26

US HOTEL OUTLOOK RECOVERY UNDER THREAT? July 23, 2020

US HOTEL OUTLOOK

R E C O V E R Y U N D E R T H R E A T ?

July 23, 2020

2CBRE U.S. HOTEL OUTLOOK

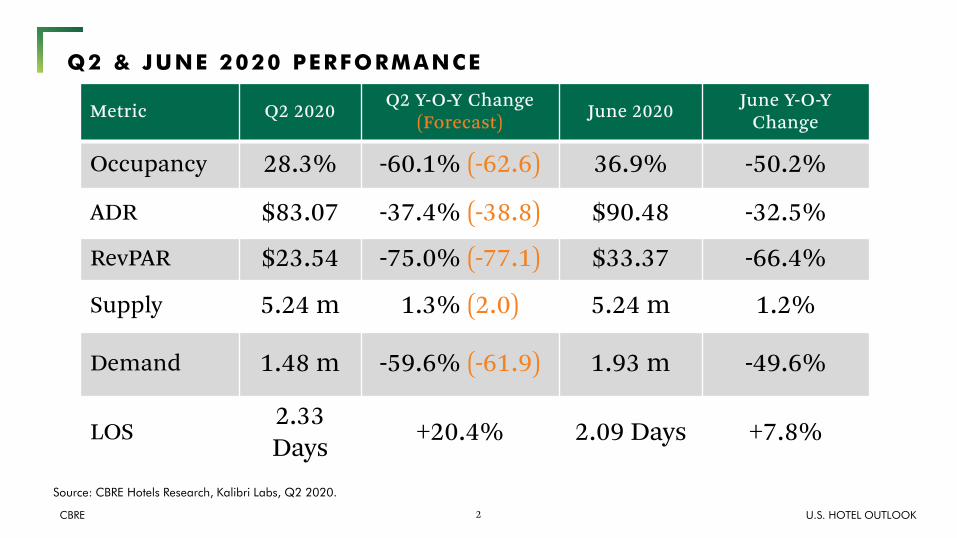

Source: CBRE Hotels Research, Kalibri Labs, Q2 2020.

Q2 & JUNE 2020 PERFORMANCE

Metric Q2 2020 Q2 Y-O-Y Change (Forecast) June 2020 June Y-O-Y

Change

Occupancy 28.3% -60.1% (-62.6) 36.9% -50.2%

ADR $83.07 -37.4% (-38.8) $90.48 -32.5%

RevPAR $23.54 -75.0% (-77.1) $33.37 -66.4%

Supply 5.24 m 1.3% (2.0) 5.24 m 1.2%

Demand 1.48 m -59.6% (-61.9) 1.93 m -49.6%

LOS2.33 Days +20.4% 2.09 Days +7.8%

3CBRE U.S. HOTEL OUTLOOK

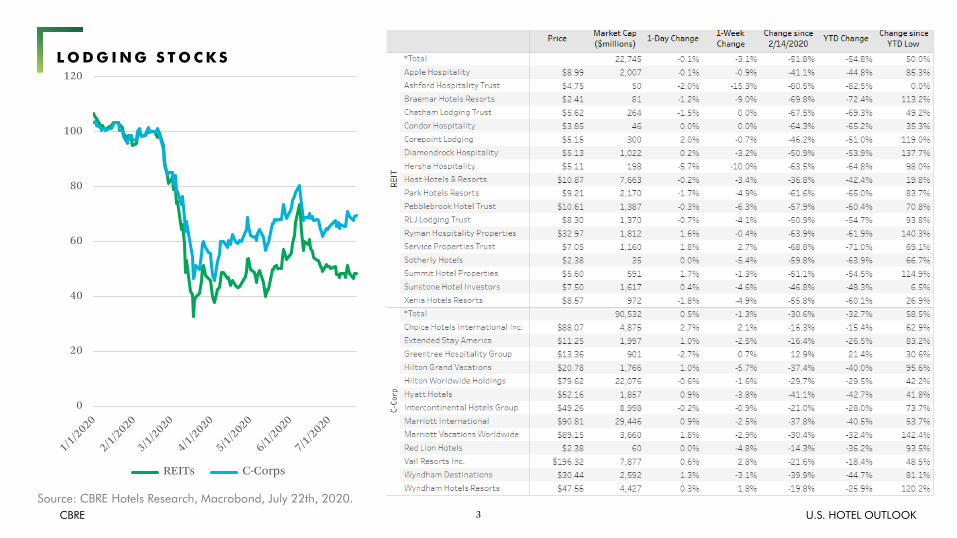

L O D G I N G S T O C K S

Source: CBRE Hotels Research, Macrobond, July 22th, 2020.

