www.parliament.uk/commons-library | intranet.parliament.uk/commons-library | [email protected]| @commonslibrary BRIEFING PAPER Number CBP-08156, 16 April 2018 Universities Superannuation Scheme (USS) By Djuna Thurley Contents: 1. Background 2. Funding status 3. The 2017 valuation 4. Proposals for reform of scheme benefits

2. Funding status 6 2.1 The process for valuing the USS 6 2.2 Recent valuations 7 2.3 The role of the Pensions Regulator 7

3. The 2017 valuation 8 3.1 Consultation with UUK 8 3.2 UCU response 10

4. Proposals for reform of scheme benefits 13 4.1 UUK’s initial proposals 13 4.2 Agreement of Joint Negotiating Committee 13 4.3 Offer of 12 March 16 4.4 Proposal for a joint expert panel - 23 March 2018 18 4.5 Questions in Parliament 19

Cover page image copyright Click & browse to copyright info for stock image

3 Commons Library Briefing, 16 April 2018

Summary Recent valuations of the USS have shown an increasing deficit, the main cause being “lower expected levels of future investment returns and lower yields on index-linked gilts” (2017 Annual Report).

In September 2017, consulted with Universities UK (UUK) on the assumptions it would take for the 2017 valuation. It proposed a “prudent” approach to the assumptions on investment returns. An important factor was that investment returns were expected to reduce in future. Other things being equal, a prudent approach to the assumptions on investment returns would require a higher level of contributions (from employers and employees) because the return on assets is expected to be lower. (USS, 2017 Actuarial Valuation, 1 September 2017, p7) On 14 November 2017, the USS trustees said UUK’s response “indicated to us that we should take a more moderate approach to risk.” They therefore agreed to “retain the 2014 approach to de-risk the scheme’s investments over the next 20 years.” In practice, this would result in a marginally lower income from investments, requiring higher contributions and increasing the estimated deficit (UUK responds to USS consultation). In a statement explaining its approach to risk on 22 March 2018 UUK said that the trustees had decided on the valuation assumptions based on their “interpretation of the Universities UK feedback, among other factors.”

A report by First Actuarial for the University and College Union (UCU) challenged the Trustee’s approach. It argued that a focused on the cash-flow needed to pay benefits showed that there was “no need to change either the contribution rate or the benefits to have a prudent funding plan.” The Trustee’s approach risked a vicious circle: on the basis that the trustees had responded to the employers’ concern that they did not want an increase in contribution rates by setting “a higher funding target and lower “investment risk”, two actions which are guaranteed to put the employers’ contribution rate up.”

On 17 November 2017, Universities UK proposed closing the scheme to the build-up of future benefits, which would be provided instead through a defined contribution (DC) scheme. Employers would continue to maintain their total contribution at 18% of salaries.

UUK put forward revised proposals, which were agreed to on 23 January 2018 by the Joint Negotiating Committee (made up of equal numbers of representatives from UUK and the UCU and an independent chair), on the casting vote of the chair. On this basis, the scheme had an estimated funding deficit of £6.1 billion and was 91% funded (USS website, proposed changes to future USS benefits).

The UCU made plans for escalating strike action following a ballot of its members in which 88% voted for strike action on a turnout of 58% (press release: 29 January 2018).

UUK and UCU agreed on 12 March to retain a defined benefit scheme for three years from 2019, during which time: member and employer contributions would increase; the accrual rate would reduce (from 1/75th to 1/85th) and members would accrue DB benefits on salary up to £42,000 (down from £55,000). Both parties would investigate risk-sharing options for the future. However, this proposal was rejected by UCU members on 13 March 2018. UUK expressed its disappointment.

On 23 March 2018, UUK and UCU proposed establishing a panel of independent experts to review the USS valuation. Its work would “reflect the clear wish of staff to have a guaranteed pension comparable with current provision whilst meeting the affordability

challenges for all parties.” Current contribution rates and pension benefits would continue until at least April 2019.

On 13 April UCU announced that its members had voted to accept the proposals and that it would “suspend its immediate industrial action plans but keep its legal strike mandate live until the agreement between UCU and USS is noted by USS.”

1. Background The Universities Superannuation Scheme (USS) a large multi-employer pension scheme, covering over 350 employers in the higher education sector. It is a funded trust-based defined benefit (DB) scheme. It has 396,278 members: 190,546 active members; 66,419 pensioner members and 139,313 deferred members.1 The scheme was reformed in 2016 (following the 2014 valuation which showed the scheme to be in deficit). The old final salary scheme was closed to future accruals and a new scheme introduced, which provides benefits based on career average revalued earnings. Key features of the USS Retirement Income Builder are that: • Members start to accrue benefits at a rate of 1/75 of each year’s

salary (up to the salary threshold - £55,000 in 2017/18) plus a tax-free cash lump sum of 3 x pension;

• Members contribute at a rate of 8% of salary.

• The normal pension age is 65 (with plans for this to rise in future in line with the State Pension age).

