Page 1

Update on New York’s No-Fault Fraud & Abuse Problem

New York Alliance Against Insurance FraudInsurance Fraud Briefing

Albany, NYMarch 25, 2003

Robert P. Hartwig, Ph.D., CPCU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Page 2

Insurance Fraud in the U.S. Costs Billions!

Prop./Casualty$22.4 billion

23%

Disability$0.5 billion

1%

Life$11.8 billion

12%

Health$61.4 billion

64%

Total Fraud Costs = $96.2 Billion

Source: Conning & Co.

Page 3

Comparative Statistics: PIP Claims Costs

Page 4

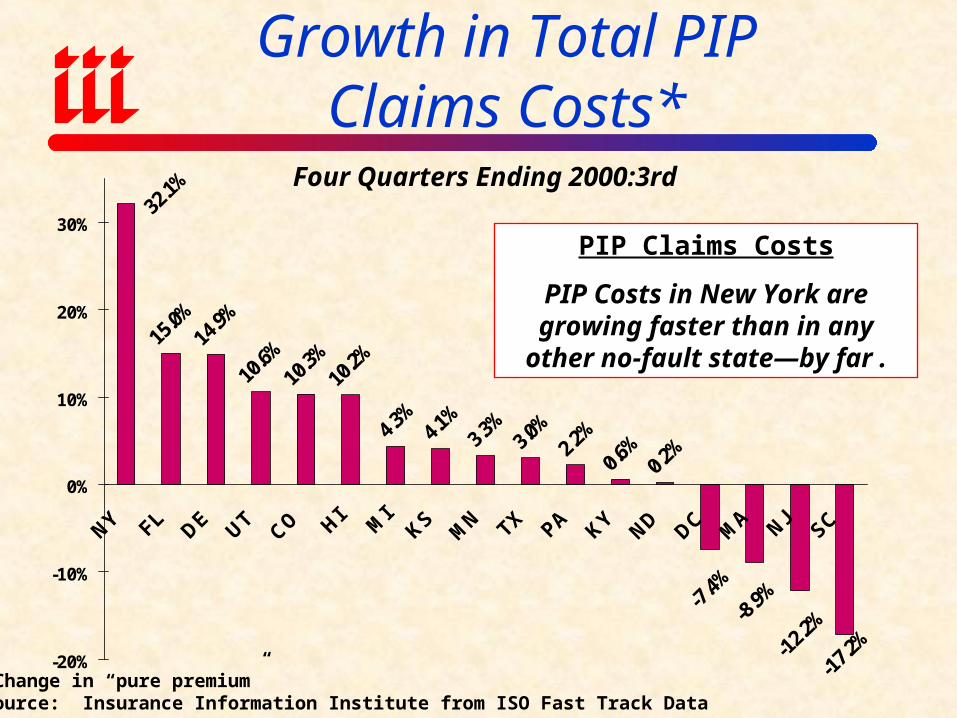

15.0%

14.9%

10.6%

10.3%

10.2%

4.3%

4.1%

3.3%

3.0%

2.2%

0.6%

0.2%

-7.4%

-8.9%

-12.2

%

-17.2

%

32.1%

-20%

-10%

0%

10%

20%

30%

NY FL DE UTCO HI M

IKS

MN TX PA KY

ND DC MA NJ

SC

Growth in Total PIPClaims Costs*

*Change in “pure premium”Source: Insurance Information Institute from ISO Fast Track Data

PIP Claims Costs

PIP Costs in New York are growing faster than in any other no-fault

state—by far .

Four Quarters Ending 2000:3rd

Page 5

18.0%

17.3%

14.2%

12.9%

10.5%

9.9%

4.3%

4.2%

4.1%

2.9%

-5.3%

-5.5%

-11.9

%

-13.9

%

28.5%

-1.6%-0

.1%

-20%

-10%

0%

10%

20%

30%

NYCO DE FL HI

UT MI

MA

MN TX PA KY KS

ND SC NJDC

Growth in Total PIPClaims Costs*

*Change in “pure premium”Source: Insurance Information Institute from ISO Fast Track Data

PIP Claims Costs

PIP Costs in New York grew faster than in any other no-fault state—by

far .

Four Quarters Ending 2000:4th

Page 6

24.7%

19.5%

14.4%

14.0%

13.0%

11.3%

5.8%

5.5%

5.4%

4.7%

0.7%

-3.6%

-3.0%-2

.4%

28.6%

1.1%2.6

%

-20%

-10%

0%

10%

20%

30%

SC MA

ND DECO FL M

IPA KY TX HI

MN UT NY

DC NJKS

Growth in Total PIPClaims Costs*

*Change in “pure premium”Source: Insurance Information Institute from ISO Fast Track Data

PIP Claims Costs

Growth NY’s PIP Costs slowed significantly during the first half of

2001.

