44

UNPACKING THE FEDERAL BUDGET – POSITIVE CASH IMPACT FOR BUSINESS Wednesday, 11 November 2020

UNPACKING THE FEDERAL BUDGET –

POSITIVE CASH IMPACT FOR BUSINESSWednesday, 11 November 2020

PANEL OF EXPERTS

MARIANA VON-LUCKENPARTNER, TAX CONSULTING

HLB MANN JUDD

P: +61 (0)2 9020 4095

ALEX KINGDIRECTOR, TAX CONSULTING

HLB MANN JUDD

P: +61 (0)2 9020 4345

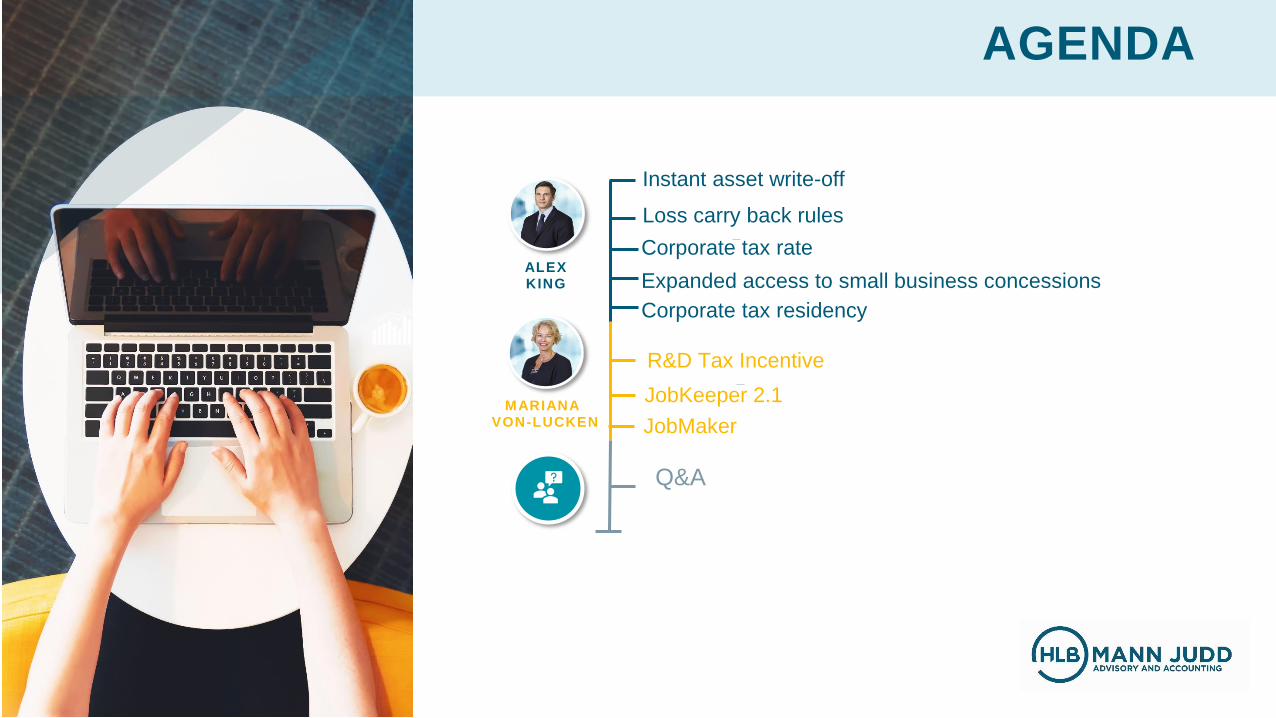

AGENDA

Instant asset write-off

Q&A

Loss carry back rules

Corporate tax rateALEXKING

R&D Tax Incentive

JobKeeper 2.1MARIANA

VON-LUCKEN

Expanded access to small business concessions

JobMaker

Corporate tax residency

What is it?

INSTANT ASSET WRITE OFF – FULL EXPENSING

OF DEPRECIABLE ASSETS (FEDA)

Full deduction for cost of

eligible depreciable assets

(no cost limit)

Used in a business in

Australia

For assets first held between 6

October 2020 and 30 June 2022

Groups with up to $5bn in

“aggregated turnover” eligible

If under $50m turnover, wider application

➢ Can be second hand

➢ Can have committed before budget night

2020

INSTANT ASSET WRITE OFF – FULL EXPENSING

OF DEPRECIABLE ASSETS (FEDA)

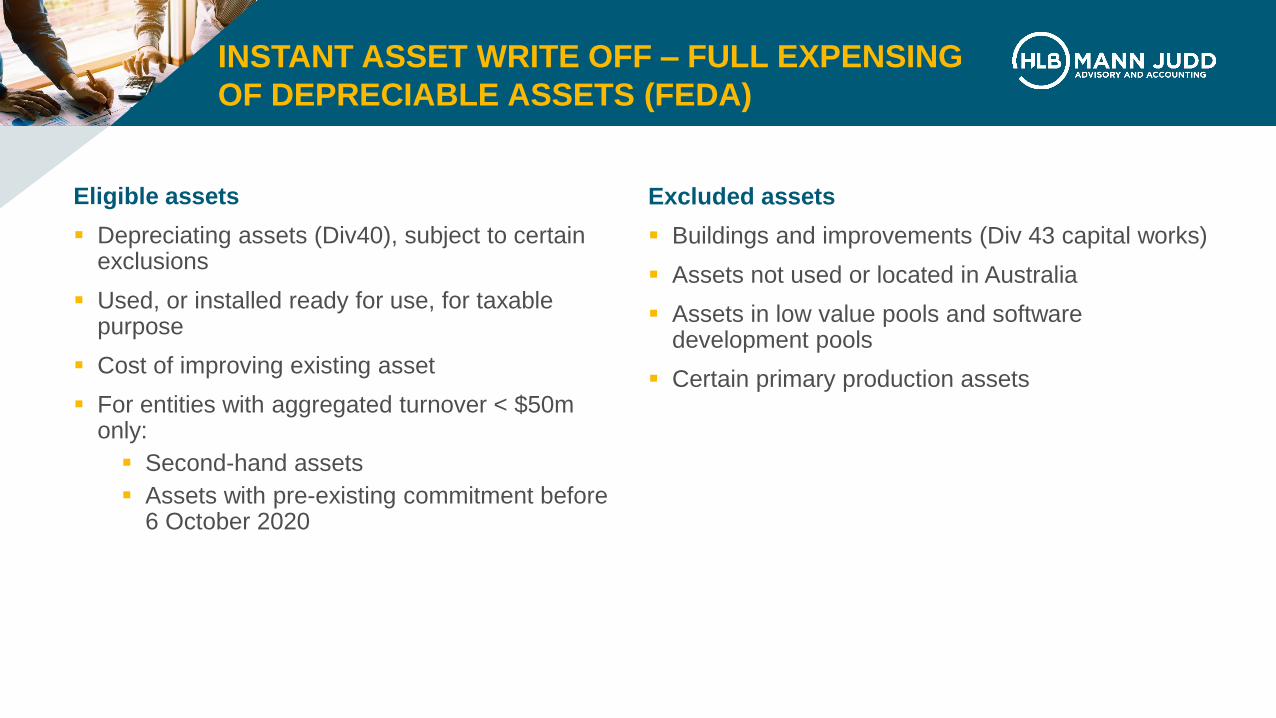

Eligible assets

▪ Depreciating assets (Div40), subject to certain exclusions

▪ Used, or installed ready for use, for taxable purpose

▪ Cost of improving existing asset

▪ For entities with aggregated turnover < $50m only:

▪ Second-hand assets

▪ Assets with pre-existing commitment before 6 October 2020

Excluded assets

▪ Buildings and improvements (Div 43 capital works)

▪ Assets not used or located in Australia

▪ Assets in low value pools and software development pools

▪ Certain primary production assets

INSTANT ASSET WRITE OFF – FULL EXPENSING

OF DEPRECIABLE ASSETS (FEDA)

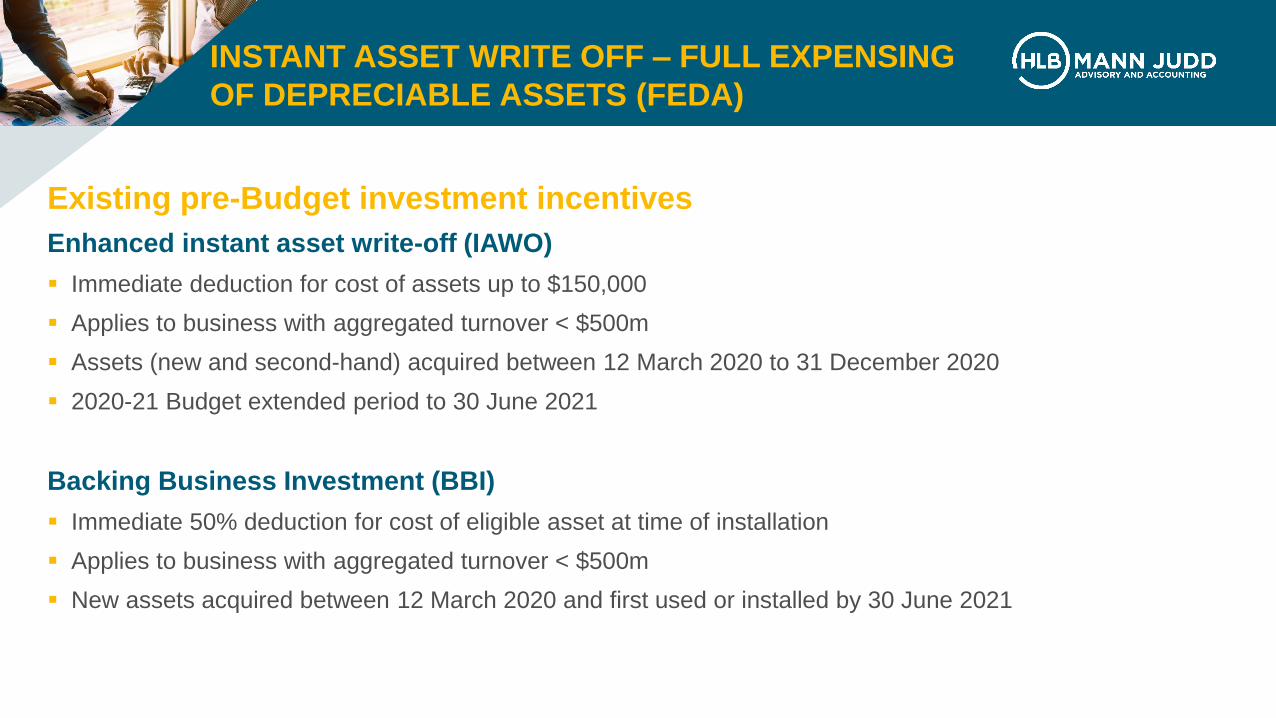

Existing pre-Budget investment incentives

Enhanced instant asset write-off (IAWO)

▪ Immediate deduction for cost of assets up to $150,000

▪ Applies to business with aggregated turnover < $500m

▪ Assets (new and second-hand) acquired between 12 March 2020 to 31 December 2020

▪ 2020-21 Budget extended period to 30 June 2021

Backing Business Investment (BBI)

▪ Immediate 50% deduction for cost of eligible asset at time of installation

▪ Applies to business with aggregated turnover < $500m

▪ New assets acquired between 12 March 2020 and first used or installed by 30 June 2021

