Page 1

© 2020. All rights reserved. IQVIA® is a registered trademark of IQVIA Inc. in the United States, the European Union, and various other countries.

Presented by:

Doug Long, VP, Industry Relations

Scott Biggs, Director, Supplier Services

August 2021

US Pharmaceutical Trends, Issues

and Outlook for NACDS TSE

Page 2

IQVIA Template (V2.1.0)

1

Each year at the NACDS Total Store Expo, IQVIA recognizes an industry leader who exemplifies the true meaning

of partnership through the extension of the Bernie Greenberg Pharmacy Partnership Award. Like the

namesake of this award, this recognition is to acknowledge an industry partner who displays and embraces such

traits as leadership, collaboration, and giving back to their organizations and others

This year, rather than awarding this to an

individual or a single industry partner,

IQVIA would like to honor ALL of the

pharmacy leaders, pharmacists, staff, and

pharmacies who have focused on caring

for their patients and customers during

the 2020 and 2021 COVID-19 crisis. You

and they ARE the heroes. As part of this

recognition, IQVIA provides a $10,000

contribution to the NACDS foundation

2013 Rite Aid Robert Thompson

2014 Walgreens Gerry Gleeson

2015 Walmart, Sam’s ClubDarren Townzen

John Luebker

2016 Kroger Phelicia Avery

2017 Walgreens Rick Gates

2018 Albertsons Dan Salemi

2019 WegmansJohn Carlo

Jack Coultry

2020 All pharmacists, staff and pharmacies

2021All pharmacy leaders, pharmacists, staff and

pharmacies

Year Company Winner(s)

IQVIA© 2021 Confidential & Proprietary

Page 3

2

COVID Cases, Deaths

and Vaccines

IQVIA – Confidential & Proprietary

Page 4

3

Daily COVID Cases in the U.S. continue to increase in recent weeks

IQVIA© 2021 Confidential & Proprietary

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1/2

3/2

0

2/6

/20

2/2

0/2

0

3/5

/20

3/1

9/2

0

4/2

/20

4/1

6/2

0

4/3

0/2

0

5/1

4/2

0

5/2

8/2

0

6/1

1/2

0

6/2

5/2

0

7/9

/20

7/2

3/2

0

8/6

/20

8/2

0/2

0

9/3

/20

9/1

7/2

0

10

/1/2

0

10

/15

/20

10

/29

/20

11

/12

/20

11

/26

/20

12

/10

/20

12

/24

/20

1/7

/21

1/2

1/2

1

2/4

/21

2/1

8/2

1

3/4

/21

3/1

8/2

1

4/1

/21

4/1

5/2

1

4/2

9/2

1

5/1

3/2

1

5/2

7/2

1

6/1

0/2

1

6/2

4/2

1

7/8

/21

7/2

2/2

1

8/5

/21

U.S. COVID Daily Cases

New Cases 7-Day Moving Avg

Source: https://covid.cdc.gov/covid-data-tracker/#trends_dailytrendscases – data as of August 18, 2021

Page 5

4

Daily COVID Deaths in the U.S. have also been increasing in recent weeks

IQVIA© 2021 Confidential & Proprietary

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1/2

2/2

020

2/5

/202

0

2/1

9/2

020

3/4

/202

0

3/1

8/2

020

4/1

/202

0

4/1

5/2

020

4/2

9/2

020

5/1

3/2

020

5/2

7/2

020

6/1

0/2

020

6/2

4/2

020

7/8

/202

0

7/2

2/2

020

8/5

/202

0

8/1

9/2

020

9/2

/202

0

9/1

6/2

020

9/3

0/2

020

10

/14

/202

0

10

/28

/202

0

11

/11

/202

0

11

/25

/202

0

12

/9/2

020

12

/23

/202

0

1/6

/202

1

1/2

0/2

021

2/3

/202

1

2/1

7/2

021

3/3

/202

1

3/1

7/2

021

3/3

1/2

021

4/1

4/2

021

4/2

8/2

021

5/1

2/2

021

5/2

6/2

021

6/9

/202

1

6/2

3/2

021

7/7

/202

1

7/2

1/2

021

8/4

/202

1

U.S. COVID Daily Deaths

Daily Deaths 7-Day Moving Avg

Source: https://covid.cdc.gov/covid-data-tracker/#trends_dailytrendscases – data as of August 18, 2021

Page 6

5

Daily Count of Total Doses Administered and Reported

IQVIA© 2021 Confidential & Proprietary

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

12

/14

/202

0

12

/21

/202

0

12

/28

/202

0

1/4

/202

1

1/1

1/2

021

1/1

8/2

021

1/2

5/2

021

2/1

/202

1

2/8

/202

1

2/1

5/2

021

2/2

2/2

021

3/1

/202

1

3/8

/202

1

3/1

5/2

021

3/2

2/2

021

3/2

9/2

021

4/5

/202

1

4/1

2/2

021

4/1

9/2

021

4/2

6/2

021

5/3

/202

1

5/1

0/2

021

5/1

7/2

021

5/2

4/2

021

5/3

1/2

021

6/7

/202

1

6/1

4/2

021

6/2

1/2

021

6/2

8/2

021

7/5

/202

1

7/1

2/2

021

7/1

9/2

021

7/2

6/2

021

8/2

/202

1

8/9

/202

1

Daily Count of Total Doses Administered and Reported to CDC by Date Administered, United States

Total Doses Administered Daily 7-Day Avg Total Doses Daily

Data Source: https://covid.cdc.gov/covid-data-tracker/#vaccination-trends – as of August 14, 2021

Page 7

6

COVID Vaccines in Retail show an uptick starting mid-July

IQVIA© 2021 Confidential & Proprietary

0

1

2

3

4

5

6

7

8

12

/18

/20

12

/25

/20

01

/01

/21

01

/08

/21

01

/15

/21

01

/22

/21

01

/29

/21

02

/05

/21

02

/12

/21

02

/19

/21

02

/26

/21

03

/05

/21

03

/12

/21

03

/19

/21

03

/26

/21

04

/02

/21

04

/09

/21

04

/16

/21

04

/23

/21

04

/30

/21

05

/07

/21

05

/14

/21

05

/21

/21

05

/28

/21

06

/04

/21

06

/11

/21

06

/18

/21

06

/25

/21

07

/02

/21

07

/09

/21

07

/16

/21

07

/23

/21

07

/30

/21

08

/06

/21

08

/13

/21

Mill

ion

s

Chain Independents Food Mass Retail Market

Data Source: IQVIA Xponent®

Page 8

7

As of August 15th, almost 51% of the entire population is vaccinated, with over 80% of the 65+ age group vaccinated

Source: https://covid.cdc.gov/covid-data-tracker/#vaccinations – Based on CDC data as of August 15th

19

8.1

16

8.4

59.7%

50.7%

0%

10%

20%

30%

40%

50%

60%

70%

20

40

60

80

100

120

140

160

180

200

At le

ast 1

Dose

Fully

Vaccin

ate

d

Perc

en

t of P

op

ula

tion

Pop

ula

tion

in M

illio

ns

VACCINES ADMINISTERED

18

5.9

15

9.2

72.0%

61.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

20

40

60

80

100

120

140

160

180

200

At le

ast 1

Dose

Fully

Vaccin

ate

d

Perc

en

t of P

op

ula

tion

Pop

ula

tion

in M

illio

ns

VACCINES ADMINISTERED

≥ 18

49.7 44.2

90.9%

80.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

40

60

80

100

120

140

160

180

200

At le

ast 1

Dose

Fully

Vaccin

ate

d

Perc

en

t of P

op

ula

tion

Pop

ula

tion

in M

illio

ns

VACCINES ADMINISTERED

≥ 651

97

.9

16

3.2

69.8%

59.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

20

40

60

80

100

120

140

160

180

200

At le

ast 1

Dose

Fully

Vaccin

ate

d

Perc

en

t of P

op

ula

tion

Pop

ula

tion

in M

illio

ns

VACCINES ADMINISTERED

≥ 12

IQVIA© 2021 Confidential & Proprietary

Page 9

8

According to a Kaiser Family Foundation Poll conducted May 18-25, 2021:

Vaccine Hesitancy – Who are the unvaccinated?

Here Are The Biggest Groups That Are Still Refusing The Covid-19 Vaccine, Poll Finds (forbes.com) retrieved on August 10, 2021

AGE

The highest share of

unvaccinated respondents were

30-49 years old (41%), followed

by 29% ages 18-29 and 20%

ages 50-64, while only 9% of

those unvaccinated were

65 and older

SOCIOECONOMIC

STATUS

More likely to have lower

education levels (46% attended

only high school or less) and

lower income levels (42% earn

less than $40,000 per year) than

their vaccinated counterparts,

who are nearly twice as likely to

have earned a college degree

or more

POLITICAL PARTY

AFFILIATION

Nearly half of unvaccinated

respondents were Republicans

(49% versus 29% Democrats),

as opposed to 31% of

vaccinated respondents who

identified as Republicans and

59% Democrats

RACIAL IDENTITY

Both unvaccinated and

vaccinated respondents were

disproportionately likely to be

white (56% unvaccinated versus

64% vaccinated), based in the

suburbs (56% unvaccinated

versus 52% vaccinated) and

have health insurance

(76% unvaccinated versus 88%

vaccinated).

