22

UNLOCKING UNLOCKING THE THE MAGIC OF NUMBERS MAGIC OF NUMBERS 2 = 3-1+ 4 2 -22+3 2 -3 DR. GEORGE WEBSTER EXECUTIVE EDUCATION PHARMACEUTICAL MARKETING ST. JOSEPH’S UNIVERSITY

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 222 times |

| Download: | 2 times |

UNLOCKINGUNLOCKINGTHETHE

MAGIC OF NUMBERSMAGIC OF NUMBERS

2 = 3-1+ 42-22+32-3DR. GEORGE WEBSTER

EXECUTIVE EDUCATION PHARMACEUTICAL MARKETING

ST. JOSEPH’S UNIVERSITY

2

VALUE CREATIONVALUE CREATION IN IN

THE PHARMACEUTICALTHE PHARMACEUTICALINDUSTRYINDUSTRY

•What is value creation?

•What are the drivers of value creation ?

•How do we measure value creation?

3

WHAT IS VALUE CREATION?WHAT IS VALUE CREATION?

• Process

• Involves decision making– Financing

– Investing

– Operating

• Includes all stakeholders

4

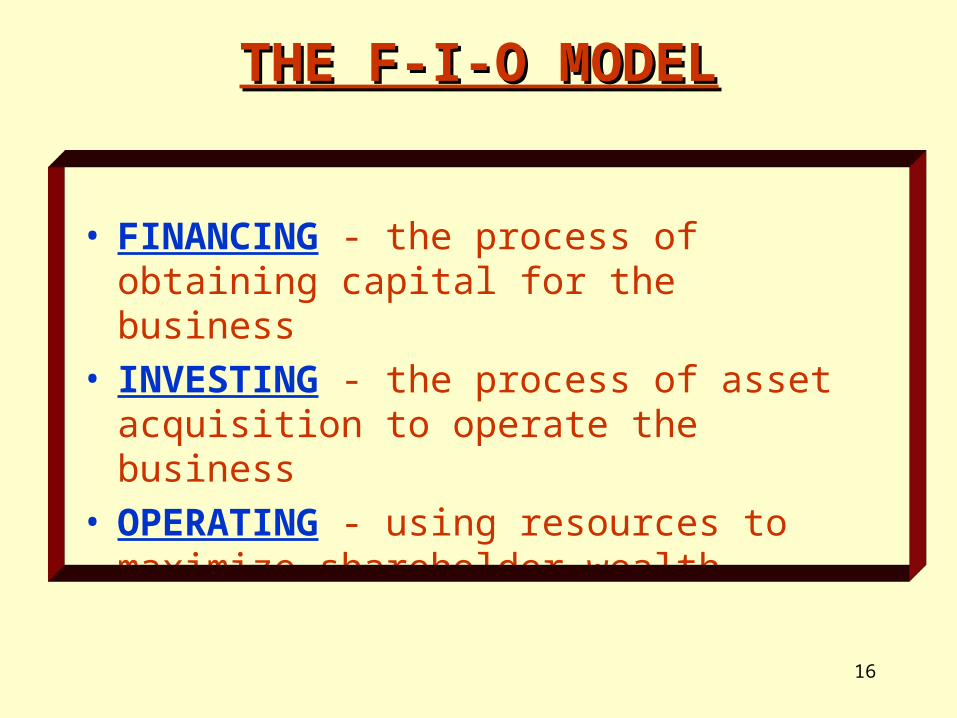

THE F-I-O MODELTHE F-I-O MODEL

• FINANCING - the process of obtaining capital for the business

• INVESTING - the process of asset acquisition to operate the business

• OPERATING - using resources to maximize shareholder wealth

5

““THE SCORECARDS”THE SCORECARDS”

• BALANCE SHEET - a statement of position at a point in time– Shows what we own and what we owe

– Of particular interest to the CFO

• INCOME STATEMENT - a statement of value creation over time– Measures how well we operated

