35

Loss Prevention, Auditing & Safety Conference 2009 Title Sponsor:

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | wing-clayton |

| View: | 54 times |

| Download: | 0 times |

Loss Prevention, Auditing & Safety Conference 2009 Title Sponsor:

Unlocking the Value of Returns

Speaker Panel

Dr. Read Hayes – Director, Loss Prevention Research Council

Libby Rabun – Vice President, Loss Prevention, AutoZone

Kevin Darnell – Director, Loss Prevention, Brown Shoe

Mark Hilinski – EVP, Strategic Accounts, The Retail Equation

Interactive Question Placeholder

Q1: What retail segment are you?

1. Large format/ Discount/Department

2. Grocery/Drug3. Home

Center/Hardware4. Specialty/Apparel5. Other

Q2: What is your return rate percentage?

1. 0-5 2. 6-10 3. 11-15 4. 16+ 5. Unknown

Presentation of Return Fraud/Abuse Survey Findings

Dr. Read Hayes – Director, Loss Prevention Research Council

Customer Returns In The Retail Industry

Conducted on 2007 data and released in 2008 Survey Objectives

Identify retail industry return rates including: total returns, receipted returns, non-receipted returns, and the various forms of fraudulent and abusive returns as identified by the retailers.

Identify current practices in the retail industry for processing customer returns.

Identify issues related to customer returns that are common among retailers.

Share the results of the survey with the retail industry as a whole.

Key Finding

$15.5 billion annual return fraud and abuse problem

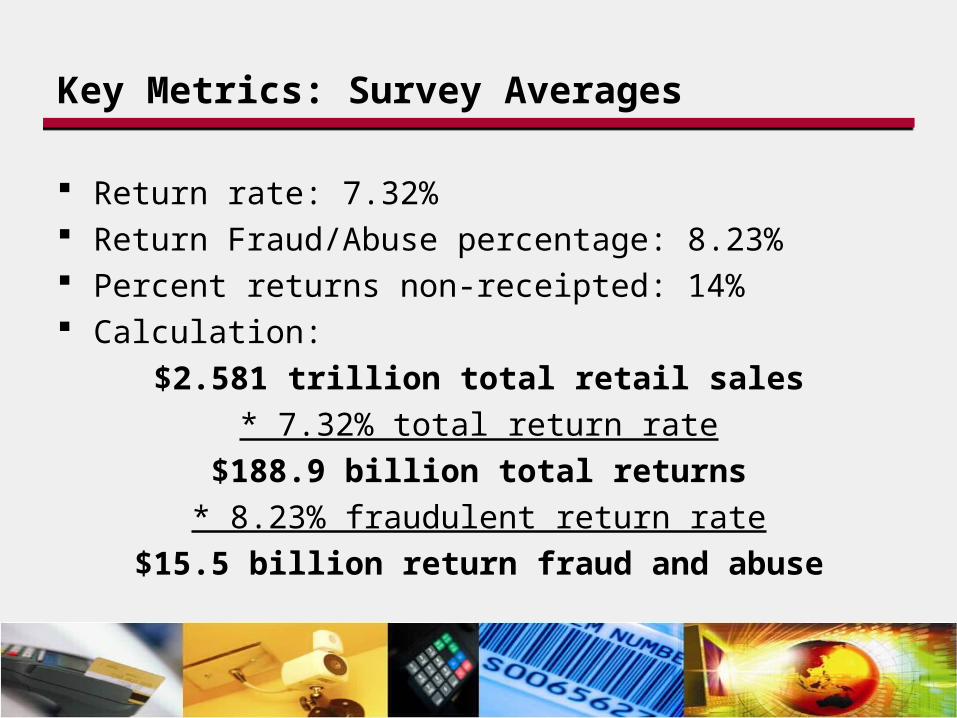

Key Metrics: Survey Averages

Return rate: 7.32% Return Fraud/Abuse percentage: 8.23% Percent returns non-receipted: 14% Calculation:

$2.581 trillion total retail sales* 7.32% total return rate

$188.9 billion total returns* 8.23% fraudulent return rate

$15.5 billion return fraud and abuse

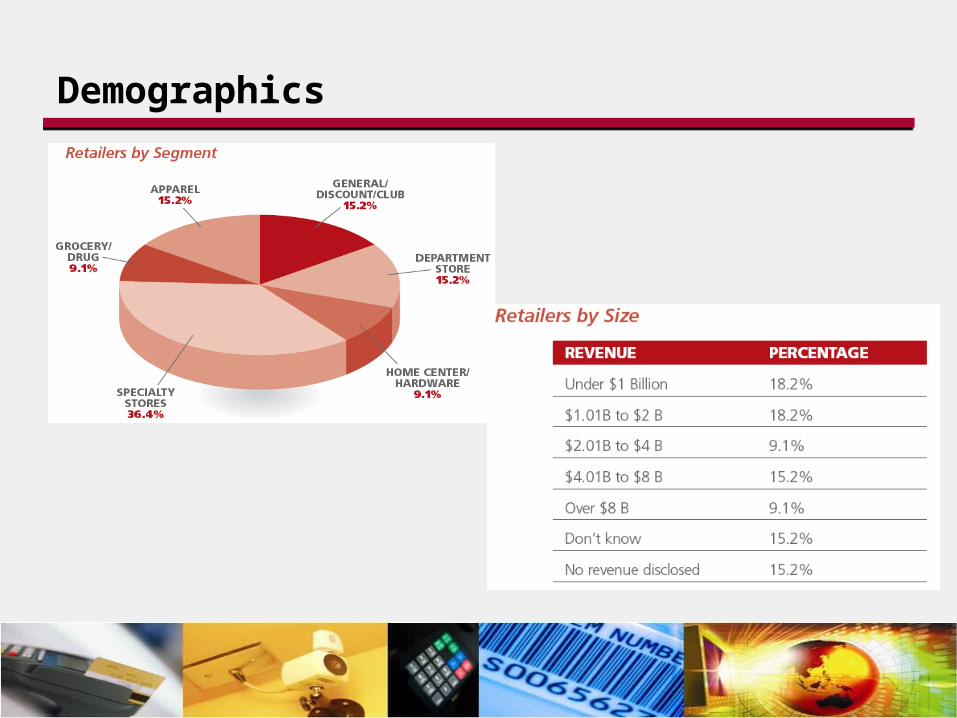

Demographics

Segment Specific Results

Findings: Importance

70% of the respondents indicated that return fraud is an important issue to their company.

The majority of retailers (64%) report that focusing on reducing refund fraud is a high priority.

Almost half of the respondents believe they have the opportunity to achieve return fraud reductions of more than 30%.

Two-thirds of retailers believe that their current return policies and systems are “ineffective” or only “somewhat” effective in deterring return fraud/abuse.

Findings: Receipts

The majority of retailers’ current processes and systems for reducing return fraud continue to focus on non-receipted rather than receipted return transactions.

But, well over half of those surveyed have found forged receipts used in committing return fraud.

This may indicate a trend and closer attention should be paid to the vulnerability of receipted returns.

Industry Trends

Fraudulent and abusive returns are a persistent problem that will likely get worse in this economy

Across the board return policy changes affect good customers as well as problem shoppers

Intelligent solutions are available

Interactive Question Placeholder

Q3: Have you recently changed your return policy in order to address return fraud?

1. Yes, it’s changed 2. Planning to change 3. No 4. Unknown

Q4: With state of the economy, have you observed incidents of return abuse and fraud…

1. Increase2. Decrease3. Remain unchanged

How AutoZone is Addressing Return Fraud and Generating Real Results

Libby Rabun – Vice President, Loss Prevention, AutoZone

At AutoZone, our philosophy is…“Always put Customers First!”

Before: Previous policy provided very limited scrutiny and

controls No ID No receipt required

Warranty data base acts as receipt Stated a 90 day return policy with little

adherence

AutoZone – Returns Management

At AutoZone, our philosophy is…“Always put Customers First!”

During (how did we convince our operations partners): Small pilot program

Delivered proof of concept and initial ROI Internal IT solution with full system integration Consistent, deliberate communication & training

plan Training, signage, brochures Gained and utilized field operators feedback

Continuous analysis Proof is in the numbers

AutoZone – Returns Management

At AutoZone, our philosophy is…“Always put Customers First!”