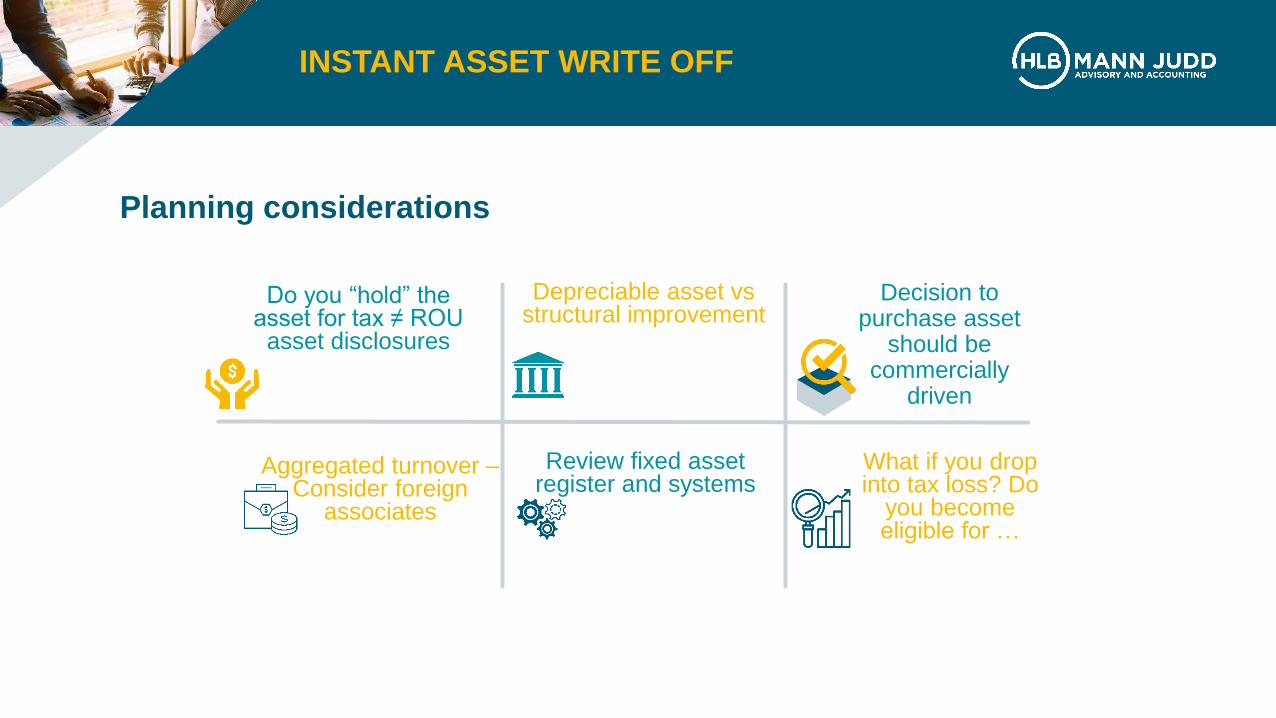

Do you “hold” the asset for

tax ≠ ROU asset disclosures

Depreciable asset vs eligible for …

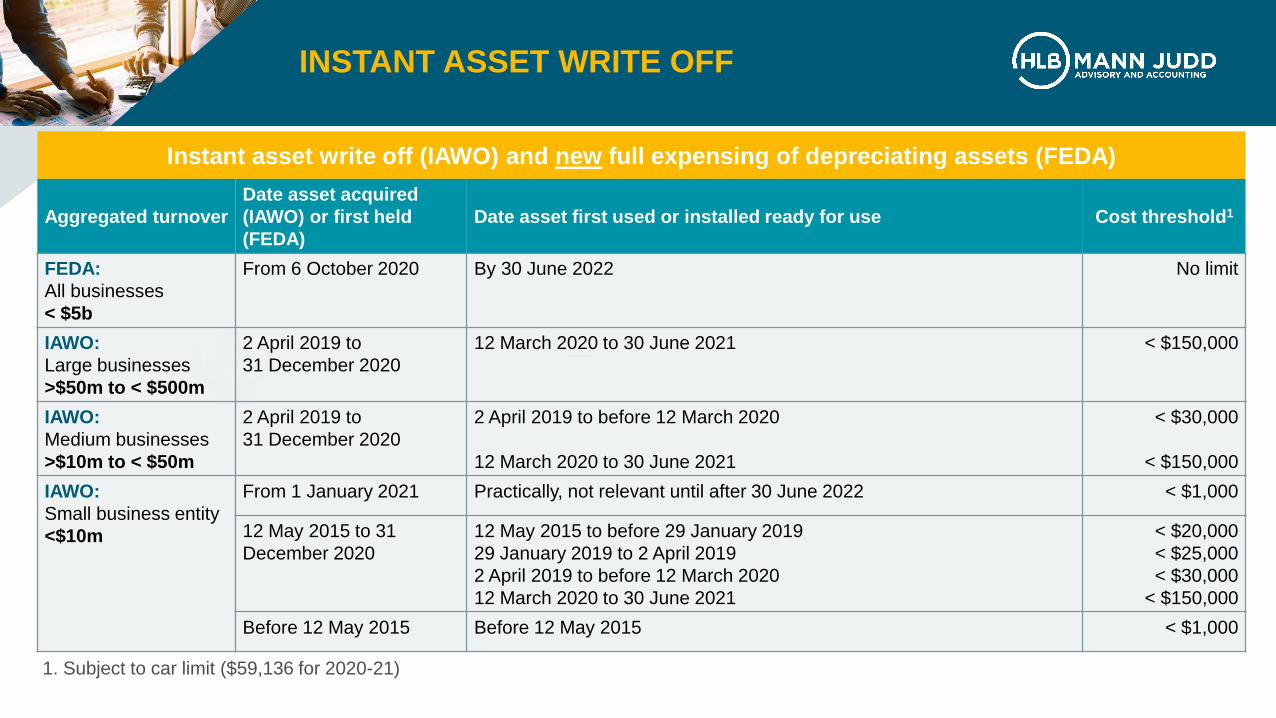

Instant asset write off (IAWO) and new full expensing of depreciating assets (FEDA)

Aggregated turnover

Date asset acquired

(IAWO) or first held

(FEDA)

Date asset first used or installed ready for use Cost threshold1

FEDA:

All businesses

< $5b

From 6 October 2020 By 30 June 2022 No limit

IAWO:

Large businesses

>$50m to < $500m

2 April 2019 to

31 December 2020

12 March 2020 to 30 June 2021 < $150,000

IAWO:

Medium businesses

>$10m to < $50m

2 April 2019 to

31 December 2020

2 April 2019 to before 12 March 2020

12 March 2020 to 30 June 2021

< $30,000

< $150,000

IAWO:

Small business entity

<$10m

From 1 January 2021 Practically, not relevant until after 30 June 2022 < $1,000

12 May 2015 to 31

December 2020

12 May 2015 to before 29 January 2019

29 January 2019 to 2 April 2019

2 April 2019 to before 12 March 2020

12 March 2020 to 30 June 2021

< $20,000

< $25,000

< $30,000

< $150,000

Before 12 May 2015 Before 12 May 2015 < $1,000

1. Subject to car limit ($59,136 for 2020-21)

INSTANT ASSET WRITE OFF

INSTANT ASSET WRITE OFF

Do you “hold” the asset for tax ≠ ROU

asset disclosures

Depreciable asset vs structural improvement

Decision to purchase asset

should be commercially

driven

Aggregated turnover –Consider foreign

associates

Review fixed asset register and systems

What if you drop into tax loss? Do

you become eligible for …

Planning considerations

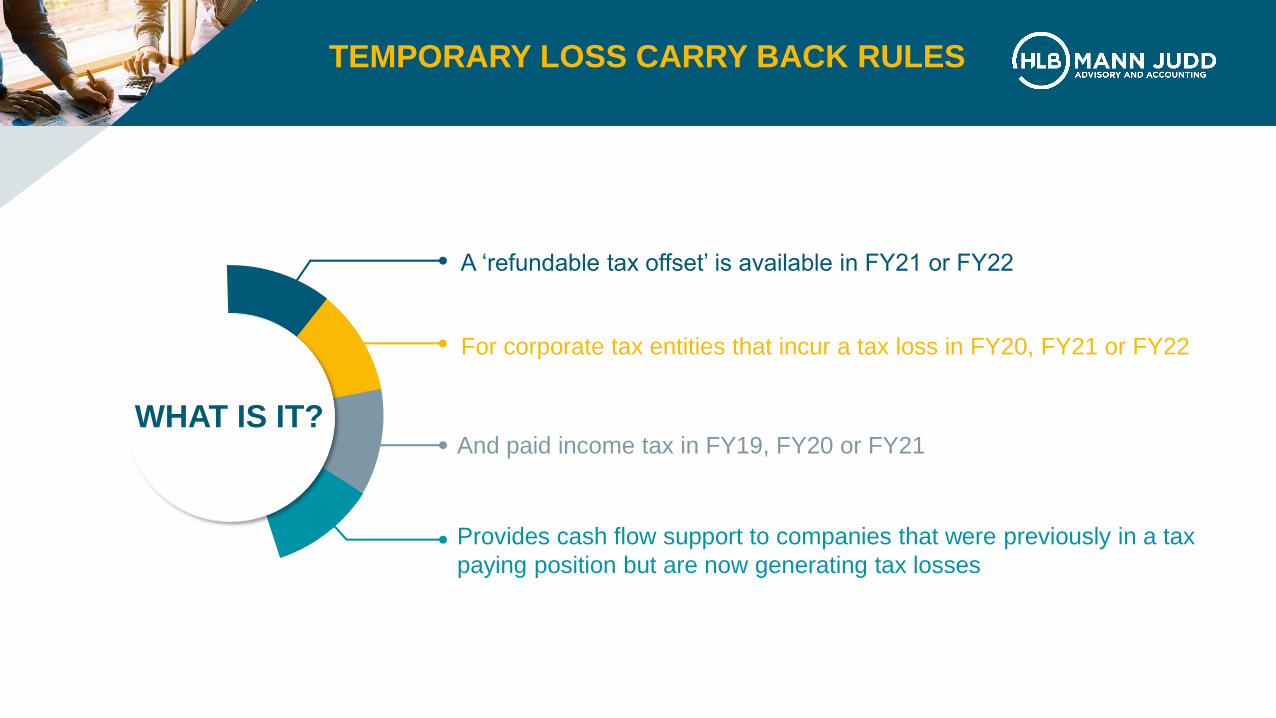

TEMPORARY LOSS CARRY BACK RULES

WHAT IS IT?

A ‘refundable tax offset’ is available in FY21 or FY22

For corporate tax entities that incur a tax loss in FY20, FY21 or FY22

And paid income tax in FY19, FY20 or FY21

Provides cash flow support to companies that were previously in a tax

paying position but are now generating tax losses

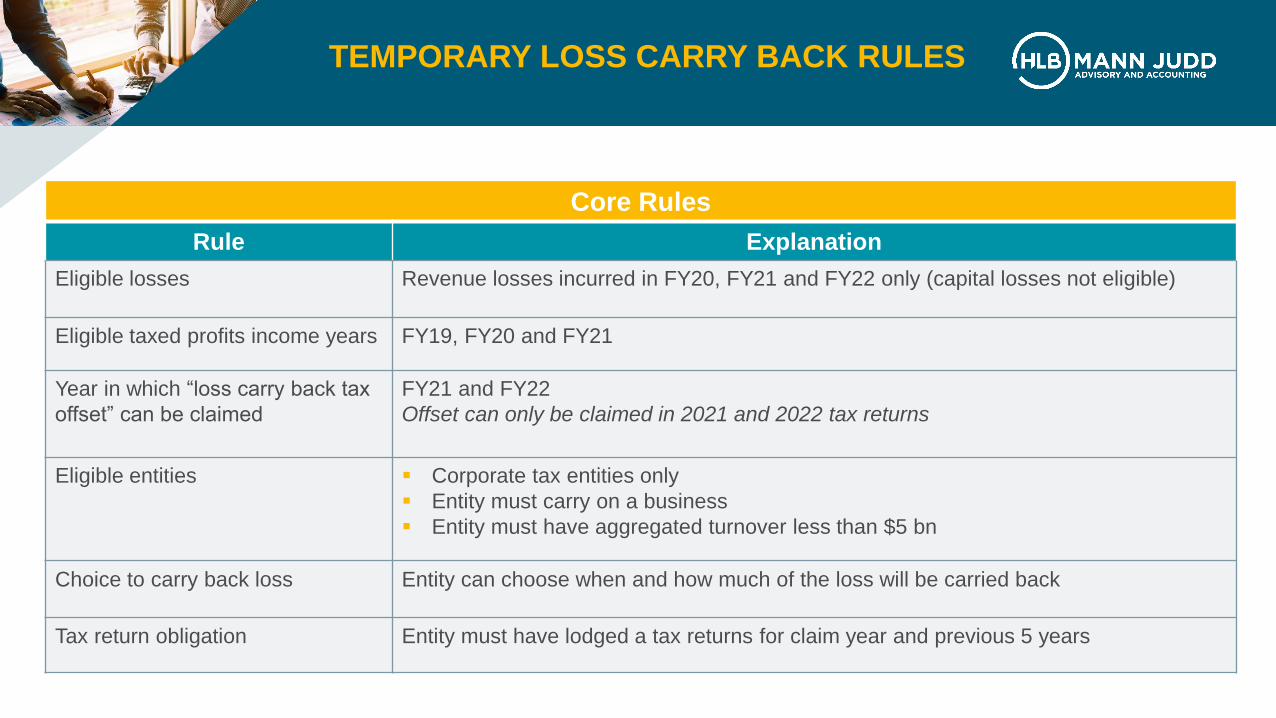

TEMPORARY LOSS CARRY BACK RULES

Core Rules

Rule Explanation

Eligible losses Revenue losses incurred in FY20, FY21 and FY22 only (capital losses not eligible)

Eligible taxed profits income years FY19, FY20 and FY21

Year in which “loss carry back tax

offset” can be claimed

FY21 and FY22

Offset can only be claimed in 2021 and 2022 tax returns

Eligible entities ▪ Corporate tax entities only

▪ Entity must carry on a business

▪ Entity must have aggregated turnover less than $5 bn

Choice to carry back loss Entity can choose when and how much of the loss will be carried back

Tax return obligation Entity must have lodged a tax returns for claim year and previous 5 years

TEMPORARY LOSS CARRY BACK RULES

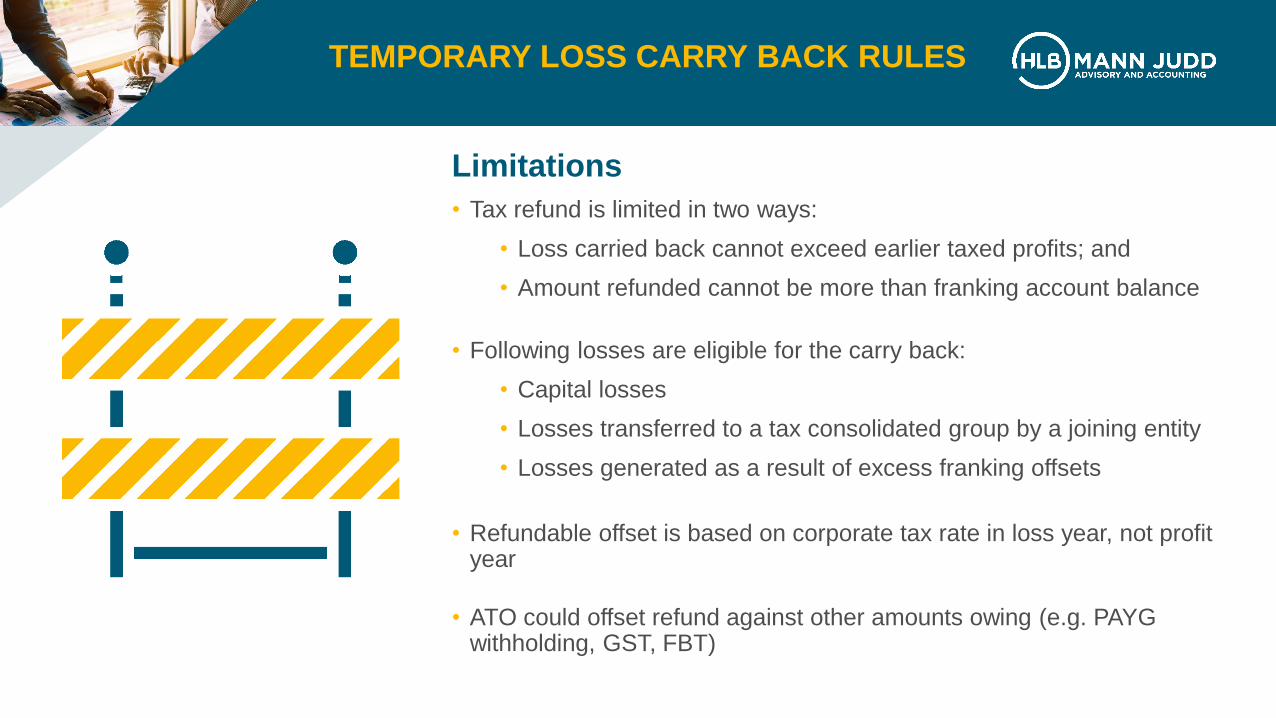

Limitations

• Tax refund is limited in two ways:

