33

U.S. Crude Exports Where Would They Go? 2 nd Annual Crude-by-Water Conference Houston, TX November 17, 2015 John R. Auers Executive Vice President

U.S. Crude Exports Where Would They Go?

2nd Annual Crude-by-Water Conference Houston, TX

November 17, 2015

John R. Auers Executive Vice President

• International consulting practice since 1971

• Downstream focus; refinery/chemical engineers

• Industry and financial clients – Strategic Studies

– FMV Assessments & Venture Analyses

– National Policy Studies

• Publish various outlook and multi-client subscription reports – Crude and Refined Products Outlook – Refinery Construction Outlook – North American Crude and Condensate Outlook

• Several editions

– World Crude Outlook • Released in October 2015

TM&C Overview

2

TM&C “White Paper” on Exports

• Issued Report on September 8th

– Analysis of likely U.S. crude export destinations – Considered quality, regional demand and logistics,

other factors – Focused on light crude

• Available at www.turnermason.com – Top of the page under Publications U.S. Light

Crude Oil Exports: Likely Destinations

3

Presentation Outline

• Evolving U.S. Crude Balance

• “Fit” into Atlantic Basin Refineries

• Transportation Costs/Other Factors

• Final Analysis/Thoughts

4

U.S. Crude Production

0

1

2

3

4

5

6

7

8

9

10

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

U.S

. Cru

de P

rodu

ctio

n (M

illio

n BP

D)

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013 2014 2015

U.S

. Cru

de P

rodu

ctio

n (M

illio

n BP

D)

Bakken

Eagle Ford

Niobrara

Permian

All Other

U.S. Production

had risen over 90% since

2008

Growth dominated by

LTO production

8.8

9

9.2

9.4

9.6

9.8

Jan-

15

Feb-

15M

ar-1

5

Apr-

15

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct

-15

5

Domestic Lights Latin American & Canadian Heavies Middle

Eastern Design

Basis ->

0.6

0.8

1

1.2

1.4

1.6

30.0

30.5

31.0

31.5

32.0

32.5

1985 1990 1995 2000 2005 2010 2015

Sulfu

r, w

t. %

Gra

vity

, API

2015 YTD, API 31.8, Sulfur 1.40

Changing U.S. Refinery Crude Slates (1985-2015)

LTO growth has led to a much

lighter U.S. crude slate

6

U.S. Refiners Geared for Heavy Crude

• U.S. Refiners had spent billions in the 1990’s and 2000’s to “heavy up”

• Significantly increased complexity; more suited to run heavier crudes

• More recently spending focused on light crude

Comparison of U.S. to Global Refiners

Region Total

Upgrading Cat

Cracking Coking Hydrocracking U.S. - 1981 41% 28% 8% 5% U.S. – 2015 56% 31% 15% 11% Asia 19% 13% 3% 6% Europe 26% 14% 3% 9% Latin + South America 25% 16% 4% 5% World 28% 16% 5% 7% *O&G Journal, as of Jan. 1, 2015

7

8

Light Crude Investment - 2012 to 2018

Spent To Date Total

PADD I

100 50

Spent To Date Total

PADD II

1100 800

Spent To Date Total

PADD III

3900 1800

Spent ToDate

Total

PADD V

Spent To Date Total

PADD IV

1500 900

Drop in Oil Price Could Delay $500 to

$1000+ MM of Investments

100 200

*Millions of $

Spent To Date Total

U.S. Total

3600 6800

Imports Down/Allowable Exports Up

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Crud

e Ex

port

s (Th

ousa

nd B

PD)

Processed Condensate Canada

0

2

4

6

8

10

12

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Crud

e Im

port

s (M

illio

n BP

D)

Medium Light Canadian Heavy PADD V

Light/Medium Imports Decline from 4.8

MMBPD in 2006 & 2007 to 1.5 MMPBD in 2015

9

0

100

200

300

400

500

600

700

800

900

1000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Impo

rts (

MBP

D)

Eastern Canadian Imports (Ontario, Quebec, Maritime Provinces)

Heavy

Light (Non U.S.)

Light (U.S.)

