34

Construction activity will grow in 2016, but at a slower rate United States Construction Perspective Q4 2015

| Date post: | 19-Jan-2017 |

| Category: |

Real Estate |

| Upload: | jll |

| View: | 5,012 times |

| Download: | 2 times |

Construction activity will grow

in 2016, but at a slower rateUnited States

Construction Perspective

Q4 2015

2015 was a banner year for post-recession construction activity:

• Office space under construction peaked at 92.8 m.s.f.

• Industrial construction was the shining star as consumer confidence grew.

• Construction costs increased in primary office markets, driven by skyrocketing

labor costs, which motivated growth in secondary markets.

While construction activity will continue to grow, in 2016 the ascent will

be slower as executives think strategically about in which sectors and

markets to invest:

• China’s economic struggles will start to affect the United States economy-

though the construction industry lags the economy by a year, so the full effects

of the lag will not reach the construction market until 2017 or 2018.

• Consumer demand will start to decline, influencing retail and manufacturing

demand.

• Labor shortages in the construction industry, along with skyrocketing sheet

glass prices, will stoke fears of rising costs, shaking business confidence in

some sectors.

Key construction markets

3

Source: JLL Research

The impact of the decline in energy prices on construction began to rear its head at the end of 2015, as office

construction activity in energy markets like Houston dropped drastically, while sublease space reached record

highs. With energy prices projected to stay low in 2016, construction will continue to stall. However, experts

predict oil prices will rise again by 2017, which will restart the cycle.

The South has become the new frontier for construction activity. In 2015, thanks to low labor and land costs,

many large companies moved there to build new manufacturing and office spaces, driving a population influx into

cities like Charleston, Atlanta and Charlotte.

Primary tech markets, like San Francisco and Silicon Valley, will continue to sport some of the highest

construction costs nationwide, thanks to high demand as the economy continues to become more tech-focused.

There will be an increase in office construction demand for secondary tech markets, like Chicago and Austin, in

2016.

Renovation activity reached new highs in 2015, thanks to a push for sustainable office development focused on

attracting and retaining millennial talent, while enhancing corporate social responsibility. This push for new build

outs was not limited to office spaces, with retail and industrial developers redeveloping existing space to include

new technology and engage consumers in unique ways. This trend will continue in 2016.

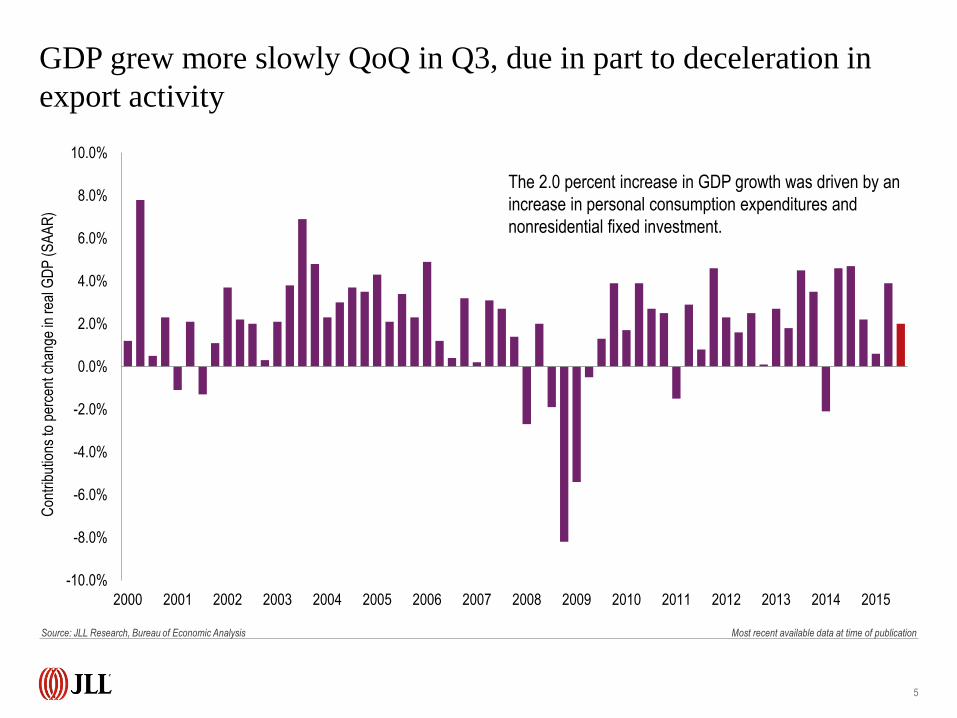

Economic growth in 2015

GDP grew more slowly QoQ in Q3, due in part to deceleration in

export activity

5

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Con

trib

utio

ns to

per

cent

cha

nge

in r

eal G

DP

(S

AA

R)

The 2.0 percent increase in GDP growth was driven by an

increase in personal consumption expenditures and

nonresidential fixed investment.

Source: JLL Research, Bureau of Economic Analysis Most recent available data at time of publication

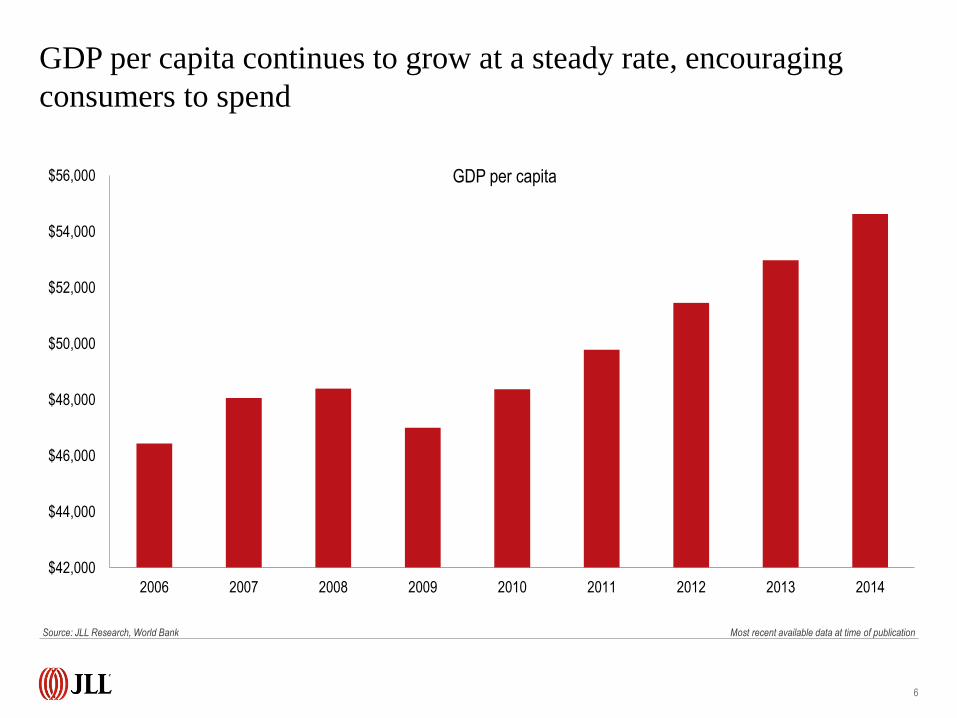

GDP per capita continues to grow at a steady rate, encouraging

consumers to spend

6

Source: JLL Research, World Bank Most recent available data at time of publication

$42,000

$44,000

$46,000

$48,000

$50,000

$52,000

$54,000

$56,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

GDP per capita

7

Con

stru

ctio

n em

ploy

men

t (n

umbe

r of

em

ploy

ees,

in th

ousa

nds)

Overall em

ployment (num

ber of employees, in thousands)

