22

OIL PRICE OUTLOOK US FEBRUARY 2017

| Date post: | 12-Apr-2018 |

| Category: |

Documents |

| Upload: | truonghanh |

| View: | 221 times |

| Download: | 2 times |

OIL PRICE

OUTLOOK

US

FEBRUARY 2017

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017

2

1. OPEC output deal may have a limited impact on prices. Despite signs

of compliance, implementation and monitoring is challenging in some

countries

2. Going forward, inventory correction and the lagged effect of CAPEX

cuts should lead to higher prices

3. The recovery of U.S. shale production is expected to prevent a steep

upturn in prices; nevertheless, there is uncertainty on the extent and

speed of the rebound

4. Little to no upside from demand. Demand growth continues to be

supported by emerging markets and the U.S., but it has eased

5. Slow recovery and convergence to $60/bbl, which would be a sweet

spot for both consumers and producers

Key Messages

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

OPEC DEAL

OPEC deal carries

prices back above

$50/bbl

3 Source: BBVA Research & Haver Analytics

• Deal should be seen as an

effort to stabilize the market

• Rather than triggering a rapid

and sustained increase in

prices, cuts imposed an

effective price floor

BRENT CRUDE OIL PRICES

$ per barrel

09

/20

/16

09

/27

/16

10

/04

/16

10

/11

/16

10

/18

/16

10

/25

/16

11

/01

/16

11

/08

/16

11

/15

/16

11

/22

/16

11

/29

/16

12

/06

/16

12

/13

/16

12

/20

/16

12

/27

/16

01

/03

/17

01

/10

/17

01

/17

/17

01

/24

/17

01

/31

/17

02

/07

/17

40

42

44

46

48

50

52

54

56

58

60OPEC

Meeting

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

30

35

40

45

50

55

60

1 2 3 4 5 6 7 8 9 10 11 12

Months Ahead

02/09/17

1 month ago

3 months ago

6 months ago

30

35

40

45

50

55

60

1 2 3 4 5 6 7 8 9 10 11 12

Months Ahead

02/09/17

1 month ago

3 months ago

6 months ago

WTI CRUDE FUTURES

$ per barrel BRENT CRUDE FUTURES

$ per barrel

Source : BBVA Research & Bloomberg 4

FUTURES

Futures rise as markets perceive that OPEC has retaken its role of

market stabilizer

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

5

OPEC MONITOR

January was first big test for OPEC production deal, with estimated

compliance more than halfway to target

*No production adjustment for Libya or Nigeria; Proposed production increase of 90K for Iran

OPEC PROGRESS TOWARDS PRODUCTION COMMITMENTS*

Production Cut

Goal (K, bbl/d) Goal Achieved? Status Update

Saudi Arabia 486 Estimated cuts of 500K bbl/d, surpassing target

Iraq 210

(120)

Kurdistan region unwilling to cooperate with cuts; difficulties in lowering output

without triggering contractual obligations to pay IOCs

UAE 139 Estimated cuts of 160K bbl/d, surpassing target

Kuwait 131 Estimated cuts of 150K bbl/d, surpassing target

Venezuela 95

(70)

Announced in late December that cut would be implemented starting Jan. 1, but

then Maduro announced plan to stabilize oil prices

Angola 78

(0)

State oil company has announced output cuts in accordance with deal

Algeria 50 Estimated cuts of 70K bbl/d, surpassing target

Qatar 30

(5)

Started informing customers in December of supply cuts starting Jan. 1

Ecuador 26

(20)

Reduction to be result of allowing production at mature oil fields to fall; peak

reductions to occur in March and April

Gabon 9 Estimated cuts of 15K bbl/d, surpassing target; rejoined OPEC in July; faced

falling oil production last year, headlined by a large-scale strike by oil workers

Source: BBVA Research, Bloomberg & news sources

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

6

NOPEC MONITOR

Bulk of non-OPEC production cuts to come from Russia, but

achievement of goal will take time

NON-OPEC PROGRESS TOWARDS PRODUCTION COMMITMENTS

Production Cut

Goal (K, bbl/d) Goal Achieved? Status Update

Russia 300

(117)

Surpassed Jan. goal of 50K; expect to reach 300K by end of 1H2017, but has

announced increase in oil exports in 2017

Mexico 100 ? Reduction to be result of allowing production at mature oil fields to fall

Oman 45 ? Energy minister said that daily production quotas for oil producing companies

have been set, but that country will maintain production of 1M bbl/d this year.

