University of Melbourne 1 Funding Australia’s Future: From where do we begin? & Implications for Mutual ADIs Kevin Davis Professor of Finance, University of Melbourne Research Director, Australian Centre for Financial Studies (and Professor, Monash University)

Transcript

University of Melbourne 1

Funding Australia’s Future:From where do we begin?

& Implications for Mutual ADIs

Kevin Davis

Professor of Finance, University of Melbourne

Research Director, Australian Centre for Financial Studies (and Professor, Monash University)

University of Melbourne 2

Background and Objectives

• Funding Australia’s Future project at ACFS– Identify possible developments in demand

for and supply of finance– Implications for financial flows and financial

sector structure– Impediments to efficient financing

• Stage 1: three background papers– Release July 10, Sydney Conference Aug 7

• Stage 2: further commissioned studies on specific topics

University of Melbourne 3

Rationale and Issues

• Financial sector in continual state of evolution– Adjusting to technology, regulation,

changing pattern of real sector demand & supply of finance

• Future development will be influenced by current situation and recent trends

• What does Australian financial sector look like (vis a vis others) and why?

• Are recent trends transitory or long-lasting?• What are some scenarios?

– & policy and strategy issues

University of Melbourne 4

Session Overview

1. Major Post GFC changes

2. Special Characteristics of the Australian Financial Sector

3. Future-gazing

4. Mutual ADI issues

University of Melbourne 5

Post GFC Changes

• Initial table discussion• Identify 4-5 of the major changes in financial

trends post the GFC, whether they are likely to be permanent or transitory, and implications

• These could include aspects of: financial flows / patterns of financing; sectoral (household, corporate, govt, international) balance sheets; financial products; financial sector prices; financial sector structure; etc

• (We’ll then discuss and compare with my list)

University of Melbourne 6

1. Financial sector growth relative to GDP has ceased

Both activity level and asset valuation effects are relevant

* Table excludes assets of SMSF

Financial Institution Assets / GDP

1997 2007 2008 2009 2010 2011 20120.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Securitisation Vehicles

General Insurance

Managed Funds

Superannuation

Life Offices

Registered Financial Corporations

ADIs

University of Melbourne 7

1. Financial sector growth relative to GDP has ceased (cont.)

Year*

1979 4.70%

1985 5.04%

1990 6.38%

1995 6.85%

2000 8.05%

2005 9.37%

2006 10.03%

2007 10.65%

2008 10.27%

2009 10.06%

2010 10.22%

2011 10.13%

2012 10.27%

Finance & Insurance: contribution to Gross Value Added

3 year spread (Government Bond less Term Deposit: Average overQuarter)

3 month spread (Bank Bill less Term Deposit: Average over Quarter)