– Of particular interest to the CEO

• CASH FLOW STATEMENT - puts operations on a cash basis– Gives sources and uses of cash

– Of particular interest to the COO

6

BALANCE SHEET- FACSIMILE COMPANY DECEMBER 31, 19XX

ASSETS LIABILITIES & O.E.CURRENT ASSETS CURRENT LIABILITIES Cash 3000 Accts. Payable 2000 Accts. Rec. 2000 Wages Payable 1000 Inventory 8000 13000 Rent 1000 4000

LONG TERM LONG TERM P & E 25000 Long Term Debt 7000 Other 4000 OWNER’S EQUITYTOTAL 29000 Common Stock 5000 Ret. Earnings 26000 TOTAL 31000

TOTAL ASSETS 42000 TOTAL LIAB. & OE 42000

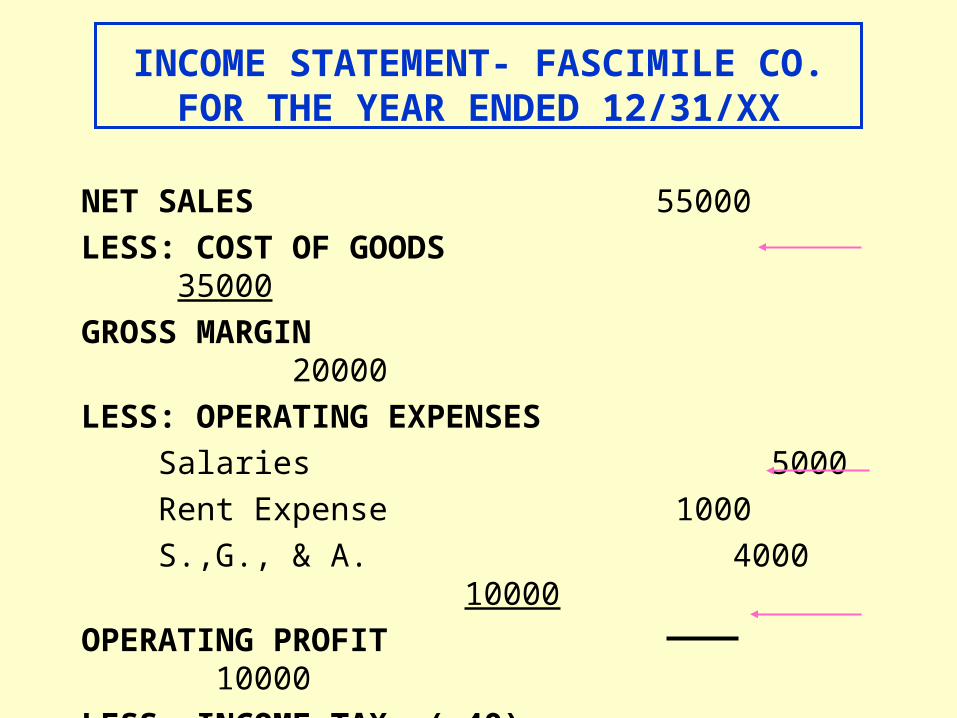

INCOME STATEMENT- FASCIMILE CO.FOR THE YEAR ENDED 12/31/XX

NET SALES 55000

LESS: COST OF GOODS 35000

GROSS MARGIN 20000

LESS: OPERATING EXPENSES

Salaries 5000

Rent Expense 1000

S.,G., & A. 4000 10000

OPERATING PROFIT 10000

LESS: INCOME TAX (.40) 4000

NET INCOME AFTER TAX 6000

STATEMENT OF CASH FLOWS-FASCIMILE CO.

FOR THE YEAR ENDED 12/31/XX

•CASH FROM OPERATIONS

Net Income 2000

Depreciation 500 2500

•CASH FROM INVESTING ACTIVITIES

Capital Expenditures 5000

Acquisitions 15000 20000

•CASH FROM FINANCING ACTIVITIES

Issuance of Long Term Debt 700

Sale of Common Stock 11500

Cash Dividends 400 11800

•NET CHANGE IN CASH -5700

9

WHAT ARE THE DRIVERS OF WHAT ARE THE DRIVERS OF VALUE?VALUE?