No More Room In Canada

Three-month Rolling Average

10

300 MBPD Line 9 reversal startup imminent, will displace U.S. crude

with Western Canadian Barrels

0

2

4

6

8

10

12

14

16

18

20

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Current Forecast

Other Exports Splitter Runs U.S. Production Waterborne Imports Canadian Imports Total Refinery Runs

0

2

4

6

8

10

12

14

16

18

20

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Mill

ion

BPD

Early 2014 Forecast

Potential Export Volumes

U.S. Exports 2020: 1.1 MMBPD 2025: 1.3 MMBPD

U.S. Exports 2025: 700 MBPD

Exports Required

11

* *Includes Canadian exports and exports of lightly processed condensate

Presentation Outline

• Evolving U.S. Crude Balance

• “Fit” Into Atlantic Basin Refineries

• Transportation Costs/Other Factors

• Final Analysis/Thoughts

12

Atlantic Basin Refining Environment

Latin America

9%

Europe 19%

U.S. 21%

Atlantic Basin: 49% Global

Refining Capacity Russia 6%

Asia-Pacific

29%

Middle East 9%

Africa 4%

13

European Region

Northwest Europe

12 Countries 56 Refineries 8.4 MMBPD

Mediterranean Europe 10 Countries 43 Refineries 5.5 MMBPD

Eastern Europe 9 Countries

28 Refineries 2.8 MMBPD

Total Europe 31 Countries

127 Refineries 16.7 MMBPD

• Three distinct regions: NW, Med, and Eastern Europe

• Total crude runs of 14.5 MMBPD in 2014;

• Limited and declining regional production; 60% is imported

• EU has over 70% imports

14

Designed for Lighter Crudes

0%

10%

20%

30%

40%

50%

60%

70%

Avg.

Nor

thw

est

Med

iterr

anea

n

East

ern

Avg.

PADD

I

PADD

III

Europe U.S.%

of C

rude

Cap

acity

% Coking % Cracking % Hydrocracking Total Upgrading

0%

20%

40%

60%

80%

100%

0.0

1.0

2.0

3.0

4.0

5.0

NorthernEurope

Eastern Europe Med Europe Ligh

t Cru

de, %

of T

otal

Impo

rts

Impo

rts,

Mill

ion

BPD

Total Light % Light

• European refiners less complex than U.S. counterparts – Even PADD I, the least

complex U.S. region, has significantly greater cracking capacity

• Almost all crude imports are light (>31 API)