After: Our philosophy does not change New program began with clearly stated goals:

Reduce overall return rate through Reduced internal related fraud and abuse Reduced external related fraud and abuse

Increase net sales Increase Store Manager satisfaction Ensure consistent following of written returns

policies

AutoZone – Returns Management

At AutoZone, our philosophy is…“Always put Customers First!”

After: We now:

Reserve the right to limit a return regardless of receipt

Ask for ID Ask for receipt

Still use transaction file and warranty data base Use third party to review authorization requests and

respond with approval, warning, or denial response

AutoZone – Returns Management

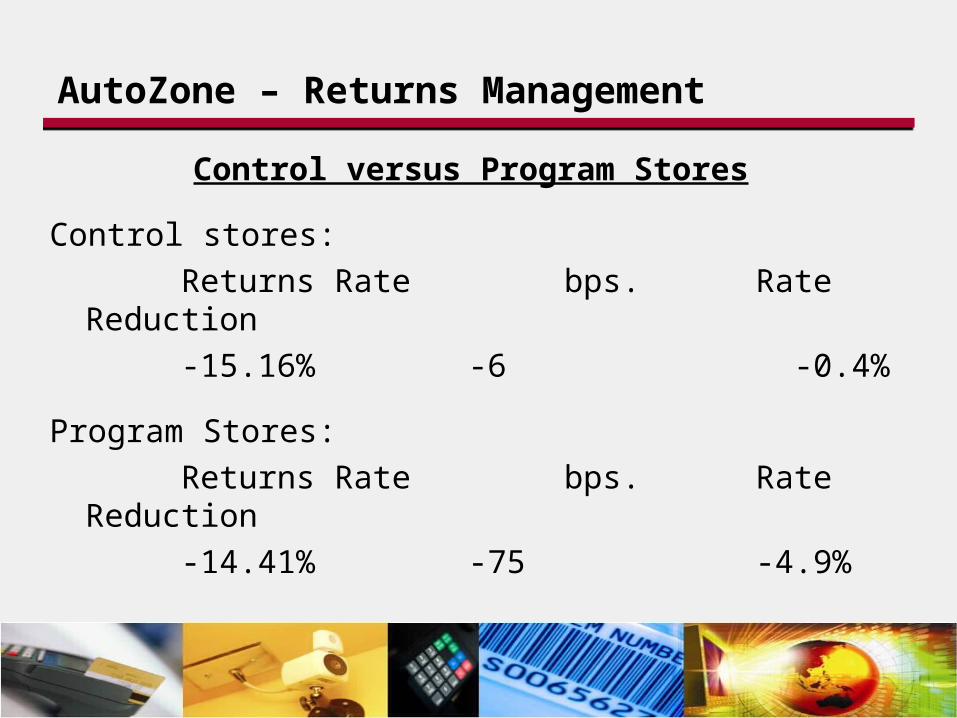

Control versus Program Stores

Control stores: Returns Rate bps. Rate

Reduction-15.16% -6 -0.4%

Program Stores:Returns Rate bps. Rate

Reduction-14.41% -75 -4.9%

AutoZone – Returns Management

AutoZone – Returns Management

Customers’ Responses to AutoZone's Overall Return Policies & Ease of Returning

**All KPIs remained flat or showed improvement

The best is yet to come!

Override percentages began at mid 90’s Majority of stores on program for less than 9

months Currently at 43% override percentage

Weekly KPI reporting On-going communication plan Continuous ROI analysis

AutoZone – Returns Management

Quotes from SVP-Stores

AutoZone – Returns Management

Interactive Question Placeholder

Q5: Is reducing return rate on your current initiative list?

1. Yes2. No3. Unknown

Q6: Have you performed an analysis to see if high returns correlate to high shrink?