Four Quarters Ending 2001:2nd

Page 7

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Growth in Total PIPClaims Costs*

*Change in “pure premium”Source: Insurance Information Institute from ISO Fast Track Data

PIP Claims Costs

Growth NY’s PIP Costs are began to rise again after slowing during late 2001, early 2002

Four Quarters Ending 2002:3rd

Page 8

Private Passenger Auto:6 Least Profitable States, 2000

(Profit as a % of Direct Premium Earned)

7.7

-1.2

-2.6-3.2 -3.3

-4.0

-9.8-10

-8

-6

-4

-2

0

2

4

6

8

U.S. New York Texas Montana Florida S. Carolina Louisiana

Source: NAIC; Insurance Information Institute

•NY ranked 44th in terms of profitability in 2000

•FL ranked 48th

Page 9

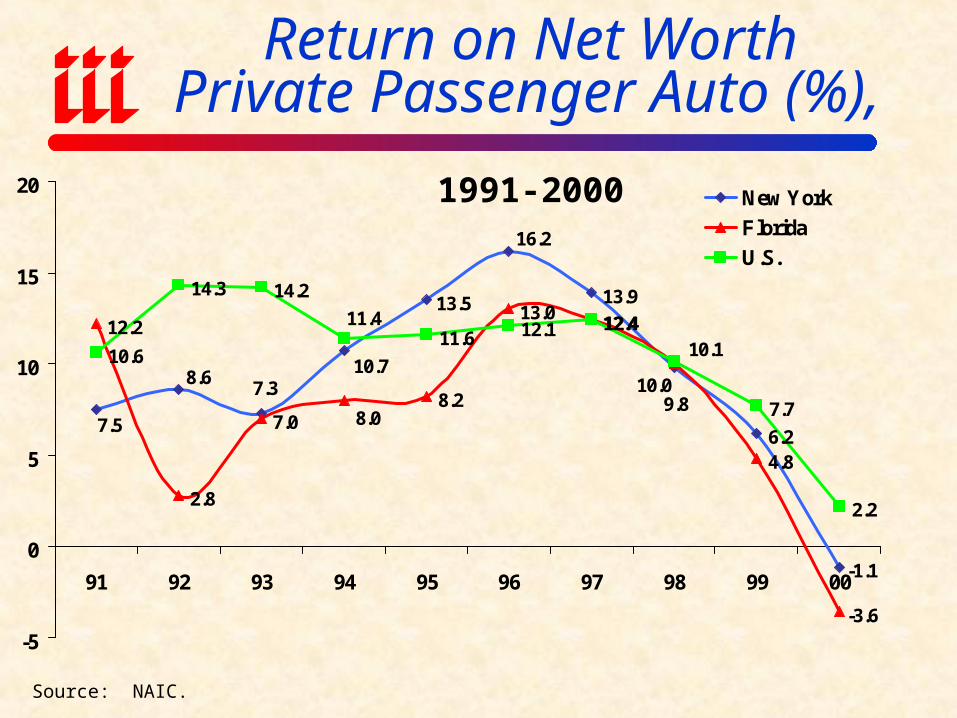

Return on Net WorthPrivate Passenger Auto (%),

13.9

6.2

-1.1

12.2

2.8

7.08.2

13.012.4

4.8

-3.6

10.6

14.3 14.2

11.6 12.1 12.4

7.7

2.2

9.8

16.2

13.5

10.77.3

8.6

7.5

10.0

8.0

10.1

11.4

-5

0

5

10

15

20

91 92 93 94 95 96 97 98 99 00

New York

Florida

U.S.

Source: NAIC.

1991-2000

Page 10

PIP Fraud and Abuse in New York State

Page 11

0%

50%

100%

150%

200%

250%

300%

U.S. New York

*Through 4 quarters ending 2000:3rd.Source: American Insurance Association/ISO FastTrack; Insurance Information Institute

Change in PIP Loss Costs:New York vs. US:1987-2000*

By 2000, growth in New York PIP loss costs were more than twice (121%) the national average.

Page 12

0%

50%

100%

150%

200%

250%

U.S. New York

*Through 4 quarters ending 2002:3rd.Source: American Insurance Association/ISO FastTrack; Insurance Information Institute

Change in PIP Loss Costs:New York vs. US:1993-2002*

In 2002:III, cumulative growth in New York PIP loss costs were nearly twice (+89% above) the national average.

Page 13

Year Ending 2001:2nd2.27 2.26

2.11

1.90 1.87 1.86 1.801.68

1.60 1.60

0.0

0.5

1.0

1.5

2.0

2.5

NY MA CO FL DE UT MN NJ HI US*

*US excludes New York and Florida

Personal Injury Protection Paid Claim Frequency

Source: Insurance Information Institute and Insurance Services Office.