For salary above £55,000 and additional voluntary contributions, there is a separate defined contribution (DC) scheme – USS Investment Builder.

Benefits build up before April 2016 were calculated based on salary and length of service at that point. The pension and cash value resulting from this calculation is revalued to retirement. At retirement, the resulting “service credit” is added to any further benefits accrued under the scheme from April 2016 onwards. 2

In October 2016, USS Investment Builder, a new DC arrangement was introduced for members with salaries in excess of the £55,000 threshold and for the investment of additional voluntary contributions. Detailed guides about the scheme are on the USS website.

1 USS Annual Report and Accounts 2017 2 USS, Benefits earned before April 2016

2. Funding status Defined Benefit occupational pension schemes need to be valued periodically – at least every three years. The purpose is to establish how much the scheme’s assets are worth and how much the scheme needs to be able to pay pensions as they fall due. Where a scheme is in deficit, the trustees must draw up a “recovery plan” and send this to the Pensions Regulator.3

2.1 The process for valuing the USS The USS Trustee explains its approach to the valuation process as follows:

The process begins with an assessment of the financial strength of our sponsoring employers.

This is the foundation of the valuation as it shows the trustee just how much financial support employers can provide to the scheme and how much investment risk could be taken. (The level of investment risk to be taken is set following detailed discussions with employers).

For this year’s valuation, for example, we undertook a very detailed study informed by independent expert advice which concluded that, despite uncertainty about the short-term impact of Brexit, the employers’ ability to provide financial support for the scheme remains strong – and can be expected to continue to be so for at least 30 years.

Another key part of the process is estimating how much money we think we will need in order to provide the current level of benefits.

There is no easy answer, so we look at a wide range of data and identify trends to predict what might happen in the future, with the main areas being:

• The level of return we can expect from our investments;

• Price inflation and, in turn, how much pensions might increase;

• How much you might earn in the future and therefore pay into your pension over your working life;

• How long you might live and be claiming your pension; and

• Whether you have any beneficiaries who might also receive a pension after your death.

[…]

Employer (UUK) and UCU representatives will, through the Joint Negotiating Committee…look to reach agreement on any changes required to contribution rates, future benefits, or both. If any changes are agreed by the committee, employers will then consult with affected employees.

3 Pensions Act 2004, Part 3

For more information, see

Library Briefing Paper CBP-4877 Defined benefit pension scheme funding (October 2017)

At the end of the process we will have agreed a strategy of contributions, benefits and investments as well as a realistic plan to recover the existing deficit.4

For a more detailed account, see the introduction to the consultation on the 2017 valuation.

2.2 Recent valuations Recent valuations of the USS have shown an increasing deficit:

• The 2011 actuarial valuation showed a £2.9 billion deficit and a 92% funding ratio. A 10-year recovery plan was adopted to address this.5

• The 2014 valuation showed a £5.3 billion deficit and an 89% funding ratio. A longer recovery plan of 17 years was adopted.6

The 2014 valuation reflected reforms to future benefit accrual discussed in section 1 above, which “reduced the deficit by £5.2 bn.”7 The 2017 Annual Report showed the deficit to have increased from £5.3 bn in 2014 to £12.6bn at 31 March 2017. The funding ratio was 83%. The main cause was the lower expected levels of future investment returns and lower yields on index-linked gilts. The scheme asset returns had mitigated the impact on the deficit but the impact on the expected future cost of pensions was more significant.8

2.3 The role of the Pensions Regulator In a response to chair of the Work and Pensions Committee, Frank Field, the Pensions Regulator explained that early engagement with large schemes was part of its risk-based approach and that it had been continuously engaged with the USS since 2010. It said:

Whilst it is difficult to measure the impact of our engagement on any scheme with certainty, we believe we made a significant contribution to the development of the USS approach in the context of the 2011 and 2014 valuations. Our interventions on risk management and risk allocation helped to set an overarching set of risk and funding principles for the USS. These principles include:

• The principle that the pension risk within the USS should be proportionate to the amount of financial support available from its sponsoring employers, and specifically that there should be no increase in the reliance placed on that support over time; and

• An express intention to take opportunities for long term, gradual risk reduction given the right economic conditions and following appropriate dialogue.9

4 USS website/the 2017 valuation/questions and answers/how do you estimate how

much you’ll need in order to pay pensions 5 USS Annual Report and Accounts 2012, p2 6 USS Annual Report and Accounts 2017, p104 7 Letter from the TPR to chair of the work and pensions committee, September 2017 8 USS Annual Report and Accounts 2017, p14 9 Letter from the TPR to chair of the work and pensions committee, September 2017

3.1 Consultation with UUK In September 2017, the Trustee launched a 4-week consultation with Universities UK (UUK) on the assumptions it would take for the 2017 valuation.10 It proposed a “prudent” approach to the assumptions on investment returns, which would result in an increase in the contributions required:

Our prudent proposals – based on a fundamental building blocks analysis of future investment returns and the maximum available risk budget – forecast average annual returns of CPI + 0.9% and resulted in a funding deficit of £5.1bn (92% funded).