With the result that…

University of Melbourne 15

6. Increasing scale and leverage of household balance sheets has paused

scaleleverage

Debt/ Assets

Housing Debt/

Housing Assets

Debt/ Income*

Total Assets/ Income

Financial Assets/ Income

Interest Payments/

Income

Housing Interest

Payments/ Income

Jun-1987 8.7 11.9 43.3 430.1 169.1 7.6 5.2

Jun-1997 11.6 18.6 74.7 560.4 222.0 6.1 4.7

Jun-2007 16.1 25.8 153.5 841.1 350.6 11.3 9.2

Jun-2008 17.1 26.9 150.9 787.6 318.3 13.1 10.8

Jun-2009 18.4 29.6 146.1 714.7 288.7 9.0 7.2

Jun-2010 17.3 26.9 152.2 783.8 302.1 11.1 9.0

Jun-2011 17.7 28.3 150.1 743.7 296.2 11.5 9.4

Jun-2012 18.2 30.0 148.0 723.6 299.2 10.4 8.5

University of Melbourne 16

Household financial asset composition changed

Deposits Shares Super/LifeUnfunded Super Other

Sep-90 29% 10% 36% 13% 11%

Sep-00 19% 19% 44% 9% 9%

Sep-07 15% 27% 46% 6% 5%

Sep-12 22% 16% 46% 11% 5%

University of Melbourne 17

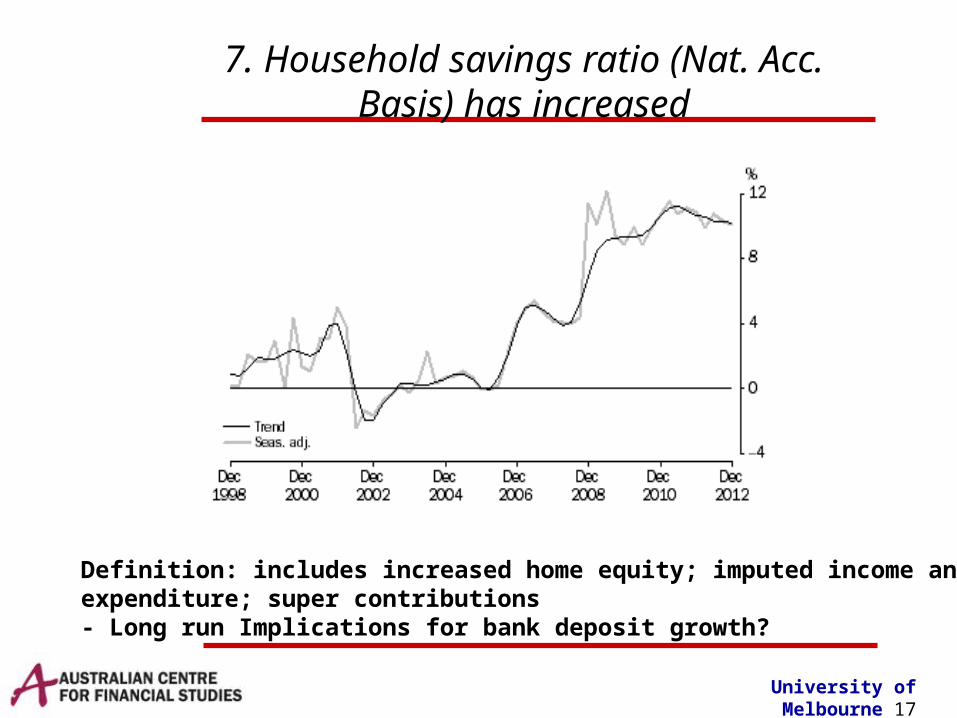

7. Household savings ratio (Nat. Acc. Basis) has increased

Definition: includes increased home equity; imputed income andexpenditure; super contributions - Long run Implications for bank deposit growth?

University of Melbourne 18

Change in household financial position

Jun-89 Jun-93 Jun-97 Jun-01 Jun-05 Jun-09-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Value Transactions

Source: ABS cat 5230.0 Table 20

Four Quarter Moving Average

University of Melbourne 19

Household Sector: Net transactions:

Jun-90 Jun-94 Jun-98 Jun-02 Jun-06 Jun-100

5000

10000

15000

20000

25000

30000

35000

40000

Deposits Super Borrowings

eight quarter moving average

University of Melbourne 20

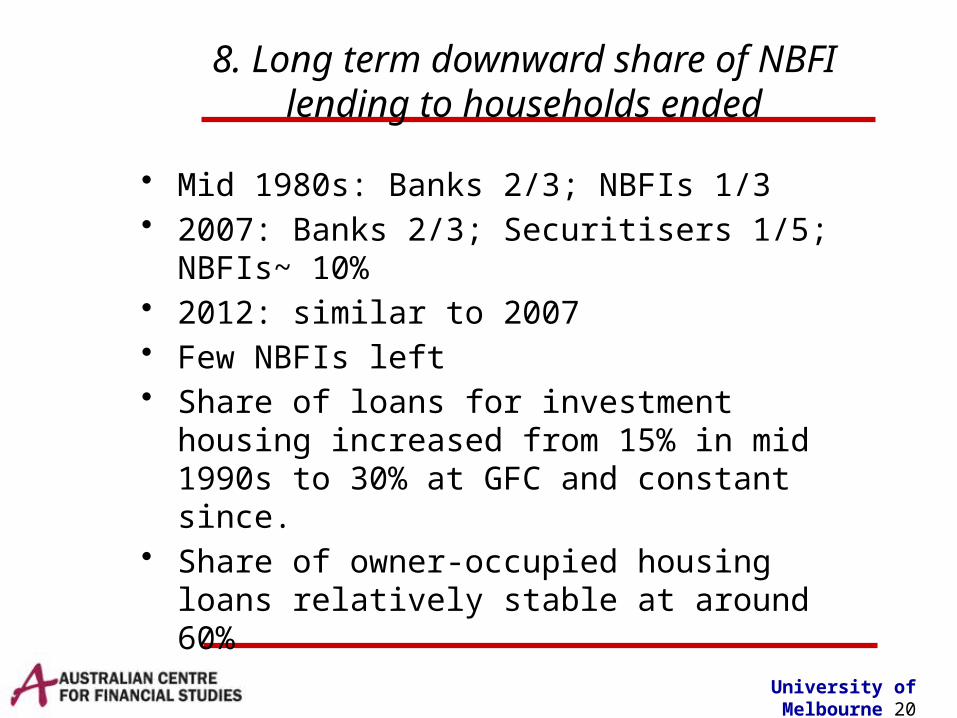

8. Long term downward share of NBFI lending to households ended

• Mid 1980s: Banks 2/3; NBFIs 1/3• 2007: Banks 2/3; Securitisers 1/5; NBFIs~ 10%• 2012: similar to 2007• Few NBFIs left• Share of loans for investment housing increased

from 15% in mid 1990s to 30% at GFC and constant since.

• Share of owner-occupied housing loans relatively stable at around 60%

University of Melbourne 21

9. Gradual decline in corporate leverage in the decades prior to the GFC ceased

Liabilities = Debt + Market Value of Equity

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

Gross Leverage (Debt/Total Liabilities)

Net Leverage (Debt - Financial assets)/(Total Liabilities - Financial Assets))

University of Melbourne 22

10. Increase in net funding of the business sector by households and the ROW relative to financial sector

Inter Sectoral Net Financial Claims ($billion, at September) Net financial claims of On 2002 2007 2012 Household Non-Financial Corporations 87 219 357 Rest of World Non-Financial Corporations 223 383 613 Financial Corporations Non-Financial Corporations 354 862 677

Recent RBA research: large business gross saving by foreign owned minersRetained earnings count as income debits on BOP current a/cCorresponding (offsetting) capital inflow creditBanks have ceased to be main vehicles for funding BOP

University of Melbourne 23

14. Finance Sector Funding of BOP declined

Finance & Insurance Share of International Liabilities

0.46

0.48

0.5

0.52

0.54

0.56

0.58

0.6

2007 2008 2009 2010 2011 2012

Source: ABS 5302 Table 84

University of Melbourne 24

11. Corporate accumulation of financial assets slowed markedly after the GFC

• Corporate sector holdings of financial assets– increased 13.2% p.a. over 2002 – 2007– increased 3.1% p.a. 2007 - 2012

• Main changes– share holdings: -5.1 % p.a. v 12.1% p.a

(partly valuation effects)– accounts receivable growth slowed from

17.3% to 4.3% p.a.

University of Melbourne 25

12. Decline in Government Debt/GDP over the prior decade was reversed

Government Lending/GDP

-8.00-6.00-4.00-2.000.002.004.00

1997 2002 2007 2012

Pe

rce

nta

ge

Federal Govt Federal Authorities

State Govt State Authorities

University of Melbourne 26

13. Increased holdings of Federal Govt debt by the ROW.

• Table Discussion• In what ways does the Australian financial

system differ from those found in other advanced economies? Are there any implications for business opportunities, risks etc for ADIs

• Differences could relate to types of institutions; financial markets; financial products; demand, supply and allocation of finance; etc

University of Melbourne 28

Current Features of Australian Financing Patterns

1. banks and superannuation funds dominate the financial sector, holding approximately ¾ of financial sector assets.• relatively few financial assets held by non-prudentially

Relative to GDP, Australia’s domestic bond market is of comparable size to most other OECD countries

Private Debt Securities/GDP: 2010

0.0020.0040.0060.0080.00

100.00120.00140.00160.00180.00200.00

Austra

lia

Austri

a

Belgium

Canada

Denmar

k

Finlan

d

Franc

e

Germ

any

Hong K

ong S

AR, Chin

a

Icela

nd

Irelan

d

Japa

n

Luxe

mbo

urg

Nether

lands

Norway

Singap

ore

Sweden

Switzer

land

United K

ingdom

United S

tate

s

But few non-financial corporate issues

University of Melbourne 33

The Australian banking sector is of comparable size to that of other OECD countries

• bank assets/GDP = 131.4 in 2010 versus median bank assets/GDP = 130.9 for the OECD). – (There is significant dispersion in this

measure with the USA = 64.6 and the UK = 202.6).

