18

US Coal Export Market and Terminal Saurabh Pandey Director of Business Development SunCoke Energy Platts Coal Marketing Days Sept 22-23, 2014

US Coal Export Market and Terminal

Saurabh Pandey

Director of Business Development

SunCoke Energy

Platts Coal Marketing Days

Sept 22-23, 2014

TM

2

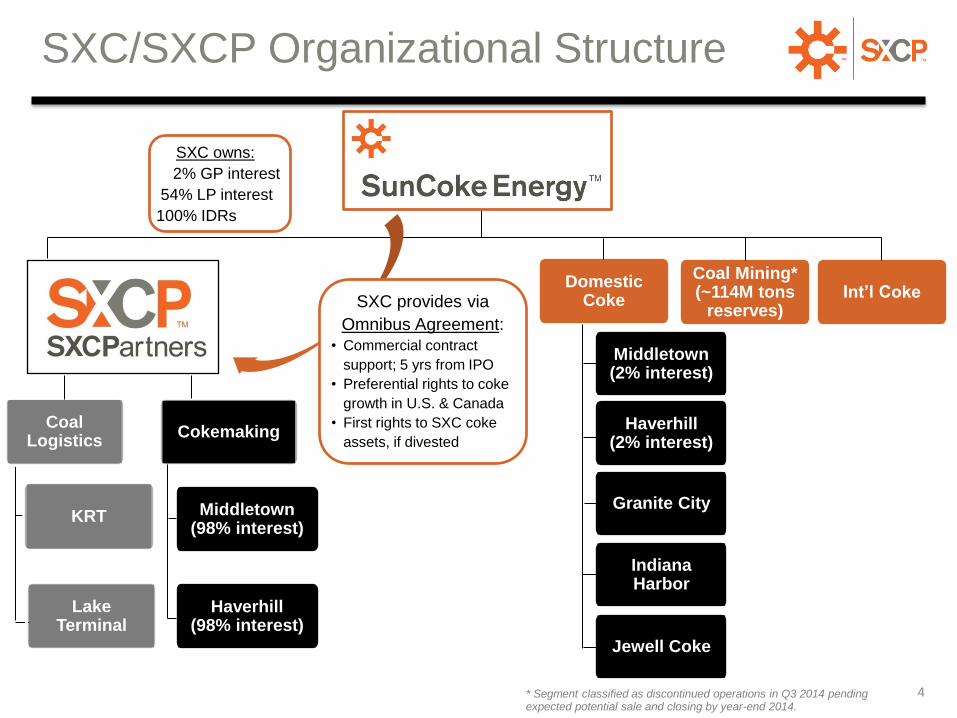

SXC and SXCP

TM

Odisha, India

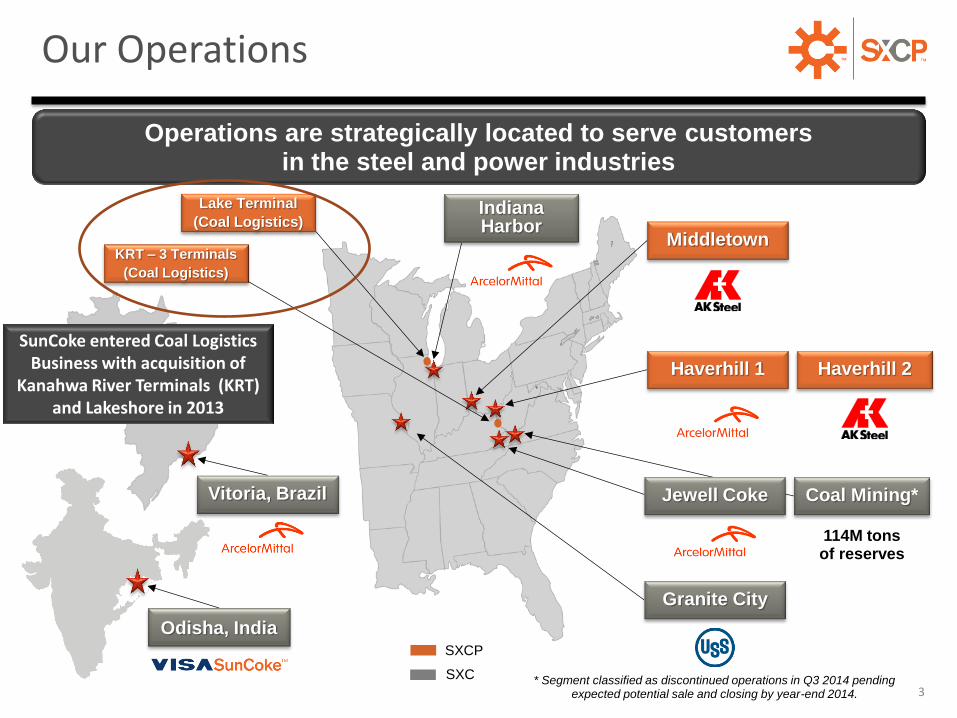

Operations are strategically located to serve customers in the steel and power industries

3

Middletown

Haverhill 1 Haverhill 2

Granite City

Coal Mining* Jewell Coke

Indiana Harbor

Vitoria, Brazil

114M tons of reserves

Lake Terminal

(Coal Logistics)

KRT – 3 Terminals

(Coal Logistics)

SXCP

SXC * Segment classified as discontinued operations in Q3 2014 pending expected potential sale and closing by year-end 2014.

Our Operations

SunCoke entered Coal Logistics Business with acquisition of

Kanahwa River Terminals (KRT) and Lakeshore in 2013

TM

4

Middletown (98% interest)

SXC owns:

2% GP interest

54% LP interest

100% IDRs

Haverhill (98% interest)

Cokemaking Coal

Logistics

Coal Mining* (~114M tons

reserves) Int’l Coke

Haverhill (2% interest)

Middletown (2% interest)

Indiana Harbor

Jewell Coke

Granite City

Domestic Coke

KRT

Lake Terminal

SXC provides via

Omnibus Agreement:

• Commercial contract

support; 5 yrs from IPO

• Preferential rights to coke

growth in U.S. & Canada

• First rights to SXC coke

assets, if divested

* Segment classified as discontinued operations in Q3 2014 pending expected potential sale and closing by year-end 2014.

SXC/SXCP Organizational Structure

TM

5

Area of focus Cokemaking Coal Logistics Iron Ore Processing

Strategy

Greenfield development and/or acquisition of existing cokemaking

facilities with long-term off-take agreements

Acquisition or development

of selective coal handling & processing assets,

with long-term off-take arrangements

and limited commodity exposure

Investment in ferrous side of steel value chain, such as in concentrating, pelletizing and

transport/handling of iron ore

• Production ramp-up at Indiana Harbor • Received permit for

new plant in May 2014

• Exploring greenfield development opportunities

• Evaluating potential greenfield DRI opportunities

• Preferential rights to cokemaking growth opportunities

• Two acquisitions completed • Evaluating targeted

opportunities

• Received favorable rulings on qualifying income status of concentrating & pelletizing and DRI

Growth Strategy

TM

• Access to all U.S. East Coast, Gulf Coast and Great Lakes ports; Two railroads at Ceredo – CSX and NS