On this approach, the current combined contribution rate of 26% of payroll (8% employee; 18% employer) would have to increase by between 6% and 7% in order to maintain the current level of benefits.11

An important factor in this was that although investment returns had been higher than expected,12 these were likely to reduce in future:

Since 2014, the investment environment has been much more challenging than anticipated: yields on government bonds (gilts) have fallen further than ever before as governments around the world have bought them in order to inject money into struggling economies.

The reduced availability of government bonds has caused investors, particularly those linked to pension funds like USS, to seek other forms of steady, inflation-linked returns.

USS was already operating successfully in these alternative markets – but the continued pressure in the gilts market has prompted other investors to follow suit, with the effect of driving prices up and, in turn, potential future returns down.

So while the investment team has continued to be successful against the benchmarks set, its expectations of how successful it can be in future reflect the reduced returns available in the markets.

This expected future investment return forms an important part of the valuation of the scheme’s liabilities, as we subtract the amount we can reasonably expect USS to make in future from the total cost of providing pensions to give us a present day view of the scheme funding level.13

On its “best estimate” view (a 50% probability that investment forecasts are met or exceeded), the scheme had a surplus of £8.3 billion. However, the trustee had a “legal duty to be prudent in its

10 USS 2017 Actuarial Valuation. A consultation with Universities UK on the proposed

assumptions for the scheme’s technical provisions and Statement of Funding Principles, 1 September 2017; USS, 2017 Report and Accounts, p14

11 USS, UUK response to USS’s consultation on funding proposals, 2017 12 £18.2 bn, compared to £7.2 bn, decreasing the deficit by around £11 billion over

this period 13 USS website/the 2017 valuation/questions and answers/why are you expecting such

funding assumptions.” With a confidence level of 67%, the scheme had a deficit of just over £5 billion.14

Another important factor in its judgement was the volatility in contributions employers would be prepared to support. It had decided to stick with its ‘Test 1’ approach, whereby it would try to keep funding levels within a defined distance of self-sufficiency. This would involve moving to lower risk investments from year 11, with the aim of reducing the reliance on employers to £10bn in 20 years’ time, compared to £23bn in March 2017.15

See also – USS, Six things you should know about the 2017 valuation.

UUK response On 14 November 2017, the USS Trustee said UUK’s response indicated that it should take a more moderate approach to risk:

USS, as trustee, outlined the maximum level of risk we could contemplate taking in funding the scheme on a prudent basis (a statutory requirement).

This was based on independent expert analysis of the levels of future contributions that could be afforded ‘in extremis’ by participating employers, should the funding assumptions ultimately prove inadequate.

We then sought employers’ views as to whether taking the maximum level of risk was appropriate – crucial to how we set the level of contributions to fund the pension.

Our prudent proposals – based on a fundamental building blocks analysis of future investment returns and the maximum available risk budget – forecast average annual returns of CPI + 0.9% and resulted in a funding deficit of £5.1bn (92% funded).

On this approach, the current combined contribution rate of 26% of payroll (8% employee; 18% employer) would have to increase by between 6% and 7% in order to maintain the current level of benefits.

UUK’s responses indicated to us that we should take a more moderate approach to risk. The trustee board accordingly agreed to retain the 2014 approach to de-risk the scheme’s investments over the next 20 years. In practice, over time, this means holding slightly fewer growth-seeking assets and more fixed income assets, which in turn results in a marginally lower income from investments to fund the current level of benefits and recover the funding deficit.

As a result, the board agreed a revised future average annual returns forecast of CPI + 0.71%, resulting in a funding deficit of £7.5bn (89% funded). Maintaining the current level of benefits would, in turn, require a combined contribution rate of 37.4% of pay, including increasing deficit recovery contributions from 2.1% of pay currently to 6%.16

In March 2018, UUK made a statement explaining its approach:

14 USS website, Consultation with Universities UK (UUK) commences; USS, In the news

USS’s 2017 valuation 15 UUK, Employers propose reforms to ensure USS pension scheme remains sustainable

and attractive to members, 17 November 2017, p9 16 USS, UUK response to the USS’s consultation on funding proposals, 2017

The USS trustee in reaching its view on the valuation assumptions consulted with Universities UK as formal USS employer representative in September 2018 on a proposed set of assumptions upon which to calculate the scheme’s liabilities as at the actuarial valuation date, 31 March 2017.

The initial assumptions proposed by the USS trustee in September 2017 required taking more risk than at the previous valuation. The USS deficit at March 2017 would have been £8.5 billion, had the 2014 assumptions been carried forward on a like for like basis. The revised assumptions that the USS trustee consulted on in September 2017 would have significantly reduced the deficit to £5.1 billion.

The USS trustee already takes considerably more risk that almost all other trustees do because the scheme is supported by 350 strong and long-standing employers. The Independent Pensions Regulator and the USS trustee’s covenant advisors, PWC, expressed concern about the level of risk proposed in the September 2017 technical provisions.