15

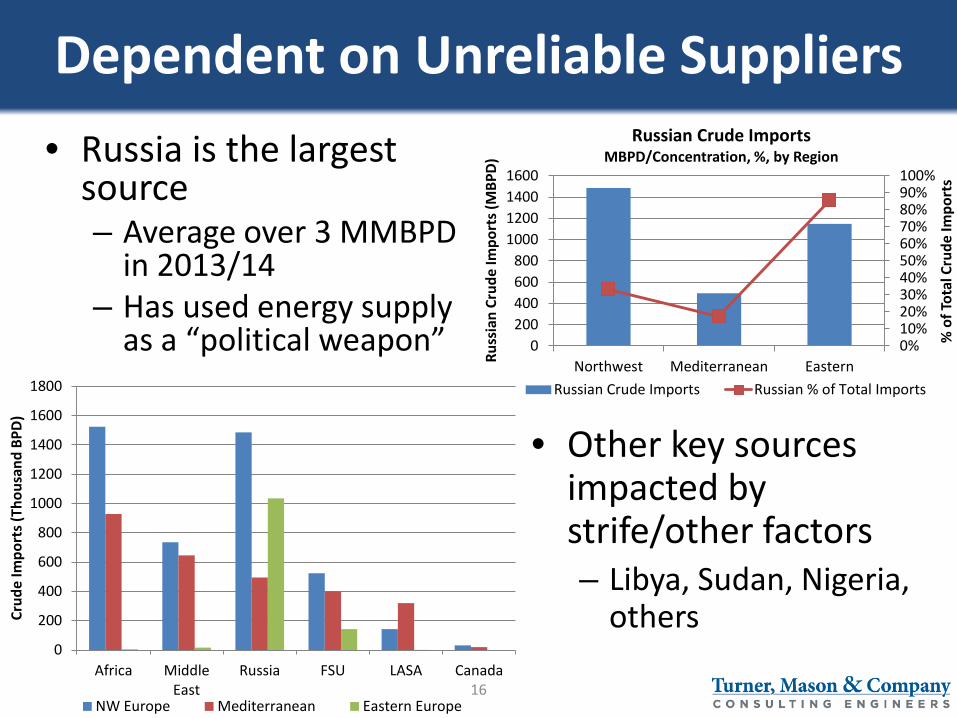

Dependent on Unreliable Suppliers

0

200

400

600

800

1000

1200

1400

1600

1800

Africa MiddleEast

Russia FSU LASA Canada

Crud

e Im

port

s (Th

ousa

nd B

PD)

NW Europe Mediterranean Eastern Europe

• Russia is the largest source – Average over 3 MMBPD

in 2013/14 – Has used energy supply

as a “political weapon” 0%10%20%30%40%50%60%70%80%90%100%

0200400600800

1000120014001600

Northwest Mediterranean Eastern

% o

f Tot

al C

rude

Impo

rts

Russ

ian

Crud

e Im

port

s (M

BPD)

Russian Crude Imports MBPD/Concentration, %, by Region

Russian Crude Imports Russian % of Total Imports

• Other key sources impacted by strife/other factors – Libya, Sudan, Nigeria,

others

16

Declining Volumes From Major Suppliers

-

2

4

6

8

10

12

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Crude Production - Africa

Libya Sudan + S. Sudan AngolaAlgeria Nigeria Rest of Africa

0

1

2

3

4

5

6

7

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Crud

e Pr

oduc

tion

(Mill

ion

BPD)

Crude Production – North Sea

Other U.K. Norway

17

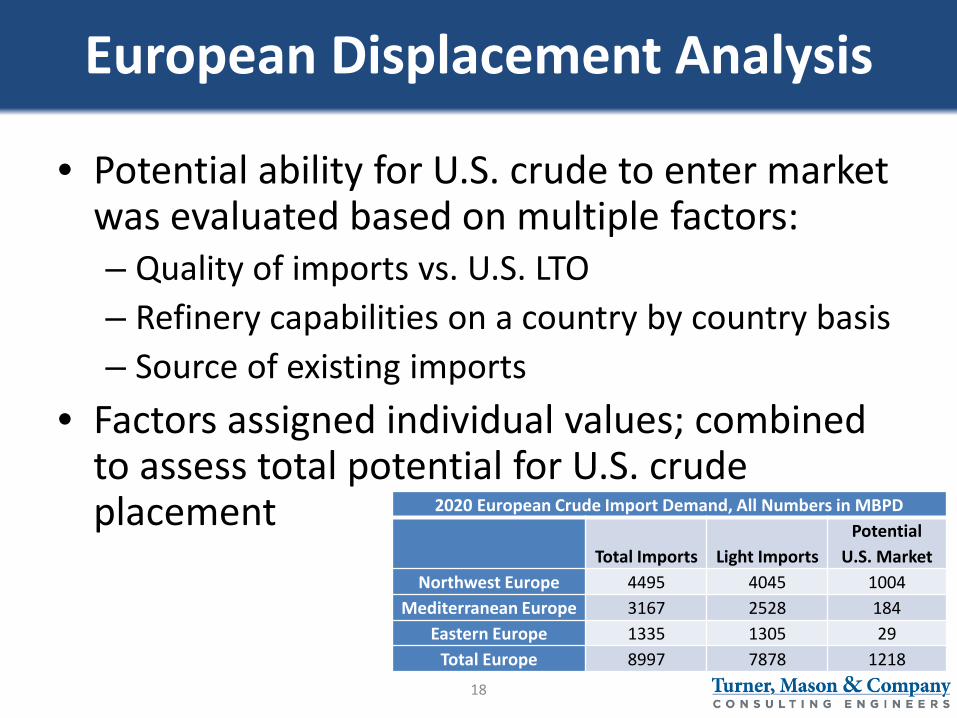

European Displacement Analysis

• Potential ability for U.S. crude to enter market was evaluated based on multiple factors: – Quality of imports vs. U.S. LTO – Refinery capabilities on a country by country basis – Source of existing imports