• EFFECTIVENESS - How much revenue do we generate from the assets we have?

• EFFICIENCY - How well do we use the assets we own?

• LEVERAGE - How much debt do we have in the capital structure?

10

EFFECTIVENESSEFFECTIVENESS

EFFECTIVENESS =Total SalesTotal Assets

BMS -1998 =$18,284,000,000$16,272,000,000

BMS - 1998 Effectiveness is 1.12

BMS - 1996 Effectiveness is 1.03

11

EFFICIENCYEFFICIENCY

EFFICIENCY =Net IncomeTotal Sales

BMS -1998 = $3,052,000,000$18,284,000,000

BMS - 1998 Efficiency is .167

BMS - 1996 Efficiency is .187

12

LEVERAGELEVERAGE

LEVERAGE = Total AssetsOwner’s Equity

BMS -1998 =$16,272,000,000$7,576,000,000

BMS - 1998 Leverage is 2.15

BMS - 1996 Leverage is 2.24

13

HOW WE MEASURE VALUE HOW WE MEASURE VALUE CREATIONCREATION

• ROI - Return on investment

• ROE - Return on equity

• EPS - Earnings per share

• EVA - Economic value added

14

RETURN ON INVESTMENTRETURN ON INVESTMENT

RETURN ON INVESTMENT = Net IncomeTotal Assets

ROI =Net Income

SalesX

Sales

Total Assets

ROI = Net Margin X Asset Turnover

BMS 1998 ROI = .167 X 1.12 = .187

BMS 1996 ROI = .187 X 1.03 = .193

15

RETURN ON EQUITYRETURN ON EQUITY

RETURN ON EQUITY = Net IncomeOwner’s Equity

(Effectiveness) X (Efficiency) X (Leverage)

Total Assets

Owner’s Equity

Sales

Total AssetsX

Net Income

SalesX

BMS 1998 ROE = $3,052,000,000 / $7,576,000,000 = .40

= 1.12 X .167 X 2.15 = .40

16

THE F-I-O MODELTHE F-I-O MODEL

• FINANCING - the process of obtaining capital for the business

• INVESTING - the process of asset acquisition to operate the business

• OPERATING - using resources to maximize shareholder wealth

17

(Effectiveness) X (Efficiency) X (Leverage)

HOW WE MEASURE VALUE HOW WE MEASURE VALUE CREATIONCREATION

Total Assets

Owner’s Equity

Sales

Total AssetsX

Net Income

SalesX

Investing Operating Financing

FIO MODELFIO MODEL

(Asset Turnover) X (Net Margin) X (Degree Financial Leverage)