IQVIA© 2021 Confidential & Proprietary

Page 10

9

Based on race/ethnicity data available for 57% of people who have received at least one vaccine dose

Figure 1: Race/Ethnicity of People Receiving a COVID-19 Vaccine in the U.S. as of August 2, 2021

KFF

Race/Ethnicity of People Receiving a COVID-19 Vaccine in the U.S. as of August 2, 2021

Note: Totals may not sum to 100 due to rounding, Persons of Hispanic origin may be of any race but are categorized as Hispanic; other groups are non-Hispanic, Other race includes multiple race individuals

Source: Centres for Disease Control and Prevention, Demographic Characteristics of People Receiving COVID-19 Vaccinations in the United States, data as of August 2, 2021, accessed August 3, 2021,

http://covid.cdc.gov/covid-data-tracker/#vaccination-demographic; Latest Data on COVID-19 Vaccinations by Race/Ethnicity | KFF Retrieved on August 10, 2021

59%

45%

61%

10%

15%

12%

16%26%

17%6% 4%

6%1% 1%1%8% 8% 2%

People who have Received at least One Dose People who Initiated Vaccination in Last 14 Days Total U.S. Population

White Black Hispanic Asian AIAN NHOPI Other

IQVIA© 2021 Confidential & Proprietary

Page 11

10

Percent of Total Population that Has Received at Least One COVID-19 Vaccine Dose by Race/Ethnicity, March 1 to August 2, 2021

Figure 4: Percent of Total Population that Has received at Least One COVID-19 vaccine Dose by Race/Ethnicity, March 1 to August 2, 2021

Source: Vaccination data based on KFF analysis of publicity available data on state websites; total population data used to calculate rates based on KFF analysis of 2019 American Community Survey data

7%

11%

15%

20%24%

27%29%

31% 33%34% 36%

38%

5%9%

13%

19%

25%

29%32%

35%38%

39% 41% 43%

13%

19%

25%32%

38%40%

43% 44%46% 47% 48%

49%

11%16%

23%

33%

45%

50%

54%57%

60%62%

65%66%

3/1/202136 States

3/15/202139 States

3/29/202140 States

4/12/202143 States

4/26/202143 States

5/10/202142 States

5/24/202140 States

6/7/202141 States

6/21/202140 States

7/6/202140 States

7/19/202140 States

8/2/202140 States

Black Hispanic White Asian

IQVIA© 2021 Confidential & Proprietary

Page 12

11

Non-COVID weekly vaccine utilization is flat compared to 2020 after a period of accelerated activity that compensated for lockdown dips

IQVIA© 2021 Confidential & Proprietary

Source: IQVIA Weekly Sales Perspectives (WSP), July 20 – July 21; Note: Data reflects sales to clinic channel as defined by IQVIA –

No methodology has been applied to determine VACCINE USE BY AGE

0

100

200

300

400

500

600

700

07

/20

08

/20

09

/20

10

/20

11

/20

12

/20

01

/21

02

/21

03

/21

04

/21

05

/21

06

/21

Thousands

Weeks

Weekly Volume Unit Clinic Sales for Selected Pediatric Vaccines*

-4%

-80%

-40%

0%

40%

80%

120%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Weeks

YoY Weekly Growth %Pediatric Vaccine Market Basket vs. Actual 2020

Weekly Growth Cumulative Growth

3%

-100%

-50%

0%

50%

100%

150%

200%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Weeks

YoY Weekly Growth %Adult Vaccine Market Basket vs. Actual 2020

Weekly Growth Cumulative Growth

0

50

100

150

200

250

300

07

/20

08

/20

09

/20

10

/20

11

/20

12

/20

01

/21

02

/21

03

/21

04

/21

05

/21

06

/21

Thousands

Weeks

Weekly Volume Unit Clinic Sales for Selected Adult Vaccines*

Page 13

12

Last season flu vaccinations at Retail were up 37% on a YoY basis, the new flu vaccination season is starting slower so far

IQVIA© 2021 Confidential & Proprietary

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7/2

/21

7/1

6/2

1

7/3

0/2

1

8/1

3/2

1

8/2

7/2

1

9/1

0/2

1

9/2

4/2

1

10

/8/2

1

10

/22

/21

11

/5/2

1

11

/19

/21

12

/3/2

1

12

/17

/21

12

/31

/21

1/1

4/2

2

1/2

8/2

2

2/1

1/2

2

2/2

5/2

2

3/1

1/2

2

3/2

5/2

2

Total Retail Flu Vaccinations - YoY Trend Comparisons

2019-20 Season 2020-21 Season 2021-22 Season

37.2

51.0

2019-20 Season 2020-21 Season

Flu Vaccines @ Retail – Prior 2 Seasons

Data Source: IQVIA Xponent®

Page 14

13

The Flu season in Australia can be an early indicator of our season in the US and current trends are showing a weak season

IQVIA© 2021 Confidential & Proprietary

71.5% of

Australians 18-65

have received a flu

vaccine, compared

to 71.8% at the

same time last

year

90.4% of

Australians 65+

have received a flu

vaccine, compared

to 90% at the

same time last

year

Data Source: https://info.flutracking.net/reports-2/australia-reports/Data Source: https://www.9news.com.au/national/influenza-vaccine-

warning-as-number-of-aussies-seeking-flu-shot-falls-by-almost-half-from-

2020/11e65b73-1283-4ef2-adaa-81bd67eb9ed5

Page 15

14

The FAN® report for all symptoms indicates more cases beginning in May in comparison to the the last two years

IQVIA© 2021 Confidential & Proprietary

0

5

10

15

20

25

30

35

40

45

8/1

5/2

0

8/2

9/2

0

9/1

2/2

0

9/2

6/2

0

10

/10

/20

10

/24

/20

11

/7/2

0

11

/21

/20

12

/5/2

0

12

/19

/20

1/2

/21

1/1

6/2

1

1/3

0/2

1

2/1

3/2

1

2/2

7/2

1

3/1

3/2

1

3/2

7/2

1

4/1

0/2

1

4/2

4/2

1

5/8

/21

5/2

2/2

1

6/5

/21

6/1

9/2

1

7/3

/21

7/1

7/2

1

7/3

1/2

1

Mill

ion

s

All Symptoms

2020-2021 2019-2020 2018-2019 3-Year Average

Data Source: IQVIA FAN® Report

Page 16

15

Across the different symptoms on the FAN® report, Cough, Earache, Nasal and Sore Throat are running ahead of seasonal norms

IQVIA© 2021 Confidential & Proprietary

05

10152025303540

8/1

5/2

0

10

/15

/20

12

/15

/20

2/1

5/2

1

4/1

5/2

1

6/1

5/2

1

Mill

ion

s

Cough

2020-2021

2019-2020

2018-2019

3-YearAverage

0

5

10

15

20

25

30

8/1

5/2

0

9/1

5/2

0

10

/15

/20

11

/15

/20

12

/15

/20

1/1

5/2

1

2/1

5/2

1

3/1

5/2

1

4/1

5/2

1

5/1

5/2

1

6/1

5/2

1

7/1

5/2

1

Mill

ion

s

Fever

0

2

4

6

8

10

8/1

5/2

0

9/1

5/2

0

10

/15

/20

11

/15

/20

12

/15

/20

1/1

5/2

1

2/1

5/2

1

3/1

5/2

1

4/1

5/2

1

5/1

5/2

1

6/1

5/2

1

7/1

5/2

1

Mill

ion

s

ILI

0

0.5

1

1.5

2

2.5

8/1

5/2

0

9/1

5/2

0

10

/15

/20

11

/15

/20

12

/15

/20

1/1

5/2

1

2/1

5/2

1

3/1

5/2

1

4/1

5/2

1

5/1

5/2

1

6/1

5/2

1

7/1

5/2

1

Mill

ion

s

Earache

0

5

10

15

20

25

30

8/1

5/2

0

9/1

5/2

0

10

/15

/20

11

/15

/20

12

/15

/20

1/1

5/2

1

2/1

5/2

1

3/1

5/2

1

4/1

5/2

1

5/1

5/2

1

6/1

5/2

1

7/1

5/2

1

Mill

ion

s

Nasal

0

5

10

15

20

25

8/1

5/2

0

9/1

5/2

0

10

/15

/20

11

/15

/20

12

/15

/20

1/1

5/2

1

2/1

5/2

1

3/1

5/2

1

4/1

5/2

1

5/1

5/2

1

6/1

5/2

1

7/1

5/2

1

Mill

ion

s

Sore Throat

2020-2021 2019-2020 2018-2019 3-Year AverageData Source: IQVIA FAN® Report

Page 17

16

0

1

2

3

4

5

6

7

8

9

8/1

5/2

0

8/2

9/2

0

9/1

2/2

0

9/2

6/2

0

10

/10

/20

10

/24

/20

11

/7/2

0

11

/21

/20

12

/5/2

0

12

/19

/20

1/2

/21

1/1

6/2

1

1/3

0/2

1

2/1

3/2

1

2/2

7/2

1

3/1

3/2

1

3/2

7/2

1

4/1

0/2

1

4/2

4/2

1

5/8

/21

5/2

2/2

1

6/5

/21

6/1

9/2

1

7/3

/21

7/1

7/2

1

7/3

1/2

1

Mill

ion

s

Influenza Like Illness (ILI)

2020-2021 2019-2020 2018-2019 3-Year Average

A focus on ILI from the FAN® report shows that instances of flu continue to remain very low as we wrap up the season

IQVIA© 2021 Confidential & Proprietary

Data Source: IQVIA FAN® Report

Page 18

17

Market Trends:

UtilizationMedical claims/activity

Page 19

18

Telemedicine contribution to weekly medical claims growth continues to diminish, reaching 7.8% of total claims

IQVIA© 2021 Confidential & Proprietary

Data for latest week date controlled against prior periods; estimates have been applied to reflect anticipated late-adjudicated claims based on historical rates

Source: IQVIA: Medical Claims Data Analysis, 2021; Week 30 2019 = 8/2/2019; Week 30 2020 = 7/31/2020; Week 29 2020 = 7/24/2020; Week 29 2021 = 7/23/2021

Estimated amounts for latest weeks applied based on likely claims still to be received due to data latency or claim processing delays; See Appendix for further details

0M

5M

10M

15M

20M

25M

30M

35M

40M

45M

50M

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Week

Total Claims by Service Type: 52 weeks through W/E 07/23

INSTITUTIONAL OFFICE TELEMEDICINE

• From 5/7/2021 through 7/23/2021,

total claims volume is decreasing

nearly 2% per week

• Institutional claims have dropped the

most significantly, losing more than

3% per week over the same time

period, with telemedicine not far

behind at 3%

Potential Implications

Cla

ims V

olu

me

-2%

Page 20

19

Weekly institutional claims continue to stay below LY. Recent weekly growth in office doesn’t yet translate to cumulative growth

IQVIA© 2021 Confidential & Proprietary

-19%-20%

-18%

-18%

-18%

5%

-32%

-14%-14%

-13%-14%

-15%

-15%

-15%

-18%

-17%

-19%-19%

-19%-21%

-24%

0%

-23%

-22%

-19%-17%

-19%

-21%-19%

-32%

-11%-11%

6%3%6%1%2%

12%9%

7%7%5%8%

29%

-13%

9%9%8%

26%

-9%

9%13%

-40%

-20%

0%

20%

40%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Ye

ar

ove

r Y

ea

r %

Week

Year over Year Growth* – Office Claims Across Time Aligned Weeks

Weekly Growth % Cumulative Growth %

-24%

-6%

-11%

-10%

-11%

4%

-20%-10%

-10%-9%

-10%

-10%

-10%-21%

-4%-9%

-11%

-11%-7%

-12%-13%

-7%

-19%

-11%-10%

-8%

-10%

-9%

-10%-18%

-4%-5%

2%0%2%

7%

1%5%4%

-11%

8%

0%2%

10%

-6%-1%

-1%

-2%

-11%

-32%-30%

-29%-40%

-30%

-20%

-10%

0%

10%

20%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Ye

ar

ove

r Y

ea

r %

Week

Year over Year Growth* – Institutional Claims Across Time Aligned Weeks

Weekly Growth % Cumulative Growth %

Source: IQVIA: Medical Claims Data Analysis, 2021; Week 30 2019 = 8/2/2019; Week 30 2020 = 7/31/2020; Week 29 2020 = 7/24/2020; Week 29 2021 = 7/23/2021