• Factors assigned individual values; combined to assess total potential for U.S. crude placement 2020 European Crude Import Demand, All Numbers in MBPD

Total Imports Light Imports Potential

U.S. Market Northwest Europe 4495 4045 1004

Mediterranean Europe 3167 2528 184 Eastern Europe 1335 1305 29

Total Europe 8997 7878 1218 18

Latin America

Brazil 13 Refineries 1.9 MMBPD

Mexico 6 Refineries 1.5 MMBPD

Rest of Latin America

20 Countries 51 Refineries 3.9 MMBPD

Total Latin America

22 Countries 70 Refineries 7.4 MMBPD

• Home to two OPEC members, Venezuela and Ecuador

• Region is net long crude; but quality is “mismatched” with refinery capability

• Have not been able to execute projects to fix “mismatch.”

• Light crude has market as diluent for blending with very heavy.

19

Refinery Complexity • Like European refiners,

Latin American facilities are less complex than U.S. – Avg. 40 MBPD larger – Avg. 26% more complex

• These refiners are well suited to process light crude

• Latin American crude production is increasingly heavy – Trend forecast to continue

0

2

4

6

8

10

12

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025Crud

e Pr

oduc

tion

(Mill

ion

BPD)

Latin American Crude Production Forecast

Latin American Med+Hvy Latin American Lt.

0%

10%

20%

30%

40%

50%

60%

70%

Avg. Mexico Brazil Rest Avg. PADD I PADD III

Latin America U.S.

% o

f Cru

de C

apac

ity

% Coking % Cracking % Hydrocracking Total Upgrading

20

Latin American vs. U.S. Refiners Comparison of Latin American to U.S. Refiners

# of Refineries

Capacity (MMBPD)

Total Upgrading

Cat Cracking Coking

Hydro-cracking

U.S. 123 18.02 56% 31% 15% 11% ● PADD 1 9 1.24 48% 38% 6% 3% ● PADD 3 55 9.22 60% 31% 16% 13% Latin America 70 7.39 30% 21% 8% 2% ● Mexico 6 1.54 37% 25% 12% -- ● Brazil 13 1.92 32% 26% 6% -- ● Venezuela 5 1.28 29% 18% 11% -- ● Argentina 10 0.61 40% 22% 15% 3% ● Netherlands Antilles 1 0.32 16% 16% -- -- ● Cuba 4 0.30 5% 5% -- -- ● Colombia 5 0.29 31% 31% -- -- ● Chile 3 0.23 49% 22% 6% 22% *O&G Journal, As of Jan 1, 2015

21

Latin American Crude Balance • Overall crude demand increases as there is some

refinery expansion • Demand will primarily be for lighter crudes as

regional production of heavy grows/is exported

7%

27%

17%

49%

Latin American Crude Import Sources, 2014

Russia

Middle East

North Africa

West Africa

0

100

200

300

400

Mex

ico

Trin

idad

/Tob

ago

Jam

aica

Dom

inic

an R

epub

lic

Braz

il

Vene

zuel

a

Chile

Peru

Uru

guay

Caribbean/CentralAmerica

South America

Impo

rts (

MBP

D)