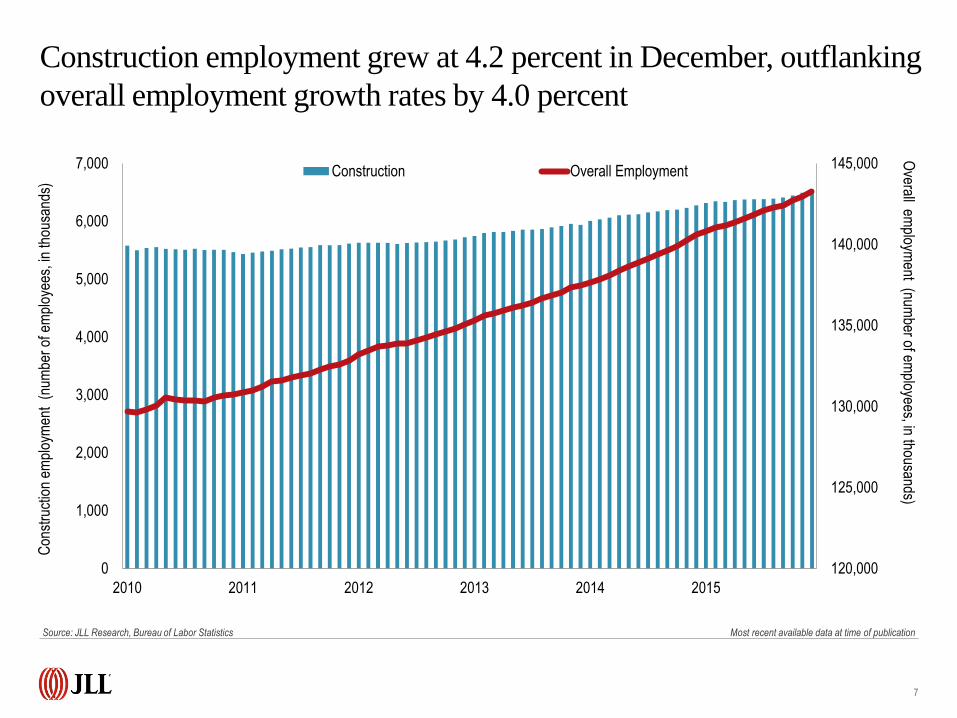

Construction employment grew at 4.2 percent in December, outflanking

overall employment growth rates by 4.0 percent

120,000

125,000

130,000

135,000

140,000

145,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2010 2011 2012 2013 2014 2015

Construction Overall Employment

Source: JLL Research, Bureau of Labor Statistics Most recent available data at time of publication

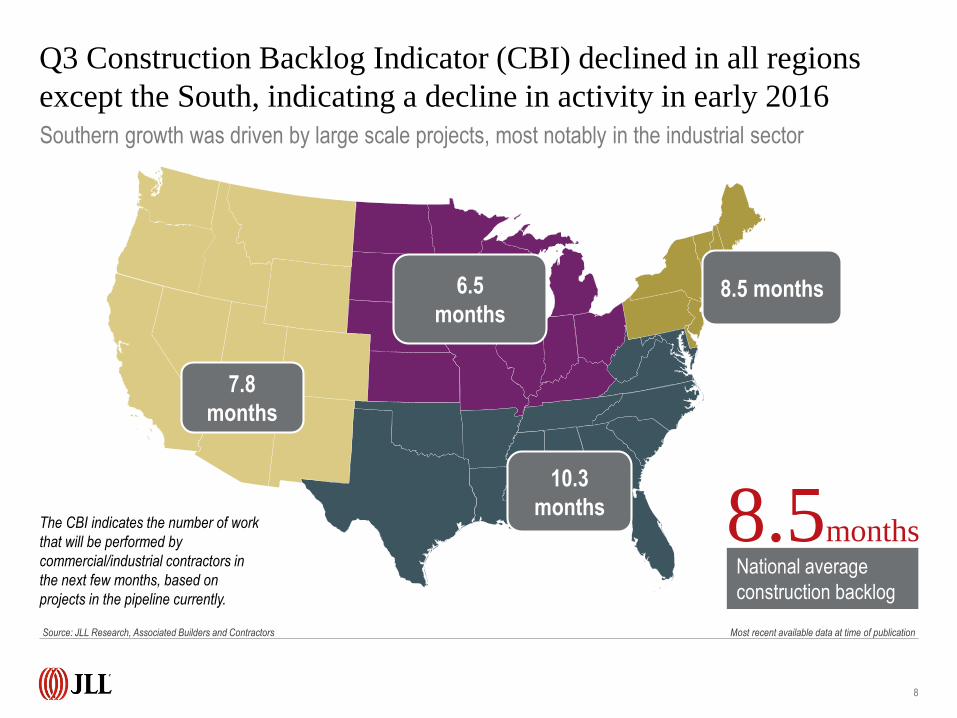

Q3 Construction Backlog Indicator (CBI) declined in all regions

except the South, indicating a decline in activity in early 2016

8

Southern growth was driven by large scale projects, most notably in the industrial sector

7.8

months

10.3

months

8.5 months6.5

months

National average

construction backlog

8.5monthsThe CBI indicates the number of work

that will be performed by

commercial/industrial contractors in

the next few months, based on

projects in the pipeline currently.

Source: JLL Research, Associated Builders and Contractors Most recent available data at time of publication

9

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Current H1 2016 H2 2016 2019