Estimated amounts for latest weeks applied based on likely claims still to be received due to data latency or claim processing delays; See Appendix for further details

*Week 10-25 continue to be evaluated against a “Calibrated” 2020 both for weekly and cumulative growth calculations

Data for latest week date controlled against prior periods; estimates have been applied to reflect anticipated late-adjudicated claims based on historical rates

Page 21

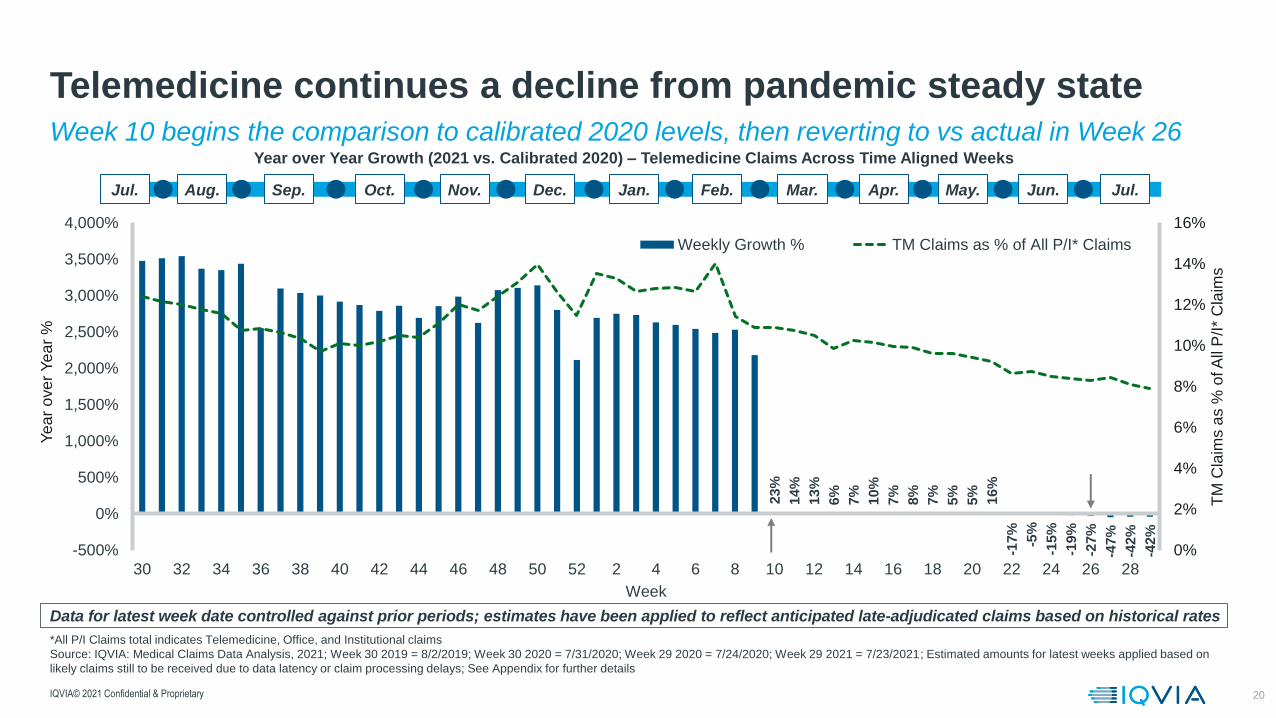

20

23

%

14

%

13

%

6%

7%

10

%

7%

8%

7%

5%

5%

16

%

-17

%

-5%

-15

%

-19

%

-27

%

-47

%

-42

%

-42

%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-500%

0%

500%

1,000%

1,500%

2,000%

2,500%

3,000%

3,500%

4,000%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

TM

Cla

ims a

s %

of A

ll P

/I*

Cla

ims

Ye

ar

ove

r Y

ea

r %

Week

Weekly Growth % TM Claims as % of All P/I* Claims

Week 10 begins the comparison to calibrated 2020 levels, then reverting to vs actual in Week 26

Telemedicine continues a decline from pandemic steady state

IQVIA© 2021 Confidential & Proprietary

Year over Year Growth (2021 vs. Calibrated 2020) – Telemedicine Claims Across Time Aligned Weeks

Data for latest week date controlled against prior periods; estimates have been applied to reflect anticipated late-adjudicated claims based on historical rates

*All P/I Claims total indicates Telemedicine, Office, and Institutional claims

Source: IQVIA: Medical Claims Data Analysis, 2021; Week 30 2019 = 8/2/2019; Week 30 2020 = 7/31/2020; Week 29 2020 = 7/24/2020; Week 29 2021 = 7/23/2021; Estimated amounts for latest weeks applied based on

likely claims still to be received due to data latency or claim processing delays; See Appendix for further details

Feb.Jul. Aug. Sep. Oct. Nov. Dec. Jan. Mar. Apr. May. Jun. Jul.

Page 22

21

Elective Procedures: Weekly YoY and cumulative growth

IQVIA© 2021 Confidential & Proprietary

Source: IQVIA: Medical Claims Data Analysis, 2021; Week 30 2019 = 8/2/2019; Week 30 2020 = 7/31/2020; Week 29 2020 = 7/24/2020; Week 29 2021 = 7/23/2021; Elective procedures based on IQVIA custom analysis;

Data includes claims from inpatient and outpatient sites of care; Latest two weeks are estimates using a recency data factor that is adjusted out as all claims are received; See Appendix for further details

Week 10-25 continue to be evaluated against a “Calibrated” 2020 both for weekly and cumulative growth calculations

-9%-10%

-9%

-8%

-7%

20%

-25%

-4%-5%

-3%-2%-2%-4%

-2%

-8%-7%

-9%-10%

-11%-12%

-14%

19%

0%

-20%

-13%-11%

-11%-12%

-9%

-20%

-6%-4%

6%

0%

4%

-3%-4%

8%8%7% 5%

2%5%

29%

-20%

2%1%

-2%

20%

-24%

-8%

-24%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

30 32 34 36 38 40 42 44 46 48 50 52 2 4 6 8 10 12 14 16 18 20 22 24 26 28

Ye

ar

ove

r Y

ea

r %

Week

Year over Year Growth – Elective Procedure Across Time Aligned Weeks

Weekly Growth % Cumulative Growth %

Feb.Jul. Aug. Sep. Oct. Nov. Dec. Jan. Mar. Apr. May. Jun. Jul.

Page 23

22

0M

20M

40M

60M

80M

100M

120M

140M

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

In 2020 there were almost 1 billion diagnosis visits that did not happen

IQVIA© 2021 Confidential & Proprietary

A leading indicator of long-term impact

-967M

-18.8%

Total Gap of Diagnosis

Visits in 2020 (Unique patient-provider diagnosis events)

-2000 -1500 -1000 -500 0

GASTRO

UROLOGY

NEURO

ONCOLOGY

PCP

RHEUM

ENDO

Leading Specialties in 2020 by Dx Visits Gap/HCP

Dx Visit/HCP Ratio

% of Expected

Diagnosis Visits

in 2020

What is the “diagnosis visit gap”?

Difference between diagnosis visits1 expected during a

hypothetical non-COVID scenario and the number of

diagnosis visits we actually see

IQVIA: Medical Claims Data Analysis, 2021, IQVIA Analysis1A diagnosis visit is for one single diagnosis per patient, per HCP; a patient can have more than one diagnosis visit assigned to them, with either more than one diagnosis per doctor or more than one doctor per diagnosis

Expected diagnosis visits in

2020 if there was no COVID-19

Actual diagnosis visits in 2020

The

Diagnosis

Visit Gap

Page 24

23

0M

20M

40M

60M

80M

100M

120M

Jan Feb Mar Apr May Jun

Non-COVID vs. COVID Diagnosis Visits 2021

Lower-than-expected total diagnosis visit volumes in May have created more separation than previously forecast; vaccine deployment and other triggers will continue to influence these dynamics

Post-COVID dynamics continue to have an impact – nearly 300M diagnosis visits have not occurred in the first half of 2021

IQVIA© 2021 Confidential & Proprietary

-270.2MTotal Forecast

Diagnosis Visit

Gap in 1H 2021

% of Expected

Diagnosis Visits

in 1H 2021 -10.8%Forecast diagnosis visits in

2021 if there was no COVID-19

Forecast diagnosis visits in

2021 with COVID

(actual data through 5/28/21)

Page 25

24

US Primary Intelligence

BrandImpact HCP Network = ~3,600 unique HCPs including Oncology, Specialty and Primary Care; Specialty includes, but not limited to, Allergy, Cardiology, Dermatology, Gastroenterology, Endocrinology, Neurology,

Pulmonology, Psychiatry, Rheumatology & Urology

Total Biopharma Patient Visits by Type

Total patient visits in July for Biopharma and Primary Care were lower than last year due to a decline in remote visits

