U.S. Uranium and Nuclear Power Outlook: 2008 - 2030 Presented to: National Research Council of the National Academies Presented by: Tom Pool Chairman, International Nuclear November 18, 2008

Transcript

U.S. Uranium and Nuclear Power Outlook: 2008 - 2030

Presented to:National Research Council of the National Academies

Presented by: Tom Pool

Chairman, International Nuclear

November 18, 2008

U.S. Electricity Generation 2006

Coal49%

Petroleum2%

Natural Gas20%

Nuclear20%

Hydro7%

Renewables2%

Nuclear power is important in the US

U.S. Nuclear Power Generation

0

200

400

600

800

1000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Bill

ion

kWhr

s

Deregulation gave nuclear power a profit motive.

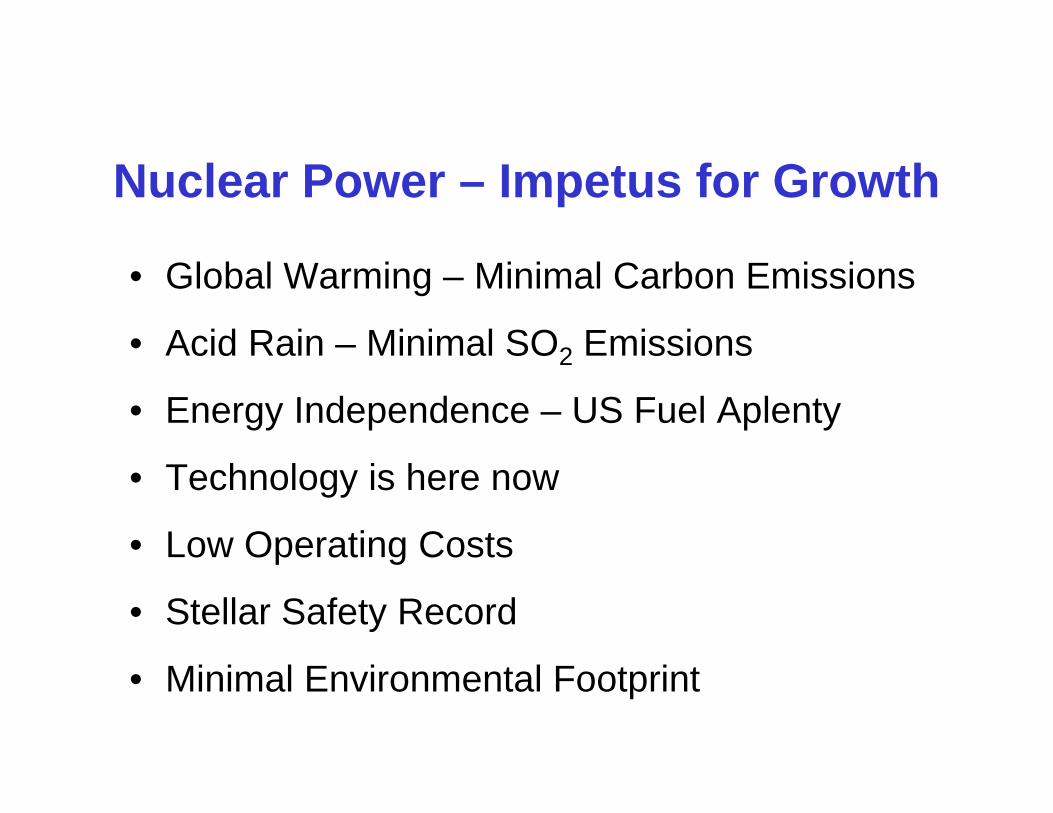

Nuclear Power – Impetus for Growth

• Global Warming – Minimal Carbon Emissions

• Acid Rain – Minimal SO2 Emissions

• Energy Independence – US Fuel Aplenty

• Technology is here now

• Low Operating Costs

• Stellar Safety Record

• Minimal Environmental Footprint

Electricity Production Costs(Operation, Maintence & Fuel)

0

2

4

6

8

10

12

1995 1997 1999 2001 2003 2005 2007

cent

s pe

r ki

low

att-

hour

CoalGasNuclearPetroleum

Nuclear Power – Constraints on Growth

• High Capital Cost, Particularly in the Current World Financial Crisis

Nuclear Power – Means of Growth

• Capacity Factor

• License Extensions

• Uprates

• New Units

40%

50%

60%

70%

80%

90%

100%

1971 1976 1981 1986 1991 1996 2001 2006

Capacity Factor - U.S. Nuclear Reactors

US Reactor License Extensions(20 years)

• Renewed – 49

• Filed for Renewal – 17

• Expected to File – 33

• Thus, 99 out of 104 existing licenses are expected to be renewed.