0

20

40

60

80

100

120

REITs C-Corps

4CBRE U.S. HOTEL OUTLOOK

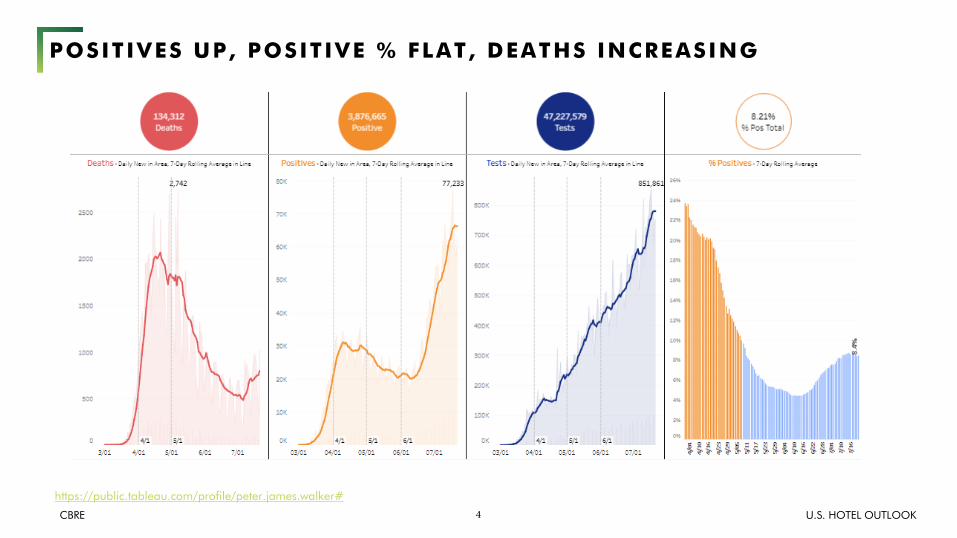

POSITIVES UP, POSITIVE % FLAT, DEATHS INCREASING

https://public.tableau.com/profile/peter.james.walker#

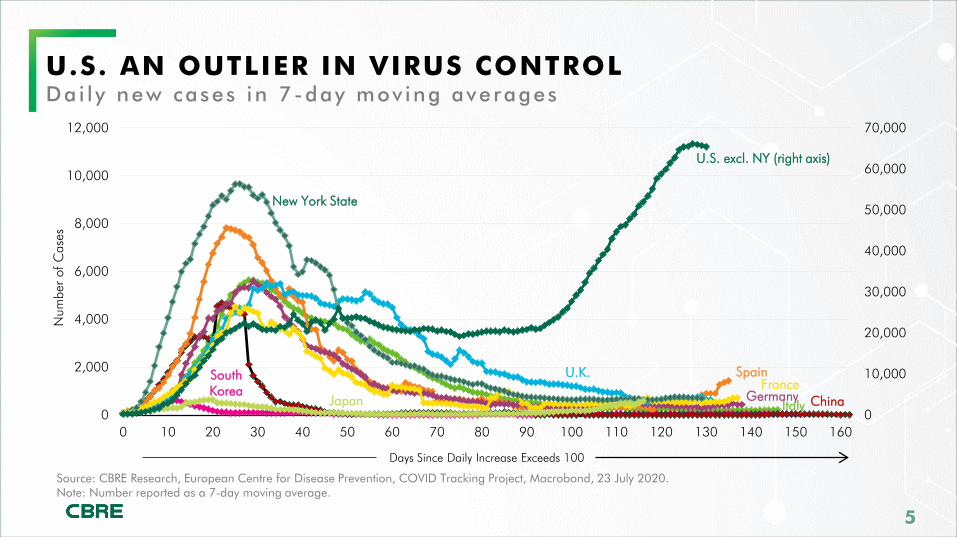

Italy

South Korea

China

Spain

Germany

U.K.France

New York State

Japan

U.S. excl. NY (right axis)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0

2,000

4,000

6,000

8,000

10,000

12,000

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160

Num

ber

of C

ases

U.S. AN OUTLIER IN VIRUS CONTROLDai l y new cases in 7-day mov ing averages

Source: CBRE Research, European Centre for Disease Prevention, COVID Tracking Project, Macrobond, 23 July 2020.Note: Number reported as a 7-day moving average.

Days Since Daily Increase Exceeds 100

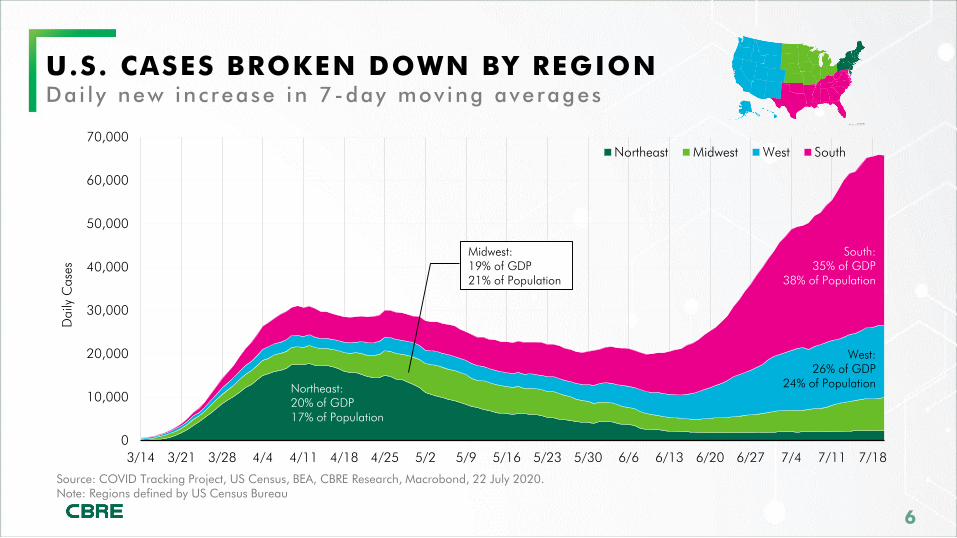

U.S. CASES BROKEN DOWN BY REGIONDai l y new inc rease in 7-day mov ing averages

Source: COVID Tracking Project, US Census, BEA, CBRE Research, Macrobond, 22 July 2020.Note: Regions defined by US Census Bureau

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

3/14 3/21 3/28 4/4 4/11 4/18 4/25 5/2 5/9 5/16 5/23 5/30 6/6 6/13 6/20 6/27 7/4 7/11 7/18

Dai

ly C

ases

Northeast Midwest West South

West: 26% of GDP

24% of Population Northeast: 20% of GDP 17% of Population

Midwest: 19% of GDP 21% of Population

South: 35% of GDP

38% of Population

7CBRE U.S. HOTEL OUTLOOK

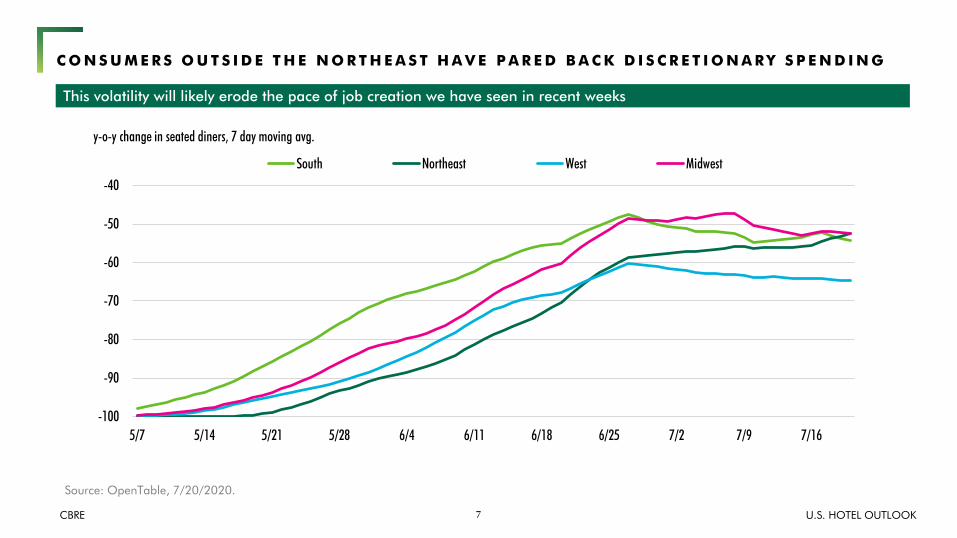

Source: OpenTable, 7/20/2020.