Primary Care Patient Visits by Type

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Jul

Aug

Sep

Oct

No

v

De

c

Jan-2

1

Feb

Ma

r

Apr

Ma

y

Jun

Jul

In-Person Pt Visits Remote Pt Visits

80%

20%

88%

12%

0

10,000

20,000

30,000

40,000

50,000

60,000

Jul

Aug

Sep

Oct

No

v

De

c

Jan-2

1

Feb

Ma

r

Apr

Ma

y

Jun

Jul

In-Person Pt Visits Remote Pt Visits

88%

12%

81%

19%

IQVIA© 2021 Confidential & Proprietary

Page 26

25

0M

20M

40M

60M

80M

100M

120M

140M

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Ma

r

Apr

Ma

y

Jun

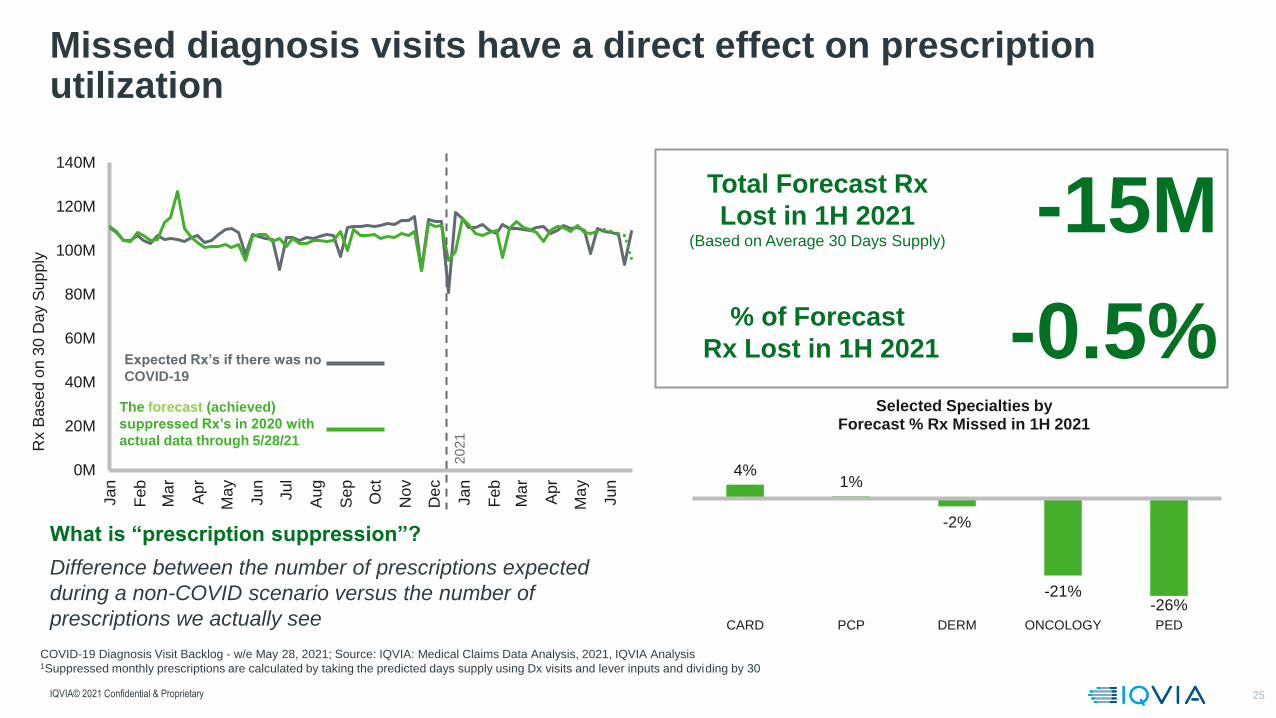

Missed diagnosis visits have a direct effect on prescription utilization

IQVIA© 2021 Confidential & Proprietary

-15M

-0.5%

Total Forecast Rx

Lost in 1H 2021 (Based on Average 30 Days Supply)

4%1%

-2%

-21%-26%

CARD PCP DERM ONCOLOGY PED

Selected Specialties by Forecast % Rx Missed in 1H 2021

% of Forecast

Rx Lost in 1H 2021

What is “prescription suppression”?

Difference between the number of prescriptions expected

during a non-COVID scenario versus the number of

prescriptions we actually see

COVID-19 Diagnosis Visit Backlog - w/e May 28, 2021; Source: IQVIA: Medical Claims Data Analysis, 2021, IQVIA Analysis1Suppressed monthly prescriptions are calculated by taking the predicted days supply using Dx visits and lever inputs and dividing by 30

Expected Rx’s if there was no

COVID-19

The forecast (achieved)

suppressed Rx’s in 2020 with

actual data through 5/28/21Rx B

ase

d o

n 3

0 D

ay S

up

ply

20

21

Page 27

26

Specialties with greater gaps in claims in 2020 are working to address the patient backlog – namely ophthalmologists and dermatologists

Hard hit specialists continue to fill the 2020 diagnosis gap

-7%

-9%

-12%

-12%

-13%

-16%

-17%

-17%

-19%

-20%

-20%

-20%

-20%

-21%

-29%

2020 % change from baseline

Source: IQVIA: National Prescription Audit; IQVIA: Medical Claims data. Note: Baseline defined as the average of the first full eight weeks of 2020. NBRx are Retail only. NBRx include all prescriptions a HCP writes, not only those specific to the therapy area.

-17%

59%

-15%

-19%

-14%

-7%

-12%

-20%

-18%

-26%

-22%

-16%

-12%

-22%

-54%PED

OPHTH

ALLER

PCP

PULM

GE

CARD

UROL

OB/GYN

NEURO

ENDO

RHEUM

ONC

PSYCH

DERM

Excluding flu vaccines

in 2020, ONC = -7%

Claims NBRx

IQVIA© 2021 Confidential & Proprietary

Fewer claims, fewer NBRx

More claims, more NBRxFewer claims, more NBRx

More claims, fewer NBRx

ALLER

PCP

OB/GYN

CARD DERM

ENDO

GE

NEURO

OPHTH

PED

PULM

PSYCH

RHEUM

UROL

ONC

ONC, no COVID vaccine NBRx

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-15% -10% -5% 0% 5% 10% 15% 20% 25%

% C

ha

nge

in

NB

Rx,

20

20

v.

20

21

% Change in claims, 2020 v. 2021

% Change in claims and NBRx, weeks 1–25, 2020 v. 2021

Page 28

27

Where Are We Now?

IQVIA – Confidential & Proprietary

Page 29

28

The Non-Retail channel is recovering from effects of COVID-19

Growth (%) of Sales

Total Market (Retail, Non-Retail and Mail) Retail and Mail

Source: IQVIA, National Sales Perspectives, Jun 2021

Note: Limited to Rx and OTC Insulins; Includes Retail, Non-Retail and Mail

Non-Retail

6.0%

10.6%

7.5%

1.8%

4.9%

6.1%

2017 2018 2019 2020 MATJun

2021

YTD Jun2021

1.9%

6.4%5.8%

4.3%

6.0%7.0%

2017 2018 2019 2020 MATJun

2021

YTDJun

2021

0.3%

4.6% 5.0% 5.4%6.5%

7.3%

2017 2018 2019 2020 MATJun

2021

YTDJun

2021

IQVIA© 2021 Confidential & Proprietary

Page 30

29

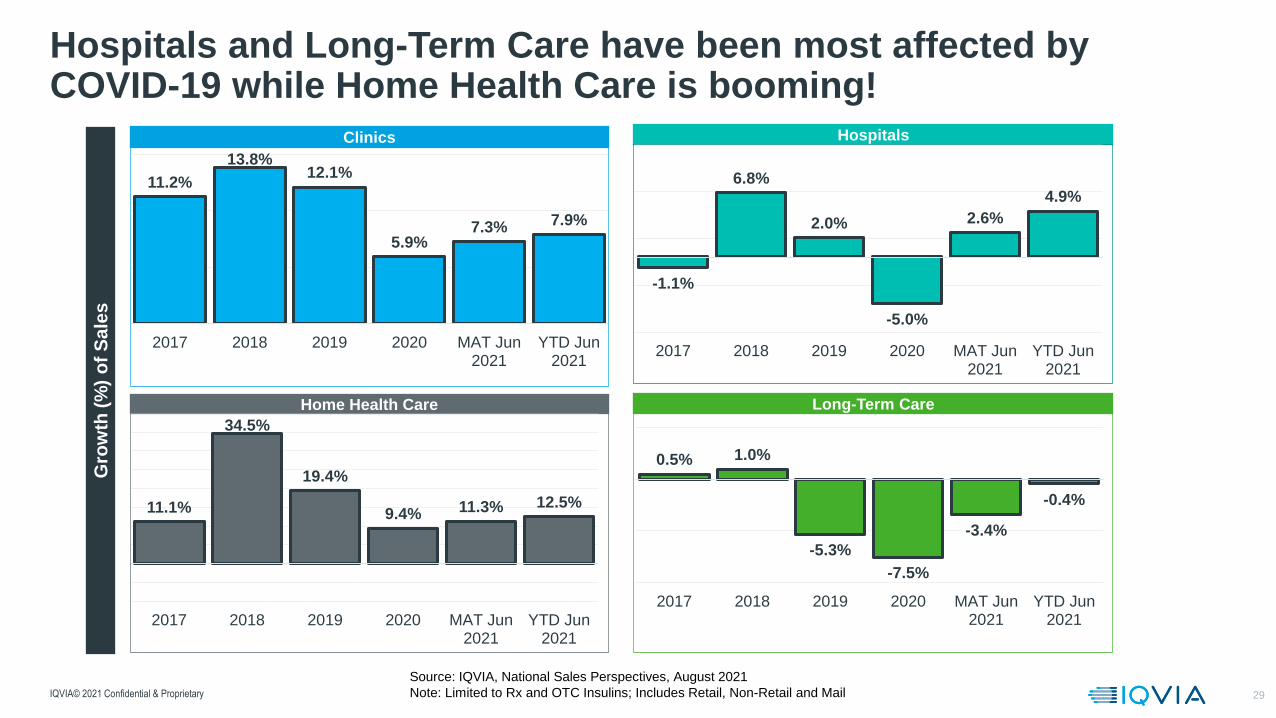

Hospitals and Long-Term Care have been most affected by COVID-19 while Home Health Care is booming!