In order to discharge its role as employer representative for USS, Universities UK undertook a survey of employers in September 2017.116 employers responded, representing 92% of active scheme members.

On the question of risk, a small majority of employers (53%) had a preference to accept the level of risk proposed, with half of that group qualifying that the proposals were at the very limit of what they would find acceptable. A significant minority (42%) of survey respondents wanted less risk to be taken. A small minority (5%) were willing to accept more risk than that put forward by the trustee in its September 2017 technical provisions response. […]

Our response to USS was shared with employers by email on 13 October 2017. It did not indicate that less risk should be taken. It indicated that “UUK’s view is that the proposed assumptions are at the top end (in terms of risk) of what would be acceptable.” We also noted that “it would be remiss not to recognise the large number of employers who are uncomfortable with the maximum level of risk proposed by the trustee, and UUK also acknowledges the significant concerns raised by the Pensions Regulator and the trustee on short term reliance.” We asked USS to “consider carefully whether the proposed investment strategy (including the degree of interest rate hedging) is optimal for the level of risk being run and the targeted level of returns.17

3.2 UCU response The UCU has published an analysis of the proposals by First Actuarial, which disagrees with the proposed approach, stating that the “primary concern of the employers, and therefore a primary question for the valuation, is that their contribution rate should not go over the current 18%.” It argues that a direct look at the cash flows in and out is often more illuminating than the actuarial model:

Running a continuing pension scheme is a matter of cash flow management. If we look directly at the cash flows, we can see what we need to achieve with the investments. By working only with an actuarial model, we are at risk of not distinguishing

between a problem in the cash flows and a problem in the model.18

It concluded from its cash flow analysis that the current contribution rate from the 2014 valuation remained a “prudent contribution rate, given the current benefit design of the USS”:

In a scenario of “best estimate” pay rises, the benefits of the USS can very nearly be paid from contributions, without reliance on the assets. There is no need to change either the contribution rate or the benefits to have a prudent funding plan. The strong likelihood is that the USS can be invested to outperform the return required to safely deliver the benefits. Given time, the outperformance will increase the funding level to any desired target. Any formulation of the sign off of the valuation which maintains the current contribution rate and the current benefits is acceptable.19

If it was agreed that the current contribution rate was prudent, there were a number of ways in which the parameters of the valuation and the USS’s three funding tests could be adjusted. This was captured by “Test 2”, which aimed to “measure the degree of stability in contributions in the funding approach,” with a high level of confidence that contributions could be kept “within reasonable bounds.”20 It argues that targets to deliver an overall return of at least 1.9% pa relative to CPI would keep the scheme on track:

Investments chosen to deliver an income of at least 1.0% pa and an overall return of at least 1.9% pa real relative to CPI will keep the scheme on track (2.1% pa real if investment performance is to pay for longevity improvements). These are not difficult targets. A better long run return will improve the funding level and help attain any desired funding target without the need for additional contributions.21

It said that switching to low risk/low return investments (as closed schemes do to manage their cash flow, at high cost to their sponsor) did not need to be done until the scheme was closed, if it ever is.22 The Trustee’s proposed approach risked a vicious circle:

The risk is that the more the employers say they do not wish to take risk (where the risk they are mainly concerned about is the risk of their immediate contribution rate going up) the more the trustee interprets this as meaning they must set a higher funding target and lower “investment risk”, two actions which are guaranteed to put the employers’ contribution rate up. To control the employers’ cost, the members’ future benefits are then likely to be cut.

If we keep going around this circle without regard to other objectives, such as the cost-efficient provision of benefits, the end point will be such benefit accruals as can be afforded using a gilt yield discount rate and investment strategy. The advantages of

18 First Actuarial, Report for UCU. Progressing the valuation of the USS, 15 September

2017, p3 19 Ibid 20 First Actuarial, Report for UCU. Progressing the valuation of the USS, September

having an open scheme with sponsoring employers of excellent aggregate covenant will have been discarded.23

On 22 January, the UCU announced that turnout for its ballot for strike action had been 58%, with 88% voting for strike action and 93% for action short of a strike.24 Its higher education committee (HEC) agreed escalating strike action in the event of an unsatisfactory outcome to the talks.25

On 13 April 2018, UCU announced that it would suspend its immediate plans for strike action, following a vote by members to agree to the establishment of a Joint Expert Panel to examine the 2017 valuation.26

23 Ibid, p7 24 UCU website, USS ballot results announced, 22 January 2018 25 UCU website, USS strike action agreed, 22 January 2018 26 UUK, Ballot result on Joint Expert Panel, 13 April 2018; Members vote to accept

employers’ proposal on USS – action suspended, UCU press release, 13 April 2018

4.1 UUK’s initial proposals On 17 November 2017, UUK proposed closing the scheme to the build-up of future benefits, which would be provided instead through a defined contribution (DC) scheme. Employers would continue to maintain their total contribution at 18% of salaries.27

A group of academics wrote expressing their concern about the proposed reforms, which they said the proposals would mean:

