSSION OF CERTAIN FACTORS TO BE CONSIDERED PRIOR TO VOTING, PLEASE SEE ARTICLE 8 HEREOF.

THIS DISCLOSURE STATEMENT CONTAINS SUMMARIES OF CERTAIN PROVISIONS OF THE PLAN, CERTAIN STATUTORY PROVISIONS, CERTAIN DOCUMENTS RELATED TO THE PLAN, CERTAIN EVENTS IN THE DEBTORS

CHAPTER 11 CASES AND CERTAIN FINANCIAL INFORMATION. ALTHOUGH THE DEBTORS BELIEVE THAT SUCH SUMMARIES ARE FAIR AND ACCURATE, SUCH SUMMARIES ARE QUALIFIED IN THEIR ENTIRETY TO THE EXTENT THAT THEY DO NOT SET FORTH THE ENTIRE TEXT OF SUCH DOCUMENTS OR STATUTORY PROVISIONS. FACTUAL INFORMATION CONTAINED IN THIS DISCLOSURE STATEMENT HAS BEEN PROVIDED BY THE DEBTORS

MANAGEMENT EXCEPT WHERE OTHERWISE SPECIFICALLY NOTED. THE DEBTORS DO NOT WARRANT OR REPRESENT THAT THE INFORMATION CONTAINED HEREIN, INCLUDING THE FINANCIAL INFORMATION, IS WITHOUT ANY MATERIAL INACCURACY OR OMISSION.

2

ARTICLE 2 THE REORGANIZED DEBTORS

Section 2.1 Overview of Business

a. Introduction

Delta is a major air carrier that provides scheduled air transportation for passengers and cargo throughout the United States and around the world. Delta offers customers service to more destinations than any global airline, with Delta and Delta Connection carrier service to 303 destinations in 52 countries. With more than 50 new international routes added to its network since 2005, Delta is the fastest growing international airline in the United States and is a leader across the Atlantic with flights to 31 trans-Atlantic destinations. Delta offers more than 400 weekly flights to 56 destinations in Latin America and the Caribbean. Delta is a founding member of SkyTeam, a global airline alliance that provides customers with extensive worldwide destinations, flights and services. Including its SkyTeam and worldwide codeshare partners, Delta offers flights to 459 worldwide destinations in 97 countries.

b. Operations Overview

Delta s route network is centered around the hub system it operates at airports in Atlanta, Cincinnati, New York (John F. Kennedy International Airport ( JFK )) and Salt Lake City. Each of these hub operations includes Delta flights that gather and distribute traffic from markets in the geographic region surrounding the hub to domestic and international cities and to other Delta hubs. Delta s hub system also provides passengers with access to its principal international gateways in Atlanta and JFK.

As briefly discussed below, other key characteristics of Delta s route network include its alliances with foreign airlines, the Delta Connection program, the Delta Shuttle and its domestic marketing alliances, including with Continental Airlines, Inc. ( Continental ) and Northwest Airlines, Inc. ( Northwest ).

1. International Alliances

Delta has formed bilateral and multilateral marketing alliances with foreign airlines to improve its access to international markets and provide an additional revenue source to Delta. These arrangements can include codesharing, frequent flyer benefits, shared or reciprocal access to passenger lounges, joint promotions, common use of airport gates and ticket counters, ticket office co-location and other marketing agreements. These alliances often present opportunities in other areas, such as airport ground handling arrangements and aircraft maintenance insourcing.

Delta s international codesharing agreements enable it to market and sell seats to an expanded number of international destinations. Under international codesharing arrangements, Delta and a foreign carrier each publish their respective airline designator codes on a single flight

3

operation, thereby allowing Delta and the foreign carrier to offer joint service with one aircraft, rather than operating separate services with two aircraft. These arrangements typically allow Delta to sell seats on a foreign carrier s aircraft that are marketed under Delta s DL

designator

code and permit the foreign airline to sell seats on Delta s aircraft that are marketed under the foreign carrier s two-letter designator code. Delta has international codeshare arrangements in effect with Aeromexico, Air France, Alitalia, Avianca, China Airlines, China Southern, CSA Czech Airlines, El Al Israel Airlines, KLM Royal Dutch Airlines, Korean Air and Royal Air Maroc (and some affiliated carriers operating in conjunction with these airlines).