PIP frequency was 42% above the US average

Page 14

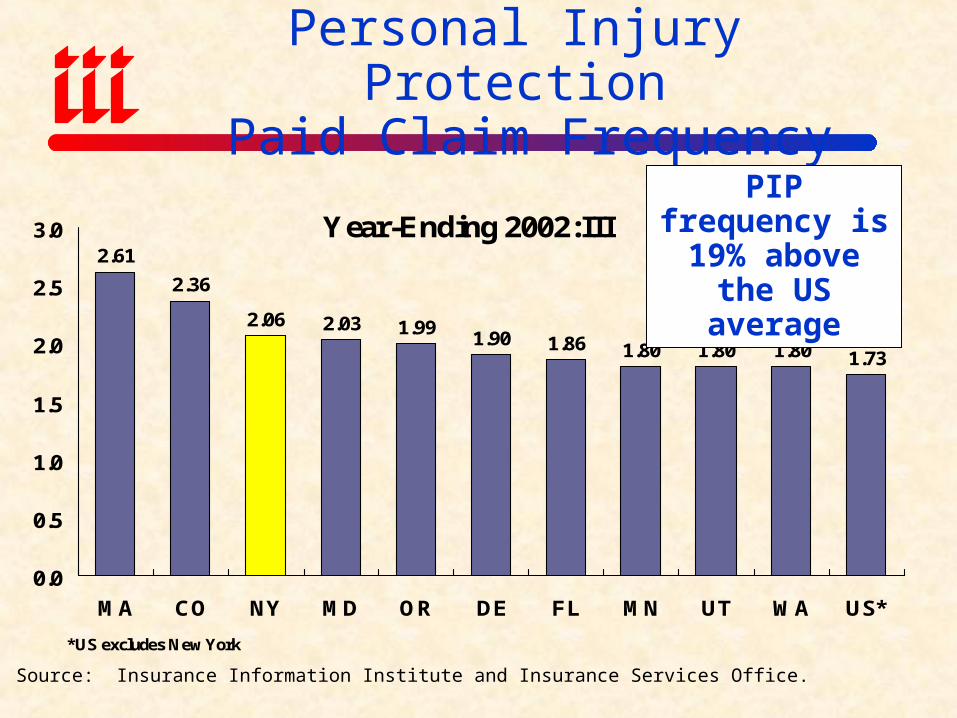

Year-Ending 2002:III2.61

2.36

2.06 2.03 1.991.90 1.86 1.80 1.80 1.80 1.73

0.0

0.5

1.0

1.5

2.0

2.5

3.0

MA CO NY MD OR DE FL MN UT WA US*

*US excludes New York

Personal Injury Protection Paid Claim Frequency

Source: Insurance Information Institute and Insurance Services Office.

PIP frequency is 19% above the

US average

Page 15

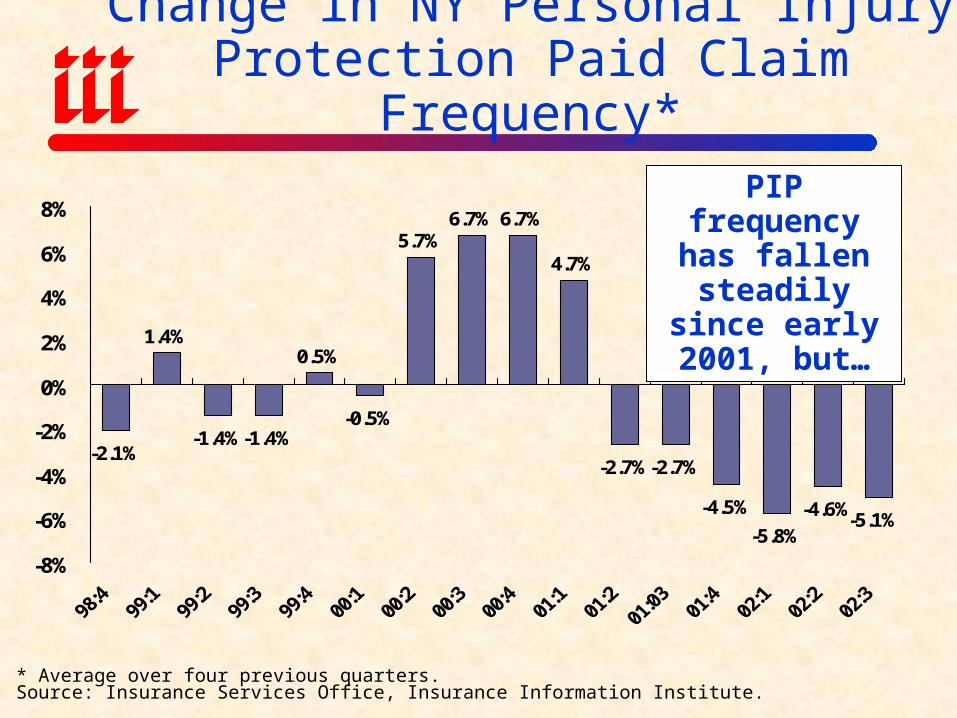

-2.1%

1.4%

-1.4%-1.4%

0.5%

-0.5%

5.7%6.7% 6.7%

4.7%

-2.7%-2.7%

-4.5%

-5.8%

-4.6%-5.1%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Change in NY Personal Injury Protection Paid Claim Frequency*

* Average over four previous quarters.Source: Insurance Services Office, Insurance Information Institute.