Improving Stable Declining

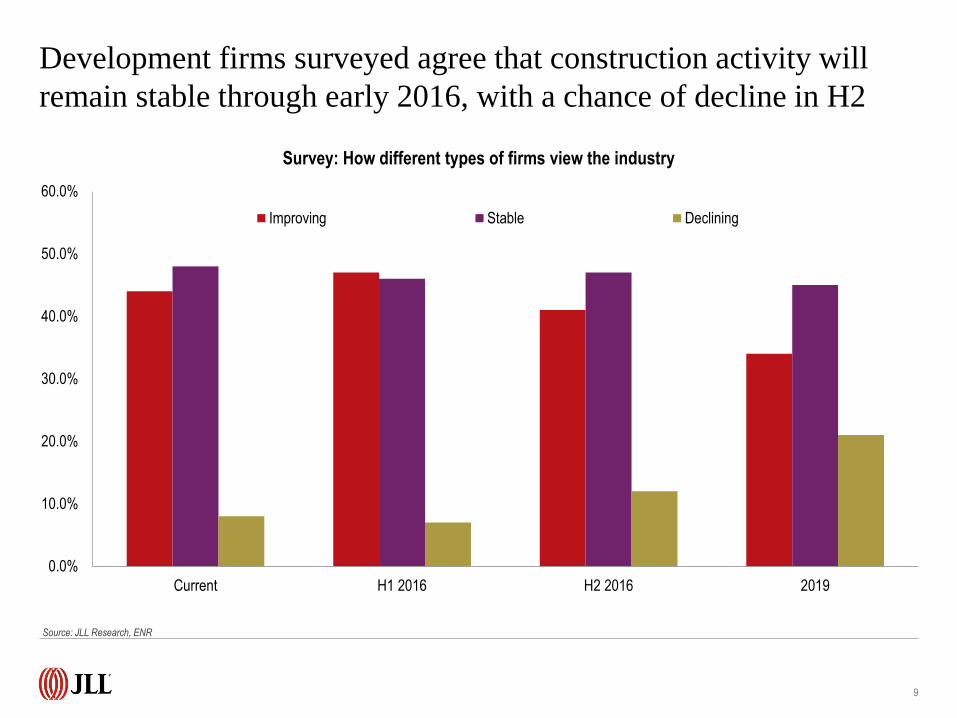

Survey: How different types of firms view the industry

Development firms surveyed agree that construction activity will

remain stable through early 2016, with a chance of decline in H2

Source: JLL Research, ENR

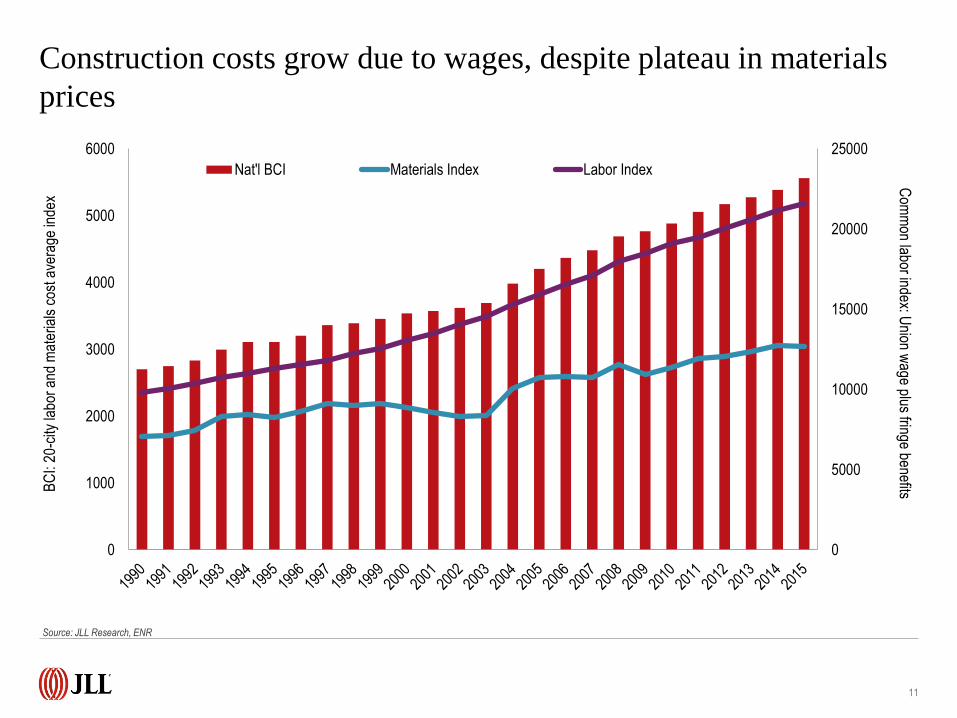

Cost trends: wages are growing, driving overall cost increase

BC

I: 20

-city

labo

r an

d m

ater

ials

cos

t ave

rage

inde

x

0

5000

10000

15000

20000

25000

0

1000

2000

3000

4000

5000

6000

Nat'l BCI Materials Index Labor Index

11

Com

mon labor index: U

nion wage plus fringe benefits

Construction costs grow due to wages, despite plateau in materials

prices

Source: JLL Research, ENR

1500

1700

1900

2100

2300

2500

2700

2900

3100

3300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

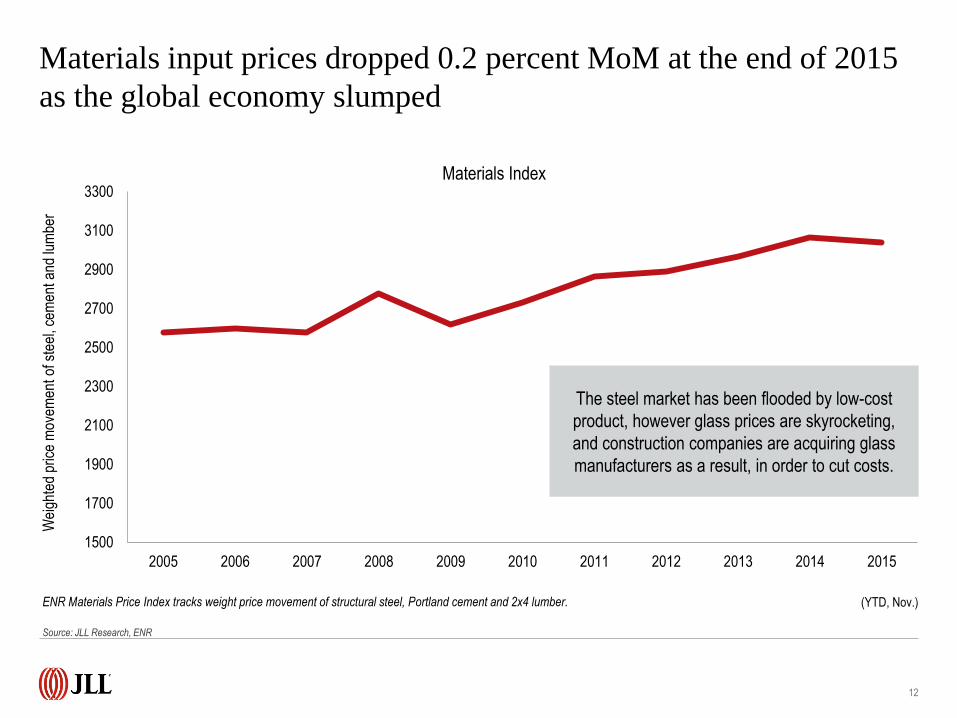

Materials Index

12

ENR Materials Price Index tracks weight price movement of structural steel, Portland cement and 2x4 lumber.

Wei

ghte

d pr

ice

mov

emen

t of s

teel

, cem

ent a

nd lu

mbe

r

The steel market has been flooded by low-cost

product, however glass prices are skyrocketing,

and construction companies are acquiring glass

manufacturers as a result, in order to cut costs.

(YTD, Nov.)

Materials input prices dropped 0.2 percent MoM at the end of 2015

as the global economy slumped

Source: JLL Research, ENR

13

Mat

eria

ls p

rice

infla

tion

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0S

truc

tura

l Ste

el

Rei

nfor

cing

Bar

s

Lum

ber

Asp

halt

Ply

woo

d

Gyp

sum

She

et M

etal

Cem

ent

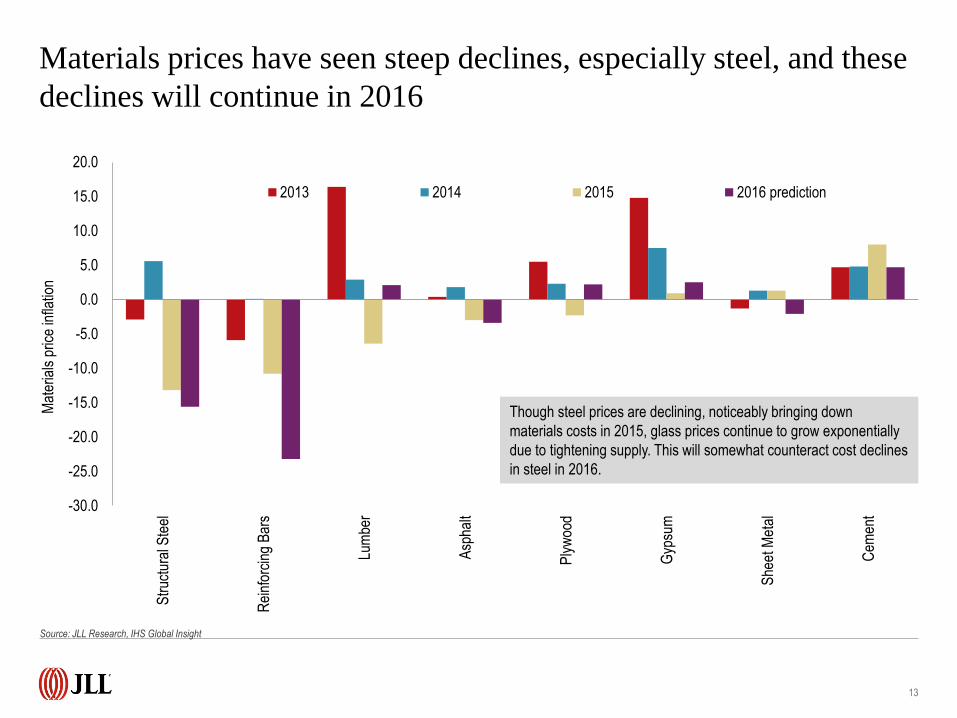

2013 2014 2015 2016 prediction

Though steel prices are declining, noticeably bringing down

materials costs in 2015, glass prices continue to grow exponentially

due to tightening supply. This will somewhat counteract cost declines

in steel in 2016.

Materials prices have seen steep declines, especially steel, and these

declines will continue in 2016

Source: JLL Research, IHS Global Insight

$0

$200

$400

$600

$800

$1,000

$1,200

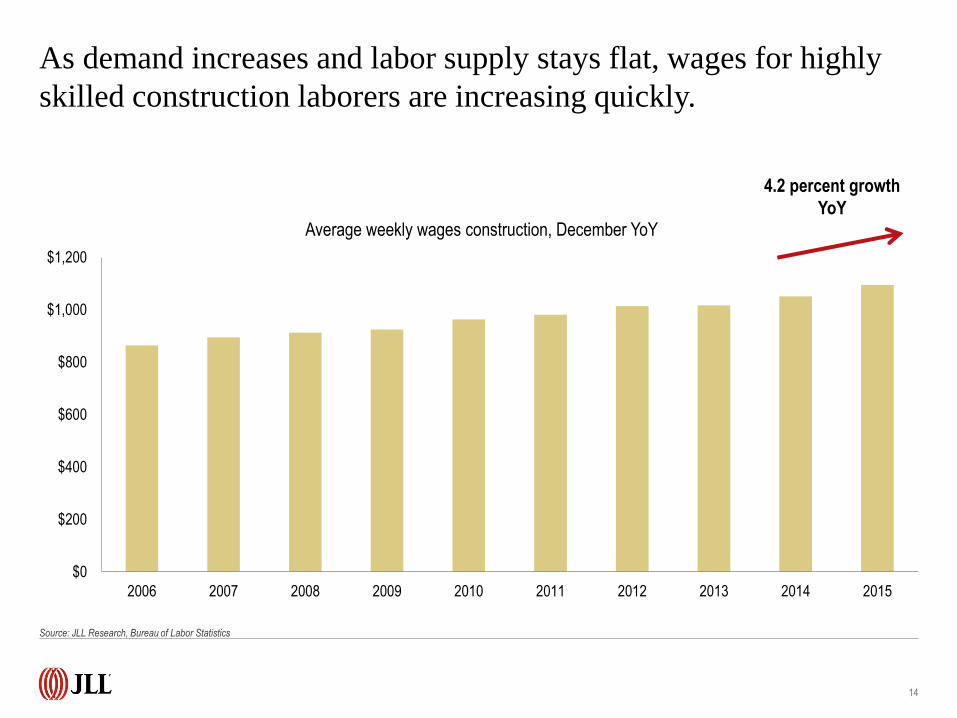

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Average weekly wages construction, December YoY

14

4.2 percent growth

YoY

As demand increases and labor supply stays flat, wages for highly

skilled construction laborers are increasing quickly.

