26

UNIVERSAL AND SONY PICTURES HOME ENTERTAINMENT AUSTRALIA Executive Summary

UNIVERSAL AND SONY PICTURES

HOME ENTERTAINMENT AUSTRALIA

Executive Summary

Executive Summary - Contents

• Overview of the JV • High Level Timeline• Organisational Structure• Vision and Values• Location Assumptions• IT Overview and Timeline• Budget Process Timelines (including cashflow)• Transition Plan • Board Timings• Commercial Planning Process – The Operating model for the JV• Appendix

Operating Principles• Genuine partnership. Mutual respect, common history, shared vision

• First class operation, with great leadership and talent and world class content from Universal and SPHE• Unique in Australia – exciting potential First mover advantage means delivering at pace – February 2011

• More product choice and a better service “offer” for our customers• Combination means best scale commercial opportunities create greater efficiencies in a declining marketplace

Structure, Scope and Leadership• We are establishing a joint venture structure with 50/50

ownership between the two business• Rights to products distributed by the JV will be granted to

the JV by each of SPHE and Universal• There will be a single shared back office function in

Australia• New Zealand will be out of scope for the JV, with separate

office distribution arrangements.• The JV is expected to be fully operational by February 1st

2012• The MD of the JV will be Jim Batchelor• The JV’s Board members will be drawn 50/50 from SPHE

& UNI

Strategic rationale

Operating principles

Commercial, Sales & Marketing• Pricing of products and services will be determined by the

JV• Suppliers and sourcing on non-product related goods and

services will be determined by the JV• Terms on supply of product to the JV will be negotiated and

agreed separately by SPHE and Universal• The JV will design and manage all marketing programs and

plans• The marketing programs and plans will be agreed in

advance by each of SPHE and Universal separately for their respective products

Operations• Sony DADC will continue to undertake physical

distribution and order management on behalf of the JV• The commercial arrangements will be market-tested

within the JV on an ongoing basis• Manufacturing suppliers will remain as per current until

the expiry of current contracts

Finance, IT, HR, location• The JV will operate a single set of financial reports• It will report to the parent organisations on items related to

their individual products and volumes• There will be a single HR function and single IT function in

the JV.• The JV will operate on the Sony set of systems.• There will be a single head quarters office location in central

Sydney – No.1 Market Street.

High Level Timeline to Go-Live

• Announce Date ......................................... 6th September• Notify Customers/Vendors ....................... 6th September• Team Appointed ....................................... 19th September• Vendor Negotiations ................................ Sept / Oct• Customer Negotiations ............................. Sept / Oct• Estimated ACCC Clearance ....................... 20th October• Systems Go Live ........................................ 31st October• Office Refit................................................. December/January• Full team in Market Street ........................9th /16th January• GO LIVE....................................................... February 2012

Vision & ValuesUNIVERSAL SONY PICTURES HOME ENTERTAINMENT AUSTRALIA PTY LTD

MISSION: “Lead, entertain, move and inspire...anywhere, anytime, anyone.”

VALUE STATEMENTS: • U.S.A. will be the largest entertainment house in Australia, with the most diverse range.• Our consolidated supply chain will mean easier & more efficient transactions for our

customers.• U.S.A. represents the two most customer-centric, grounded, solutions focused businesses in

the industry coming together.• U.S.A. offer Australia’s biggest box office hits.CUSTOMER VALUE PROPOSITION• a collaborative approach• consolidated supply chain efficiencies• the big box office hits• a breadth and depth of product• all from a trusted team of expertsPREDATORY POSITIONING

“Our synergies give us the energy to move, entertain and inspire.”

Foundation: Sageprogressive people focused

smart fun

relia

ble

cou

rage

ou

scon

fide

nt

colla

bo

rativ e

Core: Hero

POSITIONING

Universal Sony Pictures Home Entertainment Australia Pty. Ltd.

BreadthA large and diverse range of over XXXX (tbc) active titles spanning the latest blockbusters, library classics, cult TV series, Kids and Special Interest content= a product for every need.

DepthClose to 20 New Release Blockbusters (>$10m Box Office) slated for 2012 = products that are highly desired.

UbiquityExtensive distribution partnerships through Retail & Rental, Physical, Kiosk & Digital, Purchase, Rental & Streaming= content conveniently in reach of every Australian

StorytellingApplying the art & science of visual storytelling= keeps people emotionally connected with content

SimplicityOne consolidated supply chain and customer team= easy and efficient to do business with.