18

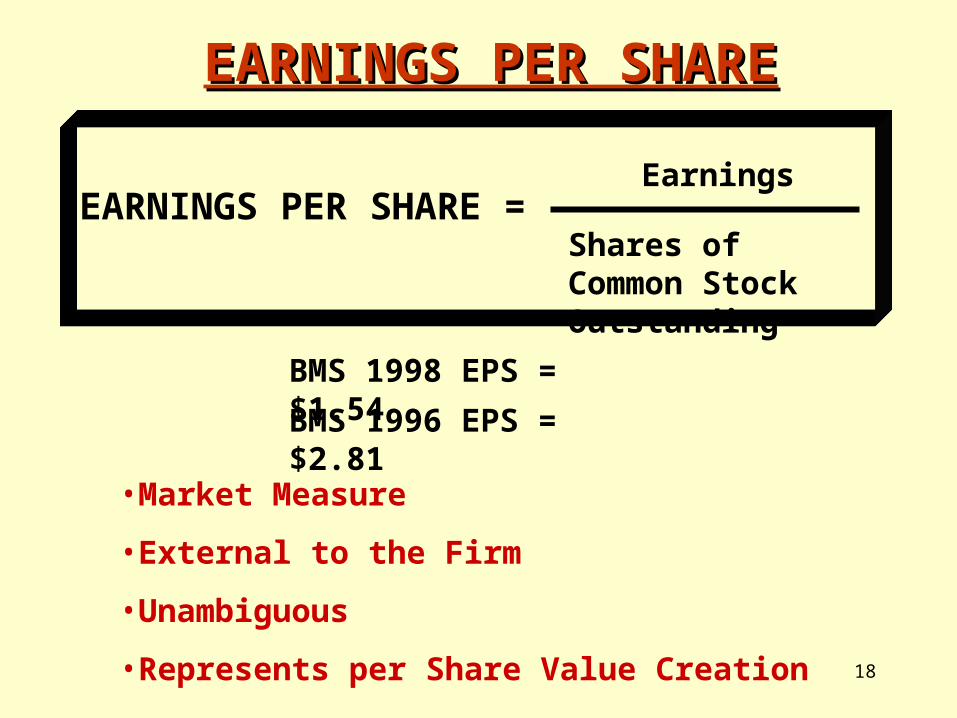

EARNINGS PER SHAREEARNINGS PER SHARE

EARNINGS PER SHARE =Earnings

Shares of Common Stock Outstanding

BMS 1998 EPS = $1.54

BMS 1996 EPS = $2.81

•Market Measure

•External to the Firm

•Unambiguous

•Represents per Share Value Creation

19

ACTIVITY/PERFORMANCE/ACTIVITY/PERFORMANCE/LEVERAGE MEASURESLEVERAGE MEASURES

BMS SCHERING P&G

ACTIVITY

Total Asset Turnover 1.12 1.03 1.20

PERFORMANCE

Net Margin (%) 16.7 21.7 10

Return on Equity (%) 40 44 31

LEVERAGE

Total Assets/ Equity 2.15 1.96 2.53

20

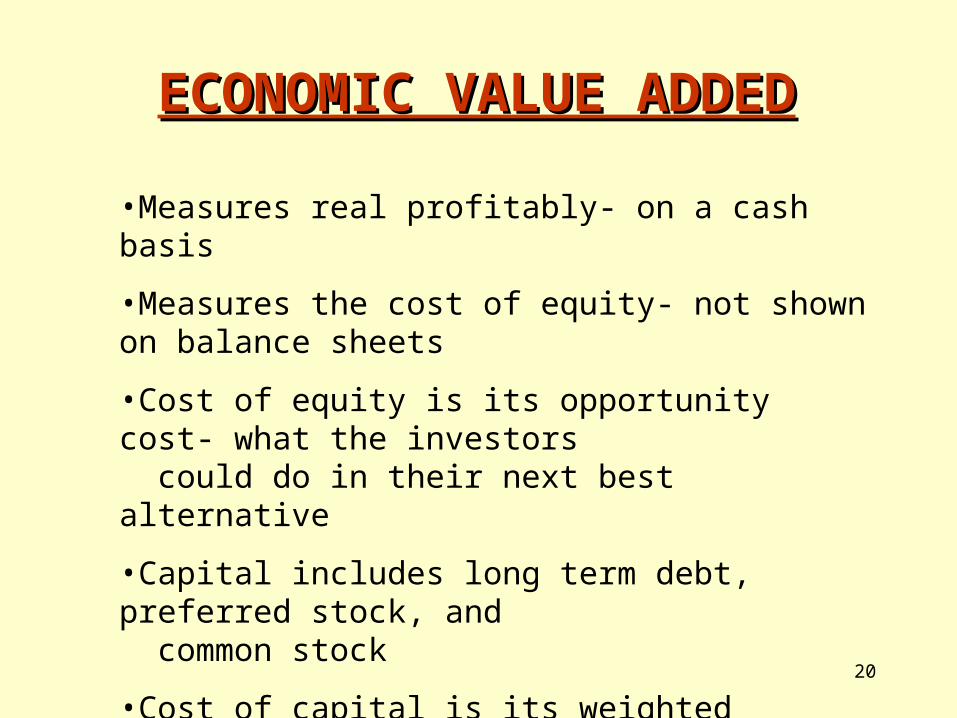

ECONOMIC VALUE ADDEDECONOMIC VALUE ADDED

•Measures real profitably- on a cash basis

•Measures the cost of equity- not shown on balance sheets

•Cost of equity is its opportunity cost- what the investors

could do in their next best alternative

•Capital includes long term debt, preferred stock, and common stock