Azerbaijan 35

Began implementing production cuts on January 1. Energy minister said output

had been cut to 789K in Jan

Kazakhstan 20 Energy ministry stated that commitment had already been met, but plans to

increase output in 2017

Malaysia 20 ? State oil firm to implement cuts starting in January; 2nd straight year of

production decline

Equatorial Guinea 12 ? Applied to join OPEC

Bahrain 10 ? No status update

South Sudan 8 In the process of doubling crude production after 2 year halt

Brunei 4 ? No status update

Sudan 4 ? No status update

Source: BBVA Research, Bloomberg & news sources

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

SUPPLY

Upside risks from Libya and Nigeria remain subdued

Source: BBVA Research & Haver Analytics

OPEC: CHANGE IN CRUDE OIL PRODUCTION BY COUNTRY

YoY, million barrels per day

-1200

-1000

-800

-600

-400

-200

0

200

400

600

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Nigeria

Libya

7

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

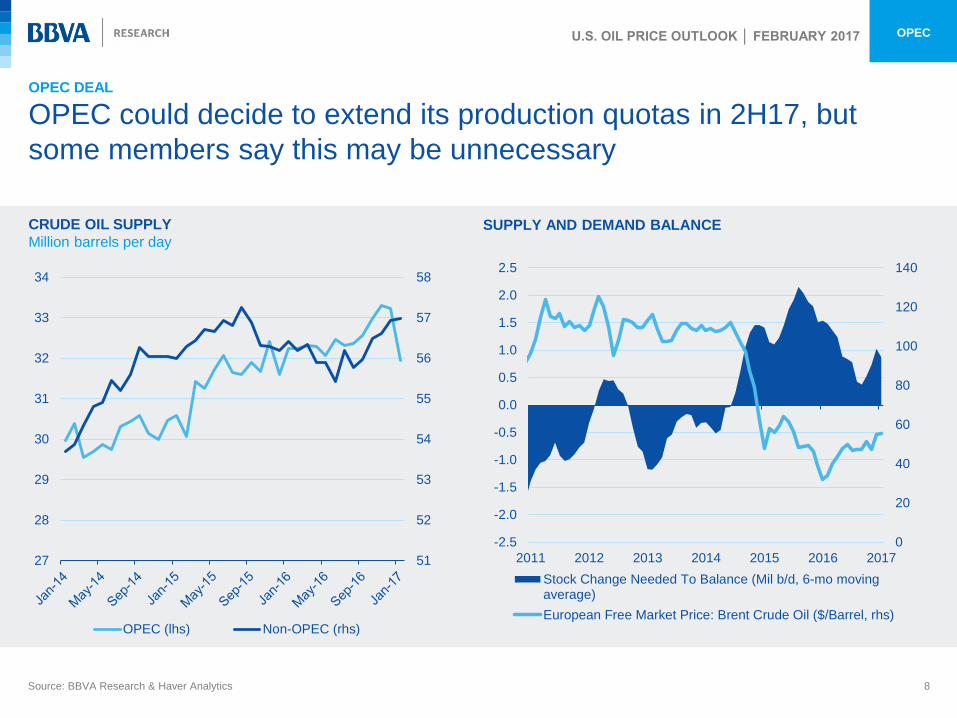

OPEC DEAL

OPEC could decide to extend its production quotas in 2H17, but

some members say this may be unnecessary

Source: BBVA Research & Haver Analytics

CRUDE OIL SUPPLY

Million barrels per day SUPPLY AND DEMAND BALANCE

51

52

53

54

55

56

57

58

27

28

29

30

31

32

33

34

OPEC (lhs) Non-OPEC (rhs)

8

0

20

40

60

80

100

120

140

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2011 2012 2013 2014 2015 2016 2017

Stock Change Needed To Balance (Mil b/d, 6-mo movingaverage)