Gro

wth

(%

) o

f S

ale

s

Clinics Hospitals

-1.1%

6.8%

2.0%

-5.0%

2.6%

4.9%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Source: IQVIA, National Sales Perspectives, August 2021

Note: Limited to Rx and OTC Insulins; Includes Retail, Non-Retail and Mail

11.2%

13.8%12.1%

5.9%7.3% 7.9%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Long-Term Care

0.5% 1.0%

-5.3%

-7.5%

-3.4%

-0.4%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Home Health Care

11.1%

34.5%

19.4%

9.4% 11.3% 12.5%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

IQVIA© 2021 Confidential & Proprietary

Page 31

30

In MAT June 2021,specialty spend grew by 6.9% while traditional growth grew 5.2%

For the total market, specialty growth is outpacing traditional growth and now has ~49% share of total non-discounted spend

$196.0$218.9

$243.8$261.9

$271.7

$259.0

$264.8$269.2

$275.1 $283.6$455.0

$483.7$513.0 $537.0 $555.3

-30%

0%

30%

$

$100

$200

$300

$400

$500

Gro

wth

N

on

-Dis

co

un

ted

Sp

en

d (

BN

s)

SPECIALTY TRADITIONAL SPECIALTY GROWTH TRADITIONAL GROWTH TOTAL MARKET GROWTH

Source: IQVIA, National Sales Perspectives, June 2021

Share of Sales 2017 2018 2019 2020 MAT JUN 2021

SPECIALTY 43.1% 45.3% 47.5% 48.8% 48.9%

TRADITIONAL 56.9% 54.7% 52.5% 51.2% 51.1%

IQVIA© 2021 Confidential & Proprietary

Page 32

31

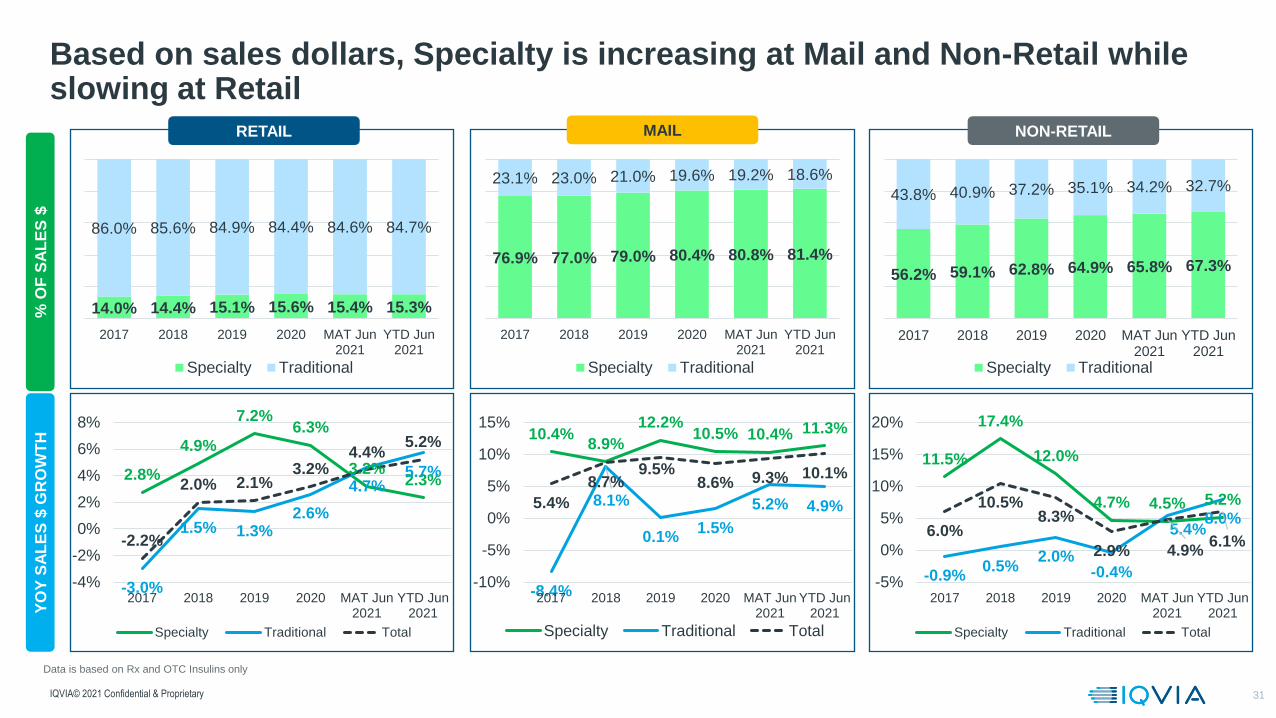

Based on sales dollars, Specialty is increasing at Mail and Non-Retail while slowing at Retail

56.2% 59.1% 62.8% 64.9% 65.8% 67.3%

43.8% 40.9% 37.2% 35.1% 34.2% 32.7%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional

NON-RETAIL

% O

F S

AL

ES

$

14.0% 14.4% 15.1% 15.6% 15.4% 15.3%

86.0% 85.6% 84.9% 84.4% 84.6% 84.7%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional

RETAIL

76.9% 77.0% 79.0% 80.4% 80.8% 81.4%

23.1% 23.0% 21.0% 19.6% 19.2% 18.6%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional

MAIL

11.5%

17.4%

12.0%

4.7% 4.5% 5.2%

-0.9%0.5%

2.0%-0.4%

5.4%8.0%

6.0%

10.5%8.3%

2.9% 4.9%6.1%

-5%

0%

5%

10%

15%

20%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional Total

2.8%

4.9%

7.2%6.3%

3.2%2.3%

-3.0%

1.5% 1.3%2.6%

4.7%5.7%

-2.2%

2.0% 2.1%3.2%

4.4%5.2%

-4%

-2%

0%

2%

4%

6%

8%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional Total

10.4%8.9%

12.2%10.5% 10.4% 11.3%

-8.4%

8.1%

0.1%1.5%

5.2% 4.9%5.4%

8.7%9.5%

8.6% 9.3% 10.1%

-10%

-5%

0%

5%

10%

15%

2017 2018 2019 2020 MAT Jun2021

YTD Jun2021

Specialty Traditional Total

YO

Y S

AL

ES

$ G

RO

WT

H

Data is based on Rx and OTC Insulins only

IQVIA© 2021 Confidential & Proprietary

Page 33

32

Immunology showed greatest Specialty growth on spend in Mail

RETAIL

Therapy MAT June

2021

YoY

Growth

HIV ANTIVIRALS 16.4 1.5%

IMMUNOLOGY 7.7 9.5%

ONCOLOGICS 2.3 -3.0%

MENTAL HEALTH 2.2 6.6%

ANTI-INFLAMMATORY AND

DIGESTIVE ENZYMES AND

MODULA2.0 11.3%

VIRAL HEPATITIS 1.2 -16.3%

LIPID REGULATORS 1.0 35.9%

MULTIPLE SCLEROSIS 0.7 -10.5%

SEX HORMONES (ANDROGENS, OESTROGENS,

PROGESTOGENS)

0.6 21.3%

IMMUNOSUPPRESSANTS 0.5 -6.3%

MAIL

Therapy MAT June

2021

YoY Growth

IMMUNOLOGY 61.0 20.3%

ONCOLOGICS 20.2 9.1%

MULTIPLE SCLEROSIS 11.3 -10.2%

HIV ANTIVIRALS 5.1 -0.6%

ALL OTHER

RESPIRATORY3.8 21.6%

OTHER

CARDIOVASCULARS2.3 13.1%

GROWTH HORMONES 2.2 0.2%

RESPIRATORY AGENTS 2.2 13.4%

VIRAL HEPATITIS 2.1 -20.9%

BLOOD COAGULATION 1.9 0.5%

NON-RETAIL

Therapy MAT June

2021

YoY

Growth

ONCOLOGICS 52.8 7.0%

IMMUNOLOGY 15.6 9.9%

MULTIPLE SCLEROSIS 5.2 4.0%

POLYVAL

IMMUNOGLOBLULINS IV&IM4.6 5.6%

HIV ANTIVIRALS 4.5 2.0%

HEMATOPOIETIC GROWTH

FACTORS3.8 -11.6%

ERYTHROPOIETINS 2.7 -9.6%

MENTAL HEALTH 2.1 9.3%

OCULAR ANTINEOVASCULARISATION

1.9 -9.5%

RESPIRATORY AGENTS 1.9 14.2%

Top 10 Specialty Therapies for Retail, Mail, and Non-Retail - MAT June 2021 (in $ billions)

Source: IQVIA, National Sales Perspectives, June 2021

Limited to Rx and OTC Insulins

*For Client’s internal use only

IQVIA© 2021 Confidential & Proprietary

Page 34

33

33

Slowing growth was occurring prior to COVID-19, and is not the sole contributor

All therapies demonstrate short-term growth except MS; Immunology and Anticoagulants show the greatest one- and five-year growth

Top-10 therapy area growth % ($)

-10%

-5%

0%

5%

10%

15%

20%

25%

-4% -2% 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 22%

RESPIRATORY AGENTS

IMMUNOLOGY

ONCOLOGICS

MENTAL HEALTH

Historic growth (% 5-year CAGR, 2016-2021)

Sh

ort

-te

rm g

row

th (

% Y

oY

,20

20

-20

21

)

ANTIDIABETICS

ANTICOAGULANTS

HIV ANTIVIRALS

MULTIPLE SCLEROSIS

PAIN VACCINES (PURE, COMB, OTHER)

Specialty Traditional Jun 2021 MAT sales, Bn

IQVIA National Sales Perspectives, June 2021, Rx’s and OTC Insulins Only

IQVIA© 2021 Confidential & Proprietary

Page 35

IQVIA Template (V2.1.0)

34

Antidiabetics is the top therapy class and Eliquis is a top product in the Retail Market based on sales dollars

Therapies

Rank Therapy

MAT

June

2021

YoY Growth

1 ANTIDIABETICS 64.0 13.9%

2 RESPIRATORY AGENTS 21.6 -0.1%

3 ANTICOAGULANTS 18.1 16.2%

4 HIV ANTIVIRALS 16.4 1.5%

5 MENTAL HEALTH 13.3 6.4%

6 PAIN 10.2 8.1%

7 ADHD 8.1 0.1%

8 IMMUNOLOGY 7.7 9.6%

9 GI PRODUCTS 6.8 5.1%

10 NERVOUS SYSTEM DISORDERS 6.5 -6.1%

Products

Rank Product

MAT

June

2021

YoY Growth

1 ELIQUIS 10.9 25.5%

2 TRULICITY 8.5 37.2%

3 OZEMPIC 5.6 70.9%

4 JARDIANCE 5.6 40.7%

5 XARELTO 5.4 9.1%

6 BIKTARVY 5.2 27.6%

7 JANUVIA 5.0 3.8%

8 LANTUS SOLOSTAR 4.0 17.2%

9 VYVANSE 3.7 2.8%

10 LATUDA 3.3 11.4%

Top 10 Therapies and Products for Retail based on Sales - MAT June 2021 (MAT in Billions)

Source: IQVIA, National Sales Perspectives, June 2021

Limited to Rx and OTC Insulins

IQVIA© 2021 Confidential & Proprietary

Page 36

IQVIA Template (V2.1.0)