In addition to Delta s agreements with individual foreign airlines, Delta is a member of SkyTeam. The other members of SkyTeam are Aeroflot, Aeromexico, Air France, Alitalia, Continental, CSA Czech Airlines, KLM Royal Dutch Airlines, Korean Air and Northwest. SkyTeam links the route networks of the member airlines, providing opportunities for increased connecting traffic while offering enhanced customer service through mutual codesharing arrangements, reciprocal frequent flyer and lounge programs and coordinated cargo operations.

In 2002, Delta, Air France, Alitalia, CSA Czech Airlines and Korean Air received limited antitrust immunity from the U.S. Department of Transportation (the DOT ) that enables Delta and its immunized partners to offer a more integrated route network and develop common sales, marketing and discount programs for customers.

2. Delta Connection Program

The Delta Connection program ( Delta Connection ) is Delta s regional carrier service, which feeds traffic to its route system through contracts with regional air carriers that operate flights serving passengers primarily in small- and medium-sized cities. The program enables Delta to increase the number of flights it has in certain locations, to better match capacity with demand and to preserve its presence in smaller markets. The Delta Connection program operates the largest number of regional jets in the United States.

Through the Delta Connection Program, Delta has contractual arrangements with seven regional carriers to operate regional jet and, in certain cases, turbo-prop aircraft using Delta s DL

designator code. Delta s wholly-owned subsidiary, Comair, operates all of its flights under Delta s code. Atlantic Southeast Airlines, Inc. ( ASA ), which Delta sold to SkyWest Holdings, Inc. ( SkyWest ) in September 2005, continues to operate all of its flights under Delta s code. In addition, Delta has agreements with the following regional carriers that operate some of their flights using Delta s code: SkyWest Airlines, Inc. ( SkyWest Airlines ), a subsidiary of SkyWest; Chautauqua Airlines, Inc., a subsidiary of Republic Airways Holdings, Inc. ( Republic Holdings ); Shuttle America Corporation, a subsidiary of Republic Holdings; Freedom Airlines, Inc., a subsidiary of Mesa Air Group, Inc.; and American Eagle Airlines, Inc. ( Eagle ).

Delta generally pays the regional carriers, including Comair, amounts defined in their respective contract carrier agreements, which are based on a determination of the carriers

respective cost of operating those flights and other factors intended to approximate market rates

4

for those services. Each of these agreements are long-term agreements, usually with initial terms of at least ten years, that grant Delta the option to extend the initial term and provide Delta the right to terminate the agreement for convenience, in whole or in part, upon certain advance written notice to the regional carrier. Delta s arrangement with Eagle, which is limited to certain flights operated to and from the Los Angeles International Airport as well as a portion of the flights operated using Delta s code by SkyWest Airlines, are structured as revenue proration agreements. These proration agreements establish a fixed dollar or percentage division of revenues for tickets sold to passengers traveling on connecting flight itineraries.

3. Delta Shuttle

Delta operates a high frequency service targeted to northeast business travelers (the Delta Shuttle ). The Delta Shuttle provides nonstop, hourly service on business days between

New York - LaGuardia Airport ( LaGuardia ) and both Boston - Logan International Airport ( Logan ) and Washington, D.C. - Ronald Reagan National Airport ( Reagan ).

4. Domestic Alliances

Delta has entered into marketing alliances with (i) Continental and Northwest (including regional carriers affiliated with each) and (ii) Alaska Airlines and Horizon Air Industries, both of which include mutual codesharing and reciprocal frequent flyer and airport lounge access arrangements. These marketing relationships are designed to permit the carriers to retain their separate identities and route networks while increasing the number of domestic and international connecting passengers using the carriers

route networks.

c. Reorganized Delta s Business Strategy

Delta s reorganization in chapter 11 has involved a fundamental transformation of its business, rather than simply a balance sheet restructuring like many other bankruptcies. In September 2005, Delta introduced a comprehensive restructuring plan to achieve $3 billion in annual financial improvements by the end of 2007. As of September 30, 2006, Delta had achieved 85% of its $3 billion goal and had unrestricted cash and cash equivalents and short-term investments of $2.8 billion. At the same time, Delta has made great strides in customer service and product improvements, even as it has implemented the largest international expansion in its history, adding more than 50 new international routes. Customer satisfaction levels are now among the highest of the network carriers.8

As a result of its reorganization, Delta expects to emerge from bankruptcy as a strong, competitive, stand-alone airline with a truly global network. Delta expects to be the airline of choice for customers by continuing to improve the customer experience on the ground and in the

8 Additional information about the Debtors in-court restructuring can be found in Section 4.2 of this Disclosure Statement. Additional information about the Debtor s restructuring initiatives prior to the Chapter 11 Cases can be found in Section 3.3 of this Disclosure Statement.