• Serves 2 SunCoke facilities as well as steel, coal and utility companies

• Provides precision blending services

• Acquired for $86M

6

SunCoke Coal Logistics - KRT

Ceredo Coal Terminal

• Throughput Capacity: 18M tons/year

• Storage Capacity: 425K tons

• Rail/Barge in; Rail/Barge out

Kentucky Coal Terminal

• Throughput Capacity: 6M tons/year

• Storage Capacity: 250K tons

• Truck in; Barge out

Ceredo Liquids Terminal

• Three 250K gallon finished prod tanks

• Four heated 1M gallon raw storage tanks

• Truck, Barge, Rail in/out

Quincy Coal Terminal

• Throughput Capacity: 6M tons/year

• Storage Capacity: 250K tons

• Truck in; Rail/Barge out

TM

Asset

•Coal blending site adjacent to SunCoke’s Indiana Harbor facility

•10-year contract to provide services to Indiana Harbor

Location East Chicago, Indiana

Acquisition Price

$29.4 million

7

SunCoke Coal Logistics - Lakeshore

TM

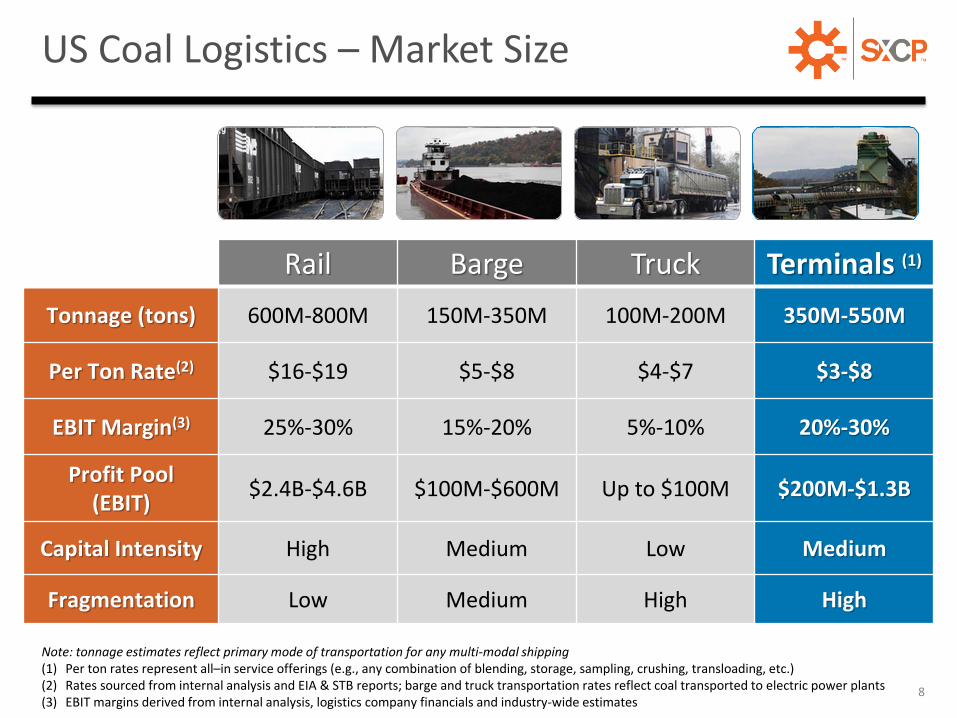

Note: tonnage estimates reflect primary mode of transportation for any multi-modal shipping (1) Per ton rates represent all–in service offerings (e.g., any combination of blending, storage, sampling, crushing, transloading, etc.) (2) Rates sourced from internal analysis and EIA & STB reports; barge and truck transportation rates reflect coal transported to electric power plants (3) EBIT margins derived from internal analysis, logistics company financials and industry-wide estimates

Rail Barge Truck Terminals (1)

Tonnage (tons) 600M-800M 150M-350M 100M-200M 350M-550M

Per Ton Rate(2) $16-$19 $5-$8 $4-$7 $3-$8

EBIT Margin(3) 25%-30% 15%-20% 5%-10% 20%-30%

Profit Pool (EBIT)