1. Yes2. No3. Unknown

Example of Return Fraud Solutions in Action

Kevin Darnell – Director, Loss Prevention, Brown Shoe

Return Authorization at Brown Shoe

2006 Rollout Information captured

ID Name Phone Number Address

Reports Compliance Reports Internal/External

External Fraud

•49 Total Returns•Returns at 6

different stores•$2,328 in returns

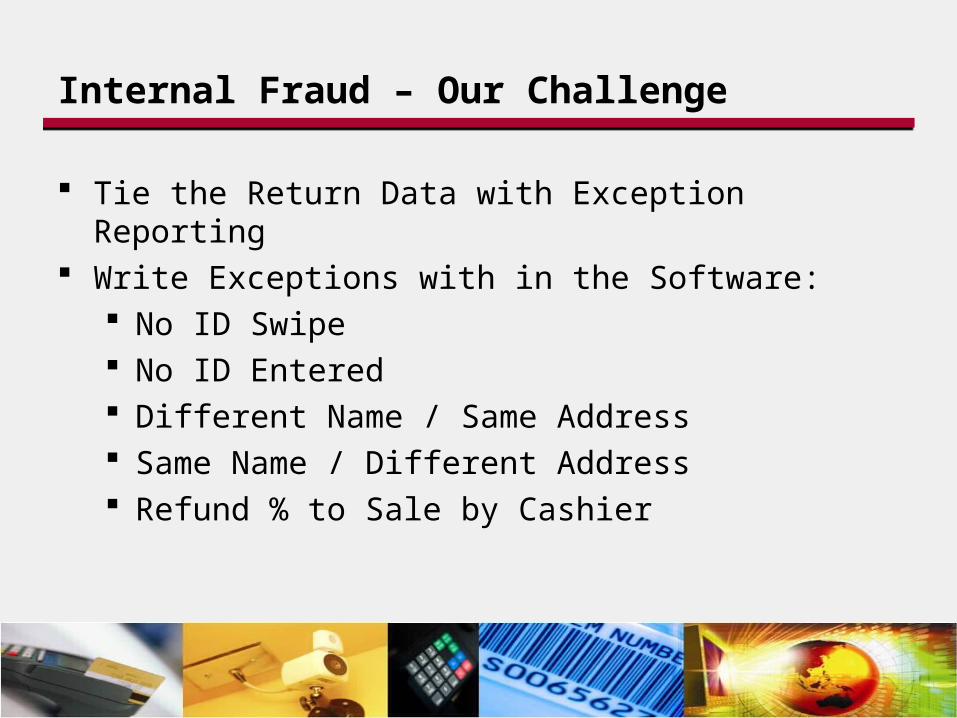

Internal Fraud – Our Challenge

Tie the Return Data with Exception Reporting Write Exceptions with in the Software:

No ID Swipe No ID Entered Different Name / Same Address Same Name / Different Address Refund % to Sale by Cashier