C O N S U M E R S O U T S I D E T H E N O R T H E A S T H A V E P A R E D B A C K D I S C R E T I O N A R Y S P E N D I N G

This volatility will likely erode the pace of job creation we have seen in recent weeks

-100

-90

-80

-70

-60

-50

-40

5/7 5/14 5/21 5/28 6/4 6/11 6/18 6/25 7/2 7/9 7/16

South Northeast West Midwest

y-o-y change in seated diners, 7 day moving avg.

8CBRE U.S. HOTEL OUTLOOK

-

50

100

150

200

(38)

(34)

(30)

(26)

(22)

(18)

(14)

(10) (6

) (2

) 2 6 10

14

18

22

26

30

34

38

42

46

50

54

58

62

66

70

74

78

82

86

90

94

98

102

106

110

114

118

122

126

130

134

138

142

146

150

154

158

162

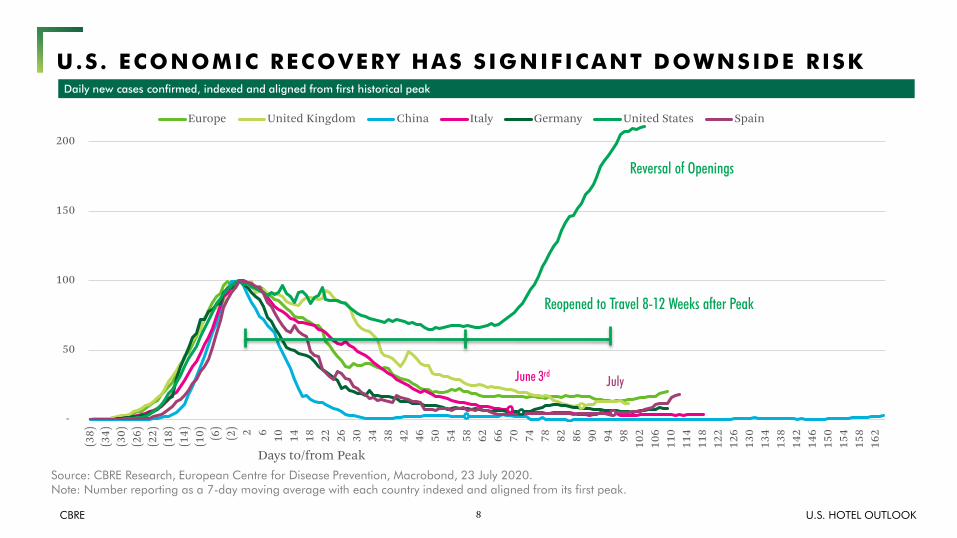

Days to/from Peak

Europe United Kingdom China Italy Germany United States Spain

Source: CBRE Research, European Centre for Disease Prevention, Macrobond, 23 July 2020.Note: Number reporting as a 7-day moving average with each country indexed and aligned from its first peak.

Reopened to Travel 8-12 Weeks after Peak

June 3rdJuly

U.S. ECONOMIC RECOVERY HAS SIGNIFICANT DOWNSIDE RISKDaily new cases confirmed, indexed and aligned from first historical peak

Reversal of Openings

9CBRE U.S. HOTEL OUTLOOK

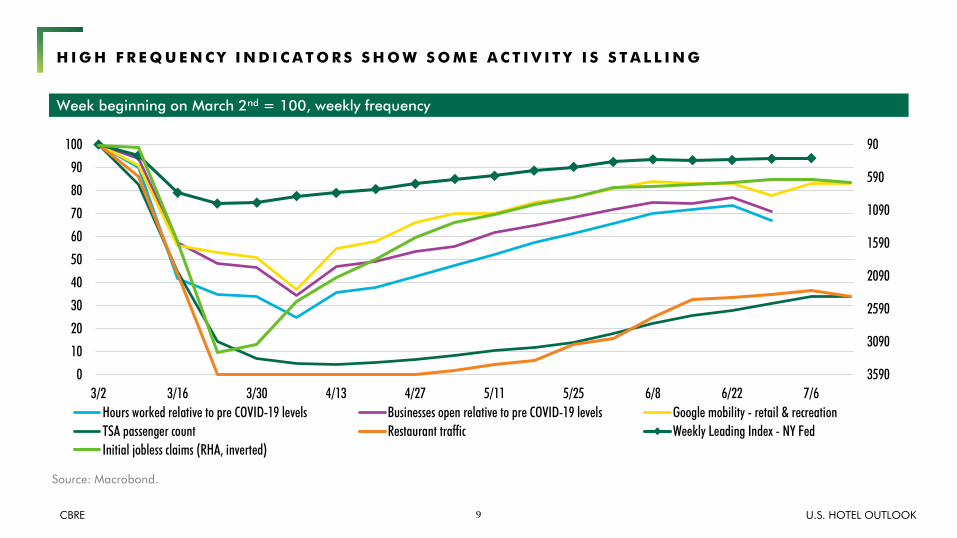

90

590

1090

1590

2090

2590

3090

35900

10

20

30

40

50

60

70

80

90

100

3/2 3/16 3/30 4/13 4/27 5/11 5/25 6/8 6/22 7/6Hours worked relative to pre COVID-19 levels Businesses open relative to pre COVID-19 levels Google mobility - retail & recreationTSA passenger count Restaurant traffic Weekly Leading Index - NY FedInitial jobless claims (RHA, inverted)

Source: Macrobond.