• Similarly bank deposits/GDP of 98.8 (a lower figure reflecting the role of wholesale and equity funding of assets) is close to the OECD median

University of Melbourne 34

But “Bloody Big Building Societies”

Residential real estate loans to total loans

Commercial real estate loans to total loans

Australia 62.7 9.7 Canada 34.7 2.9 China 15.8 6.8 Germany 16.7 5.7 Ireland 29 15.5 Italy 18.7 8.8 Korea 21.8 20.6 Norway 41.4 2 Portugal 32.9 10.4 South Africa 32.8 9.5 Switzerland 33.6 6.8 UK 16.2 3.6 USA 35.6 15.8

University of Melbourne 35

Household sector a net borrower from banks.

• Bank deposits $660 bill; loans from banks $1,130 bill.• Household equity in super and insurance $1,491 billion• shares in financial corporations $151 billion, prepaid

insurance premiums $54 billion. • Loans from securitisers $310 billion; loans from other

depository corporations $100 billion. • Net claims on financial corporations overall (incl. super)

of around $857 billion.• Since 1990s share of financial assets in household total

assets has been relatively stable (37 to 42 per cent)– increased value of superannuation assets largely

matched by increased valuations of housing.

University of Melbourne 36

Aggregate Household balance sheet not unusual by international standards

Household Assets and Liabilities (relative to Disposable Income)

0

100

200

300

400

500

600

700

Non Financial Assets

Financial Assets

Debt

Sources: OECD Economic Outlook No. 92 (database); RBA Bulletin

University of Melbourne 37

Low Corporate Leverage

University of Melbourne 38

Limited Corporate Use of Debt Capital Markets

Corporate Liabilities

0.0

0.5

1.0

1.5

2.0

2.5

2006 2007 2008 2009 2010 2011 2012

Year (Sept)

$ T

rilli

on

bills of exchange One name paper Bonds, etc.

Loans and placements Shares and other equity

University of Melbourne 39

Low Government Debt/GDP

Country Gross Government Debt /GDP 2012AUS 27CAN 88CHN 22DNK 47FRA 90DEU 83ITA 126JPN 237KOR 33ESP 91GBR 89USA 107

University of Melbourne 40

Finance and Insurance Sectors: Share of Gross Value Added

Year Gross Value Added

Australia 2010 10.6%

Canada 2008 6.6%

France 2011 4.7%

Germany 2011 5.2%

Italy 2011 5.4%

UK 2011 8.3%

USA 2012 7.9%

Figures – treat with caution, but…Explanations?

University of Melbourne 41

Equity Bias in International Investments

Australian foreign financial asset holdings

-

100

200

300

400

500

600

700B

illi

on

Sep-2000 Sep-2004 Sep-2008 Sep-2012

Share of FDI in stock of overseas assets has fallen from over 40% atstart of 2000’s to around 30% (growth of superfund portfolio investment)

University of Melbourne 42

Significant Financing by Rest of World

External Financial Liabilities and Assets

0

500000

1000000

1500000

2000000

2500000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Australian financial assets held by ROW

ROW financial assets held by Australia

University of Melbourne 43

Foreign Direct Investment (Stock)

Inward Stock of FDI / Stock Market Capitalization

0% 20% 40% 60% 80% 100% 120%

JapanKorea,

USACanada

MalaysiaUK

BrazilAustralia

FranceSpain

GermanyTaiwan

Italy

University of Melbourne 44

Net Stock of FDI

Net Stock of Inward FDI (USD mill): 2011Largest net recipients G7 (& 7 of 10 largest net providers)China 1440000 Canada -75415Brazil 467084 Italy -179528Mexico 190221 Germany -504464Australia 172790 United Kingdom -532216Indonesia 152427 France -628203Poland 147494 Japan -737005Turkey 112354 United States -1772778Czech Republic 109776Russian Federation 95373India 90475Chile 89128Source: http://www.oecd.org/statistics/