Source: JLL Research, Bureau of Labor Statistics

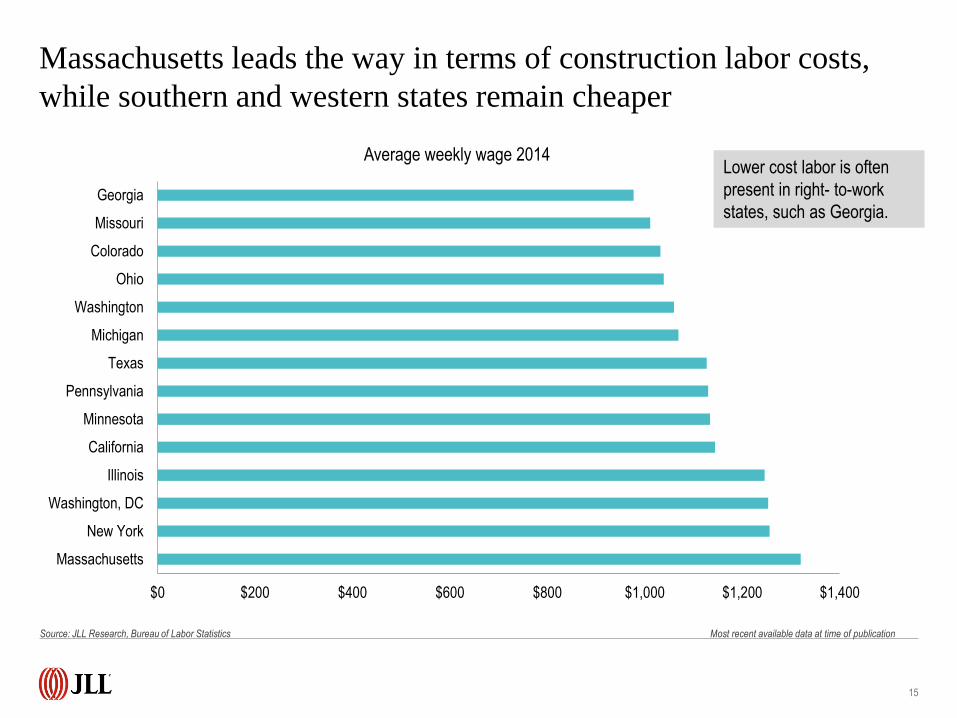

15

$0 $200 $400 $600 $800 $1,000 $1,200 $1,400

Massachusetts

New York

Washington, DC

Illinois

California

Minnesota

Pennsylvania

Texas

Michigan

Washington

Ohio

Colorado

Missouri

Georgia

Average weekly wage 2014Lower cost labor is often

present in right- to-work

states, such as Georgia.

Massachusetts leads the way in terms of construction labor costs,

while southern and western states remain cheaper

Source: JLL Research, Bureau of Labor Statistics Most recent available data at time of publication

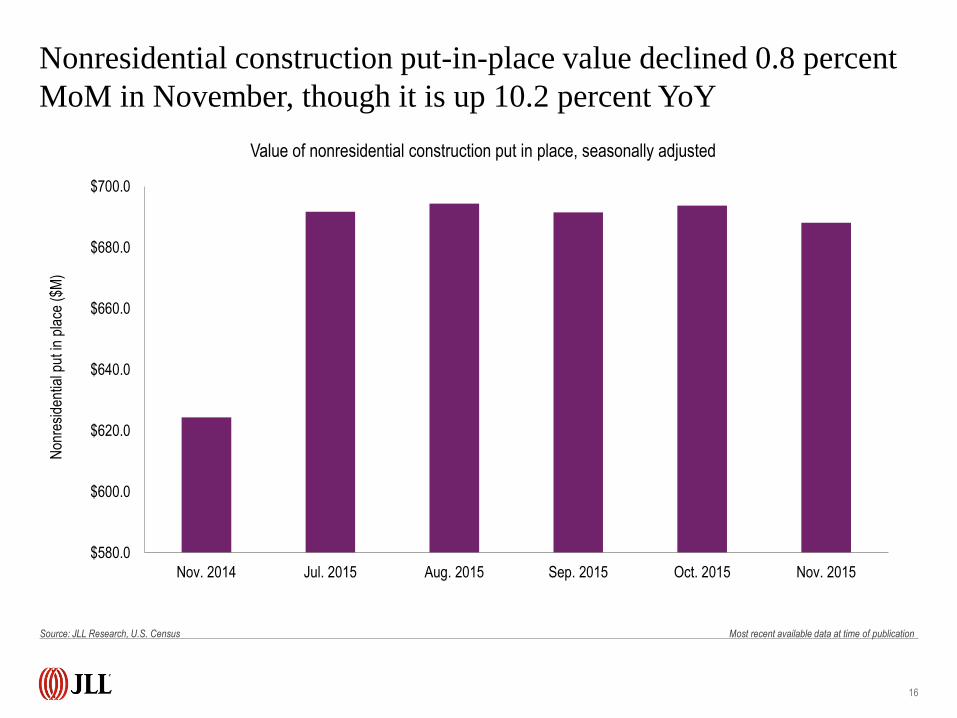

16

Non

resi

dent

ial p

ut in

pla

ce (

$M)

$580.0

$600.0

$620.0

$640.0

$660.0

$680.0

$700.0

Nov. 2014 Jul. 2015 Aug. 2015 Sep. 2015 Oct. 2015 Nov. 2015

Value of nonresidential construction put in place, seasonally adjusted

Nonresidential construction put-in-place value declined 0.8 percent

MoM in November, though it is up 10.2 percent YoY

Source: JLL Research, U.S. Census Most recent available data at time of publication

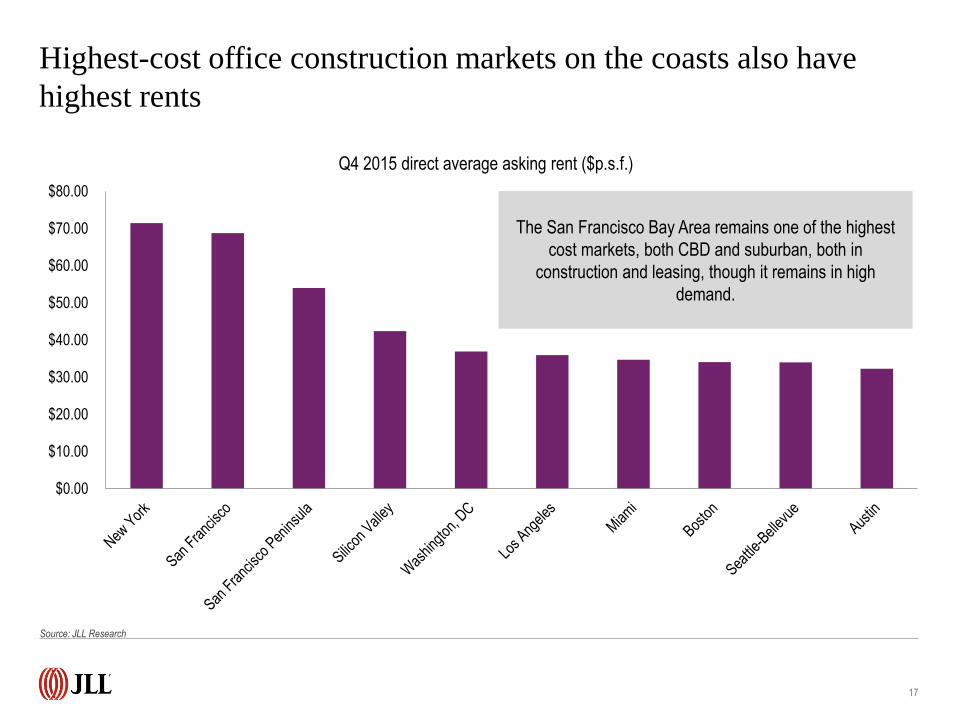

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Q4 2015 direct average asking rent ($p.s.f.)