FlexibilityLarge, local, independent, collaborative, customer centric business= tailored customer solutions InsightSignificant research resources= intimate understanding of consumer and customer needs to deliver results ForesightScale, SONY ties along with diverse & trusted management expertise= smarter thought leadership with the ability to influence change

Australia’s Leading Entertainment House

Entertain . Move . Inspire

Our brand DNA

The Management Team

• Managing Director, Jim Batchelor

• Strategy Director, Catherine Tan

• Finance Director, Peter Ayling

• Marketing Director, Cindy McCulloch

• Sales Director, Paul Courtney

• Operations Director, Kate Bradbury

• Legal and Business Affairs Manager, John Bourne

• HR Manager, Kelly Dowen

Universal & Sony Pictures Home Entertainment Australia Pty LtdSenior Management Team

Confidential

MANAGINGDIRECTOR

Jim Batchelor

STRATEGYDIRECTORCatherine Tan

HUMANRESOURCESMANAGERKelly Dowen

LEGAL /BUSINESSAFFAIRSJohn Bourne

OPERATIONSDIRECTORKate Bradbury

SALESDIRECTORPaul Courtney

FINANCEDIRECTORPeter Ayling

EXECASST TO MDFiona Cole

MARKETING DIRECTORCindy McCulloch

DIRECTOR OFACQUISITIONSUNIJoanna White

SPHEACQUISITIONS& DIGITALDIRECTORSPHEDIGITAL ACCTMANAGER

ACQUISITIONSMANAGERUNILuke Trigwell