PIP frequency has fallen

steadily since early 2001, but…

Page 16

6.8%

1.2%4.1%

6.9%

10.5%

17.0%

21.7%23.9%

19.9%

14.9%

3.0%

-6.2%-5.3%-3.2%

3.5%

11.0%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Change in NY Personal Injury Protection Average Loss (Severity)*

PIP severity is rising at double-digit rates again after a brief lull, more than offsetting lower

frequency

* Average over four previous quarters.Source: Insurance Services Office, Insurance Information Institute.

Page 17

-2.1

%

1.4

%

-1.4

%

-1.4

%

0.5

%

-0.5

%

5.7

%

6.7

%

6.7

%

4.7

%

-2.7

%

-2.7

%

-4.5

%

-5.8

%

-4.6

%

-5.1

%

6.8

%

1.2

% 4.1

% 6.9

% 10.5

%

17.0

% 21.7

%

23.9

%

19.9

%

14.9

%

3.0

%

-6.2

%

-5.3

%

-3.2

%

3.5

%

11.0

%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%PIP Frequency PIP Severity

Change in NY Personal Injury Protection Claim Frequency & Average Loss*

PIP frequency and severity

were falling by the 2nd half of

2001; now diverging

* Average over four previous quarters.Source: Insurance Services Office, Insurance Information Institute.