5

air. Delta s emergence business strategy, as described in more detail below, touches all facets of Delta s operations

the destinations Delta will serve, the way Delta will serve its customers, and

the fleet Delta will operate

in order to earn customer preference and continue to improve

revenue performance. At the same time, Delta expects to remain focused on maintaining the competitive cost structure it has obtained from its reorganization in order to improve its financial position and pursue long-term stability as a stand-alone carrier.

1. Leveraging Network Strength to Provide Expanded International Service

A significant component of Delta s restructuring has been to realign and diversify Delta s network to increase Delta s international operations without expanding its aircraft fleet. Delta will continue to focus on international growth because international traffic to and from the U.S. is growing significantly faster than domestic traffic. In addition, international routes generally have greater profit potential than domestic routes. With its geographically-balanced hubs, Delta is well-positioned for international growth by capturing traffic flows from the United States to Europe and Latin America. In addition, Delta s hubs will help fuel international expansion plans to Africa and Asia.

Delta s international growth will take advantage of the strength of its domestic network, which currently offers service to 51 states and U.S. territories. Delta s full-service domestic network has been significantly strengthened by using technology to better match Delta s schedule to customer demand and reallocating its fleet within the network. For example, rather than flying the same schedule each day, Delta can offer fewer seats or flights on days such as Tuesdays and Saturdays when demand is lower. In addition to utilizing these technological tools, Delta has shifted a number of larger aircraft from domestic service to international service while continuing to serve existing domestic routes with smaller aircraft. This realignment, in coordination with the simplification of Delta s fleet, will make Delta a smaller but more formidable airline by 2007.

2. Maintaining Focus on Improving the Customer Experience

Delta is committed to continuous improvement throughout its operations in order to earn its customers

preference. First and foremost is Delta s continued focus on safety

its number one priority. Furthermore, while Delta has been actively engaged in restructuring its business, it has also renewed its focus on improving its product and customer service.

Over the next two years, Delta is upgrading its customers

onboard experience in several ways. A major component of this upgrade is introducing lie-flat business class seats to premium cabins in the international fleet, reducing the number of all-coach aircraft that Delta operates and including premium cabins in all new aircraft. In addition, Delta will provide all of its customers a superior onboard experience through investments in new, clean and bright interiors, state of the art in-flight entertainment, new and more comfortable leather seats and other enhancements.

Delta is as focused on improving the customer experience on the ground as it is in the air. Delta is improving and expanding its Crown Room Clubs, making important investments at two

6

of Delta s leading airport hubs, Atlanta and JFK, so that customers can check-in and get to their gates with minimal hassle, and improving convenience by adding more kiosks and more features to www.delta.com. In addition, Delta is implementing initiatives that are designed to improve Delta s on-time performance and its baggage handling systems.

In the midst of right-sizing its network and simplifying its fleet during its restructuring, Delta s product enhancements and customer service have already driven its customer satisfaction numbers up, barely missing the top spot in overall customer service for network airlines in J.D. Power and Associates

survey for 2006, and taking the top spot in three of Delta s focus areas: aircraft condition/cleanliness, boarding/deplaning/baggage and flight crew. Improvements are expected to continue with Delta s emergence from chapter 11. The combination of a strong route network, improved aircraft interiors and amenities and a renewed dedication to superior customer service is expected to make Delta the airline of choice for its customers.