[…] the replacement of guaranteed pensions with a defined contribution scheme that will be wholly dependent on movements in stocks and shares. First Actuarial estimates that a typical lecturer will receive £208,000 less under the proposals than presently. For universities that rely on the USS to help recruit and retain staff this will be a disaster, with lecturers enjoying retirement income of an estimated £400,000 less than their colleagues in the rival Teachers’ Pension Scheme, which mainly enrols staff in post-92 universities.28

4.2 Agreement of Joint Negotiating Committee

On 18 January 2018, UUK put forward revised proposals for reform. Its six specific propositions – which it said were intended to align with the priorities put forward by UCU -were:

6.2 Risk sharing alternatives: In the lead-up to the 18 December 2017 JNC UCU requested that parties should consider alternative risk sharing scheme structures that might provide members with greater certainty in retirement, such as CDC. UUK sets out clearly in this revised proposal that it wants to engage with UCU and the USS trustee to consider, on an ongoing future basis, how risks are shared between members and employers, and to evaluate the merits of such novel scheme designs. It is noted that CDC is not believed to be an option currently available to stakeholders, as the UK lacks the secondary legislation required to make CDC possible.

6.3 DB re-introduction: UCU want to maintain a level of guaranteed benefits as part of the USS benefit design. UUK believes that the managing scheme risk now is the best way to ensure meaningful DB can be reintroduced and sustained in the future should economic conditions improve. Employers would be willing to explore the framework within which stakeholders might decide on the re-introduction of a level of DB benefits (in addition to death and ill health benefits) in future as part of the longer term strategic direction for USS. We would envision these

27 UUK, Employers propose reforms to ensure USS pension scheme remains sustainable

and attractive to members, 17 November 2017 28 Letter: shrinking pensions could lead to retirement disaster, Times Higher Education

Supplement, 18 January 2018; UCU website; UCU 1,000 professors on the importance of USS

discussions to take place concomitant with considerations of alternative risk-sharing options (such as CDC).

6.4 Better DC options in retirement: UCU have raised concerns that DC places greater uncertainty on members in retirement and facing a high cost of commercial annuities. UUK proposes discussions with UCU and the USS trustee on how to benefit from the genuinely valuable flexibilities that DC saving can enable for members in terms of how and when they access their pension savings. UUK is working with the USS trustee through the JNC to undertake a review of retirement, and is also committed to working with stakeholders to fully explore new and innovative post-retirement options that can be genuinely attractive for members. UUK believes member outcomes can be significantly improved by making sure appropriate work is carried out on post-retirement options for our employees.

6.5 Lower deficit recovery contributions (DRCs): UCU has expressed significant concern regarding the increased DRCs that the USS trustee suggests will be required at this valuation. UUK shares this concern, as significantly higher DRCs constrain funding for future service benefits and has serious ramifications for the higher education sector. Whilst a matter to be determined by the trustee subject to consultation with UUK, UUK would be supportive of jointly making requests to the trustee to reconsider the level of DRCs which the trustee is seeking from 1 April 2019 and to ensure that these are no higher than necessary (it is emphasised that UUK would continue to make its own representations on these issues, on behalf of employers, as appropriate).

6.6 Investment de-risking: UCU have raised several questions regarding the USS trustee’s proposed investment de-risking. The way that the fund’s investments are assumed to change over time, in with the context of the trustee’s building block approach for determining the discount rate with the technical provisions, is a matter on which the trustee has consulted and decided its position – and is outside the remit of the JNC. However, UUK believes that it would be useful – over and above that which is included in any consultation on the statement of investment principles – to allow additional engagement with stakeholders on the way that any investment de-risking is to be implemented by the trustee, for example to ensure that any specific portfolio de-risking approaches deliver the most benefit for the associated expected reduction in target return. To confirm UUK is not proposing to try to reopen the technical provisions discussion which is already agreed and is outside of the remit of the JNC.

6.7 Employer contributions: UCU have proposed that employers should increase their contributions to USS. UUK has considered this option fully and has explained why any increase above 18% is unaffordable. However, UUK does understand that certainty of employers’ commitment to contributions is valuable and could help discussions on the longer-term design of USS. In accordance, employers propose further extending the duration of their commitment to maintaining employer contributions at 18% of salaries for a period of six years following the valuation date (i.e. March 2023).29

29 Revised UUK proposal to the JCN for future benefit reform – 23 January 2018

The USS said that this decision resulted in an estimated funding deficit of £6.1 billion, meaning the scheme was 91% funded. It summarised the proposals as follows:

Benefits already earned by both active and deferred members are protected by law and in the scheme rules. Benefits already being paid to retired members are not affected by this decision.