Page 18

$4,862 $4,969

$5,675$6,064

$6,700

$8,335

$3,976$4,183 $4,352

$4,699$4,963

$4,523

1995 1996 1997 1998 1999 2000

New York

Other No-Fault States*

* Excluding Michigan

Average PIP Claim

PIP Claim Severity 1995-2000:New York vs. United States

Source: Fast Track Monitoring System, Fourth Quarter 2000 Report

Page 19

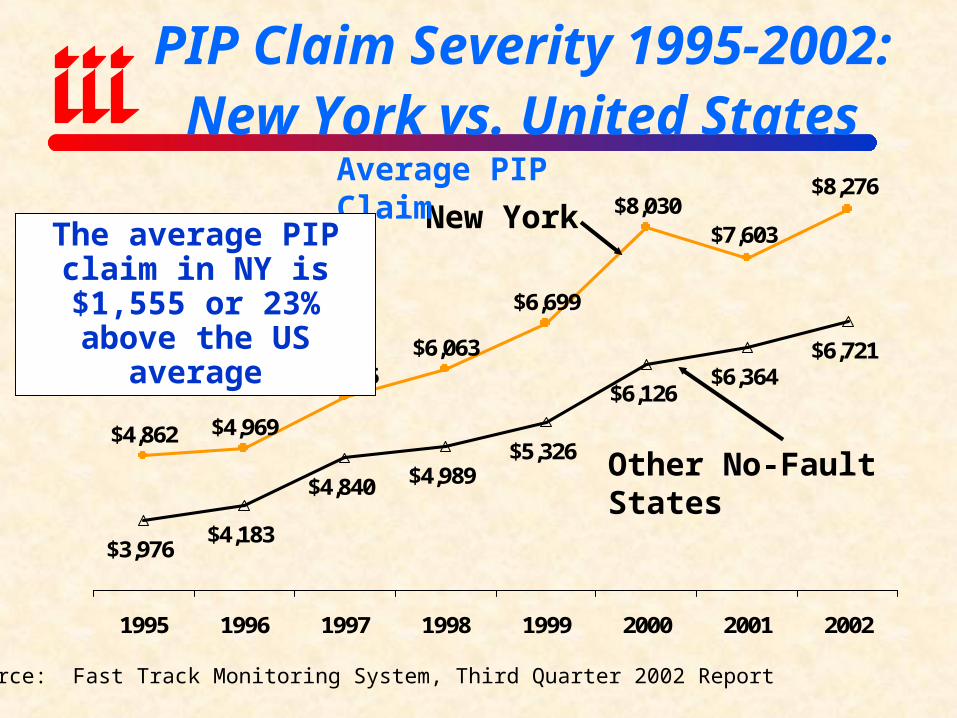

$4,862 $4,969

$5,675$6,063

$6,699

$8,030$7,603

$8,276

$3,976$4,183

$4,840

$5,326

$6,126$6,364

$6,721

$4,989

1995 1996 1997 1998 1999 2000 2001 2002

New York

Other No-Fault States

Average PIP Claim

PIP Claim Severity 1995-2002:New York vs. United States

Source: Fast Track Monitoring System, Third Quarter 2002 Report

The average PIP claim in NY is $1,555 or 23% above the US average

Page 20

Impact on Cost of Auto Insurance in New York State

Page 21

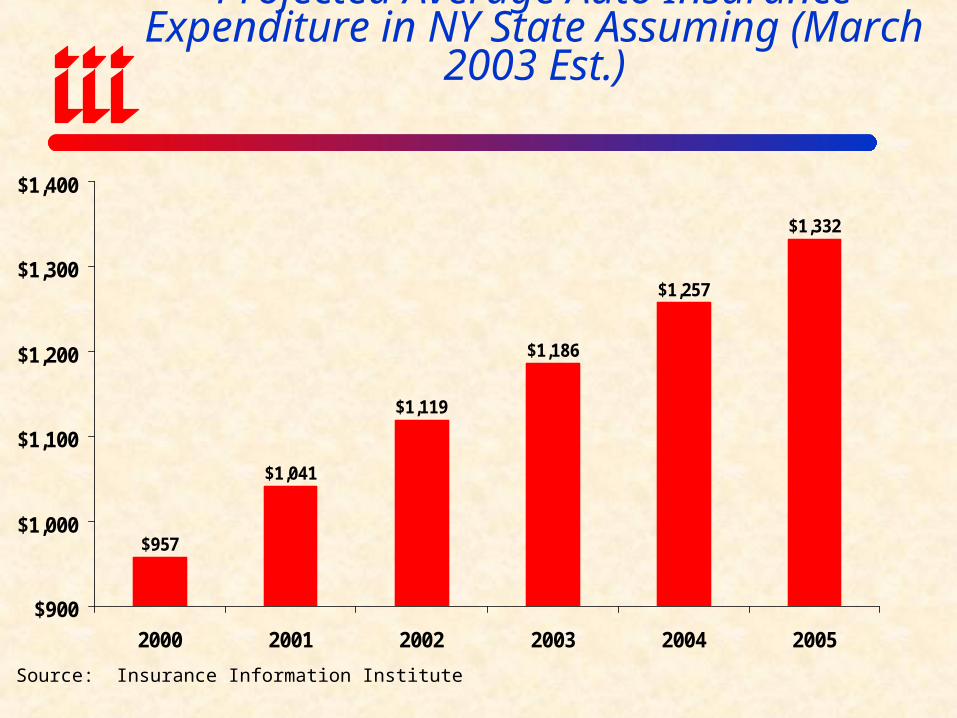

Projected Average Auto Insurance Expenditure in NY State Assuming (March 2003 Est.)

$957

$1,041

$1,119

$1,186

$1,257

$1,332

$900

$1,000

$1,100

$1,200

$1,300

$1,400

2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

Page 22

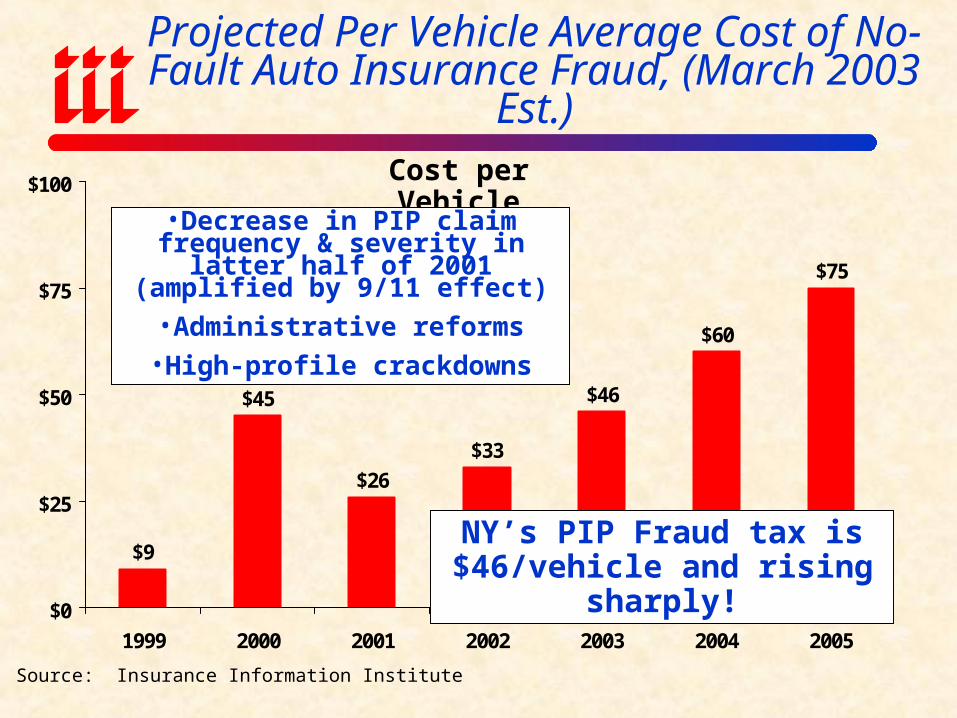

Projected Per Vehicle Average Cost of No-Fault Auto Insurance Fraud, (March 2003 Est.)

$9

$45

$26

$33

$46

$60

$75

$0

$25

$50

$75

$100

1999 2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

Cost per Vehicle

•Decrease in PIP claim frequency & severity in latter half of 2001

(amplified by 9/11 effect)•Administrative reforms

•High-profile crackdowns

NY’s PIP Fraud tax is $46/vehicle and rising sharply!

Page 23

Annual Cost of No-Fault Auto Insurance Fraud in NY, (March 2003 Est.)