35

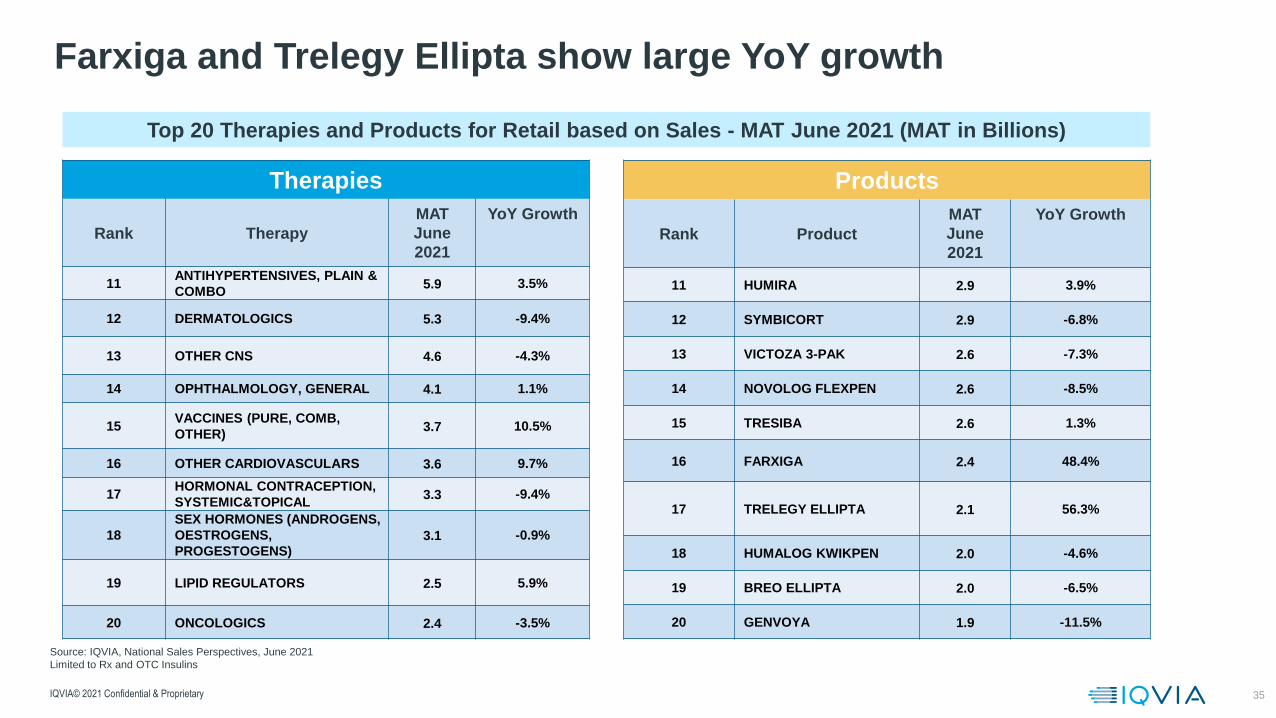

Farxiga and Trelegy Ellipta show large YoY growth

Therapies

Rank Therapy

MAT

June

2021

YoY Growth

11ANTIHYPERTENSIVES, PLAIN &

COMBO5.9 3.5%

12 DERMATOLOGICS 5.3 -9.4%

13 OTHER CNS 4.6 -4.3%

14 OPHTHALMOLOGY, GENERAL 4.1 1.1%

15VACCINES (PURE, COMB,

OTHER)3.7 10.5%

16 OTHER CARDIOVASCULARS 3.6 9.7%

17HORMONAL CONTRACEPTION,

SYSTEMIC&TOPICAL3.3 -9.4%

18

SEX HORMONES (ANDROGENS,

OESTROGENS,

PROGESTOGENS)3.1 -0.9%

19 LIPID REGULATORS 2.5 5.9%

20 ONCOLOGICS 2.4 -3.5%

Products

Rank Product

MAT

June

2021

YoY Growth

11 HUMIRA 2.9 3.9%

12 SYMBICORT 2.9 -6.8%

13 VICTOZA 3-PAK 2.6 -7.3%

14 NOVOLOG FLEXPEN 2.6 -8.5%

15 TRESIBA 2.6 1.3%

16 FARXIGA 2.4 48.4%

17 TRELEGY ELLIPTA 2.1 56.3%

18 HUMALOG KWIKPEN 2.0 -4.6%

19 BREO ELLIPTA 2.0 -6.5%

20 GENVOYA 1.9 -11.5%

Top 20 Therapies and Products for Retail based on Sales - MAT June 2021 (MAT in Billions)

Source: IQVIA, National Sales Perspectives, June 2021

Limited to Rx and OTC Insulins

IQVIA© 2021 Confidential & Proprietary

Page 37

Brand Inflation has slowed in recent years, currently it is running between 4 and 5% according to Nephron Research

Source: Nephron Research, IQVIA, Glass Box Analytics

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Dec

-13

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

Dec

-14

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

Dec

-15

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

Dec

-16

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

Dec

-17

Feb

-18

Ap

r-1

8

Jun

-18

Au

g-1

8

Oct

-18

Dec

-18

Feb

-19

Ap

r-1

9

Jun

-19

Au

g-1

9

Oct

-19

Dec

-19

Feb

-20

Ap

r-2

0

Jun

-20

Au

g-2

0

Oct

-20

Dec

-20

Feb

-21

Sale

s-W

eigh

ted

In

flat

ion

Hillary Clinton tweets onegregious

drug pricingValeant is

subpoeaned over pricing

actionsAllergan issues its Social Contract and pledges to

take single digit gross increases

Trump tweets that drug makers are "getting away with murder"

Leaked presidential draft proves to be pharma friendly

Manufacturers limited themselves to a single

price increase

January price increases

HHS introduces rebate/discount

rule for 1/1/20

HHS withdraws

Rebate Rule

2H18 price increases rescinded

Pelosi unveils drug plan

+4% to +5% is the new

normal

Trump EO Released

Page 38

37

311.0

359.0

61.9

8.4 51.6

3.9-78.1

200.0

250.0

300.0

350.0

400.0

450.0

2015 New brands Protected brandsprice

Protected brandsvolume

LOE Generics 2020

Manufacturer net revenue Growth Declines

Net Manufacturer Revenues and Growth 2015–2020, All Channels, US$Bn

Manufacturer net revenues increased by $48 billion over the pastfive years primarily driven by new products and protected brand volume

Source: IQVIA Institute, May 2021

-13.7-18.6

-25

-20

-15

-10

-5

0

5

10

15

20

2016 2017 2018 2019 2020

13.2

13.9

-25

-20

-15

-10

-5

0

5

10

15

20

7.0

-9.5-25

-20

-15

-10

-5

0

5

10

15

20

2016 2017 2018 2019 2020

4.5

18.7

-25

-20

-15

-10

-5

0

5

10

15

20

2016 2017 2018 2019 2020

1.3-0.8

-25

-20

-15

-10

-5

0

5

10

15

20

2016 2017 2018 2019 2020

2016 2020

IQVIA© 2021 Confidential & Proprietary

Page 39

38

Wholesaler Acquisition Cost (WAC) Growth and Net Price Growth for Protected Brands

Protected brand list prices increased 4.4% in 2020, while netprices decreased -2.9% - the fourth year at or below the CPI

IQVIA© 2021 Confidential & Proprietary

Source: IQVIA Institute, National Sales Perspectives, Dec 2020; Bureau of Labor Statistics, CPI Data, Dec 2015–Dec 2020

7.9%

9.3%

7.0%6.6%

5.2%4.4%

1.6%

2.9%

2.1% 0.3%1.7%

-2.9%

0.7%2.1%

2.1% 1.9%2.3%

1.3%

-4%

-2%

0%

2%

4%

6%

8%

10%

2015 2016 2017 2018 2019 2020

Brands WAC price growth % Estimated net price growth % CPI

Page 40

39

Unadjusted Rx growth for MAT May is negative and YTD May is positive, but adjusted growth is higher, at 2.5% for MAT May and 3.6% year to date

Growth (%) of Dispensed Rx

Unadjusted Rx Adjusted Rx

-5.6%

-0.6% -0.4%

-2.4%

0.3%

2.7%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

2017* 2018 2019 2020 MATJun

2021

YTDJun

2021

-3.8%

2.7% 2.4% 1.9%2.7%

4.2%

-7.0%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

2017* 2018 2019 2020 MATJun

2021

YTDJun

2021

Source: IQVIA, National Prescription Audit & RxInsight, May 2021; Retail, Mail, and LTC limited to Rx and OTC Insulins

*Note: Declines between 2016 and 2017 are due to VRAF enhancement from 2017 onwards

Gro

wth

(%

)

Gro

wth

(%

)

IQVIA© 2021 Confidential & Proprietary

Page 41

40

Unadjusted growth trends have been positive for the last several weeks, mainly being driven by COVID vaccinations at Retail

Data Source: IQVIA Xponent - Copyright 2021

-1.2

%

-3.7

%

8.4

%

-9.2

%

1.2

%

0.1

%

-0.9

%

-1.6

%

-1.7

%

-1.9

%

-2.7

%

-5.1

%

-3.0

%

-4.4

%

-4.5

%

-6.3

%

-4.9

%

-7.6

%

-1.5

%

-6.3

%

-4.1

%

-3.0

%

-2.8

%

-4.0

%

-5.4

%

-3.8

%

-12

.4%

-1.0

%

-2.7

0%

-5.3

%

-11

.6%

4.2

%

11

.4%

15

.0%

17

.9%

19

.1%

18

.4%

17

.1%

14

.5%

13

.9%

22

.1%

2.3

%

10

.6%

9.4

%

8.3

%

7.5

%

3.0

%

7.0

%

8.7

%

7.6

%

8.9

%

7.9

%

-50%

0%

50%

8/2

1/2

0

8/2

8/2

0

9/0

4/2

0

9/1

1/2

0

9/1

8/2

0

9/2

5/2

0

10

/02

/20

10

/09

/20

10

/16

/20

10

/23

/20

10

/30

/20

11

/06

/20

11

/13

/20

11

/20

/20

11

/27

/20

12

/04

/20

12

/11

/20

12

/18

/20

12

/25

/20

1/0

1/2

1

1/0

8/2

1

1/1

5/2

1

1/2

2/2

1

1/2

9/2

1

2/0

5/2

1

2/1

2/2

1

2/1

9/2

1

2/2

6/2

1

3/0

5/2

1

3/1

2/2

1

3/1

9/2

1

3/2

6/2

1

4/0

2/2

1

4/9

/21

4/1

6/2

1

4/2

3/2

1

4/3

0/2

1

5/7

/21

5/1

4/2

1

5/2

1/2

1

5/2

8/2

1

6/4

/21

6/1

1/2

1

6/1

8/2

1

6/2

5/2

1

7/2

/21

7/9

/21

7/1

6/2

1

7/2

3/2

1

7/3

0/2

1

8/6

/21

8/1

3/2

1

To

tal U

na

dj.