17

The San Francisco Bay Area remains one of the highest

cost markets, both CBD and suburban, both in

construction and leasing, though it remains in high

demand.

Highest-cost office construction markets on the coasts also have

highest rents

Source: JLL Research

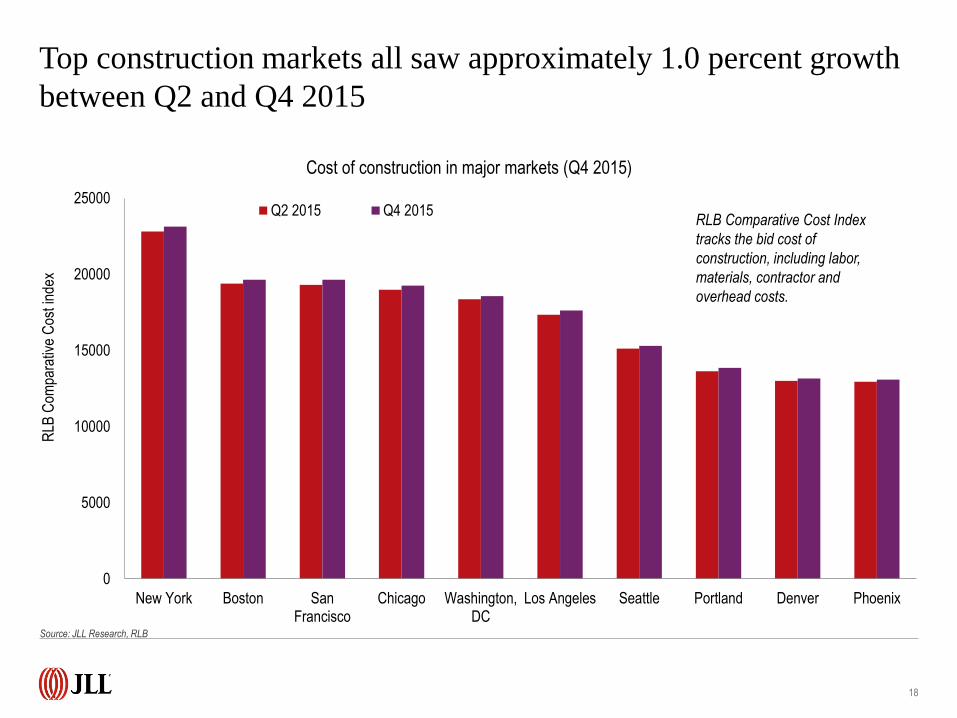

0

5000

10000

15000

20000

25000

New York Boston SanFrancisco

Chicago Washington,DC

Los Angeles Seattle Portland Denver Phoenix

Q2 2015 Q4 2015

18

Cost of construction in major markets (Q4 2015)

RLB Comparative Cost Index

tracks the bid cost of

construction, including labor,

materials, contractor and

overhead costs.

RLB

Com

para

tive

Cos

t ind

exTop construction markets all saw approximately 1.0 percent growth

between Q2 and Q4 2015

Source: JLL Research, RLB

19

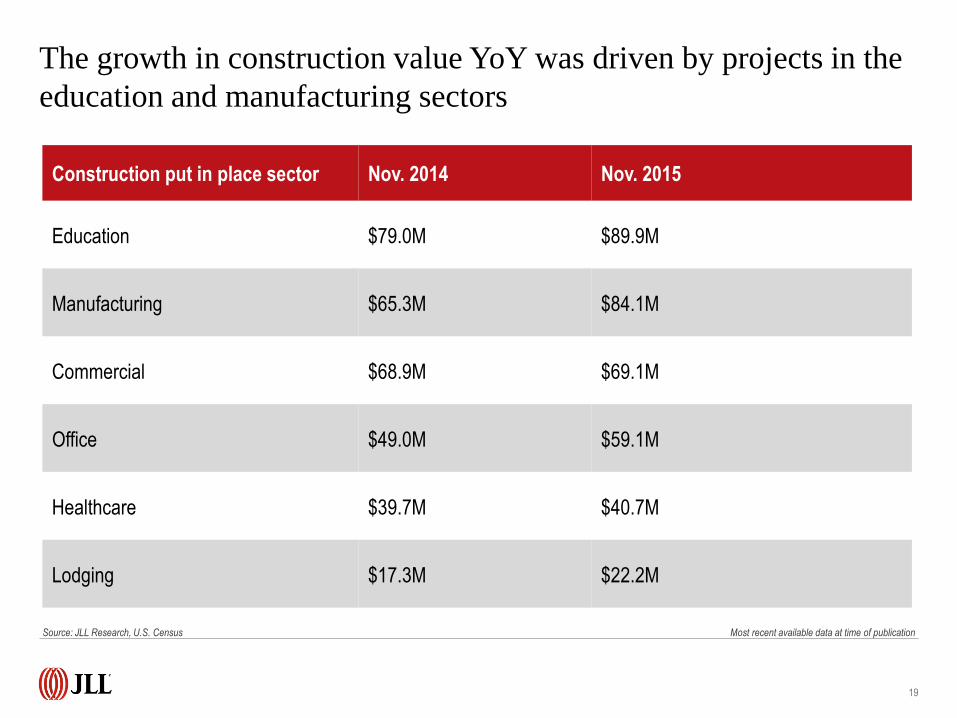

Construction put in place sector Nov. 2014 Nov. 2015

Education $79.0M $89.9M

Manufacturing $65.3M $84.1M

Commercial $68.9M $69.1M

Office $49.0M $59.1M

Healthcare $39.7M $40.7M

Lodging $17.3M $22.2M

The growth in construction value YoY was driven by projects in the

education and manufacturing sectors

Source: JLL Research, U.S. Census Most recent available data at time of publication

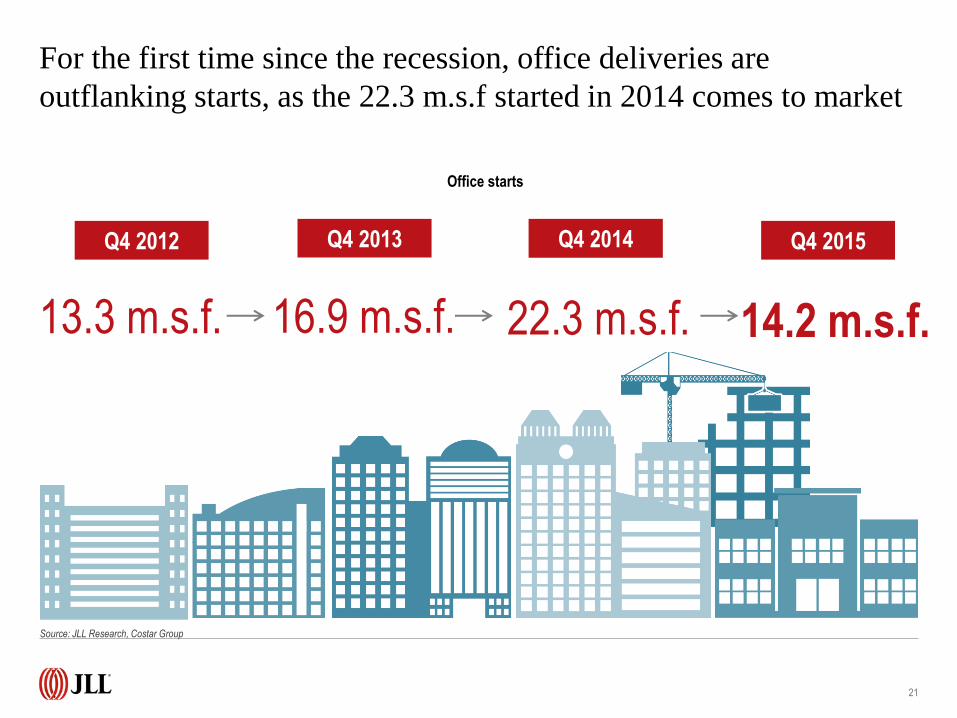

2015 was a strong growth year for all property types, but growth is beginning to slow

21

16.9 m.s.f. 22.3 m.s.f. 14.2 m.s.f.

Q4 2012

13.3 m.s.f.