$77

$388

$238

$309

$432

$572

$732

$0

$250

$500

$750

$1,000

1999 2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

$ Millions

No-fault fraud will cost drivers in NY state $432 million in 2003,

or $1.2 million per day.

Page 24

Cumulative Cost of No-Fault Auto Insurance Fraud in NY, (March 2003 Est.)

$77

$466

$704

$1,013

$1,445

$2,017

$2,748

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1999 2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

$ Millions

No-fault fraud has cost NY insurers and policyholder more

than $1 billion dollars so far through 2002.

Page 25

No-Fault Fraud Statistics in New York State

Page 26

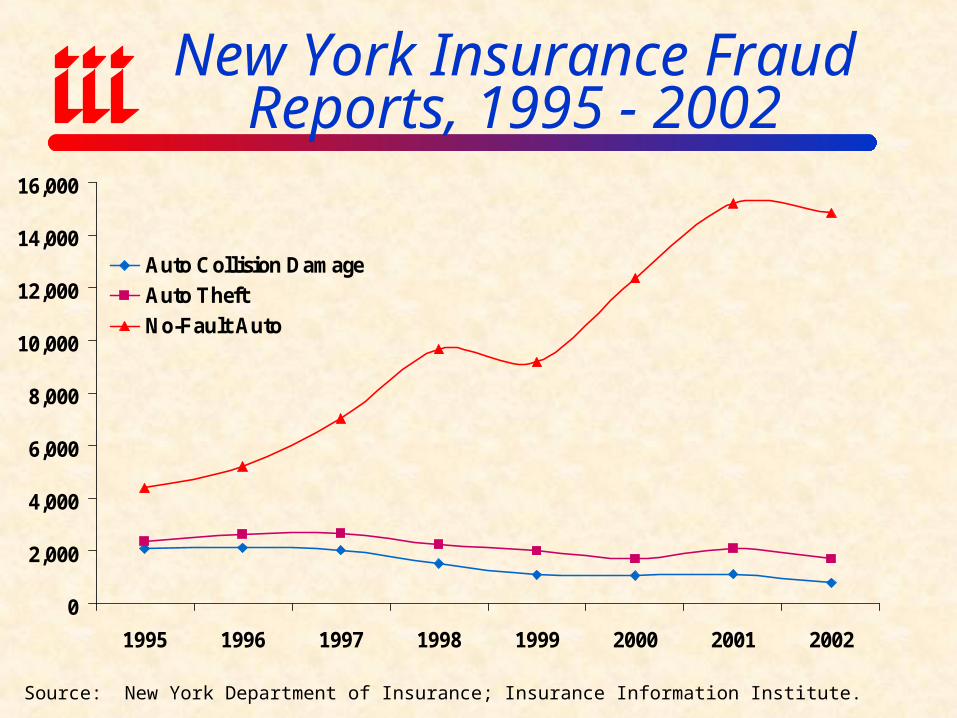

New York Insurance Fraud Reports, 1995 - 2002

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1995 1996 1997 1998 1999 2000 2001 2002

Auto Collision Damage

Auto Theft

No-Fault Auto

Source: New York Department of Insurance; Insurance Information Institute.

Page 27

New York Insurance Fraud Reports, 1995 - 2002

1,7331,086

4,3935,214

7,042

9,6599,191

12,372

15,219 14,852

862798661698758851

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1995 1996 1997 1998 1999 2000 2001 2002

Workers' Compensation

No-Fault Auto

Source: New York Department of Insurance; Insurance Information Institute.