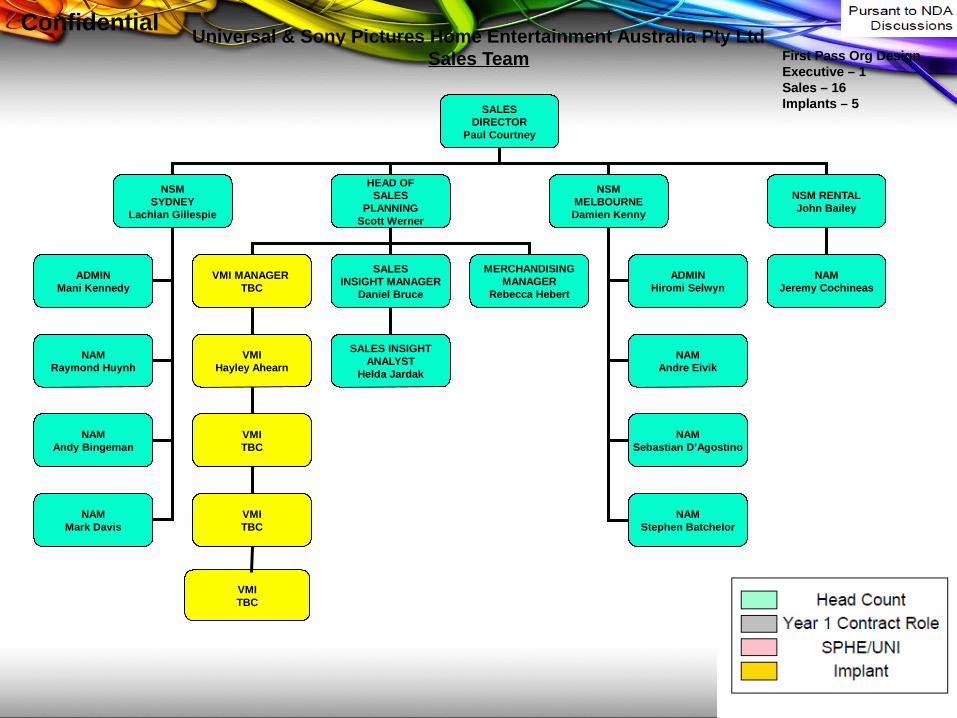

Universal & Sony Pictures Home Entertainment Australia Pty LtdSales Team

SALESDIRECTOR

Paul Courtney

NSMSYDNEY

Lachlan Gillespie

HEAD OFSALES

PLANNINGScott Werner

NSMMELBOURNEDamien Kenny

VMI MANAGER TBC

SALESINSIGHT MANAGER

Daniel Bruce

ADMINMani Kennedy

NAMRaymond Huynh

NAMAndy Bingeman

SALES INSIGHTANALYST

Helda Jardak

VMIHayley Ahearn

VMITBC

ADMINHiromi Selwyn

NAMAndre Eivik

NAMSebastian D’Agostino

VMITBC

NAMMark Davis

NAMStephen Batchelor

MERCHANDISINGMANAGER

Rebecca Hebert

NSM RENTALJohn Bailey

NAMJeremy Cochineas

ConfidentialFirst Pass Org DesignExecutive – 1Sales – 16Implants – 5

VMITBC

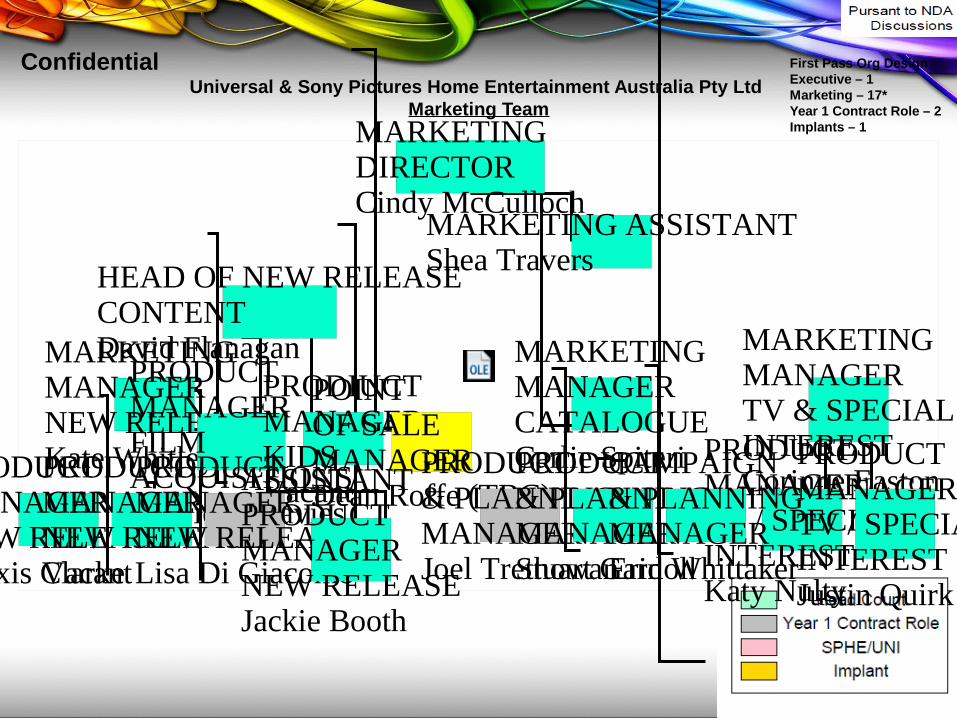

Universal & Sony Pictures Home Entertainment Australia Pty Ltd Marketing Team

Confidential First Pass Org DesignExecutive – 1Marketing – 17*Year 1 Contract Role – 2 Implants – 1MARKETING

DIRECTORCindy McCulloch

HEAD OF NEW RELEASECONTENTDavid Flanagan

MARKETING ASSISTANTShea Travers

MARKETINGMANAGERNEW RELEASEKate Whitley

PRODUCTMANAGERFILMACQUISITIONSGabrielle Davies

PRODUCTMANAGERNEW RELEASEAlexis Clarke

PRODUCTMANAGERNEW RELEASEVacant

PRODIUCTMANAGERKIDSVacant

PRODUCTMANAGERNEW RELEASELisa Di Giacomo

POINTOF SALEMANAGERDean Roffe (TBC)