H I G H F R E Q U E N C Y I N D I C A T O R S S H O W S O M E A C T I V I T Y I S S T A L L I N G

Week beginning on March 2nd = 100, weekly frequency

10CBRE U.S. HOTEL OUTLOOK

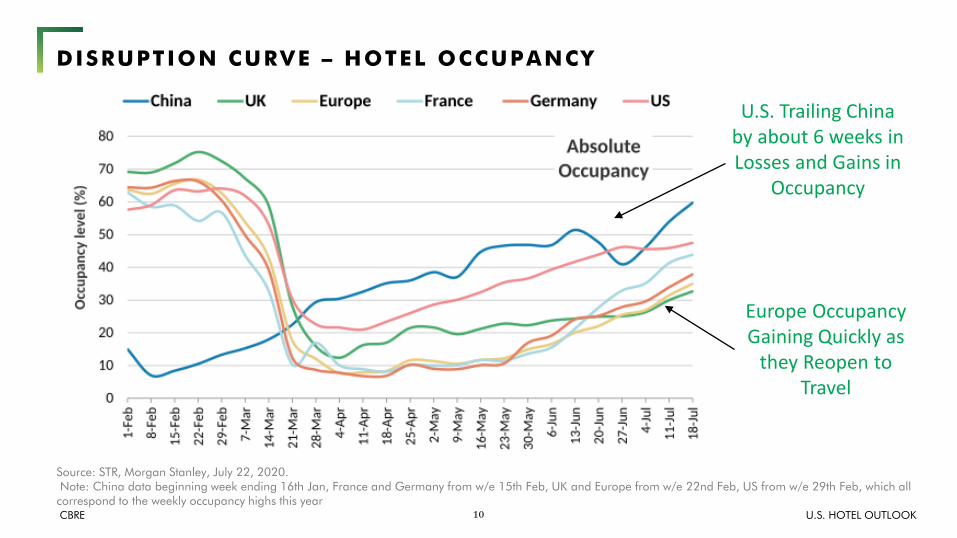

DISRUPTION CURVE – HOTEL OCCUPANCY

Source: STR, Morgan Stanley, July 22, 2020.Note: China data beginning week ending 16th Jan, France and Germany from w/e 15th Feb, UK and Europe from w/e 22nd Feb, US from w/e 29th Feb, which all correspond to the weekly occupancy highs this year

Europe Occupancy Gaining Quickly as

they Reopen to Travel

U.S. Trailing China by about 6 weeks in Losses and Gains in

Occupancy

ECONOMY

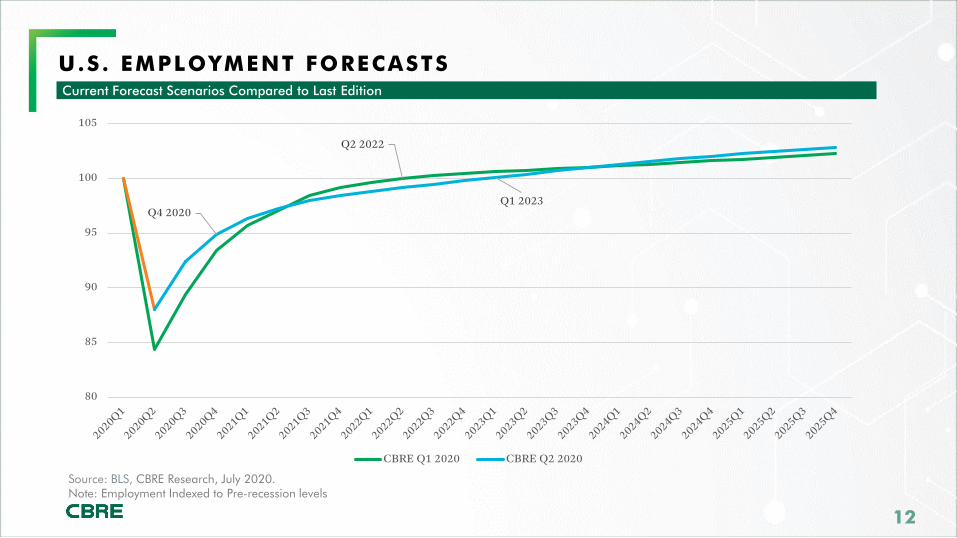

U.S. EMPLOYMENT FORECASTSCurrent Forecast Scenarios Compared to Last Edition

Source: BLS, CBRE Research, July 2020.Note: Employment Indexed to Pre-recession levels

Q2 2022

Q4 2020Q1 2023

80

85

90

95

100

105

CBRE Q1 2020 CBRE Q2 2020

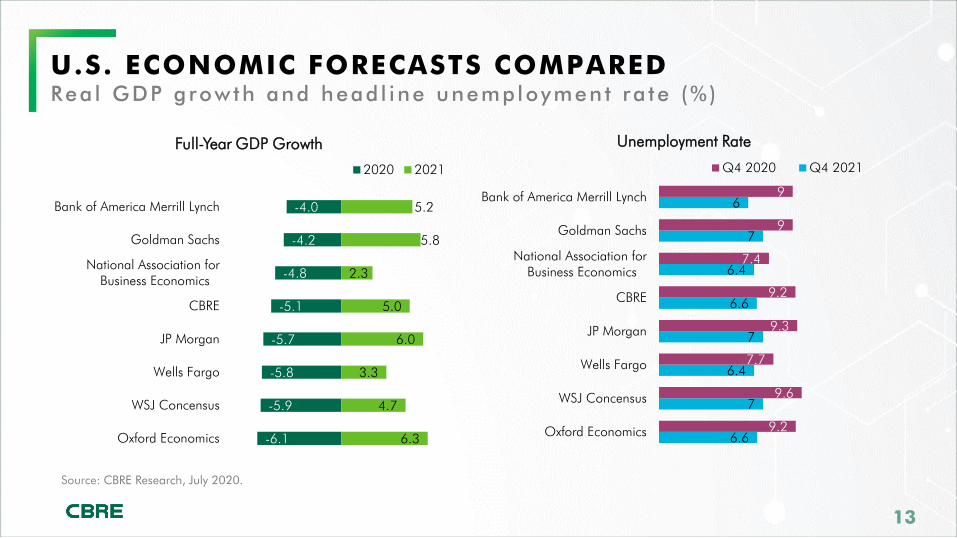

U.S. ECONOMIC FORECASTS COMPARED Rea l GDP growth and head l ine unemployment ra te (%)

Source: CBRE Research, July 2020.