Page 28

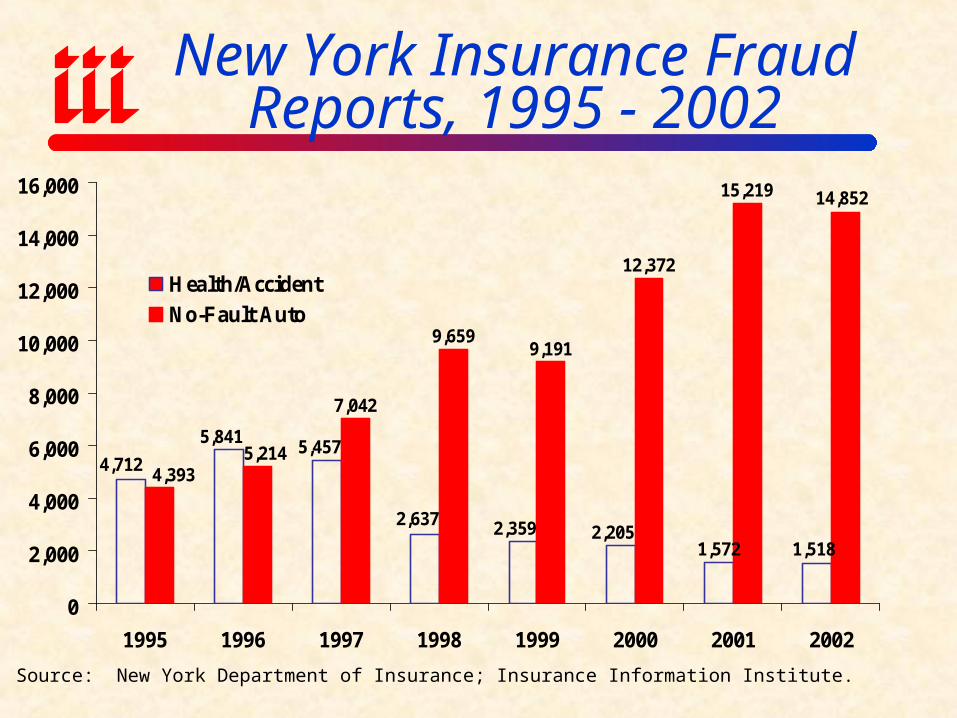

New York Insurance Fraud Reports, 1995 - 2002

1,572 1,518

7,042

9,6599,191

12,372

15,219 14,852

2,2052,3592,637

5,4575,841

4,7125,214

4,393

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1995 1996 1997 1998 1999 2000 2001 2002

Health/Accident

No-Fault Auto

Source: New York Department of Insurance; Insurance Information Institute.

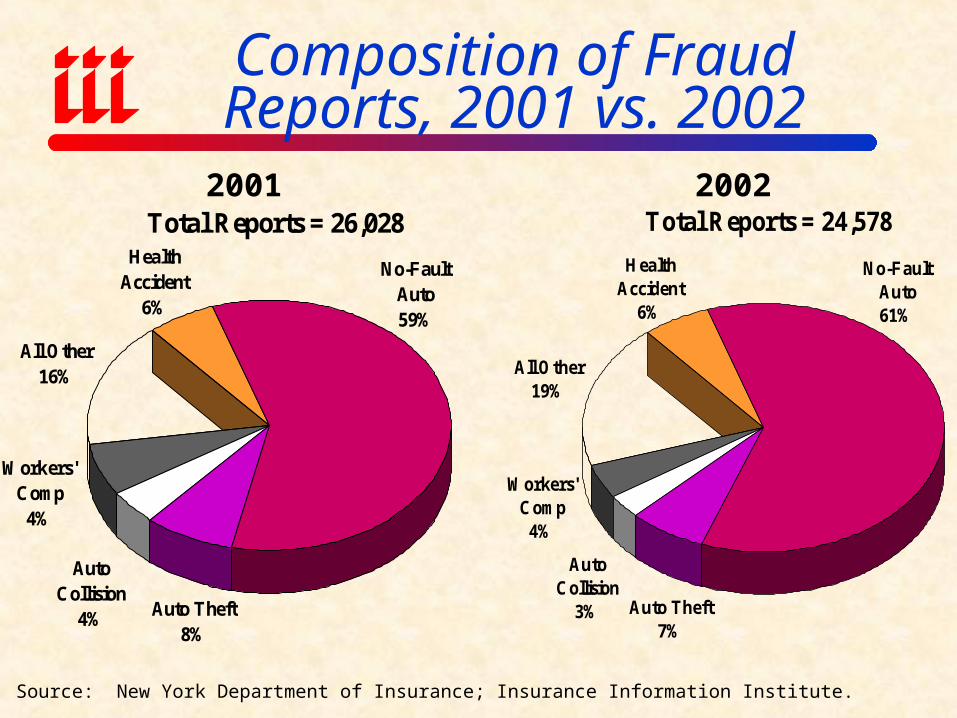

Page 29

Total Reports = 26,028

No-Fault Auto59%

Auto Theft8%

Auto Collision

4%

Health Accident

6%

Workers' Comp

4%

All Other16%

Composition of Fraud Reports, 1995 vs. 2001

2001Total Reports = 20,205

Workers' Comp3.9%

All Other29%

Health Accident

23%

AutoTheft7.6%

Auto Collision

10%No-Fault Auto22%

1995

Source: New York Department of Insurance; Insurance Information Institute.

Page 30

Total Reports = 26,028

No-Fault Auto59%

Auto Theft8%

Auto Collision

4%

Health Accident

6%

Workers' Comp

4%

All Other16%

Composition of Fraud Reports, 2001 vs. 2002

20022001

Source: New York Department of Insurance; Insurance Information Institute.