3. Maximizing a Streamlined and Upgraded Fleet

During the Chapter 11 Cases, Delta significantly streamlined its fleet by retiring four older, less efficient fleet types: the 737-200, 737-300, 737-300G and 767-200. In addition, Delta has been able to lower aircraft costs by returning grounded aircraft and negotiating significant reductions in lease expenses on many of the remaining aircraft in its fleet. At the same time, Delta is supporting the ongoing changes to its network by bolstering its internationally-capable mainline fleet. For example, Delta is scheduled to take delivery of ten international-range 757 aircraft between July 2007 and November 2007, and has plans to acquire additional international-range 757s. Delta is awaiting Bankruptcy Court approval to amend its purchase agreements with Boeing, so that Delta will have additional international capability and flexibility in its fleet. Delta plans to pursue additional strategic improvements to its fleet by adding high-performance aircraft that will enable Delta to serve new destinations with appropriate capacity. These additions to Delta s fleet are expected to enhance Delta s ability to improve its unit revenue while minimizing the introduction of additional costs and complexity.

4. Capturing the Benefit of Competitive Cost Structure

Delta expects that its focus on increasing its international service, improving its operational performance and upgrading its fleet will have a positive effect on its unit revenue. At the same time, however, Delta recognizes that it must maintain the competitive unit cost structure that it has developed through its restructuring efforts. Through initiatives undertaken during the Chapter 11 Cases and previous productivity initiatives, Delta currently has one of the lowest mainline unit cost structures of any full service carrier. These efforts have resulted in reduced costs throughout Delta, including reductions in employment costs, retiree pension and healthcare costs, fleet costs and many other areas. In addition, Delta s network, notably the location of its hubs, provides a structural cost advantage.

7

5. Generating Cash Flow from Operations Necessary to Fund Capital Expenditures and Reduce Debt

Over an extended period following emergence from chapter 11, Delta intends to balance long-term operating growth with overall credit improvement. The Reorganized Debtors will have reduced their total debt levels to nearly 50% of pre-petition levels, with total debt levels expected to remain fairly stable at $10 billion over the next several years, despite significant reinvestment requirements during that time. Ongoing improvements to Delta s financial condition are, however, necessary for Delta to withstand industry and economic volatility and to have favorable, consistent access to capital markets. Delta s Financial Projections, which includes various assumptions described in the plan, projects that Delta will achieve this result because cash flow from operations is expected to be sufficient to allow necessary reinvestment in the business without incurring unmanageable debt.

Section 2.2 Management and Employee Matters

a. Management

The management team of Delta is comprised of highly capable professionals with substantial airline and other applicable industry experience. Information regarding the executive officers of Delta is as follows:

Name Position Gerald Grinstein Chief Executive Officer and Director

James M. Whitehurst Chief Operating Officer

Edward H. Bastian Executive Vice President and Chief Financial Officer

Michael H. Campbell Executive Vice President

Human Resources and Labor Relations

Glen W. Hauenstein Executive Vice President

Network Planning and Revenue Management

Kenneth F. Khoury Executive Vice President and General Counsel

Joseph C. Kolshak Executive Vice President

Operations

Lee A. Macenczak Executive Vice President

Sales and Customer Service

Gerald Grinstein. Age 74. Mr. Grinstein has been a Director of Delta since 1987 and the Chief Executive Officer of Delta since 2004. From 1999 to 2002, he served as the non-executive Chairman of the Board of Agilent Technologies, Inc. From 1997 to 1999, he served as the non-executive Chairman of Delta s Board of Directors. He is also the Retired Chairman of Burlington Northern Santa Fe Corporation (successor to Burlington Northern Inc.). He served as an executive officer, including Chief Executive Officer, of Burlington Northern Inc. and certain affiliated companies from 1987 to 1995. From 1985 to 1987, he served as Chief Executive Officer of Western Air Lines, Inc.

8

James M. Whitehurst. Age 39. Mr. Whitehurst has served as the Chief Operating Officer of Delta since July 2005. From 2004 to July 2005, he served as Delta s Senior Vice President and Chief Network and Planning Officer. From 2002 to 2004, he served as Senior Vice President

Finance, Treasury and Business Development of Delta. Prior to joining Delta in

2001, Mr. Whitehurst served in positions of increasing responsibility with Boston Consulting Group from 1994 to 2001, including as a Vice President and Director in 2001.

Edward H. Bastian. Age 49. Mr. Bastian has served as Executive Vice President and Chief Financial Officer of Delta since July 2005. Mr. Bastian served as Chief Financial Officer of Acuity Brands from June 2005 to July 2005. From 2000 to April 2005, he served as Delta s Senior Vice President

Finance and Controller. From 1998 to 2000, Mr. Bastian served as Vice President and Controller of Delta.