Latin America Crude Imports

2014

2020

22

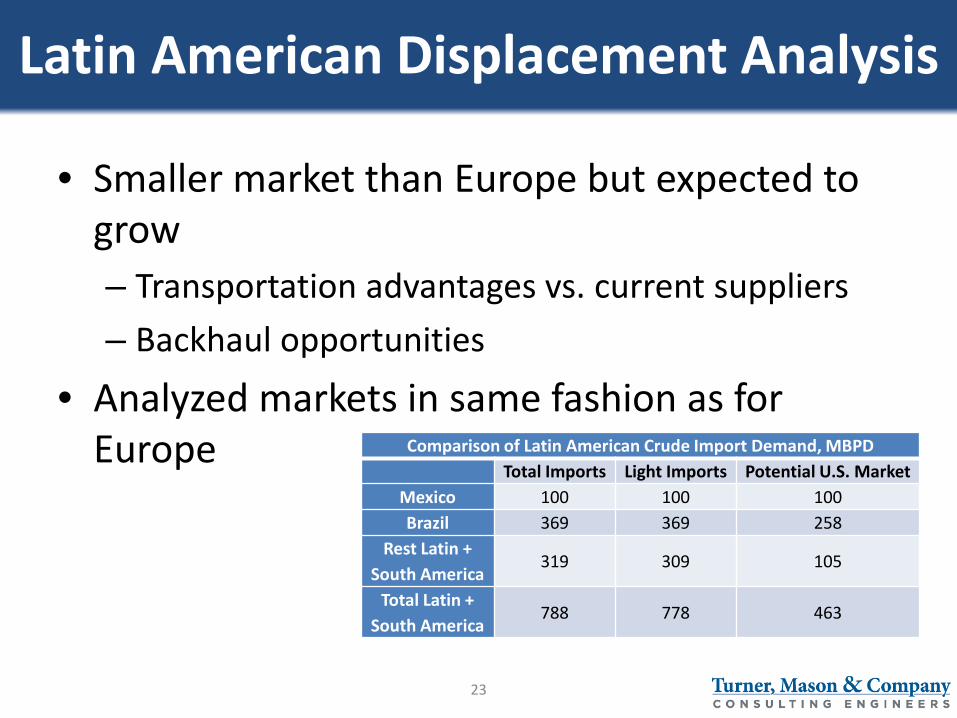

Latin American Displacement Analysis

• Smaller market than Europe but expected to grow – Transportation advantages vs. current suppliers – Backhaul opportunities

• Analyzed markets in same fashion as for Europe

Comparison of Latin American Crude Import Demand, MBPD Total Imports Light Imports Potential U.S. Market

Mexico 100 100 100 Brazil 369 369 258

Rest Latin + South America

319 309 105

Total Latin + South America

788 778 463

23

Presentation Outline

• Evolving U.S. Crude Balance

• “Fit” Into Atlantic Basin Refineries

• Transportation Costs/Other Factors

• Final Analysis/Thoughts

24

Worldwide Shipping Costs

• $2-3/bbl advantage to stay in Atlantic Basin

25

Worldwide Transit Times

• 10+ day advantage to stay in Atlantic Basin

26

• Middle East sees similar export costs and times to Europe vs. Asia/Pacific

• West Africa would see greatest impact from U.S. exports, as exports to Asia/Pacific $1-3/bbl higher, up to 15 days longer

Middle East/West Africa Costs & Times

27

Other Factors and Considerations • Relations between West and Russia on the “outs”

– Russia supplies over 3 MMBPD of oil to Europe – European dependency a potential political weapon

• U.S. a “secure” source of supply for Europe – Alternative sources subject to disruption

• China unlikely to want to be dependent on U.S. – China and U.S. are economic competitors – LTO from U.S. to Asia logistically disadvantaged

• U.S. potential supply source for Israel – Important Middle Eastern ally, imports about 250 MBPD – Russia has been a major source; Gulf producers not an option

• Synergies between LTO producers and their refineries – Several companies have LTO production in U.S. and European