•Cost of capital is its weighted average

21

ECONOMIC VALUE ADDEDECONOMIC VALUE ADDED

ECONOMIC VALUE ADDED =[Net Operating Profit After Tax - After Tax Dollar Cost of

Capital]

Net Operating Profit After Tax = Operating Profit - Income Tax

Cost of Capital = Weighted After Tax Cost of Capital

Capital = Total Capital Employed = Common and Preferred Stock + Long Term Debt

After Tax Dollar Cost of Capital= Cost of Capital (%) X Capital

22

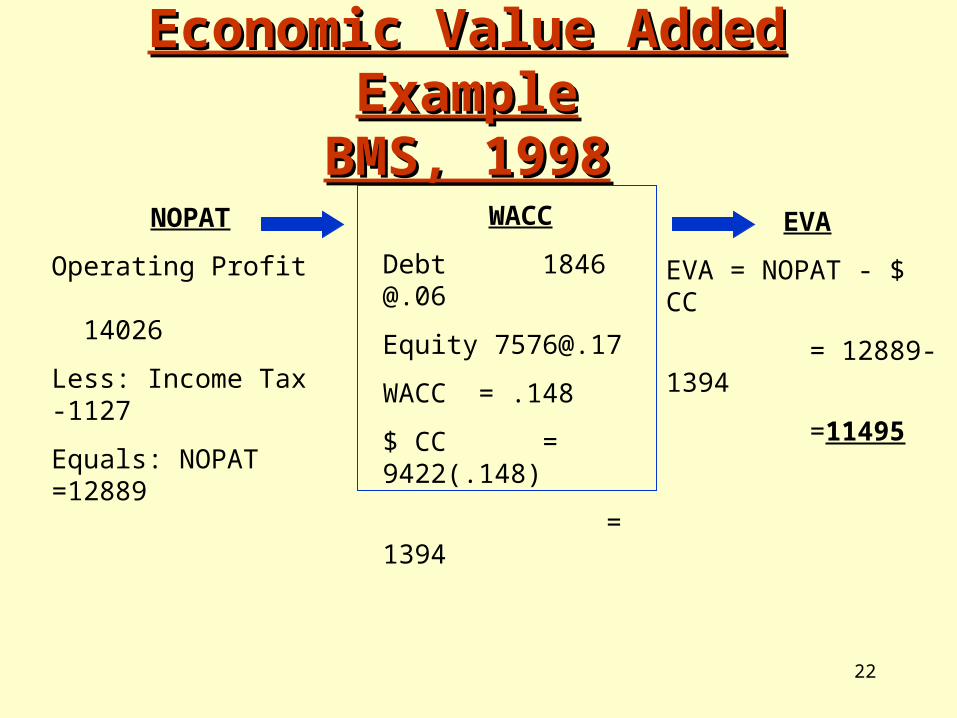

Economic Value Added ExampleEconomic Value Added ExampleBMS, 1998BMS, 1998

NOPAT

Operating Profit 14026

Less: Income Tax -1127

Equals: NOPAT =12889

EVA

EVA = NOPAT - $ CC

= 12889-1394

=11495

WACC

Debt 1846 @.06

Equity [email protected]

WACC = .148

$ CC = 9422(.148)

= 1394

![₪[martin gardner] the magic numbers of dr matrix](https://static.documents.pub/doc/80x56/568cad1f1a28ab186daa633b/martin-gardner-the-magic-numbers-of-dr-matrix.jpg)