Q4 2013 Q4 2014 Q4 2015

Office starts

For the first time since the recession, office deliveries are

outflanking starts, as the 22.3 m.s.f started in 2014 comes to market

Source: JLL Research, Costar Group

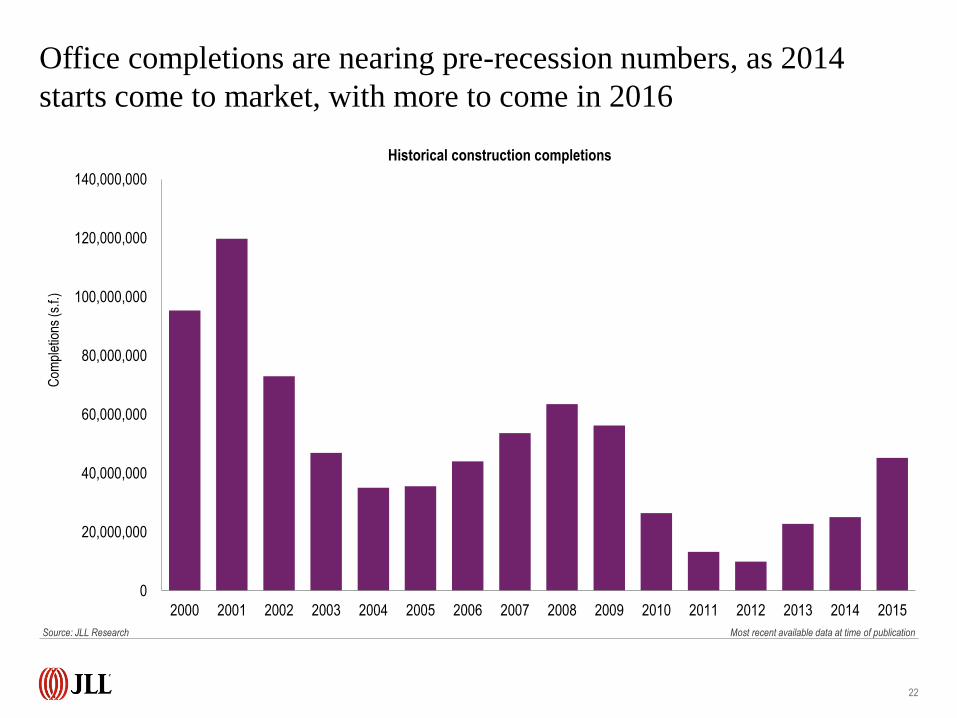

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Com

plet

ions

(s.

f.)

22

Historical construction completions

Office completions are nearing pre-recession numbers, as 2014

starts come to market, with more to come in 2016

Source: JLL Research Most recent available data at time of publication

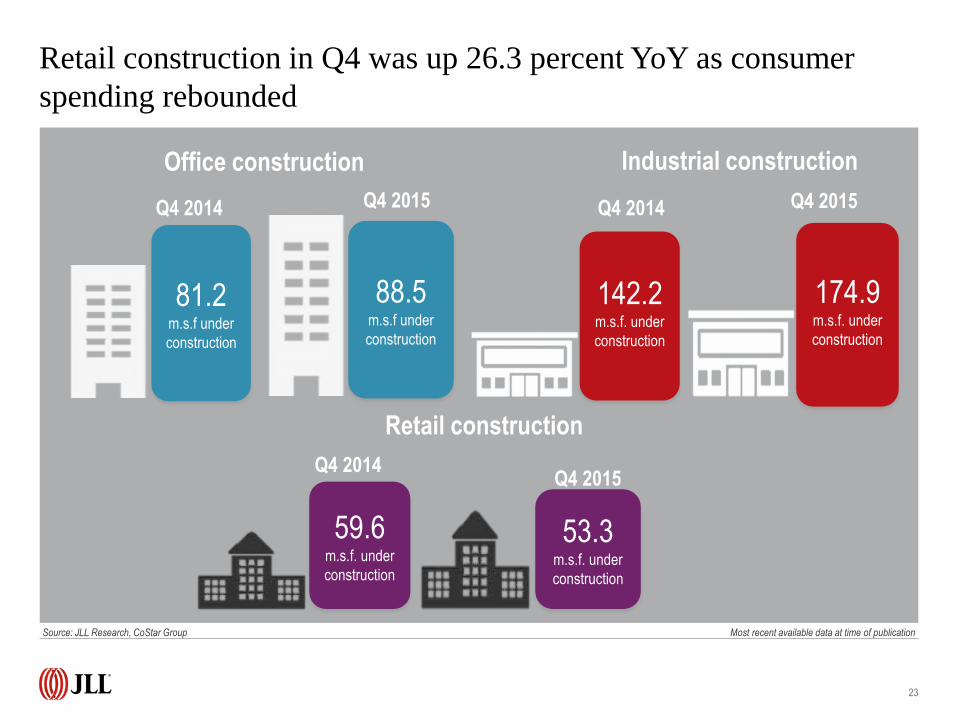

23

Industrial construction

Retail construction

142.2m.s.f. under

construction

Q4 2015 Q4 2014 Q4 2015

174.9m.s.f. under

construction

59.6m.s.f. under

construction

53.3m.s.f. under

construction

Q4 2014Q4 2015

Office construction

Q4 2014

88.5m.s.f under

construction

81.2m.s.f under

construction

Retail construction in Q4 was up 26.3 percent YoY as consumer

spending rebounded

Source: JLL Research, CoStar Group Most recent available data at time of publication

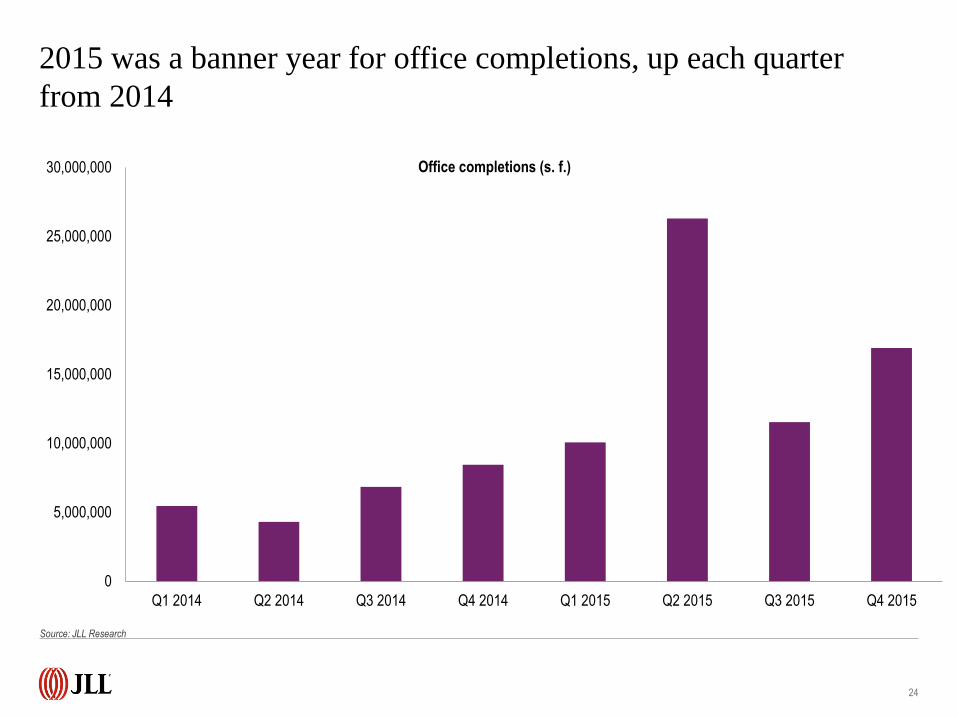

24

Office completions (s. f.)