-6.1

-5.9

-5.8

-5.7

-5.1

-4.8

-4.2

-4.0

6.3

4.7

3.3

6.0

5.0

2.3

5.8

5.2

Oxford Economics

WSJ Concensus

Wells Fargo

JP Morgan

CBRE

National Association for Business Economics

Goldman Sachs

Bank of America Merrill Lynch

Full-Year GDP Growth

2020 2021

6.6

7

6.4

7

6.6

6.4

7

6

9.2

9.6

7.7

9.3

9.2

7.4

9

9

Oxford Economics

WSJ Concensus

Wells Fargo

JP Morgan

CBRE

National Association for Business Economics

Goldman Sachs

Bank of America Merrill Lynch

Unemployment Rate

Q4 2020 Q4 2021

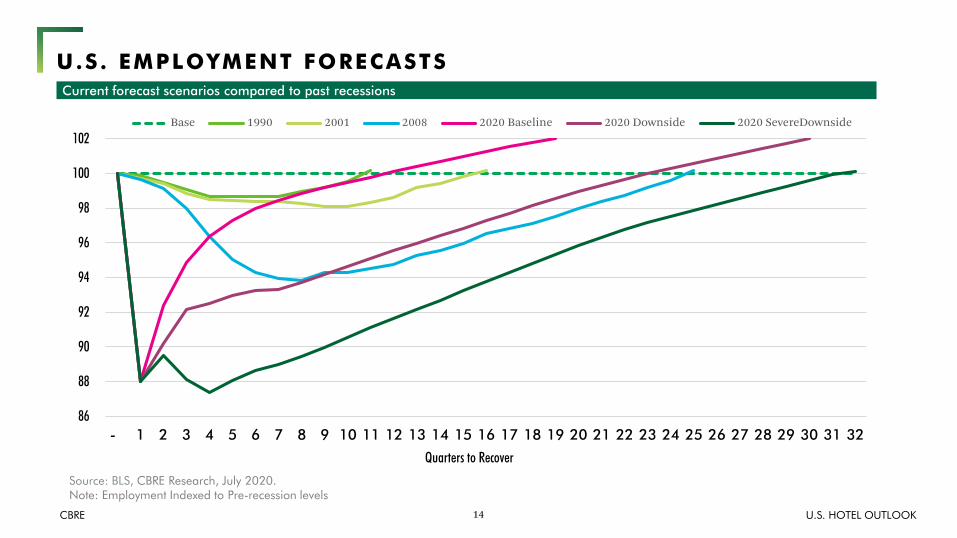

14CBRE U.S. HOTEL OUTLOOK

86

88

90

92

94

96

98

100

102

- 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32

Quarters to Recover

Base 1990 2001 2008 2020 Baseline 2020 Downside 2020 SevereDownside

Source: BLS, CBRE Research, July 2020.Note: Employment Indexed to Pre-recession levels

U.S. EMPLOYMENT FORECASTSCurrent forecast scenarios compared to past recessions

15CBRE U.S. HOTEL OUTLOOK

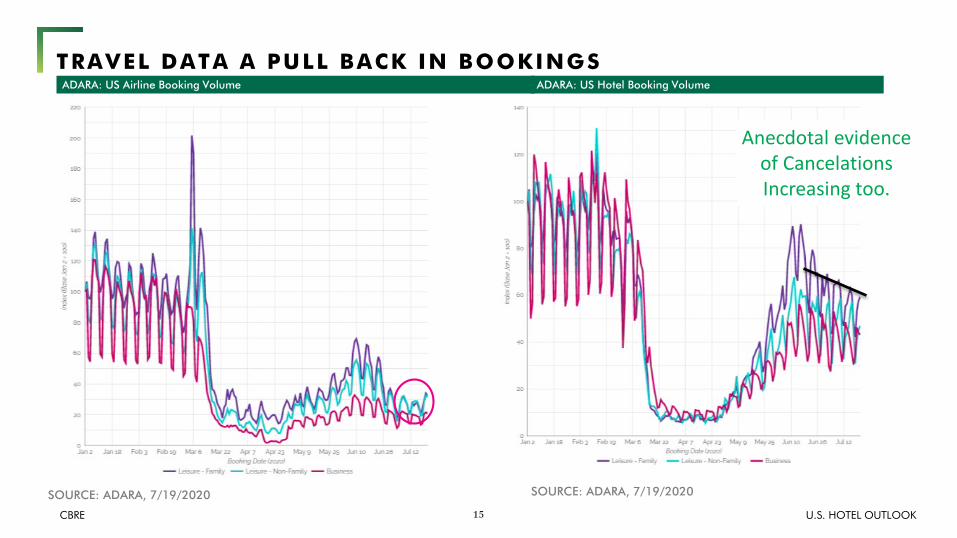

TRAVEL DATA A PULL BACK IN BOOKINGS

SOURCE: ADARA, 7/19/2020

ADARA: US Airline Booking Volume ADARA: US Hotel Booking Volume

Anecdotal evidence of Cancelations Increasing too.

SOURCE: ADARA, 7/19/2020

16CBRE U.S. HOTEL OUTLOOK

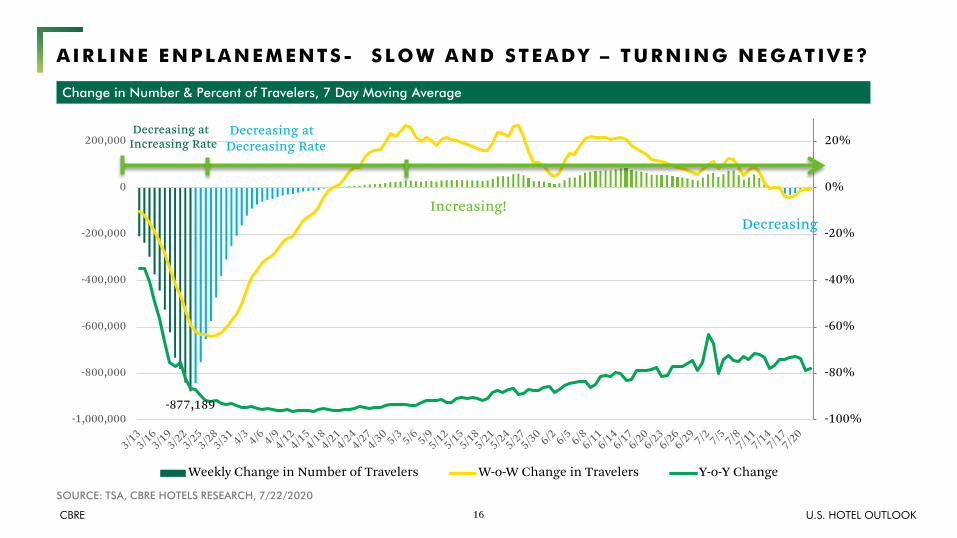

AIRL INE ENPLANEMENTS- SLOW AND STEADY – TURNING NEGATIVE?

SOURCE: TSA, CBRE HOTELS RESEARCH, 7/22/2020

Change in Number & Percent of Travelers, 7 Day Moving Average

-877,189-100%

-80%

-60%

-40%

-20%

0%

20%

-1,000,000

-800,000

-600,000

-400,000

-200,000

0

200,000

Weekly Change in Number of Travelers W-o-W Change in Travelers Y-o-Y Change

Decreasing atDecreasing Rate

Increasing!