MARKETINGMANAGERCATALOGUECarlie Spiteri

MARKETINGMANAGERTV & SPECIALINTERESTCorinne Easton

PRODUCT& PLANNINGMANAGERJoel Trethowan

PRODUCT& PLANNINGMANAGERStuart Gardoll

PRODUCTMANAGERTV / SPECIALINTERESTKaty Nulty

PRODUCTMANAGERTV / SPECIALINTERESTJustin Quirk

CAMPAIGN& PLANNINGMANAGERErin Whittaker

ASSISTANTPRODUCTMANAGERNEW RELEASEJackie Booth

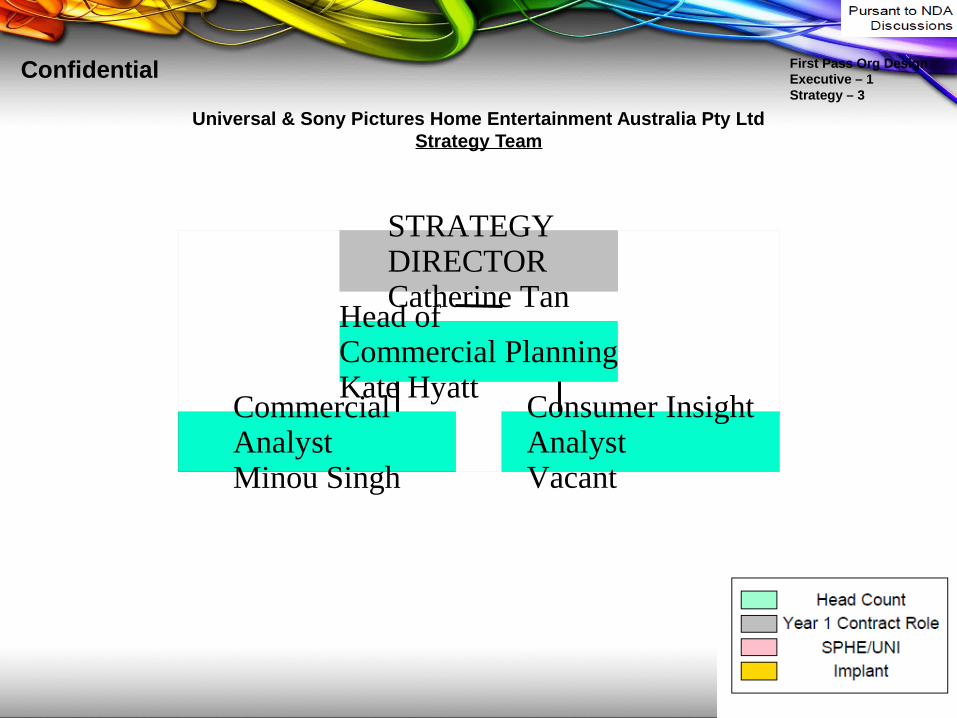

Universal & Sony Pictures Home Entertainment Australia Pty LtdStrategy Team

Confidential First Pass Org DesignExecutive – 1Strategy – 3

STRATEGYDIRECTORCatherine Tan

Head ofCommercial PlanningKate Hyatt

CommercialAnalystMinou Singh

Consumer InsightAnalystVacant

Universal & Sony Pictures Home Entertainment Australia Pty Ltd Operations Team

ConfidentialFirst Pass Org DesignExecutive – 1Operations – 4Implants – 2Year 1 Contract Role – 1OPERATIONS DIRECTOR