Michael H. Campbell. Age 57. Mr. Campbell has been Executive Vice President

Human Resources and Labor Relations of Delta since July 2006. From 2005 to 2006, Mr. Campbell was of counsel with the Atlanta-based law firm Ford & Harrison. From 1997 to 2005, he served as Senior Vice President, Human Resources and Labor Relations at Continental Airlines. From 1978 to 1997, Mr. Campbell was a partner at Ford & Harrison.

Glen W. Hauenstein. Age 46. Mr. Hauenstein has been Executive Vice President

Network Planning and Revenue Management of Delta since April 2006. From August 2005 to April 2006, he served as Delta s Executive Vice President and Chief of Network and Revenue Management. Mr. Hauenstein previously served as Vice General Director

Chief Commercial Officer and Chief Operating Officer of Alitalia from 2003 to 2005. He also held a variety of positions at Continental Airlines, including Senior Vice President

Network (2003), Senior Vice President

Scheduling (2001 to 2003) and Vice President

Scheduling (1998 to 2001).

Kenneth F. Khoury. Age 55. Mr. Khoury has been Executive Vice President and General Counsel of Delta since September 2006. From April 2006 to September 2006, Mr. Khoury served as Senior Vice President and General Counsel for Weyerhaeuser Company. From 1990 to December 2005, Mr. Khoury served as Vice President and Deputy General Counsel of Georgia-Pacific Corporation. From 1988 to 1990, he served as Senior Vice President and Associate General Counsel of Shearson Lehman Hutton, Inc.

Joseph C. Kolshak. Age 49. Mr. Kolshak has been the Executive Vice President

Operations of Delta since April 2006. From July 2005 to April 2006, he served as Executive Vice President and Chief of Operations of Delta. From 2004 to 2005, Mr. Kolshak served as Delta s Senior Vice President and Chief of Operations. He has also served as Senior Vice President

Operations (2002 to 2004), Vice President

Flight Operations (2001 to 2002), Director, Investor Relations (1998 to 2001), General Manager

Flight Operations (1996 to 1998), Flight Operations Manager and Assistant Chief Pilot (1994 to 1996), Flight Operations Coordinator

Atlanta (1993 to 1994) and Special Assignment Supervisor to the Vice President of Flight Operations (1991 to 1993). Additionally, Mr. Kolshak is a 757/767/777 Captain.

9

Lee A. Macenczak. Age 45. Mr. Macenczak has been the Executive Vice President of Sales and Customer Service of Delta since April 2006. He has served in a variety of positions at Delta, including Executive Vice President and Chief Customer Service Officer (July 2005 to April 2006), Senior Vice President and Chief Customer Service Officer (2004 to 2005), Senior Vice President and Chief Human Resources Officer (June 2004 to October 2004), Senior Vice President

Sales and Distribution (2000 to 2004), Vice President

Customer Service (1999 to 2000), Vice President

Reservation Sales (1998 to 1999) and Vice President

Reservation Sales and Distribution Planning (1996 to 1998).

b. Employee Matters

Collective Bargaining

As of September 30, 2006, the Debtors had a total of approximately 55,700 full-time equivalent employees. Approximately 17% of these employees are represented by unions. The following table presents certain information concerning the union representation of the Debtors

domestic employees.

Employee Group

Approximate Number of Employees Represented Union

Date on which Collective Bargaining Agreement Becomes Amendable

Delta Pilots 5,390 ALPA December 31, 2009 Delta Flight Superintendents 170 PAFCA January 1, 2010 Comair Pilots 1,810 ALPA May 21, 2007 Comair Maintenance Employees 550 IAM May 31, 2009 Comair Flight Attendants 1,080 IBT July 19, 2008

Labor unions periodically engage in organizing efforts, seeking to represent various groups of employees of the Debtors that are not represented for collective bargaining purposes. The timing and outcome of these organizing efforts cannot presently be determined.