Decreasing atIncreasing Rate

Decreasing

TURNING TO HOTELS

18CBRE U.S. HOTEL OUTLOOK

Source: CBRE Hotels Research, Kalibri Labs, Q2 2020.

JUNE 2020 TOP 10 MARKET PERFORMANCE

RevPAR Rank Market Occupancy

Y-o-Y RevPAR

1 Tucson 44.2% -33.2%

2 Jacksonville 53.8% -40.7%

3 San Bernardino/Riverside 55.7% -44.2%

4 St. Petersburg 46.1% -47.0%

5 Savannah 50.3% -47.7%

6 Virginia Beach/Norfolk 48.7% -49.3%

7 Memphis 46.6% -52.2%

8 Phoenix 38.4% -52.7%

9 Columbia 41.3% -53.0%

10 Charleston 49.8% -53.0%Bottom 10 Markets: Hawaii, Boston, San Francisco, Chicago, Washington DC, Orlando, New York, Seattle, New Orleans, San Jose

19CBRE U.S. HOTEL OUTLOOK

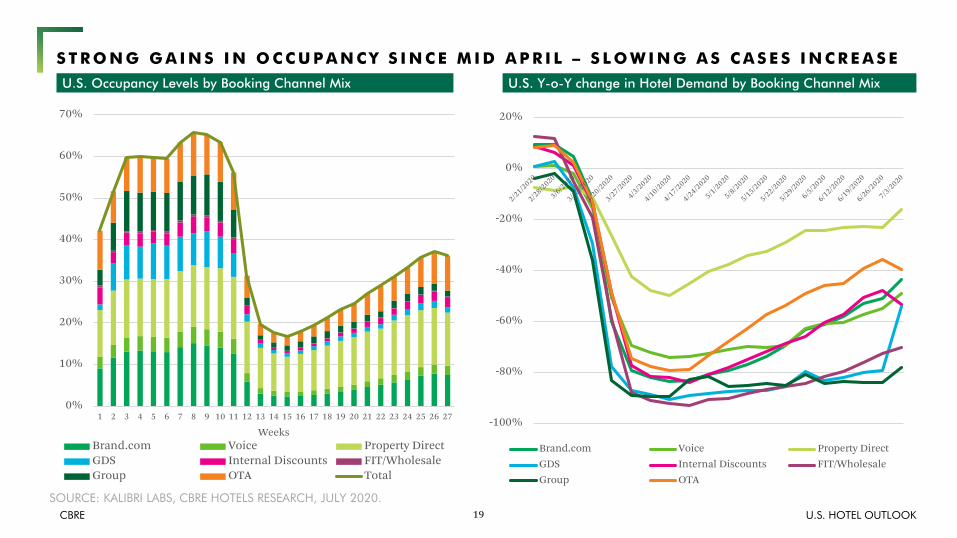

S T R O N G G A I N S I N O C C U P A N C Y S I N C E M I D A P R I L – S L O W I N G A S C A S E S I N C R E A S E

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

WeeksBrand.com Voice Property DirectGDS Internal Discounts FIT/WholesaleGroup OTA Total

-100%

-80%

-60%

-40%

-20%

0%

20%

Brand.com Voice Property DirectGDS Internal Discounts FIT/WholesaleGroup OTA

SOURCE: KALIBRI LABS, CBRE HOTELS RESEARCH, JULY 2020.

U.S. Occupancy Levels by Booking Channel Mix U.S. Y-o-Y change in Hotel Demand by Booking Channel Mix

20CBRE U.S. HOTEL OUTLOOK

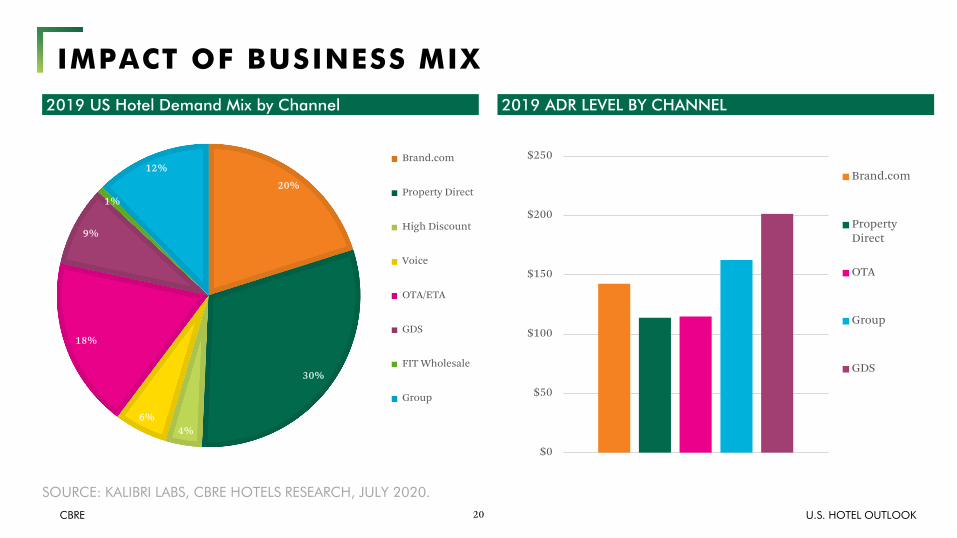

IMPACT OF BUSINESS MIX

20%

30%

4%6%

18%

9%

1%

12% Brand.com

Property Direct

High Discount

Voice

OTA/ETA

GDS

FIT Wholesale

Group

SOURCE: KALIBRI LABS, CBRE HOTELS RESEARCH, JULY 2020.