Kate BradburyDEMAND PLANNINGMANAGERDario Falzon PRE-PRODUCTION MANAGER

Naomi Black

LOGISTICS MANAGERSteve Tulett

PRE-PRODUCTION CO-ORDINATORGreg Thornton

DADCDISTRIBUTOR

CUSTOMER SERVICEVia Distribution Centre

CREDIT CONTROL

ACCOUNT MANAGEMENT

IT PROGRAMMING

INVENTORYMANAGERViktoria MorganINVENTORY

COORDINATORFiona Drummond

LOGISTICS MANAGERShainaz Tamrazians

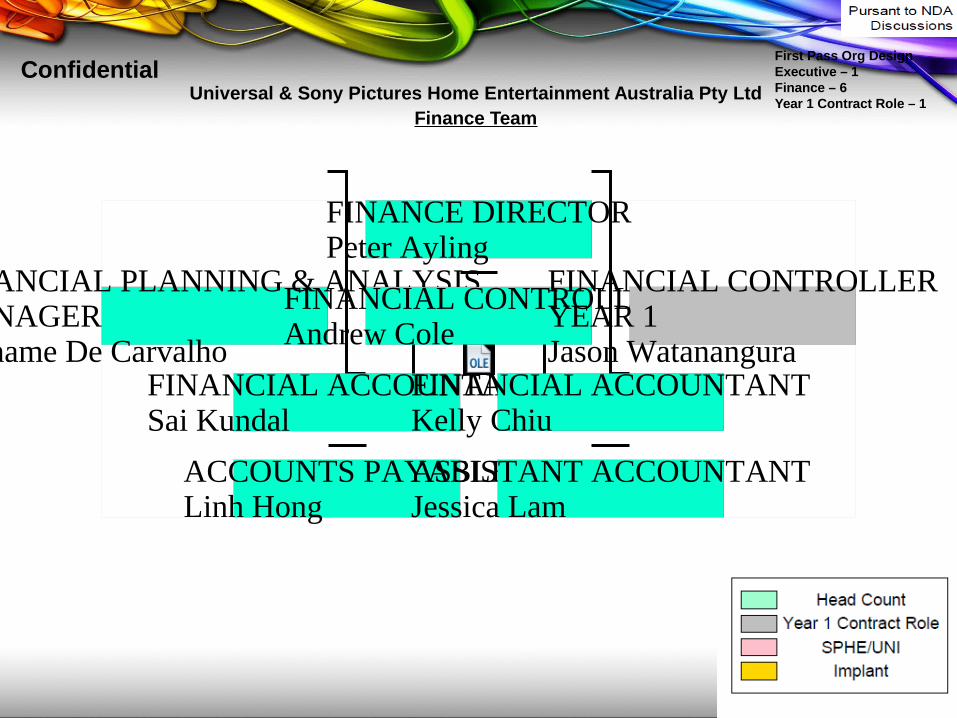

Universal & Sony Pictures Home Entertainment Australia Pty Ltd Finance Team

ConfidentialFirst Pass Org DesignExecutive – 1Finance – 6Year 1 Contract Role – 1

FINANCE DIRECTORPeter Ayling

FINANCIAL PLANNING & ANALYSIS MANAGERGrahame De Carvalho

FINANCIAL CONTROLLERAndrew Cole

FINANCIAL CONTROLLERYEAR 1Jason Watanangura

FINANCIAL ACCOUNTANTSai Kundal

FINANCIAL ACCOUNTANTKelly Chiu

ACCOUNTS PAYABLELinh Hong

ASSISTANT ACCOUNTANTJessica Lam

System Overview

High Level IT Plan

Board StructureLocal Executive Board

– Managing Director, Jim Batchelor– Finance Director, Peter Ayling– Strategy Director, Catherine Tan

Universal & Sony Board– 50:50– 3 Senior Executives from each organisation

Board Meeting Schedule & Assumptions 2011 & Board

– Cashflow from 1 Dec – 30 Sept Completed & Submitted to USA Board– Oct Board Meeting Week 3 Oct– December Board Meeting Week 1 Dec–2012 Qtrly Board Meetings To be scheduled 2 VTC 2 in Australia

Universal: Eddie CunninghamMelanie LaithwateIan Foster

Sony: Matt Brown/Kim OverallBill StellmanT.Paul Miller

SCHEDULE STATUS

JV Legal Company Directors

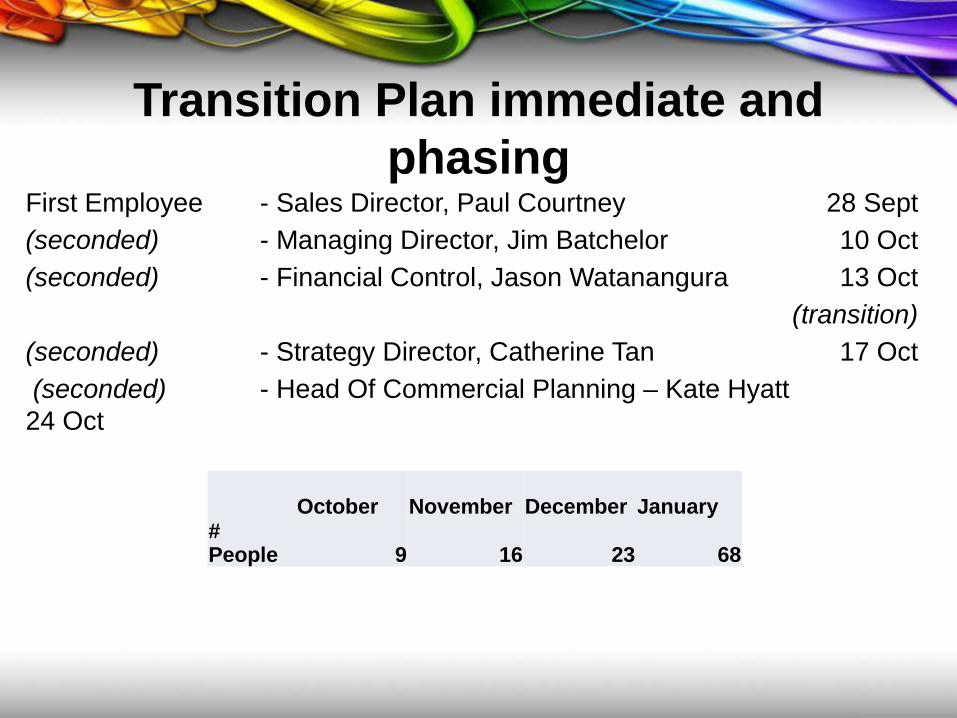

Transition Plan immediate and phasing

First Employee - Sales Director, Paul Courtney 28 Sept

(seconded) - Managing Director, Jim Batchelor 10 Oct

(seconded) - Financial Control, Jason Watanangura 13 Oct

(transition)