• Loss carried back cannot exceed earlier taxed profits; and

• Amount refunded cannot be more than franking account balance

• Following losses are eligible for the carry back:

• Capital losses

• Losses transferred to a tax consolidated group by a joining entity

• Losses generated as a result of excess franking offsets

• Refundable offset is based on corporate tax rate in loss year, not profit year

• ATO could offset refund against other amounts owing (e.g. PAYG withholding, GST, FBT)

TEMPORARY LOSS CARRY BACK RULES

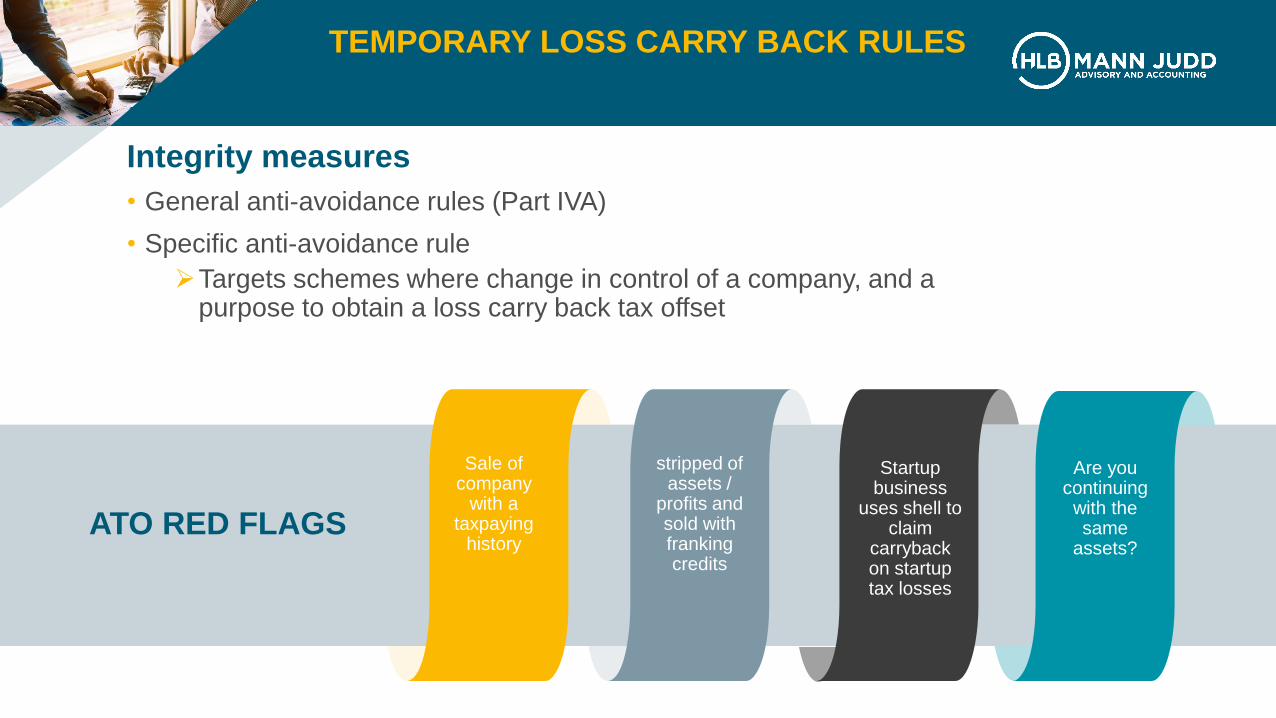

Integrity measures

• General anti-avoidance rules (Part IVA)

• Specific anti-avoidance rule

➢Targets schemes where change in control of a company, and a purpose to obtain a loss carry back tax offset

stripped of assets /

profits and sold with franking credits

Startup business

uses shell to claim

carryback on startup tax losses

Sale of company

with a taxpaying

history

Are you continuing with the same

assets?ATO RED FLAGS

TEMPORARY LOSS CARRY BACK RULES

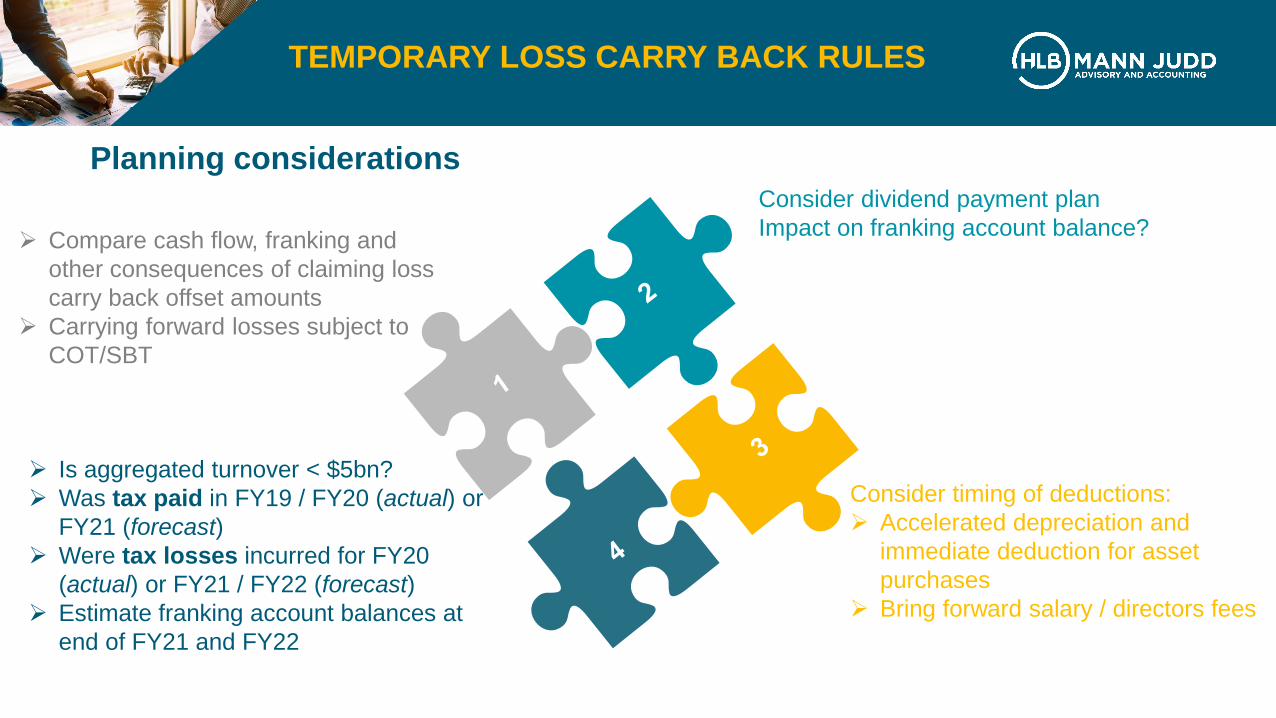

➢ Compare cash flow, franking and

other consequences of claiming loss

carry back offset amounts

➢ Carrying forward losses subject to

COT/SBT

Consider dividend payment plan

Impact on franking account balance?

Consider timing of deductions:

➢ Accelerated depreciation and

immediate deduction for asset

purchases

➢ Bring forward salary / directors fees

➢ Is aggregated turnover < $5bn?

➢ Was tax paid in FY19 / FY20 (actual) or

FY21 (forecast)

➢ Were tax losses incurred for FY20

(actual) or FY21 / FY22 (forecast)

➢ Estimate franking account balances at

end of FY21 and FY22

Planning considerations

EXAMPLE –

TEMPORARY LOSS CARRY BACK RULES

2019-20 2020-212018-19

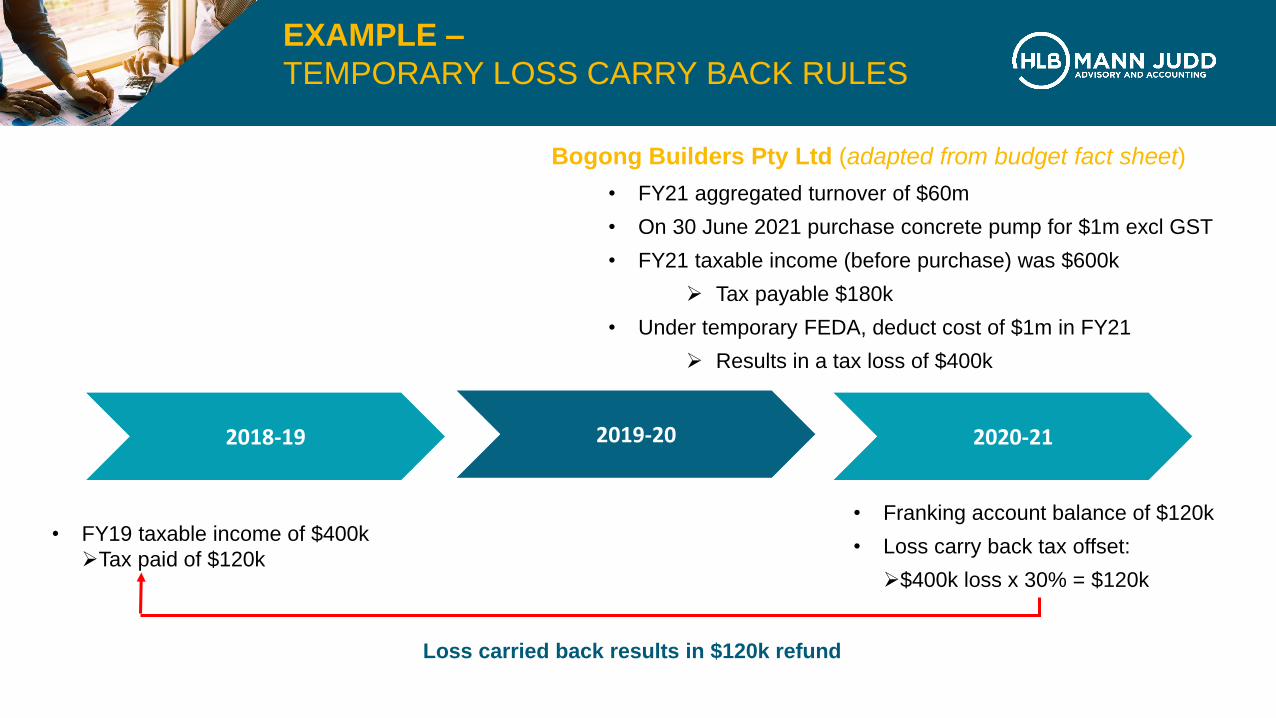

• FY21 aggregated turnover of $60m

• On 30 June 2021 purchase concrete pump for $1m excl GST

• FY21 taxable income (before purchase) was $600k

➢ Tax payable $180k

• Under temporary FEDA, deduct cost of $1m in FY21

➢ Results in a tax loss of $400k

• FY19 taxable income of $400k

➢Tax paid of $120k

• Franking account balance of $120k

• Loss carry back tax offset:

➢$400k loss x 30% = $120k

Bogong Builders Pty Ltd (adapted from budget fact sheet)

Loss carried back results in $120k refund

CORPORATE TAX RATE

Do you “hold” the asset for

tax ≠ ROU asset disclosures

Depreciable asset vs eligible for …

Corporate tax rate

• No changes announced in Budget to corporate tax rate

• Non-base rate entities: remains 30%

• Aggregated turnover threshold remains at $50m

• Base rate entities: previously announced progressive reduction (no change)

➢ FY19 and FY20: 27.5%

➢ FY21: 26%

➢ FY22: 25%

• Corporate tax rate for base rate entities relevant for:

➢Maximum franking rate of dividends

➢ Loss carry back tax offset

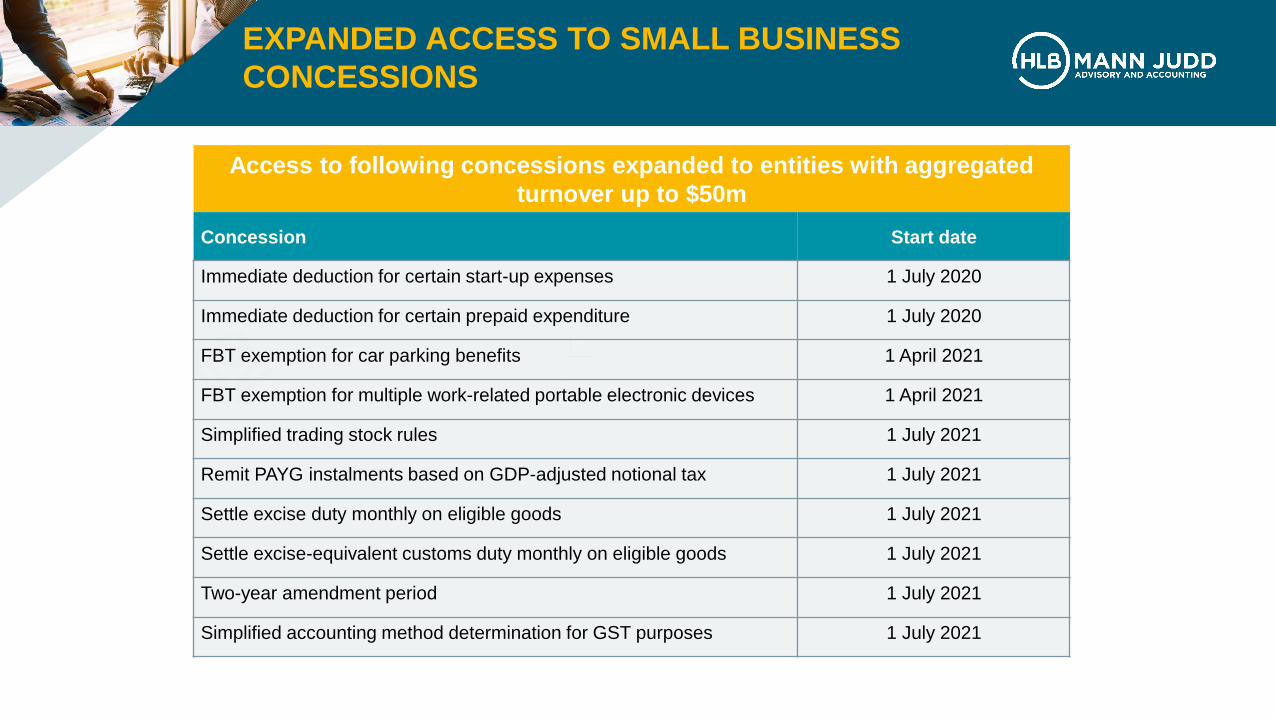

EXPANDED ACCESS TO SMALL BUSINESS

CONCESSIONS

Do you “hold” the asset for

tax ≠ ROU asset disclosures

Depreciable asset vs eligible for …

Access to following concessions expanded to entities with aggregated

turnover up to $50m

Concession Start date

Immediate deduction for certain start-up expenses 1 July 2020

Immediate deduction for certain prepaid expenditure 1 July 2020

FBT exemption for car parking benefits 1 April 2021

FBT exemption for multiple work-related portable electronic devices 1 April 2021

Simplified trading stock rules 1 July 2021

Remit PAYG instalments based on GDP-adjusted notional tax 1 July 2021

Settle excise duty monthly on eligible goods 1 July 2021

Settle excise-equivalent customs duty monthly on eligible goods 1 July 2021

Two-year amendment period 1 July 2021

Simplified accounting method determination for GST purposes 1 July 2021

CHANGE TO CORPORATE TAX

RESIDENCY

Depreciable asset vs eligible for …

Proposed change to corporate tax residency

▪ Foreign incorporated company will only be resident if it has ‘significant economic connection’ to Australia

▪ Core commercial activities undertaken in Australia, and

▪ Central management and control in Australia

▪ Returns corporate residency rules to status quo before the Bywater case ruling

R&D Tax Incentive

JobKeeper 2.1MARIANA

VON-LUCKEN JobMaker

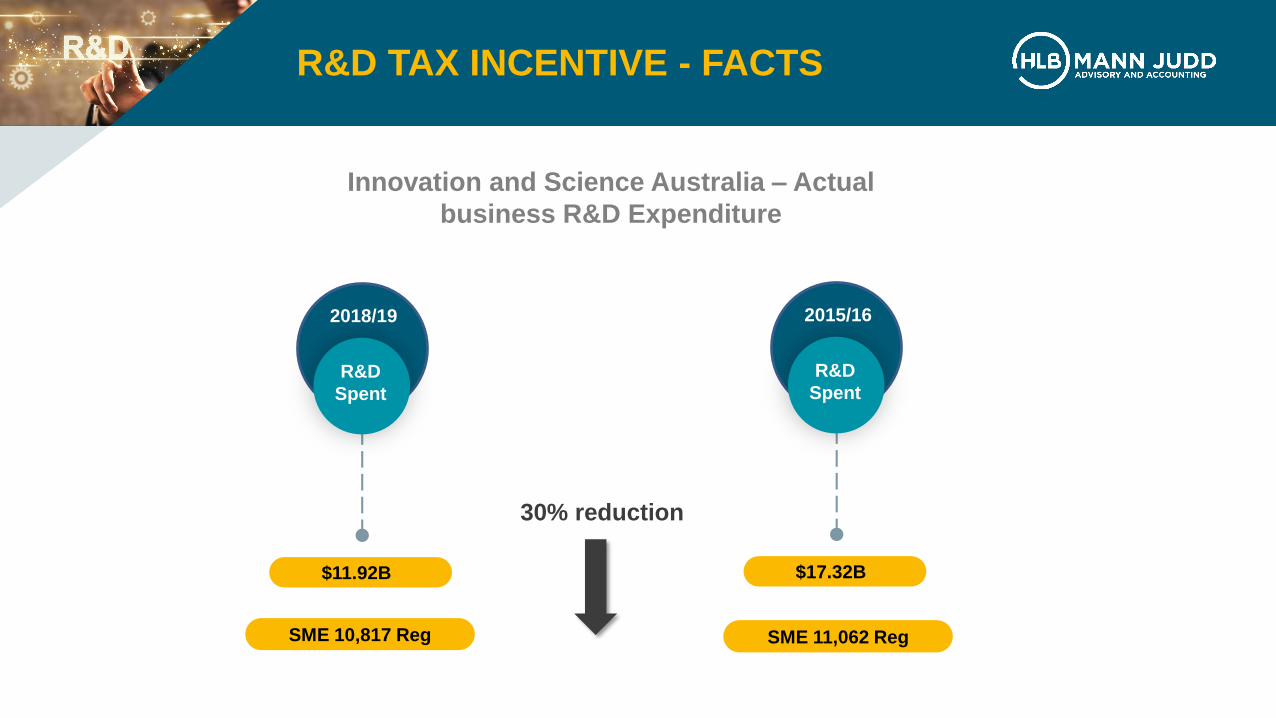

R&D TAX INCENTIVE - FACTS

Innovation and Science Australia – Actual

business R&D Expenditure

$11.92B

R&D

Spent

2018/19

$17.32B

R&D

Spent

2015/16

30% reduction

SME 10,817 Reg SME 11,062 Reg

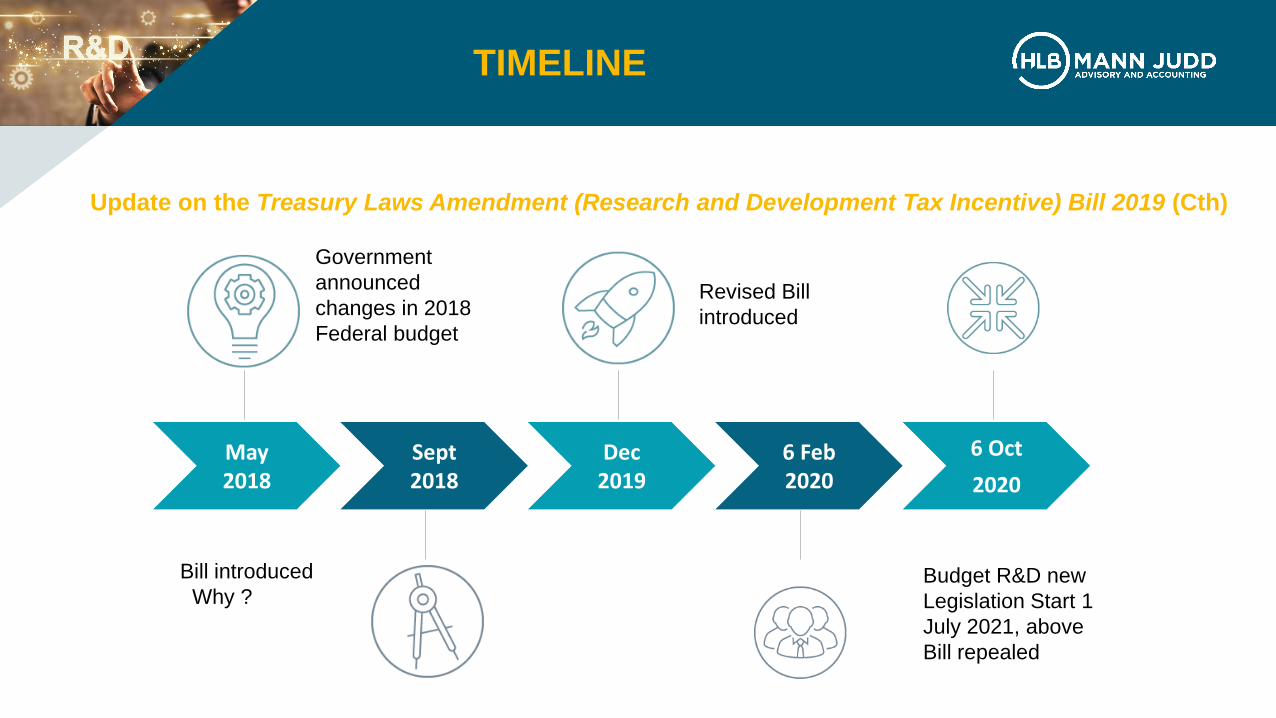

TIMELINE

Sept 2018

Dec 2019

6 Feb 2020

6 Oct

2020

May 2018

Government

announced

changes in 2018

Federal budget

Bill introduced

Why ?Budget R&D new

Legislation Start 1

July 2021, above

Bill repealed

Revised Bill

introduced

Update on the Treasury Laws Amendment (Research and Development Tax Incentive) Bill 2019 (Cth)

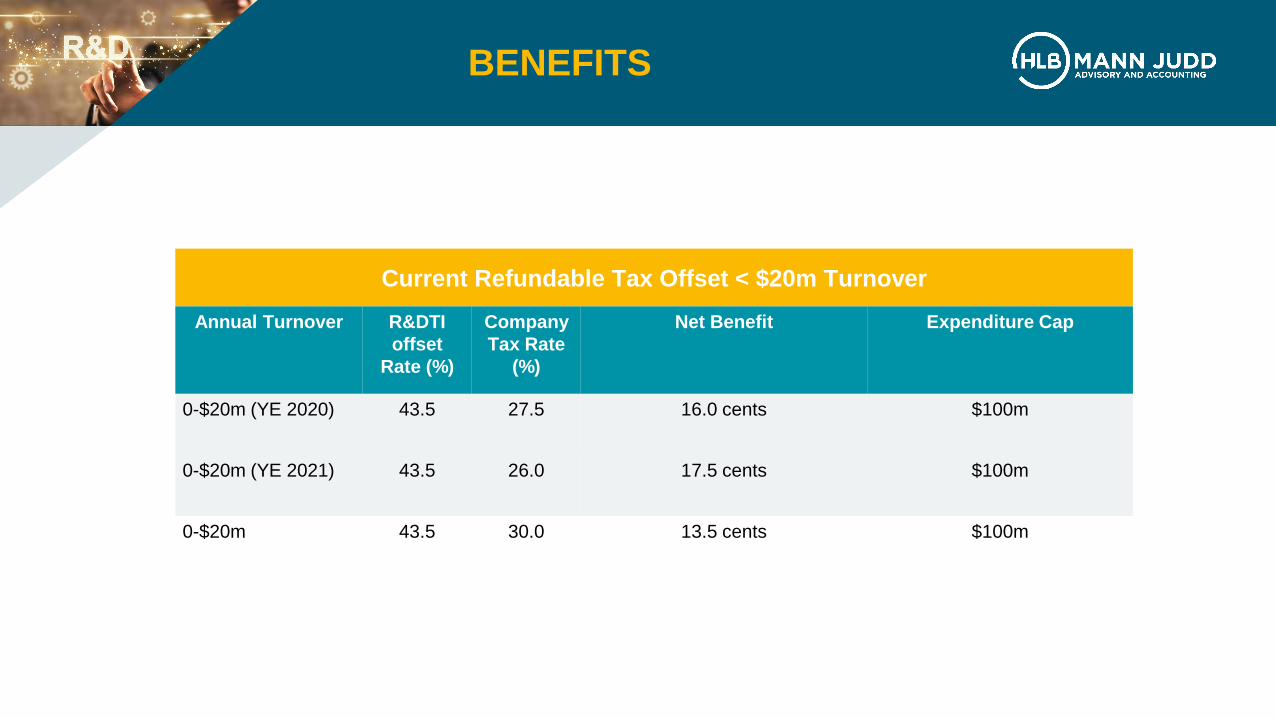

BENEFITS

Current Refundable Tax Offset < $20m Turnover

Annual Turnover R&DTI

offset

Rate (%)

Company

Tax Rate

(%)

Net Benefit Expenditure Cap

0-$20m (YE 2020) 43.5 27.5 16.0 cents $100m

0-$20m (YE 2021) 43.5 26.0 17.5 cents $100m

0-$20m 43.5 30.0 13.5 cents $100m

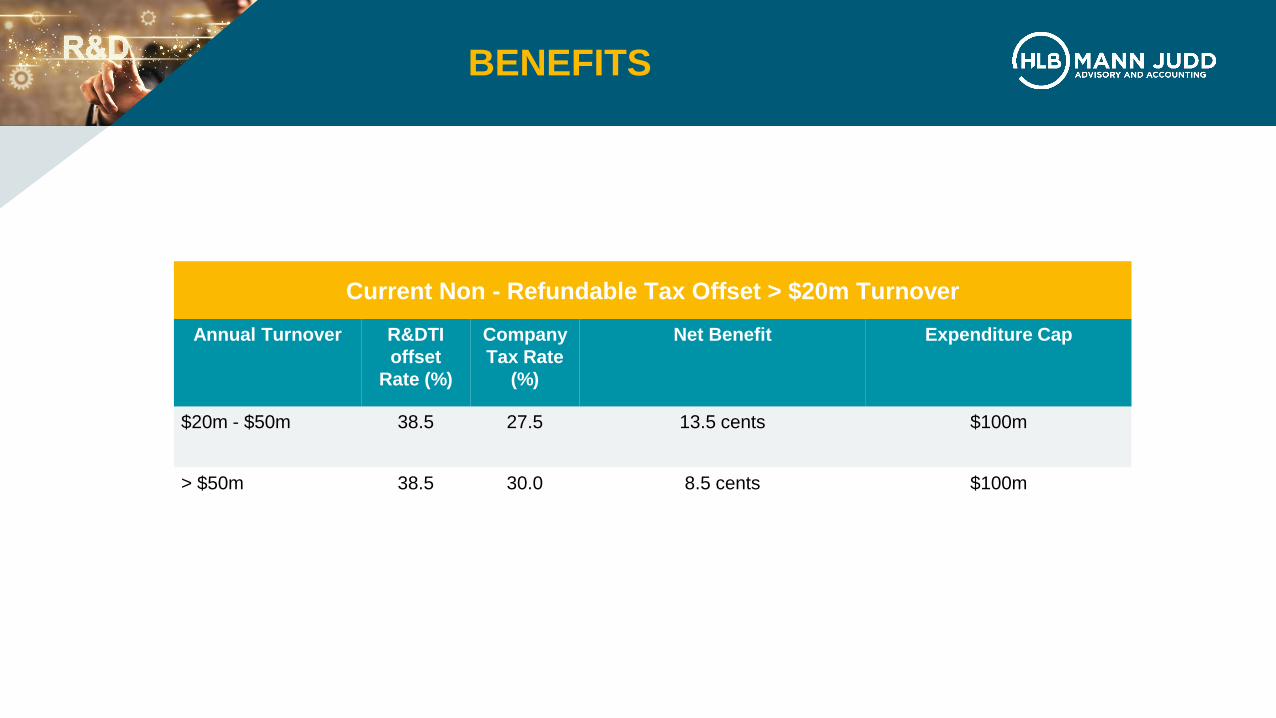

BENEFITS

Current Non - Refundable Tax Offset > $20m Turnover

Annual Turnover R&DTI

offset

Rate (%)