2019 US Hotel Demand Mix by Channel 2019 ADR LEVEL BY CHANNEL

$0

$50

$100

$150

$200

$250

Brand.com

PropertyDirect

OTA

Group

GDS

21CBRE U.S. HOTEL OUTLOOK

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 2 3 4 5 6 7 8 9 10 11 12

Month

2015 - 2019 2020

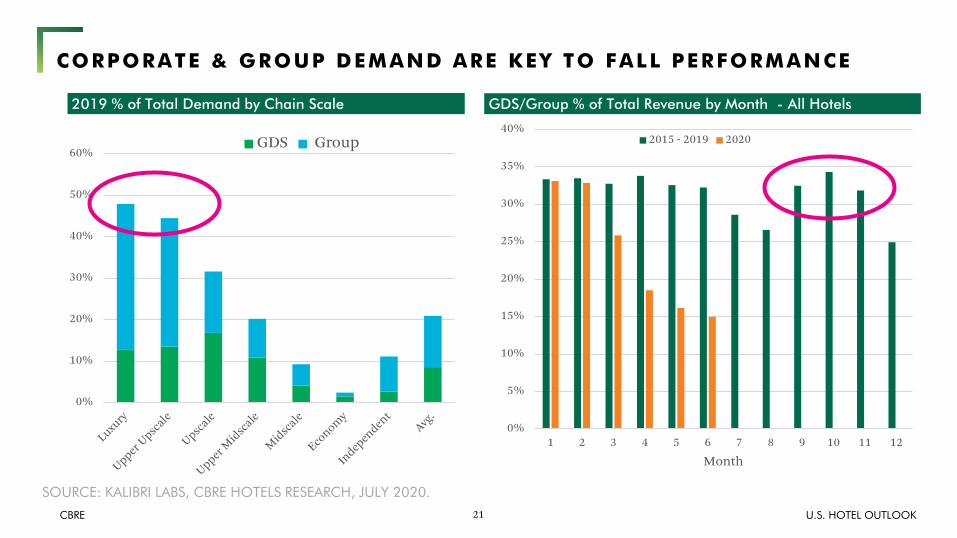

CORPORATE & GROUP DEMAND ARE KEY TO FALL PERFORMANCE

0%

10%

20%

30%

40%

50%

60%GDS Group

SOURCE: KALIBRI LABS, CBRE HOTELS RESEARCH, JULY 2020.

2019 % of Total Demand by Chain Scale GDS/Group % of Total Revenue by Month - All Hotels

22CBRE U.S. HOTEL OUTLOOK

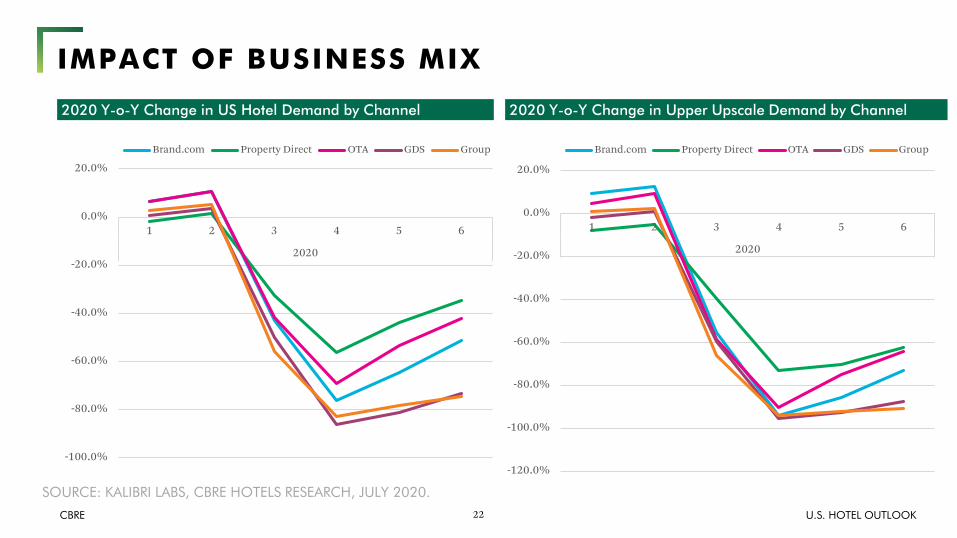

IMPACT OF BUSINESS MIX

SOURCE: KALIBRI LABS, CBRE HOTELS RESEARCH, JULY 2020.

2020 Y-o-Y Change in US Hotel Demand by Channel

-100.0%

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

1 2 3 4 5 6

2020

Brand.com Property Direct OTA GDS Group

2020 Y-o-Y Change in Upper Upscale Demand by Channel

-120.0%

-100.0%

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

1 2 3 4 5 6

2020

Brand.com Property Direct OTA GDS Group

23CBRE U.S. HOTEL OUTLOOK

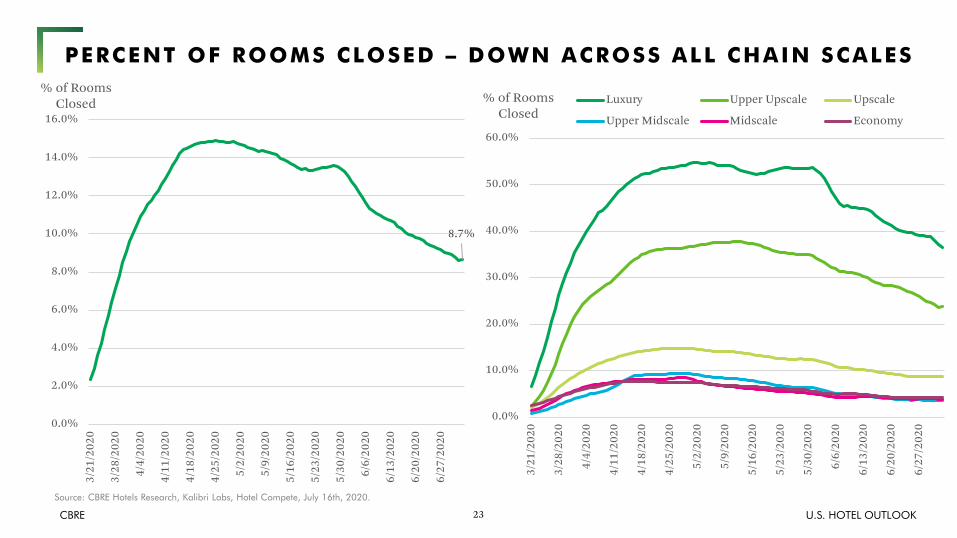

PERCENT OF ROOMS CLOSED – DOWN ACROSS ALL CHAIN SCALES

Source: CBRE Hotels Research, Kalibri Labs, Hotel Compete, July 16th, 2020.