Section 2.3 Emergence Corporate Structure

Pursuant to Section 6.2 of the Plan, on or after the Effective Date, the Reorganized Debtors may engage in or continue to enter into Roll-Up Transactions and may take such actions as may be necessary or appropriate to effect further corporate restructurings of their respective businesses, including actions necessary to simplify, reorganize and rationalize the overall reorganized corporate structure of the Reorganized Debtors. Implementation of the Roll-Up Transactions shall not affect any distributions, discharges, exculpations, releases or injunctions set forth in the Plan.

The Debtors will describe any Roll-Up Transactions that they intend to undertake in a Plan Supplement to be filed at a later date. If no such Roll-Up Transactions were undertaken, the corporate structure of the Reorganized Debtors would be as depicted in Section 3.1 of this Disclosure Statement.

10

Section 2.4 Reorganized Capital Structure

Pursuant to the Plan, the Reorganized Debtors expect to have the capital structure described below upon their emergence from chapter 11.

a. Delta Equity Ownership

1. New Delta Common Stock

(i) Distribution of New Delta Common Stock

Reorganized Delta expects to have 1,500,000,000 authorized shares of common stock, $0.0001 par value. In connection with the Plan, Reorganized Delta will issue up to an aggregate of ________ shares of New Delta Common Stock for distribution to holders of Allowed General Unsecured Claims and those holders of Allowed Non-Convenience Class Retiree Claims against Delta receiving shares of New Delta Common Stock and for sale on behalf of those holders of Allowed Non-Convenience Class Retiree Claims who elected to receive Cash in lieu of shares of New Delta Common Stock. Additional shares will be issued and/or reserved (i) to establish the Disputed Claims Reserves and (ii) to satisfy required distributions under the Compensation Programs.

(ii) Rights Offering

Delta currently intends to offer to each Rights Offeree the opportunity to purchase, on a pro rata basis, shares of New Delta Common Stock pursuant to the New Equity Investment Rights Offering and to participate in certain Oversubscription Rights in connection therewith. The key terms of the New Equity Investment Rights Offering, including its aggregate amount, the total number of shares, the price per Subscription Right or Oversubscription Right and the procedures for subscription will be described in a revised version of the Disclosure Statement that will also include a Rights Offering Appendix. Certain terms of the New Equity Investment Rights Offering are described in Section 5.9 hereof.

2. New Delta Preferred Stock

Reorganized Delta expects to have 500,000,000 authorized shares of preferred stock, $0.0001 par value ( New Delta Preferred Stock ). The Plan does not contemplate the issuance of any New Delta Preferred Stock. However, the New Delta Preferred Stock will be issuable post-emergence in one or more series, and the New Delta Board will be authorized to fix the amounts, descriptions, powers and preferences with respect to any series of New Delta Preferred Stock.

b. Secured Debt

Reorganized Delta expects to have approximately $7.7 billion principal amount of secured debt outstanding on the Effective Date, including the following:

11

1. New Credit Facility

On or after the Effective Date, Reorganized Delta and certain of the Reorganized Subsidiary Debtors will enter into the New Credit Facility. Reorganized Delta will use the New Credit Facility to repay the DIP Facility Claims and the Amex Post-Petition Facility Claims, to make other payments required under the Plan and to fund the post-reorganization operations of the Reorganized Debtors. The Debtors will consult with the Creditors

Committee regarding the terms of the New Credit Facility, which terms will be set forth in a Plan Supplement that shall be filed no later than 20 calendar days before the Voting Deadline.

Confirmation of the Plan shall constitute approval of the New Credit Facility (and all transactions contemplated thereby and all obligations to be incurred by the Reorganized Debtors thereunder) and authorization for the applicable Reorganized Debtors to execute and deliver the New Credit Facility Documents and such other documents as the New Credit Facility Agents or the New Credit Facility Lenders may reasonably require to consummate the New Credit Facility.