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

2015 was a banner year for office completions, up each quarter

from 2014

Source: JLL Research

25

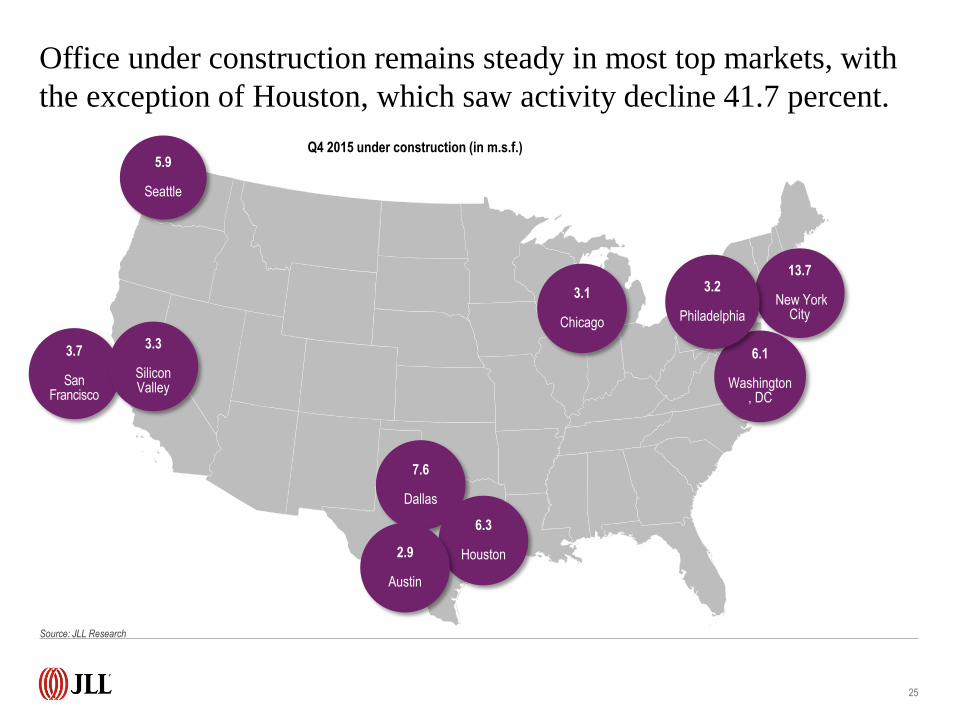

7.6

Dallas

5.9

Seattle

3.7

San Francisco

3.3

Silicon Valley

6.3

Houston

3.1

Chicago

2.9

Austin

13.7

New York City

6.1

Washington, DC

3.2

Philadelphia

Q4 2015 under construction (in m.s.f.)

Office under construction remains steady in most top markets, with

the exception of Houston, which saw activity decline 41.7 percent.

Source: JLL Research

Office vacancies are highest in Rust Belt and smaller East Coast

markets, signaling a decline in new construction in these markets

26

The lowest vacancy rate in Q4

was in Salt Lake City, with total

vacancy of 6.4 percent.

-5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

New Jersey

Fairfield County

Westchester County

Phoenix

Cleveland

Milwaukee

Detroit

Dallas

Hartford

CincinnatiTotal vacancy (%)

YTD total net absorption (% of Inventory)

Source: JLL Research

27

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

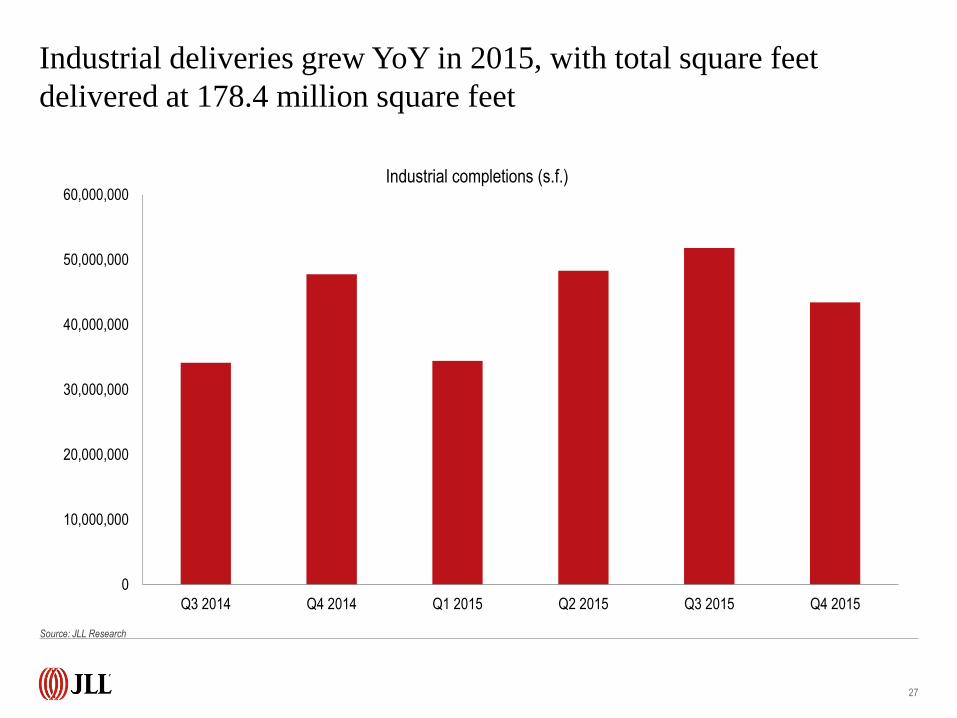

Industrial completions (s.f.)

Industrial deliveries grew YoY in 2015, with total square feet

delivered at 178.4 million square feet

Source: JLL Research

18.6m.s.f.Inland Empire

7.3m.s.f.Reno

28

19.7m.s.f.Dallas

4.3m.s.f.Los

Angeles

4.3m.s.f.

Oakland

8.6m.s.f.

Houston

12.8m.s.f.

Chicago

5.4m.s.f.

Kansas City

19.6m.s.f.Atlanta

11.3m.s.f.

Philadelphia

Q4 2015 under construction

St. Louis fell out of the top 10,

while new development in

Oakland spurred it to ninth.

Overall, activity across the board

dropped in Q4, in part due to

seasonal fluctuations.

Dallas and Atlanta eclipsed Inland Empire in Q4, as the South

continues its rapid development, driven by low costs

Source: JLL Research

29

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

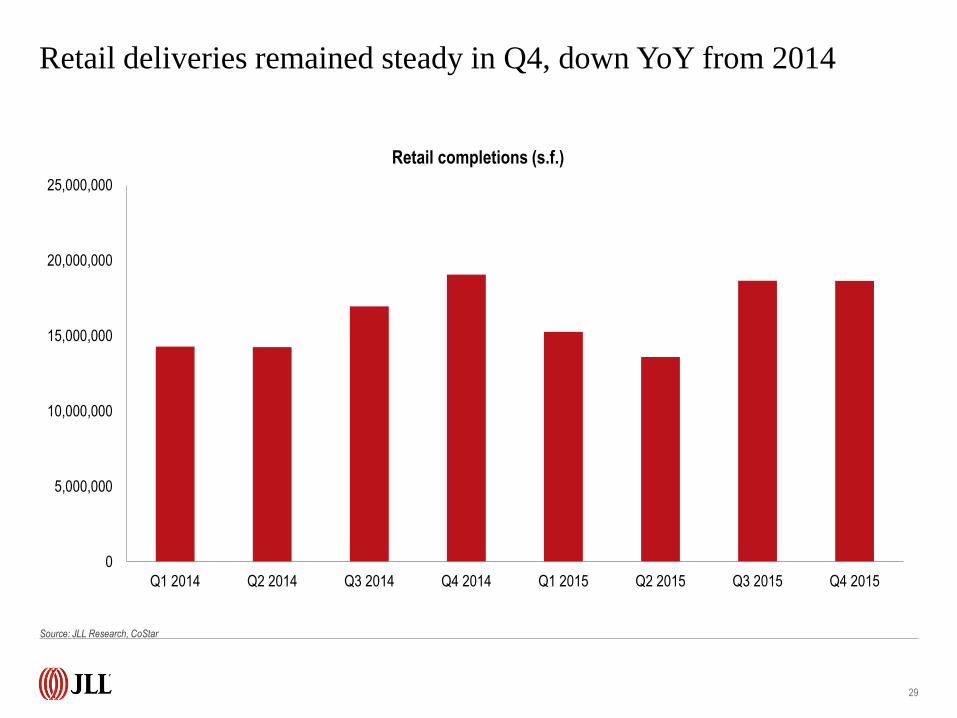

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Retail completions (s.f.)