Outward FDI relatively low (but lots of portfolio investment)

University of Melbourne 45

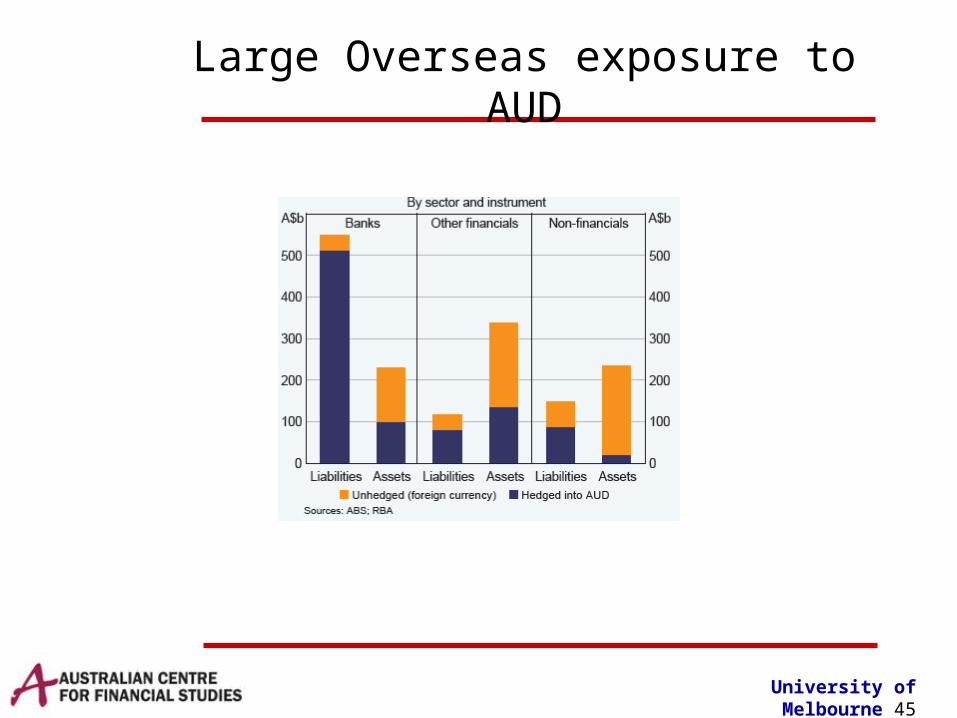

Large Overseas exposure to AUD

University of Melbourne 46

Sector Financial Positions: Dec 2012 ($Trillion)

Owed by to

Assets / liabilitiesInclude equity& debt

University of Melbourne 47

An Overview

• Financial sector not markedly different to others, but:– Household savings flow into super for ultimate

investment– Households major borrowers from banks– Australian companies use less debt– Large ROW financing: was a large role for bank

borrowing– Small Aust. corporate and government bond

market– Large financial sector by developed world

standards

University of Melbourne 48

Thinking about the Future

• GFC provided transitory shock to financing patterns– But unleashed regulatory reform with major

implications for future financing patterns– Took attention away from long term issues

• Financing patterns haven’t fully adapted to implications of compulsory superannuation– Flows of funds, liquidity creation

• Tax system features are a major influence– Incentives for household sector risk taking– Patterns of corporate financing

• Structural changes in financing likely

University of Melbourne 49

Financial System Structure “Lagging”

• Superannuation has “re-routed” financial flows– Household savings increasingly fund securities

investments, not lending and real sector project assessment (or the creation of securities)

– Some credit / project risk appraisal by super funds and new security creation - commercial property, infrastructure.• Should there be more (super & home

mortgages?)• What are consequences of increasing ownership of

national capital stock by super for: achievable returns, innovation & entrepreneurship, capital stock growth?