$2.4B-$4.6B $100M-$600M Up to $100M $200M-$1.3B

Capital Intensity High Medium Low Medium

Fragmentation Low Medium High High

8

US Coal Logistics – Market Size

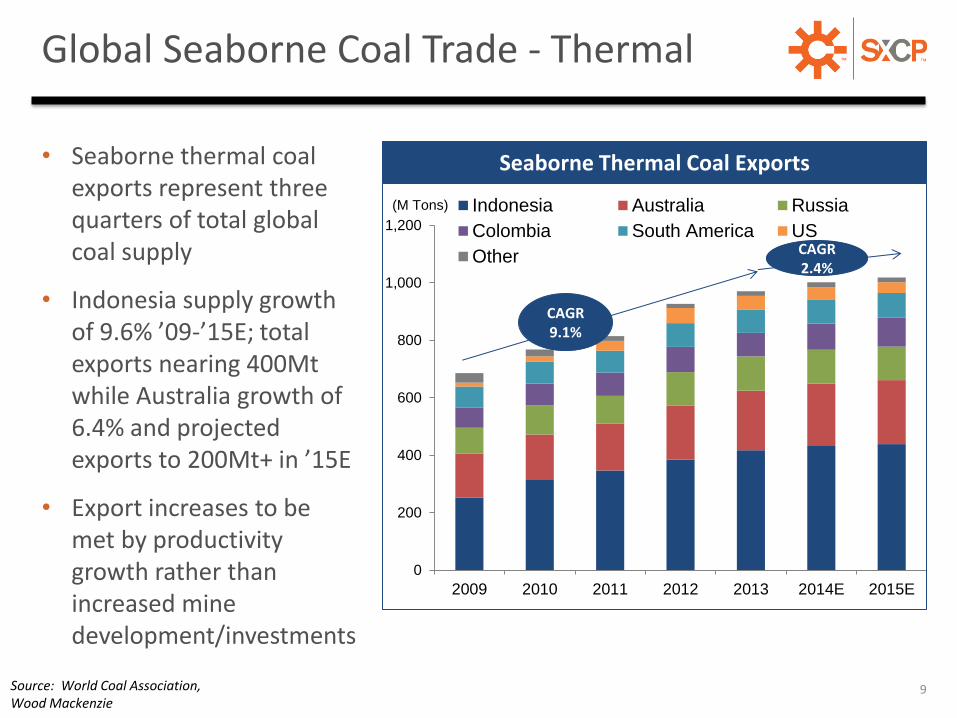

TM Global Seaborne Coal Trade - Thermal

• Seaborne thermal coal exports represent three quarters of total global coal supply

• Indonesia supply growth of 9.6% ’09-’15E; total exports nearing 400Mt while Australia growth of 6.4% and projected exports to 200Mt+ in ’15E

• Export increases to be met by productivity growth rather than increased mine development/investments

9 Source: World Coal Association,

Wood Mackenzie

0

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014E 2015E

Indonesia Australia Russia

Colombia South America US

Other

Seaborne Thermal Coal Exports

(M Tons)

CAGR 2.4%

CAGR 9.1%

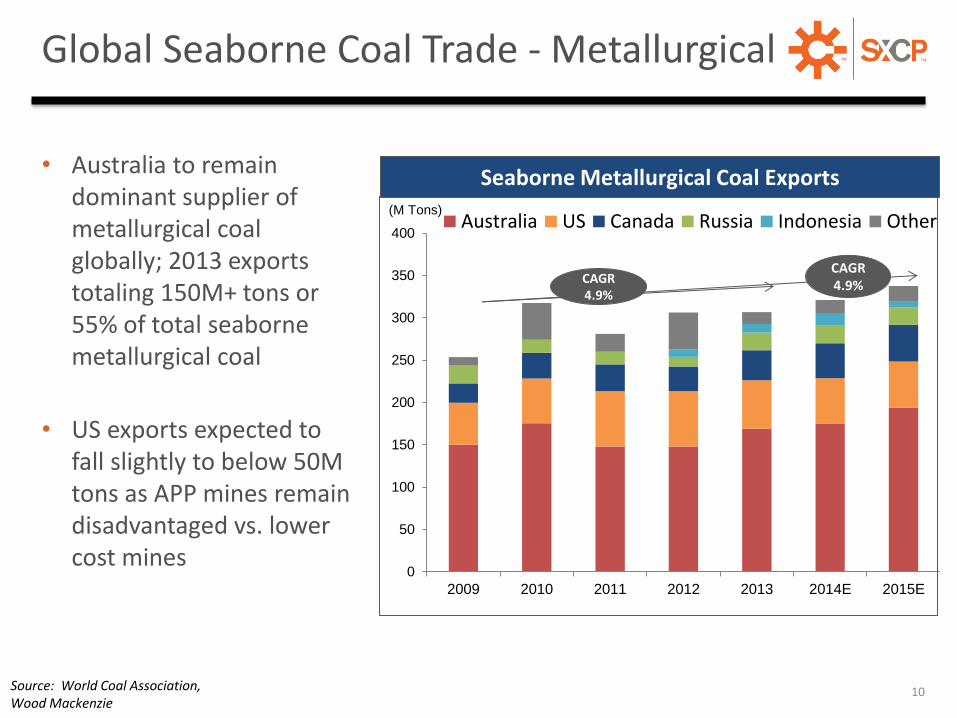

TM Global Seaborne Coal Trade - Metallurgical

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014E 2015E

Australia US Canada Russia Indonesia Other

Seaborne Metallurgical Coal Exports

10

• Australia to remain dominant supplier of metallurgical coal globally; 2013 exports totaling 150M+ tons or 55% of total seaborne metallurgical coal