European Free Market Price: Brent Crude Oil ($/Barrel, rhs)

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 OPEC

9

SUPPLY

A more competitive environment will continue to hinder the ability of

OPEC to stabilize the market

Source: Rystad Energy UCube; production forecasts could differ from BBVA Research baseline based on variance in assumptions

NET ADDITIONS IN GLOBAL LIQUIDS SUPPLY BY SUPPLY SEGMENT GROUP

YoY, million barrels per day

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2013 2014 2015 2016 2017 2018 2019 2020

OPEC

Other Onshore

Shale/Tight oil

Oil sands

Offshore shelf

Offshoremidwater

Offshoredeepwater

Total Supply

Forecasts

No

n-O

PE

C

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 USA

INVENTORIES

Signs of a more balanced market will emerge as inventories continue

to decline

10 Source: BBVA Research & Haver Analytics

U.S. STOCKS OF CRUDE OIL EXCLUDING SPR

EOP, million barrels

GLOBAL OIL INVENTORIES

EOP, million barrels

250

300

350

400

450

500

550

1500

1700

1900

2100

2300

2500

2700

2900

3100

3300

2011 2012 2013 2014 2015 2016 2017

Oil Inventories: OECD (EOP, Mil.Bbl)

Oil Inventories: Non-OECD (EOP, Mil.Bbl)

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 USA

CAPEX

Shale producers to increase CAPEX in response to upturn in prices

Source: Rystad Energy UCube

• Slowdown in capital spending

resulted from a weak price

environment

• Many shale companies covering

CAPEX with cash flows, moving

away from strong reliance on

debt

• CAPEX expected to rise this

year, especially as larger U.S.

companies spend on drilling and

completing wells

CAPITAL AND OPERATING EXPENDITURES FOR U.S. SHALE OIL

Billion USD

0

50

100

150

200

250

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Opex

Exploration Capex

Capex

11

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 USA

U.S. RECOVERY

Economics of fracking continue to remain favorable

12

ASSET BREAKEVEN OIL PRICE BY SHALE PLAY, PRODUCING

USD/bbl, Brent-linked

Source: Rystad Energy UCube & Haver Analytics

0

10

20

30

40

50

60

Average

Oil Price (2/8/17)

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 USA

U.S. RECOVERY

Recent production gains explained by uptick in completed wells

13 Source: BBVA Research & Haver Analytics

U.S. RATIO OF DCU TO COMPLETED WELLS

Units

Source: Rystad Energy UCube

0

20

40

60

80

100

120

2011 2012 2013 2014 2015 2016

Bakken Eagle FordHaynesville/Bossier MarcellusNiobrara Permian Delaware TightPermian Midland Tight Utica

U.S. ACTIVE RIG COUNT AND CRUDE OIL PRODUCTION

0

100

200

300

400

500

600

700

800

8000

8200

8400

8600

8800

9000

9200

9400

Jan-1

6

Feb

-16

Ma

r-1

6

Apr-

16

Ma

y-1

6

Jun-1

6

Jul-1

6

Aug-1

6

Sep-1

6

Oct-

16

No

v-1

6

De

c-1

6

Jan-1

7

Feb

-17

US Weekly Crude Oil Field Production (Thous. Barrels/Day)

Baker Hughes Active Rig Count: US (Units, rhs)

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 USA

POLICY

Trump’s America First Energy Plan: Make oil & gas great again

14 Source: S&P Global Platts, The Brattle Group, White House, Bloomberg

• Destination Based Cash Flow Tax (DBCFT) – would lower corporate tax rate to 20%

• U.S. oil industry incentivized to export more crude oil and products and import less;

refiners would shift toward domestic crude sourcing

• Advancing pipelines is expected to decrease costs of moving oil to refineries and lower

breakevens

• However capacity to generate further investments in oil and gas will be challenged by

the current levels of oil prices

• Withdrawal from CPP, COP21; elimination of Climate Action Plan

• Suspending social cost of carbon calculation

• Possibility of turning over federal lands to local control, which could facilitate drilling