From 1 April 2019 (at the earliest):

• The salary threshold (the salary up to which defined benefits currently build up) would reduce to zero;

• All future benefits, until further review, would be built up in the USS Investment Builder (the defined contribution part of the scheme), except death in service and ill health retirement benefits – see below;

• There would be no changes to the provision of death in service or ill health retirement benefits. These would remain based on full salary regardless of the salary threshold;

• The employer contribution is proposed to remain at 18% of salary; as is the case now, this would cover deficit recovery contributions, the subsidy of investment management charges and scheme running costs, and their part of death and incapacity benefit contributions; 13.25% of their overall contribution would go into members’ USS Investment Builder funds;

• Members would continue to contribute 8% of pay, but would have access to a lower cost option of contributing 4% while still receiving the full employer contribution into the USS Investment Builder of 13.25%;

• Members’ 8% (or 4%) would include a contribution to partly finance their death in service and ill health retirement benefits.

The ‘match’ – the additional 1% employer contribution currently available when members contribute an additional 1% to the USS Investment Builder – would be discontinued.30

The Joint Negotiating Committee (JNC) agreed to this proposal on 23 January. A UUK spokesperson said:

UUK has designed a lower-cost saving option to ensure that USS remains a suitable scheme for all. In this option, members can pay contributions of 4% rather than 8% of salary while still benefitting from the 18% employer contribution. USS would continue to offer very valuable life assurance and substantial benefits in the event of ill-health.

Pension benefits already built up are protected by law and cannot be changed retrospectively.31

UCU said the proposal had been imposed, with the chair siding with the employers’ representatives:

The chair sided with the employers' representatives and their plans to transform the scheme from one with a guaranteed

30 Proposed changes to future USS benefits, USS website January 2018 31 Proposal agreed to reform USS Pensions, 23 January 2018

retirement income to a defined contribution scheme where pension income is subject to changes in the stock market.

The union said it was disappointed that the talks ended with the changes being imposed on USS members.32

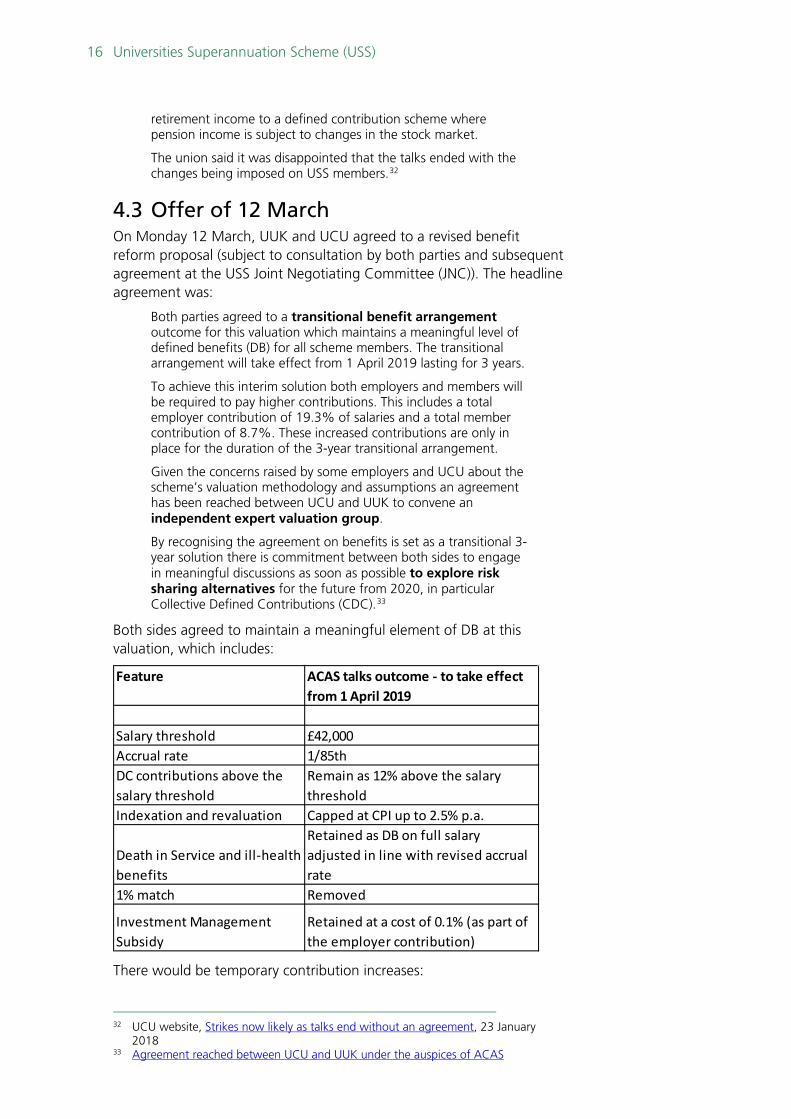

4.3 Offer of 12 March On Monday 12 March, UUK and UCU agreed to a revised benefit reform proposal (subject to consultation by both parties and subsequent agreement at the USS Joint Negotiating Committee (JNC)). The headline agreement was:

Both parties agreed to a transitional benefit arrangement outcome for this valuation which maintains a meaningful level of defined benefits (DB) for all scheme members. The transitional arrangement will take effect from 1 April 2019 lasting for 3 years.