• US exports expected to fall slightly to below 50M tons as APP mines remain disadvantaged vs. lower cost mines

Source: World Coal Association, Wood Mackenzie

(M Tons)

CAGR 4.9% CAGR

4.9%

TM US Coal Exports

• Europe is the largest importer of thermal coal from the US

• Europe and Asia followed by S. America are the largest importers of US Met coal

• China’s import growth expected to slow as domestic production increases, steel production growth slows, new environmental regulations implemented

• Slight European decline in Met imports in 2013 driven primarily by decreased steel production

11

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013

Americas Europe Asia Other

Met Coal Exports by Destination (M Tons)

Source: EIA short-term energy outlook

0

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013

Americas Europe Asia Other

Thermal Coal Exports by Destination (M Tons)

TM East Coast Export Volume

12

-

10

20

30

40

50

60

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Mil

Sho

rt t

on

s

Coal Exports from Norfolk, VA

-

10

20

30

40

50

60

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Mil

Sho

rt t

on

s

Coal Exports from Baltimore, MD

Source: EIA

Export from the five major E. Coast terminals has grown significantly adding both steam and met exports to Europe, Brazil, and Asia; expected to drop-off in ‘14 & ‘15

0%

20%

40%

60%

80%

100%

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Steam Met

0%

20%

40%

60%

80%

100%

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Steam Met

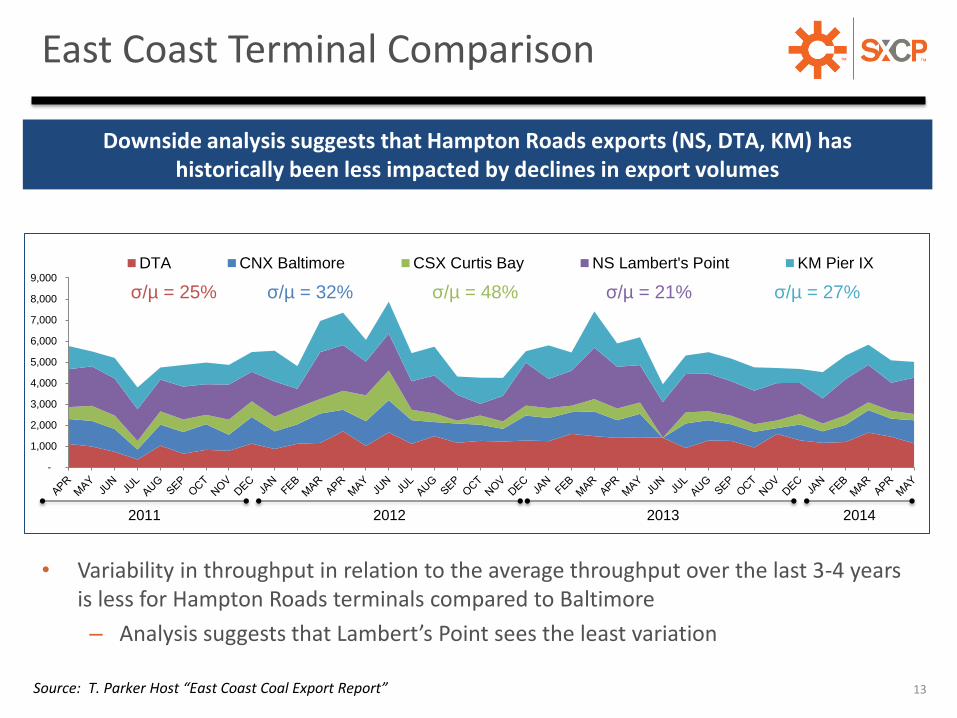

TM East Coast Terminal Comparison

Source: T. Parker Host “East Coast Coal Export Report”