Retail deliveries remained steady in Q4, down YoY from 2014

Source: JLL Research, CoStar

30

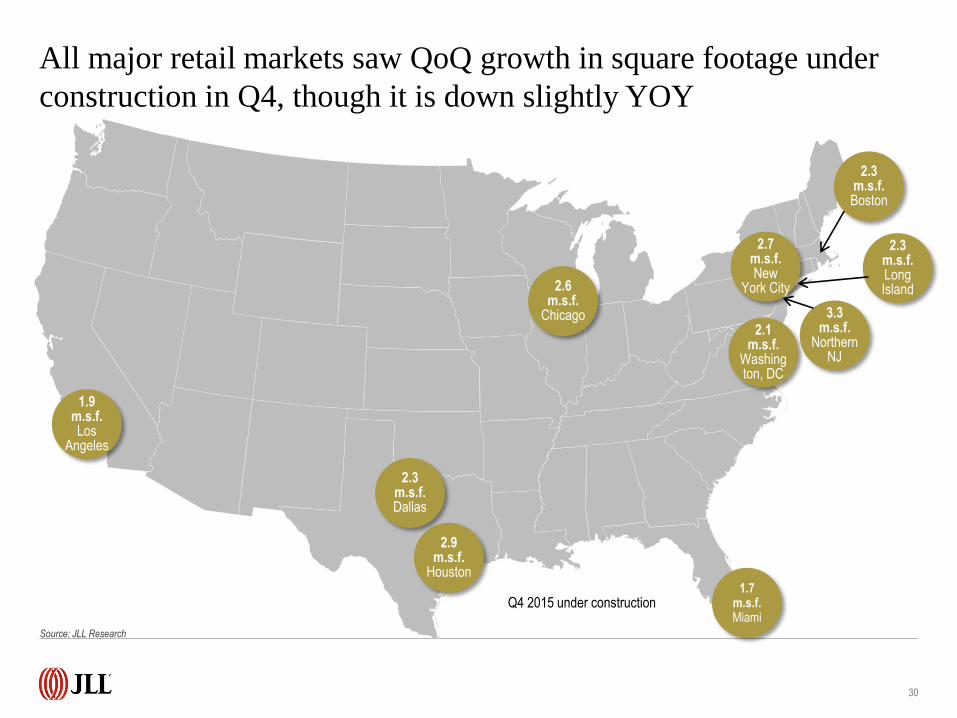

2.9m.s.f.

Houston

1.9m.s.f.Los

Angeles

2.3m.s.f.Dallas

2.6m.s.f.

Chicago 2.1

m.s.f.Washington, DC

3.3m.s.f.

Northern NJ

2.3m.s.f.Long Island

2.7m.s.f.New

York City

2.3m.s.f.Boston

Q4 2015 under construction1.7

m.s.f.Miami

All major retail markets saw QoQ growth in square footage under

construction in Q4, though it is down slightly YOY

Source: JLL Research

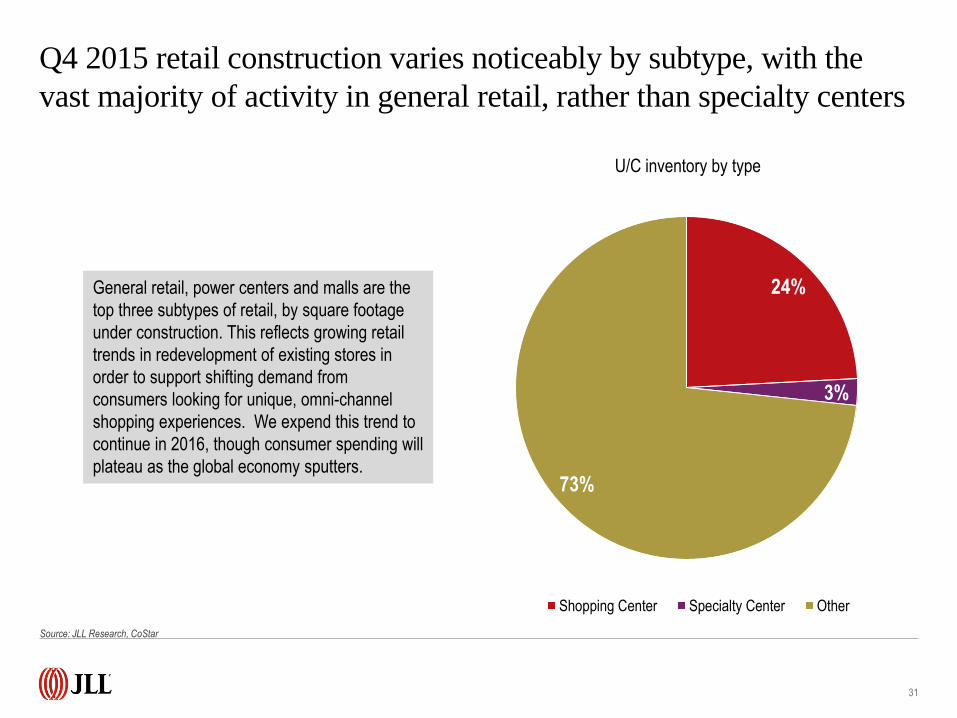

Q4 2015 retail construction varies noticeably by subtype, with the

vast majority of activity in general retail, rather than specialty centers

31

24%

3%

73%

U/C inventory by type

Shopping Center Specialty Center Other

General retail, power centers and malls are the

top three subtypes of retail, by square footage

under construction. This reflects growing retail

trends in redevelopment of existing stores in

order to support shifting demand from

consumers looking for unique, omni-channel

shopping experiences. We expend this trend to

continue in 2016, though consumer spending will

plateau as the global economy sputters.

Source: JLL Research, CoStar

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

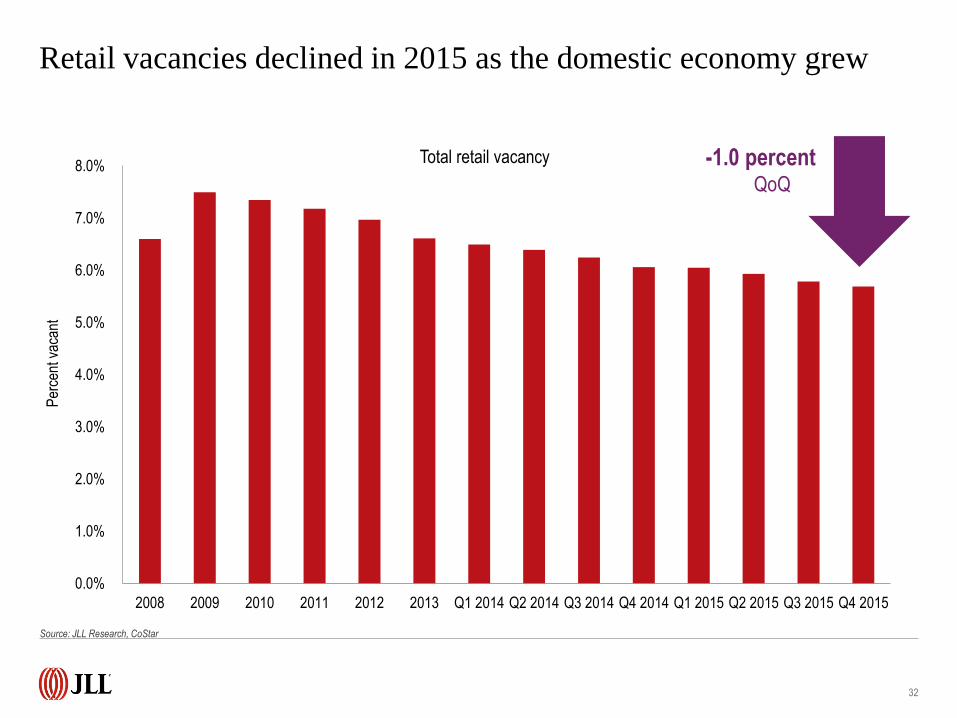

2008 2009 2010 2011 2012 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Total retail vacancy

32

Per

cent

vac

ant

-1.0 percentQoQ

Retail vacancies declined in 2015 as the domestic economy grew

Source: JLL Research, CoStar

What’s next for construction?

Politics as un-usual: The 2016 election is ramping up and will affect consumer behavior as domestic residents weigh

who they think will become the next leader. Further, the upcoming fight over the debt ceiling could delay government

buildings and other public works if the government delays its budget.

The Fed increased interest rates, indicating faith in the domestic economy; however, the global economy has

slowed, and contractors are uncertain how this may affect the markets. Most noticeably, many inputs, such as low-cost

steel, are manufactured in bulk in China. As its manufacturing sector continues to decline, materials prices will

continue to drop into 2016.

Wages will remain the key cost driver for construction, as materials prices remain relatively low in the short term.

There remains a dearth of trained construction employees, especially in trade positions, and wages are rising as a

result.

Increase in starts in 2016 will continue, but at a lower rate. General economic growth nationwide has slowed, and

the construction industry will be no different. However, demand from downstream markets will stay strong and

construction profit margins will continue to grow, keeping construction growing at a faster rate than the overall

economy. However, developers are starting to be more wary and will be more careful in starting projects, especially in

single-industry markets, such as Houston.

© 2016 Jones Lang LaSalle IP, Inc.

All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Thank you

Dana Westgren

Research Analyst

Project and Development Services

+1 (202) 719 5003