To achieve this interim solution both employers and members will be required to pay higher contributions. This includes a total employer contribution of 19.3% of salaries and a total member contribution of 8.7%. These increased contributions are only in place for the duration of the 3-year transitional arrangement.

Given the concerns raised by some employers and UCU about the scheme’s valuation methodology and assumptions an agreement has been reached between UCU and UUK to convene an independent expert valuation group.

By recognising the agreement on benefits is set as a transitional 3-year solution there is commitment between both sides to engage in meaningful discussions as soon as possible to explore risk sharing alternatives for the future from 2020, in particular Collective Defined Contributions (CDC).33

Both sides agreed to maintain a meaningful element of DB at this valuation, which includes:

There would be temporary contribution increases:

32 UCU website, Strikes now likely as talks end without an agreement, 23 January

2018 33 Agreement reached between UCU and UUK under the auspices of ACAS

Feature ACAS talks outcome - to take effect from 1 April 2019

Salary threshold £42,000Accrual rate 1/85thDC contributions above the salary threshold

Remain as 12% above the salary threshold

Indexation and revaluation Capped at CPI up to 2.5% p.a.

Death in Service and ill-health benefits

Retained as DB on full salary adjusted in line with revised accrual rate

1% match Removed

Investment Management Subsidy

Retained at a cost of 0.1% (as part of the employer contribution)

Contribution increases are temporary for the duration of this 3-year valuation period at a level of 19.3% of salaries for employers and 8.7% for members. This assumes a deficit recovery contribution of 4.5%, which is subject to consideration by the USS trustee.34

There would be an independent valuation review and risk-sharing alternatives would be considered for the future:

Independent valuation review

UCU and UUK jointly agree to form an independent expert group on valuation with an independent chair, involving academics and pension professionals, and liaising with USS.

The objective will be to inform the next USS valuation and therefore will be completed by the end of 2019.

The group will consider issues of methodology, assumptions and monitoring, aiming to promote greater transparency and understanding, and will take account of the real strengths, sustainability and viability of the scheme.

Risk sharing alternatives

The agreement on benefits noted above is transitional for the period of this valuation (from 1 April 2019 to 31 March 2022). Recognising this both UCU and UUK agree to work together to explore alternative options for the future of the scheme. The consideration of any alternative would include the potential impact on recruitment and retention, with a view to reviewing the different provision within the sector. The focus of this work will be to develop alternative ways of risk sharing, in line with CDC, seeking to maintain and develop members’ confidence in the scheme. This will also include work with Government so that suitable statutory underpinning is available to adopt this.35

However, the proposal was rejected by UCU members.36 UCU said:

The overwhelming view of branches was that while the proposal retained defined benefit it did so at too low a level (only the first £42,000 of salary and that the proposed reduction in accrual rate was also unacceptable. Branches were also clear that the refusal of the employers to shift their position on taking more risk was disappointing.37

UUK expressed its disappointment:

It is hugely disappointing that students' education will be further disrupted through continued strike action.

We have engaged extensively with UCU negotiators to find a mutually acceptable way forward. The jointly developed proposal on the table, agreed at ACAS, addresses the priorities that UCU set out.

We have listened to the concerns of university staff and offered to increase employer contributions to ensure that all members would receive meaningful defined benefits.

We recognised concerns raised about the valuation and have agreed to convene an independent expert valuation group.

34 Ibid 35 Ibid 36 UCU press release, 13 March 2018 37 Twitter: UCU strike 13 March 2018

Our hope is that UCU can find a way to continue to engage constructively, in the interests of students and those staff who are keen to return to work.38

On 14 March, it said it was “consulting with the scheme’s employers to get their views on the joint proposals developed at ACAS” and planned “more, urgent talks with UCU to end the dispute.”39

4.4 Proposal for a joint expert panel - 23 March 2018

On 23 March 2018, UUK and UCU proposed to jointly establish a panel of independent experts to review the USS valuation, processes and assumptions and to agree key principles to underpin the future joint approach to the valuation of the USS fund. Its work would reflect the clear wish of staff to have a “guaranteed pension comparable with current provision whilst meeting the affordability challenges for all parties within the current regulatory framework.” It would “require maintenance of the status quo in respect of both contributions into USS and current pension benefits, until at least April 2019.”40

Sally Hunt said substantial concessions had been made:

UCU has been trying to challenge the valuation methodology employed by USS for years. Now we have an independent review and the status quo in pension arrangements while it makes its deliberations. We also have a commitment from the employers to provide a guaranteed 'defined benefit' pension for the foreseeable future, even if there are future ups and downs in the fund, and a recognition from the employers of the importance of this guarantee in retirement to UCU members. 41

On 13 April, the UCU announced that its members had voted by 64% to 36% on a turnout of 63.5% to support the establishment of a Joint Expert Panel to examine the USS 2017 valuation:

The result was as follows:

Total balloted: 53,415 Total votes cast: 33,973 Total number valid votes: 33,913 Turnout: 63.5%

Yes to accept the UUK offer 21,683 (64%)

No to reject the UUK offer 12,230 (36%)

This represents the highest turnout in any national ballot or consultation of any kind in UCU's history.