2012

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

DTA CNX Baltimore CSX Curtis Bay NS Lambert's Point KM Pier IX

σ/µ = 25% σ/µ = 48% σ/µ = 21% σ/µ = 27% σ/µ = 32%

2011 2013 2014

Downside analysis suggests that Hampton Roads exports (NS, DTA, KM) has historically been less impacted by declines in export volumes

• Variability in throughput in relation to the average throughput over the last 3-4 years is less for Hampton Roads terminals compared to Baltimore

– Analysis suggests that Lambert’s Point sees the least variation

13

TM Summary

• The global seaborne coal trade remains healthy and will be a vital part of the global economy for the foreseeable future

• After peaking in 2012, US coal export volumes are forecast to decline for the next 18-24 months

• Weakness in Europe, slower growth in Asia, and increased seaborne coal supply from low cost Australian producers will impact the three primary export areas of the US (West Coast, Gulf Coast, and East Coast)

• Despite Appalachian coals being marginally competitive on a global cash cost basis, US East Coast exports are primarily driven by European and South American demand – two areas where the US is logistically advantaged

14

US Coal Export Market and Terminal - Appendix

Saurabh Pandey

Director of Business Development

SunCoke Energy

Platts Coal Marketing Days

Sept 22-23, 2014

TM Asian Demand

16 Source: World Steel Dynamics, Goldman Sachs “The Thermal Coal Paradox”

500

1,250

2,000

2,750

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Thermal - Coal Fired Boiler Utilities Met. – Steel Production Total Steel Production

500

1,250

2,000

2,750

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

500

600

700

800

900

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Total Met Coal Consumption

(M tons)

(M tons)

(M tons)

Total Crude Steel Production - BF/BOF

India is now forecast to become the largest single market for seaborne thermal coal, helping to offset muted import demand growth in China

• Although China has been the key driver in thermal seaborne demand as of late, it faces headwinds from oversupply, environmental regulations, and a more diverse fuel mix shifting towards renewable energy

• India forecasted to become the biggest single market for seaborne thermal coal, as domestic production falls behind demand of the country’s highly coal-dependent power sector (~70% coal share of overall fuel mix)

Share of Coal in Fuel Mix (2012)

Seaborne Thermal Coal Import

by Region

CAGR 1.35%

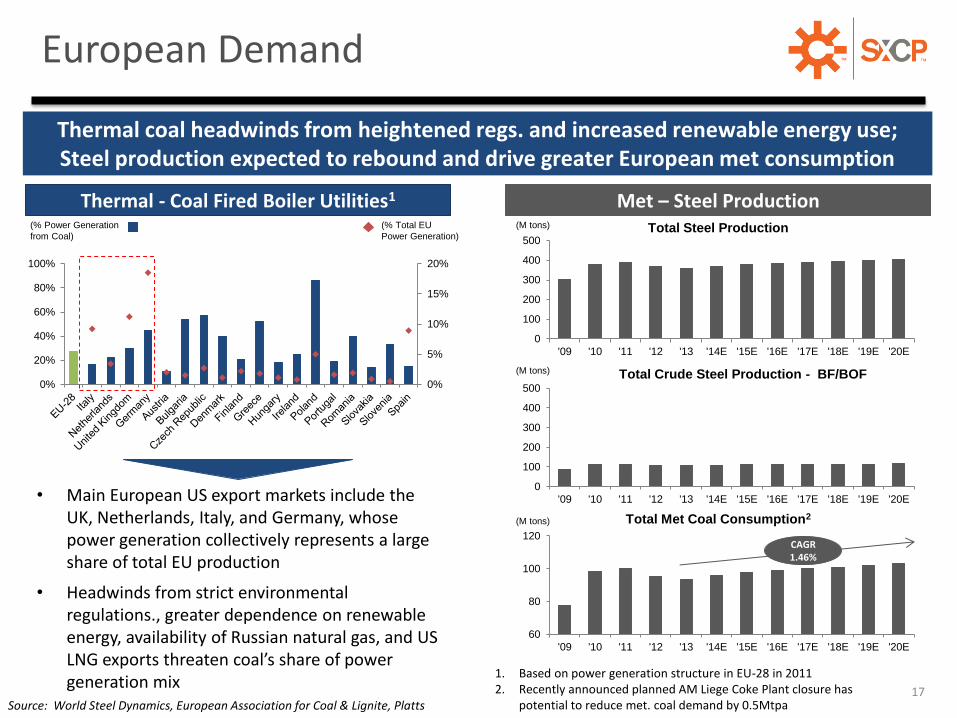

TM European Demand

Source: World Steel Dynamics, European Association for Coal & Lignite, Platts

0

100

200

300

400

500

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Thermal - Coal Fired Boiler Utilities1 Met – Steel Production Total Steel Production