(seconded) - Strategy Director, Catherine Tan 17 Oct

(seconded) - Head Of Commercial Planning – Kate Hyatt 24 Oct

October November December January# People 9 16 23 68

Budget Process + TimingsCurrent:Universal current financial year = Calendar Jan-Dec

Sony current financial year = April 1 – March 31

GO LIVE DATE for JV = Feb 1

JV financial year = April 1 – March 31

Year 1 Operating Plan = Feb 1 – Jan 31 + 2 mths to March

31st

Budget Process Working Assumptions for Year 1:• Universal budget submission completed for Jan 2012 - Dec2012• Sony budget to March 31st 2012 completed• Sony budget submission for April 2012–March 2013 = Nov/Dec 2011• Build aggregate budget for Year 1 including Jan/Feb 2013 . Universal forecast to provide

financial assumptions for Year 1 Operating Plan• Quarterly rolling forecast to ensure we meet both Universal & Sony corporate financial

reporting requirements.

Budget & Forecast Approach

FY2013 BUDGET & FORECAST (By Qtr) NewCo Financial Year - Year 1 NewCo Financial Year - Year 2Budget/FC to Home Office

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

NEWCO FY2013 (Q1) FY2013 (Q2) FY2013 (Q3) FCY2013 (Q4) FY2014 (Q1) FY2014 (Q2) FY2014 (Q3) FCY2014 (Q4) UNIVERSAL FY2012 (Q1) FY2012 (Q2) FY2012 (Q3) FY2012 (Q4) FY2013 (Q1) FY2013 (Q2) FY2013 (Q3) FY2013 (Q4) FY2014 (Q1)

SONY PIC'S FY2012 (Q4) FY2013 (Q1) FY2013 (Q2) FY2013 (Q3) FCY2013 (Q4) FY2014 (Q1) FY2014 (Q2) FY2014 (Q3) FCY2014 (Q4)

UUniversal's FY12 "Q5" Forecast

Universal's FY13 "Q5" Forecast

JV Cost AssumptionsSet up till December 31st 2011• All title related costs (COG'S, Marketing etc) paid before December

31 will be expensed to legacy companies as and when incurred .• Employee costs, including T&E, on early transitioned employees will

be met by legacy companies until Go Live Date and then reconciled (as agreed in Uni/Sony calls)

• Final budget & progress payment schedule for office fit-out yet to be confirmed. Will confirm after tender submission selection. Estimate $415k + GST

• Excludes a Security Deposit of 2 months rent ($11,880) paid to Christie Offices by SPHE in August. This will be refunded to SPHE 60 days after end of lease.

JV Cost AssumptionsNewCo Cash Flow Aug Sep Oct Nov Dec Total

Shareholder Funding - SPHE $0 $0 $110,000 $85,000 $135,000 $330,000 - Universal $0 $0 $110,000 $85,000 $135,000 $330,000

Revenue $0 $0 $0 $0 $0 $0COGS/Marketing $0 $0 $0 $0 $0 $0 (1)

GP (Titles) $0 $0 $0 $0 $0 $0Overhead $0 $0 $0 $0 $0 $0 (2)

Distribution Fee $0 $0 $0 $0 $0 $0

JV Capitalizable Costs Excl.GSTMarket Street - Level 30 Refit Project $0 $0 -$176,000 -$110,000 -$170,500 -$456,500 (3) 415,000- Market Street - Level 19 Refit Project (Relocation of TV) $0 $0 -$16,500 -$11,000 -$22,000 -$49,500 45,000- NewCo IT Equipment - Desktops/Laptops/Phones etc $0 $0 $0 -$39,600 -$19,800 -$59,400 54,000- NewCo IT System Costs - Sales Bank / Network & Inf. $0 $0 $0 -$16,500 -$53,900 -$70,400 64,000-

Cash Roll-forward $0 $0 $27,500 $20,400 $24,200

Transition Costs (To be settled by Legacy Co's) Aug Sep Oct Nov Dec Total Excl.GST

Spring Street - Office Rent & Outgoings $0 -$13,070 -$6,753 -$7,091 -$7,091 -$34,004 (4) 30,913- Vision & Values Workshop - Step Change Workshop -$10,519 -$11,454 $0 $0 $0 -$21,973 19,975- Trading Terms Negotiations - Grist Consulting $0 $0 $0 -$19,250 $0 -$19,250 17,500- JV Staff Team Building Day $0 $0 $0 -$27,500 $0 -$27,500 25,000-

Location Assumptions/Rationale• No.1 Market Street, Level 30.