Industrial action would be suspended but the union would keep its “legal strike mandate live until the agreement between UCU and UUK is noted by USS.”42

38 UCU rejects proposals jointly agreed at ACAS, 13 March 2018 39 UUK planning more talks with UCU to end pensions dispute, 14 March 2018 40 UUK, Joint Expert Panel proposed, 23 March 2018 41 Latest UUK proposal: your questions answered, 26 March 2018 42 Members vote to accept employers’ latest offer, 13 April 2018

The UUK said the review would build confidence and increase transparency:

Reviewing the methodology and assumptions in the current valuation will build confidence, trust and increase transparency in the valuation process. It will provide an opportunity to consider the questions raised about the valuation by scheme members and employers. It is important that interested parties engage with the panel and remain open-minded about its possible findings.

It would work with UCU to appoint a jointly agreed chair for the panel as soon as possible, before developing its terms of reference, order of work and timescales.43

4.5 Questions in Parliament On 22 December 2017, Universities Minister, Jo Johnson said the Government had no role in relation to the USS:

Universities are autonomous institutions and they are responsible for their own pension provision. Government has no role in relation to the Universities Superannuation Scheme (USS) beyond regulation as is applied to all workplace pension schemes by The Pensions Regulator. Neither my Rt hon. Friend the Secretary of State nor the Minister of State for Universities, Science, Research and Innovation has discussed the USS with Universities UK (UUK) or the University and College Union. Officials have sought updates from UUK on the latest developments regarding the USS. These were informal discussions and there were no outcomes.44

The then Work and Pensions Secretary David Gauke said:

Any changes that might be made to this scheme are a matter for the scheme’s joint negotiation committee, not for the Government. The independent Pensions Regulator remains in ongoing discussion with the USS’s stakeholders. Nothing has been brought to the DWP’s attention that we consider to be of concern. It would be improper for the Government to tell the joint negotiation committee how to run the scheme.45

An Early Day Motion in the name of Carol Monaghan, with 65 signatures, says:

That this House recognises that academic staff in universities make a vital contribution to ensuring the supply of skilled graduates to UK businesses; believes all staff working in universities should have access to a secure and decent pension; notes with concern the proposal by Universities UK to close the defined benefit portion of the Universities Superannuation Scheme (USS) to all future service; further believes this would significantly reduce the security of retirement income for academic staff in many UK universities, making careers in those institutions less attractive; and calls on the Government to review the current situation and urge Universities UK to work with University and College Union to find a better solution which ensures that USS remains competitive compared with pensions

43 UUK, Ballot result on Joint Expert Panel, 13 April 2018 44 PQ 119989, 22 December 2017 45 HC Deb 18 December 2017 c740

offered to other education staff and those in other professional occupations.46

On 12 March 2018, Universities Minister, Sam Gyimah said the Government had no plans to underwrite the USS:

Dan Jarvis: To ask the Secretary of State for Education, what assessment his Department has made of potential merits of indemnifying the Universities Superannuation Scheme against university bankruptcy.

Sam Gyimah: The Universities Superannuation Scheme (USS) is a private pension scheme, and government has no role in relation to the USS beyond regulation as applied to all work-based pension schemes by The Pensions Regulator.

The government has no plans to underwrite the USS, which is one of the country’s largest pension schemes. It has nearly 400,000 members, along with sizable assets and liabilities. The cost to the taxpayer of underwriting such a scheme could be significant, and any further government involvement in supporting the scheme would need to be considered very carefully.

The government remains concerned about the impact of industrial action called in response to proposed reforms to the USS. I have spoken with both Universities UK and the University and College Union to encourage them to continue to talk, as this is the most appropriate route towards resolving the dispute.47

46 Early day motion 619, 29 November 2017 47 PQ 131152, 12 March 2018

About the Library The House of Commons Library research service provides MPs and their staff with the impartial briefing and evidence base they need to do their work in scrutinising Government, proposing legislation, and supporting constituents.

As well as providing MPs with a confidential service we publish open briefing papers, which are available on the Parliament website.

Every effort is made to ensure that the information contained in these publicly available research briefings is correct at the time of publication. Readers should be aware however that briefings are not necessarily updated or otherwise amended to reflect subsequent changes.

If you have any comments on our briefings please email [email protected]. Authors are available to discuss the content of this briefing only with Members and their staff.

If you have any general questions about the work of the House of Commons you can email [email protected].

Disclaimer This information is provided to Members of Parliament in support of their parliamentary duties. It is a general briefing only and should not be relied on as a substitute for specific advice. The House of Commons or the author(s) shall not be liable for any errors or omissions, or for any loss or damage of any kind arising from its use, and may remove, vary or amend any information at any time without prior notice.

The House of Commons accepts no responsibility for any references or links to, or the content of, information maintained by third parties. This information is provided subject to the conditions of the Open Parliament Licence.