0

100

200

300

400

500

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

60

80

100

120

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Total Met Coal Consumption2

(M tons)

(M tons)

(M tons)

Total Crude Steel Production - BF/BOF

Thermal coal headwinds from heightened regs. and increased renewable energy use; Steel production expected to rebound and drive greater European met consumption

0%

5%

10%

15%

20%

0%

20%

40%

60%

80%

100%

• Main European US export markets include the UK, Netherlands, Italy, and Germany, whose power generation collectively represents a large share of total EU production

• Headwinds from strict environmental regulations., greater dependence on renewable energy, availability of Russian natural gas, and US LNG exports threaten coal’s share of power generation mix

1. Based on power generation structure in EU-28 in 2011 2. Recently announced planned AM Liege Coke Plant closure has

potential to reduce met. coal demand by 0.5Mtpa

(% Power Generation

from Coal)

(% Total EU

Power Generation)

CAGR 1.46%

17

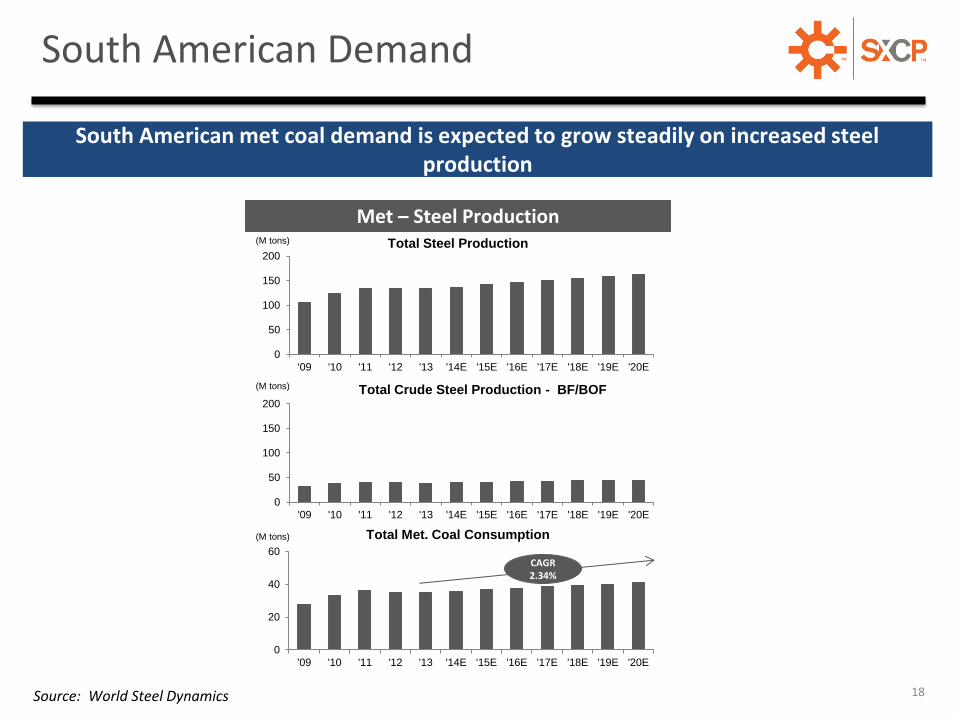

TM South American Demand

18 Source: World Steel Dynamics

0

50

100

150

200

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Met – Steel Production Total Steel Production

0

50

100

150

200

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

0

20

40

60

'09 '10 '11 '12 '13 '14E '15E '16E '17E '18E '19E '20E

Total Met. Coal Consumption

(M tons)

(M tons)

(M tons)

Total Crude Steel Production - BF/BOF

South American met coal demand is expected to grow steadily on increased steel production

CAGR 2.34%