Company

Tax Rate

(%)

Net Benefit Expenditure Cap

$20m - $50m 38.5 27.5 13.5 cents $100m

> $50m 38.5 30.0 8.5 cents $100m

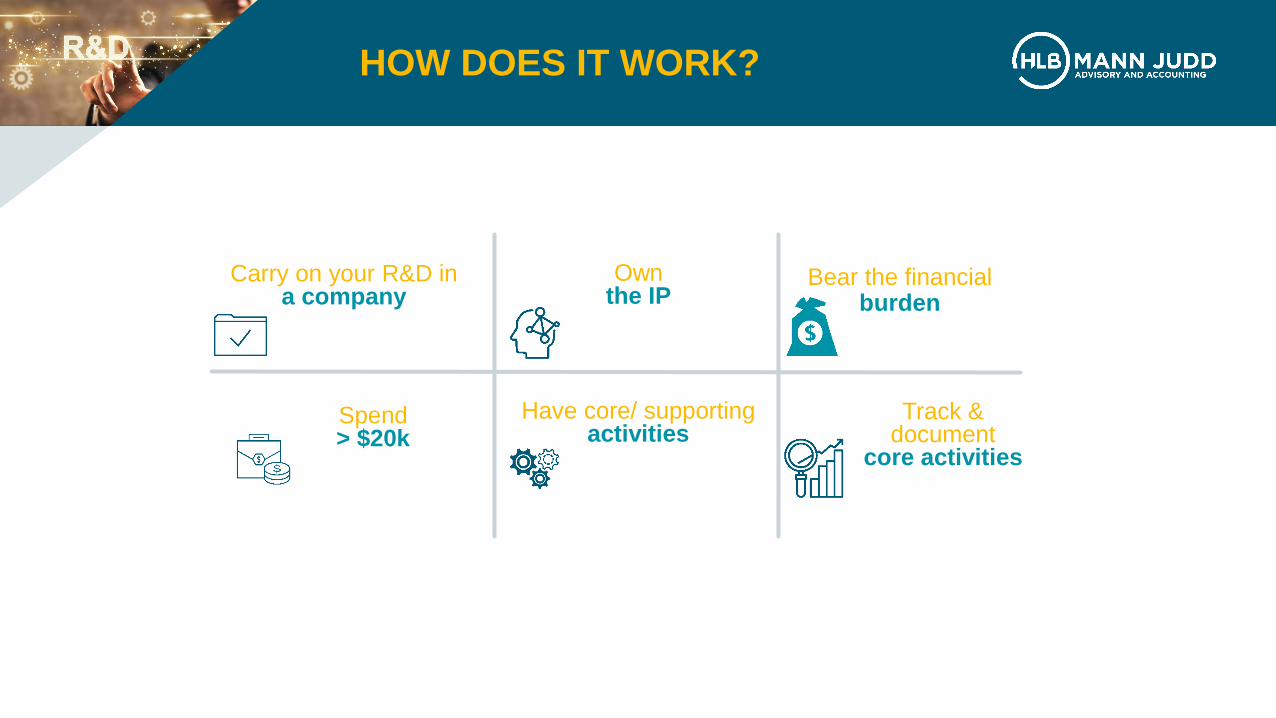

HOW DOES IT WORK?

Carry on your R&D in a company

Ownthe IP

Bear the financial burden

Spend> $20k

Have core/ supportingactivities

Track & document

core activities

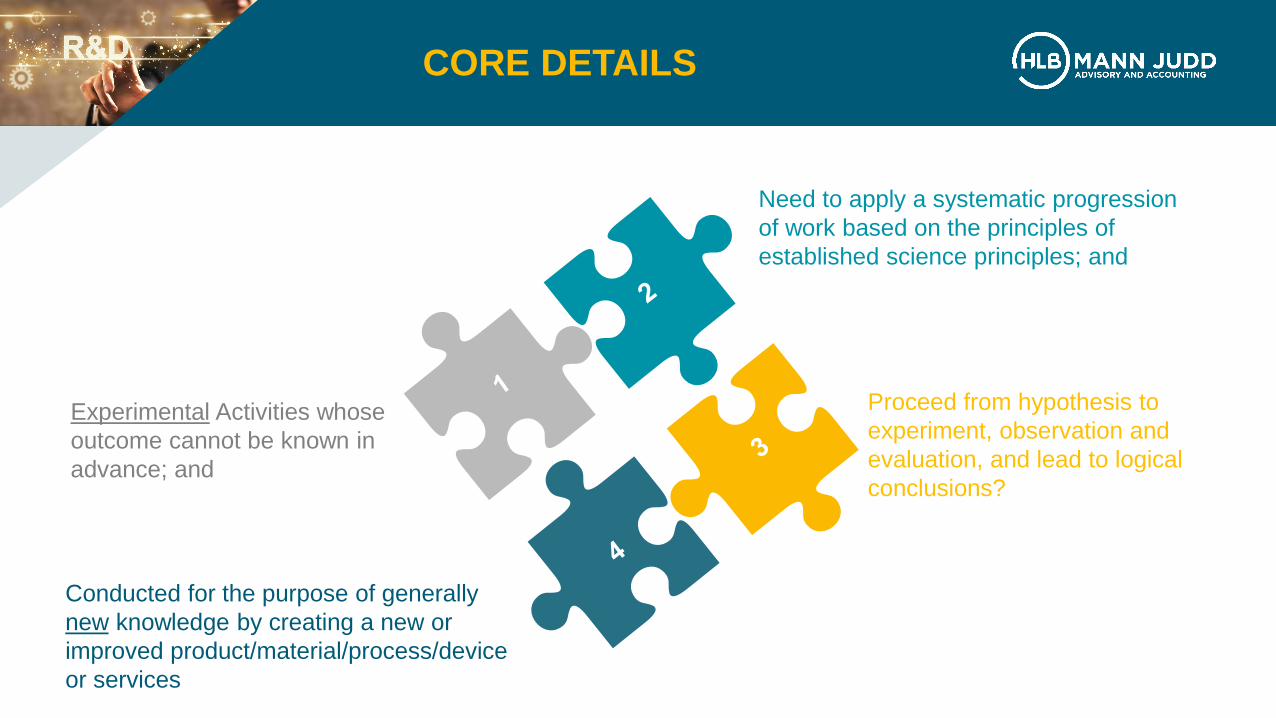

CORE DETAILS

Experimental Activities whose

outcome cannot be known in

advance; and

Need to apply a systematic progression

of work based on the principles of

established science principles; and

Proceed from hypothesis to

experiment, observation and

evaluation, and lead to logical

conclusions?

Conducted for the purpose of generally

new knowledge by creating a new or

improved product/material/process/device

or services

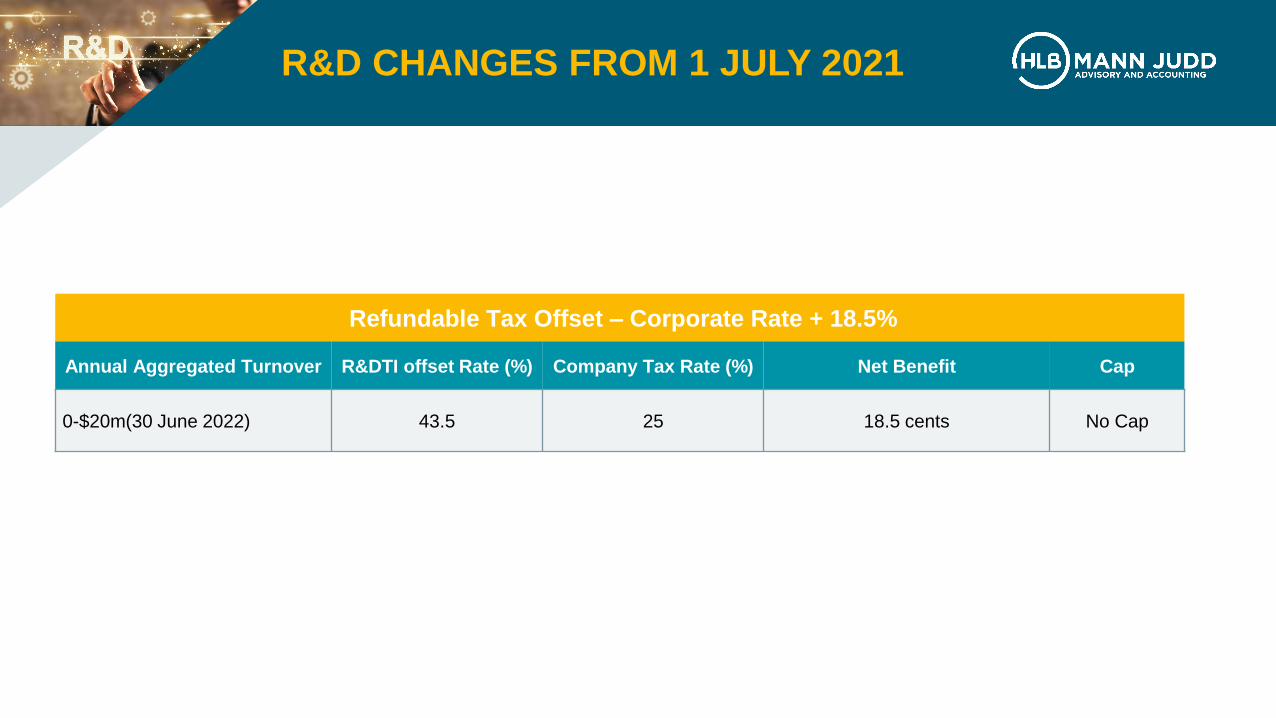

R&D CHANGES FROM 1 JULY 2021

Refundable Tax Offset – Corporate Rate + 18.5%

Annual Aggregated Turnover R&DTI offset Rate (%) Company Tax Rate (%) Net Benefit Cap

0-$20m(30 June 2022) 43.5 25 18.5 cents No Cap

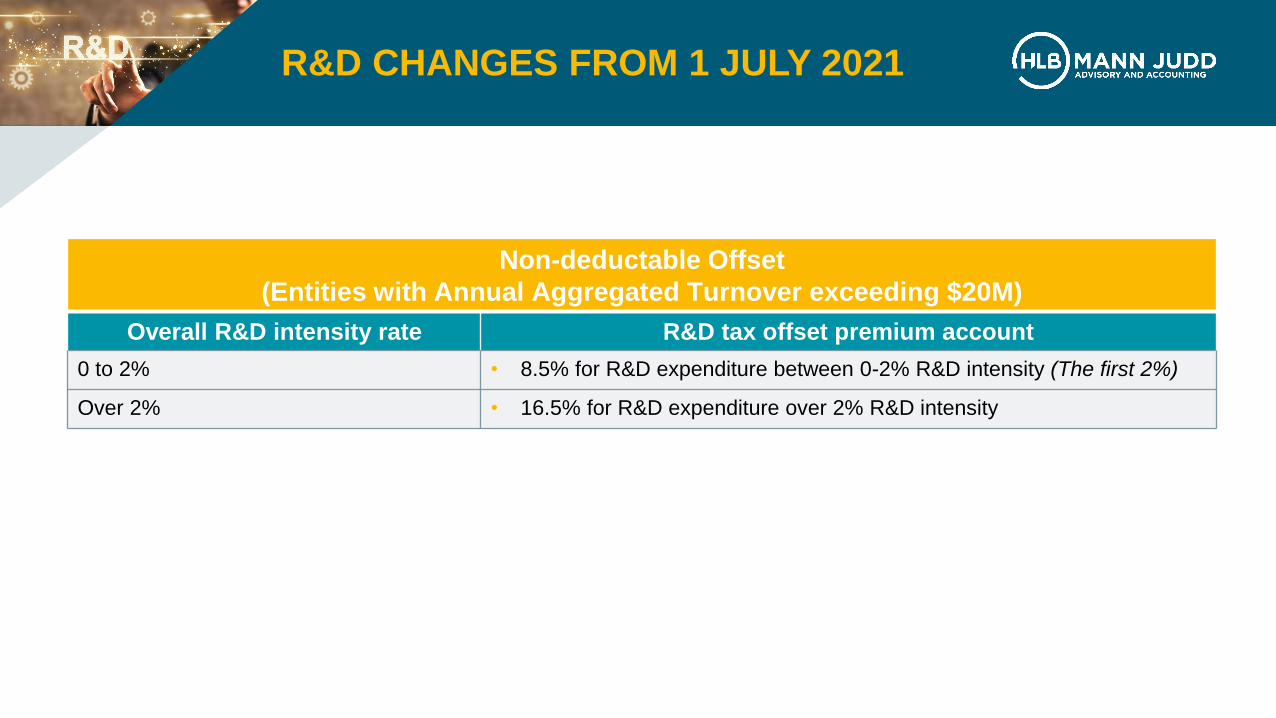

R&D CHANGES FROM 1 JULY 2021

Non-deductable Offset

(Entities with Annual Aggregated Turnover exceeding $20M)