University of Melbourne 50

Financial System Structure “Lagging”

• Long-term household portfolio balance

– Short run dynamics complicated: deposits = money• Banking sector still focused on “liquidity creation” (eg LT

housing loans, ST deposits)– Even though large stock of illiquid savings exists

(super)– Basel 3 “penalizing” bank liquidity creation

• Potential Outcomes– Bank funding via superfund investments?

• Deposit and bond products (including for SMSF)– Bank securitisation of assets, loan sales (eg

syndications)• But level of credit risk assessment skills outside

banks?– Less “commercial” more “investment” banking

• Corporate bond, equity issuance underwriting• Logic of deposit guarantees for universal banks?

– Bank structure implications?– Superfund involvement in asset creation

• Joint ventures with experts in risk assessment• In house risk assessment capabilities

University of Melbourne 53

Infrastructure Investment

• Large stock of long term savings (super) available, but:– “Greenfields” project risk (and tender costs)

• PPPs not the answer: How best to share risks?– Should government bear demand (but not

construction) risk?– “Tranching” claims and risk (securitisation)?– Pooling risk of many projects?

– “Brownfields” risk and illiquidity• Liquid claims on illiquid assets can be created • Investment structures enabling diversification• But low expected returns on low risk projects?

University of Melbourne 54

A super tax conundrum

• Dividend Imputation• Tax concessions for super• Both

– Particularly zero tax rate concessions

If all Australian equities are held by zero tax rate investors, corporate tax revenue is effectively zero – a growing Federal Budget problem!

University of Melbourne 55

Corporate Bond Market Development

• Super growth suggests demand side should be there• Basel 3 incentives for debt capital markets v on-balance

sheet lending - securitisation, corporate debt finance• Government initiatives for easier issuance• But

– Imputation: no tax bias to debt v equity funding• Except for foreign owned companies

– Investor ability to assess credit risk– Investor ability to diversify credit risk– Investor “equity bias” – imputation and capital gains

tax concession – is it super equity bias excessive?– Bank bond issues are competition

• But tendency to be “non-vanilla” (to qualify as regulatory capital)

– Financial Claims Scheme - risk free alternative

University of Melbourne 56

BOP Funding & Financial Market Development

• If less bank funding of current account deficit– More portfolio and FDI investment inflow

• Including govt debt purchases• Retained earnings of foreign owned cos.

– One of the largest net FDI recipients• Is imputation a disincentive to offshore expansion?

• Unlike domestic firms, foreign owned firms have tax incentives for debt financing– Either in domestic or offshore capital markets

University of Melbourne 57

Some Policy Issues: Financing Inadequacies

• Popular concerns (but not “evidence based”)– SME and venture capital– Infrastructure– Real estate investment bias– Retirement savings products– Equity bias– Banking competition, profits, systemic risk– Corporate bond market absence– “Too much finance”

University of Melbourne 58

Some Policy Issues: regulation and risk bearing

• What perimeter for prudential regulation?• Currently relative few assets held by non-

prudentially regulated financial institutions– Overseas interest in “ring fencing”

• But: Basel 3 should increase supply of capital market assets; demand from SMSF growth; incentives for advisers, product creators

• Personal loan markets– Credit reporting, alternative lenders

• Mortgage markets– Securitisation, new lenders / originators

• Financial advice, transactions services

University of Melbourne 60

Conclusion

• Structural changes in financial sector inevitable– Patterns of financial flows have changed– Competitive advantages have changed– Regulation has changed

• Real sector adjustments also relevant– Industry sector changes – potentially different

– Demography – demand for financial products– Income distribution – implications of open economy

and low cost international competition for “low skilled” employees

University of Melbourne 61

Conclusion: Mutual ADI future

• What competitive advantages for mutual ADIs?• Financial sector functions are: overcoming information

problems, reducing transactions costs, providing diversification and risk management services, transferring financial resources between individuals (lending / borrowing) and over time (wealth management), enabling payments

• Technology has radically changed information flows, transactions costs, creation of alternative financial products and markets etc.

• Maybe few advantages in the technical “production process” of financial services and products

• But ultimately dealing with individuals and their behavioral biases – does mutuality / customer owned banking provide an advantage and if so, how?