IQVIA – Confidential & Proprietary

-1.2

%

-3.7

%

8.4

%

-9.2

%

1.2

%

0.1

%

-0.9

%

-1.6

%

-1.7

%

-1.9

%

-2.7

%

-5.1

%

-3.0

%

-4.4

%

-4.5

%

-6.3

%

-4.9

%

-7.6

%

-1.6

%

-6.9

%

-5.1

%

-4.3

%

-4.6

%

-6.3

%

-7.9

%

-6.6

%

-15

.2%

-4.1

%

-7.2

%

-10

.4%

-16

.8%

-2.4

%

2.5

%

4.9

%

9.8

%

9.8

%

9.0

%

8.8

%

7.4

%

5.4

%

15

.1%

-2.7

%

4.8

%

3.5

%

4.2

%

4.0

%

-0.1

%

3.8

%

4.9

%

3.1

%

4.0

%

2.9

%

-50%

0%

50%

8/2

1/2

0

8/2

8/2

0

9/0

4/2

0

9/1

1/2

0

9/1

8/2

0

9/2

5/2

0

10

/02

/20

10

/09

/20

10

/16

/20

10

/23

/20

10

/30

/20

11

/06

/20

11

/13

/20

11

/20

/20

11

/27

/20

12

/04

/20

12

/11

/20

12

/18

/20

12

/25

/20

1/0

1/2

1

1/0

8/2

1

1/1

5/2

1

1/2

2/2

1

1/2

9/2

1

2/0

5/2

1

2/1

2/2

1

2/1

9/2

1

2/2

6/2

1

3/0

5/2

1

3/1

2/2

1

3/1

9/2

1

3/2

6/2

1

4/0

2/2

1

4/9

/21

4/1

6/2

1

4/2

3/2

1

4/3

0/2

1

5/7

/21

5/1

4/2

1

5/2

1/2

1

5/2

8/2

1

6/4

/21

6/1

1/2

1

6/1

8/2

1

6/2

5/2

1

7/2

/21

7/9

/21

7/1

6/2

1

7/2

3/2

1

7/3

0/2

1

8/6

/21

8/1

3/2

1

Unadju

ste

d Y

oY

Gro

wth

Un

ad

juste

d Y

oY

Gro

wth

less C

OV

ID V

accin

es

Page 42

41

Adjusted growth trends have run positive for the last several weeks driven by COVID vaccines and last spring’s weak comparison periods

Data Source: IQVIA Xponent - Copyright 2021

2.6

%

0.1

%

12

.9%

-5.3

%

6.0

%

4.2

%

2.6

%

1.9

%

1.8

%

1.9

%

0.9

%

-0.8

%

1.4

%

0.3

%

0.6

%

-1.9

%

-0.1

%

-2.3

%

6.0

%

-0.3

%

1.1

%

2.3

%

1.8

%

1.1

%

-0.3

%

1.0

%

-8.5

%

3.9

%

0.7

%

-2.8

%

-11

.2%

3.0

% 9.4

%

12

.3%

15

.8%

17

.3%

16

.2%

15

.6%

13

.5%

12

.1%

20

.7%

1.4

% 9.0

%

8.7

%

7.3

%

7.7

%

3.4

%

7.8

%

9.3

%

7.9

%

9.2

%

7.7

%

-20%

0%

20%

40%

08

/21

/20

08

/28

/20

09

/4/2

0

09

/11

/20

09

/18

/20

09

/25

/20

10

/02

/20

10

/09

/20

10

/16

/20

10

/23

/20

10

/30

/20

11

/6/2

0

11

/13

/20

11

/20

/20

11

/27

/20

12

/4/2

0

12

/11

/20

12

/18

/20

12

/25

/20

01

/01

/21

01

/08

/21

01

/15

/21

01

/22

/21

01

/29

/21

02

/05

/21

02

/12

/21

02

/19

/21

02

/26

/21

03

/5/2

1

03

/12

/21

03

/19

/21

3/2

6/2

1

4/2

/21

4/9

/21

4/1

6/2

1

4/2

3/2

1

4/3

0/2

1

5/7

/21

5/1

4/2

1

5/2

1/2

1

5/2

8/2

1

6/4

/21

6/1

1/2

1

6/1

8/2

1

6/2

5/2

1

7/2

/21

7/9

/21

7/1

6/2

1

7/2

3/2

1

7/3

0/2

1

8/6

/21

8/1

3/2

1

To

tal A

dj.

IQVIA – Confidential & Proprietary

2.3

%

2.8

%

7.5

%

-3.8

%

15

.7%

3.4

%

4.8

%

5.1

%

1.4

%

0.5

%

0.4

%

1.0

%

0.9

%

-0.2

%

-14

.7%

2.3

%

22

.3%

-2.9

%

-14

.4%

-12

.1%

27

.0%

11

.4%

-5.9

%

-3.7

%

1.5

%

0.6

%

-13

.3%

0.5

%

4.4

%

1.9

%

-4.9

%

-7.3

%

-15

.1% -1

.4%

6.5

%

8.0

%

10

.3%

11

.6%

9.1

%

7.3

%

10

.0%

1.5

% 8.4

%

5.5

%

4.7

%

3.6

%

-1.1

%

6.6

%

8.5

%

2.5

%

7.0

%

6.0

%

-20%

0%

20%

40%

8/2

1/2

0

8/2

8/2

0

9/4

/20

9/1

1/2

0

9/1

8/2

0

9/2

5/2

0

10

/02

/20

10

/09

/20

10

/16

/20

10

/23

/20

10

/30

/20

11

/6/2

0

11

/13

/20

11

/20

/20

11

/27

/20

12

/4/2

0

12

/11

/20

12

/18

/20

12

/25

/20

1/0

1/2

1

1/0

8/2

1

1/1

5/2

1

1/2

2/2

1

1/2

9/2

1

2/0

5/2

1

2/1

2/2

1

2/1

9/2

1

2/2

6/2

1

3/5

/21

3/1

2/2

1

3/1

9/2

1

3/2

6/2

1

4/2

/21

4/9

/21

4/1

6/2

1

4/2

3/2

1

4/3

0/2

1

5/7

/21

5/1

4/2

1

5/2

1/2

1

5/2

8/2

1

6/4

/21

6/1

1/2

1

6/1

8/2

1

6/2

5/2

1

7/2

/21

7/9

/21

7/1

6/2

1

7/2

3/2

1

7/3

0/2

1

8/6

/21

8/1

3/2

1

Adju

ste

d Y

oY

Gro

wth

Ad

juste

d Y

oY

Gro

wth

le

ss

CO

VID

Va

ccin

es

Page 43

42

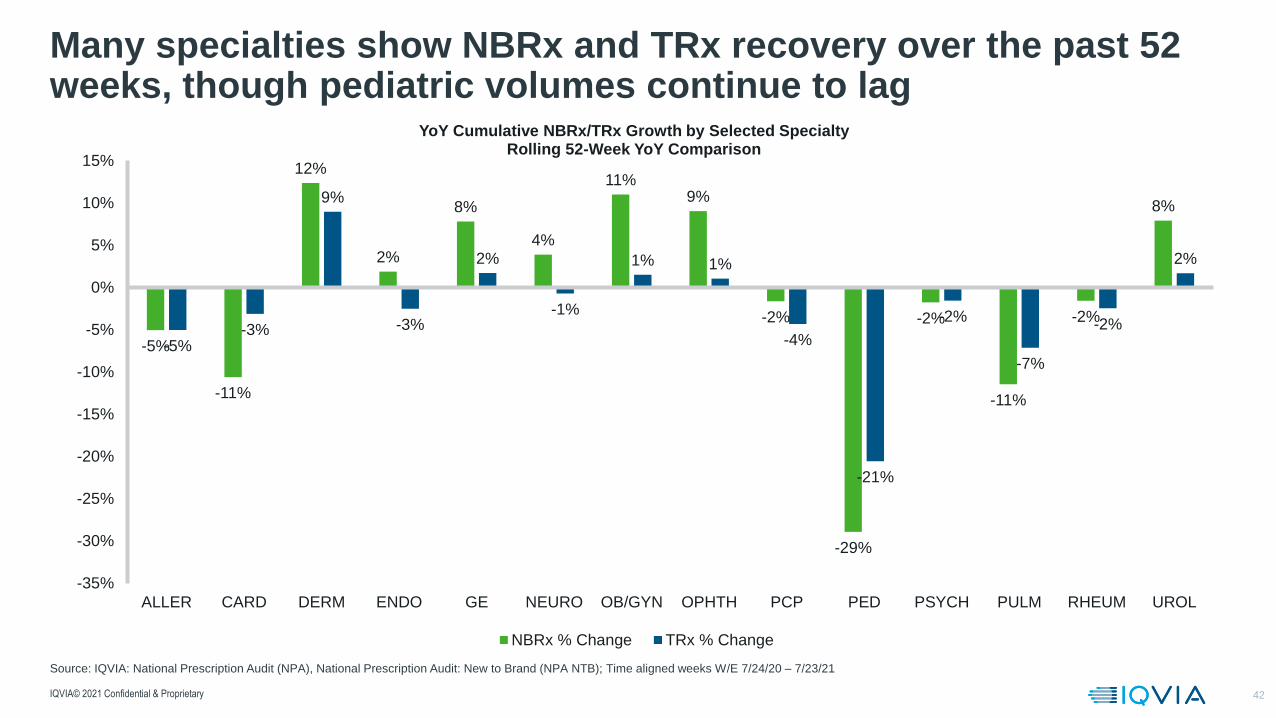

Many specialties show NBRx and TRx recovery over the past 52 weeks, though pediatric volumes continue to lag

IQVIA© 2021 Confidential & Proprietary

Source: IQVIA: National Prescription Audit (NPA), National Prescription Audit: New to Brand (NPA NTB); Time aligned weeks W/E 7/24/20 – 7/23/21

-5%

-11%

12%

2%

8%

4%

11%9%

-2%

-29%

-2%

-11%

-2%

8%

-5%-3%

9%

-3%

2%

-1%

1% 1%

-4%

-21%

-2%

-7%

-2%

2%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

ALLER CARD DERM ENDO GE NEURO OB/GYN OPHTH PCP PED PSYCH PULM RHEUM UROL

YoY Cumulative NBRx/TRx Growth by Selected SpecialtyRolling 52-Week YoY Comparison

NBRx % Change TRx % Change

Page 44

44

Acute and New Rx growth is slowing down over the last three months; driven by COVID vaccines (% change vs. 1 Year ago)