Overall R&D intensity rate R&D tax offset premium account

0 to 2% • 8.5% for R&D expenditure between 0-2% R&D intensity (The first 2%)

Over 2% • 16.5% for R&D expenditure over 2% R&D intensity

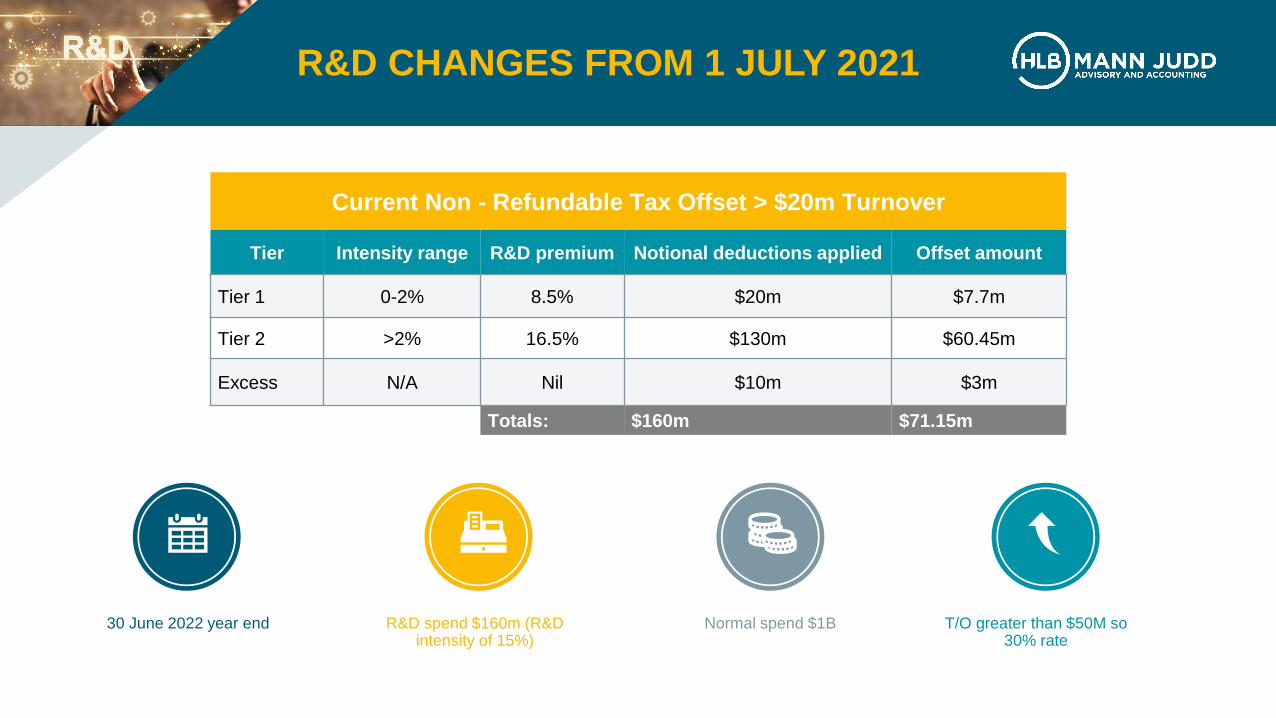

R&D CHANGES FROM 1 JULY 2021

Current Non - Refundable Tax Offset > $20m Turnover

Tier Intensity range R&D premium Notional deductions applied Offset amount

Tier 1 0-2% 8.5% $20m $7.7m

Tier 2 >2% 16.5% $130m $60.45m

Excess N/A Nil $10m $3m

Totals: $160m $71.15m

30 June 2022 year end R&D spend $160m (R&D intensity of 15%)

Normal spend $1B T/O greater than $50M so 30% rate

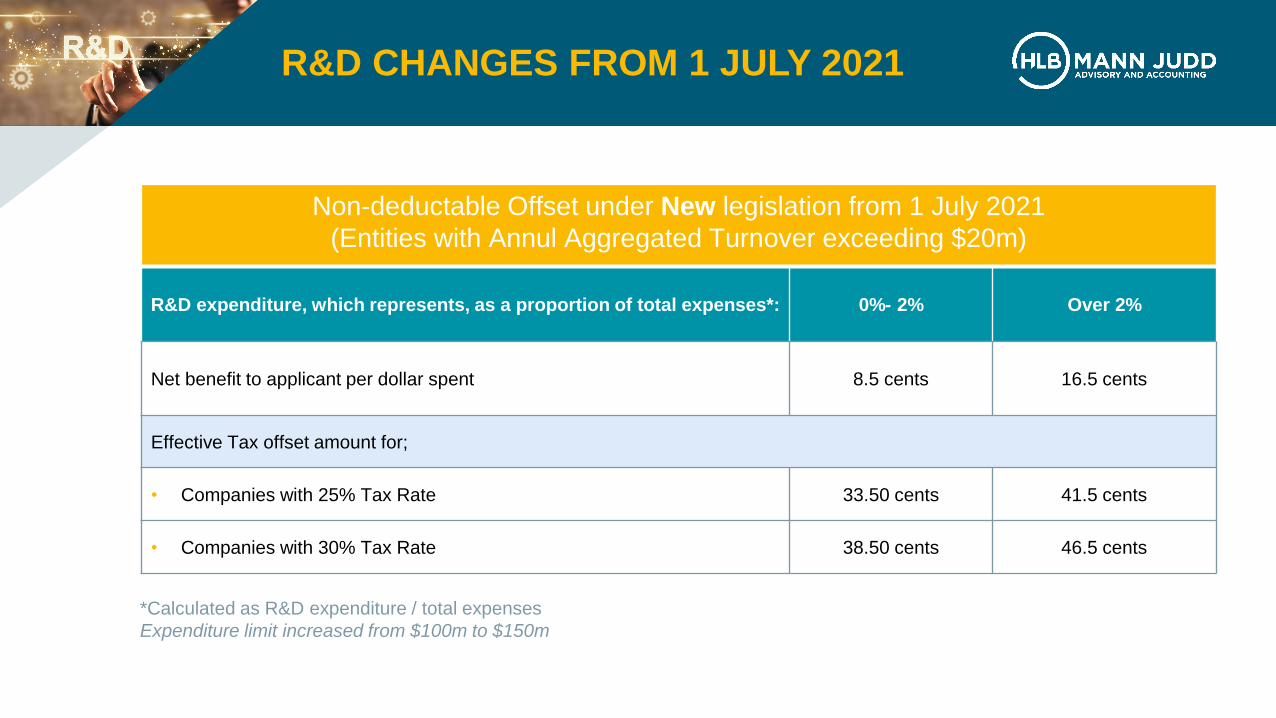

R&D CHANGES FROM 1 JULY 2021

Non-deductable Offset under New legislation from 1 July 2021

(Entities with Annul Aggregated Turnover exceeding $20m)

R&D expenditure, which represents, as a proportion of total expenses*: 0%- 2% Over 2%

Net benefit to applicant per dollar spent 8.5 cents 16.5 cents

Effective Tax offset amount for;

• Companies with 25% Tax Rate 33.50 cents 41.5 cents

• Companies with 30% Tax Rate 38.50 cents 46.5 cents

*Calculated as R&D expenditure / total expenses

Expenditure limit increased from $100m to $150m

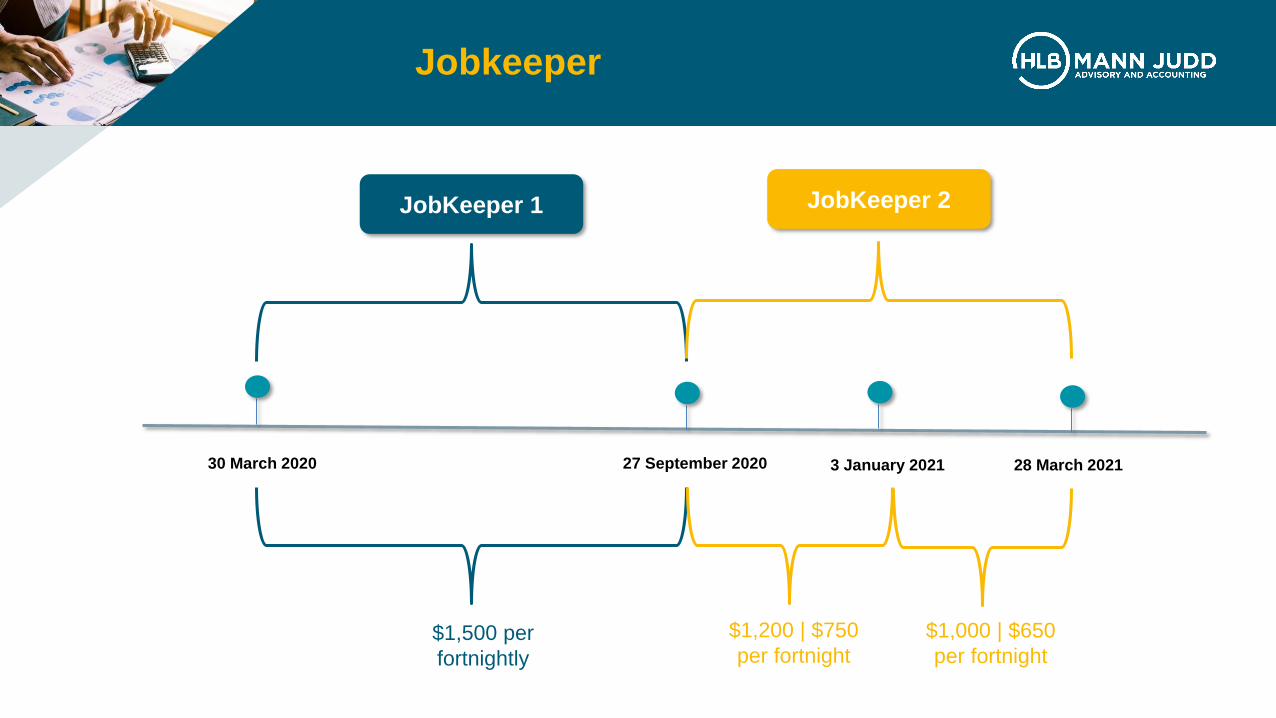

Jobkeeper

27 September 2020 3 January 2021 28 March 202130 March 2020

JobKeeper 1 JobKeeper 2

$1,500 per

fortnightly

$1,200 | $750

per fortnight

$1,000 | $650

per fortnight

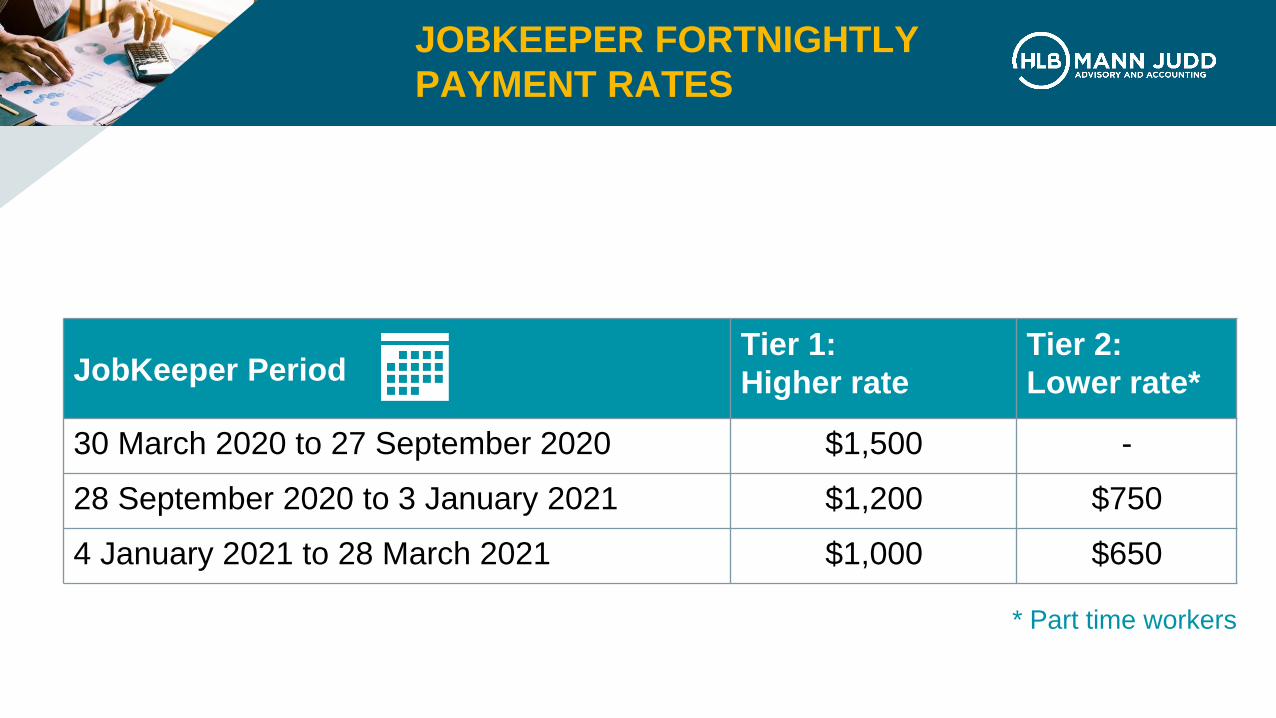

JOBKEEPER FORTNIGHTLY

PAYMENT RATES

JobKeeper PeriodTier 1:

Higher rate

Tier 2:

Lower rate*

30 March 2020 to 27 September 2020 $1,500 -

28 September 2020 to 3 January 2021 $1,200 $750

4 January 2021 to 28 March 2021 $1,000 $650

* Part time workers

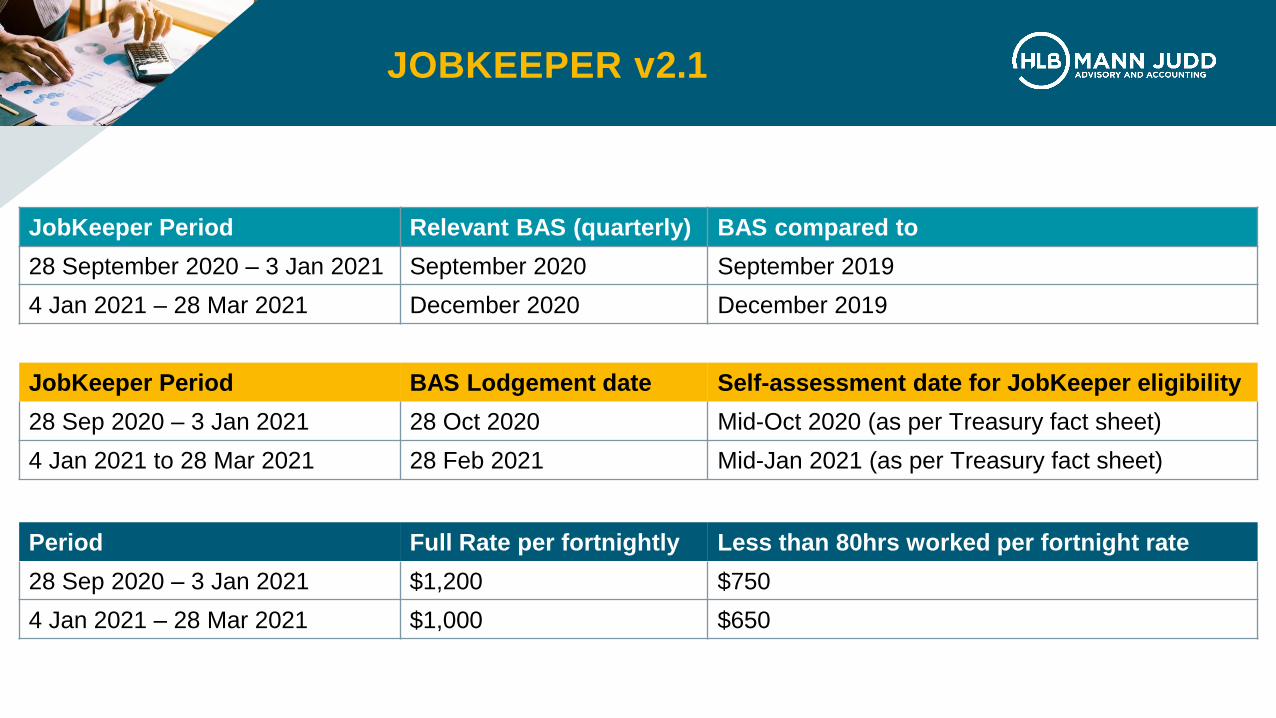

JOBKEEPER v2.1

JobKeeper Period Relevant BAS (quarterly) BAS compared to

28 September 2020 – 3 Jan 2021 September 2020 September 2019

4 Jan 2021 – 28 Mar 2021 December 2020 December 2019

JobKeeper Period BAS Lodgement date Self-assessment date for JobKeeper eligibility

28 Sep 2020 – 3 Jan 2021 28 Oct 2020 Mid-Oct 2020 (as per Treasury fact sheet)

4 Jan 2021 to 28 Mar 2021 28 Feb 2021 Mid-Jan 2021 (as per Treasury fact sheet)

Period Full Rate per fortnightly Less than 80hrs worked per fortnight rate

28 Sep 2020 – 3 Jan 2021 $1,200 $750

4 Jan 2021 – 28 Mar 2021 $1,000 $650

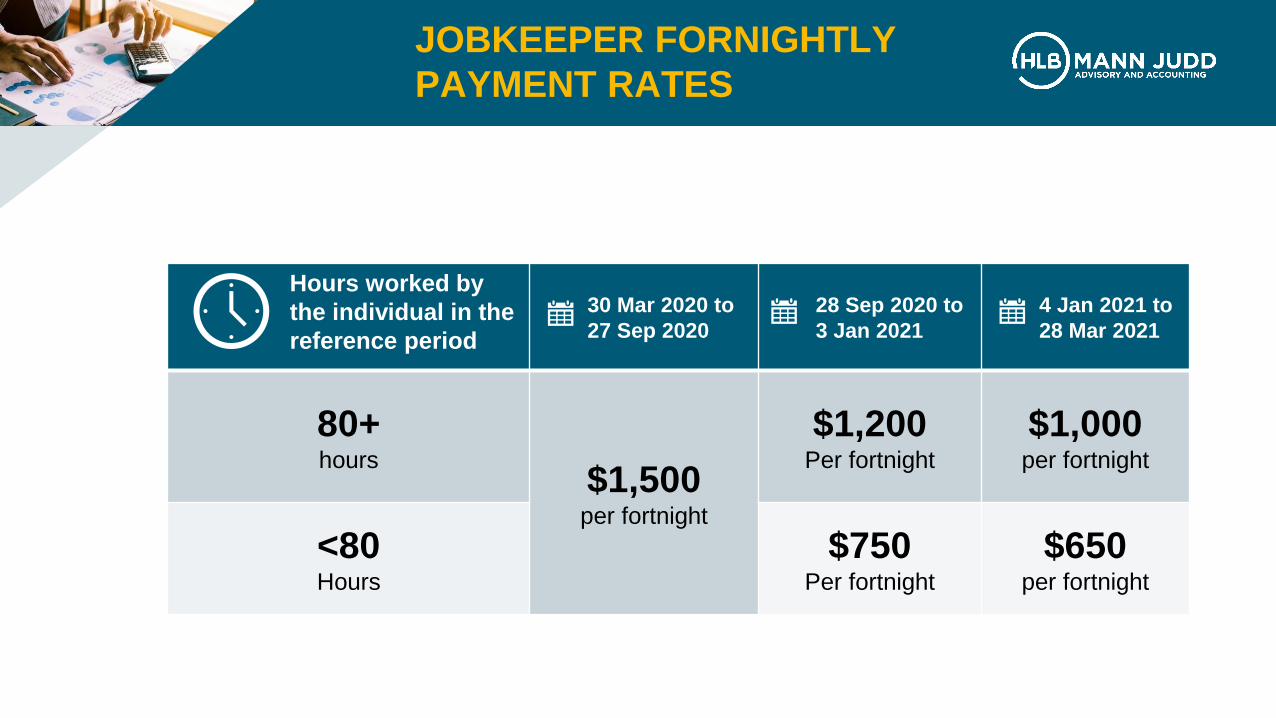

JOBKEEPER FORNIGHTLY

PAYMENT RATES

Hours worked by

the individual in the

reference period

30 Mar 2020 to

27 Sep 2020

28 Sep 2020 to

3 Jan 2021

4 Jan 2021 to

28 Mar 2021

80+hours

$1,500per fortnight

$1,200Per fortnight

$1,000per fortnight

<80Hours

$750Per fortnight

$650per fortnight

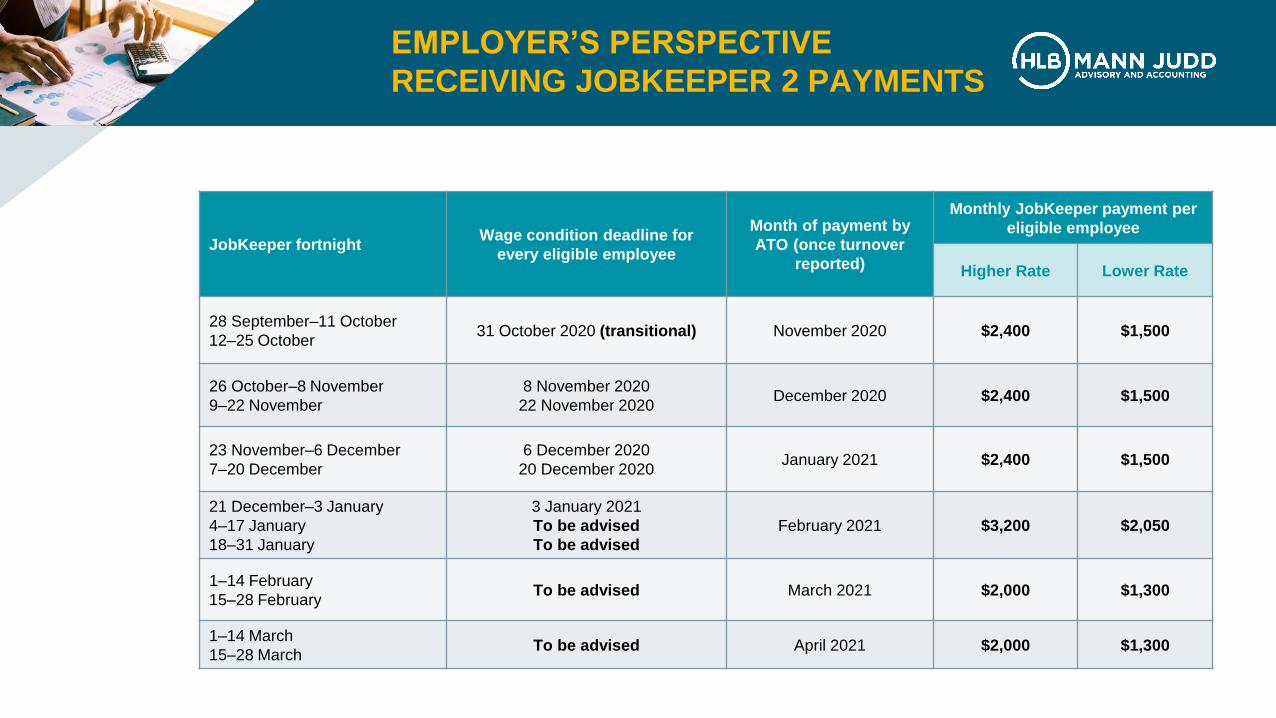

EMPLOYER’S PERSPECTIVE

RECEIVING JOBKEEPER 2 PAYMENTS

JobKeeper fortnightWage condition deadline for

every eligible employee

Month of payment by

ATO (once turnover

reported)

Monthly JobKeeper payment per

eligible employee

Higher Rate Lower Rate

28 September–11 October

12–25 October31 October 2020 (transitional) November 2020 $2,400 $1,500

26 October–8 November

9–22 November

8 November 2020

22 November 2020December 2020 $2,400 $1,500

23 November–6 December

7–20 December

6 December 2020

20 December 2020January 2021 $2,400 $1,500

21 December–3 January

4–17 January

18–31 January

3 January 2021

To be advised

To be advised

February 2021 $3,200 $2,050

1–14 February

15–28 FebruaryTo be advised March 2021 $2,000 $1,300

1–14 March

15–28 MarchTo be advised April 2021 $2,000 $1,300

NO CHANGE TO OTHER RULES

• meaning of ‘eligible employee’ (noting new 1 July 2020 employment test) and ‘eligible

business participant’

• requirement for employers to meet the wage condition

• specified percentage (DIT test) — 15% | 30% | 50%

• special rules relating to service entity arrangements

• ability of ACNC-registered charities to elect to exclude government grants from turnover

• enrolment process

• timing of monthly payment by the ATO in arrears

• monthly reporting of turnover

• rule that prevents more than one employer claiming for same employee

• tax treatment of JobKeeper payments

BASIC OR ALTERNATIVE TESTS

Basic Test• actual GST Turnover for the turnover test period quarter has declined by more

than 30% or 50% (depending on turnover).

• compare December 2020 quarter to December 2019 quarter.

Most relevant alternative tests • substantial increase in turnover test

• irregular turnover test

Current GST turnover is the amount of your sales except for the following:

• the GST you included in sales to your customers (if any)

• sales that are input taxed sales (for example, bank interest, sale of shares, residential rental

income)

• sales not connected with an enterprise that you carry on (for example, sale of private car)

• sales that are not made for payment (unless a taxable supply to an associate)

• payments for no supply (for example, JobKeeper payments)

• sales not connected with Australia, for example

o sales of services made through a business you carry on outside Australia

o sales of goods purchased and sold from a place outside Australia

o sale of real property situated outside Australia.

WHAT IS GST TURNOVER?