8.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

3/21

/202

0

3/28

/202

0

4/4/

2020

4/11

/202

0

4/18

/202

0

4/25

/202

0

5/2/

2020

5/9/

2020

5/16

/202

0

5/23

/202

0

5/30

/202

0

6/6/

2020

6/13

/202

0

6/20

/202

0

6/27

/202

0

% of Rooms Closed

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

3/21

/202

0

3/28

/202

0

4/4/

2020

4/11

/202

0

4/18

/202

0

4/25

/202

0

5/2/

2020

5/9/

2020

5/16

/202

0

5/23

/202

0

5/30

/202

0

6/6/

2020

6/13

/202

0

6/20

/202

0

6/27

/202

0

% of Rooms Closed

Luxury Upper Upscale Upscale

Upper Midscale Midscale Economy

24CBRE U.S. HOTEL OUTLOOK

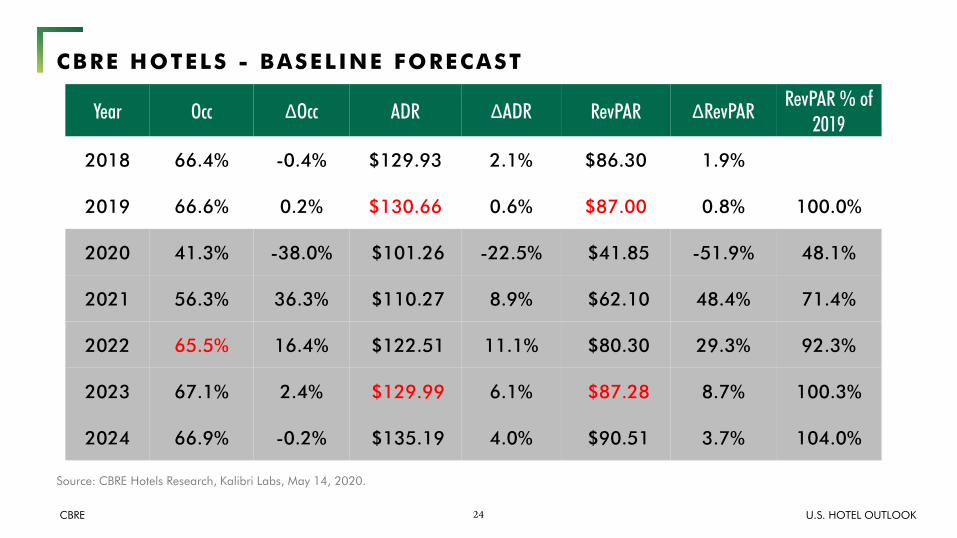

CBRE HOTELS - BASELINE FORECAST

Source: CBRE Hotels Research, Kalibri Labs, May 14, 2020.

Year Occ ΔOcc ADR ΔADR RevPAR ΔRevPAR RevPAR % of 2019

2018 66.4% -0.4% $129.93 2.1% $86.30 1.9%

2019 66.6% 0.2% $130.66 0.6% $87.00 0.8% 100.0%

2020 41.3% -38.0% $101.26 -22.5% $41.85 -51.9% 48.1%

2021 56.3% 36.3% $110.27 8.9% $62.10 48.4% 71.4%

2022 65.5% 16.4% $122.51 11.1% $80.30 29.3% 92.3%

2023 67.1% 2.4% $129.99 6.1% $87.28 8.7% 100.3%

2024 66.9% -0.2% $135.19 4.0% $90.51 3.7% 104.0%

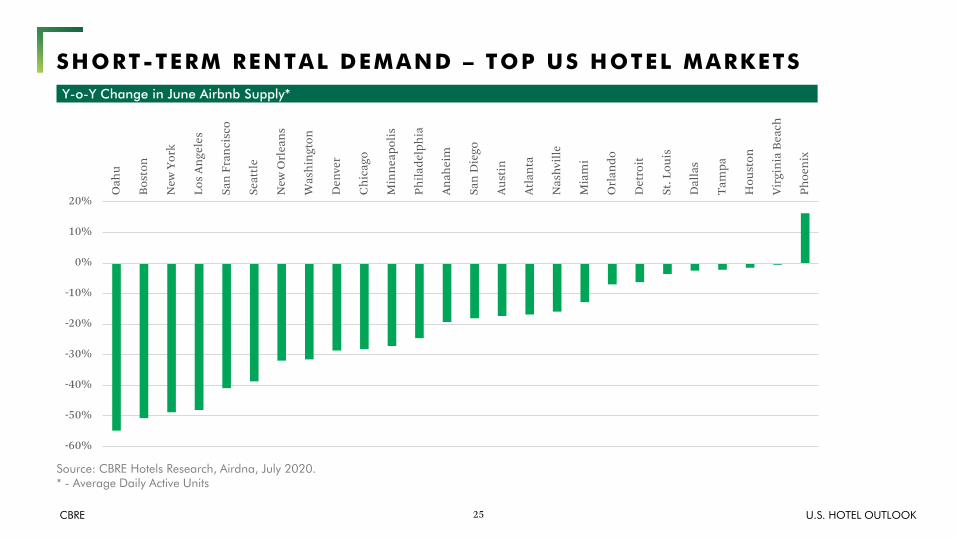

25CBRE U.S. HOTEL OUTLOOK

SHORT-TERM RENTAL DEMAND – TOP US HOTEL MARKETS

Source: CBRE Hotels Research, Airdna, July 2020.* - Average Daily Active Units

Y-o-Y Change in June Airbnb Supply*

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

Oah

u

Bos

ton

New

Yor

k

Los

Ange

les

San

Fran

cisc

o

Seat

tle

New

Orl

eans

Was

hing

ton

Den

ver

Chi

cago

Min

neap

olis

Phila

delp

hia

Anah

eim

San

Die

go

Aust

in

Atla

nta

Nas

hvill

e

Mia

mi

Orl

ando

Det

roit

St. L

ouis

Dal

las

Tam

pa

Hou

ston

Virg

inia

Bea

ch

Phoe

nix

THANK YOU!

July 23, 2020

This presentation has been prepared in good faith based on CBRE’s current views of the commercial real-estate market. Although CBRE believes its views reflect market conditions on the date of this presentation, they aresubject to significant uncertainties and contingencies, many of which are beyond CBRE’s control. In addition, many of CBRE’s views are opinion and/or projections based on CBRE’s subjective analyses of current marketcircumstances. Other firms may have different opinions, projections and analyses, and actual market conditions in the future may cause CBRE’s current views to later be incorrect. CBRE has no obligation to update its viewsherein if its opinions, projections, analyses or market circumstances later change.Nothing in this presentation should be construed as an indicator of the future performance of CBRE’s securities or of the performance of any other company’s securities. You should not purchase or sell securities – of CBREor any other company – based on the views herein. CBRE disclaims all liability for securities purchased or sold based on information herein, and by viewing this presentation, you waive all claims against CBRE and thepresenter as well as against CBRE’s affiliates, officers, directors, employees, agents, advisers and representatives arising out of the accuracy, completeness, adequacy or your use of the information herein.© Copyright 2020 CBRE