• ~2000 reactor years, ~2,000,000 mW years

p

0

200

400

600

800

1,000

1,200

1977 1982 1987 1992 1997 2002 2007

meg

awat

ts p

er y

ear

U.S. Nuclear Reactor Uprates

0

1,000

2,000

3,000

4,000

5,000

6,000

1977 1982 1987 1992 1997 2002 2007

meg

awat

ts

Cumulative U.S. Reactor Uprates

New Reactor Outlook

• 3 Early Site Permit Applications (ESP) Approved by NRC

• 2 Additional ESP Applications Under Review by NRC

• 24 Combined Construction and Operating License Applications (CCOL) Submitted to NRC

• 6 Additional CCOL Applications Expected

80,000

90,000

100,000

110,000

120,000

2005 2010 2015 2020

MW

e ne

t

LowReferenceHigh

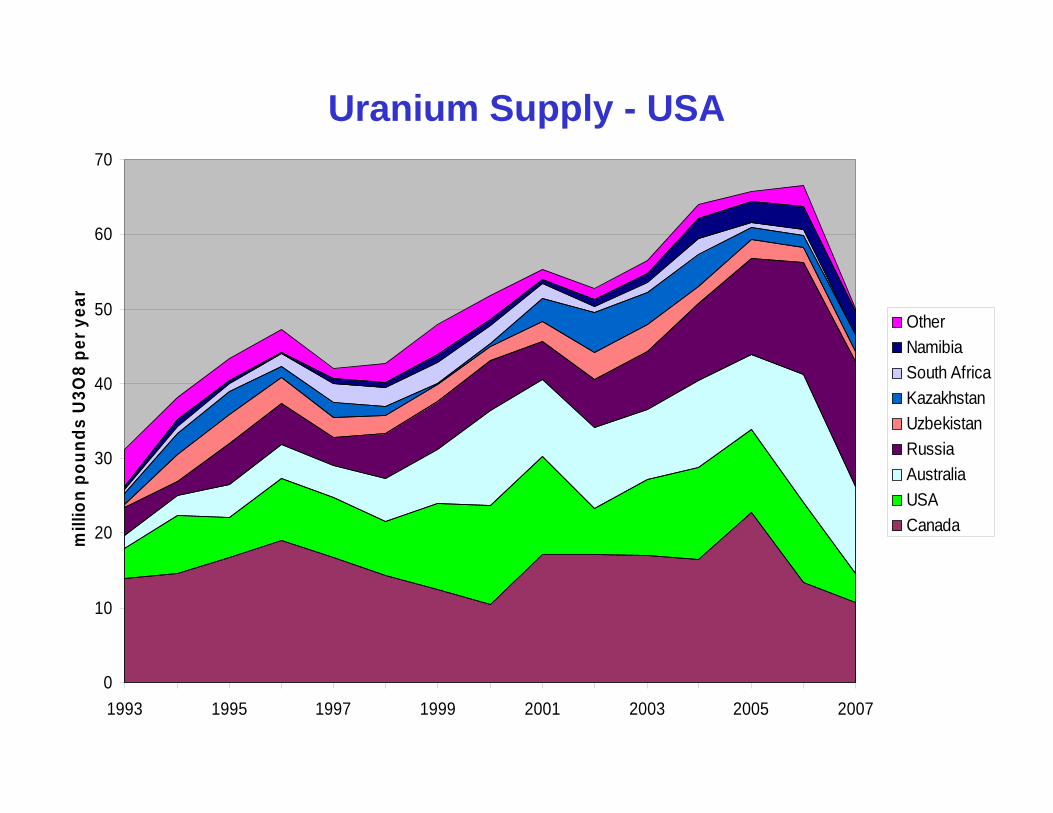

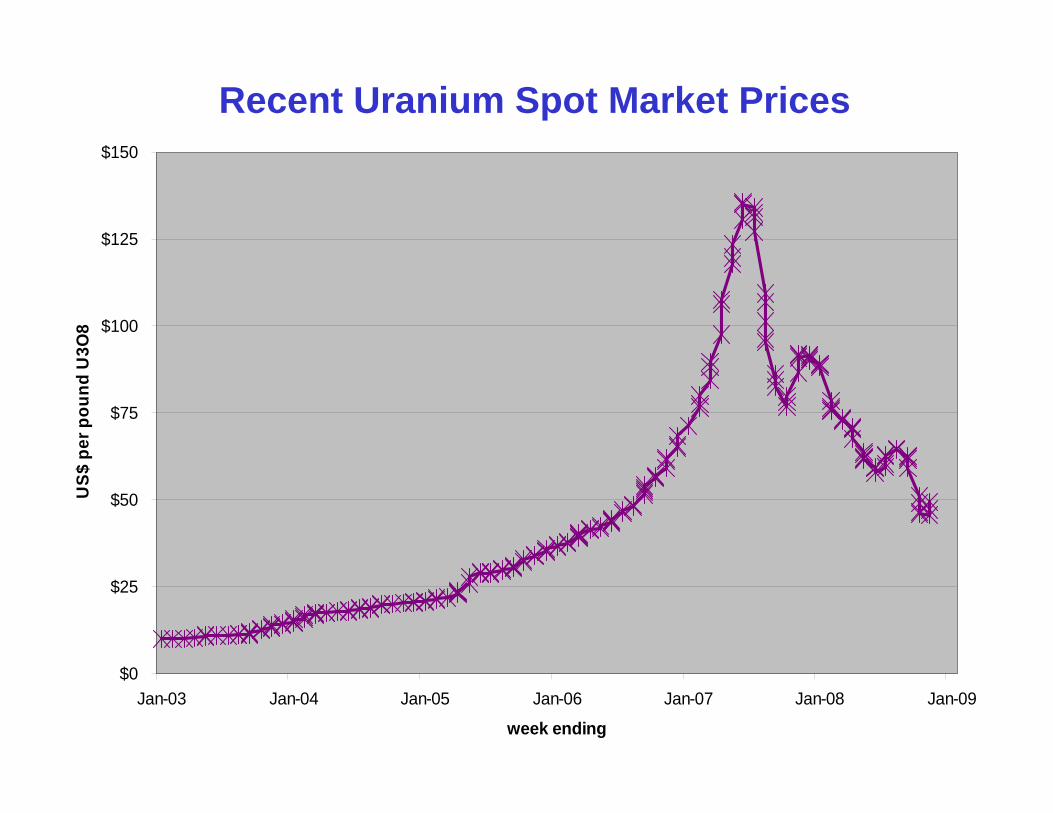

Nuclear Generating Capacity – U.S.A.(WNA 2007)

100

110

120

130

140

150

160

170

180

190

200

2000 2005 2010 2015 2020

mill

ion

poun

ds U

3O8

per y

ear

20012000

2001 = Bush/Cheney2000 = Clinton/Gore

World Uranium Requirements Forecasts(US Energy Information Administration)

Worker Safety at U.S. Nuclear Power Plants vs. U.S. Occupational Injury Rate

0

2

4

6

8

10

1980 1985 1990 1995 2000 2005

Inju

ries

per

200

,000

hou

rs

Nuclear U.S. Average

An intense safety culture exists at nuclear power plants

0

2

4

6

8

10

12

14

16

18

20

Coal Uranium Oil & Gas

Fata

litie

s pe

r Ter

awat

t-Hou

r

U.S. Energy Production Fatalities(1992-2006)

Radiation Safety

• Linear-No-Threshold– Any additional radiation causes more

![Western Uranium Corporation [Type text]western-uranium.com/media/Western Uranium Corp...2015, Western Uranium acquired Black Range Minerals Ltd to acquire additional uranium assets](https://static.documents.pub/doc/80x56/5e9e2fdc39245c320521c248/western-uranium-corporation-type-textwestern-uranium-corp-2015-western-uranium.jpg)