• One floor that can accommodate all staff & dedicated SONY and UNIVERSAL teams

• Cost per person comparable to Munn Reserve, parking in adjacent & 2 close locations.

• Refit/Rebrand per approved budget Dec/Jan.• Targeted move in date Jan 16th.• No.1 Market Street supports Sony system choice and IT support located onsite.

Commercial Planning CycleBeing Refined and functionally process mapped in October

Appendix

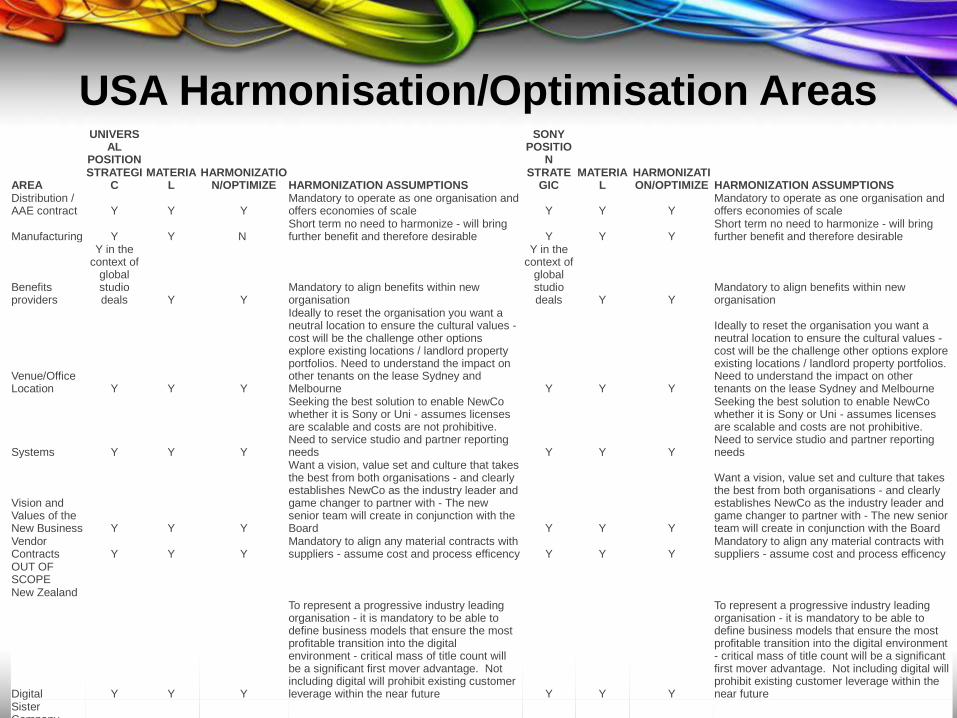

USA Harmonisation/Optimisation Areas

UNIVERSAL

POSITION

SONY POSITIO

N

AREASTRATEGI

CMATERIA

LHARMONIZATIO

N/OPTIMIZE HARMONIZATION ASSUMPTIONSSTRATE

GICMATERIA

LHARMONIZATION/OPTIMIZE HARMONIZATION ASSUMPTIONS

Distribution / AAE contract Y Y Y

Mandatory to operate as one organisation and offers economies of scale Y Y Y

Mandatory to operate as one organisation and offers economies of scale

Manufacturing Y Y N Short term no need to harmonize - will bring further benefit and therefore desirable Y Y Y

Short term no need to harmonize - will bring further benefit and therefore desirable

Benefits providers

Y in the context of

global studio deals Y Y

Mandatory to align benefits within new organisation

Y in the context of

global studio deals Y Y

Mandatory to align benefits within new organisation

Venue/Office Location Y Y Y

Ideally to reset the organisation you want a neutral location to ensure the cultural values - cost will be the challenge other options explore existing locations / landlord property portfolios. Need to understand the impact on other tenants on the lease Sydney and Melbourne Y Y Y

Ideally to reset the organisation you want a neutral location to ensure the cultural values - cost will be the challenge other options explore existing locations / landlord property portfolios. Need to understand the impact on other tenants on the lease Sydney and Melbourne

Systems Y Y Y

Seeking the best solution to enable NewCo whether it is Sony or Uni - assumes licenses are scalable and costs are not prohibitive. Need to service studio and partner reporting needs Y Y Y