Corporate Tax

Reform

Keystone and

Dakota Access

Pipelines

Deregulation

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 DEMAND

15

DEMAND

Non-OECD countries expected to lead demand in long-term, despite

signs of slowing growth

Source: BBVA Research & Haver Analytics

OIL PRODUCT DEMAND

YoY % change, million barrels per day

-1000

-500

0

500

1000

1500

2000

2500

3000

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Western Europe United States China India Total World

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 DEMAND

16

CHINA

China's rebalancing and transition to a cleaner economy may result in

slower growth of demand for fossil fuels

Source: BBVA Research & Haver Analytics

CHINA: OIL PRODUCT DEMAND AND INDUSTRIAL

PRODUCTION

YoY % change

CHINA: CRUDE AND TOTAL PETROLEUM PRODUCTS

INVENTORIES

EOP, million barrels

160

180

200

220

240

260

280

0

100

200

300

400

500

600

700

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Crude Oil Total Products (rhs)

0%

5%

10%

15%

20%

25%

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Industrial Production Oil Product Demand

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 DEMAND

ELECTRIC VEHICLES

Improvements in lithium-ion batteries could make electric vehicles

cost competitive by 2020

U.S. NEW PLUG-IN VEHICLE SALES

Thousands

0

5

10

15

20

25

2011 2012 2013 2014 2015 20160

50

100

150

200

250

300

350

400

450

500

$0

$200

$400

$600

$800

$1,000

$1,200

2008 2009 2010 2011 2012 2013 2014 2015

Battery Cost

Energy Density

PHEV* BATTERY ENERGY COST AND DENSITY

$USD/kwh & Wh/L

Source: BBVA Research & Electric Drive Transportation Association *PHEV = Plug-in hybrid electric vehicle

Source: BBVA Research & U.S. Department of Energy, International Energy Agency

17

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 FORECASTS

18

OIL PRICE FORECASTS

Slight upward revisions to 2017 and 2018 figures

Source: BBVA Research & Haver Analytics

CRUDE OIL PRICE FORECASTS

Brent, $ per barrel, avg

CRUDE OIL PRICE FORECASTS

Brent, $ per barrel, avg

Baseline Upside Downside

2015 52.8 52.8 52.8

2016 45.2 45.2 45.2

2017 57.0 66.9 46.2

2018 58.7 75.8 36.6

2019 59.6 79.3 34.1 0

20

40

60

80

100

120

2014 2015 2016 2017 2018 2019

Actual Baseline

Upside Risk Downside Risk

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 FORECASTS

19

EXCHANGE RATE

Prices are expected to move above our previous baseline, but

increases could be limited by a strong dollar

Source: BBVA Research & Haver Analytics

OIL PRICES AND U.S. DOLLAR

20

25

30

35

40

45

50

55

60

112

114

116

118

120

122

124

126

128

130

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17

Trade-Weighted Exchange Rate, $ (Jan-97=100) Brent ($/bbl, rhs)

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 FORECASTS

20

SUPPLY

More than half of liquids from new supply sources are expected to be

commercial below $60/bbl

Source: Rystad Energy UCube

GLOBAL LIQUIDS PRODUCTION BY LIFE CYCLE AND BREAKEVEN PRICE

Million barrels per day

50

60

70

80

90

100

110

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Undiscovered

Above 125

100-125

80-100

60-80

40-60

20-40

Below 20

Under development

Producing

No

n s

an

ctio

ne

d p

roje

cts

Forecasts

U.S. OIL PRICE OUTLOOK │ FEBRUARY 2017 FORECASTS

21

SUPPLY

$60/bbl would make several projects profitable again, but high-cost

producers would still be out of the market

Source: Rystad Energy UCube

COST OF SUPPLY CURVE

0

20

40

60

80

100

120

140

160

420 520 620 720 820 920 1,020 1,120 1,220

Bre

akev

en

Oil P

rice,

US

D/b

arr

el

Remaining resources as of 2016, Million bbl

Producing Onshore Middle East Extra heavy oil

Shelf North American Shale Ultra deepwater

Row onshore Russia onshore Deepwater

Oil sands Weighted average breakeven

OIL PRICE

OUTLOOK

US

FEBRUARY 2017