Total Reports = 24,578

All Other19%

Workers' Comp

4%

Health Accident

6%

Auto Collision

3% Auto Theft7%

No-Fault Auto61%

Page 31

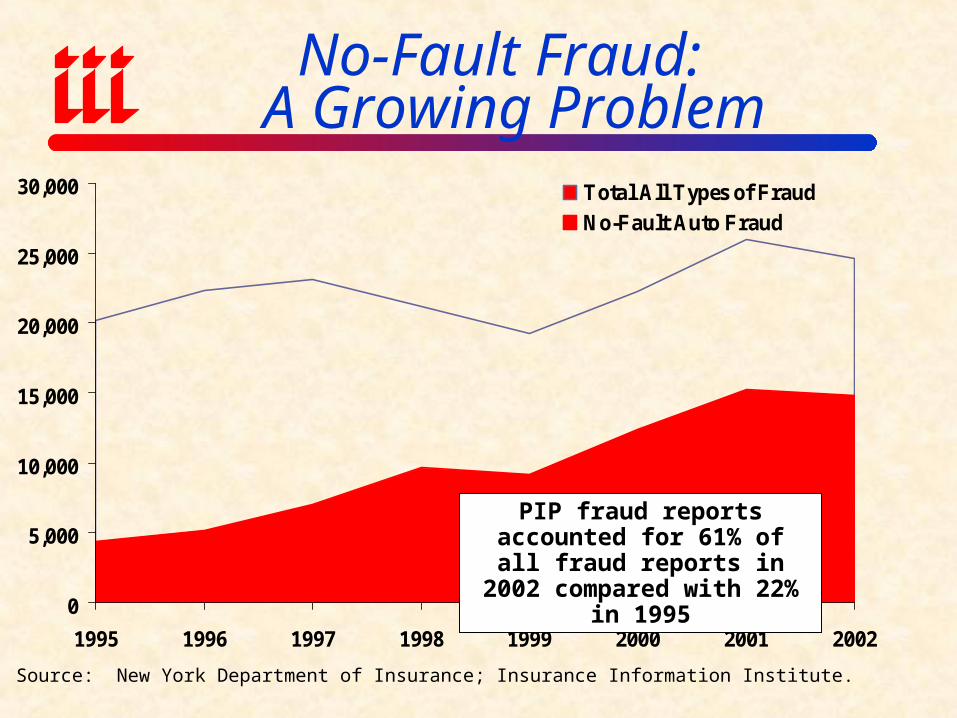

No-Fault Fraud: A Growing Problem

0

5,000

10,000

15,000

20,000

25,000

30,000

1995 1996 1997 1998 1999 2000 2001 2002

Total All Types of Fraud

No-Fault Auto Fraud

Source: New York Department of Insurance; Insurance Information Institute.

PIP fraud reports accounted for 61% of all fraud reports in 2002

compared with 22% in 1995

Page 32

Insurance Information Institute On-Line

Page 33

Projected Average Auto Insurance Expenditure in NY State Assuming No Meaningful Reform

(Jan. 2002 Est.)

$957

$1,096

$1,210

$1,317

$1,439

$1,578

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

Page 34

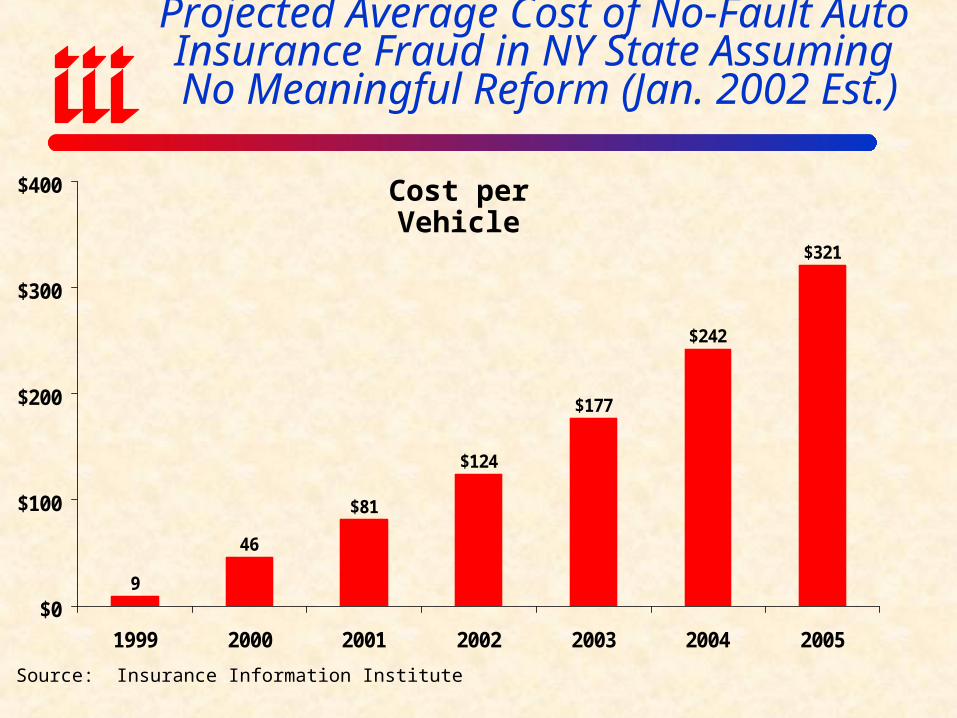

Projected Average Cost of No-Fault Auto Insurance Fraud in NY State Assuming No Meaningful Reform (Jan. 2002 Est.)

9

46

$81

$124

$177

$242

$321

$0

$100

$200

$300

$400

1999 2000 2001 2002 2003 2004 2005

Source: Insurance Information Institute

Cost per Vehicle