-40%

-20%

0%

20%

40%

60%

80%Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

Acute

-U

nadju

ste

d

-10%

0%

10%

20%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

Main

t. -

Unadju

ste

d

IQVIA© 2021 Confidential & Proprietary

New

-U

nadju

ste

dR

efill

-Unadju

ste

dAll Rx’s shown in Millions

-20%

-10%

0%

10%

20%

30%

40%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

-10%

-5%

0%

5%

10%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

To

tal R

eta

il &

Mail –

Acu

te&

Main

t., N

ew

/Refi

ll –

Un

ad

juste

d R

x’s

Page 45

45

45

Pain shows negative growth for one and five-year growth

Nervous system disorders 5-year growth is high, but short-term growth is minimal

IQVIA Xponent® June 2021, Retail, Mail and LTC

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-20% -10% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 110%

ANTIHYPERTENSIVES

NERVOUS SYSTEM DISORDERS

MENTAL HEALTH

RESPIRATORY AGENTS

Historic growth (5 year CAGR, 2016-2021)

Short

-te

rm g

row

th (

20

20

-20

21)

LIPID REGULATORS

PAIN

ANTIDIABETICS

THYROID ANTI-THYROID AND IODINE PREPS

ANTI-ULCERANTS

OTHER CNS

Jun 2021 MAT Adj Scripts

IQVIA© 2021 Confidential & Proprietary

Page 46

46

Based on adjusted Rx’s basis in Retail, Antihypertensives are the leading therapy with Atorvastatin as the top product

Therapies

Rank Therapy

MAT

July

2021

YoY Growth

1 ANTIHYPERTENSIVES, PLAIN & COMBO 1,046.5 2.6%

2 MENTAL HEALTH 492.3 6.5%

3 LIPID REGULATORS 425.1 5.6%

4 PAIN 377.6 0.2%

5 ANTIDIABETICS 352.6 3.5%

6 ANTI-ULCERANTS 214.2 4.5%

7 NERVOUS SYSTEM DISORDERS 210.9 3.4%

8THYROID ANTI-THYROID AND IODINE

PREPS189.6 1.3%

9 RESPIRATORY AGENTS 182.8 -5.2%

10 VACCINES (PURE, COMB, OTHER) 180.5 232.0%

Products

Rank Product

MAT

July

2021

YoY

Growth

1 ATORVASTATIN CA 208.3 7.6%

2 LISINOPRIL 154.1 0.6%

3 AMLODIPINE BESY 150.9 5.6%

4 LEVOTHYROXINE SOD 141.2 -2.4%

5 LOSARTAN POT 105.0 5.5%

6 METFORMIN HCL 97.1 3.5%

7 METOPROLOL SUCCIN 84.9 7.2%

8 OMEPRAZOLE (RX) 83.8 16.0%

9 HYDROCHLOROTHIAZIDE 81.2 -0.3%

10 GABAPENTIN 78.5 3.8%

Top 10 Therapies and Products for Retail - MAT July 2021 (Adjusted Rx’s in Millions)

Source: IQVIA, National Sales Perspectives, June 2021

Limited to Rx and OTC Insulins

*For Client’s internal use only

Page 47

47

When looking at Retail on an unadjusted Rx basis there are no changes for the top therapy and top product

Therapies

Rank Therapy

MAT

July

2021

YoY

Growth

1 ANTIHYPERTENSIVES, PLAIN & COMBO 527.8 -2.9%

2 PAIN 350.8 -0.3%

3 MENTAL HEALTH 332.2 2.6%

4 ANTIDIABETICS 208.8 -0.5%

5 LIPID REGULATORS 202.7 0.2%

6 VACCINES (PURE, COMB, OTHER) 178.9 242.5%

7 ANTIBACTERIALS 175.8 -16.9%

8 NERVOUS SYSTEM DISORDERS 159.2 0.9%

9 OTHER CNS 155.6 1.1%

10 RESPIRATORY AGENTS 146.2 -8.6%

Products

Rank Product

MAT

July

2021

YoY

Growth

1 ATORVASTATIN CA 99.6 1.6%

2 LISINOPRIL 75.9 -4.9%

3 AMLODIPINE BESY 74.4 -0.3%

4 LEVOTHYROXINE SOD 69.7 -8.0%

5 PFIZER COVID19 VACC 62.6

6 GABAPENTIN 59.0 2.6%

7 HYCD/APAP 52.9 -1.1%

8 LOSARTAN POT 50.8 -0.1%

9 METFORMIN HCL 49.7 -1.8%

10 OMEPRAZOLE (RX) 47.6 9.9%

Top 10 Therapies and Products for Retail - MAT July 2021 (Unadjusted Rx’s in Millions)

Source: IQVIA, National Sales Perspectives, June 2021

Limited to Rx and OTC Insulins

*For Client’s internal use only

Page 48

48

Retail Class of Trade

and Method of Payment

Performance

Page 49

49

Adjusted volumes in all COTs in June 2021 show an uptick from May 2021 volumes

190

200

210

220

230

240

250

260Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

50

70

90

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

IQVIA Copyright 2021 - Confidential - For Client Use Only

CHAIN

MASS

70

75

80

85

90

95

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

INDEP

55

60

65

70

75

80

85

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

FOOD

380

400

420

440

460

480

500

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

RETAIL

35

40

45

50

55

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Mill

ion

s

2019 2020 2021

MAIL

AD

JU

ST

ED

Rx’s

Page 50

50

COVID Vaccines are the driver of growth, though it is slowing

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

IQVIA Copyright 2021 - Confidential - For Client Use Only

CHAIN

MASS

-15%

-10%

-5%

0%

5%

10%

15%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

INDEP

-5%

0%

5%

10%

15%

20%

25%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

No

v-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

FOOD

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

RETAIL

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan

-20

Ma

r-20

Ma

y-2

0

Jul-

20

Sep-2

0

Nov-2

0

Jan

-21

Ma

r-21

Ma

y-2

1

MAIL

AD

JU

ST

ED

RX

GR

OW

TH

Page 51

51

90 Day percentage of Rx’s based on Unadjusted Rx’s shows a slight increase from May to June, excluding Mail

10%

15%

20%

25%

30%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

10%

15%

20%

25%

30%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

IQVIA Copyright 2021 - Confidential - For Client Use Only

CHAIN

MASS

10%

15%

20%

25%

30%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

INDEP

10%

15%

20%

25%

30%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

FOOD

10%

15%

20%

25%

30%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

RETAIL

70%

75%

80%

85%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

MAIL

90 D

ay P

erc

en

tag

e b

ased

on

Un

ad

j. R

x’s

Page 52

52

COT market share declines minimally from March 2021

49%

50%

51%

52%Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

12%

13%

14%

15%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

IQVIA Copyright 2021 - Confidential - For Client Use Only

CHAIN

MASS

15%

20%

25%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

INDEP

14%

15%

16%

17%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

FOOD

Mark

et

Sh

are

based

on

Ad

jus

ted

Rx’s

Page 53

53

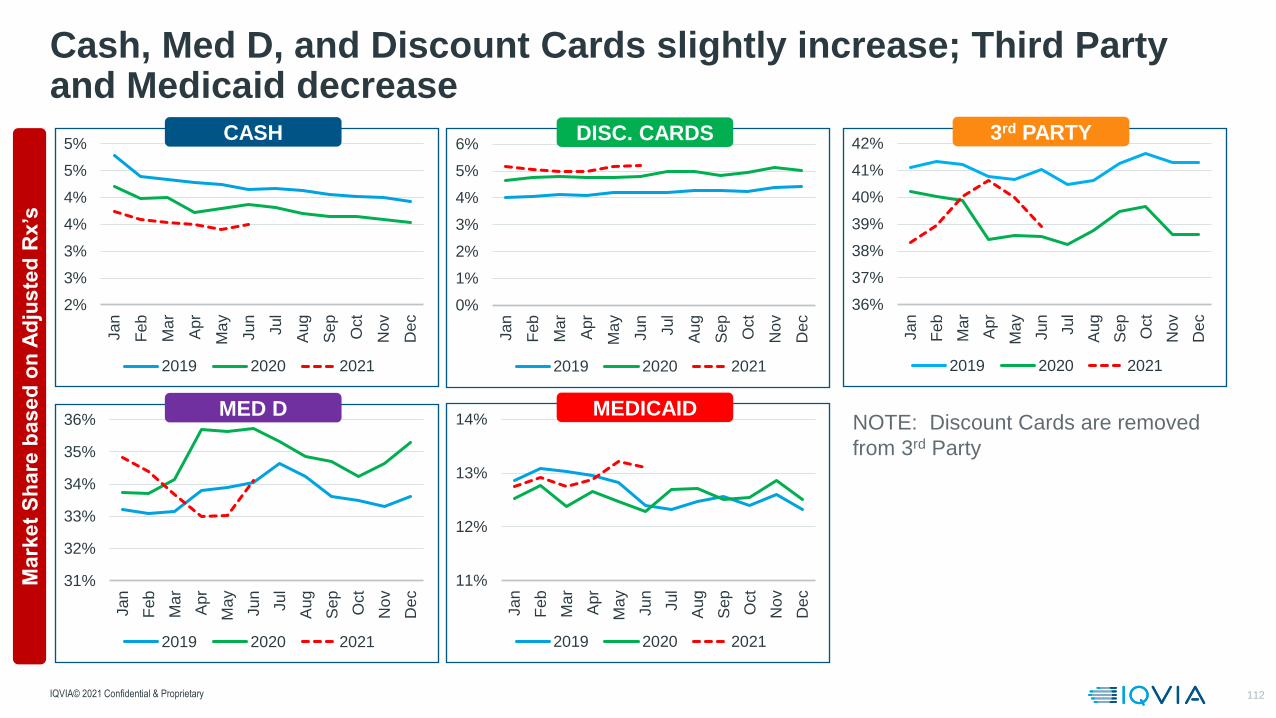

Cash, Med D, and Discount Cards slightly increase; Third Party and Medicaid decrease

2%

3%

3%

4%

4%

5%

5%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

31%

32%

33%

34%

35%

36%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

IQVIA© 2021 Confidential & Proprietary

CASH

MED D

0%

1%

2%

3%

4%

5%

6%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

DISC. CARDS

36%

37%

38%

39%

40%

41%

42%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

3rd PARTY

11%

12%

13%

14%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

MEDICAID

Mark

et

Sh

are

based

on

Ad

jus

ted

Rx’s

NOTE: Discount Cards are removed

from 3rd Party

Page 54

54

90-Day % of unadjusted Rx’s show percentages above prior year in all but Cash and Third Party

0%

5%

10%

15%

20%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

0%

10%

20%

30%

40%

50%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021

IQVIA Copyright 2021 - Confidential - For Client Use Only

CASH

MED D

0%

5%

10%

15%

20%

25%

Jan

Feb

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

2019 2020 2021