Seeking the best solution to enable NewCo whether it is Sony or Uni - assumes licenses are scalable and costs are not prohibitive. Need to service studio and partner reporting needs

Vision and Values of the New Business Y Y Y

Want a vision, value set and culture that takes the best from both organisations - and clearly establishes NewCo as the industry leader and game changer to partner with - The new senior team will create in conjunction with the Board Y Y Y

Want a vision, value set and culture that takes the best from both organisations - and clearly establishes NewCo as the industry leader and game changer to partner with - The new senior team will create in conjunction with the Board

Vendor Contracts Y Y Y

Mandatory to align any material contracts with suppliers - assume cost and process efficency Y Y Y

Mandatory to align any material contracts with suppliers - assume cost and process efficency

OUT OF SCOPE New Zealand

Digital Y Y Y

To represent a progressive industry leading organisation - it is mandatory to be able to define business models that ensure the most profitable transition into the digital environment - critical mass of title count will be a significant first mover advantage. Not including digital will prohibit existing customer leverage within the near future Y Y Y

To represent a progressive industry leading organisation - it is mandatory to be able to define business models that ensure the most profitable transition into the digital environment - critical mass of title count will be a significant first mover advantage. Not including digital will prohibit existing customer leverage within the near future

Sister Company Commitments

USA Harmonisation/Optimisation Areas

UNIVERSAL

POSITION

SONY POSITIO

N

AREASTRATEGI

CMATERIA

LHARMONIZATIO

N/OPTIMIZE HARMONIZATION ASSUMPTIONSSTRATEGIC

MATERIAL

HARMONIZATION/OPTIMIZE HARMONIZATION ASSUMPTIONS

Trading Terms Y Y YCost benefit assumption, on a customer x customer basis, Challenge customer JBHifi Y Y Y

Optimise assuming a commercial benefit to both parties and a customer reset as category lead, Challenge customer Jbhifi

Consignment y y Potentially

factors that influence the decision - commercial impact and practical reality in the context of NewCo operation - to maximise business you would ideally want them aligned y y y

Leverage from the new operating model comes via critical mass within the customers preferred Business Model - need to have one face to extract the most in the negotiations with trade

Revenue Share Y Y Potentially

factors that influence the decision - commercial impact and practical reality in the context of NewCo operation - to maximise business you would ideally want them aligned Y Y Y

Leverage from the new operating model comes via critical mass within the customers preferred Business Model - need to have one face to extract the most in the negotiations with trade

Payment Terms N

Y - cash flow Y Mandatory to operate as one organisation N

N from a relative

perspective Y Mandatory to operate as one organisation

Target Product Incentives Y

Y - strategicall

y N

Be strategic in terms of how you execute title/range incentives in the context of the aggregate NewCo offer to the customer Y

Y on a title/partne

r basis N

Be strategic in terms of how you execute title/range incentives in the context of the aggregate NewCo offer to the customer

Merchandising Vendor N Y Y absolutely

Quality of company and relative cost need to be aligned N Y Y

Key to Customer perception of NewCo and supply chain efficiency

Advertising Agency

Y in the context of

an internation

al deal Y Y

Critical to maximise effiency both from positioning, media and partner leverage and process within the operation possibly closed tender process Y Y Y

Critical to maximise effiency both from positioning, media and partner leverage and process within the operation possibly closed tender process

Windows Y Y YIdeally but you could operate on a release date basis Y Y Y

Preferable to align - there is leverage in first mover with scale

Freight N Y YMandatory to operate as one organisation and offers economies of scale N Y Y

Mandatory to operate as one organisation and offers economies of scale

Research N N Y

Align on industry suppliers and renegotiate as NewCo (GFK) share studio Agree on local Research approach and share costs within NewCo. Studio based research from Uni/Sony to be share within NewCo Y Y Y

Align on industry suppliers and renegotiate as NewCo (GFK) share studio Agree on local Research approach and share costs within NewCo. Studio based research from Uni/Sony to be share within NewCo

Structure Y Y Y

Need to align on the optimal structure to ensure new co can maximise the new go to market strategy Y Y Y

Need to align on the optimal structure to ensure new co can maximise the new go to market strategy

Remuneration Total Package inc of all benefits Y Y Y

Got to be a clear approach for the new business, roles in the NewCo need to be neutral in refernence to organisation origin Y Y Y

The leadership team (managment and level below) need to be of a calibre to lead a new business model in the industry and therefore need to be remenurated accordingly