refinery assets, potential supply chain optimization

28

Presentation Outline

• Evolving U.S. Crude Balance

• “Fit” Into Atlantic Basin Refineries

• Transportation Costs/Other Factors

• Final Analysis/Thoughts

29

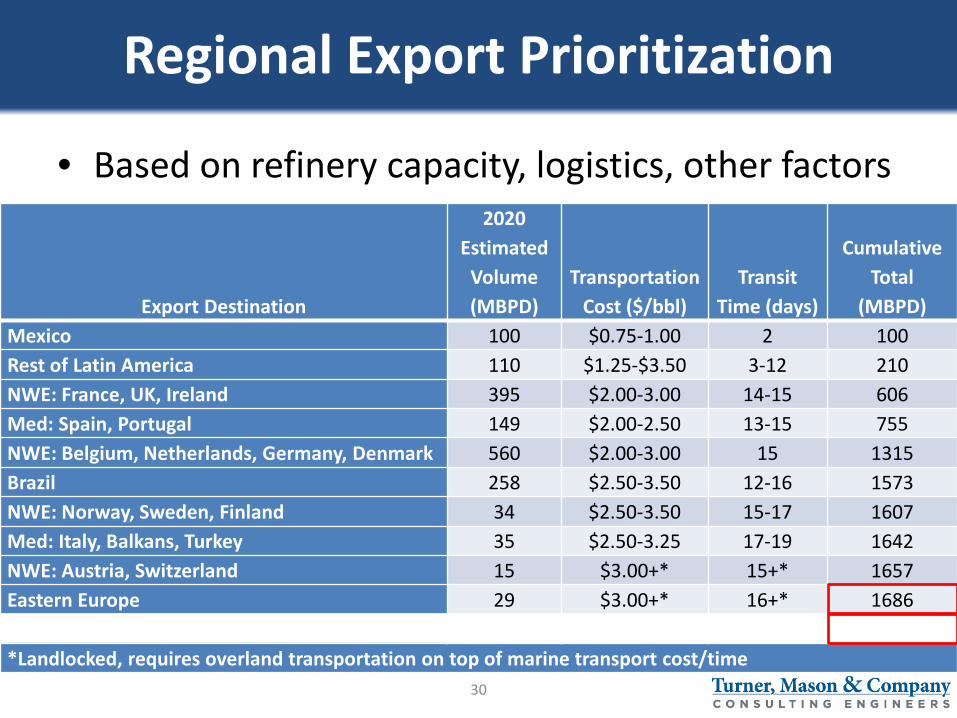

Regional Export Prioritization

• Based on refinery capacity, logistics, other factors

Export Destination

2020 Estimated

Volume (MBPD)

Transportation Cost ($/bbl)

Transit Time (days)

Cumulative Total

(MBPD) Mexico 100 $0.75-1.00 2 100 Rest of Latin America 110 $1.25-$3.50 3-12 210 NWE: France, UK, Ireland 395 $2.00-3.00 14-15 606 Med: Spain, Portugal 149 $2.00-2.50 13-15 755 NWE: Belgium, Netherlands, Germany, Denmark 560 $2.00-3.00 15 1315 Brazil 258 $2.50-3.50 12-16 1573 NWE: Norway, Sweden, Finland 34 $2.50-3.50 15-17 1607 Med: Italy, Balkans, Turkey 35 $2.50-3.25 17-19 1642 NWE: Austria, Switzerland 15 $3.00+* 15+* 1657 Eastern Europe 29 $3.00+* 16+* 1686 Israel 250 $3.00-3.50 20 1936 *Landlocked, requires overland transportation on top of marine transport cost/time

30

Recent Developments

• House approved oil export bill on October 9 – Bipartisan vote of 261 to 159 – President threatens veto; 29 votes short of 2/3rds

• Being Considered in Senate – Also unlikely to get 2/3rds majority – Possibility does exist for a “horse trade” – Strategy to attach to highway bill failed on 11/5

• Mexico swaps have been approved – 75 MBPD for next 12 months – Multiple applications for swaps to other countries

have been denied

31

Final Thoughts

• U.S. LTO exports “fit” well into Atlantic Basin

• Logistics favor Atlantic Basin over Asian markets

• Sources of light crude to Atlantic Basin declining • Country-by-country analysis shows room for > 1.5

MMBPD of light U.S. crude in Europe/LatAm • Geopolitical/other factors also support exports to

Atlantic Basin

• Exports will not go exclusively to Atlantic Basin • Significant need for exports not necessary until U.S.

production >10.5 MMBPD

32

Presenter

John R. Auers, P.E. Executive Vice President • Univ. of Nebraska Chem. Engr.

• Univ. of Houston MBA

• Formerly with Exxon

• Industry studies/analysis, forecasting, modeling

• Leads Outlook team

• Contact Info – [email protected] Office – 214-223-8887

33