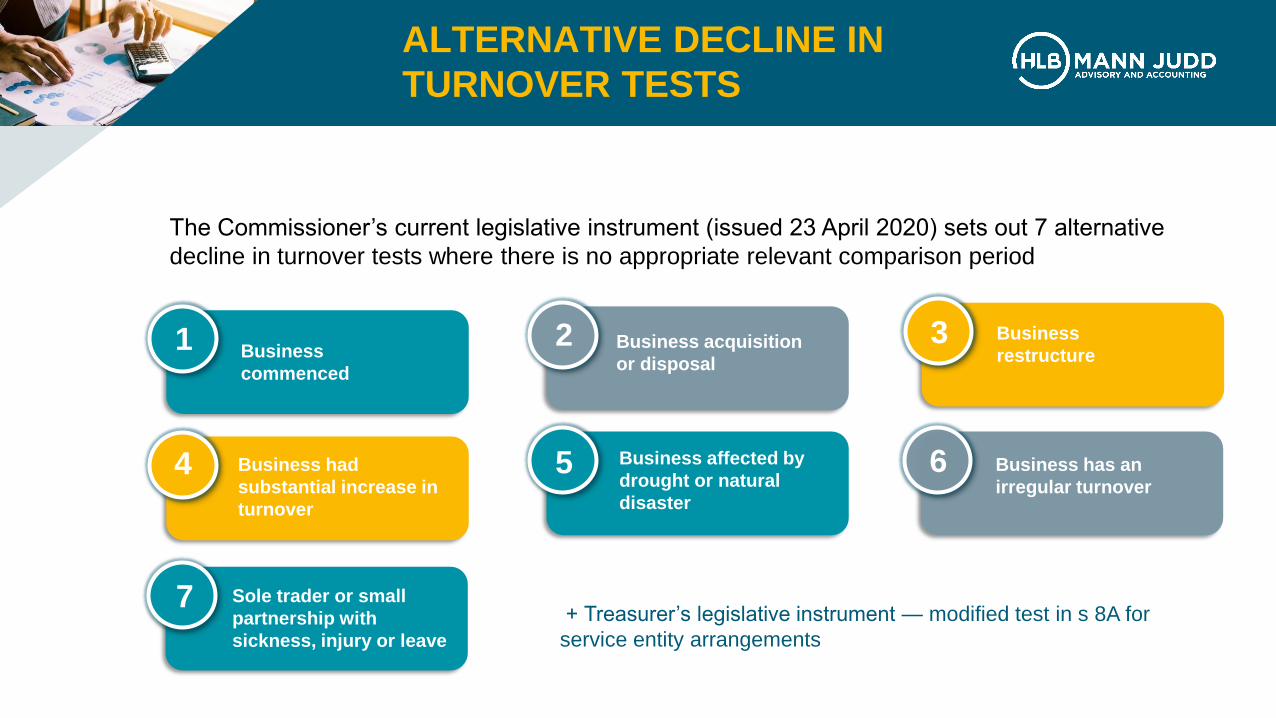

ALTERNATIVE DECLINE IN

TURNOVER TESTS

Business

commenced

The Commissioner’s current legislative instrument (issued 23 April 2020) sets out 7 alternative

decline in turnover tests where there is no appropriate relevant comparison period

1 Business acquisition

or disposal

2 Business

restructure 3

Business had

substantial increase in

turnover

4 Business affected by

drought or natural

disaster

5 Business has an

irregular turnover 6

Sole trader or small

partnership with

sickness, injury or leave

7+ Treasurer’s legislative instrument — modified test in s 8A for

service entity arrangements

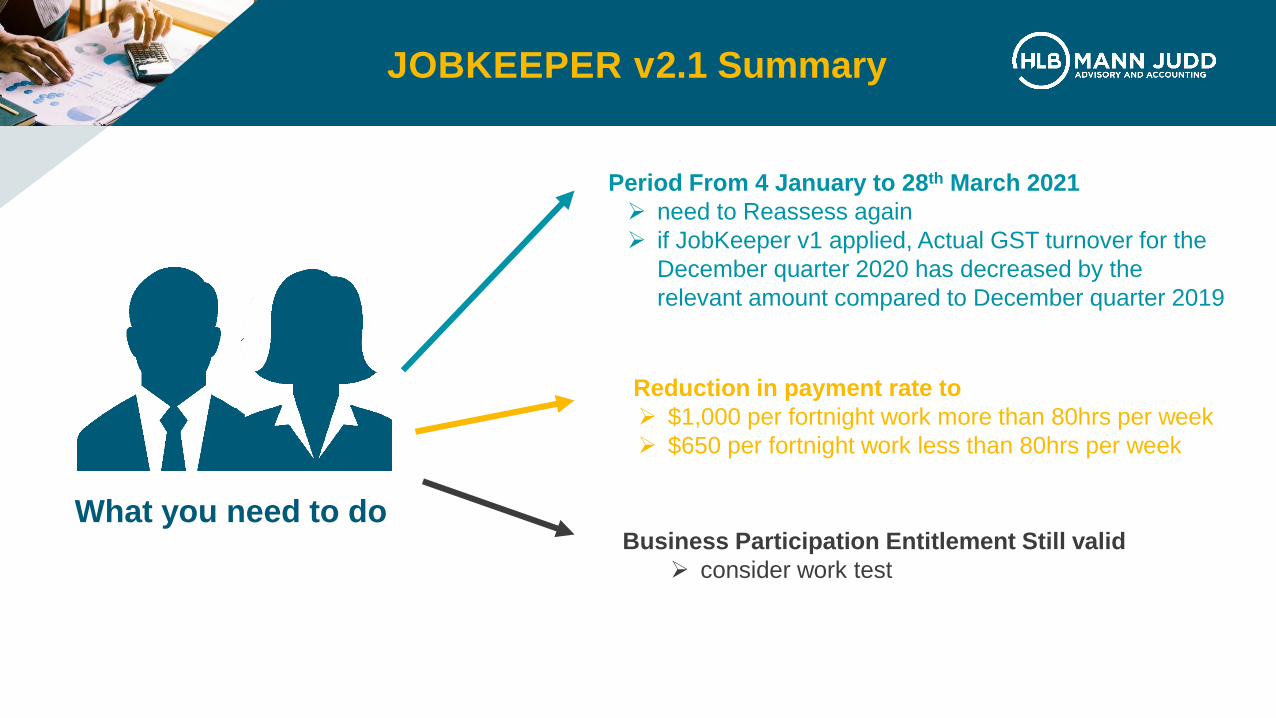

Business Participation Entitlement Still valid

➢ consider work test

JOBKEEPER v2.1 Summary

What you need to do

Period From 4 January to 28th March 2021

➢ need to Reassess again

➢ if JobKeeper v1 applied, Actual GST turnover for the

December quarter 2020 has decreased by the

relevant amount compared to December quarter 2019

Reduction in payment rate to

➢ $1,000 per fortnight work more than 80hrs per week

➢ $650 per fortnight work less than 80hrs per week

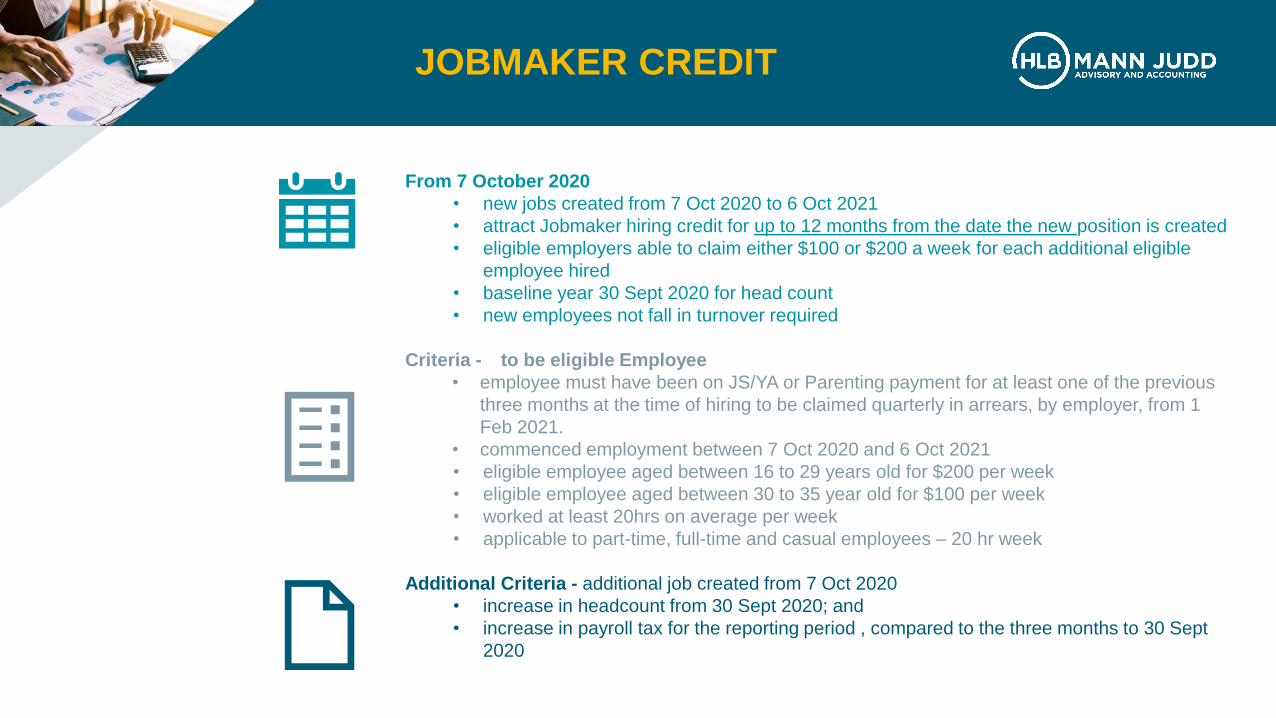

JOBMAKER CREDIT

From 7 October 2020

• new jobs created from 7 Oct 2020 to 6 Oct 2021

• attract Jobmaker hiring credit for up to 12 months from the date the new position is created

• eligible employers able to claim either $100 or $200 a week for each additional eligible

employee hired

• baseline year 30 Sept 2020 for head count

• new employees not fall in turnover required

Criteria - to be eligible Employee

• employee must have been on JS/YA or Parenting payment for at least one of the previous

three months at the time of hiring to be claimed quarterly in arrears, by employer, from 1

Feb 2021.

• commenced employment between 7 Oct 2020 and 6 Oct 2021

• eligible employee aged between 16 to 29 years old for $200 per week

• eligible employee aged between 30 to 35 year old for $100 per week

• worked at least 20hrs on average per week

• applicable to part-time, full-time and casual employees – 20 hr week

Additional Criteria - additional job created from 7 Oct 2020

• increase in headcount from 30 Sept 2020; and

• increase in payroll tax for the reporting period , compared to the three months to 30 Sept

2020

JOBMAKER CREDIT

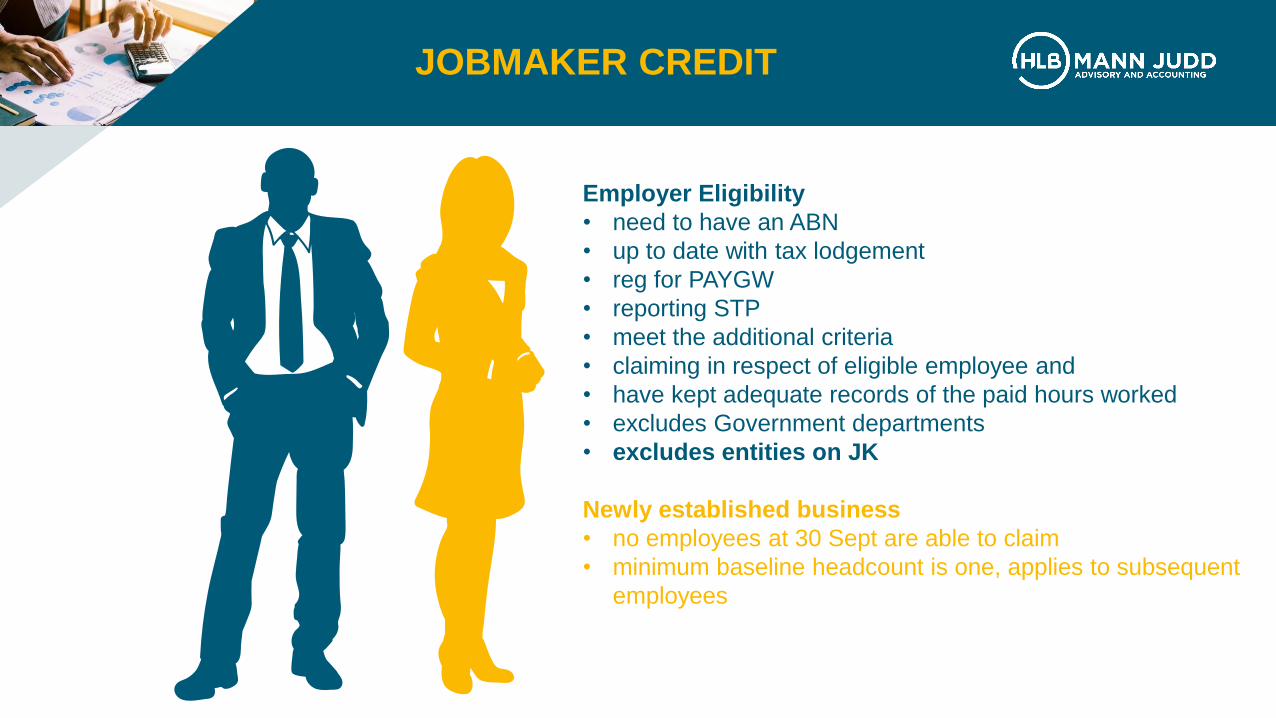

Employer Eligibility

• need to have an ABN

• up to date with tax lodgement

• reg for PAYGW

• reporting STP

• meet the additional criteria

• claiming in respect of eligible employee and

• have kept adequate records of the paid hours worked

• excludes Government departments

• excludes entities on JK

Newly established business

• no employees at 30 Sept are able to claim

• minimum baseline headcount is one, applies to subsequent

employees

JOBMAKER CREDIT

Action to Take

➢ check you are eligible employer

➢ track how many employees full time/part time/casual at 30 Sept

➢ track new employees or employee between age range

➢ don’t need to reg at time of hire

➢ reg opens in portal from 7th Dec 2020

➢ have 3 months to submit claims

➢ first reporting period of 7/10/2020 to 6/1/2021

➢ submit claims from 1 Feb 2021, should get money in Feb 2021

➢ paid 3 months in arrears, paid to employer

➢ receive $100 per week of new employee for 12months each quarter in

arrears – aged 30 to 35 years old at time of employment

➢ receive $200 per week of new employee for 12months each quarter in

arrears – aged 16 to 29 years old at time of employment

➢ at time of hire employee fills out nomination form – employer keeps

JOBMAKER CREDIT

Employer Head Count/Payroll Commentary

Baseline

30 September 2020

Payroll July - September

2

$30,000

Age 16 to 29 - $200 per week

Age 30 to 35 $100 per week

First relevant quarter

7 October 2020 – 6 June 2021

Payroll October - December

4

$60,000

2 new staff - in Oct 2020

• Emma aged 28 years - $200 per week

• Jessica aged 31 years - $100 per week

• Wage > 20 hrs average per week for the

quarter

Need nomination forms Enrol in Feb 2021 to get Jobmaker

Paid in Feb 2021

QUESTIONS

TALK TO US

If you have any further questions, or if you require assistance please

feel free to contact :

Poll Question

• I would like someone from HLB Mann Judd to contact me regarding the

following…

MARIANA VON-LUCKEN

PARTNER, TAX CONSULTING

HLB MANN JUDD

P: +61 (0)2 9020 4095

ALEX KING

DIRECTOR, TAX CONSULTING

HLB MANN JUDD

P: +61 (0)2 9020 4345