2. Other GE Secured Debt

As of the Effective Date, Delta also expects to have outstanding secured notes payable to General Electric Capital Corporation ( GE ) in the principal amounts of approximately $153 million, $246 million and $109 million (collectively, the GE Secured Notes ). These notes are secured by spare engines, spare parts and aircraft, respectively. Delta also has an irrevocable, direct pay letter of credit issued by GE totaling approximately $403 million, with $14 million currently drawn and $381 million to back Delta s obligations with respect to outstanding principal amounts of certain municipal bonds. Delta is obligated pursuant to a reimbursement agreement (the GE Reimbursement Agreement ) to reimburse GE for drawings under these letters of credit, and these reimbursement obligations are also secured by aircraft and other Collateral.

c. Secured Aircraft-Related Debt

As of the Effective Date, the Reorganized Debtors expect to have in place a significant number of secured aircraft-related financing arrangements, with installments due from 2007 to 2023. On the Effective Date, approximately $4.8 billion in aircraft-related debt will be outstanding and secured by aircraft. This amount includes an outstanding principal amount of $1.1 billion in various issuances of private aircraft-backed mortgage debt and $3.8 billion in enhanced equipment trust certificates ( EETCs ).

d. Municipal Bonds

As of the Effective Date, Reorganized Delta expects to have a total of approximately $558 million principal amount of special facilities revenue bonds due through 2035 that were issued to finance the acquisition and construction of certain facilities in Atlanta, Chicago, Los Angeles and certain other locations ($263 million of which would be classified as obligations under operating leases).

12

Delta Airlines, Inc.

e. Unsecured Debt

In connection with the Plan, Reorganized Delta expects to issue senior unsecured notes with an aggregate principal amount of up to $875 million. The New Delta ALPA Notes will be senior unsecured notes with an aggregate principal amount of up to $650 million that will be issued as set forth in and pursuant to the terms of the Bankruptcy Restructuring Agreement Delta entered into with ALPA. However, pursuant to the terms of the Bankruptcy Restructuring Agreement, Reorganized Delta may elect to distribute to the Initial Holder (as defined in the Bankruptcy Restructuring Agreement) cash in lieu of all or any portion of the New Delta ALPA Notes. The New Delta PBGC Notes are senior unsecured notes with an aggregate principal amount of up to $225 million that will be issued as set forth in and pursuant to the terms of the PBGC Settlement Agreement. However, pursuant to the PBGC Settlement Agreement, Reorganized Delta retains the right and, in certain circumstances, the obligation, to distribute to PBGC Cash in lieu of all or any portion of the New Delta PBGC Notes. See Section 4.3(g)(2) for more information regarding the New Delta ALPA Notes and Section 4.3(i) for more information regarding the New Delta PBGC Notes.

Section 2.5 Additional Information and Historical Financials

Additional information concerning the Debtors

business operations and Delta s financial results are set forth in Delta s filings with the Securities and Exchange Commission (the SEC ), including its Annual Report on Form 10-K for the year ended December 31, 2005 and its Quarterly Report on Form 10-Q for the quarterly period ended September 30, 2006. These filings are available on the SEC s website at www.sec.gov

or on Delta s website at www.delta.com.

ARTICLE 3 THE DEBTORS AND EVENTS LEADING UP TO THE CHAPTER 11 CASES

Section 3.1 The Debtors

The Debtors consist of Delta and most of its direct and indirect U.S. subsidiaries. The chart below depicts the corporate structure, as of the date of this Disclosure Statement, of Delta and its subsidiaries that are Debtors. The descriptions of Delta s business in Section 2.1 of this Disclosure Statement and of each of Delta s subsidiaries and their respective businesses below the chart do not give effect to any changes in the corporate structure of the Debtors that will be made in connection with or under the Plan.

13

Delta Technology

Song

Delta Corporate

Identity

Crown Rooms

Kappa Capital Management

Delta Benefits Management

ASA Holdings

Comair Holdings

Comair

DAL Moscow

DAL Aircraft

Trading

Delta AirElite Business Jets

Epsilon Trading

Delta Loyalty

Management Services

Comair Services

Delta

Delta Connection Academy

DAL Global Services

Delta Ventures

Note: AON Group, Inc. owns 10% of equity via

Class B Shares

A brief description of the specific operations of each of the subsidiaries of Delta that are Debtors follows:

ASA Holdings is the former parent of ASA, which ASA Holdings sold to SkyWest on September 7, 2006.

Comair Holdings is the holding company that owns Comair and Comair Services.

Comair is engaged in the business of transportation by air of passengers and freight using regional jets.

Comair Services manages businesses involving air transportation and air vehicles. Comair Services owns Delta AirElite Business Jets and Delta Connection Academy.

Crown Rooms holds liquor licenses for serving alcoholic beverages in certain Delta Crown Room Clubs.