Video Overview

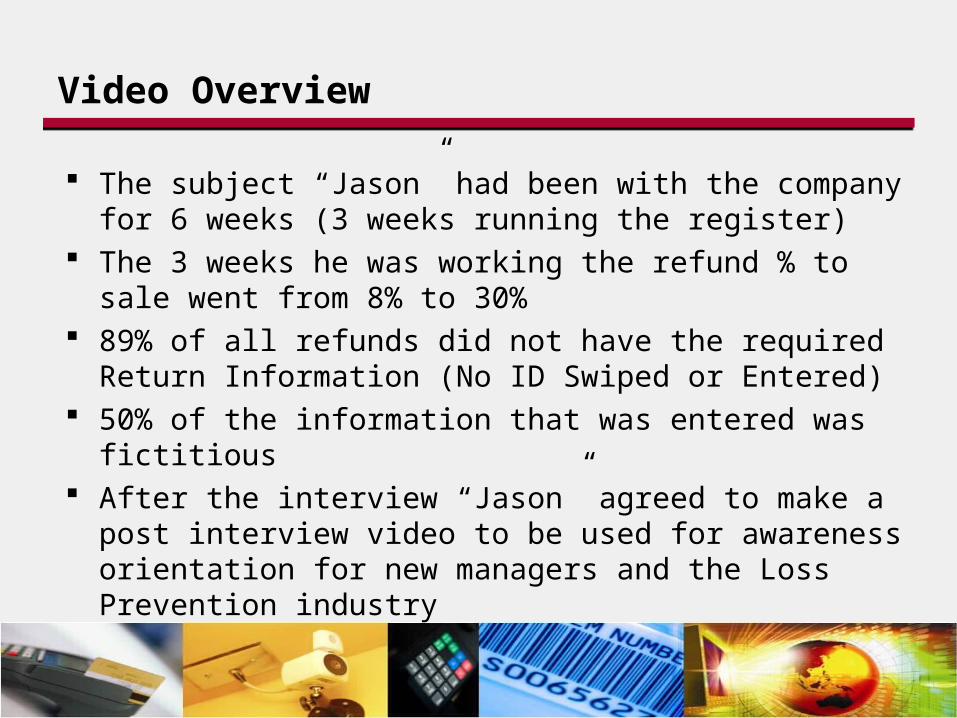

The subject “Jason” had been with the company for 6 weeks (3 weeks running the register)

The 3 weeks he was working the refund % to sale went from 8% to 30%

89% of all refunds did not have the required Return Information (No ID Swiped or Entered)

50% of the information that was entered was fictitious

After the interview “Jason” agreed to make a post interview video to be used for awareness orientation for new managers and the Loss Prevention industry

Make The Right Choice

(Play video)

Interactive Question Placeholder

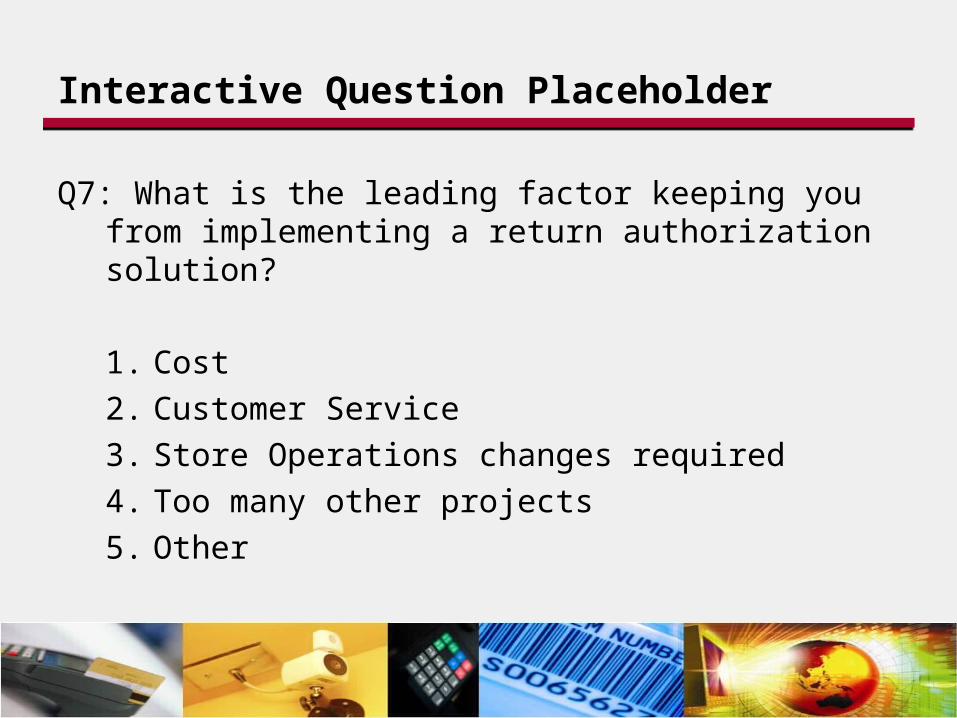

Q7: What is the leading factor keeping you from implementing a return authorization solution?

1. Cost2. Customer Service3. Store Operations changes required4. Too many other projects5. Other

Possible Solutions to Address Return Fraud and Abuse

Mark Hilinski – EVP, Strategic Accounts, The Retail Equation

Solutions

From the LPRC survey: Retailers continue to use a variety of methods,

both manual and automated, in order to identify “bad returners” and stop the attempted return transaction.

Tools employed include: policy changes, abuser lists, exception reports, real-time fraud detection systems, pos receipt validation, video analysis, and more.

Recommendations

Ask for an ROI. Reducing fraudulent returns is a measurable action and should come with a documented ROI.

Think twice before you let a restrictive return policy impact your good customers.

Fraud occurs in both receipted and non-receipted returns.

Do your research yourself; other functional areas do not always think like a loss prevention expert when selecting solutions.

Questions?